Picture this: You wake up one morning to discover that your top competitor reduced their prices overnight. And now your shopper traffic has tanked and your sales have taken a hit.

Unfortunately, this is a common scenario because your customers can compare prices online in seconds—and loyalty lies with the budget.

So, how can you protect your business? Price monitoring.

Price monitoring solutions can help you keep abreast of competitor price changes—which, of course, will help you improve your pricing strategies, retain your customers, and maximize your profits.

How? In this article, we’ll explore:

- What is price monitoring

- The key benefits of price monitoring for retailers and brands

- What a capable price monitoring solution can do

What Is Price Monitoring?

Price monitoring is the process of tracking and analyzing your competitor’s prices across various online and offline platforms. By monitoring competitors’ prices, you can understand market price trends and adjust your prices strategically—which, in turn, helps you remain competitive, increase margins, and improve customer retention.

5 Benefits of Price Monitoring

Competitor price monitoring can help you:

- Gain a competitive edge: Competitor price tracking allows you to adjust your prices to remain attractive to consumers.

- Maximize revenue: With timely pricing data, you’re empowered to identify optimum price points that strike a delicate balance between maximizing revenue and maintaining customer loyalty.

- Retain customers: Consumers are looking for the most value for their dollar, so maintaining consistently competitive pricing is crucial for retaining loyal customers.

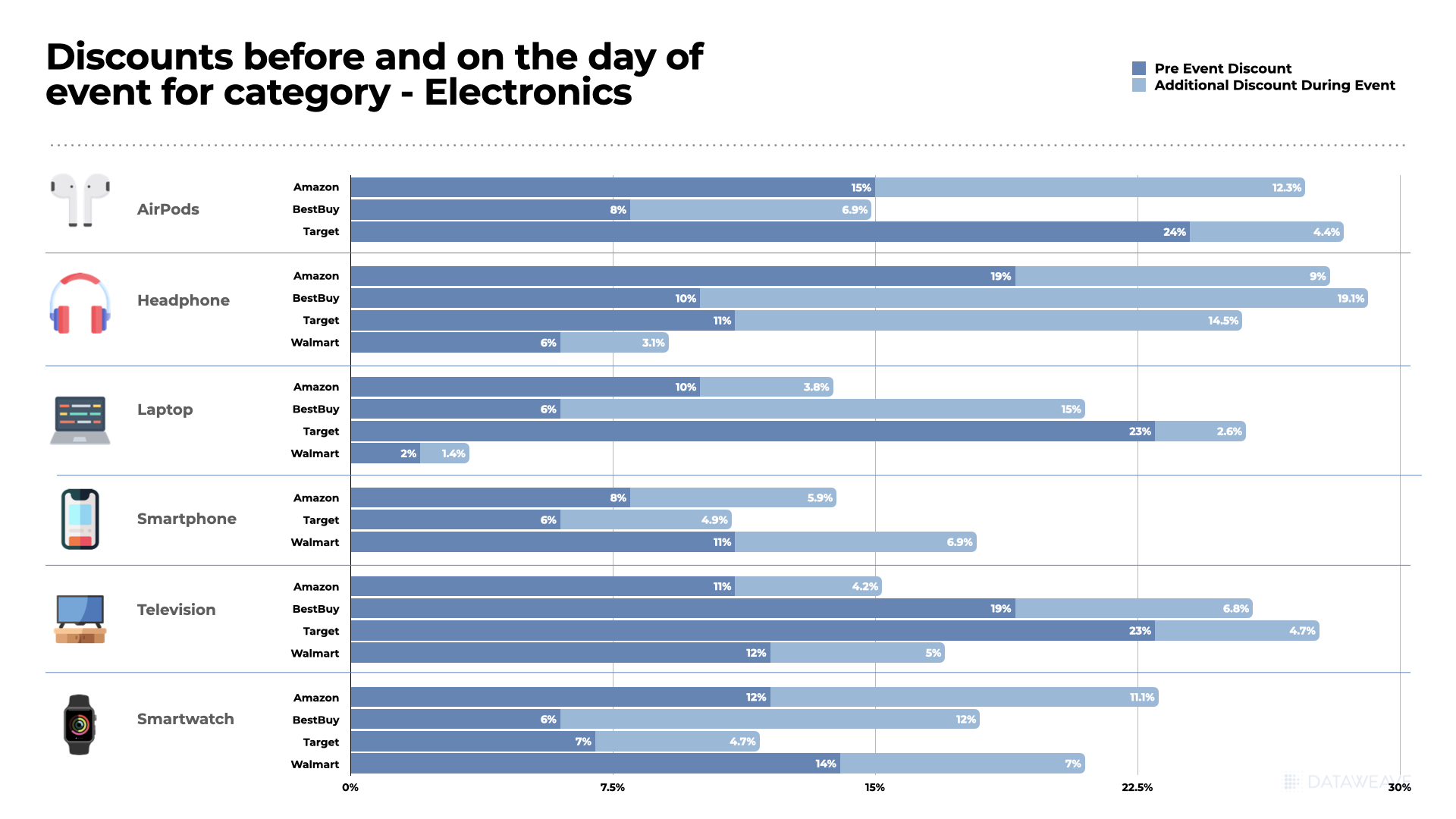

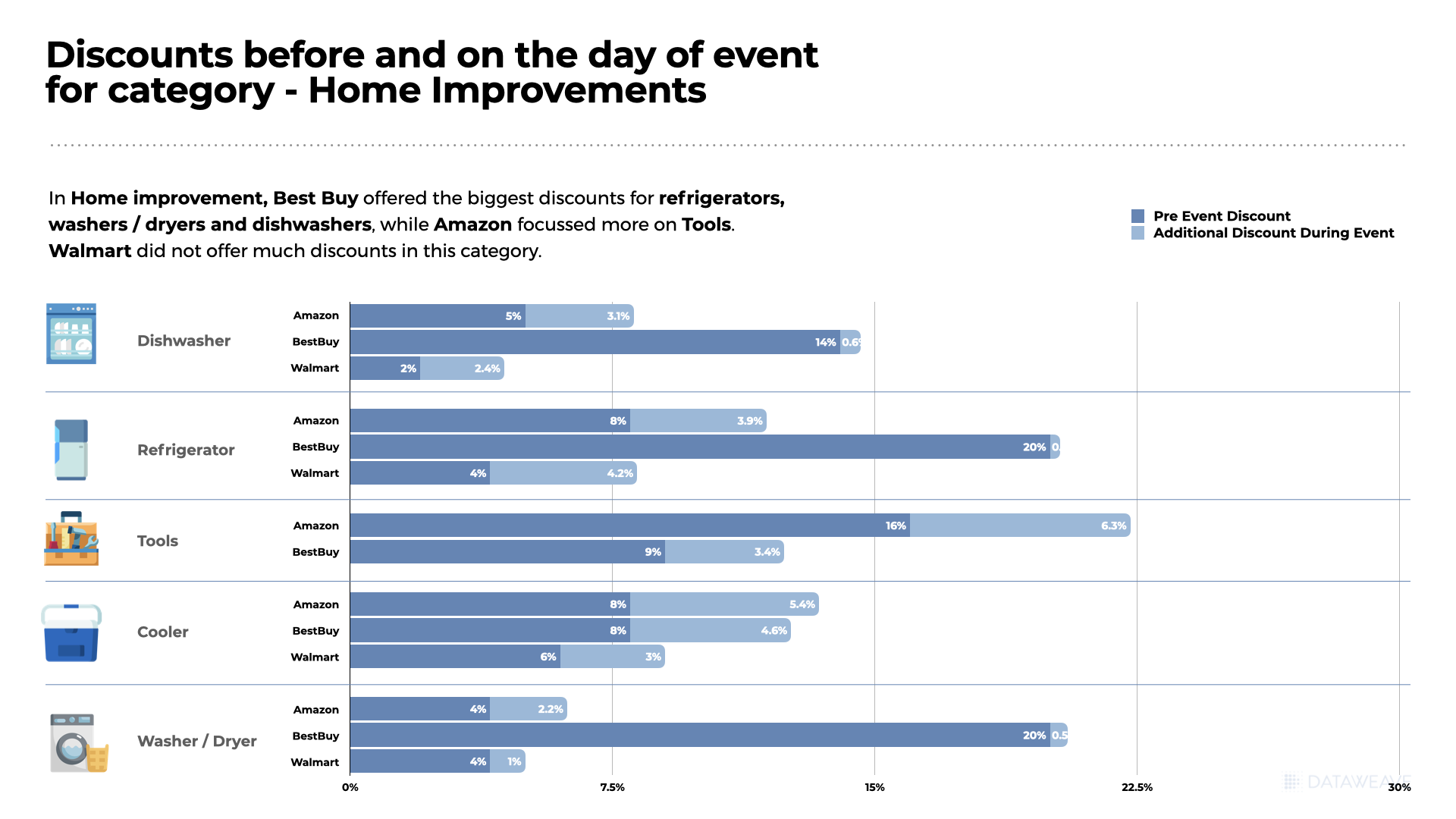

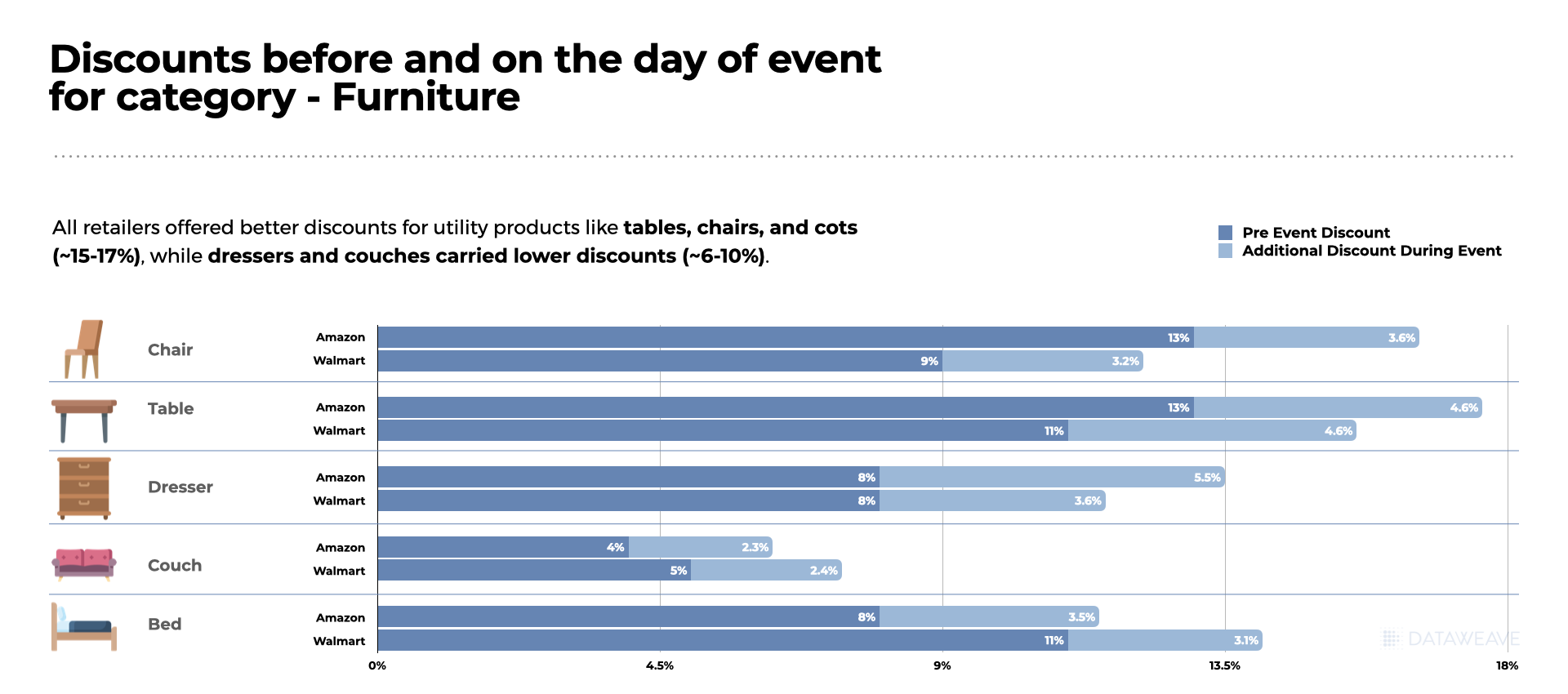

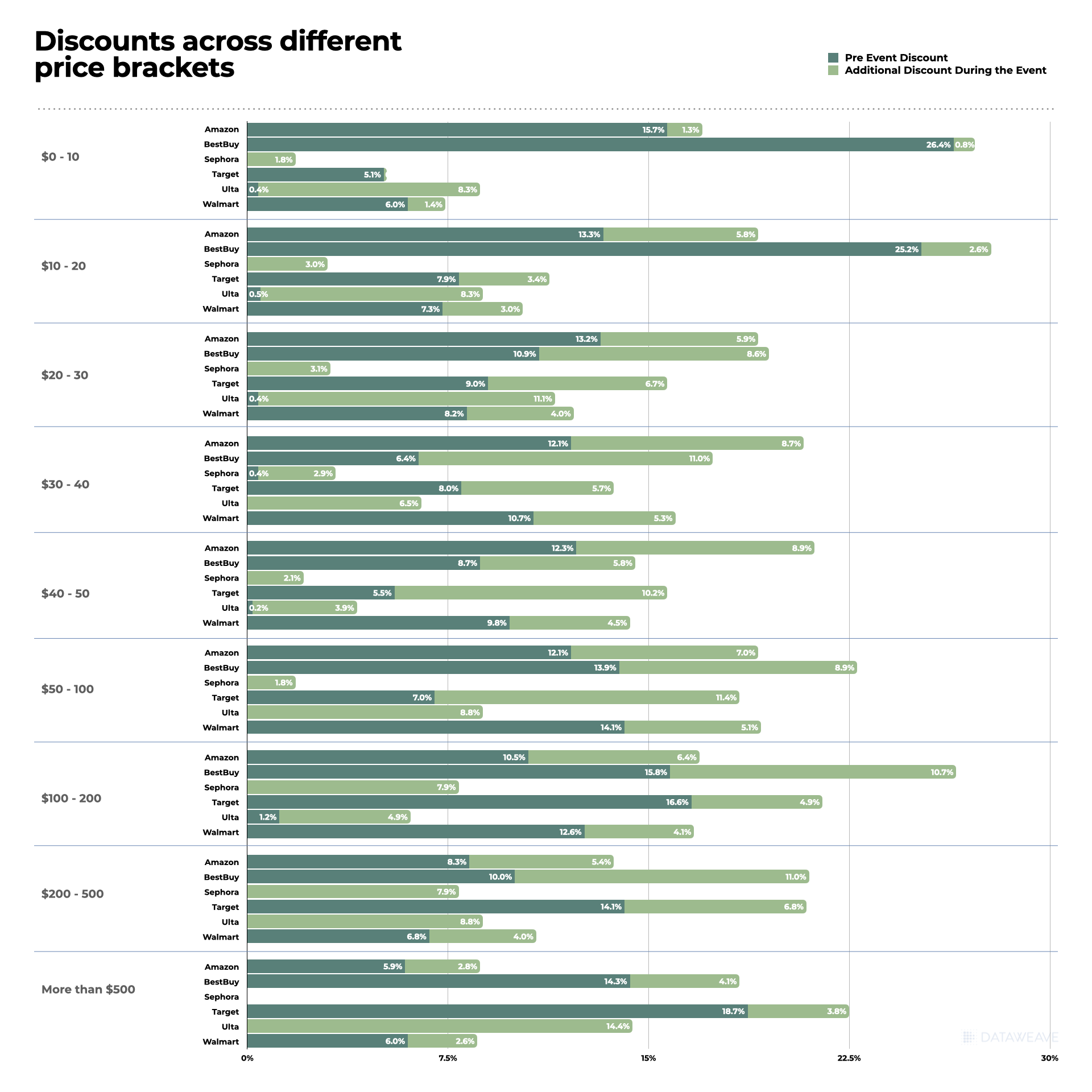

- Understand promotional effectiveness: Price monitoring helps businesses evaluate the effectiveness of their promotions and discounts. By comparing the impact of different pricing strategies, businesses can refine their promotional tactics to maximize sales and customer engagement.

- Understand market movements: By analyzing historical pricing data, you’re better positioned to anticipate future pricing changes — and adjust your strategies accordingly.

4 Essential Capabilities of Price Monitoring Software

Here are four capabilities to look for when choosing a price monitoring system.

1. AI-Driven Product Matching

Product matching is the process of identifying identical or similar products across different platforms to ensure accurate price comparisons.

If your price monitoring solution can’t reliably match your products with competitors’ across various sales channels at scale, you’ll end up with poor data. Inaccurate data will then lead you to make misinformed pricing decisions.

Product matching needs to be accurate and comprehensive, covering a wide range of products and product variations—even for including private label products.

For example, AI-driven product matching can recognize a specific brand and model of sneakers across multiple online stores—even if product descriptions and images differ. Here’s how it works in a nutshell:

- Sophisticated algorithms and deep learning architecture enable AI to identify and match products that aren’t identical but share key characteristics and features.

- Using unified systems for text and image recognition, the AI matches similar SKUs across hundreds of eCommerce stores and millions of products.

The AI zeroes in on critical product elements in images, like a t-shirt’s shape, sleeve length, and color. - The AI also extracts unique signatures from photos for rapid, efficient identification and grouping across billions of indexed items.

DataWeave’s AI algorithm can initially match products with 80–90% accuracy. Then, humans can bring contextual judgement and make nuanced decisions that the AI might miss to correct errors quickly and push for accuracy closer to 100%. By integrating AI automation with human validation, you can achieve accurate and reliable product-matching coverage at scale.

2. Accurate and Comprehensive Data Collection and Aggregation

The insights you derive are only as good as the data you collect. However, capturing comprehensive pricing data is tough when your competitors operate on multiple platforms.

For truly effective price monitoring insights, you need consistent, comprehensive, and highly accurate data. This means your chosen price monitoring system should:

- Scrape data from various sources, such as desktop and mobile sites and mobile applications.

- Pull data from various online platforms like aggregators, omnichannel retailers, delivery intermediaries, online marketplaces, and more.

- Handle data from different regions and languages.

- Collect data at regular intervals to ensure timeliness.

DataWeave’s online price monitoring software covers all of these bases and more with a fast, automated data source configuration system. It also allows you to painlessly add new data sources to scrape.

Instead of incomplete or inaccurate data, you’ll have comprehensive and up-to-date data, allowing you to respond quickly to market changes with confidence.

3. Seamless Normalization of Product Measurement Units

You can’t compare apples to oranges—or price-per-kilogram to price-per-pound.

For price monitoring to be accurate, there must be a way to normalize measurement units—so that we’re always comparing price-per-gram to price-per-gram. If we compare prices without taking into account measurement units, our data will be misleading at best.

Let’s take a closer look. Say that your top competitor sells 12oz cans of beans for $3, and you sell 15oz cans for $3.20. At first glance, your larger cans of beans will appear more expensive—but that’s not true. If we normalize the measurement unit—in this example, an oz—the larger can of beans offers more value to customers.

Unit of measure normalization facilitates sound price adjustments based on accurate and reliable data. For this reason, every business needs a price tracking tool that can guarantee accurate comparisons by normalizing unit measurements—including weight, volume, and quantity.

4. Actionable Data and an Intuitive User Experience

Knowledge is only powerful when applied—and price monitoring insights are only useful when they’re accessible and actionable.

For this reason, the best price monitoring software doesn’t just provide insights based on accurate and comprehensive data, but it also provides several ways to understand and deploy those insights.

Ideal price monitoring solutions provide customized pricing alerts, intuitive dashboards, detailed reports, and visuals that are easy to interpret—all tailored to each particular team or a team member’s needs. These features should make it easy for team members to compare prices against those of competitors in specific categories and product groupings.

Your price tracking tool should also permit flexible API integrations and offer straightforward data export options. This way, you can integrate competitive pricing data with your pricing software, Business Intelligence (BI) tools, or Enterprise Resource Planning (ERP) system.

4 Ways Retailers Can Leverage Price Monitoring

Retailers can use price monitoring tools to remain competitive without compromising profitability—here’s how:

1. Track Competitors’ Prices

Competitor price monitoring helps you avoid being undercut—and, as a result, maintain market share. By tracking competitor prices in real-time, you can adjust prices to remain competitive, especially in dynamic markets. Ideally, you should monitor both direct competitors selling the same products and indirect competitors selling similar or alternative products. This way, you’ll have a complete picture of market prices and can make more informed pricing adjustments.

2. Understand Historical and Seasonal Price Trends

As a retailer, you may want to analyze historical data to identify price patterns and predict future price movements—especially in relation to holidays and seasonal products. Knowing what’s coming, you’re better positioned to plan for pricing changes and promotional campaigns.

3. Implement Dynamic Pricing

Dynamic pricing is the process of adjusting prices based on real-time market conditions, product demand, and competitors’ prices—allowing you to respond faster to market changes to maintain optimized prices.

4. Optimize Promotional Strategies

Price monitoring tools can track retail promotions across numerous online and offline sales avenues, providing insight into the nature and timing of competitors’ promotions. This data can help you determine which promotions are most effective—and which aren’t—allowing you to improve your own promotions and discounts, and allocate marketing resources where it matters most. This is especially beneficial during peak sales periods.

3 Ways Brands Can Employ Price Monitoring

Here are three ways brands can use price monitoring to remain profitable, protect brand equity, and gain a competitive edge.

1. Maintain Consistent Retail Prices

Minimum advertised price (MAP) policies are designed to prevent retailers from devaluing a brand while ensuring fair competition among retailers. Price monitoring applications allow your brand to track retailers’ prices to detect MAP policy violations. Data in hand, you can maintain consistent pricing across online sales channels, physical stores, and retail stores’ digital shelves — and, critically, protect your brand equity.

2. Improve Product and Brand Positioning

When you understand how your products’ prices compare to those of competitors, you can set prices to improve brand positioning. For example, if you want to position your brand as luxurious and high-quality, you need to set higher product prices than budget-friendly alternative products.

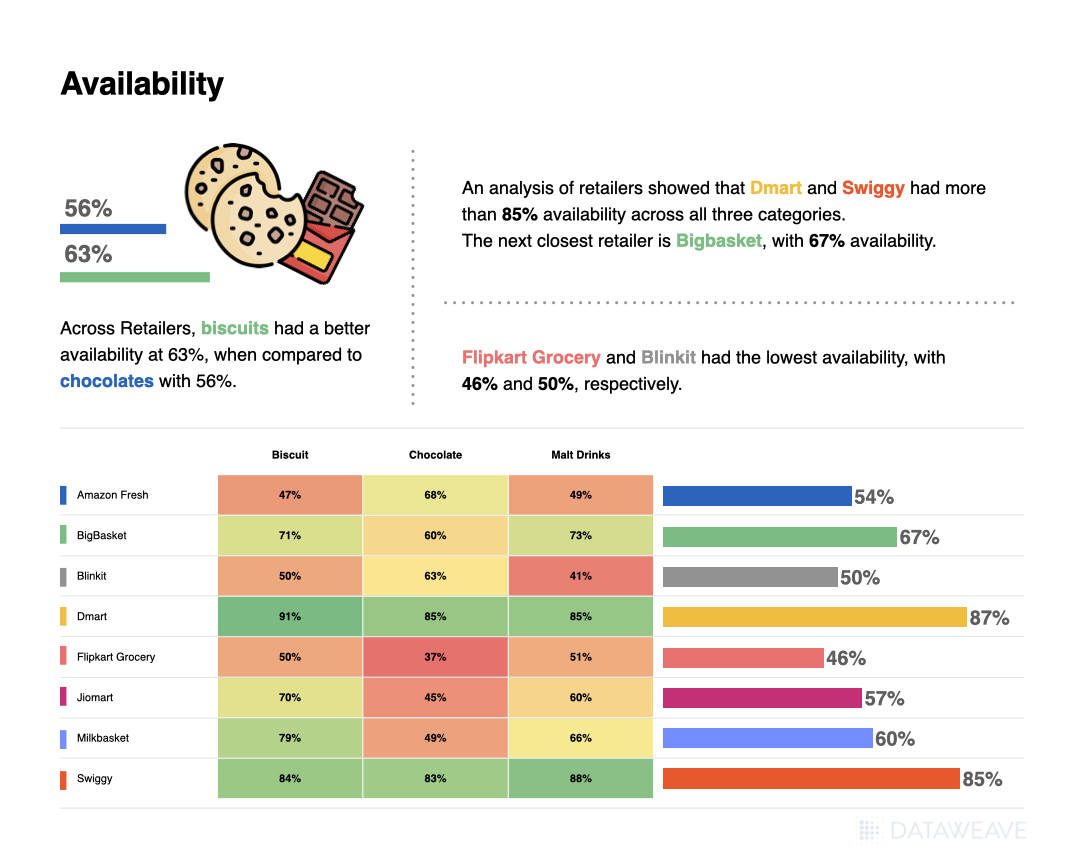

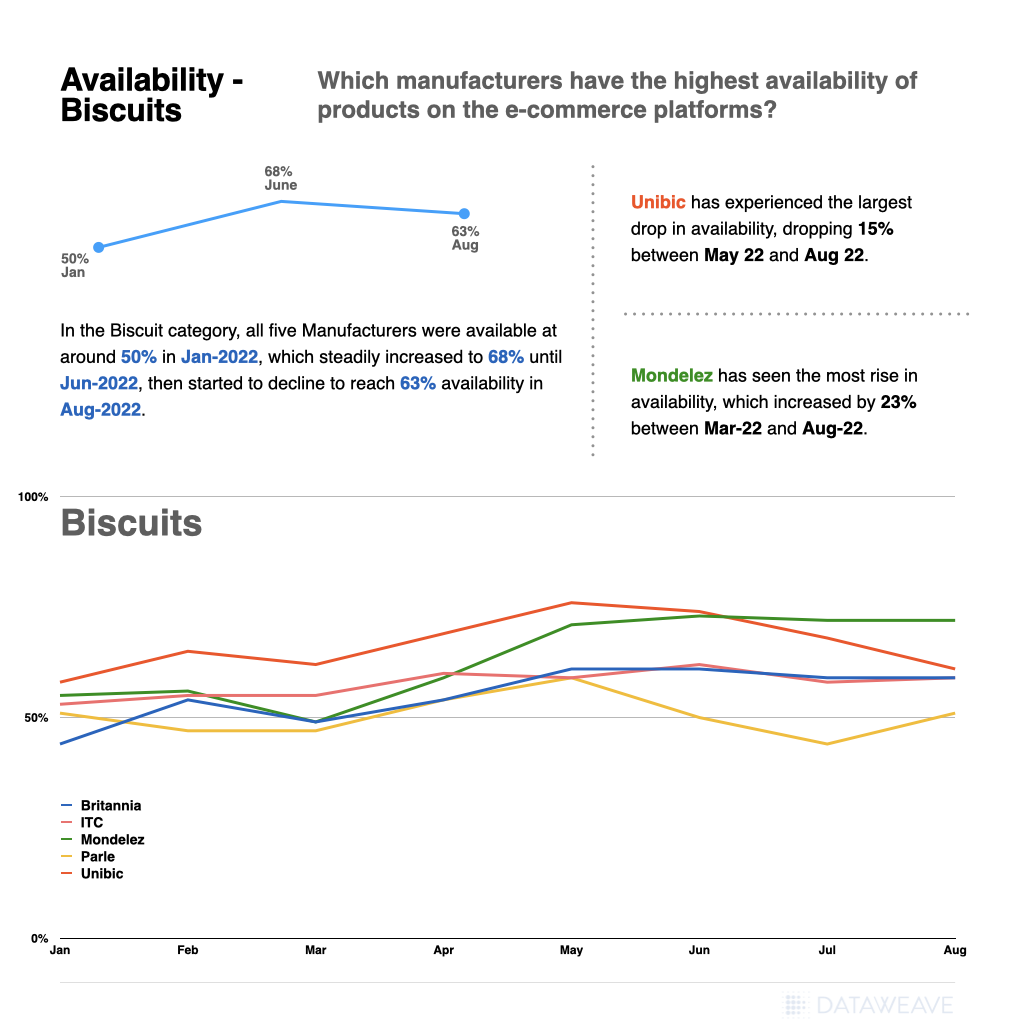

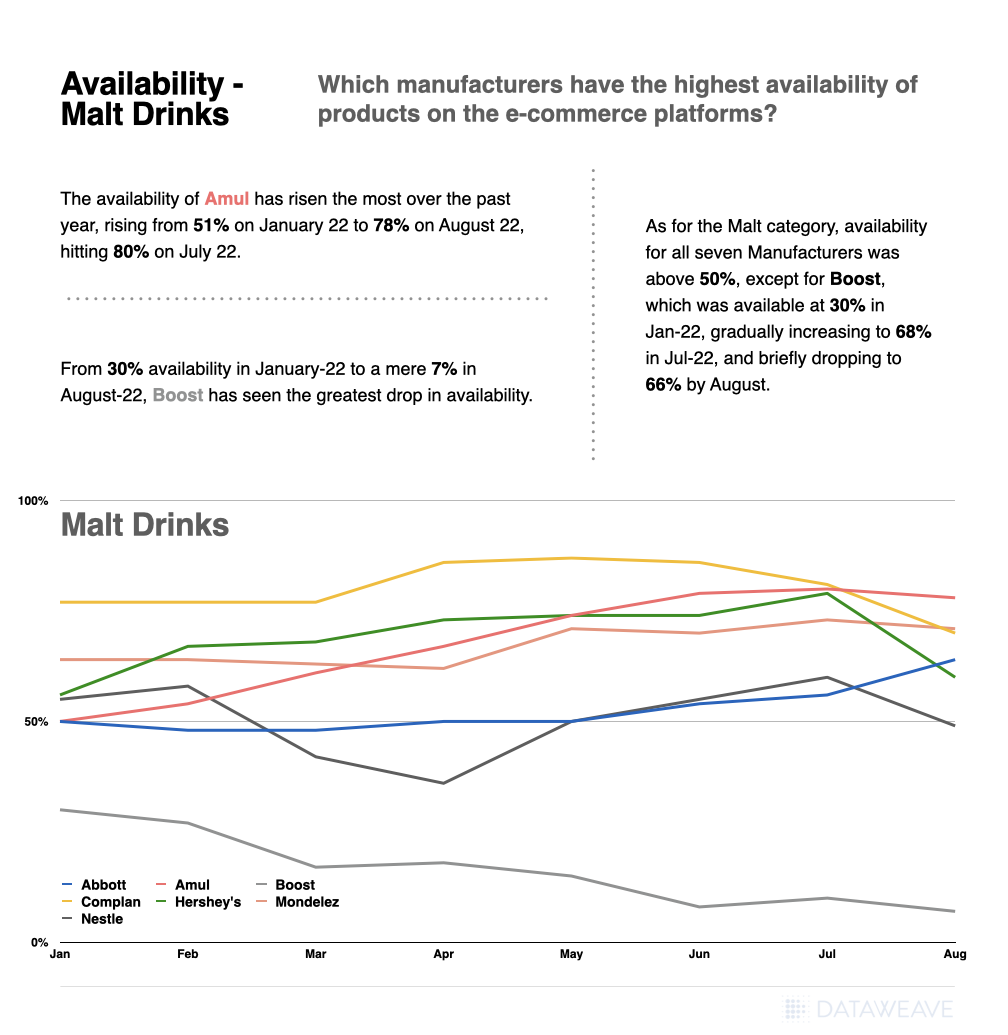

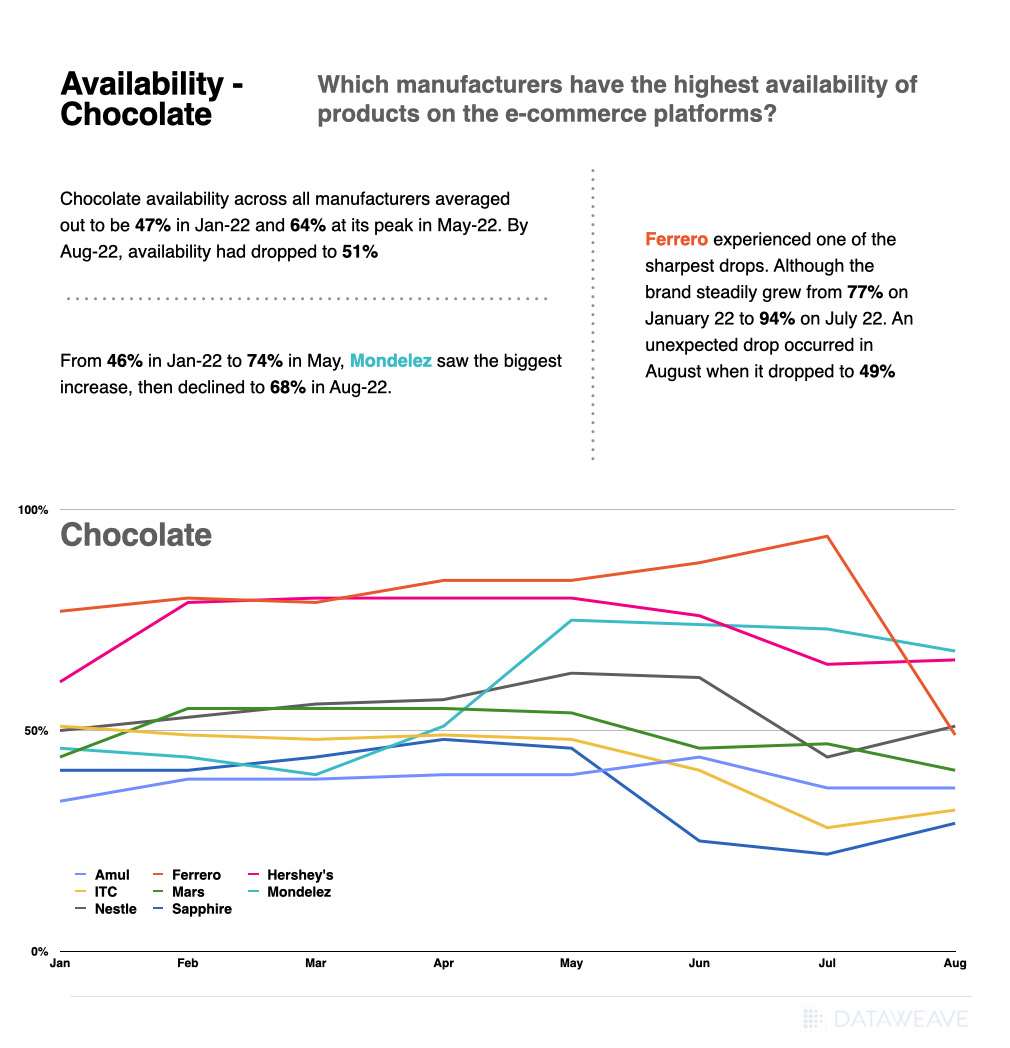

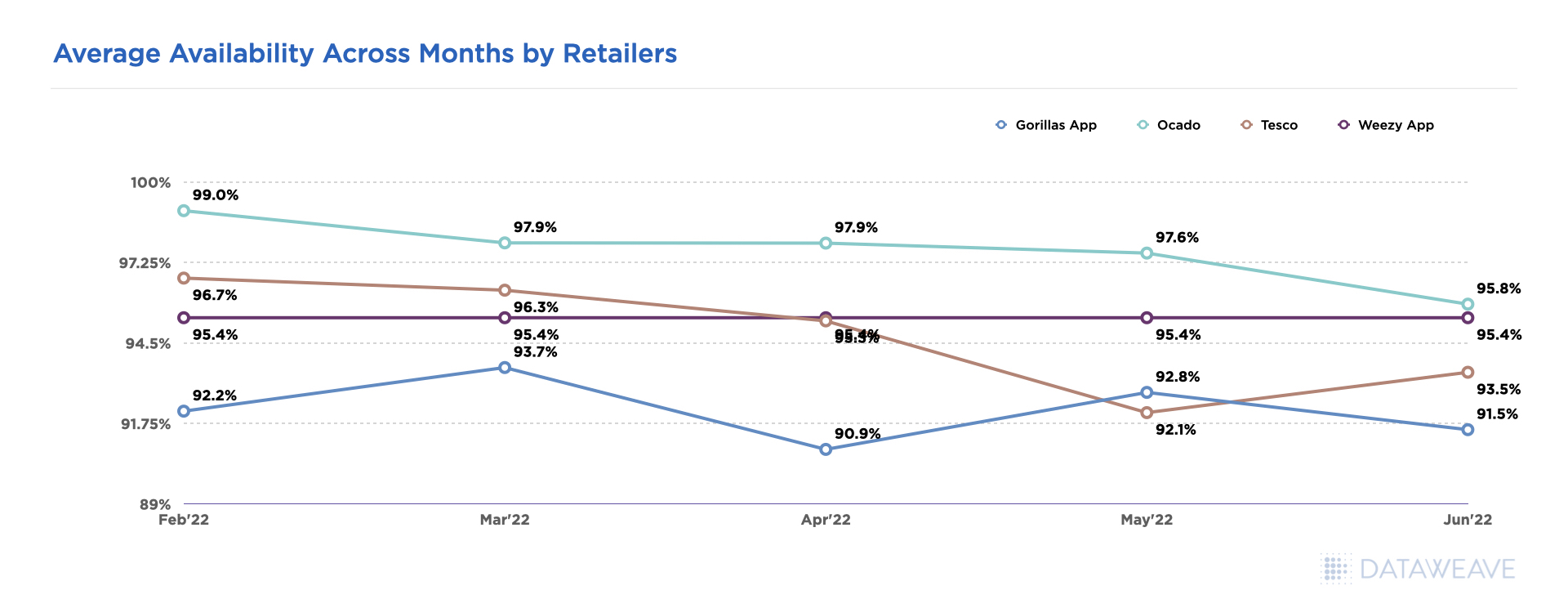

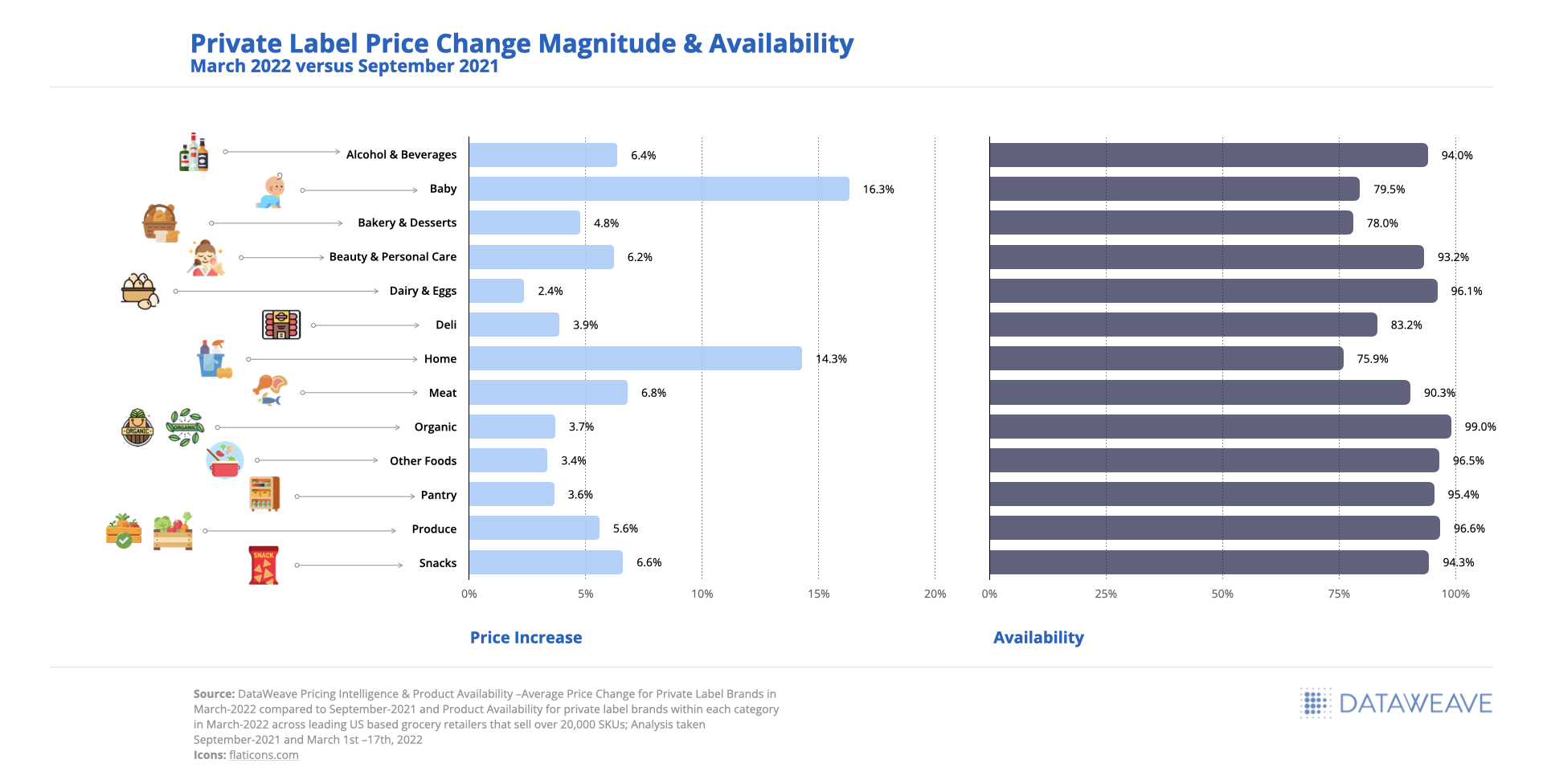

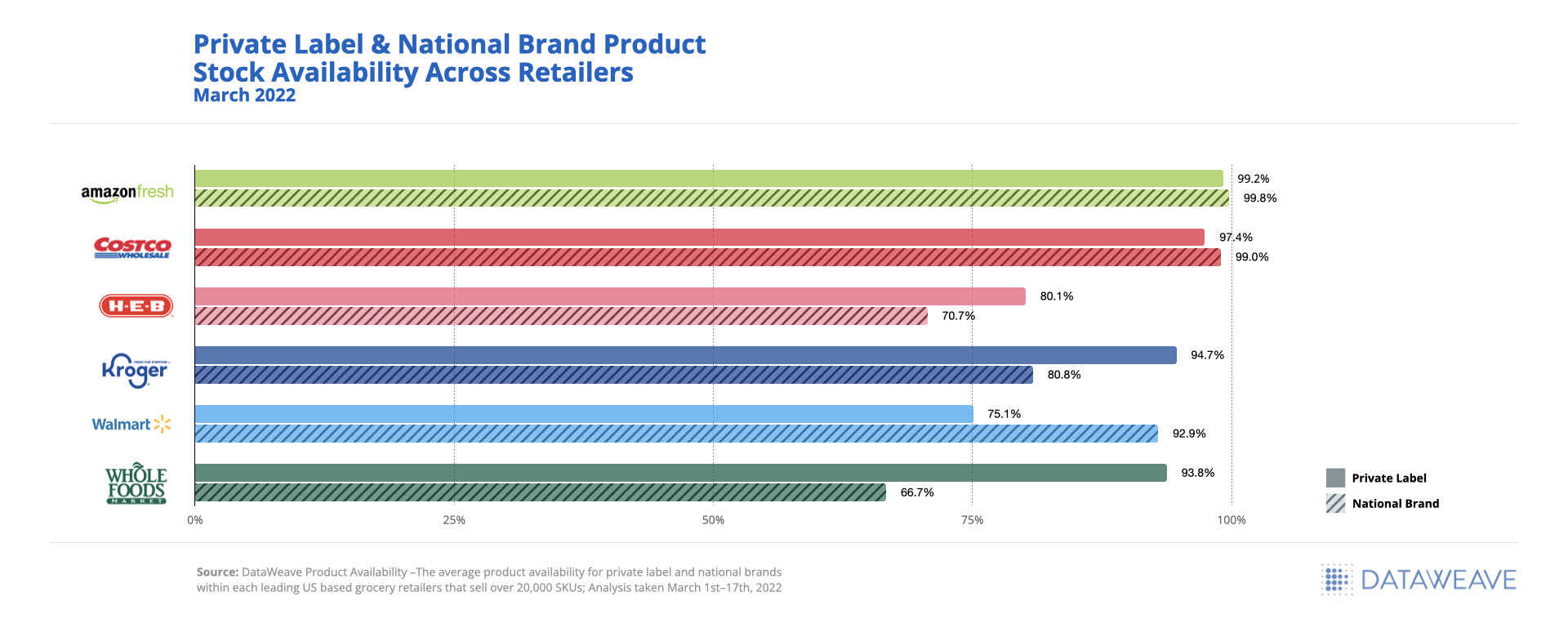

3. Ensure Product Availability

You can use a price monitoring solution to track product availability to ensure products are always in stock, even across different physical stores and online marketplaces. If a product is frequently sold out, you can adjust production levels or help retailers to improve their inventory management.

Key Takeaways: E-commerce Price Monitoring

Price monitoring software allows you to compare your products’ prices with competitors. This valuable data can help you:

- Optimize revenue through timely price changes and dynamic pricing

Avoid being undercut by competitors - Improve pricing strategies and promotions to increase sales and retain customers

- Maintain consistent prices across sales channels

To learn more, check out our article, What is Competitive Pricing Intelligence: The Ultimate Guide here or reach out and talk to us today!