Following a successful Black Friday in November, the United Kingdom geared up for the 2017 Christmas season in December. Analysts estimate the total splurge in December at about £45 billion, beating last December’s record of £43 billion.

Online sales hit £1.03billion, passing the £1billion threshold for the first time and up 7.9 percent on 2016’s £954million, according to the Centre for Retail Research. The rise of online shopping together with the timing of Christmas in 2017 meant shopper footfall in physical stores was lower than in previous years as people increasingly moved to shopping online.

Total shopper numbers were 4.5 percent down on the previous year, according to research group Springboard, which may reflect the growing strength and reliability of online’s product range and delivery responsiveness.

Major online retailers though continued to pull out the big discount guns across categories in an effort to attract online shoppers on Boxing Day, the biggest sale event in December.

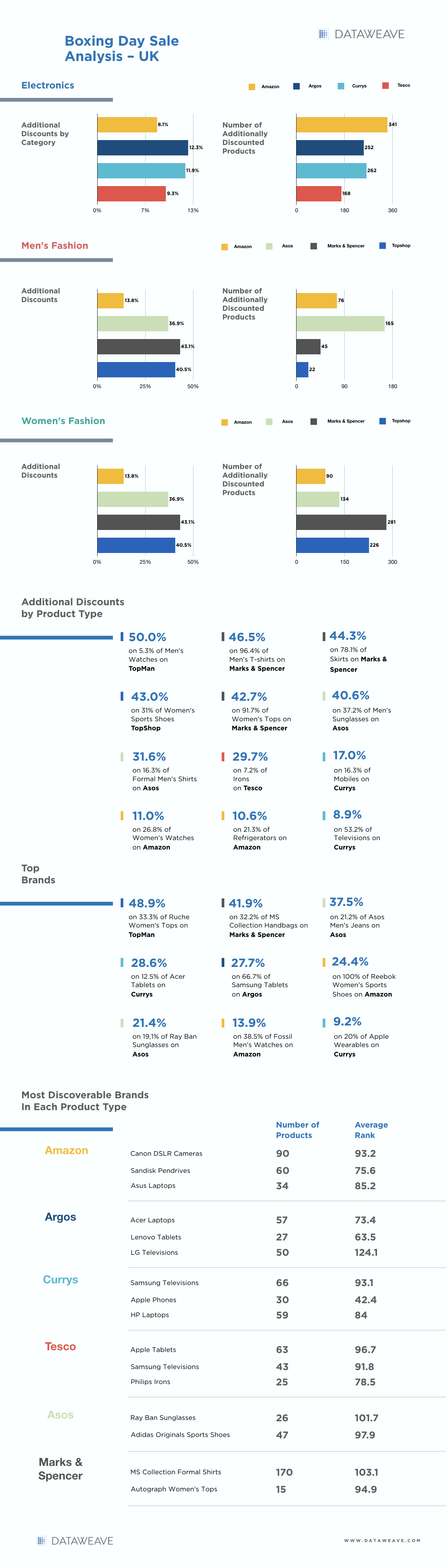

At DataWeave, we focused our proprietary data aggregation and analysis platform to analyze the top 500 ranked products in over 20 product categories across electronics and fashion retailers in the UK. Our analysis included several top UK retailers, which include Amazon, Argos, Currys, Tesco, Asos, Marks & Spencer, and Topshop.

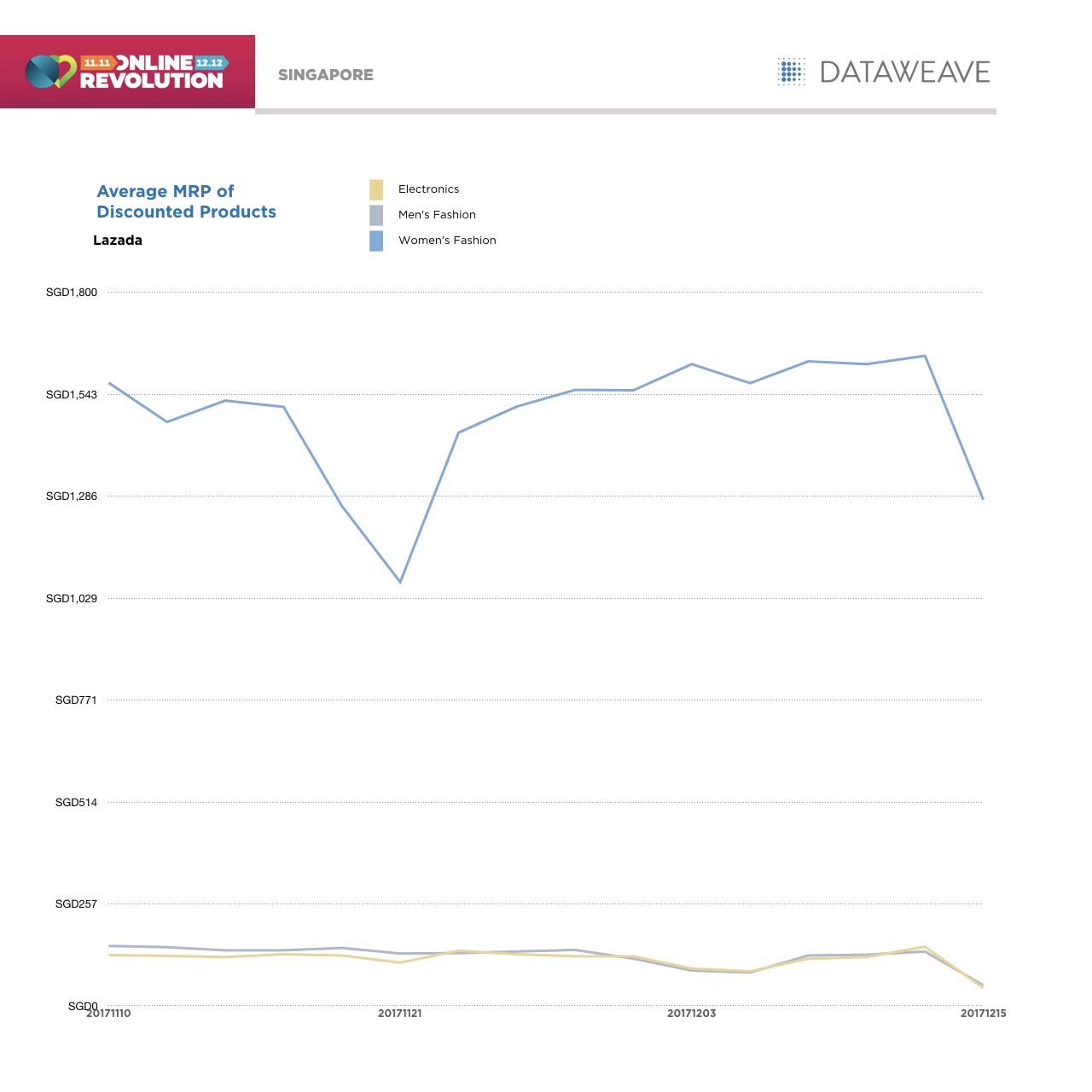

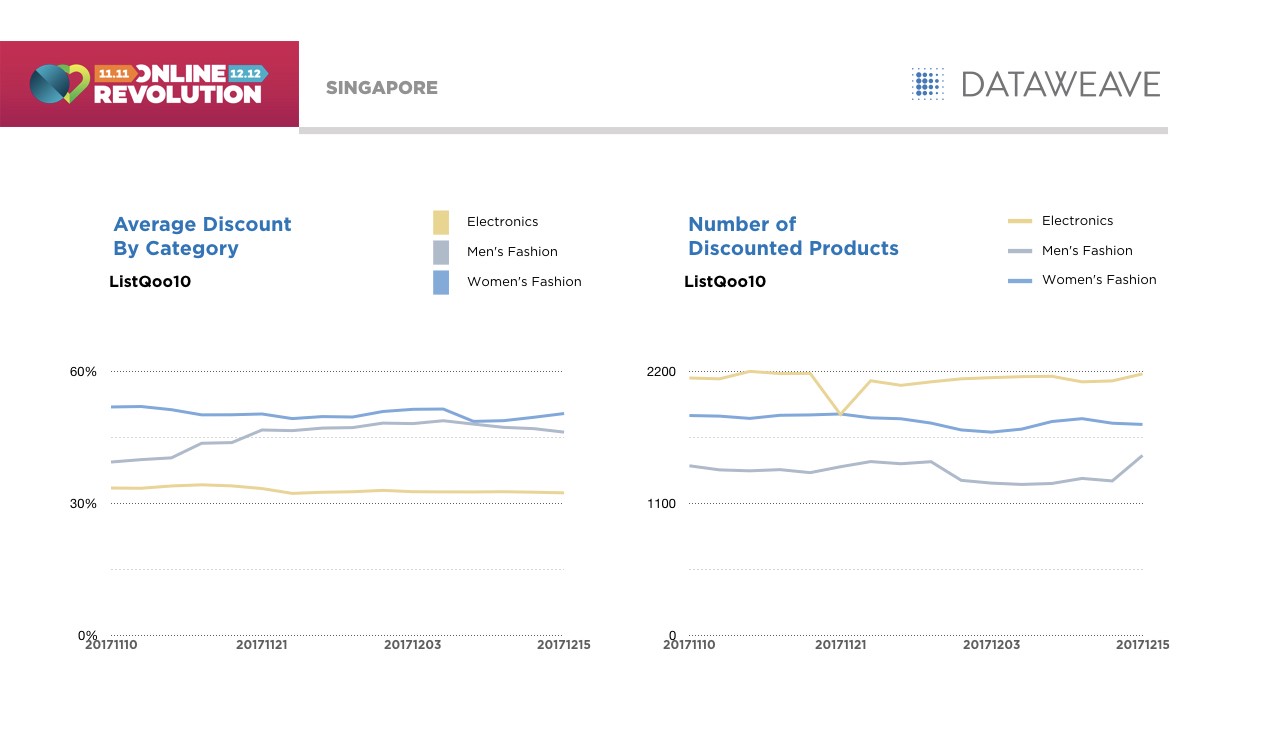

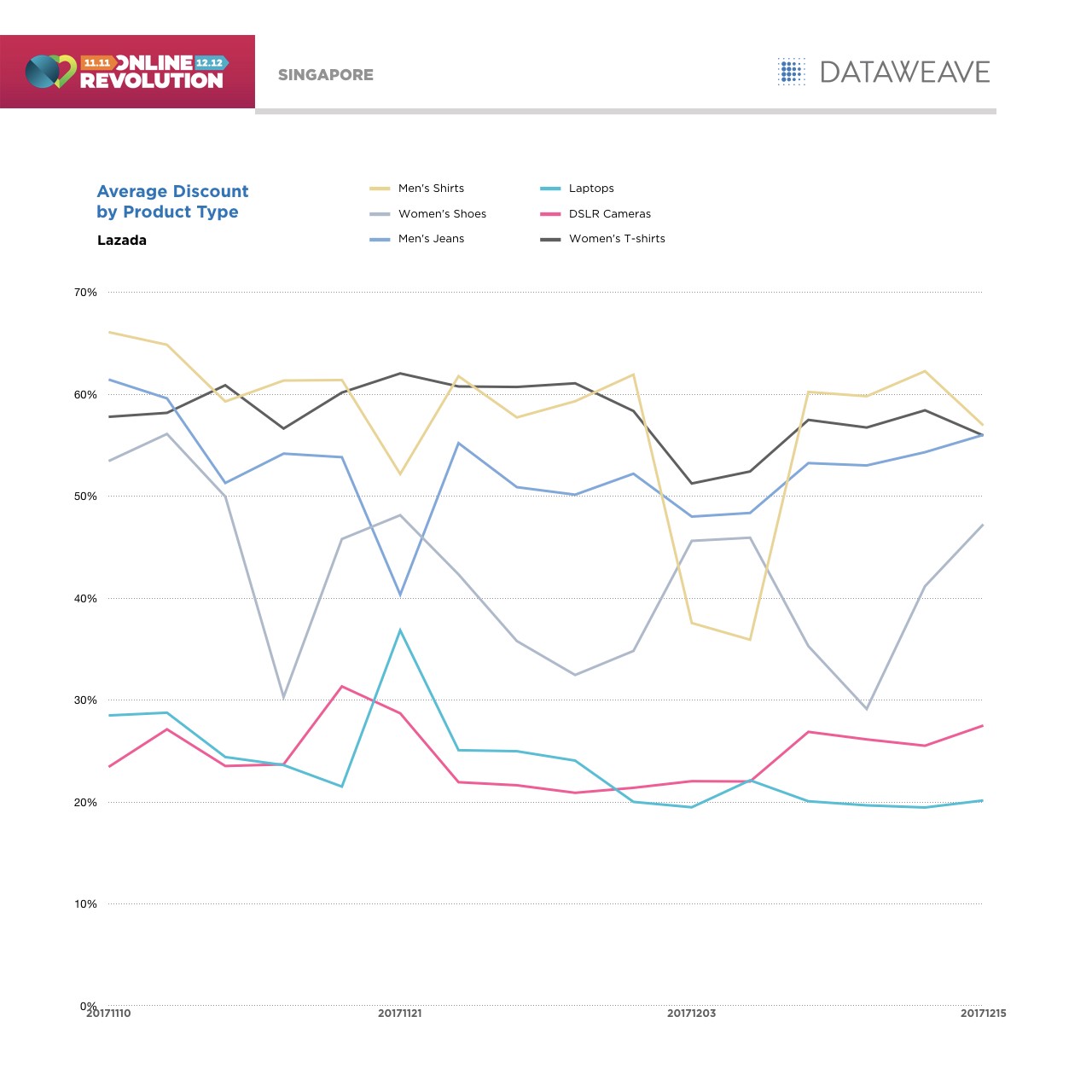

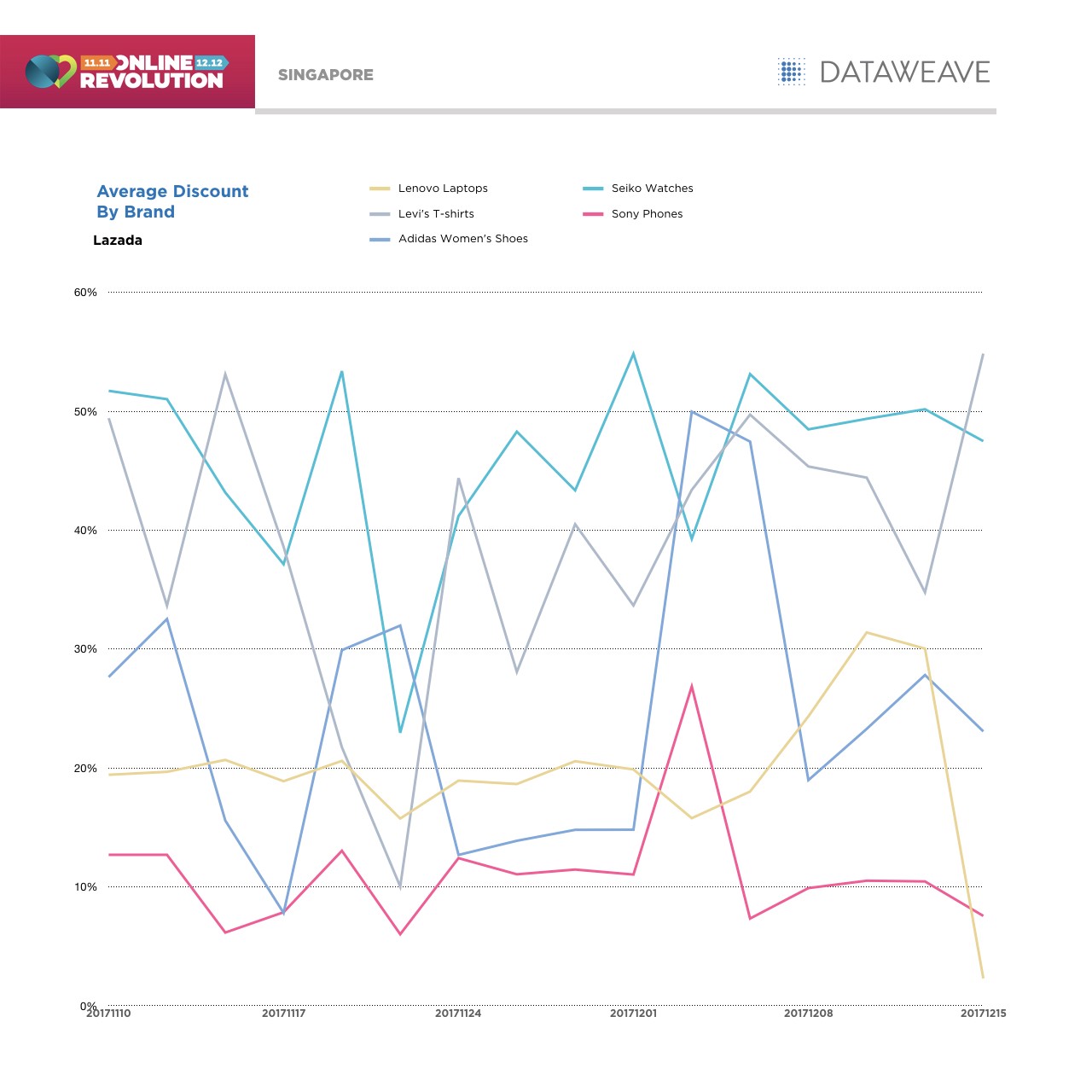

The discounts in the infographic below indicate the magnitude of reduction in prices during the sale (26th Dec), compared to before the sale (19th Dec), in order to best represent the additional value derived from the sale for shoppers.

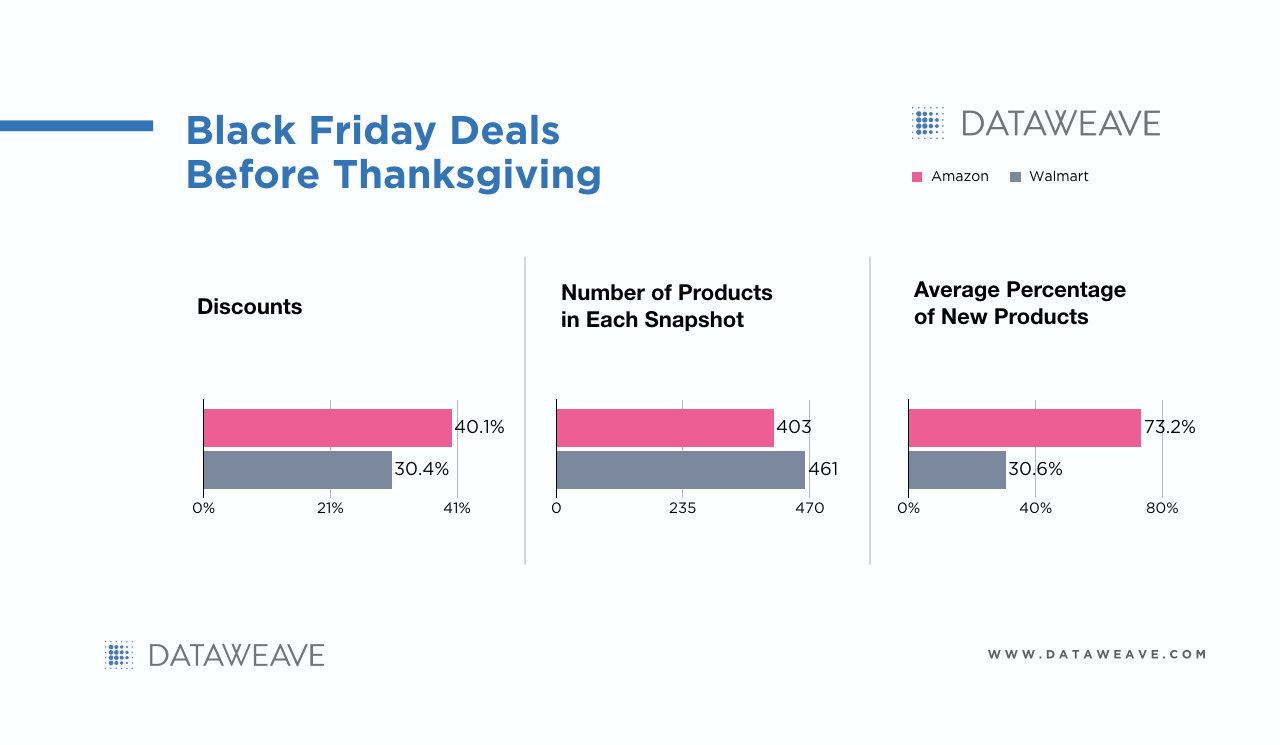

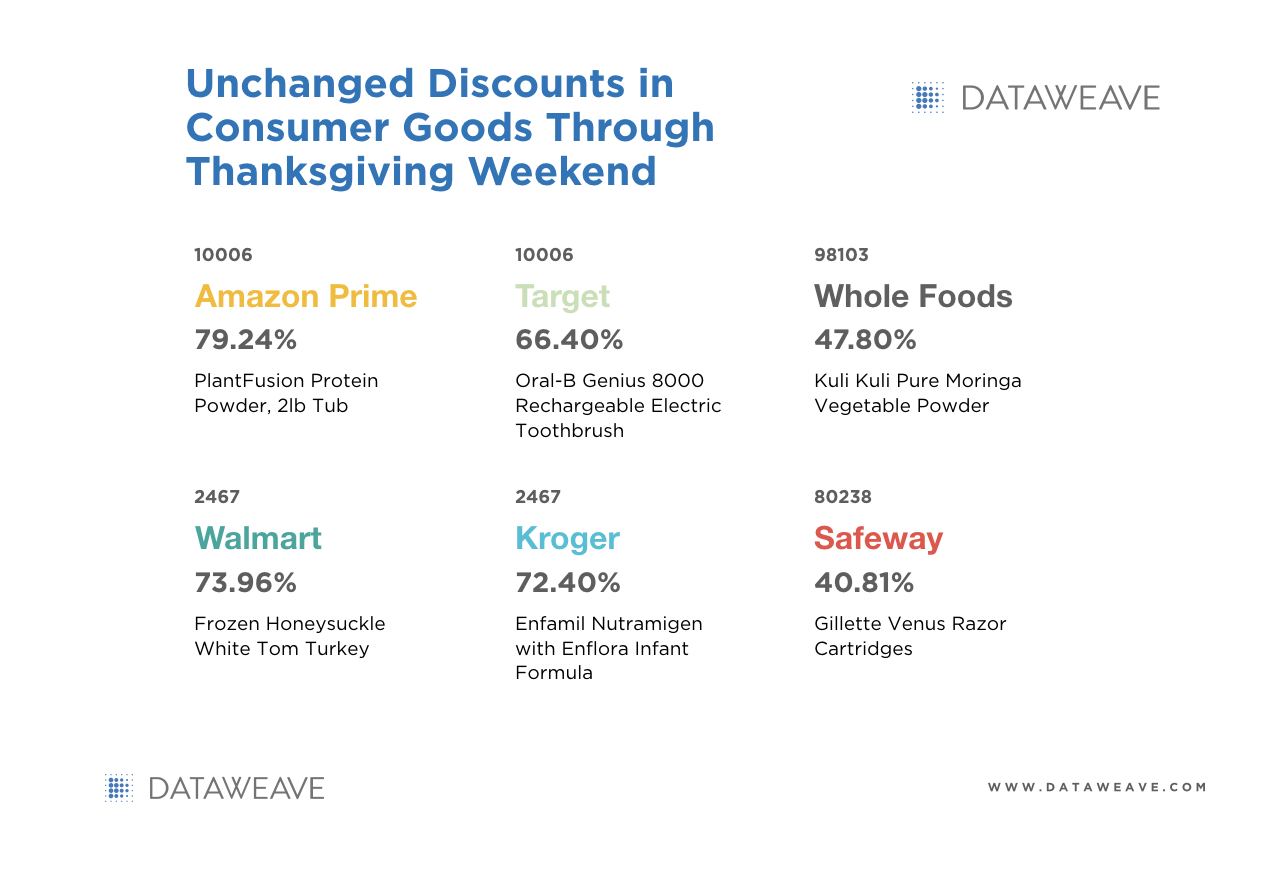

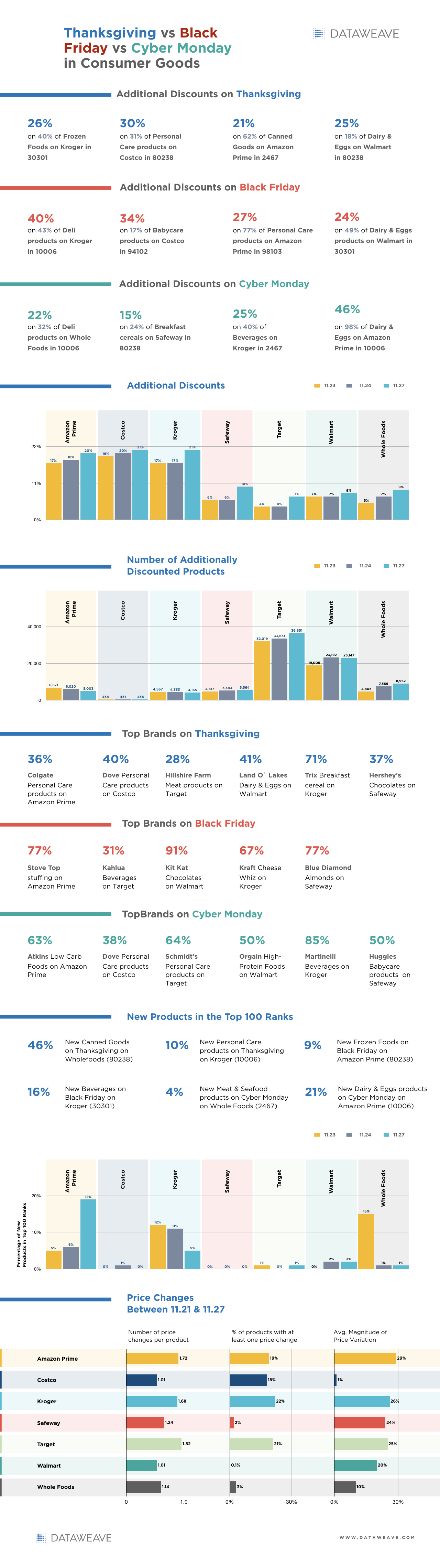

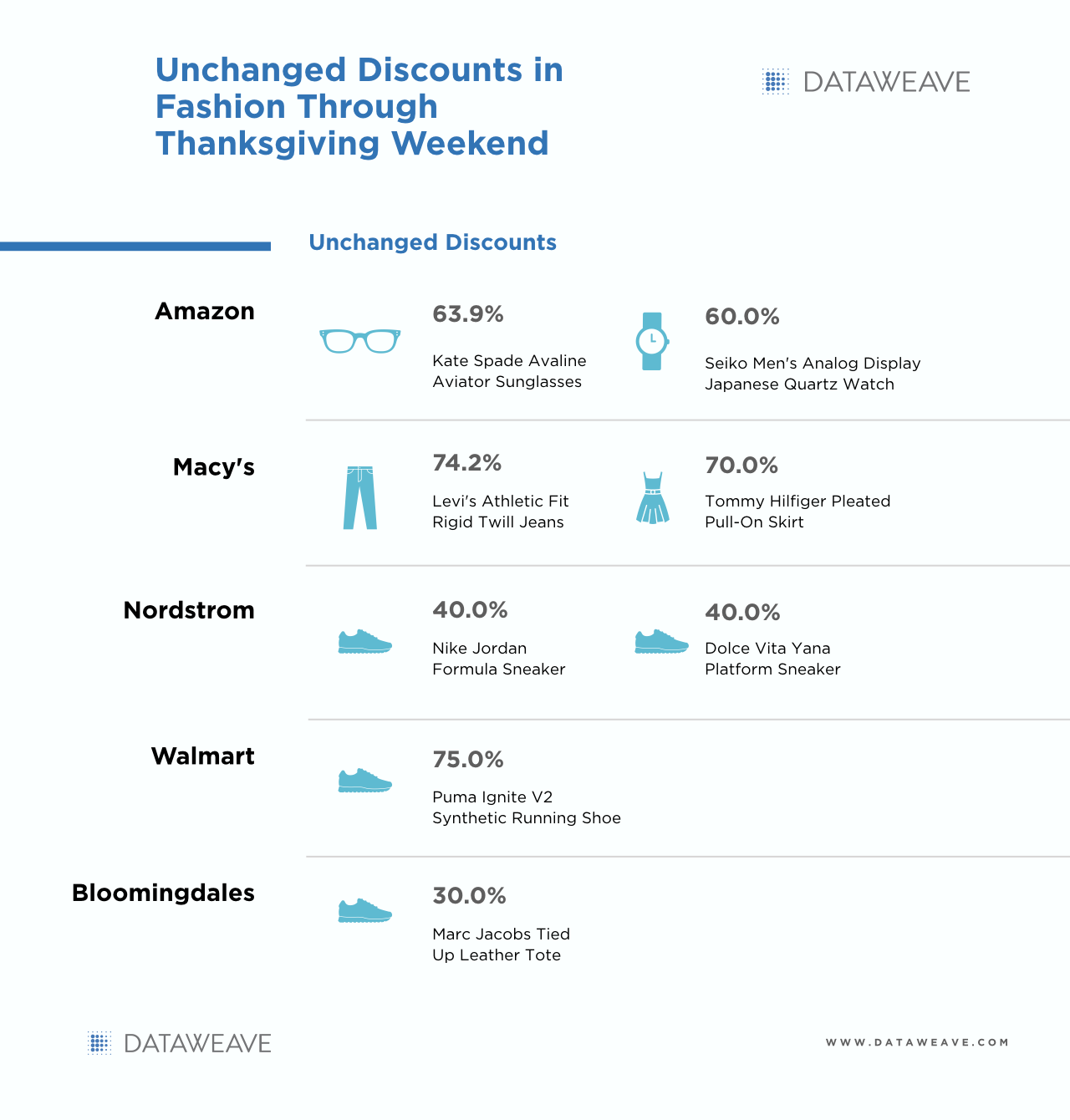

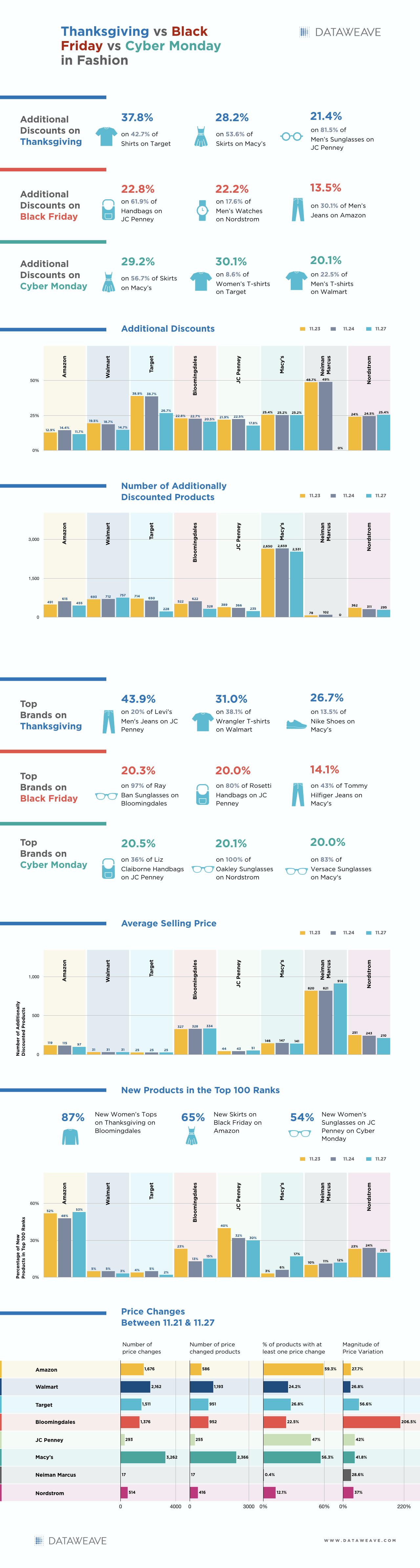

Boxing Day Sale Highlights

In electronics, while Amazon offered discounts on the most number of products, Argos was aggressive in the average size of its additional discounts.

Surprisingly, Amazon appeared to be much more conservative in the Men’s Fashion category with an average additional discount of 13.8 percent, spanning 341 products. Here, Asos deployed the most aggressive combination of high average additional discounts (36.9 percent) on a large number of products (165).

Marks & Spencer focused their targeted discounts (43.1 percent) on a tight set of Men’s Fashion products (45), while interestingly, the story almost reverses in Women’s Fashion, where both M&S (43.1 percent, 281 products) and Topshop (40.5 percent, 226 products) were aggressive in what turned out to be a critical battleground category.

Leading brands weren’t left out of the discounting action either, with the largest discount on offer going to Ruche (48.9 percent on 33.3 percent) women’s tops, closely followed by M S Collection (41.9 percent on 32.3 percent) handbags and Asos’ (37.5 percent on 21.2 percent) men’s jeans.

Most Discoverable Brands

We also analysed the most discoverable brands in each product type. This was measured as a combination of the number of the brand’s products present in the Top 500 ranks of a product type, as well as the average rank (lower the number, higher is the discoverability).

It was no surprise that Canon DSLR cameras were highly discoverable on Amazon with 90 products, along with an average ranking of 93.2, while 34 Asus laptops recorded an average ranking of 85.2. At Argos, 57 Acer laptops recorded an average ranking of 73.4 while 50 LG televisions delivered an average ranking of 124.1.

Other highly discoverable brands included MS Collection in Marks & Spencer, Apple iPhones and Tablets on Curry’s and Tesco.

The Online Retail March Continues

If we look at sales results across the world, from the United Kingdom to the United States, to Asia in countries such as India, Singapore and Indonesia through to Australia, online retail is aggressively cannibalizing traditional bricks and mortar in-store retail sales. Online retail’s demonstrated superiority in exploiting competitive intelligence and a sophisticated suite of analytics that accompany digital transactions, is surfacing in its agile discounting strategies, and its ability to continuously refresh product lines during key sales periods.

This Boxing Day in the UK, fashion proved to reveal divergent discounting strategies between retailers, while only marginal differences in approach were visible in electronics — both high volume categories around Christmas season.

Overall, December 2017 in UK marked a strong validation of online retail’s influence and we can expect a continuation of it’s ability to harness discounting with extensive product offerings, in order to lure shoppers away from in-store.

If you’re interested in DataWeave technology, and how we deliver Competitive Intelligence as a Service to retailers and consumer brands, check out our website!

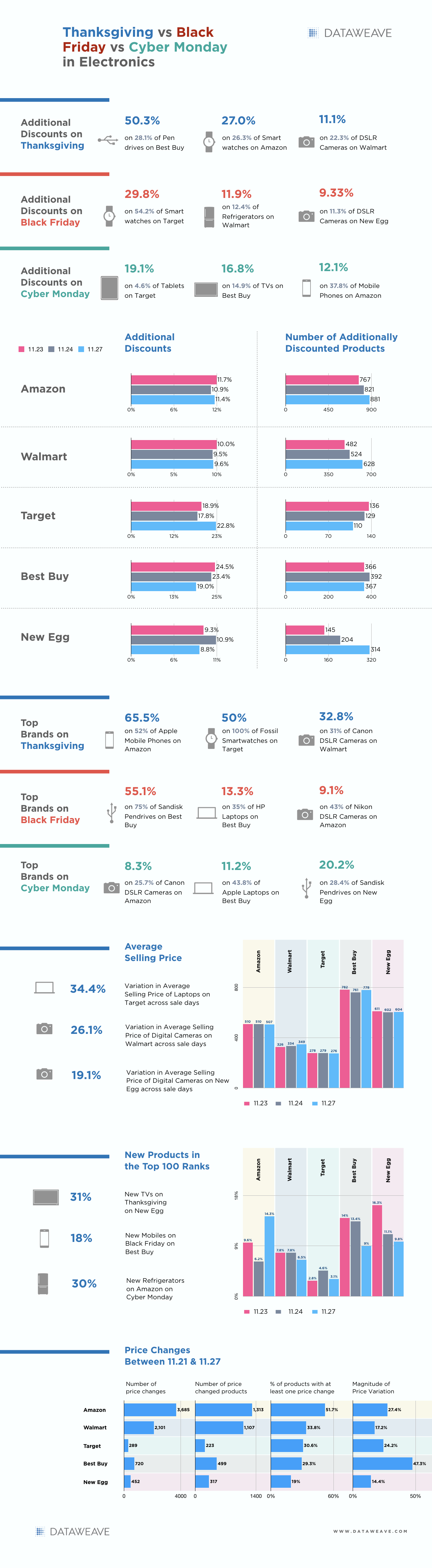

![[INFOGRAPHIC] Thanksgiving vs Black Friday vs Cyber Monday: The Electronics Price War Heats Up](https://stage-cdnblog.dataweave.com/wp-content/uploads/2018/09/a4-e1688041211819.jpeg)