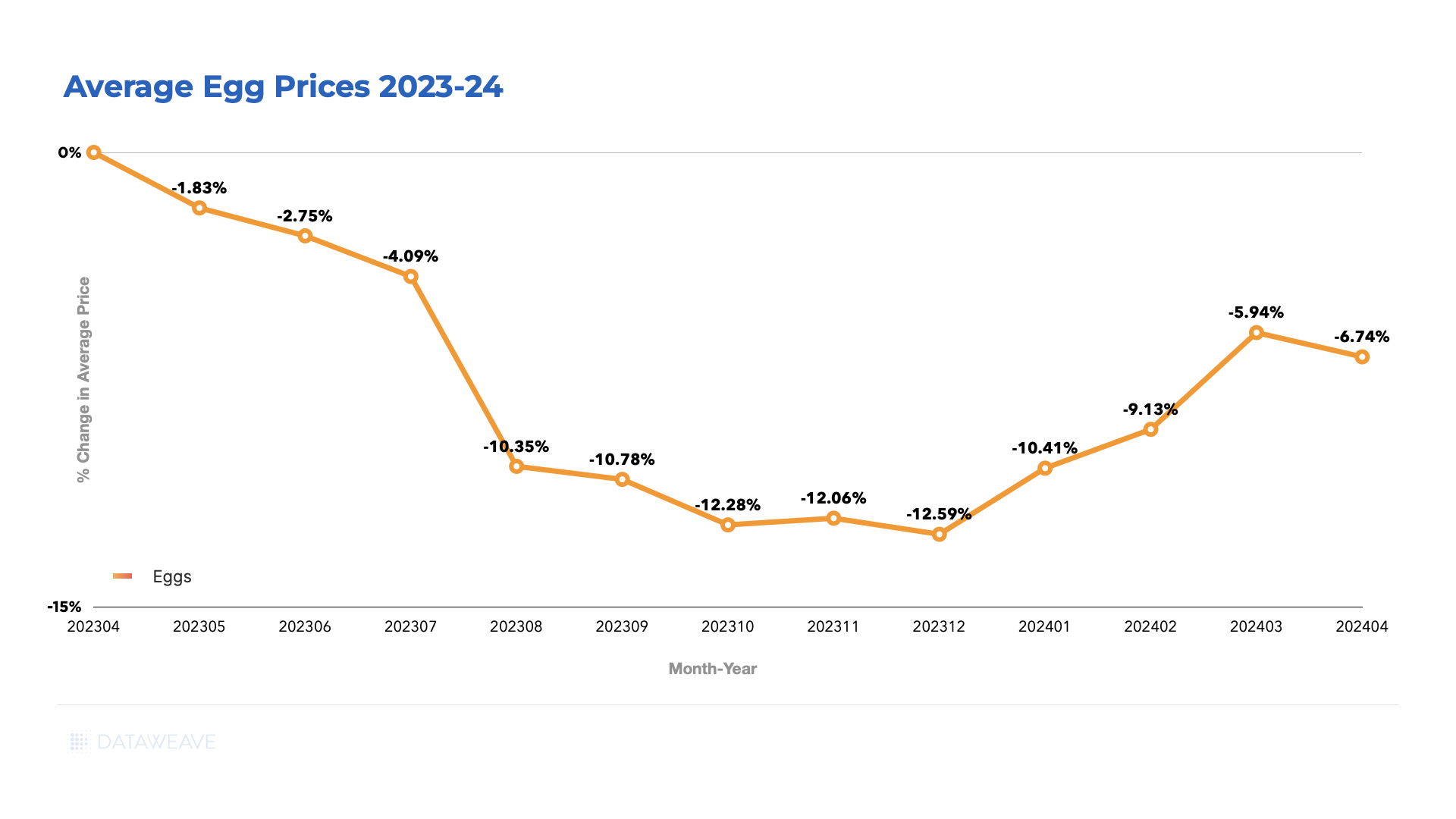

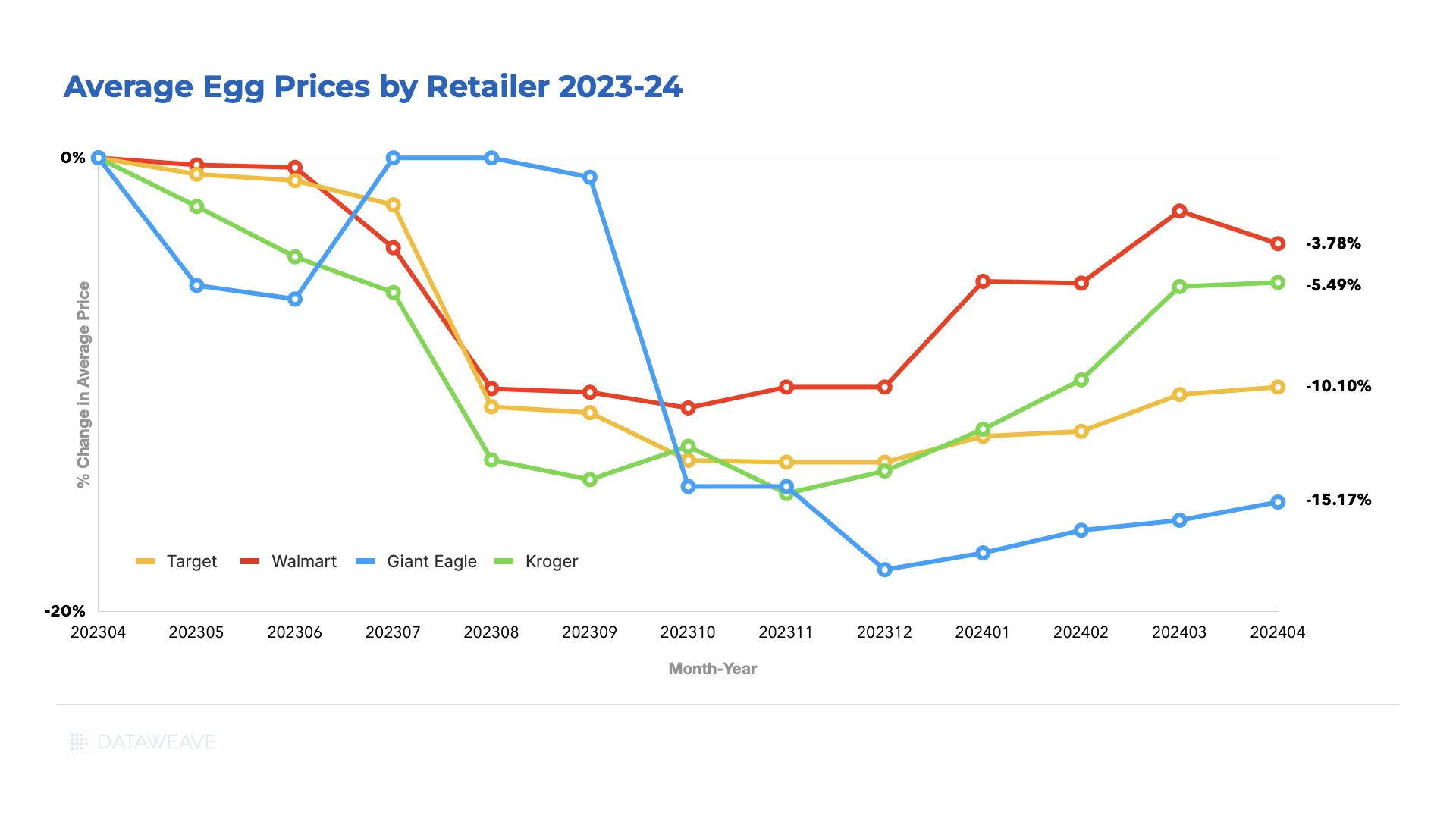

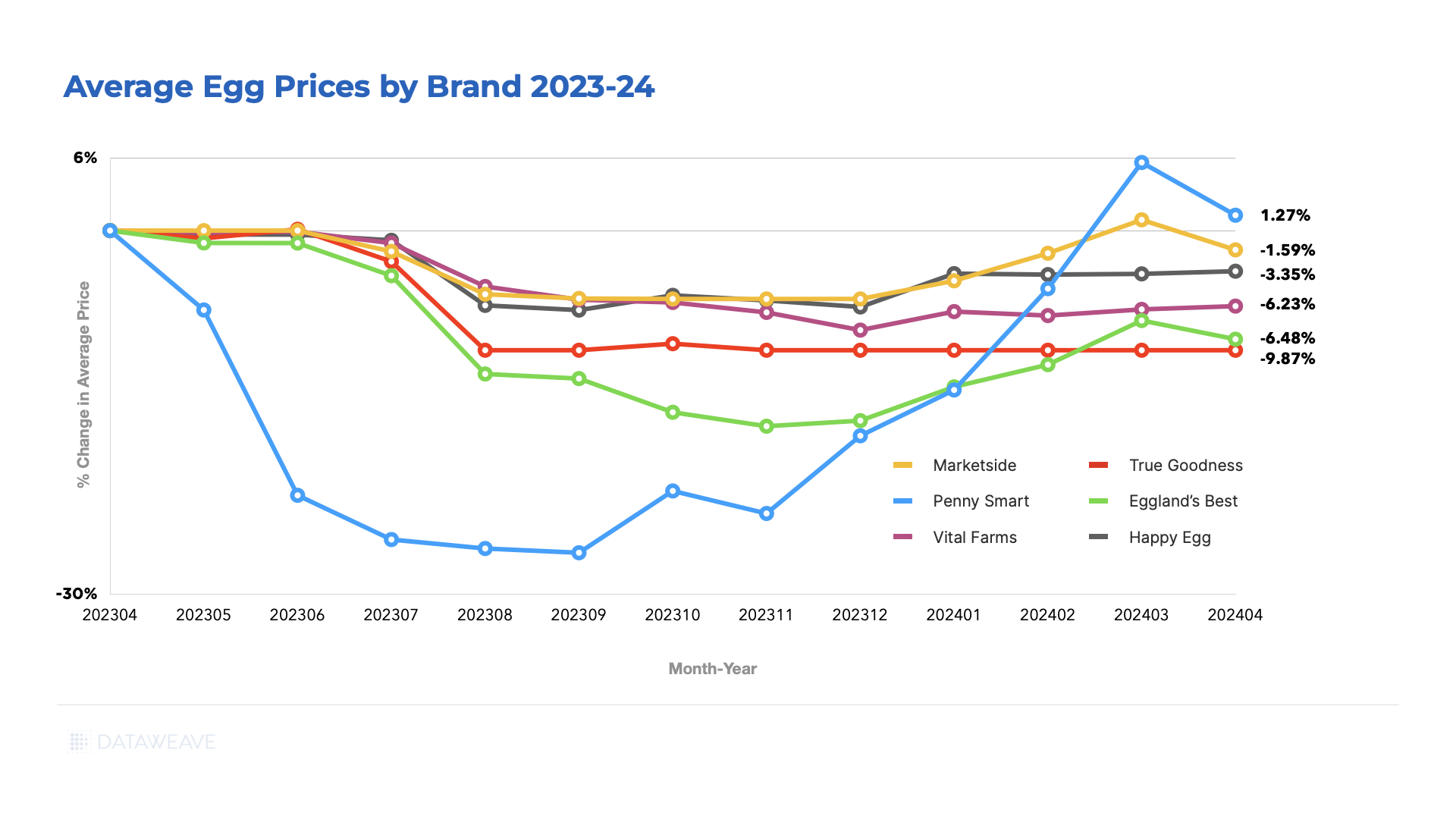

When egg prices surged 70% during the 2023 avian flu outbreak, grocery retailers faced a critical dilemma: maintain margins and risk losing customers, or absorb costs and watch profits evaporate. Similarly, rising olive oil and chocolate prices also had domino effects, cascading down from retailers to consumers. In each of these scenarios, those with sophisticated pricing intelligence systems adapted swiftly, finding the sweet spot between competitiveness and profitability. Others weren’t so fortunate.

This scenario continues to play out daily across thousands of products in the grocery sector. From breakfast cereals to fresh produce to bottled water, retailers must orchestrate pricing across a variety of categories – each with its own competitive dynamics, margin requirements, and price sensitivity patterns.

The Evolution of Grocery Pricing Intelligence

Imagine these scenarios in the grocery industry:

- Milk prices spike during a supply shortage.

- Your competitor drops egg prices by 20%.

- Fresh produce costs fluctuate with an unseasonable frost.

For grocery retailers, these aren’t occasional challenges—they’re Tuesday. Reacting to each pricing crisis as it comes isn’t just exhausting—it’s a recipe for shrinking margins and missed opportunities.

Think of it this way: If you’re constantly playing defense with your pricing strategy, you’re already two steps behind. Commoditized items like milk and eggs face intense price competition, while seasonal products and fresh produce demand constant attention. Simply matching competitor prices or adjusting for cost changes isn’t enough anymore. What’s needed is a proactive approach that anticipates market shifts before they happen and turns pricing challenges into competitive advantages. This is where price management comes in.

Price management has transformed from simple competitor checks into a strategic power play that can make or break a retailer’s market position. Weekly manual adjustments have given way to a long-term strategic view, driven by data analytics and market intelligence. Here are the basics of how price management in grocery retail works today.

Three Pillars of Grocery Price Management

1. Smart Data Collection: Building Your Foundation

The journey begins with comprehensive data collection and storage across your entire product ecosystem. This means:

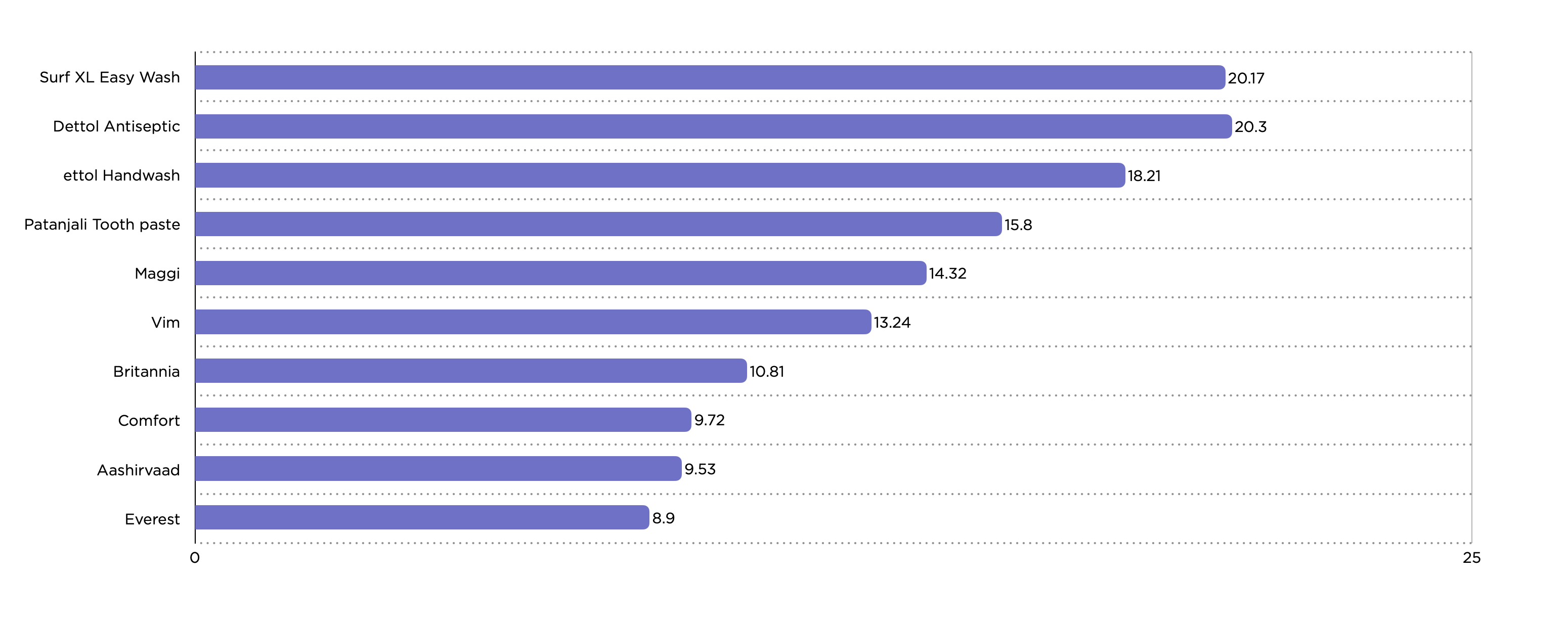

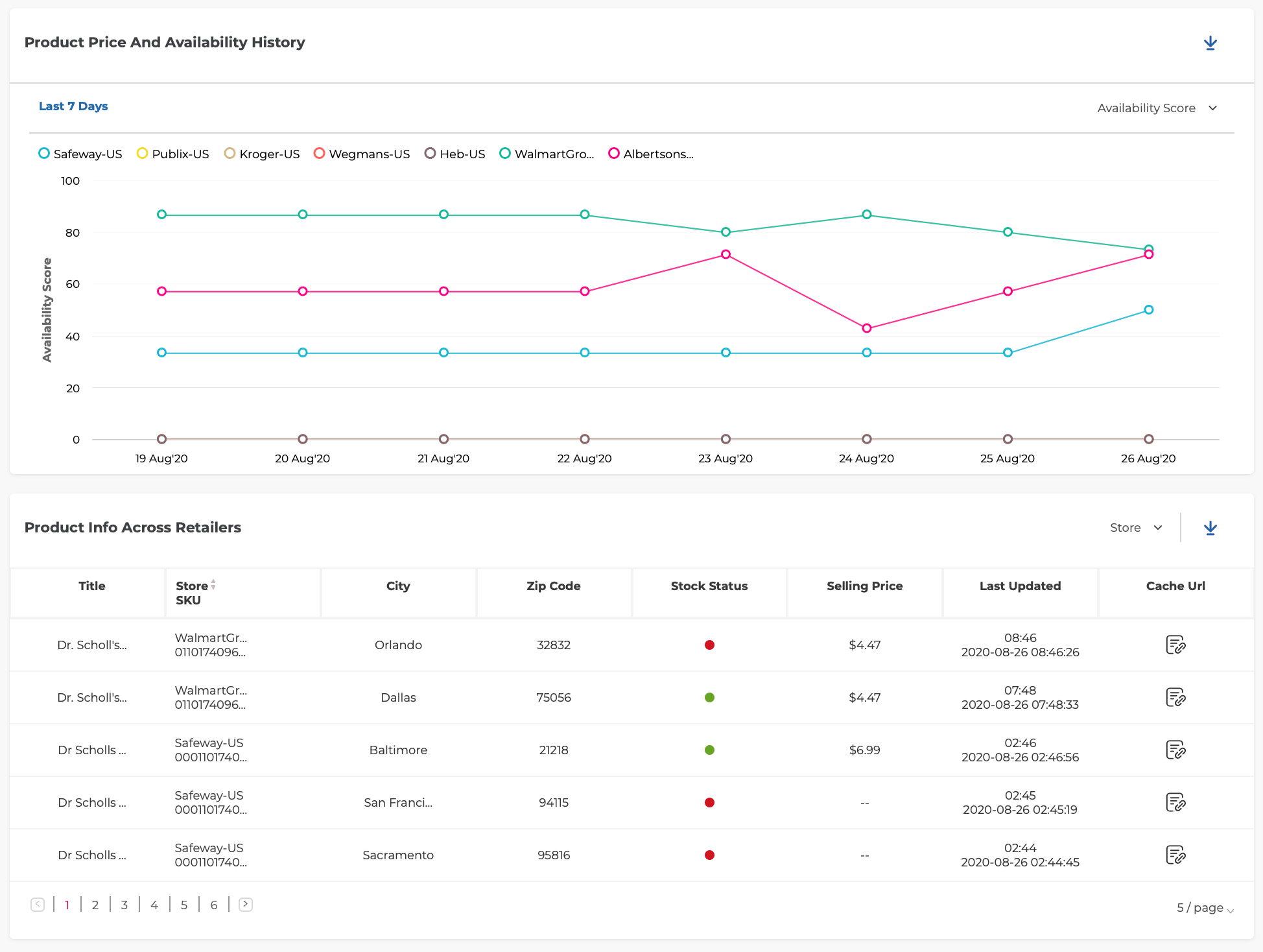

- Complete Coverage Of All SKUs Across All Stores: Tracking prices for all SKUs across all stores, with particular attention to high-velocity items and volatile categories.

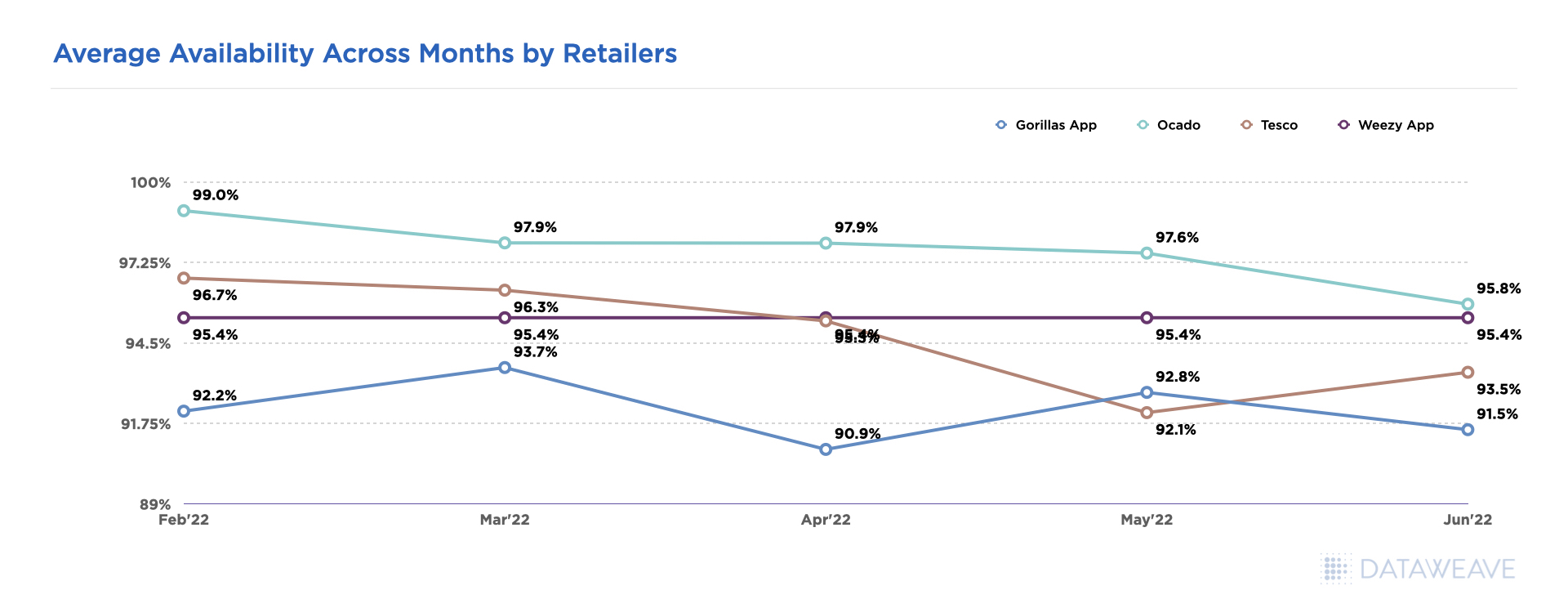

- Dynamic Monitoring: Tracking prices across different time frequencies as grocery prices are highly volatile for different categories. So daily tracking for volatile items like dairy and produce, and weekly for more stable categories may be needed.

- Competitive Intelligence: Gathering data not just on prices, but on promotions, pack sizes, and private label alternatives.

- Infrastructure to Support Large Volumes of Data: Partnering with external data and analytics providers to bridge the gap when retailers struggle with the scale of digital infrastructure these data sets require.

2. Intelligent Data Refinement: Making Sense of the Numbers

Raw data alone isn’t enough—it needs context and structure to become actionable intelligence. This is called Data Refinement—the process of establishing meaningful relationships within the data to facilitate the extraction of valuable insights. This refinement stage is closely tied to the data collection strategy, as the quality and depth of the insights derived depend on the accuracy and coverage of the collected data.

Data refinement includes several key processes:

Advanced Product Matching

Picture this: You’re tracking a competitor’s pricing on organic apples. Simple, right? Not quite. Yes, Universal Product Codes (UPCs) and Price Lookup Codes (PLUs) are present in Grocery to standardize product identification across different retailers—unlike the fashion industry’s endless style variations. Still, product matching isn’t as straightforward as scanning barcodes.

Here’s the catch: many retailer websites don’t display them. Then there’s the private label puzzle—your “Store’s Best” organic apples need to match against competitors’ house brands, each with their own unique UPC. Throw in different sizes (4 Apples vs. 1Kg of Apples), regional product names (fancy naming for plain old arugula), and international brand variations (like the name for Sprite in the USA and China), and you’ve got yourself a complex matching challenge that would make conventional pricing intelligence providers sweat.

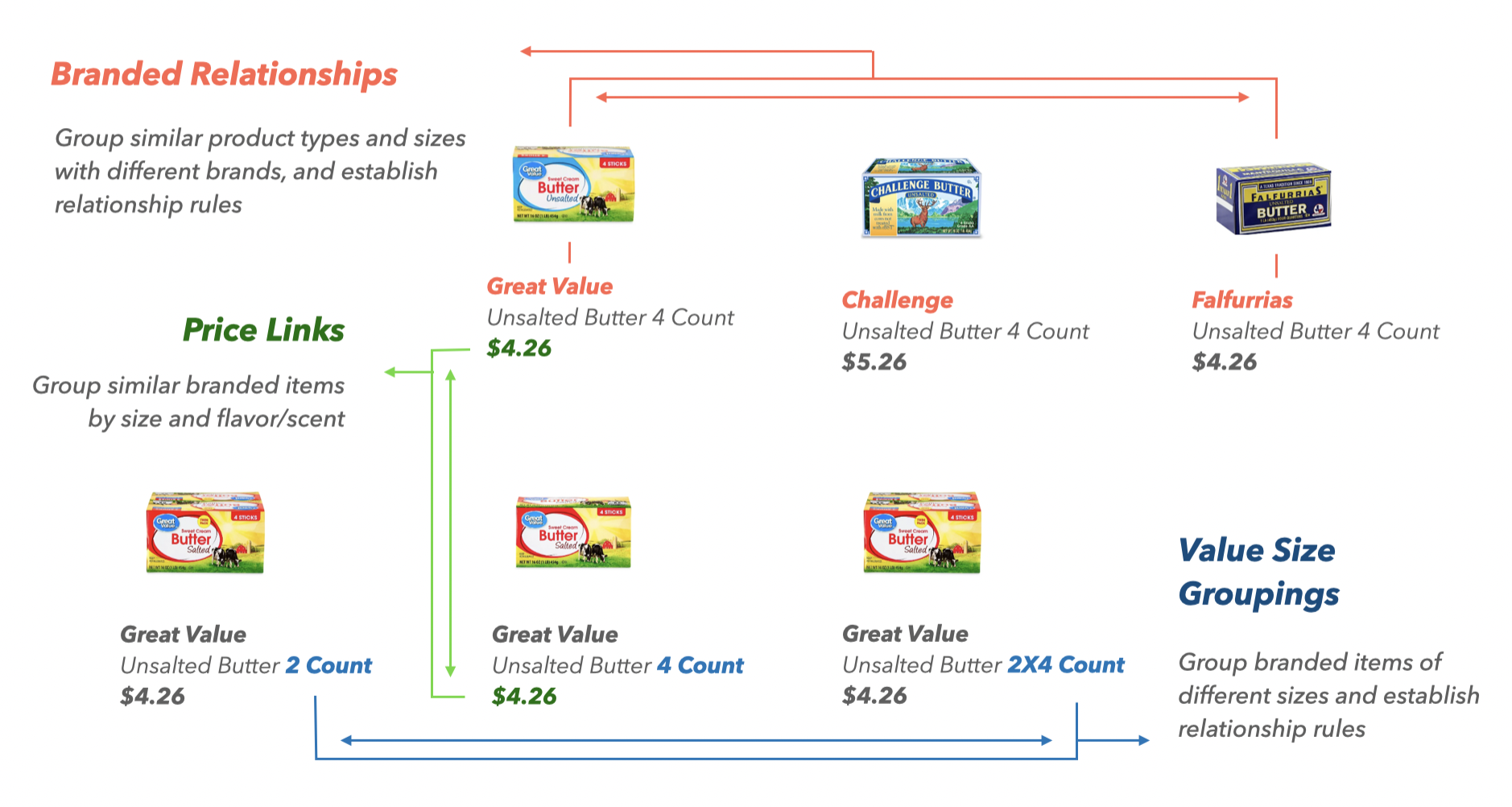

Custom Product Relationships for Consistent Pricing and Competitive Positioning

Think like a shopper browsing the dairy aisle. You regularly buy your family’s favorite organic yogurt, the 24oz tub. But today, you notice the larger 32oz size is on sale – except the 24oz isn’t. As you stand there, confused, you wonder: Is the sale only for the bigger size? Did I miss a promotion? Should I buy the 32oz even though it’s more than I need?

For shoppers, this inconsistent pricing across product variations creates a frustrating experience. Establishing clear relationships between related items in your catalog is essential for maintaining consistent pricing and a coherent competitive strategy.

Start by linking products based on attributes like size, brand, and packaging. That way, when you adjust the price of the 32oz yogurt, the 24oz version automatically updates too – no more scrambling to ensure uniform pricing across your assortment. Similarly, products of the same brand but with flavor variations should be connected to keep pricing consistent.

Taking this one step further, mapping your competitors’ exact and similar products is crucial for comprehensive competitive intelligence. Distinguishing between premium and private label tiers, national brands, and regional players gives you a holistic view of the landscape. With this understanding, you can hone your pricing strategies to maintain a clear, compelling position across your entire category lineup.

Consistent pricing, whether across your own product variations or against competitors, provides clarity and accuracy in your overall competitive positioning. By establishing these logical connections, you avoid the customer confusion of seemingly random, inconsistent discounts – and ensure your pricing strategies work in harmony, not disarray.

The Role of AI and Data Sciences in Data Refinement

On the surface, linking products based on attributes like size, brand, and packaging seems like a no-brainer. But developing and maintaining the systems to accurately and automatically identify these connections? That’s a whole different animal.

Think about it – you’re not just dealing with text-based product titles and UPCs. There are images, videos, regional variations, private labels, and a whole host of other data types and industry nuances to account for.

Luckily, DataWeave is one of the few companies that’s truly cracked the code. Our multimodal AI models are trained to process all those diverse data formats – from granular product specs to zany regional produce names. And it’s not just about technology; we also harness the power of human intelligence.

See, in the grocery world, category managers are the real decision makers. They know their shelves inside and out and can spot those tricky connections in product matching, especially when they are not UPC-based. That’s why DataWeave built in a Human-in-the-Loop (HITL) process, where their AI systems continuously learn from expert feedback. It’s a feedback loop that allows our customers to pitch in and keep product relationships accurate, reliable, and always adapting to new market realities.

So while product mapping may seem straightforward on the surface, the reality is it takes some serious horsepower to do it right. Thankfully, DataWeave has both the technical chops and the grocery industry know-how to make it happen. Because when it comes to pricing intelligence, getting those product connections right is half the battle.

3. Strategic Implementation: Turning Insights into Action

The true value of pricing intelligence (PI) is realized through its strategic application. Although many view PI as a technical function, its strategic significance is increasing, particularly in the context of recent economic pressures like inflation. Here’s why:

Tactical vs Strategic Use of Data: From Standard Reporting to Competitive Analysis

Pricing intelligence has come a long way from the days of simply reacting to daily price changes. These days, it’s not just about firefighting—it’s about driving long-term strategy.

You can use pricing data to make quick, tactical adjustments, like matching a competitor’s sudden price drop on milk. Or, you can leverage that same data to predict market trends, optimize your product lineup, and shape your overall pricing strategy. Retailers who take that strategic view can get out ahead of the curve, anticipating shifts instead of just chasing them.

DataWeave supports both of these approaches. Our Standard Reporting tools give pricing managers the nitty-gritty details they need—current practices, historical patterns, and operational KPIs. It’s all the insights you’d expect for making those tactical, day-to-day tweaks.

In addition, DataWeave offers something more powerful: Competitive analysis. This is where pricing intelligence becomes a true strategic weapon. By providing a high-level view of market positioning, competitor moves, and untapped opportunities, competitive analysis empowers leadership to make proactive, big-picture decisions.

Armed with this broader perspective, retailers can start taking a more surgical approach. Maybe you need to adjust pricing zones to better meet customer demands. Or rethink your overall strategies to stay ahead of the competition, not just keep pace. It’s the difference between constantly putting out fires and systematically fortifying your entire pricing fortress.

Beyond Pricing: Comprehensive Data for Broader Insights

Pricing intelligence is just the tip of the iceberg. When you really start to refine and harness your data, the possibilities for grocery retailers expand far beyond simple price comparisons. Think about it – all that information you’re collecting on products, markets, and consumer behavior? That’s a goldmine waiting to be tapped. Sure, you can use it to keep a pulse on competitor pricing. But why stop there?

What if you could leverage that data to optimize your product assortment, making sure you’re stocking the right mix to meet customer demands? Or tap into predictive analytics to get a glimpse of future market shifts, so you can get out ahead of the curve? How about using it to streamline your supply chain, identify availability inefficiencies, and get products to shelves faster?

Sure, pricing intelligence will always be mission-critical. But when you couple it with these other data-driven insights, that’s when grocery retailing gets really interesting. It’s about evolving from a price-matching robot to a true strategic visionary, armed with the intelligence to take your business to new heights.

Looking Ahead: The Future of Grocery Pricing Intelligence

The grocery pricing landscape continues to evolve, driven by:

- Integration of AI and machine learning for predictive pricing

- Enhanced focus on omnichannel pricing consistency

- Growing importance of personalization in pricing strategies

Pricing intelligence isn’t just about having data—it’s about having the right data and knowing how to use it strategically. Success requires a comprehensive approach that combines robust data collection, sophisticated analysis, and strategic implementation.

By embracing modern pricing intelligence tools and strategies, grocery retailers can navigate market volatility, maintain competitive positioning, and drive sustainable growth. The key lies in building a pricing ecosystem that’s both sophisticated enough to handle complex data and flexible enough to adapt to changing market conditions.

Ready to transform your pricing strategy? Check out our grocery price tracker to get month-on-month updates on grocery prices in the real world. Contact us to learn how our advanced pricing intelligence solutions can help your business stay ahead in the competitive grocery market.