Traditionally, retailers have staged multiple promotions between Black Friday and before Christmas Day to keep consumers excited about holiday shopping, so it’s easy to see why one more promotional day might fall into relative obscurity. As if ‘Early Start’ offers to Black Friday and extended ‘Cyber Weekend’ promotions weren’t enough to plan for, eBay added another day into the mix called ‘Green Monday’, much to the benefit of consumers, as it furthers the window of opportunity to secure a bargain during the holiday season.

Green Monday falls on the second Monday of December and has historically been one of the greatest sales days of the year for eBay, often attracting last-minute shoppers or those searching for last-minute deals. However, because of the 2021 Global Shipping Crisis, there is speculation that Green Monday may be the last chance this year to have items delivered in time for Christmas. For this reason, we believe it could turn into quite a fruitful event for participating retailers if it encourages procrastinating shoppers that traditionally spend closer to December 25th to buy earlier in the season.

This isn’t the first year retailers outside of eBay have offered Green Monday promotions, however. Our team has been actively monitoring activity on this day from 2017 through present, to not only assess which retailers participate in the event, but also to understand how the discounts may change surrounding the event. The categories monitored include Apparel (Clothing, Shoes & Jewelry), Bed and Bath, and Home and Garden, and we’ve identified products offered on discount by comparing each applicable product’s price on Green Monday versus the most commonly seen price for the product offered throughout the month of December.

Better Promotions Than Boxing Day

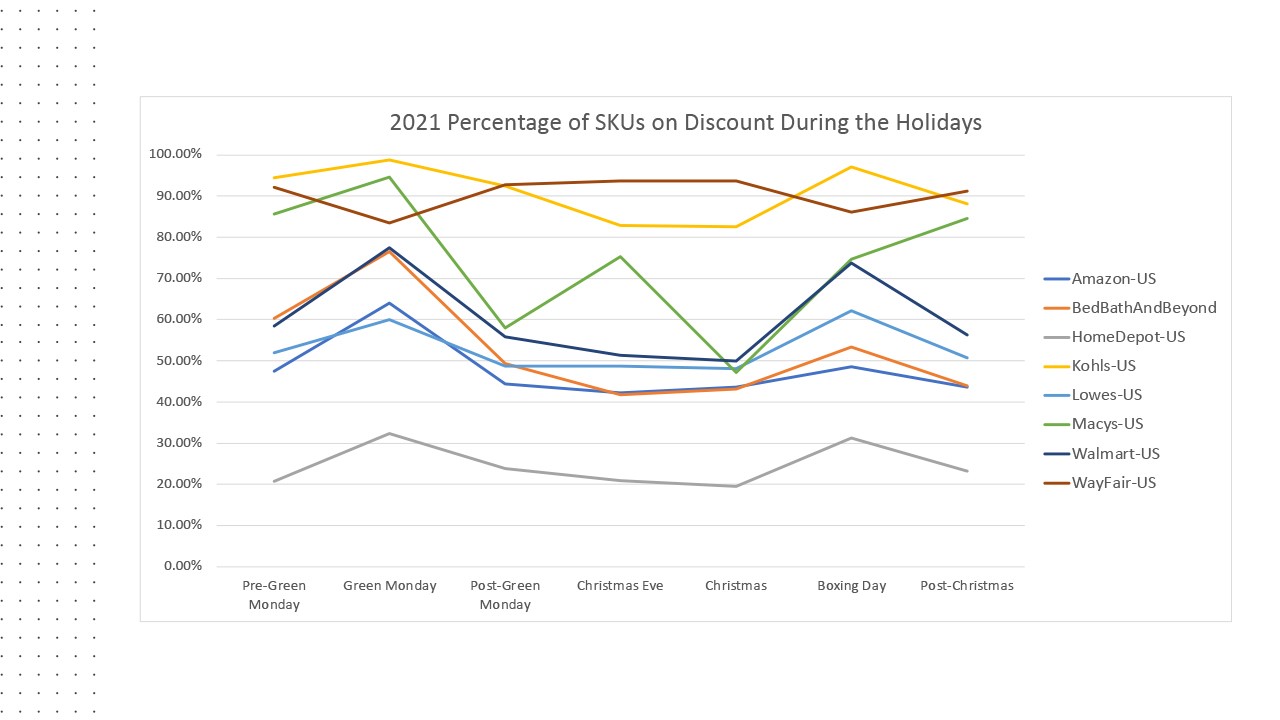

Taking a closer look at 2020 Green Monday discounts within the categories and retailers analyzed, apart from Wayfair.com, we see all offered more SKUs on discount on Green Monday versus the days leading up to and out of the event. Kohls.com led the pack with around 93% of SKUs offered on discount, followed by Macys.com with 95%, and Wayfair.com with 83%. Overall, the number of SKUs on discount on Green Monday were greater than the SKUs offered on discount on Boxing Day, which is traditionally known as a great day to bargain shop.

Source: DataWeave Commerce Intelligence – Promotional Insights tracking Apparel, Bed & Bath, and Home & Garden category product’s online price on Green Monday 2020 in the US versus regular prices for the same products in the month of December each year.

What’s in Store for Green Monday 2021?

The insights we’ve tracked over the last four years have not indicated any signs to an end for Green Monday any time soon. As we see it, for consumers it is an extremely convenient time to order holiday gifts, and for retailers it is a good time to build brand trust and loyalty by fulfilling last minute orders at a great value, in time for the holidays.

Our prediction for the categories analyzed is to expect to see more retailers participate in Green Monday 2021 to a greater degree (more SKUs on sale and enhanced promotions). For retailers in this analysis, we would anticipate HomeDepot.com to enhance the number of offers to match 2020 competitive activity, and for Wayfair.com to look at increasing the number of offers on Green Monday versus the period leading into the event.

If you are interested in learning more about the details behind this analysis or our Promotional Insights solution, be sure to contact us. We can help you evaluate the effectiveness of your holiday promotional spend with access to near real-time marketplace insights on the brands, categories, and products your rivals promote, including discounts, campaign frequency and duration and more.

The explosive growth of online shopping has forced brands to re-examine their e-commerce processes to stay competitive and profitable. In particular, out-of-stocks are a common, costly retail challenge, as product shortages frustrate online shoppers – and even prompt them to leave brands.

According to McKinsey & Company, forty-eight percent of consumers switched to a different brand in 2020 because those products were in stock. Among these consumers, seventy-three percent plan to keep using the new brands, linking product availability gaps to the erosion of sales and loyalty. Conversely, brands with effective inventory planning and replenishment can keep items in stock, drive sales and improve the customer experience.

Retailers like Walmart, collaborating with these brands to meet customer demand, are still facing inventory challenges but, as noted in 2021 Q3 earnings, inventory was up almost twelve percent year-over-year as they worked to stay ahead of increased holiday demand. They have also adjusted in-store operations to accommodate ever-growing e-commerce demands, especially within grocery-centric categories, as digital grocery buyers now amount to more than half the U.S. population.

Maximizing Conversions with Category Insights

Walmart’s dot-com strategy is paying off in spades, considering they surpassed Amazon as the leading U.S. grocery e-commerce retailer in 2020 and grew another forty-one percent in Q3, 2021. Our team has been actively tracking digital shelf analytic KPIs on Walmart.com to identify inventory and promotional performance improvement opportunities at a category level to support brands in capitalizing on these digital growth opportunities.

The latest analysis is summarized below, reviewing average category availability and discount trends occurring each week of the month, from May to August 2021, at a category level. A recent report found the 29th of each month to be the busiest day for online sales because consumers often get paid at the end of the month, which made DataWeave analysts wonder:

Which categories are maximizing their growth potential on Walmart.com and where are the greatest opportunities for improvement during periods of increased demand?

How do increased demand periods (like payday) impact category online availability?

Are category promotions offered at the right times throughout the month to best support demand?

When Seasonal Demand for Groceries and Payday Merge

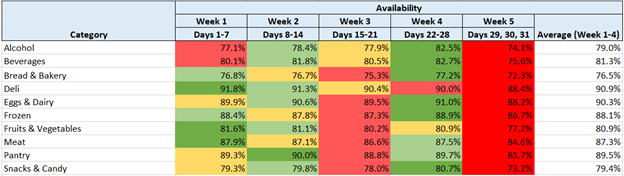

Across all Walmart.com food categories tracked, Week 5 – where payday commonly falls for most consumers, had the lowest average product availability, while Week 4 had the highest average product availability for all categories except Deli and Fruits and Vegetables. These findings may inspire Walmart’s brand partners to rethink their inventory and assortment planning, replenishment and even pricing efforts to maintain a healthy stock closer toward the end of the month to match higher demand.

The categories with the greatest difference in average availability during Week 5 versus the rest of the month were Snacks & Candy, Beverages and Alcohol, indicating consumers consistently made these types of purchases closest to payday, when income was highest throughout the month. Seasonality is a secondary factor that influenced demand for these items given events like Memorial Day, Fourth of July, Summer Break, and Back-to-School shopping all took place during our analysis. Additionally, most holidays overlapped payday, which also furthered Week 5 demand.

Source: DataWeave Digital Shelf Analytics for Brands – Category average availability percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

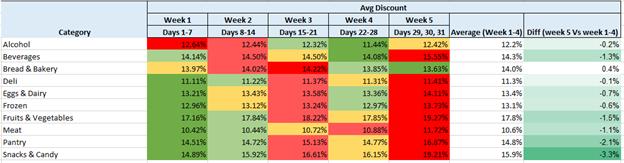

Coupling availability with discounts allows us to consider whether consumers buy more in Week 5 due to high discounts or increased purchasing power, or both. In reviewing the average category discounts offered within the same grocery-centric categories analyzed above, we found almost every grocery category showed a higher discount in Week 5 compared to the rest of the month, except for Bread & Bakery and Alcohol.

Source: DataWeave Digital Shelf Analytics for Brands – Category average discount percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

Regarding Alcohol, during Week 4, when average availability was the highest, the average discounts offered were the lowest. This can indicate inventory was primed for payday shoppers (and the holidays of course). Bread & Bakery offers the greatest average discounts when inventory levels are lowest on average, indicating Week 3 is a great time to stock up, while Week 4 might be a great time to buy the freshest inventory.

The greatest average discounts in Week 5 were in Snacks & Candy, Pantry and Fruits & Vegetables. Deeper discounts for Snacks & Candy in Week 5 may have helped brands compete for consumers’ disposable income despite being a discretionary category. Pantry brands’ discounts may have reflected a need to compete for shoppers’ attention. During this period, consumers were out of the house more and less likely to use these grocery staples compared to earlier lockdown periods and cooler months.

Making Specialty Categories and Health a Priority for Online Shoppers

Interestingly, the only two categories where inventory was higher in Week 5 versus all other weeks each month were ‘Special Diets’ foods and ‘Summer Flavors’, although ‘Special Diets’ foods consistently maintained the lowest level of average availability each week across all food categories analyzed. This consistent lack of inventory could indicate a great opportunity for brands to increase inventory for dietary products sold on Walmart.com.

Source: DataWeave Digital Shelf Analytics for Brands – Category average availability percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

The average availability for ‘Summer Flavors’ foods verifies brands are maintaining a solid replenishment strategy for these seasonal items, and a high likelihood consumers will happily find what they need to plan their Summer gatherings on Walmart.com. One alarming factor we found was the change in average discounts offered during Week 5 versus Weeks 1 through 4, indicating promotions surrounding payday may be driving sales volume versus organic demand.

Source: DataWeave Digital Shelf Analytics for Brands – Category average discount percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

Digital Growth Opportunity in Meal Kits and Kids’ Meals

Two categories primed for growth, according to Statista, are meal kits and kids’ food and beverages. Their research indicates retail sales for kids’ food has grown steadily year-over-year since 2013, and a recent report also indicates meal kit sales are expected to more than double 2017 sales in 2022, reaching $11.6 billion in the U.S., spurred by pandemic-induced demand. A concerning find in our research indicates both categories, ‘Easy Meal Solutions’ and ‘Kid Friendly Foods’ on Walmart.com, showed great volatility when it comes to in-stock availability. For example, in Week 1, ‘Easy Meal Solutions’ had an average availability nearly half the average of the rest of the month (around nineteen percent versus nearly thirty-eight percent), and in Week 5, payday week, ‘Kid Friendly Foods’ saw the biggest drop in average availability compared to Weeks 1 through 4 (over sixty-seven percent versus seventy-five percent) indicating supply may not be keeping up with the heightened demand.

Source: DataWeave Digital Shelf Analytics for Brands – Category average availability percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

The heightened average discounts offered during Week 5 for ‘Baby’ and ‘Pets’ items indicate two categories consumers will most likely stock up on during payday.

Source: DataWeave Digital Shelf Analytics for Brands – Category average discount percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

Back to School Stock-Outs

U.S. retail sales unexpectedly increased in August, likely boosted by back-to-school shopping and child tax credit payments. Meanwhile, product shortages and other supply chain issues slowed 2021’s back-to-school sales, possibly affecting school supplies’ and clothing availability on Walmart.com. According to our analysis, the average product availability in Walmart.com’s school supplies category fell from over sixty-two percent during Weeks 1 through 4 to nearly forty-two percent in Week 5.

Warmer weather, seasonal events, reduced lockdowns, and vaccination efforts led more Americans to resume in-person socializing, giving reason to update their spring and summer wardrobes. In July, Forbes shared that three-quarters of shoppers are purchasing apparel, accessories and shoes the most. On average, only around sixty-three percent of clothing items were available on Walmart.com during Weeks 1 through 4. However, in Week 5, that figure plummeted to just over thirty-eight percent, the most significant drop among all categories.

Source: DataWeave Digital Shelf Analytics for Brands – Category average availability percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

Demand for new fashion remained high throughout this period, seemingly fueled organically, as only moderate additional discounts took place in Week 5, and although the average discount on school supplies was only around twenty-seven percent during Weeks 1 through 4, it surged to just over forty-seven percent in Week 5. Generous additional discounts in Week 5 may have inspired online shoppers to shift spending from clothing to school supplies in late July and August ahead of students’ return to the classroom.

Source: DataWeave Digital Shelf Analytics for Brands – Category average discount percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

Prioritizing Product Availability with Digital Advertising Strategies

Seventy-eight percent of B2C marketers increased their 2021 digital advertising spend to fuel online product discoverability (Share of Search), and sales and market share, but out-of-stock experiences simultaneously surged 172% this year from pre-pandemic levels. Paying for ads that drive traffic to your out-of-stock products can be as detrimental to your brand as a bad user experience. Our review of the ‘Featured Products’ sold on Walmart.com show consistent, low-levels of product availability each week throughout the months reviewed.

Source: DataWeave Digital Shelf Analytics for Brands – Category average availability percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

Additionally, the average discount offered on these products tended to be higher than most other categories reviewed, indicating brands participating in the featured product section of the website were not only investing in digital ads, but also doubling down with promotional activity as well.

Source: DataWeave Digital Shelf Analytics for Brands – Category average discount percentages from May to August 2021 between Week 1 (the 1st to the 7th day of the month) and Week 5 (the 29th, 30th and 31st day of the month).

How Brands can Replenish Their Digital Shelf

It is well known just how important it is to have products available during the right time of day, week, month, or season to improve customer satisfaction rates, but with your e-commerce store open 24/7 and omnichannel fulfillment strategies in place, it drastically changes the way in which strategic execution is prioritized for a retailer to reduce basket abandonment and for brands to build loyalty.

Our greatest takeaway from this analysis is realizing how crucial it is for brands to proactively track product availability and competitive pricing insights to stay ahead of the curve and achieve their digital growth goals. Early visibility to stock replenishment could help brands align with heightened cyclical and seasonal demand to avoid out-of-stocks and grow e-commerce sales.

This is why more leading brands now rely on our Digital Shelf Analytics solutions, including Pricing and Availability insights, to keep eCommerce planning agile, to maximize online conversions, and ultimately maintain shopper satisfaction and loyalty.

As eCommerce grows in complexity, brands need new ways to grow sales and market share. Right now, brands face urgent market pressures like out-of-stocks, an influx of new competition and rising inflation, all of which erode profitability. As online marketplaces mature, more brands need to make daily changes to their digital marketing strategies in response to these market pressures, shifts in demand, and competitive trends.

eMarketer forecasts 2021 U.S. eCommerce will rise nearly 18% year-over-year (vs. 6.3% for brick-and-mortar), led by apparel and accessories, furniture, food and beverage, and health and personal care. The eCommerce industry is also undergoing fundamental changes with newer entities emerging and traditional business models evolving to adapt to the changed environment. For example, sales for delivery intermediaries such as Doordash, Instacart, Shipt, and Uber have gone from $8.8 billion in 2019 to an estimated $35.3 billion by the end of 2021. Similarly, many brands have established or are building out a Direct to Consumer (D2C) model so they can fully own and control their customer’s experiences.

In response, DataWeave has launched the next generation of our Digital Shelf Analytics suite to help brands across retail categories directly address today’s costly market risks to drive eCommerce growth and gain a competitive advantage.

“Our new enhancements help brands improve online search rank visibility and quantify the impact of digital investments – especially in time for the busy holiday season.” ~ Karthik Bettadapura, CEO and co-founder, DataWeave

The latest product enhancements provide brands access to tailored dashboard views that track KPI achievements and trigger actionable alerts to improve online search rank visibility, protect product availability and optimize share of search 24/7. Dataweave’s Digital Shelf Analytics platform works seamlessly across all forms of eCommerce platforms and models – marketplaces, D2C websites and delivery intermediaries.

Dashboard for Multiple Functions

While all brands share a common objective of increasing sales and market share, their internal teams are often challenged to communicate and collaborate, given differing needs for competitive and performance data across varying job functions. As a result, teams face pressure to quickly grasp market trends and identify what’s holding their brands back.

In response, DataWeave now offers executive-level and customized scorecard views, tailored to each user’s job function, with the ability to measure and assess marketplace changes across a growing list of online retail channels for metrics that matter most to each user. This enhancement enables data democratization and internal alignment to support goal achievement, such as boosting share of category and content effectiveness. The KPIs show aggregated trends, plus granular reasons that help to explain why and where brands can improve.

Brands gain versatile insights serving users from executives to analysts and brand and customer managers.

Prioritized, Actionable Insights

As brands digitize more of their eCommerce and digital marketing processes, they accumulate an abundance of data to analyze to uncover actionable insights. This deluge of data makes it a challenge for brands to know exactly where to begin, create a strategy and determine the right KPIs to set to measure goal accomplishment.

DataWeave’s Digital Shelf Analytics tool enables brands to effectively build a competitive online growth strategy. To boost online discoverability (Share of Search), brands can define their own product taxonomies across billions of data points aggregated across thousands of retailer websites. They can also create customized KPIs that track progress toward goal accomplishment, with the added capability of seeing recommended courses of action to take via email alerts when brands need to adjust their eCommerce plans for agility.

“Brands need an integrated view of how to improve their discoverability and share of search by considering all touchpoints in the digital commerce ecosystem.” ~ Karthik Bettadapura, CEO and co-founder, DataWeave

Of vital importance, amid today’s global supply chain challenges, brands gain detailed analysis on product inventory and availability, as well as specific insights and alerts that prompt them to solve out-of-stocks faster, which Deloitte reports is a growing concern of consumers (75% are worried about out-of-stocks) this holiday season.

User and system generated alerts provide clarity to actionable steps to improving eCommerce effectiveness.You also have visibility to store-level product availability, and are alerted to recurring out-of-stock experiences.

Scalable Insights – From Bird’s Eye to Granular Views

DataWeave’s Digital Shelf Analytics allows brands to achieve data accuracy at scale, including reliable insights from a top-down and bottom-up perspective. For example, you can see a granular view of one SKUs product content alongside availability, or you can monitor a group of SKUs, say your best selling ones, at a higher level view with the ability to drill down into more detail.

Brands can access flexible insights, ranging from strategic overviews to finer details explaining performance results.

Many brands struggle with an inability to scale from a hyper-local eCommerce strategy to a global strategy. Most tools available on the market solve for one or the other, addressing opportunities at either a store-level basis or top-down basis – but not both.

According to research by Boston Consulting Group and Google, advanced analytics and AI can drive more than 10% of sales growth for consumer packaged goods (CPG) companies, of which 5% comes directly from marketing. With DataWeave’s advanced analytics, AI and scalable insights, brands can set and follow global strategies while executing changes at a hyper-local level, using root-cause analysis to drill deeper into problems to find out why they are occurring.

As more brands embrace eCommerce and many retailers localize their online assortment strategies, the need for analytical flexibility and granular visibility to insights becomes increasingly important. Google reports that search terms “near me” and “where to buy” have increased by more than 200% among mobile users in the last few years, as consumers seek to buy online locally.

e-Retailers are now fine-tuning merchandising and promotional strategies at a hyper-local level based on differences seen in consumer’s localized search preferences, and DataWeave’s Digital Shelf Analytics solution provides brands visibility to retailer execution changes in near real-time.

Competitive Benchmarking

Brand leaders cannot make sound decisions without considering external factors in the competitive landscape, including rival brands’ pricing, promotion, content, availability, ratings and reviews, and retailer assortment. Dataweave’s Digital Shelf Analytics solution allows you to monitor share of search, search rankings and compare content (assessing attributes like number of images, presence of video, image resolution, etc.) across all competitors, which helps brands make more informed marketing decisions.

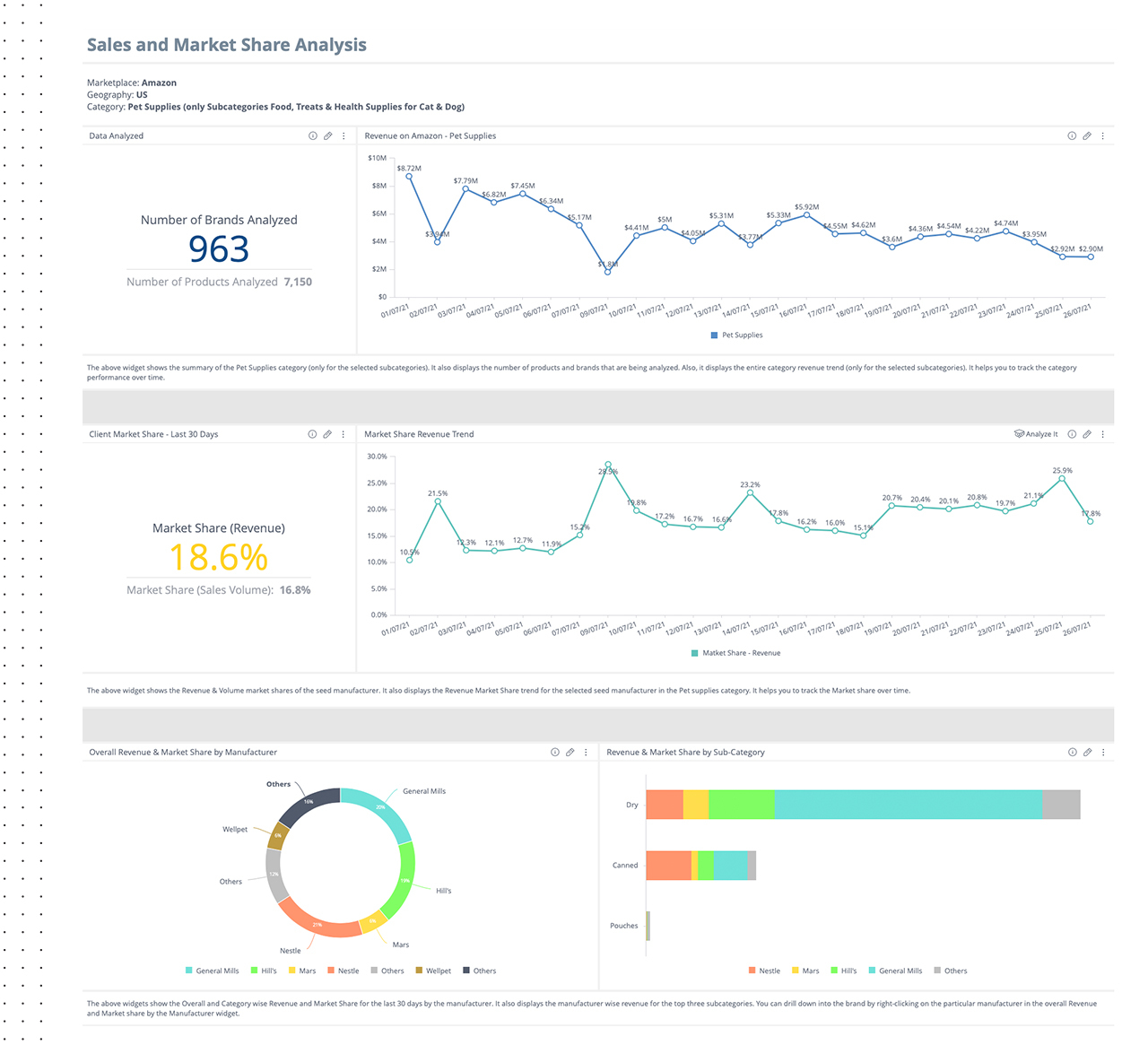

Brands are also provided visibility into competitive insights at a granular level, allowing them to make actionable changes to their strategies to stay ahead of competitors’ moves. A new module called ‘Sales and Share’ now enables brands to benchmark sales performance alongside rivals’ and measure market share changes over time to evaluate and improve competitive positioning.

Monitor competitive activity, spot emerging threats and immediately see how your performance compares to all rivals’, targeting ways to outmaneuver the competition.

Sales & Market Share Estimates Correlated with Digital Shelf KPIs

In a brick-and-mortar world, brands often use point of sale (POS) based measurement solutions from third party providers, such as Nielsen, to estimate market share. In the digital world, it is extremely difficult to get such estimates given the number of ways online orders are fulfilled by retailers and obtained by consumers. Dataweave’s Digital Shelf Analytics solution now provides sales and market share estimates via customer defined taxonomy, for large retailers like Amazon. Competitive sales and market share estimates can also be obtained at a SKU level so brands can easily benchmark their performance results.

Additionally, sales and market share data can also be correlated with digital shelf KPIs. This gives an easy way for brands to check the effect of changes made to attributes, such as content and/or product availability, and how the changes impact sales and market share. Similarly, brands can see how modified search efforts, both organic and sponsored, correspond to changes in sales and market share estimates.

Take Your Digital Shelf Growth to the Next Level

The importance of accessing flexible, actionable insights and responding in real-time is growing exponentially as online is poised to account for an increasing proportion of brands’ total sales. With 24/7 digital shelf accessibility among consumers comes 24/7 visibility and the responsibility for brands to address sales and digital marketing opportunities in real-time to attract and serve online shoppers around the clock.

Brands are turning to data analytics to address these new business opportunities, enhance customer satisfaction and loyalty, drive growth and gain a competitive advantage. Companies that adopt data-driven marketing strategies are six times more likely to be profitable year-over-year, and DataWeave is here to help your organization adopt these practices. To capitalize on the global online shopping boom, brands must invest in a digital shelf analytics solution now to effectively build their growth strategies and track measurable KPIs.

DataWeave’s next-gen Digital Shelf Analytics enhancements now further a brand’s ability to monitor, analyze, and determine systems that enable faster and smarter decision-making and sales performance optimization. The results delight consumers by helping them find products they’re searching for, which boosts brand trust.

Connect with us to learn how we can scale with your brand’s analytical needs. No project or region is too big or small, and we can start where you want and scale up to help you stay agile and competitive.

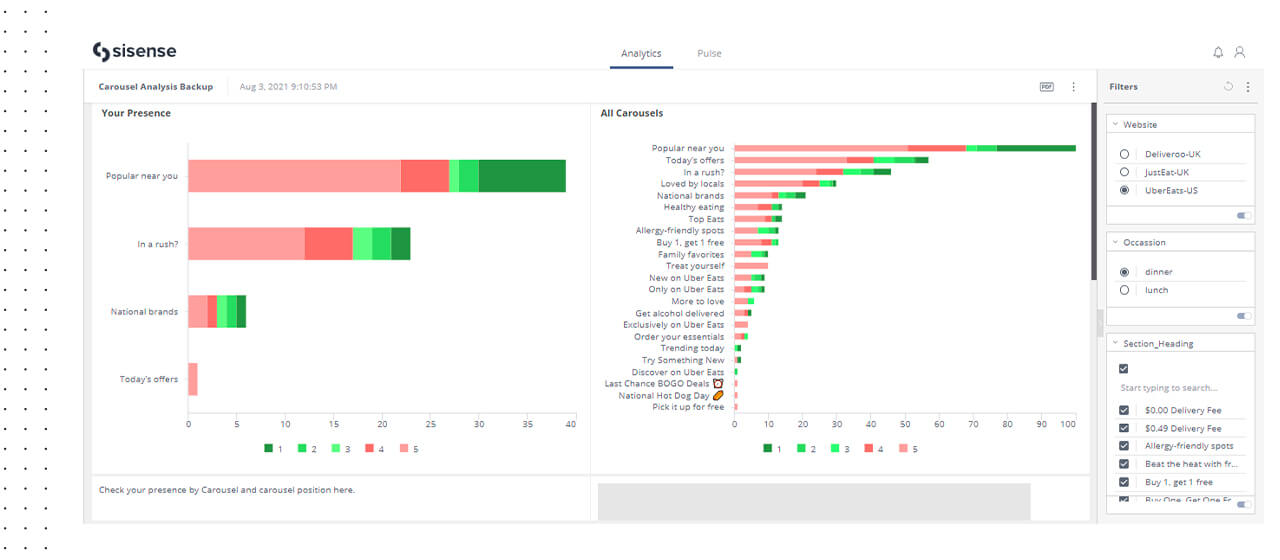

Traditionally, Quick Service Restaurants (QSRs) such as McDonald’s or Burger King, have been strategically operating on a brick and mortar model. However, according to some studies, an average QSR generates as much as 75% of its sales from online orders.

With the advent of delivery apps such as Uber Eats and Doordash, a significant portion of QSRs’ business has moved to these platforms. The war to top rank on one of these platforms is an even greater feat. With each brand competing for the top listing, it’s much less about the dollars you pay and much more about optimizing your investments.

The relationship between QSR chains and food delivery apps has its advantages and disadvantages. One of the critical grouses QSRs have against food apps is the incremental marketing spend required to participate on the platform and the inability to measure the impact of their investment. What makes matters worse is the limitation in metrics even available to measure the impact – neither the food apps provide them, nor does anyone else.

At DataWeave, we have made it our mission to enable QSRs to not only define measurable metrics to achieve a positive ROI for food app marketing investments, but we also equip QSRs with the tools to track their competitive performance at granular, zip code-based level so that localized strategies can be modified as needed. Below is an example of a 1000+ store chain QSR we partnered with to optimize a pre-existing investment made with a large food aggregator app. Within months of engagement with us, they were able to achieve a 3X increase in sales without adding any additional marketing dollars.

Below are the pain points we identified and solved together:

1. No Defined Metric

Problem – No leading metric to track marketing performance

One of the first issues we realized was that sales was not a good metric for tracking marketing performance as it’s a lagging metric and doesn’t capture the issues that help grow or suppress sales.

Most of the sales are driven by rank in the cuisine category and searches for branded keywords. But, the QSR chain had no way to track these ranks.

In fact, 70%+ sales go to the first five restaurants for the category and keyword

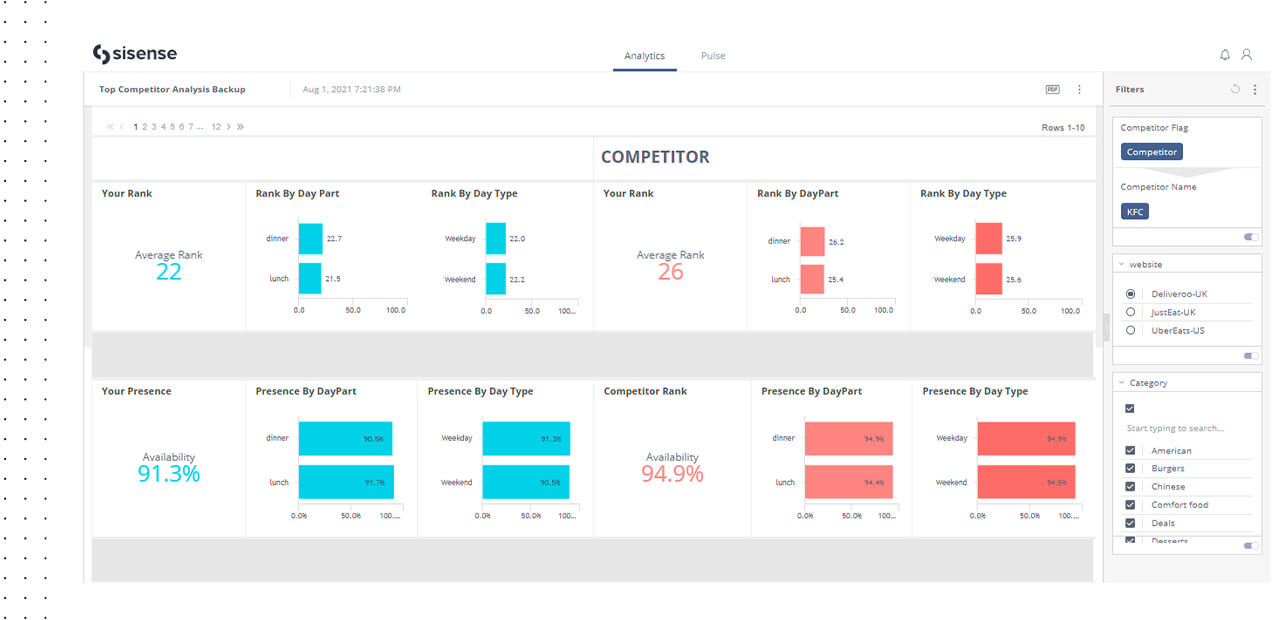

Comparing ranking on food delivery platforms across different categories and times

Solution – Establish ranking as a clear marketing metric

By aggregating data across different food app platforms comprehensively, i.e. across locations, at different times of the day, we established the ranking of the QSR chain in critical categories and for priority keywords, identifying where they under or over-performed relative to the competition. As we did this daily- this became a straightforward metric that helped establish the performance of their marketing campaign.

2. Geographical & Categorical Challenges

Problem: Identifying poor-performing stores and zip codes

We realized it was not a simple exercise to identify well performing stores on food apps since sales depend on many factors such as competition, population of the area, local cuisine preference, etc.

Solution: Zip Code Ranking and Attributes

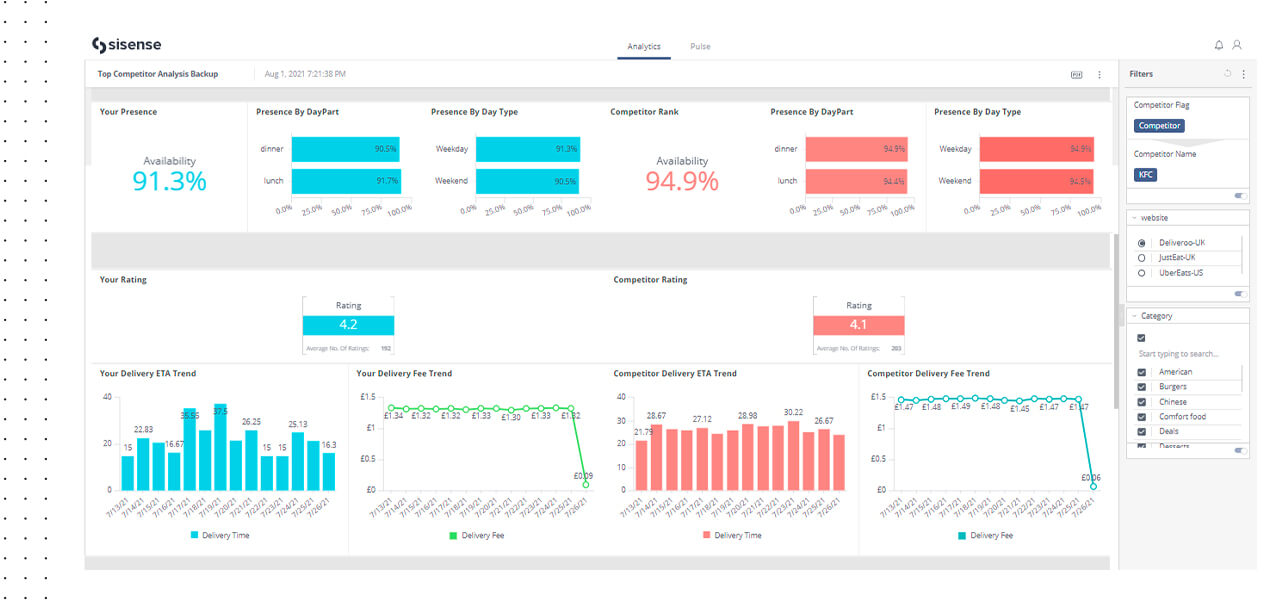

We tracked the ranking of each store within each Zip Code for keywords and created a list of poor-performing stores. We also extracted attributes such as estimated time of arrival (ETAs), Delivery Fee, Ratings, Reviews, etc., for each of these poor performing stores, to identify the reasons for the poor ranking.

Analysing key metrics at a store level – identifying worst & best performing stores

E.g., We realized 356 of the stores were not populating on first page results, primarily because of poor ratings and High ETAs. After the focused initiative, 278 of these stores started showing on the first page and increased sales by 23%.

3. Sensitivity Analysis Deficiency

Problem: Not clear about the contribution of Rating, ETAs, Fees, etc. on the Ranking

The exact ranking algorithms of these food apps are not publicly shared – so the QSR chain wasn’t clear which variable of rating, ETAs, fees, ad spend, or availability contributed more or less to the overall ranking.

Solution: Sensitivity analysis for measuring contribution

Comprehensive data for multiple zip codes in various timestamps was analyzed to determine which variable contributes most significantly to the rankings and when. We also conducted A/B testing – simultaneously testing two different variables, such as reducing ETAs at one store and improving ad spend at another, calculating which led to greater rank and sales impact.

For example, we realized reducing publicized ETA’s (even by decreasing the delivery radius) contributed much more to improve the rankings than changes to ratings.

4. An Unknown Competitive Landscape

Problem: Tracking competitor performance

For example, we found the QSR chain performed well in key urban centers, but the competition was doing even better, but there wasn’t a good way to track and compare the performance of the competitors.

Solution:

We started tracking the QSR chain and the competition for each of the metrics and started comparing performance.

Analysing competitive performance on key metrics such as ETA, Availability etc

We quickly realized ranking started quickly improving as we gained a slight edge in each metric against the competitors. For example, 5 minutes less ETA adds to higher ranking.

In six months of this exercise with the QSR chain, we improved the average ranking from 24 to 11 for the QSR chain, getting them featured on the first page.

5. Blind Advertising Investment Opportunities

Problem:

The QSR chain was not clear on which banners (Popular near you, National Favorites, etc.) to choose to invest in, and had to depend on the recommendations of the food platforms entirely.

They weren’t even provided a clear view of which position made the banner visible and at what rank among those banners was their promo visible. They were at times the 7th promo in the 6th banner, which has almost zero probability of being discovered by the user – this happened despite paying heavily for the banners.

Solution:

We aggregated data for all banners populated within each zip code and found out the ranking and in which position the QSR chain was visible.

Identifying and analysing right banners for advertising spends

The QSR chain invested in 630 zip code-based banners with guaranteed visibility, but our assessment indicated the banners were only visible in 301 zip codes. After selecting suitable banners for promotions, we improved visibility to 533 zip codes within enhancing the budget.

We are now using the same strategy for refining discounts, offers, promotions, and coupons.

6. Lack of Campaign Performance Monitoring

Problem: Unsure of the long-term impact of marketing spend

In general, increasing marketing spend does give a temporary boost to sales, but the QSR chain’s question was, how can we measure the long-term impact i.e., ranking keywords and the targeted zip codes.

Solution:

We created a simple widget for every marketing campaign which showed the rank for the keywords for selected zip codes before the campaign, during the campaign, and post the campaign, clearly establishing the midterm impact of the campaign. This constant monitoring allowed the QSR to also quickly pivot on their strategy on account of national holidays etc, and act accordingly.

7. Non-Existent ROI Measurement

Problem: Establishing the impact of ranking on sales

Though the QSR chain could track sales that were coming via the food app channel, they had no way of knowing incremental organic volume driven by marketing efforts.

One missing variable here was how much of extra sales could be attributed to improvement of QSR ranking?

Solution:

By combining the sales data with aggregated insights over time, we established for the QSR chain how much increase in sales they could anticipate from an increase in ranking, also knowing which changed variables led to the percentage of change increase.

So, in essence, we were able to tell the QSR chain that for each store how much sales would increase by improving ETAs, rating, ad visibility, availability, etc., enabling precise ROI calculations for each intervention they make for their stores.

Increasing sales by 3x within six months was only the beginning, and the journey of driving marketing efficiency using competitive and channel data has only just begun.

DataWeave for QSRs

DataWeave has been working with global QSR chains, helping them drive their growth on aggregator platforms by enabling them to monitor their key metrics, diagnose improvement areas, recommend action, and measure interventions’ impact. DataWeave’s strategy eliminates the dependence on food apps for accurate data. We aggregate food app data and websites to help you with analysis and the justification of marketing spend and drive 10-15% growth.

DataWeave’s strategy eliminates the dependence on food apps for accurate data. We aggregate food app data and websites to help you with analysis and the justification of marketing spend and drive 10-15% growth.

If you want to know learn how your brand can leverage Dataweave’s data insights and improve sales, then click here to sign up for a demo

Prime Day or not, brands need to make sure their Digital Shelf is well stocked, highly discoverable in crowded marketplaces, have the right offers and discounts to stay competitive, all while making sure their products have glowing reviews, ratings and optimized content. While this is a year-round effort, brands go the extra mile on Prime Day to make sure they’re putting their best foot forward.

Methodology To understand how brands adapted their digital shelf for Prime Day, we examined data insights across Amazon in 6 markets and compared the following brand KPIs:

Share of voice (SOV): The percentage of a brands products that appear in the search results page for relevant keywords on Amazon.

Availability: The percentage of products in stock on Amazon for Prime Day.

Additional discounts: The reduction in the listing price of a product during Prime Day compared to before or after the event to see how brands adapted their pricing strategies to stand out from rivals

Winning brands made sure their products were ‘highly’ discoverable

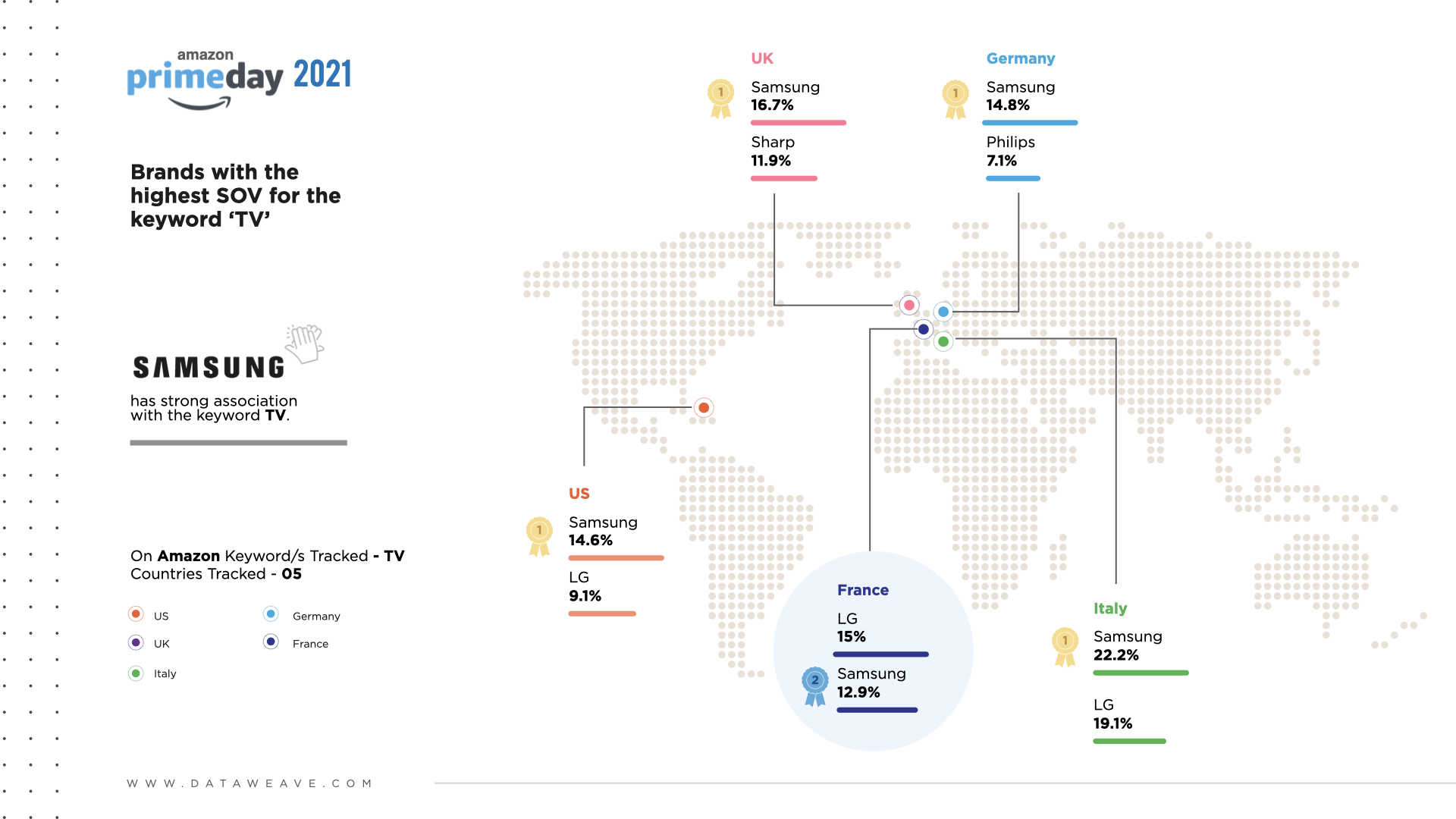

With all the global lockdowns, home entertainment hit a new high. So we looked at the word “TV” to see which brand had the highest share against this keyword during the Prime Day event.

In the US – Samsung won hands down with close to 15% SOV. LG came in at a not so close 2nd with 9% SOV.

In the UK – Samsung won again with a whooping 16.7% SOV with Sharp at # 2 at 12%.

Now let’s look at some key European markets

On Amazon Italy we saw a similar trend – Samsung & LG, neck to neck at 22% & 19% respectively.

Amazon Germany was no different – Samsung had the highest SOV at 15% and Philips far behind at 7%.

Samsung has such a strong association with the keyword TV. This means, when customers are searching for TVs on Amazon in these regions – the brand that has the largest selection up on display for them to choose from is Samsung! That’s definitely going to have a positive impact on sales, don’t you think?

Do you know which keywords you should be tracking for your brand? And do you know your Brand’s SOV against those keywords?

… & finally, an outlier!

In Amazon France, LG took the lead for a change – with 15% SOV. But we have Samsung not far behind at 13%.

Kudos to team Samsung!

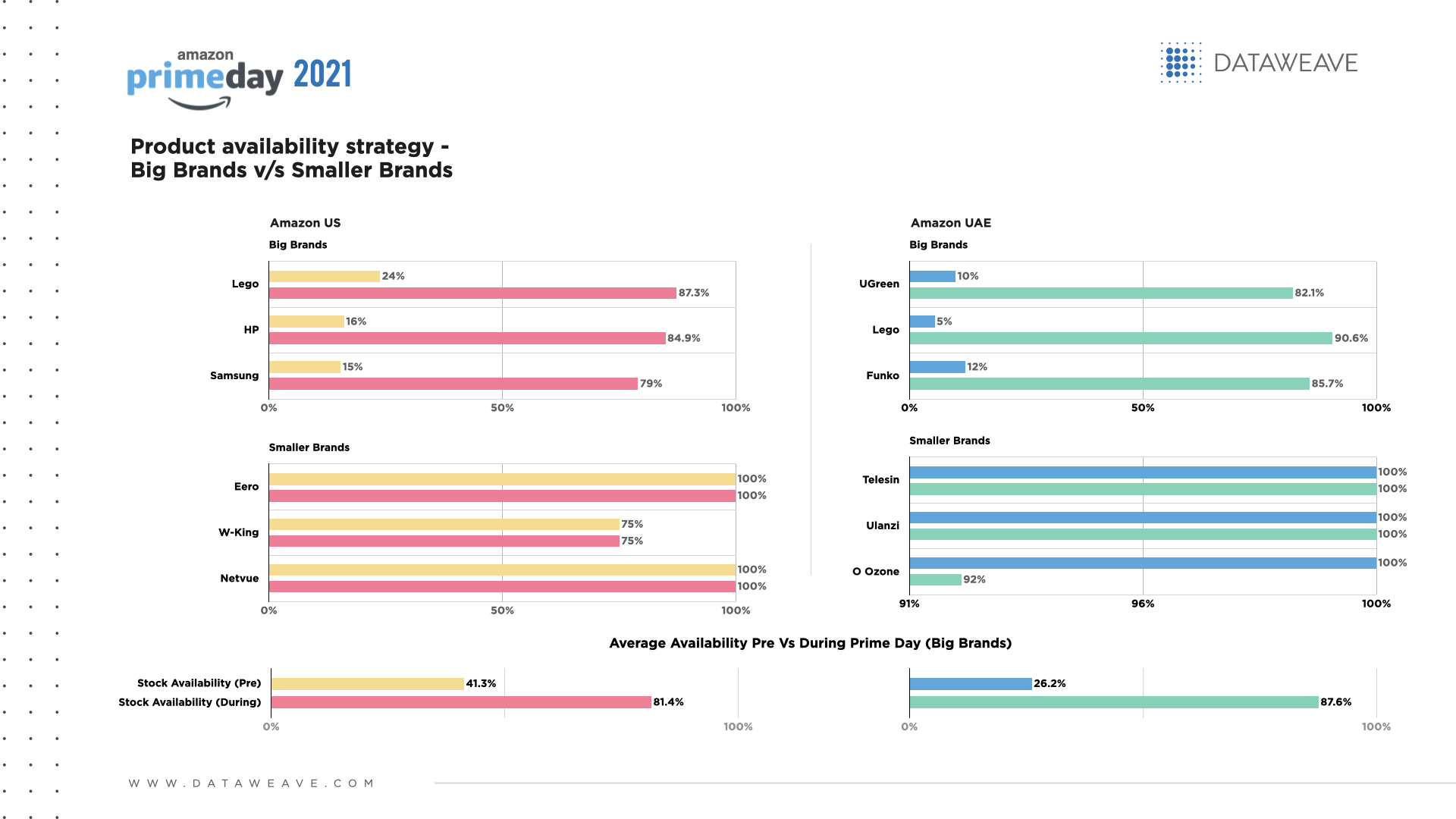

Winning Brands kept a close eye on product availability

Poor product availability leads to lost sales. But not on Amazon Prime Day! Bigger brands that sell over 500 products created artificial scarcity by listing a chunk of products out of stock before the sale. And restocked aggressively during the sale.

In contrast, the smaller brands that sold fewer than 100 products didn’t dare make such bold moves and stayed stocked up even pre-event to avoid even a single day of lost sales.

Let’s look at some data from the US

The average availability for bigger brands selling 500+ products before the sale was 41% and then went up dramatically to 81.4% the day of the sale when they aggressively restocked.

Similar trend in the UAE

Availability pre-sale was 26.2% and during the sale shot up to 87.6%!

Various other markets displayed similar patterns. And this was only possible because these brands were able to track their availability with precision and plan their stock levels accordingly.

How are you tracking your availability across marketplaces? Do you know when your products are out of stock and are in immediate need of replenishment?

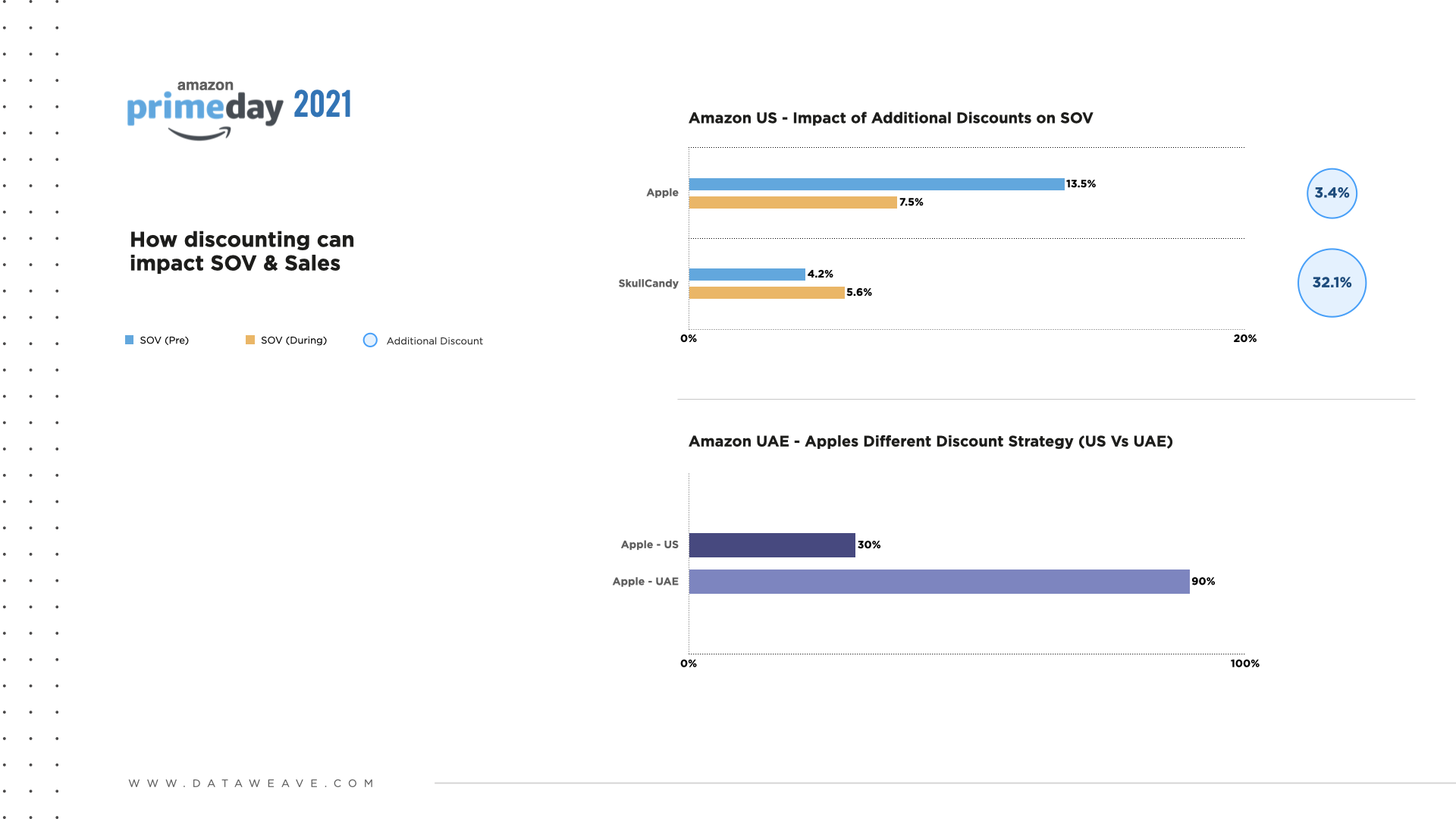

Winning Brands made strategic pricing and discounting decisions

Discounts matter. Period. And brands that use discounts strategically, win.

Let’s look at Airpods on Amazon in the US.

During the event, Apple had the highest SOV for the keyword Airpod at 7.5% followed by SkullCandy, an American audio accessory manufacturer at 5.6%.

Here’s the interesting part – during the sale Apple offered just 3.4% additional discounts while SkullCandy offered 32.1% additional discount to try and win sales from Apple. And looks like it worked! Apples SOV dropped from 13.5% before the event to 7.5% during the event and SkullCandy’s SOV improved

Now let’s look at the same data cut in the UAE – a market where Apple products have a fair penetration, but not as high as in the US. They needed a more aggressive discounting strategy in this market.

In the US, during the sale, Apple offered additional discounts on just 30% of products. However, in the UAE that number rose to 90% – a clear strategy to make their product pricing more attractive to customers to win sales

Discounts and markdowns aren’t always the answer to improving sales, but when used strategically can drive significant impact to your bottom line.

Are you tracking your competitor pricing? Do you know if they’re keeping tabs on your pricing strategy to get ahead of you?

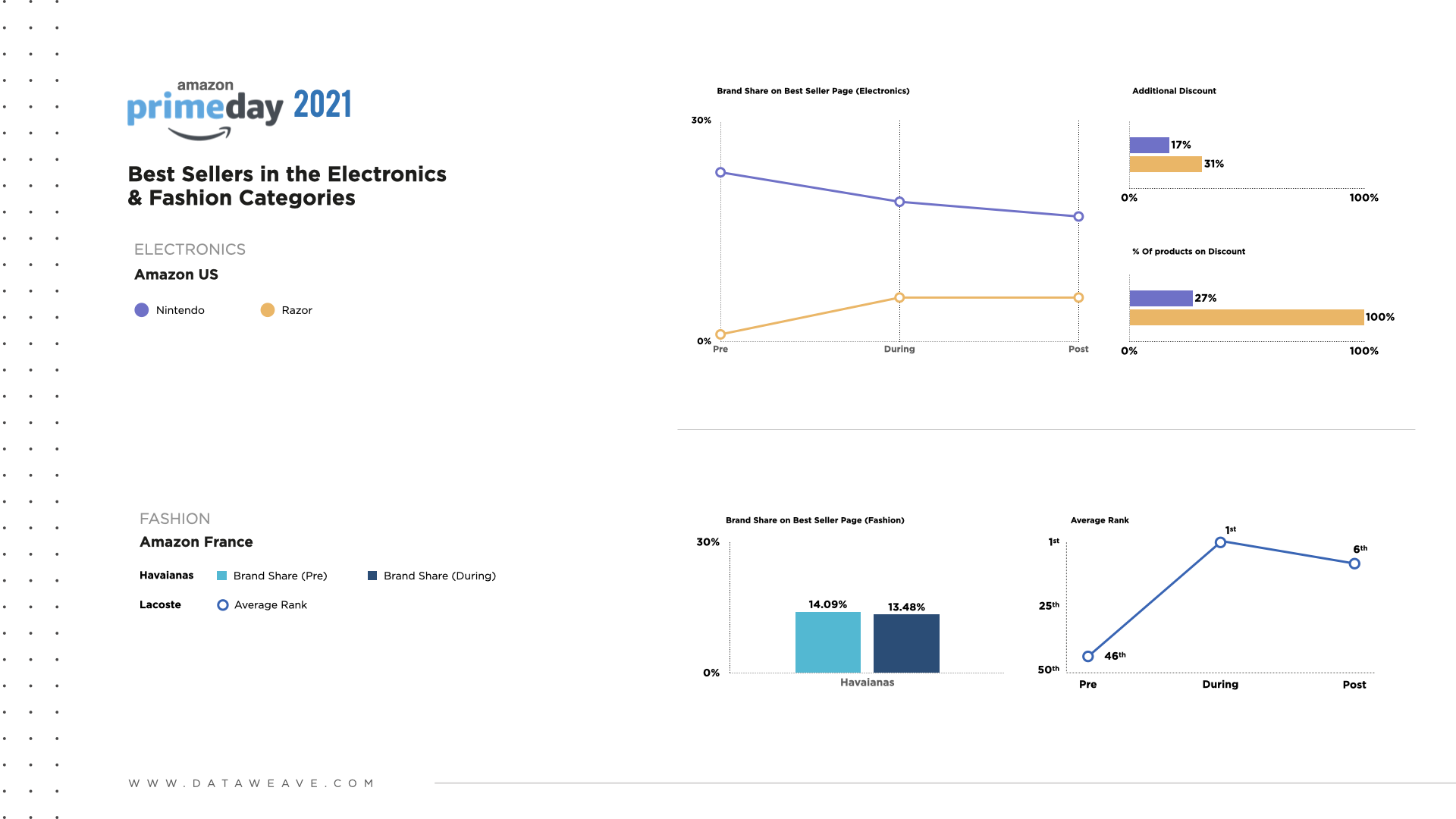

Winning Brands made it to the Amazon Best Seller list

Amazon Best Sellers are products that have the highest sales on Amazon. Products with a higher Amazon Best Seller Rank have higher sales.

In the US, Nintendo had the highest share in the Electronics Best Seller category during the sale at 18.6%. Before the sale their share stood at 22.5% – so they lost ground a little ground with a 27.2% drop in their Best Seller share. While they gave additional discounts of 17%, only 27% of their catalogue was discounted.

But here’s a brand that knocked it out of the park! The Razer had an SOV of just 1.18% before the sale and during Prime Day it shot up to 6%! A clear indication that sales for the Razer spiked exponentially during Prime Day. Could this be because Razer offered 100% of their catalogue on an additional discount of 31%? It’s a bold move that could have paid off and contributed to super high sales.

Now let’s look at France – the Fashion Capital of the World and which brand came out on top in the Fashion Best Seller Category

Footwear brand Havaianas had the highest SOV on Prime Day (13.48%) Not too surprising because before the sale they were at 14.09%

Now let’s look at the Best Seller Rank – Lacoste secured BSR #1 at the event. Pat on the back for them because before the sale they were at Rank 46! And post-sale they dropped to #6. Definitely a combination of techniques involved here that got them from #46 to #1 at super speed!

What techniques have you tried to boost sales for your products on Amazon?

Brands that do not optimize their Digital Shelf risk losing out on their share of basket. If you’ve been thinking about how to optimize your Brands Digital Shelf, then get in touch & learn how DataWeave can help!

Show moms extra love this year. With Mother’s Day coming up fast, savvy beauty and fashion brands will use this special occasion to inspire pampering and gift giving to fuel their e-commerce sales growth.

This year, beauty and fashion are poised to boom, as 40% of consumers plan to buy beauty products and 37% will buy new outfits for going out. 1 According to eMarketer,apparel and accessories e-commerce sales will grow nearly 19% this year due to pent-up demand for clothing, while health and beauty sales will rise 16%. 2

“People will be happy to go out again … there will be a fiesta in makeup and in fragrances.”

~L’Oréal CEO and Chairman Jean-Paul Agon

After beauty and apparel sales declined last year, brands now seize every opportunity to capitalize on the categories’ resurgence in 2021. To differentiate their goods, brands can use e-commerce marketing best practices to position their fashion and beauty items as spectacular gifts that moms will love.

Aligning with the latest trends can help brands boost online growth.

Hot trends dominating beauty and fashion

This Mother’s Day, shoppers can delight moms with beauty bestsellers like:

Mask-friendly makeup: As we continue to wear masks over the short-term, cosmetics like false lashes, smudge-proof mascara and ultra-hypoallergenic eyeshadow will remain popular. 3

Fragrances: Online fragrance sales rose 45% year-over-year in 2020. Clean and organic beauty categories grew 56% with fragrance brands growing the most. 4

Purpose-led brands: Consumers crave companies that care. More online searches contain keywords like “ethical beauty” and “sustainable makeup” for products that help consumers look good and feel good. 5

Online fashion is in vogue

Before the pandemic, consumers bought less than one-third of their apparel or footwear online; last year, the proportion surged to an astounding 51%. In 2021, consumers will invest even more in their wardrobes, including trends like:

Comfort: Athleisure will remain in demand as many consumers still prefer comfortable clothing when they work from home. 7

Beloved staples: Classic pieces like jeans, dresses and simple yet elegant tops are making a comeback as consumers start to go out more. 8

Retro ‘80s: Ladies are ready to party like it’s 1984. Bright and metallic colors and sequins for occasionwear (and even NFL linebacker-inspired shoulderpads) are recreating a fun, indulgent ’80s vibe. 9

Brands’ secret weapon for a competitive advantage

For successful Mother’s Day campaigns, more fashion and beauty brands will use digital shelf analytics for marketing decisions that maximize their ROI and e-commerce sales.

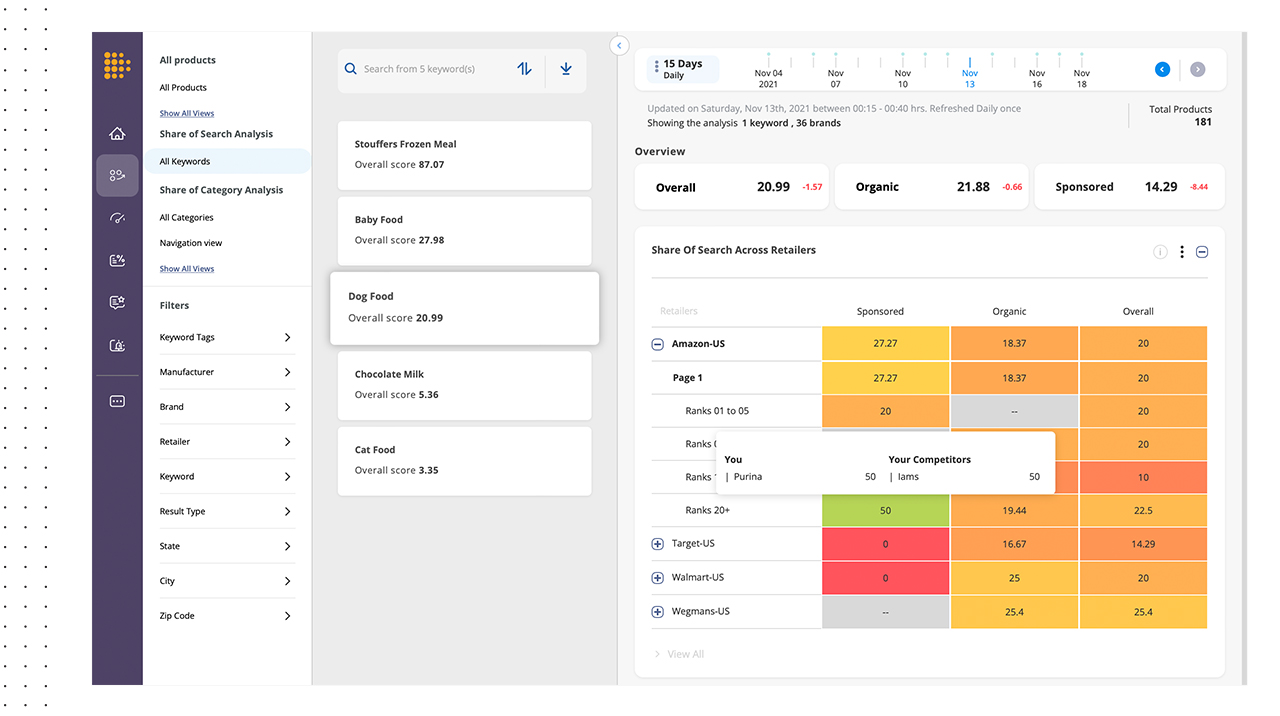

To ensure online shoppers discover Mother’s Day products with ease, brands are usingShare of Searchinsights to measure their share of digital shelf. These DataWeave analytics tell brands which keywords perform best. Brands can also benchmark their search and navigation visibility against rivals’ rankings across e-commerce categories, websites and geographic regions.

Using Content Auditinsights tells brands how their content is performing. They can discover and fill content gaps so their products show up more prominently. Optimizing content (like keywords, product page titles, descriptions, ads and sponsored space) and images to align with the retailers’ search algorithms ensures a consistent brand experience across all online channels. Improving content helps brands connect to consumers with marketing that resonates and inspires them to buy. Brands also use

Pricing and Promotionsinsights to measure the effectiveness of their online promotions and secure sales. Brands can stay competitive by ensuring their pricing and promotions are in line with rivals’ offers, such as identifying first movers and rivals with the deepest discounts across retailers and SKUs. Brands can even determine how imitating rivals’ pricing and promotional moves could impact revenue and sales volume.

Help shoppers make Mom’s day

Since Mother’s Day is almost here, beauty and fashion brands can apply these data insights to connect consumers with a variety of products moms will love. Digital shelf analytics from DataWeave can help brands deliver timely campaigns, improve their return on digital marketing spend and make effective marketing decisions to drive e-commerce sales.

1 Howland, Daphne. Wells Fargo sees permanent behavior shifts from the pandemic. Retail Dive. March 29, 2021. 2 Droesch, Blake. US Ecommerce by Category 2021. eMarketer. April 27, 2021. 3 Wood, Dana. Is Makeup Dead? The Robin Report. April 18, 2021. 4 Larson, Kristin. Fragrance Sales Pick Up As Consumers Reengage With The Outside World. Forbes. April 27, 2021. 5 What Can Brands Learn About Sustainability From Green Beauty Consumers? Beauty Business Journal. June 15, 2020. 6 Howland, Daphne. Wells Fargo sees permanent behavior shifts from the pandemic. Retail Dive. March 29, 2021. 7 Ibid. 8 Bhattarai, Abha. Americans are starting to buy real clothes again. The Washington Post. March 18, 2021. 9 Warren, Liz. Loose Denim and Bold Occasionwear on Full Display for Fall 2021. Sourcing Journal. April 2, 2021.

The proliferation of informed shoppers, e-commerce sites, and competitors of all sizes has increased the complexity of – and lucrative opportunities in – brand management.

Now more brands rely on data insights to uncover specific ways to make their digital marketing more arresting, effective and profitable. Many brands struggle with e-commerce profitability due, in part, to advertising expenses that often yield lackluster results.1

Analytics are growing in retail significance, as 88% of retail and consumer goods marketers say data improves their marketing by allowing them to personalize touchpoints. Relevant marketing and great marketers helps brands connect with consumers. Let’s see why leading brands are adding data insights to their 2021 marketing strategies to fuel online sales growth.

Brands discover how to get discovered

Consumer goods brands no longer leave it up to chance that consumers will find them online. The digital migration of companies and consumers over the past year means more noise for brands to breakthrough.

Now search is growing in importance to improve brands’ online product discovery. Here’s why:

87% of shoppers begin their hunt in digital channels3

17% rise in paid search in late 20204

24% rise in paid social advertising during the same period5

To grab consumers’ attention by being easier to see, more brands are turning to data insights to track their online visibility.

Brands need to look for ways to mitigate the high costs of acquiring customers online6

Brands use marketing analytics related to keywords and navigation searches help brands know exactly how much space on the digital shelf they occupy across different online platforms.

These DataWeave’s Share of Search solutions help brands understand what percentage of the digital shelf they command through either keywords or navigation. These insights can help brands decide whether to boost their brand visibility using sponsored ads to ensure their products show up more prominently in online search results to boost brand reach and awareness on each channel. For instance, brands can tell whether consumers search for products using branded, generic or category-specific keywords to align their marketing accordingly.

In addition, brands can see how their organic and sponsored results rank compared to their competitors to spot ways to improve their visibility rank and decrease customer acquisition costs.

Content differentiates a brand’s digital shelf

For a striking digital presence and enhanced discoverability, leading brands measure how effectively their content inspires online shoppers to choose them.

Brands can improve their digital marketing results by using Content Audit insights to spot patterns among their top-performing campaigns. They can also benchmark their content with category bestsellers to discover how to optimize their online performance to grow sales volume and market share.

Strategic advertising requires high-quality photography and data-driven content7

Using these data insights from DataWeave helps brands determine how well their content (including product description pages and images) align with e-commerce algorithms and lead to online traffic, engagement and sales. Brands also adapt faster by adjusting underperforming campaigns to reduce costs and optimize their digital marketing spends.

Brands can fill content gaps across online channels with enhanced product information that aligns content and images with brands’ product information management (PIM). Using analytics to deliver a consistent brand experience across all online channels can help brands build relationships with consumers and earn their trust.

Alluring promotions help brands secure the sale

As e-commerce evolves, brands have matured beyond Google AdWords and Facebook campaigns to offer targeted promotions across digital touchpoints, which increases marketing reach and complexity.

To boost clarity, be in demand and drive sales across online platforms, more leading brands use data insights to measure the effectiveness of their digital Promotions. Promotional insights from DataWeave keep brands informed of trending categories and products to keep their online offerings relevant and timely. Brands can pinpoint exactly which products to promote and which e-commerce sites help them drive the most profitable results with compelling digital offers.

Brands that respond quickly to their customers’ needs have the upper hand8

Analytics also keep brands competitive and relevant by benchmarking their promotional strategies with their rivals’ and continuously monitoring rivals’ online moves. For instance, brands can track the promotions their competitors offer for similar products across different e-commerce sites. These competitive insights help brands quickly spot opportunities to optimize their online conversions with appealing promotions that reflect market trends.

Better marketing decisions can help brands grow sales and share

Data insights make brands more enticing by connecting the dots among their online visibility, content and promotions. Brands uncover ways to make smarter marketing decisions faster to improve their top line and decrease customer acquisition costs. DataWeave analytics also help brands stand out and improve product discovery, engagement and sales. As a result, brands save time and boost their agility with relevant marketing that resonates and inspires shoppers to keep coming back.

1 Jansen, Caroline, Cara Salpini and Maria Monteros. 8 DTC trends to watch in 2021. Retail Dive. February 3, 2021 2 Casna, Kathryn. Ecommerce Trends That Are Shaping the Way Businesses Sell Online. Salesforce. 2021. 3 Casna, Kathryn. Ecommerce Trends That Are Shaping the Way Businesses Sell Online. Salesforce. 2021. 4 The Future of eCommerce in 2021. Shopify Plus. 2021. 5 The Future of eCommerce in 2021. Shopify Plus. 2021. 6 Jansen, Caroline, Cara Salpini and Maria Monteros. 8 DTC trends to watch in 2021. Retail Dive. February 3, 2021. 7 Glasheen, Jasmine. 2021 Forecast: Next Gens in a Brand-New World. The Robin Report. January 3, 2021. 8 Monteros, Maria. Forrester: Few brands can anticipate and act on consumer needs. Retail Dive. February 10, 2021.

The start of 2020 brought with it the promise of global economic growth. Markets in the US were on a steady rise we also witnessed demand from brands and retailers in Europe and the Middle East. All seemed to be on track to make it a year of plenty.

Out of nowhere, the end of the first quarter saw the world coming to a grinding halt. The world was held hostage by a global pandemic and the force with which we were hit, was unprecedented.

From February to mid-May we saw things come to a sharp halt. We at DataWeave seized this intermittent downtime to bolster our product offerings.

On the flip side, when the world did start opening May onwards, we saw completely new categories take center stage digitally. With new habits and trends taking shape, the pandemic single-handedly caused exceptional growth in the Food and Grocery Delivery intermediaries. Predictably, the rest of the world followed. Our existing customers saw the competition rise steeply with everyone coming online. We invested substantially in our Digital Shelf Analytics solutions after noticing that e-commerce was seeing a boom. 2020 saw brands making their online presence the new norm. This meant that small, medium and large enterprises had to now divert their spending to analytics and e-commerce.

It is interesting to note that the rise in the food and grocery delivery segment gave brands another channel to focus on vis a vis their presence. Brands that were available on these sites focused on how they could optimize their sales on these channels, which proved to be the front runners during the height of the pandemic. While the challenges and opportunities for both these segments overlapped and seemed similar, our solutions helped measure and optimize brand performance across all online channels. Some of the in-demand solutions and analytics we saw our customers use were; share of search, content audit, assortment and availability, pricing and promotions, and ratings and reviews.

There were mixed emotions in the market, with regard to the best use of marketing spends. Human resource and client cutbacks happened across the board. At DataWeave however, we had the pleasure of onboarding 25 new clients including retailers and brands ranging from food and grocery delivery, home improvement from across multiple geographies.

Infographics

Throughout the year, the work never ceased at DataWeave. The team showed incredible resilience while working remotely, making sure our deliverables were being taken care of, at all times. Due to the e-commerce boom and immense pressure from existing and new entrants in the digital space, our clients saw a need to gather more insights. With the given uptick, we are happy to report that our stellar 95%+ accuracy record for in-depth insights at scale, was maintained through the course of all the work done.

Looking forward to the year 2021:

In the US, the adoption of e-commerce accelerated as traditional brick and mortar stores shut down and pivoted. To put things into perspective, e-commerce adoption grew only by 4.3% from 2014 to 2019. In just three months in 2020, e-commerce adoption grew at 4.3%! Add to that, with approved vaccines making their way slowly to the public, we do anticipate the travel sector to open up and we look forward to working with new clients.

Nike’s Chief Executive, John Donahoe recently said, ” We know that digital is the new normal. The consumer today is digitally grounded and simply will not revert back…the shift to online sales could be a permanent trend.” We could not agree more! With online sales here to stay, brand and retailers’ requirements to keep their competitive edge will only continue to grow. We at DataWeave, look forward to delivering the results they want in this new year, and for the years to come.

According to our preliminary analysis of Prime Day 2020, Amazon’s rivals offered more generous discounts within Home categories to stay competitive as more consumers invest in their homes this year.

This year the COVID-19 pandemic has transformed consumers into homebodies who increasingly work, learn and shop from home. This year also marks the first time Prime Day took place in the Fall, jumpstarting the holiday sales season.

At DataWeave, we wanted to know whether Prime Day 2020 lived up to the hype and how Amazon’s deals compared to other retailers’ discounts. Our analysis examines products across four popular Home categories: Bed & Bath, Furniture, Kitchen and Pet Care.

Our Methodology

We tracked the pricing of several leading retailers (Home Depot, Target, Walmart and Amazon) selling the Home categories of Bed & Bath, Furniture, Kitchen and Pet Care to assess their pricing and assortment strategies during this annual sales event. Our analysis focused on additional discounts offered during the sale to estimate the true value that the sale represented to consumers. Our calculations compared product prices on Prime Day versus the prices prior to the sale. The sample consisted of up to the top 750 ranked products across 16 popular product types for the home.

The Verdict

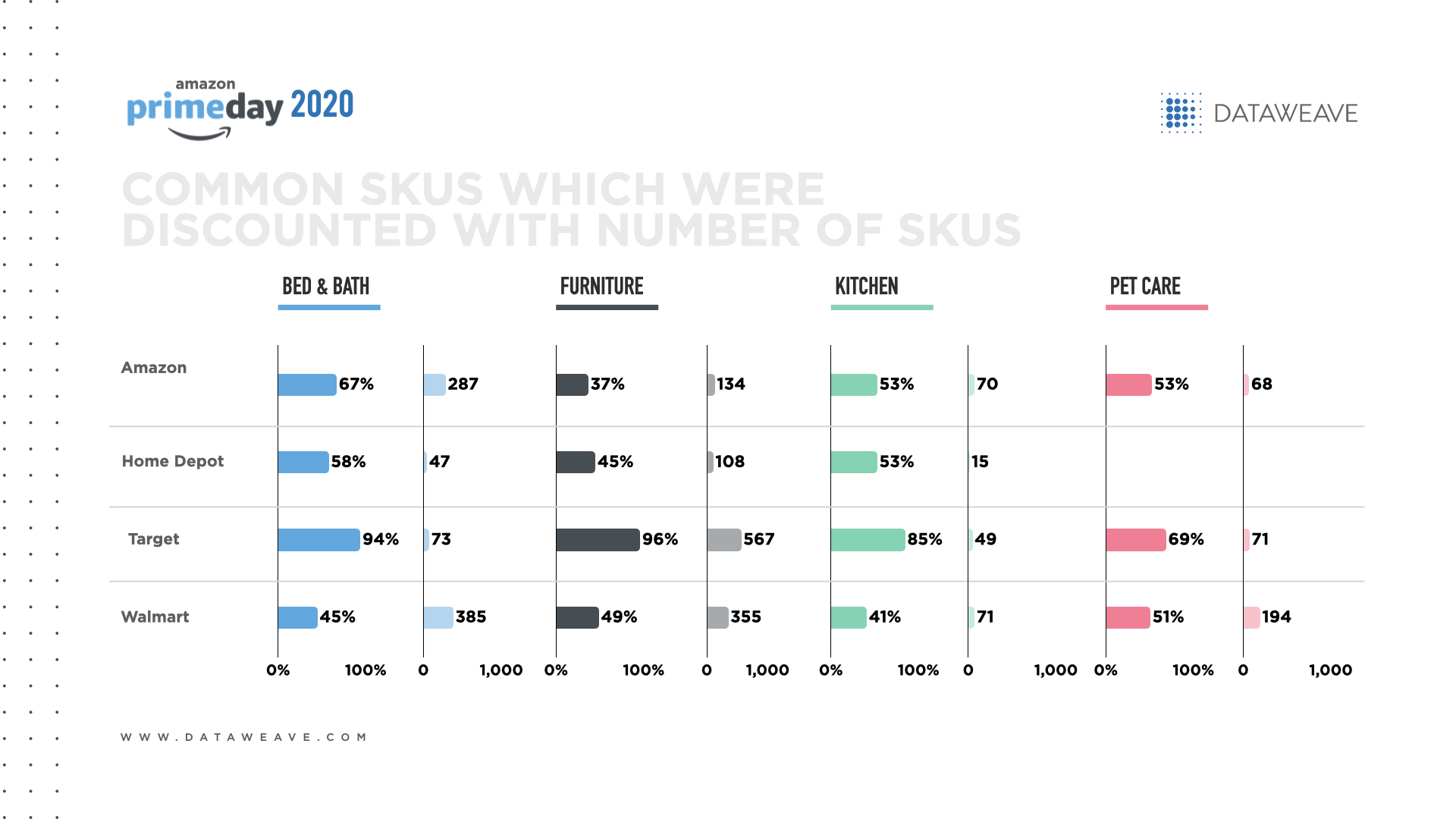

Overall, Amazon reported the lowest price reduction in all Home categories (12.4%), compared to Target (22.1%), Home Depot (16.5%), and Walmart (15.1%). Yet Amazon reported the second-highest percentage of additionally discounted products (9.6% vs. 11.0% for Target).

After Prime Day ended, certain retailers’ Home assortments saw more significant price increases than others. For instance, 88% of Target’s 760 products in Bed & Bath, Furniture, Kitchen and Pet Care received a price increase during the post-sale period, compared to 47% of Walmart’s 1005 products. Walmart’s everyday low price strategy helps to explain the difference between the two big box retailers.

These results suggest that Prime Day 2020 may boost Amazon’s marketing and PR engagement yet its rivals offered the most generous deals in Home categories. As home-related categories’ sales soared during the pandemic, Amazon’s competitors offered deep discounts to stand out online and grow their market share. As such, consumers may want to embrace the habit of comparing multiple retailers’ websites to discover the best Prime Day deals in Home categories.

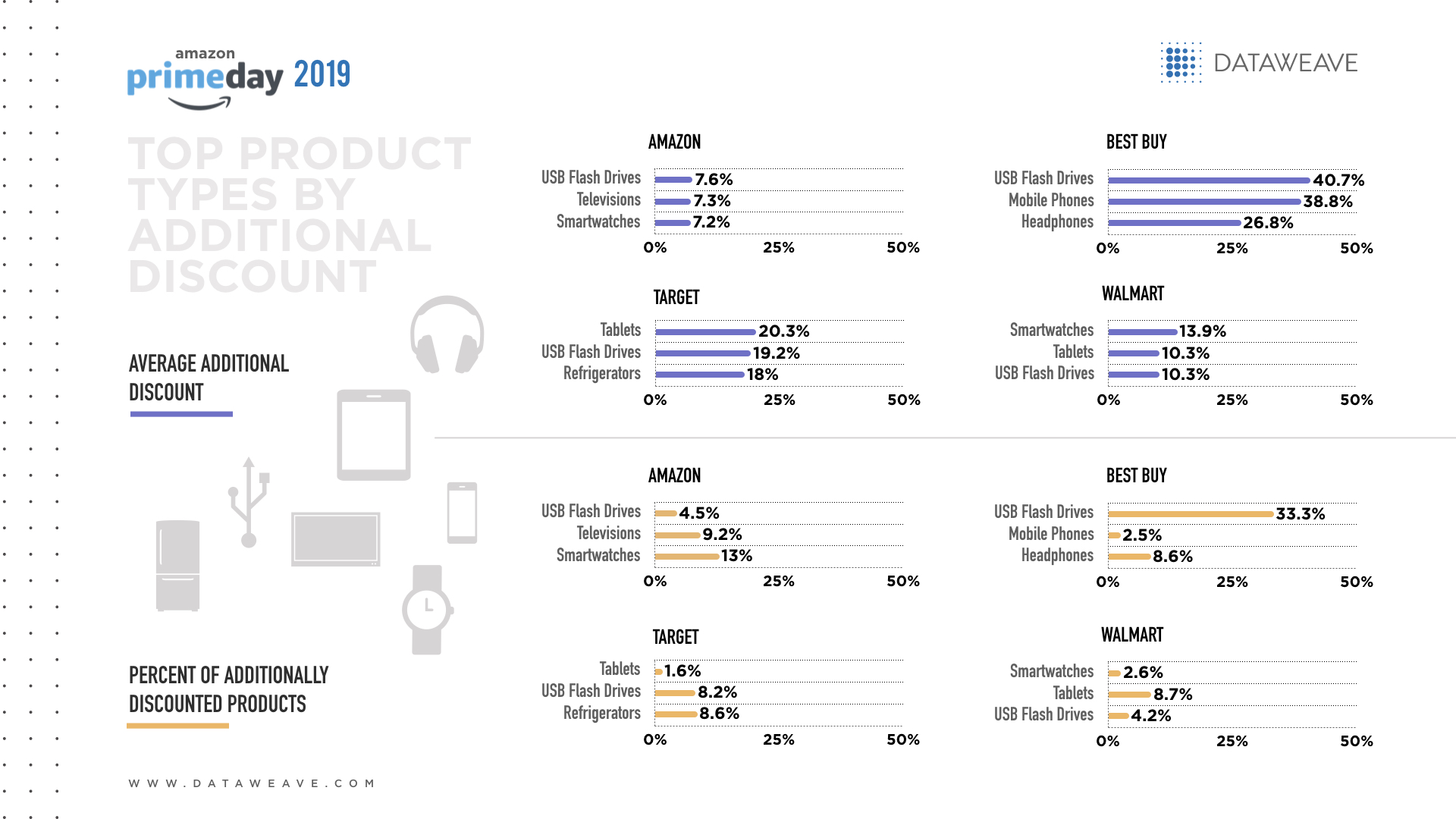

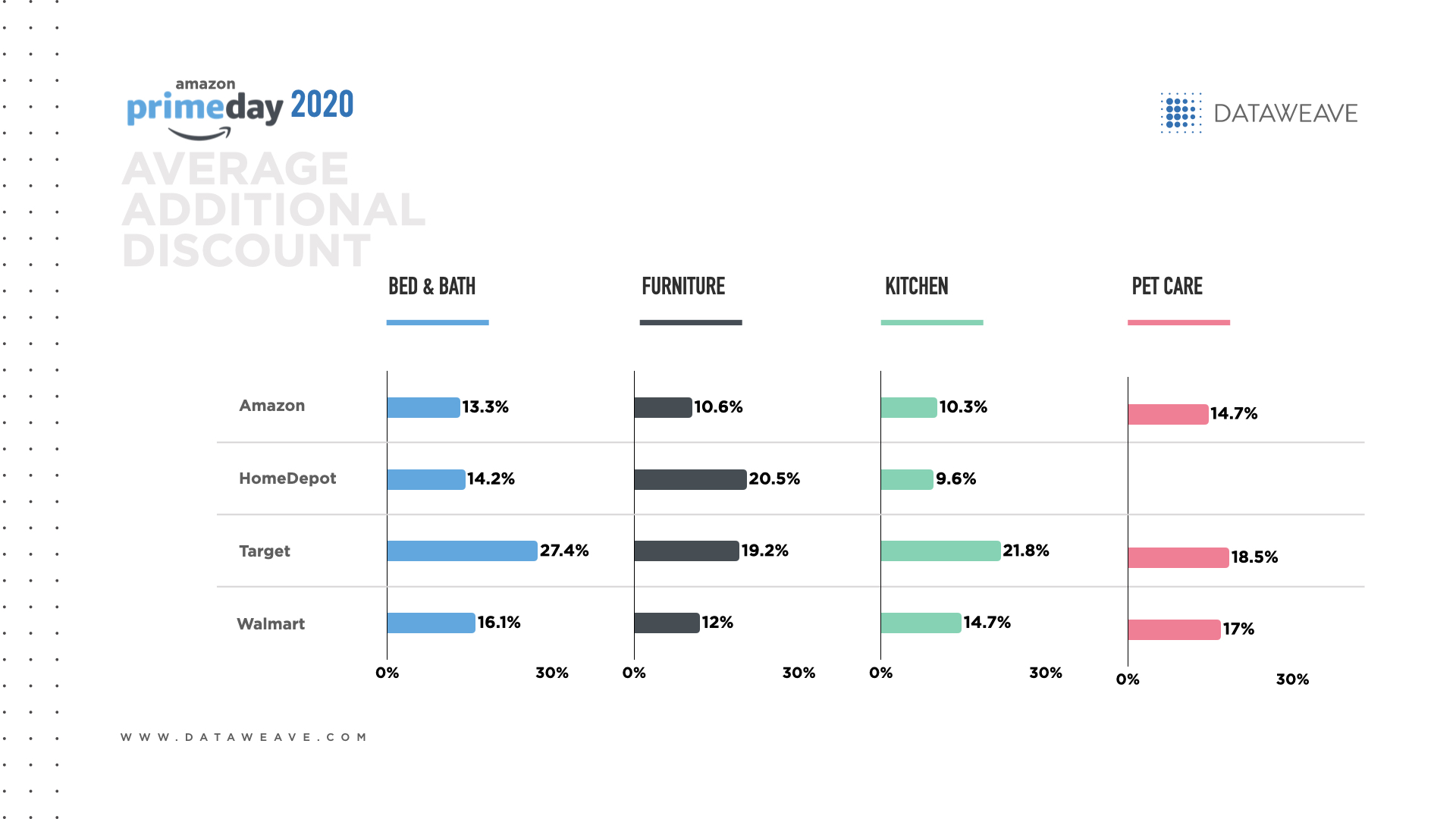

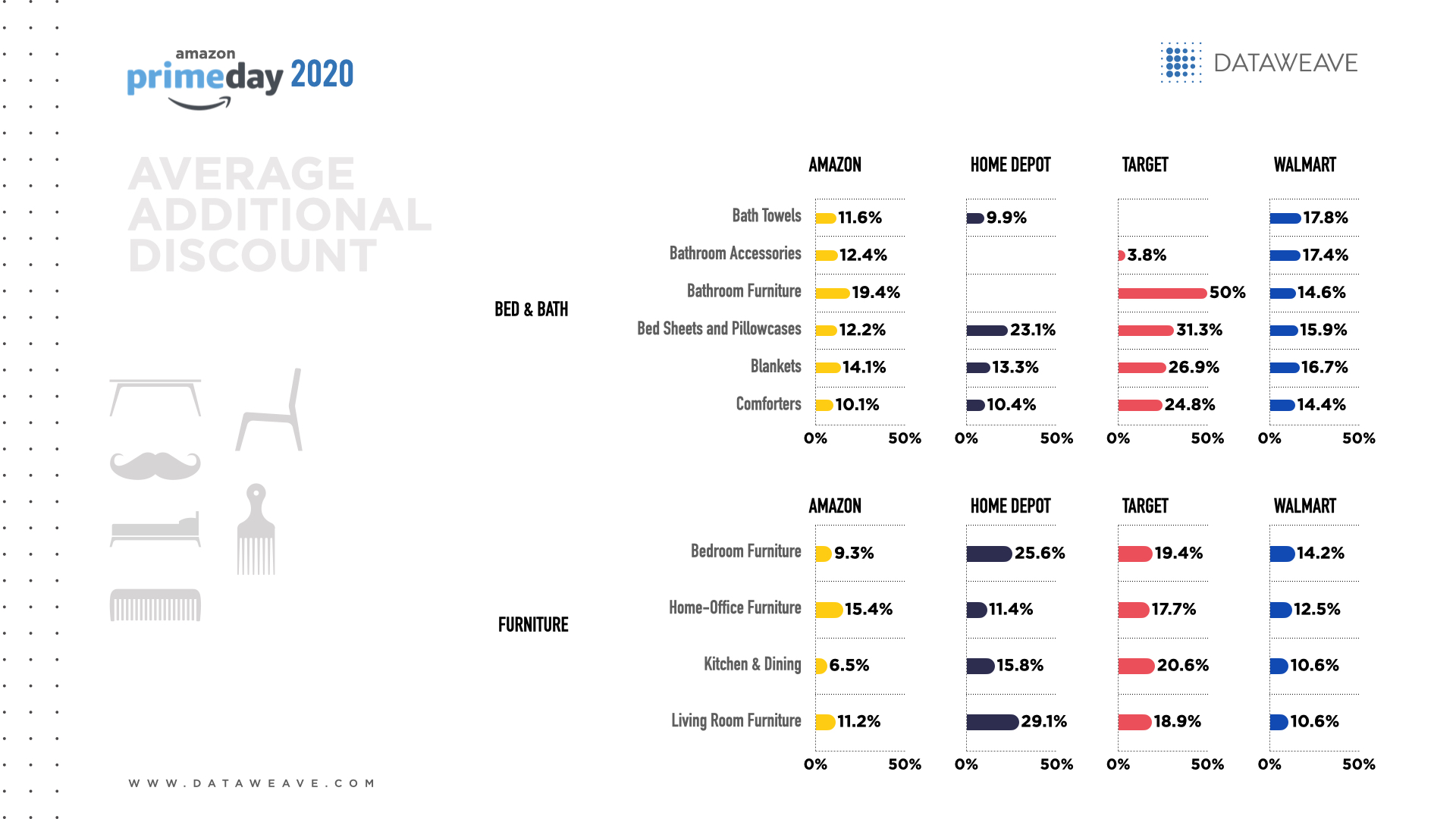

Top product types by additional discount

In Bed & Bath, Target offered the biggest average additional discount (27.4%) and Amazon offered the lowest (13.3%). Bed sheets and pillowcases were a popular product category for additional discounts across all four retailers, with Target offering the best average additional discount at 31.3%. Other popular product types among rival retailers included blankets, comforters and bathroom furniture.

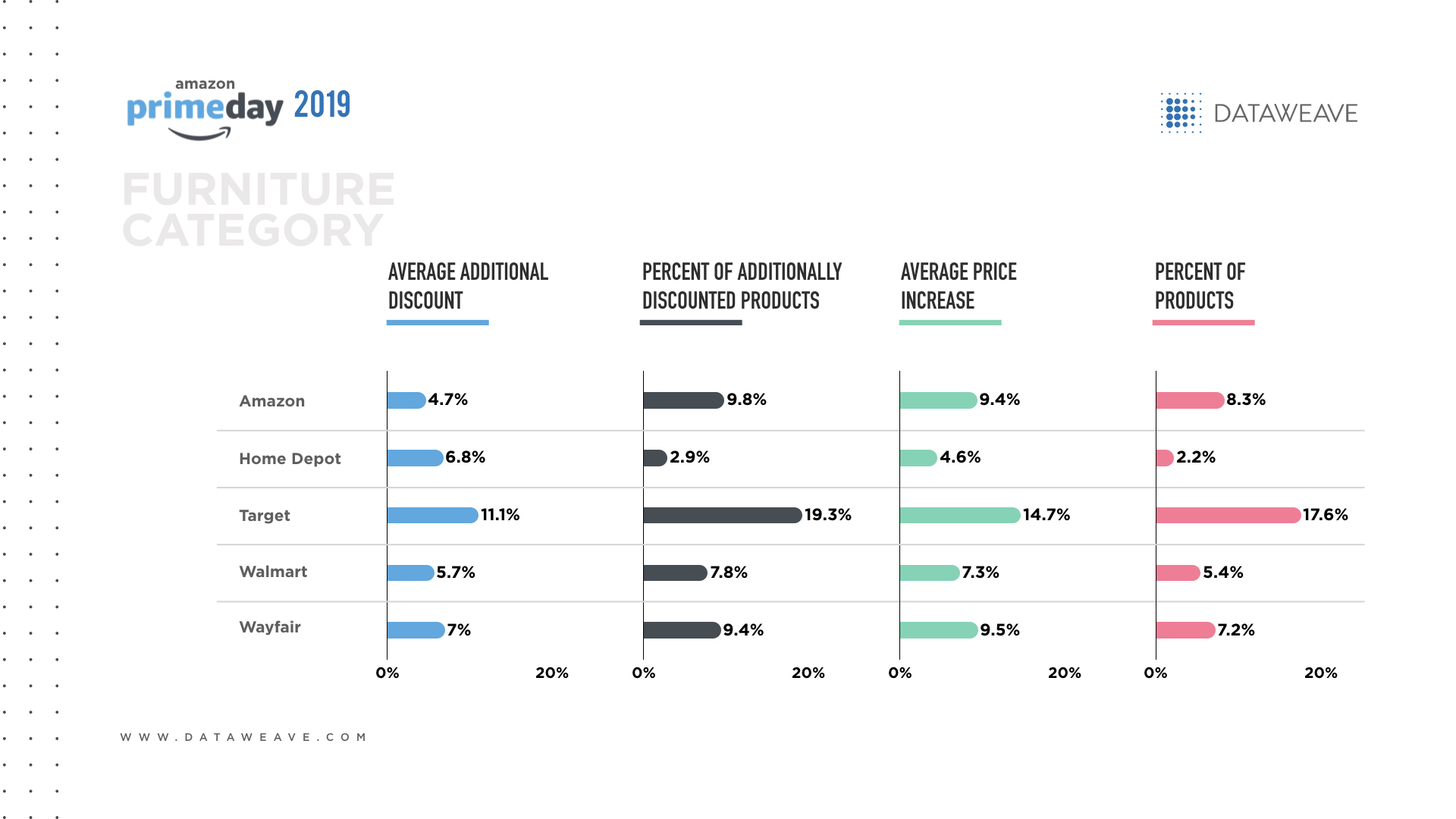

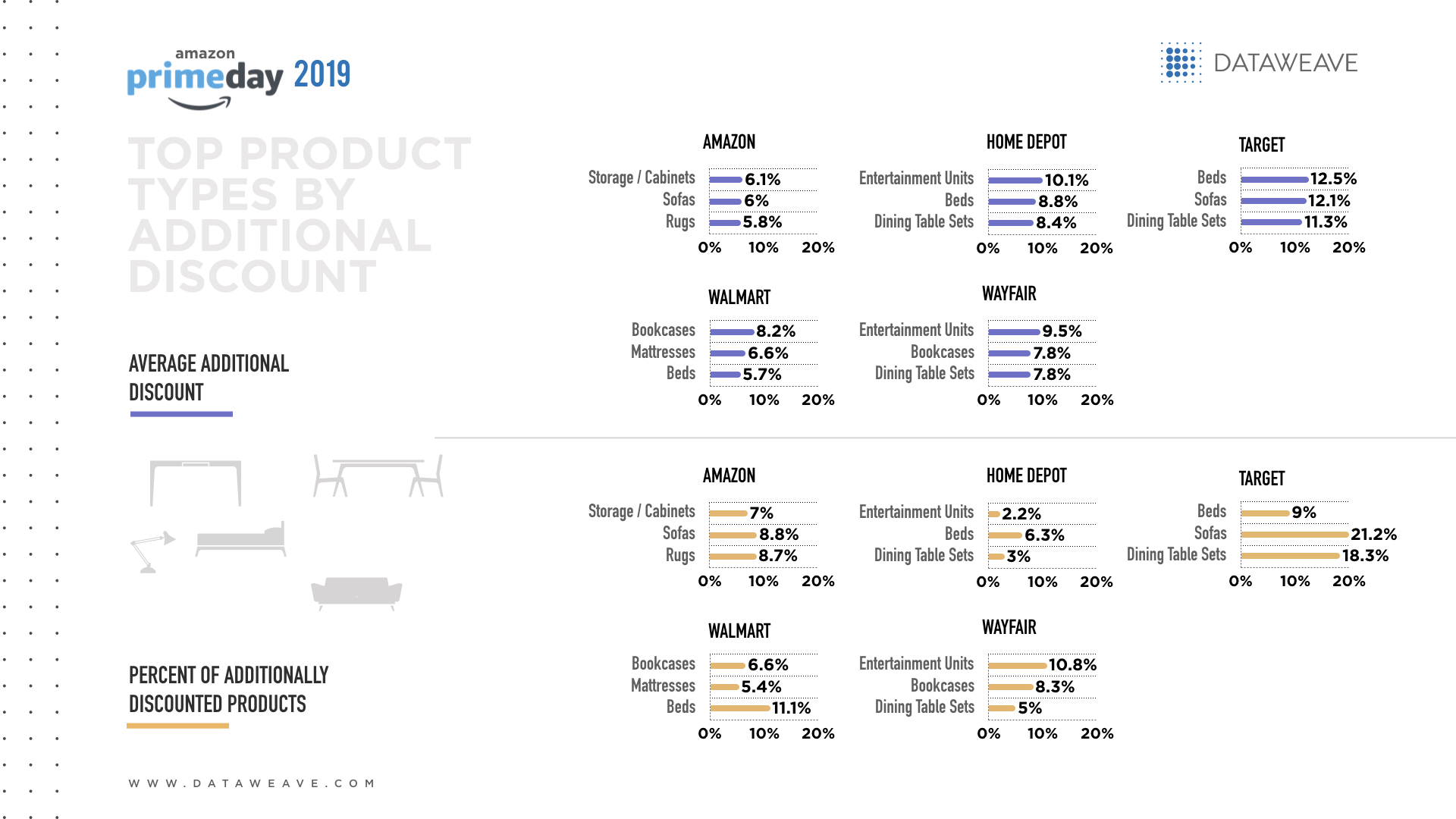

In Furniture, Home Depot (20.5%) offered the biggest overall additional discount, closely followed by and Target (19.2%). Living room furniture was a popular subcategory for all four retailers, with Home Depot offering the highest additional discount (29.1%). Other popular product types included furniture for the bedroom, home office, kitchen and dining room.

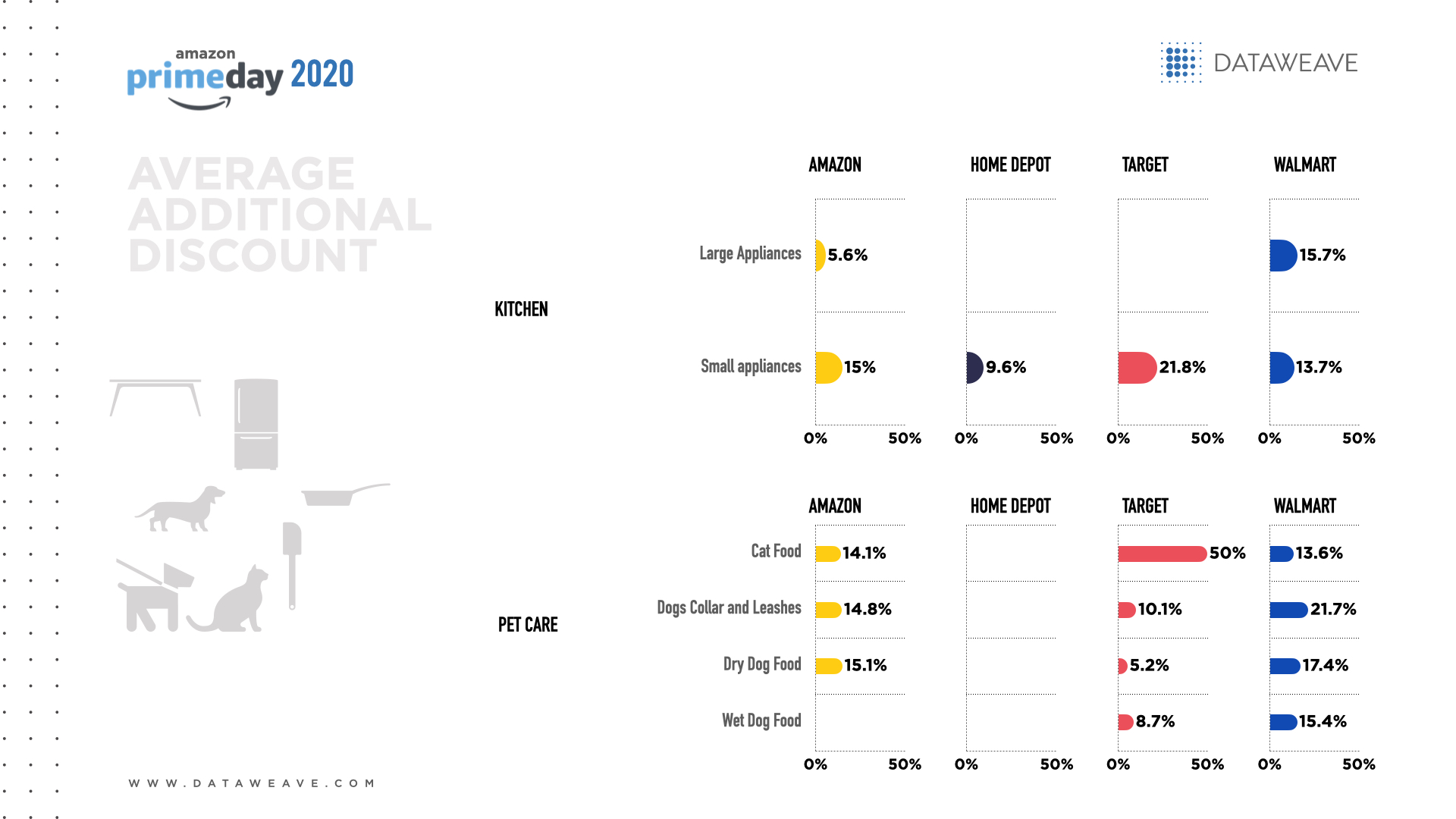

In the Kitchen category, Target offered the biggest average additional discount for small appliances (21.8%), a subcategory in which all four retailers offered discounts. Within the large appliance subcategory, Walmart’s additional discounts were nearly triple Amazon’s (15.7% vs. 5.6%).

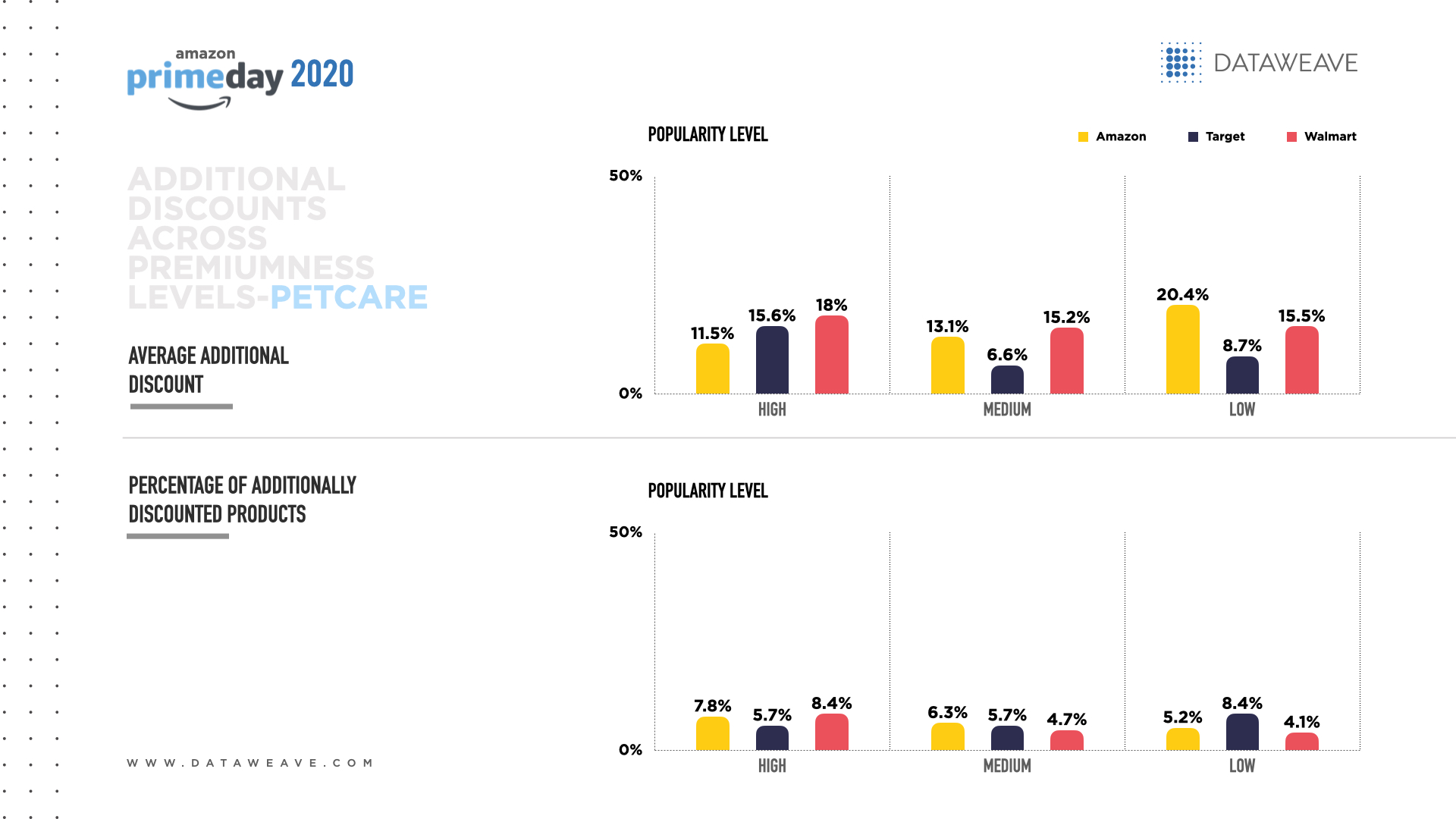

Within the Pet Care category, Target offered the biggest average additional discount (18.5%). Cat food was a popular product category, with Target offering the best average additional discount (50.0%). Other popular product types across all four retailers included dog collars, leashes and dry dog food.

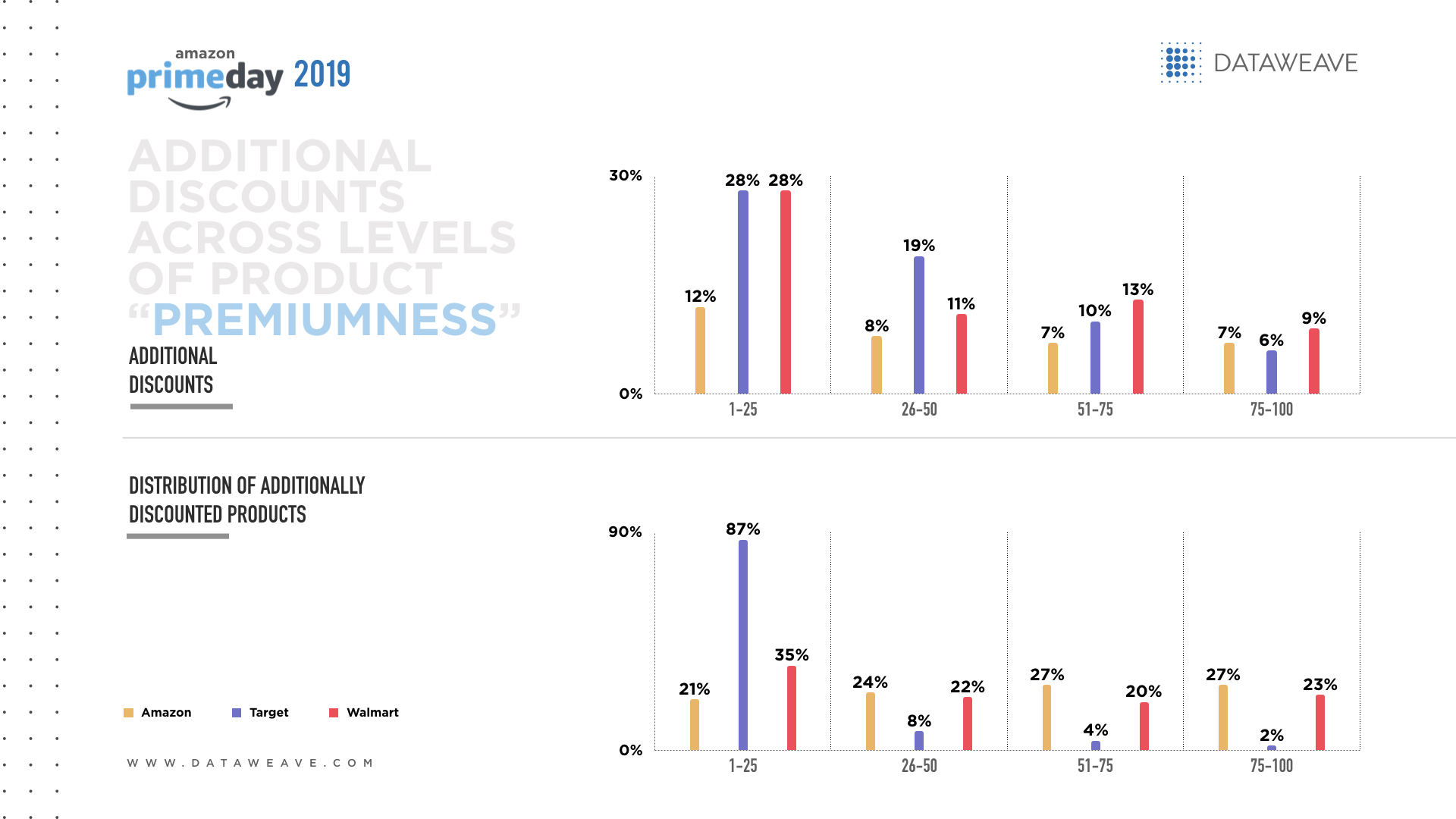

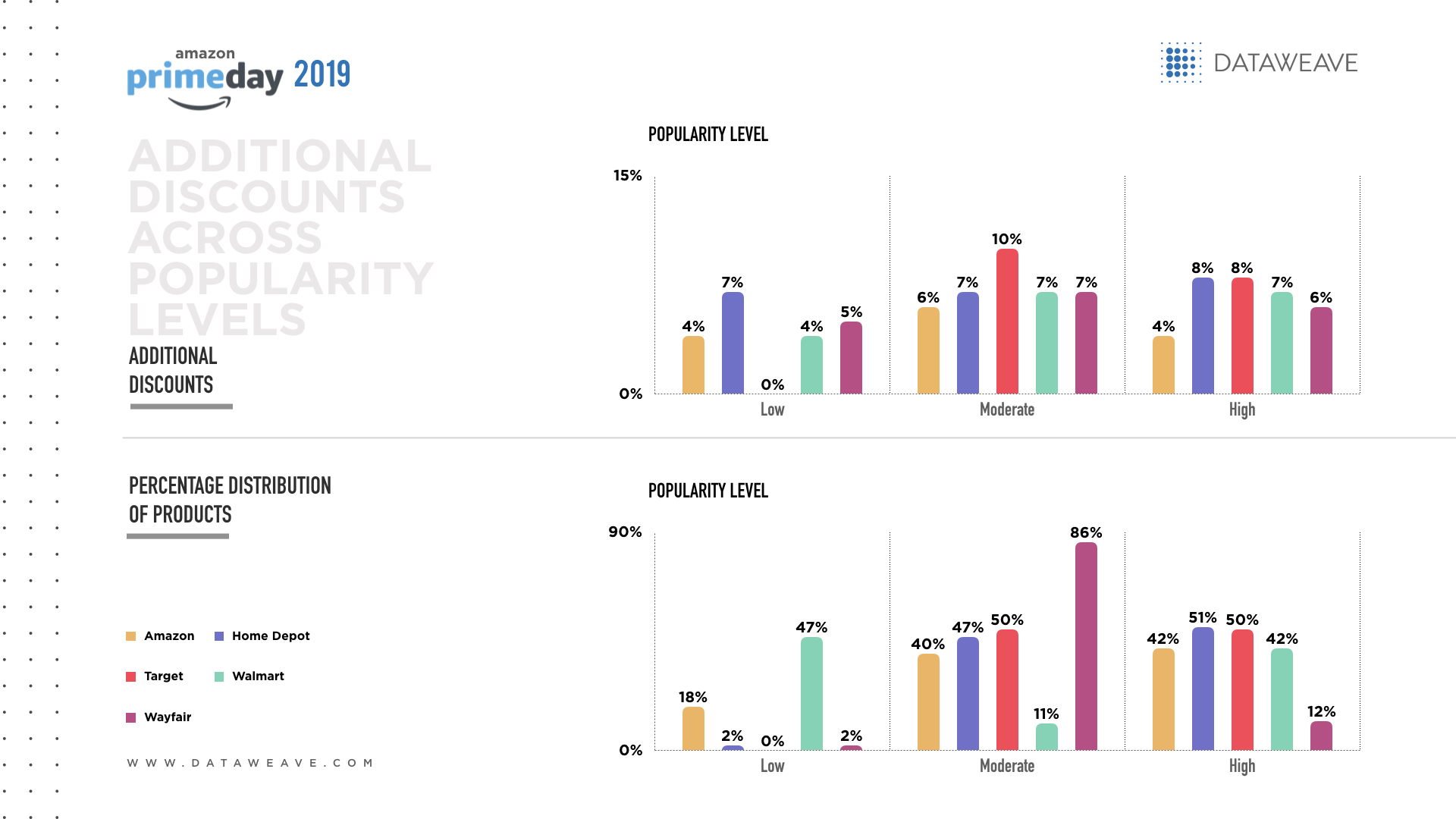

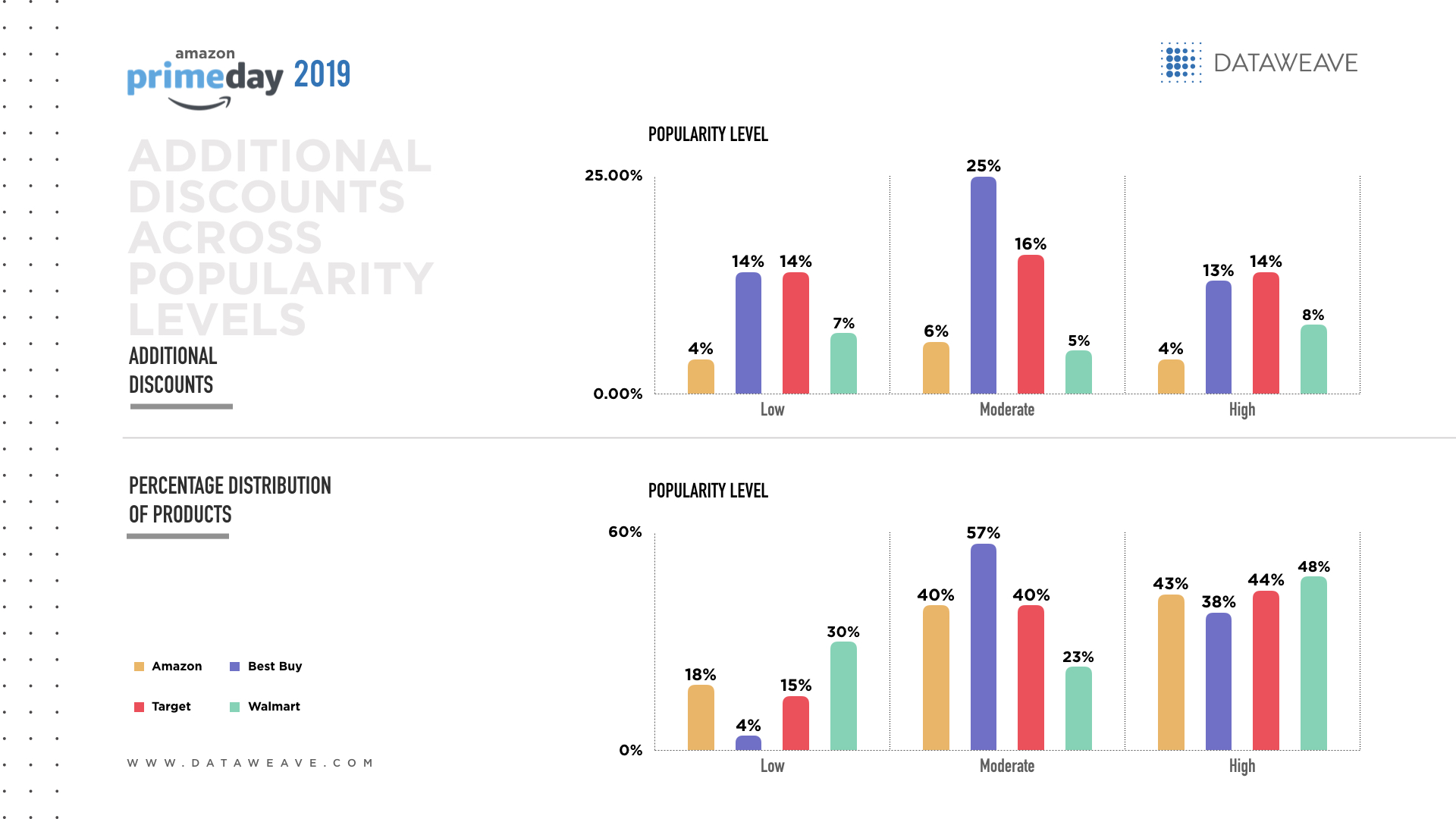

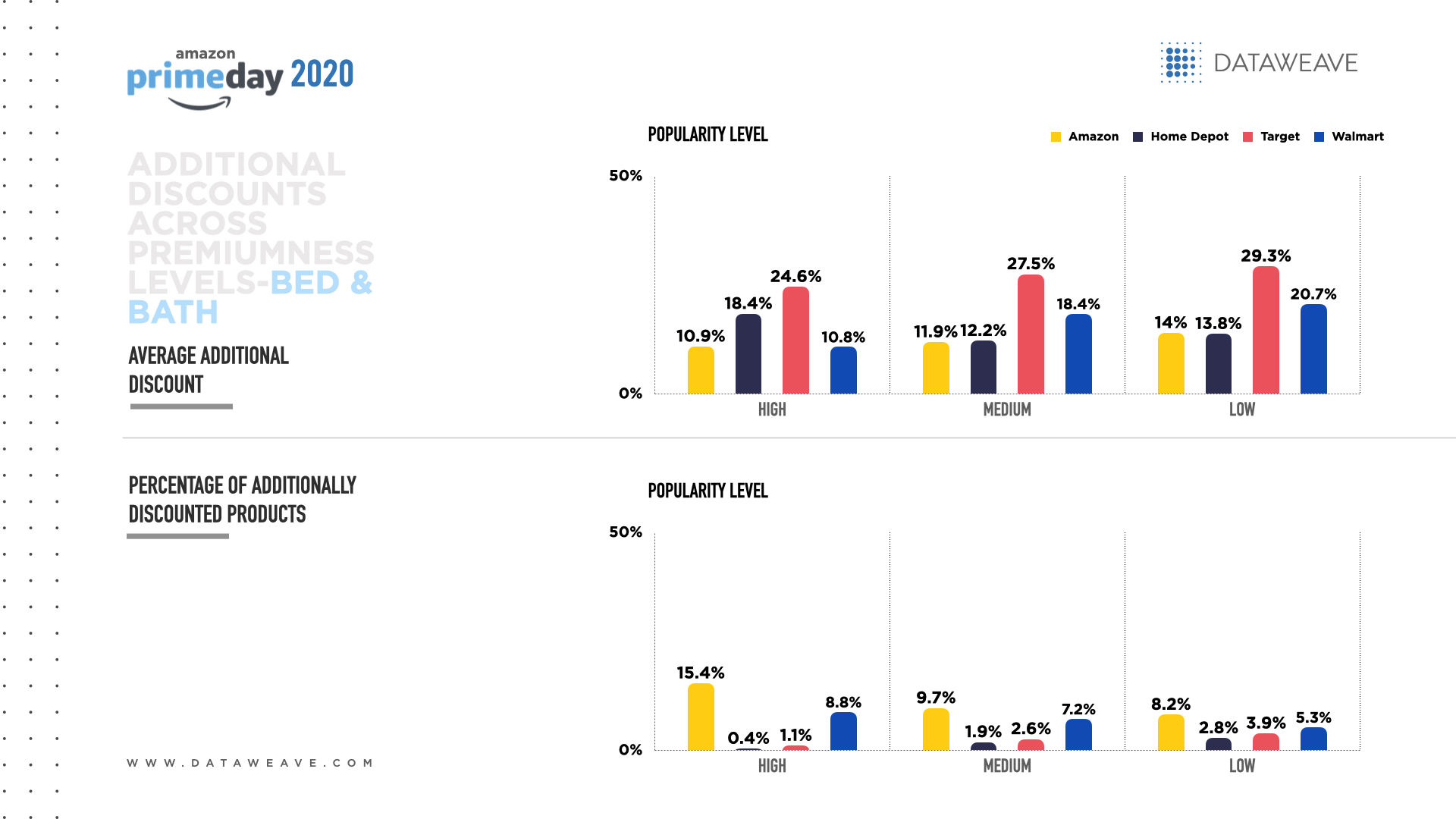

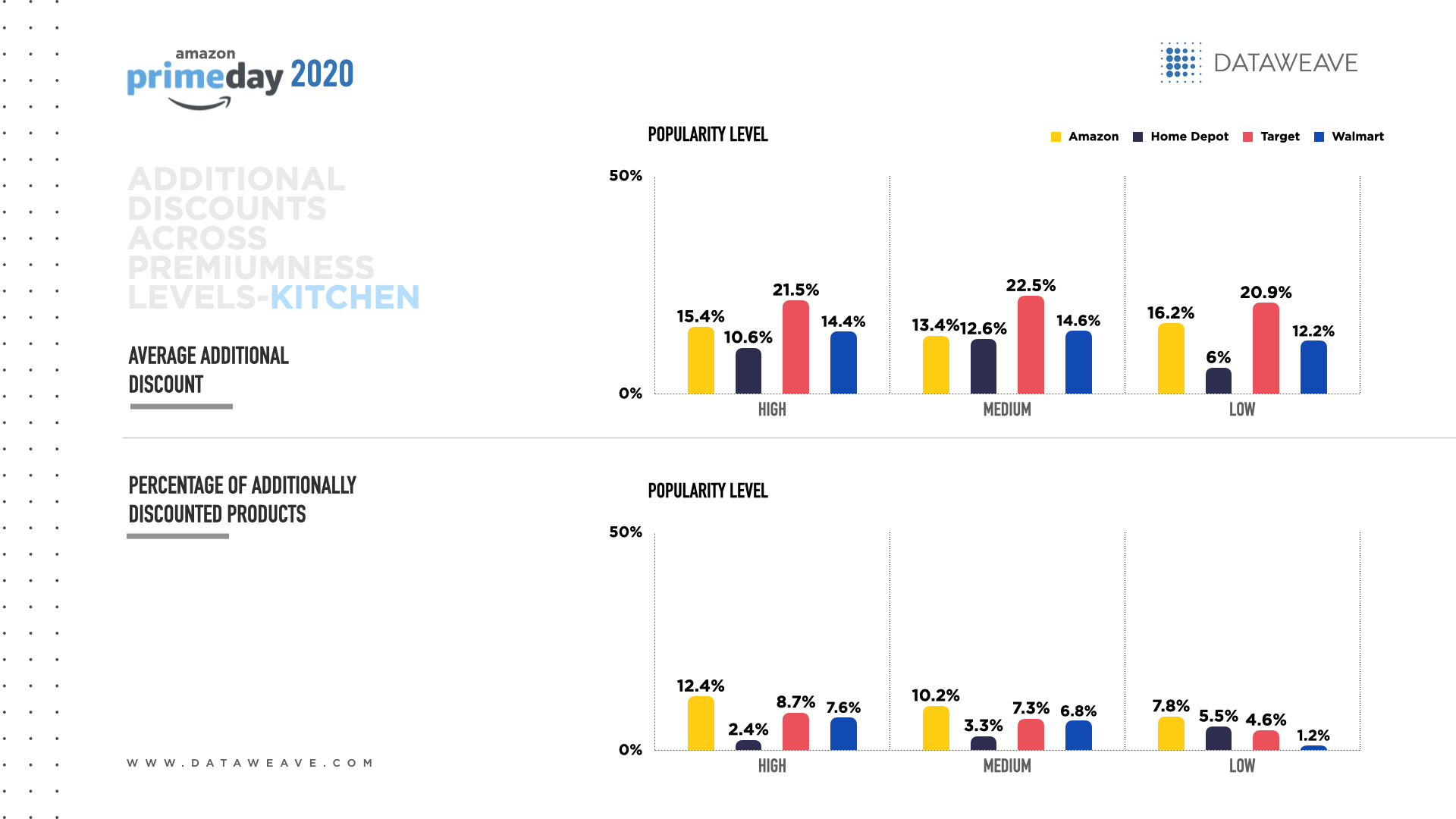

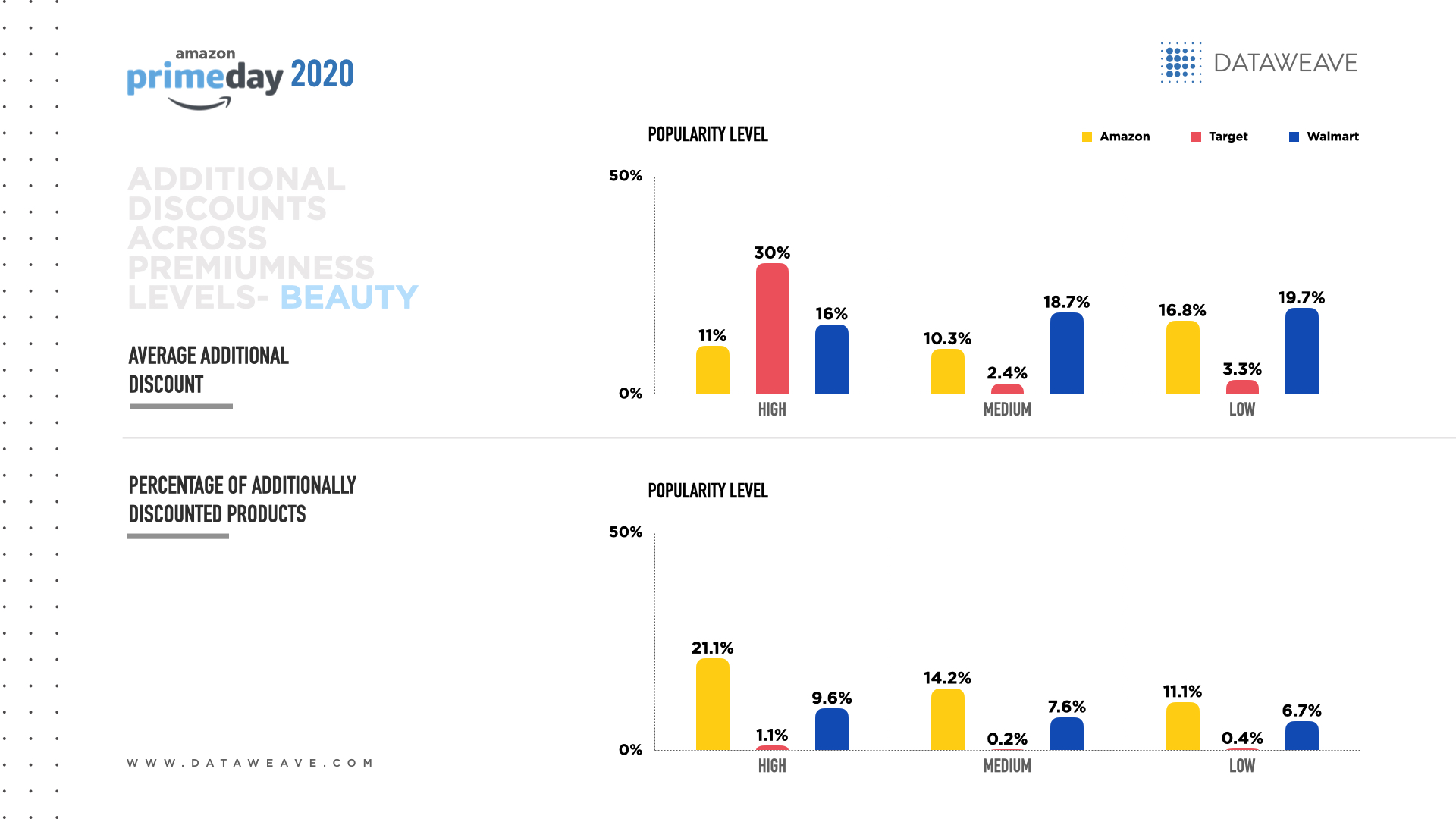

Additional discounts across product “premiumness” levels

Premiumness was calculated as the average selling price before the sale event. This was divided into low, medium and high premiumness levels, with high indicating higher selling prices.

In Bed & Bath, most retailers showed an inverse relationship between their additional discounts and the products’ level of premiumness. Target offered the biggest additional discounts across all levels of premiumness, more than double Amazon’s discounts (27.2% vs. 12.3%). Target’s bold discounting strategy shows a commitment to protecting its competitive position across the entire Bed & Bath category.

By far, Amazon offered the greatest percentage of additional discounts in Bed & Bath compared to its rivals across all levels of premiumness. Comparatively pervasive discounts help the e-commerce giant offer a greater variety of appealing deals within this category.

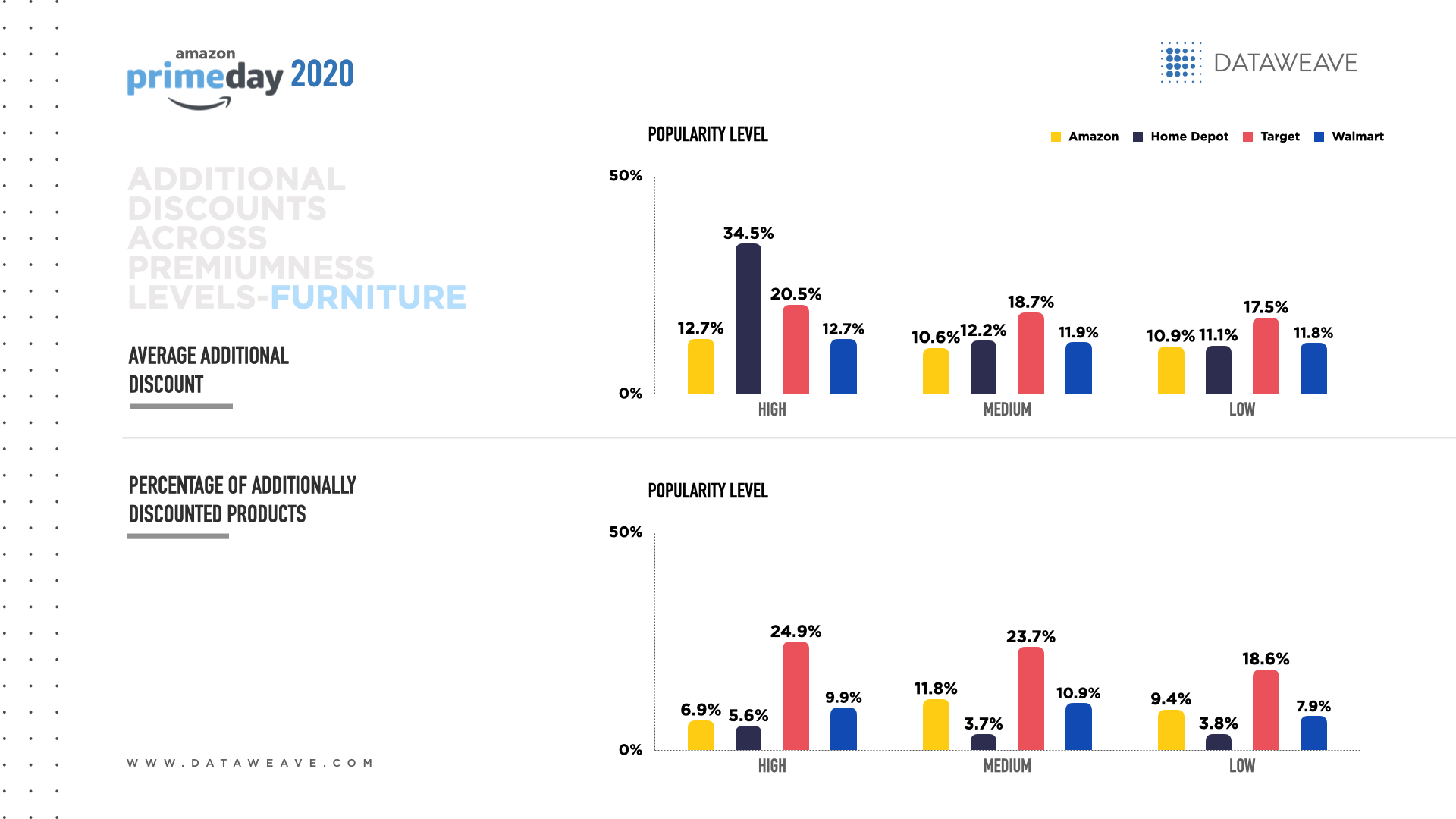

In Furniture, most retailers showed a direct relationship between their additional discounts and the level of premiumness. Notably, Home Depot offered massive additional discounts at the high premium level, nearly triple Amazon and Walmart (34.5% vs. 12.7%). This move suggests Home Depot is serious about winning the business of upscale consumers in the Furniture category.

Target differentiated its assortment by discounting by far the greatest portion of its Furniture at all premiumness levels (22.4%) and Home Depot discounted the least (4.4%). Amazon and Walmart distributed the greatest portion of their additional discounts to the moderate level of premiumness. Target’s strategy tries to attract all Furniture shoppers while Amazon and Walmart try to make their mid-market offerings affordable to more consumers.

Across all levels of premiumness for Kitchen products, Target offered the biggest additional discounts, including almost double Amazon’s discounts at the medium level (22.5% vs. 13.4%). Target’s aggressive discounting shows a desire to be more competitive by attracting consumers at all levels of the Kitchen category.

In the Kitchen category, most retailers offered a direct relationship between the proportion of additional discounts and the level of premiumness, yet Home Depot showed an inverse relationship. Amazon’s proportion of additional discounts across all levels of premiumness nearly tripled Home Depot’s (10.1% vs. 3.7%). This discount strategy shows Amazon’s willingness to offer shoppers deals across a broader variety of Kitchen items.

In Pet Care, Walmart offered the highest overall additional discounts (16.2%), which could fortify its low-cost leadership position for pet lovers at all price points.

While Target offered the greatest overall percentage of additional discounts in Pet Care, Amazon applied more discounts to the higher end of the premium spectrum and Target focused on the lower end.

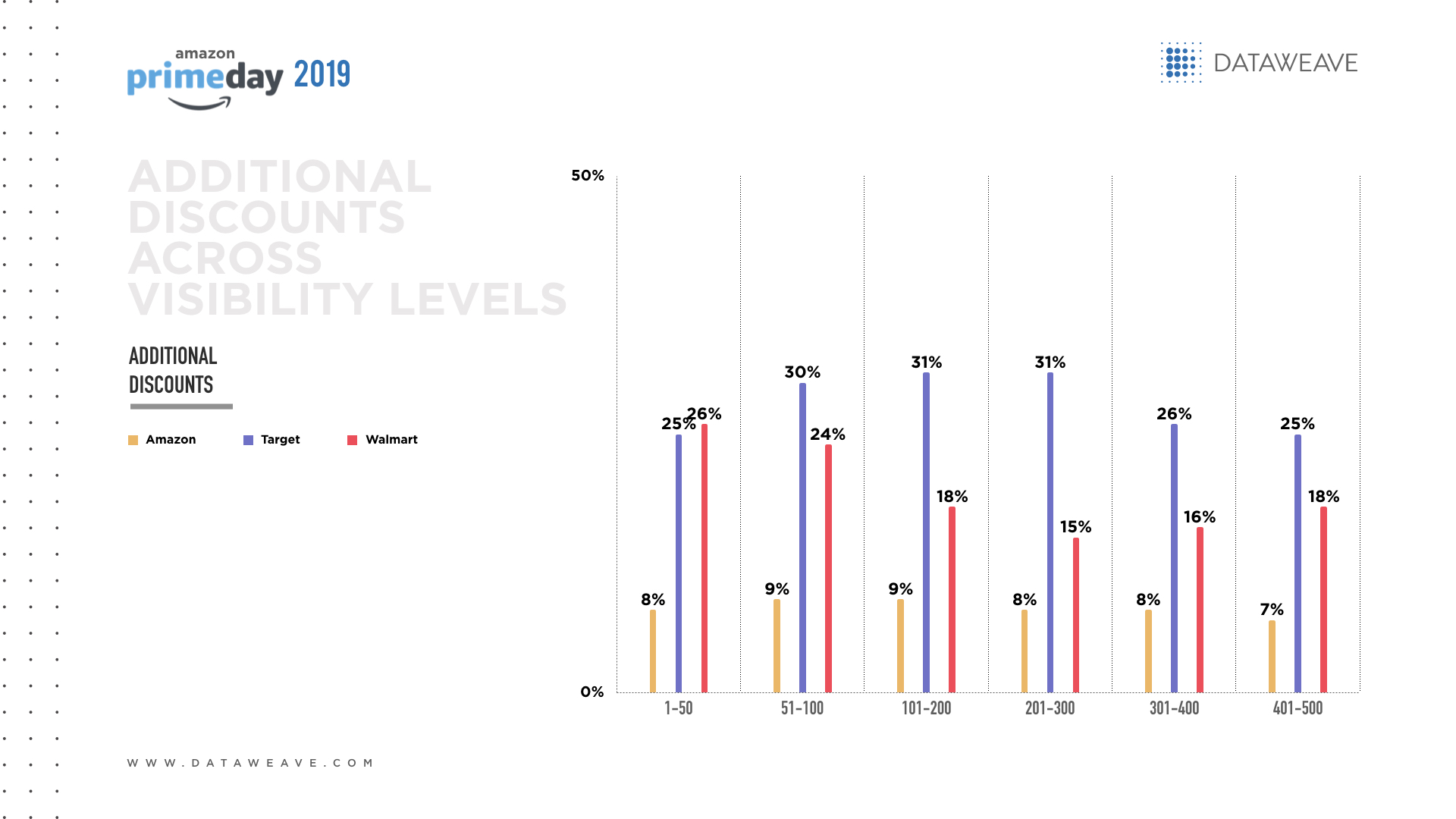

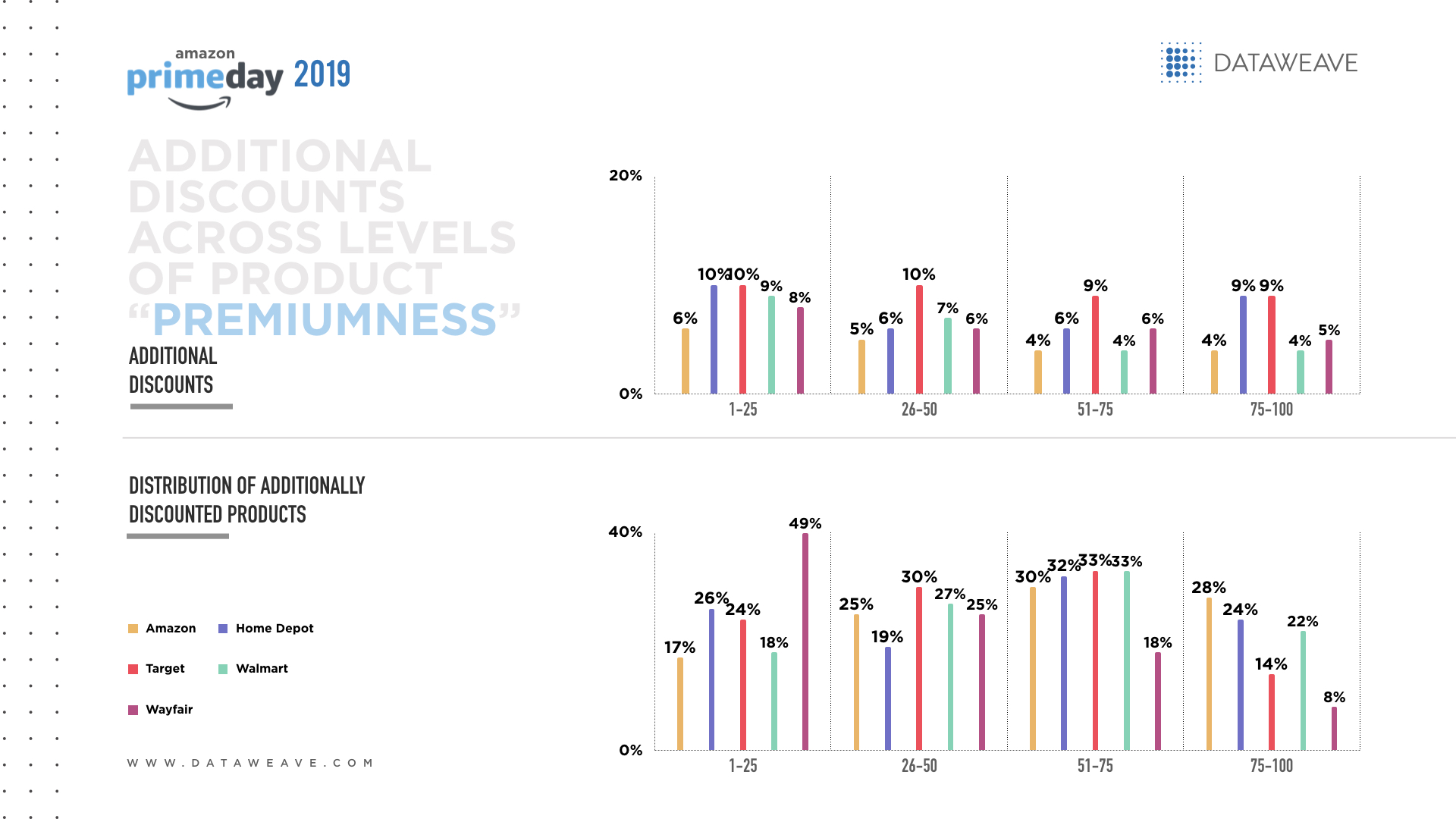

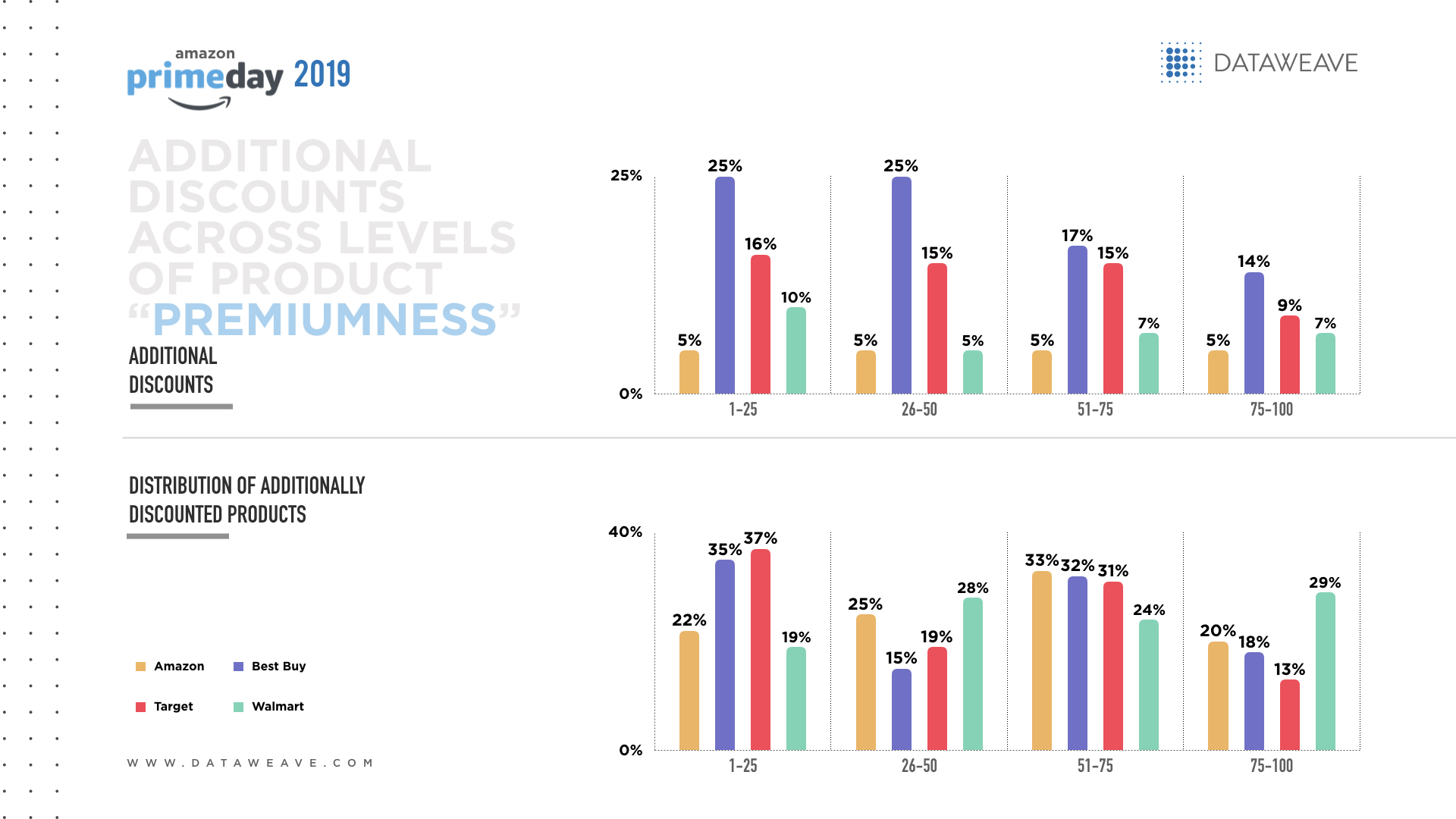

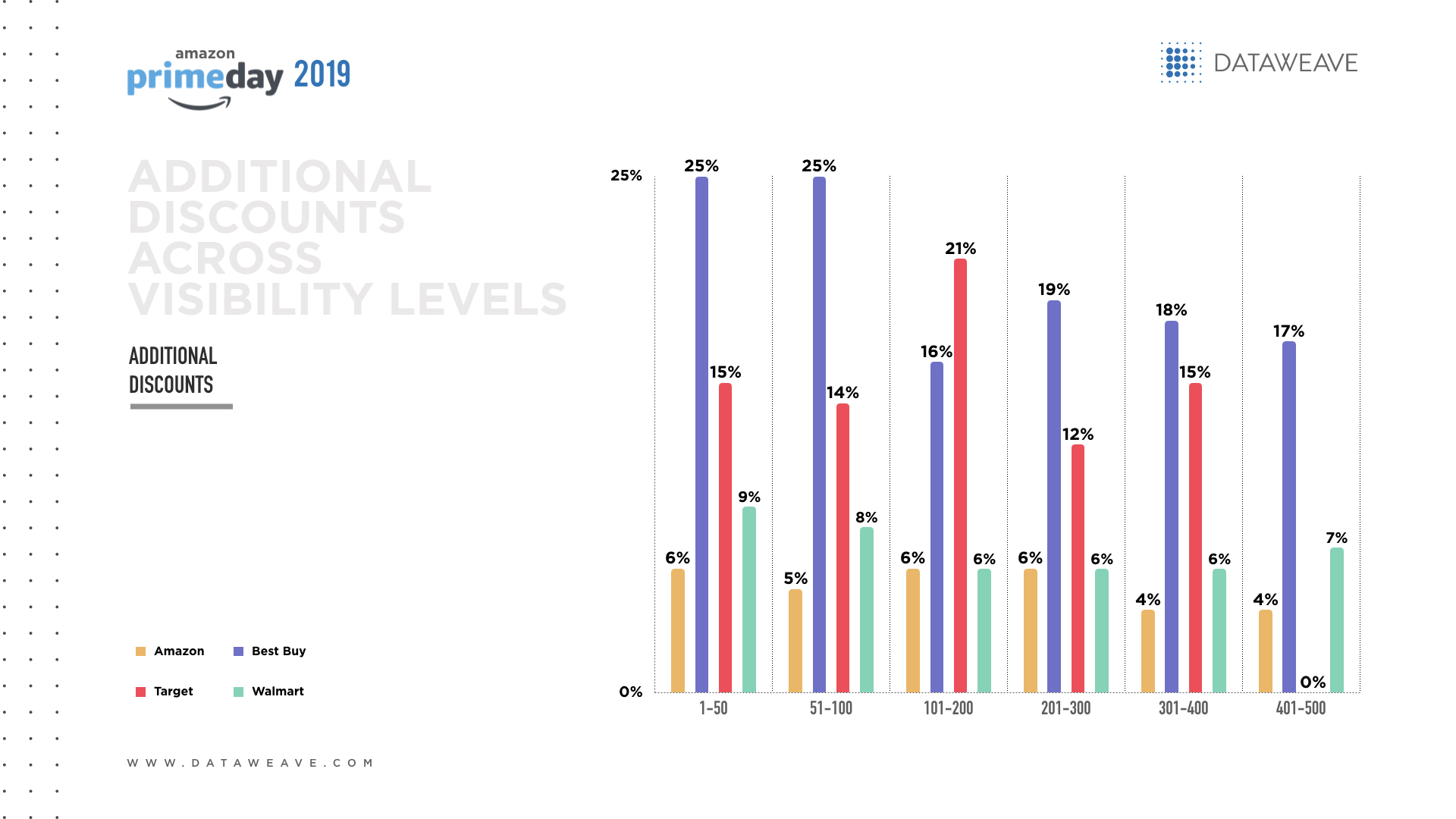

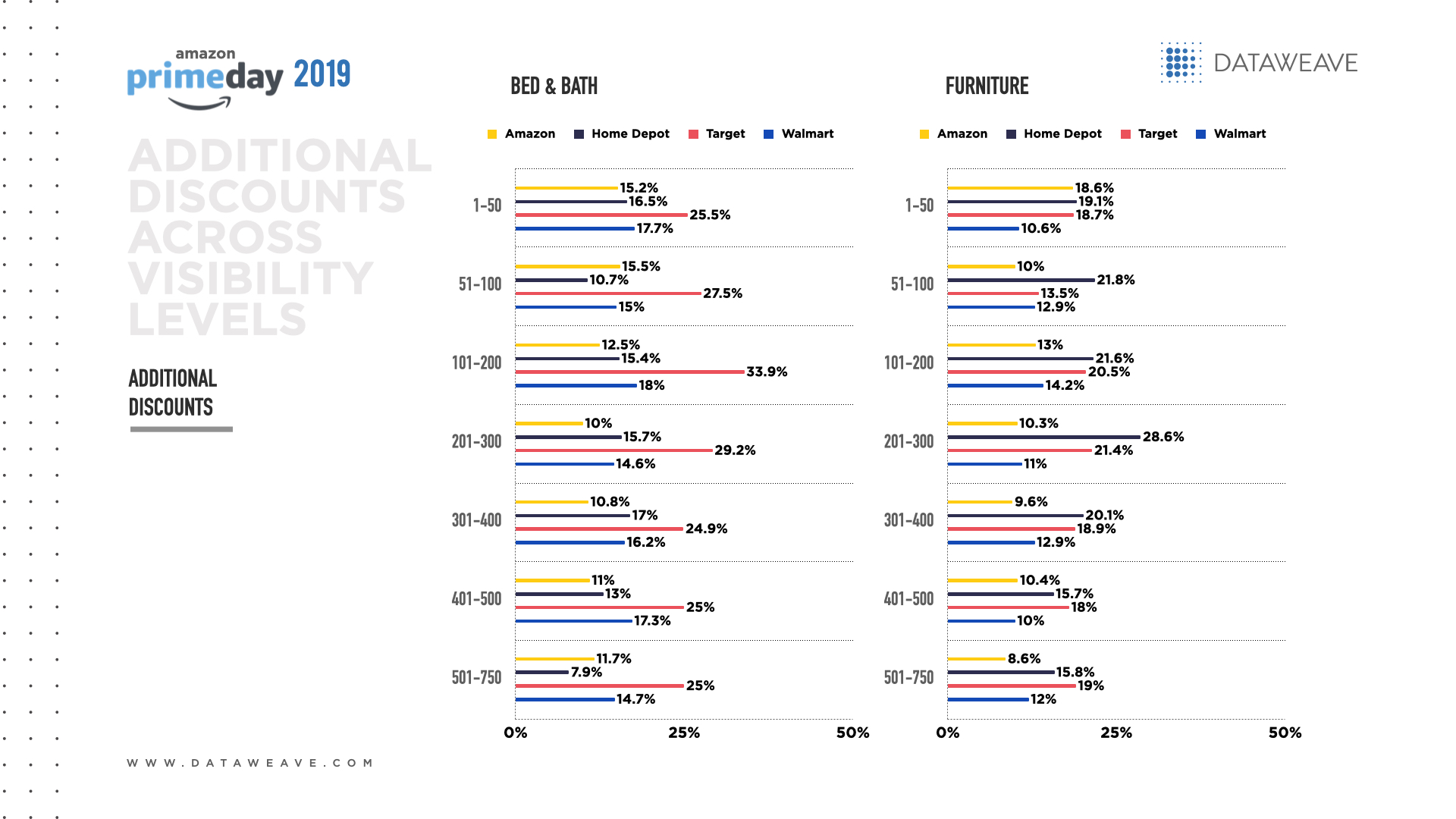

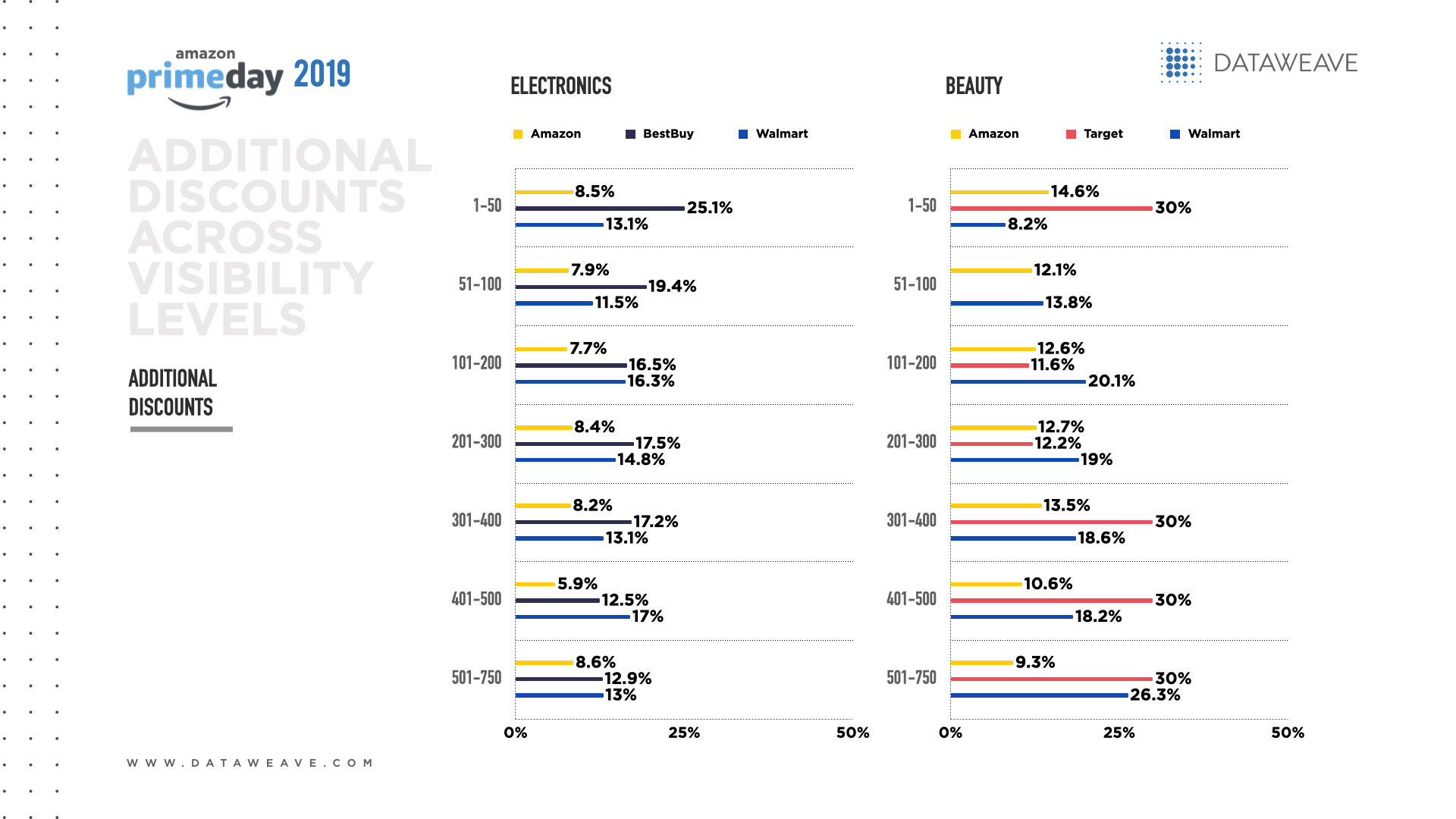

Additional discounts across visibility levels

In Bed & Bath, Target offered the highest overall additional discounts across all levels of visibility (27.3%) and Amazon offered the lowest (12.4%). Amazon focused its additional discounts on the most visible Bed & Bath products to help online shoppers discover those items with ease and make them appealing enough to add to their cart.

Amazon offered the lowest additional discounts in the Furniture category across all levels of product visibility. Yet, among the Furniture category’s most visible items, Amazon offered its highest additional discounts. Home Depot’s additional discounts approach was the most aggressive except among the lowest product visibility levels. Home Depot’s discount strategy shows a desire to compete for Furniture’s most visible items.

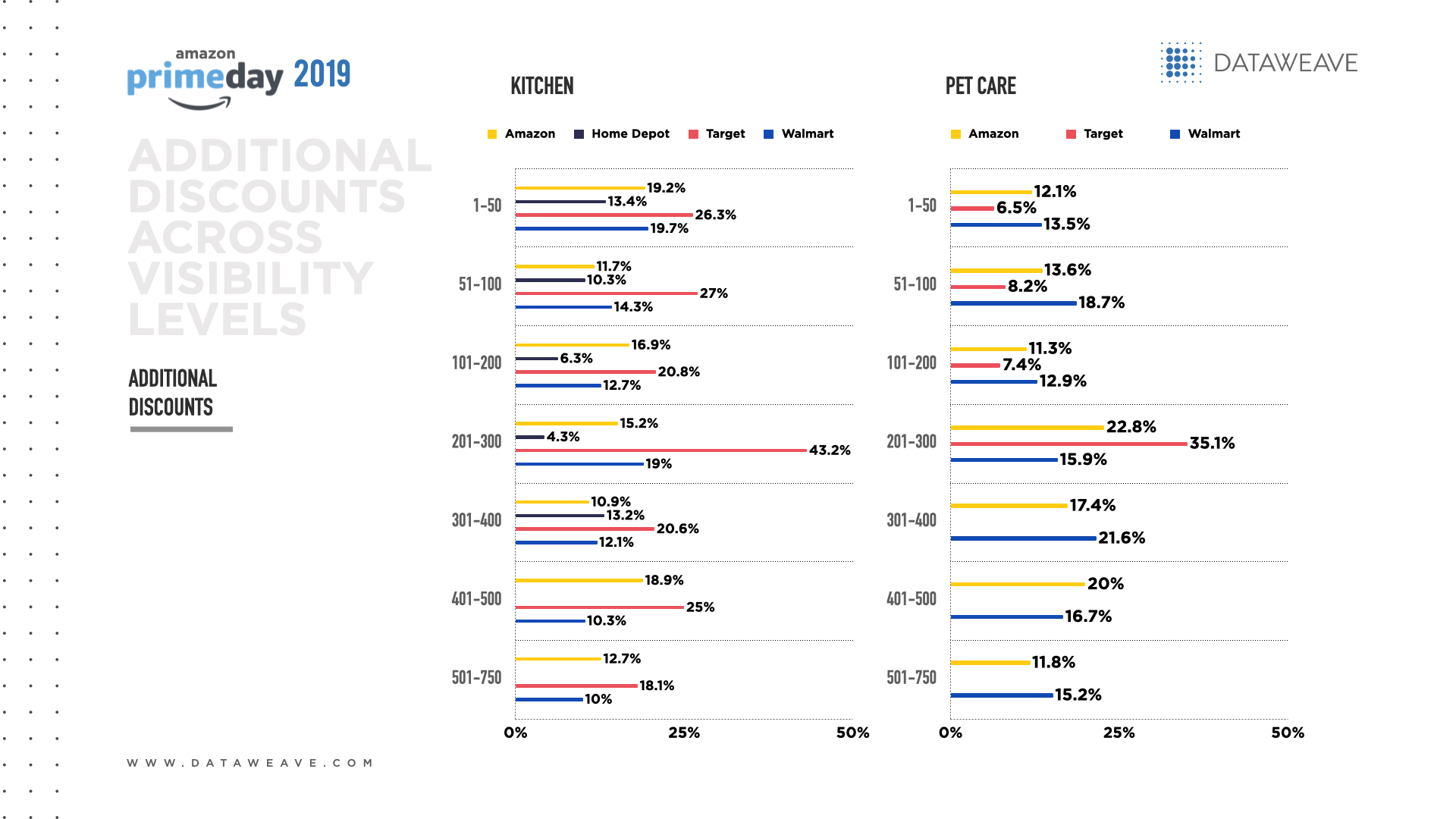

In the Kitchen category, Home Depot consistently offered the lowest additional discounts among products at the higher visibility levels. Conversely, Target was the most aggressive in this category, offering additional discounts of up to 43.2% at moderate levels of visibility and double Home Depot’s discounts (26.3% vs. 13.4%) among the most visible items. Amazon may feel confident that men already choose Amazon for their apparel needs.

In Pet Care, the retailers generally offered the most additional discounts for items in the middle of the visibility spectrum. Walmart offered the most aggressive additional discounts among the most visible Pet Care items, more than double Target’s discounts (13.5% vs. 6.5%).

Overall, Prime Day 2020 offered an ideal time for Amazon to attract homebound consumers to invest in domestic products, yet its rivals offer much higher additional discounts in Bed & Bath, Furniture, Kitchen and Pet Care. How about other categories? Watch this space for more insights!

Our preliminary analysis reveals that Prime Day 2020 motivated Amazon’s rivals to offer deeper discounts in key categories to try to make their merchandise more magnetic and lure consumers away from the e-commerce giant.

This year’s Prime Day is momentous, as the COVID-19 pandemic has encouraged more consumers to make online shopping a more regular habit. It also marks the first time Prime Day took place in the strategically significant final quarter of the year, kicking off the holiday sales season.

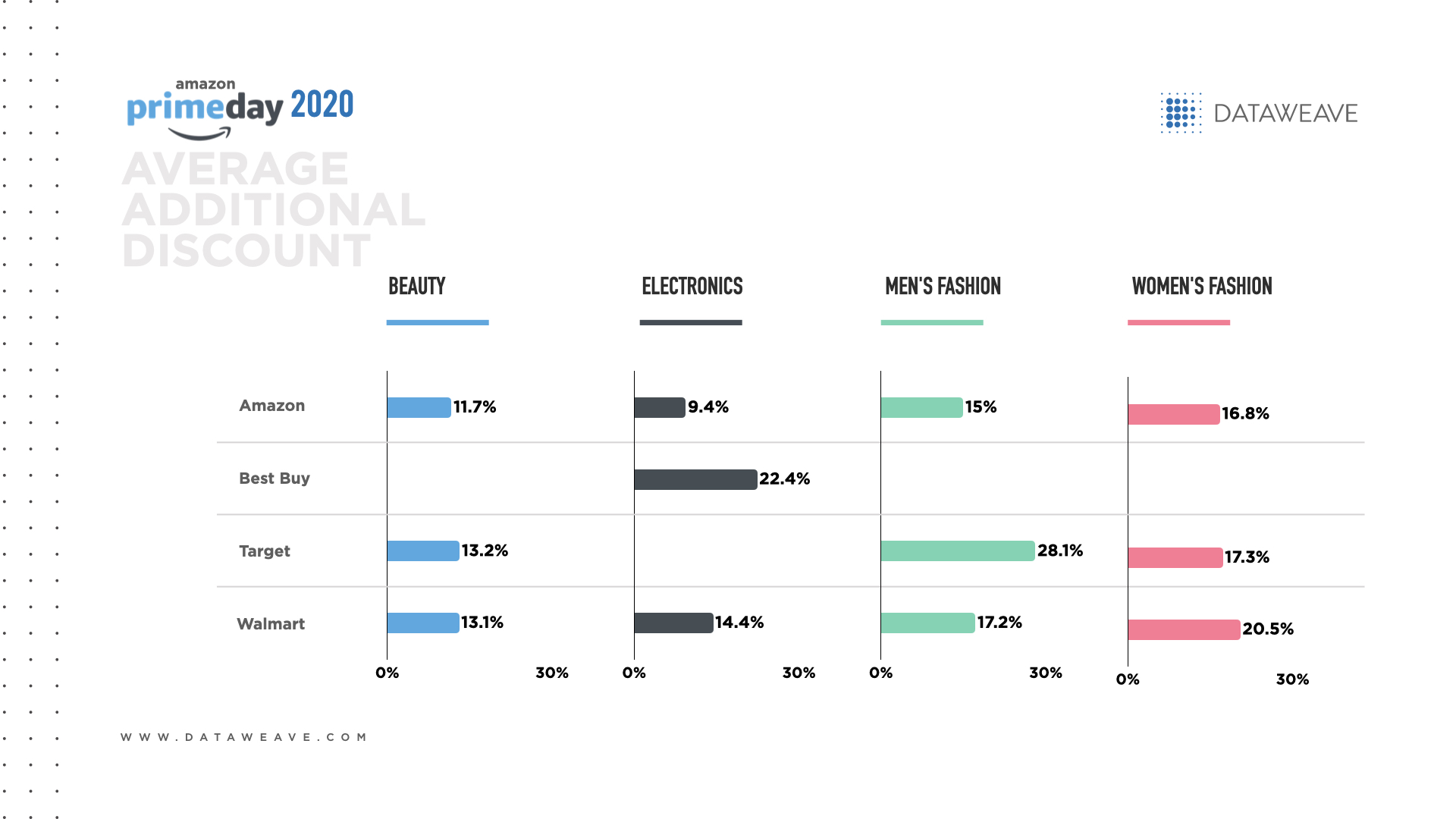

At DataWeave, we wanted to know whether Prime Day 2020 lived up to the hype and how Amazon’s deals compared to other retailers’ discounts. Our analysis examines products across three popular categories: electronics, beauty and fashion.

Our Methodology

We tracked the pricing of several leading retailers (Best Buy, Target, Walmart and Amazon) selling consumer electronics, beauty and fashion to assess their pricing and assortment strategies during this annual sales event.

Our analysis focused on additional discounts offered during the sale to estimate the true value that the sale represented to consumers. Our calculations compared product prices on Prime Day versus the prices prior to the sale. The sample consisted of up to the top 750 ranked products across 21 popular product types in consumer electronics, beauty and fashion.

The Verdict

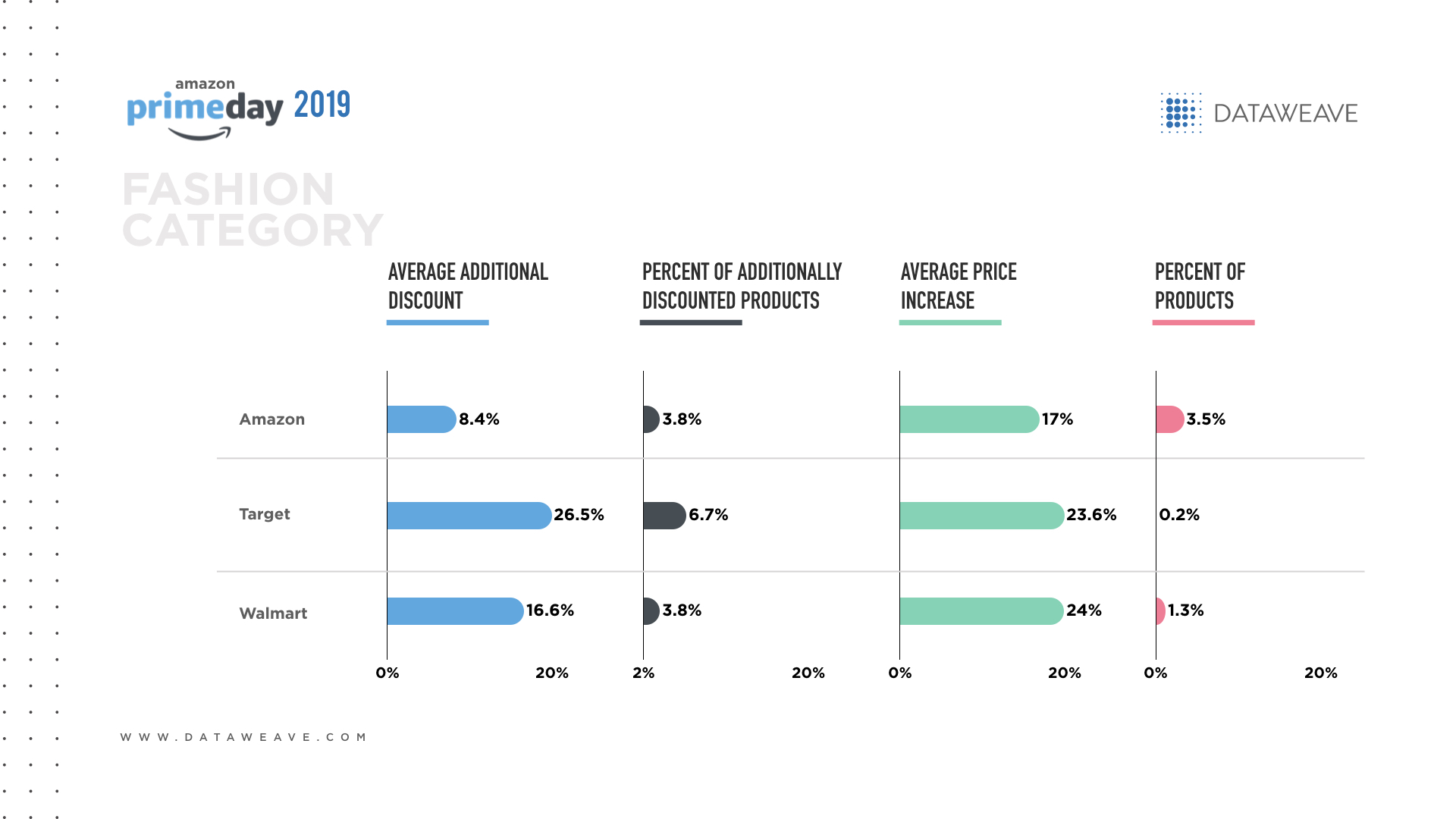

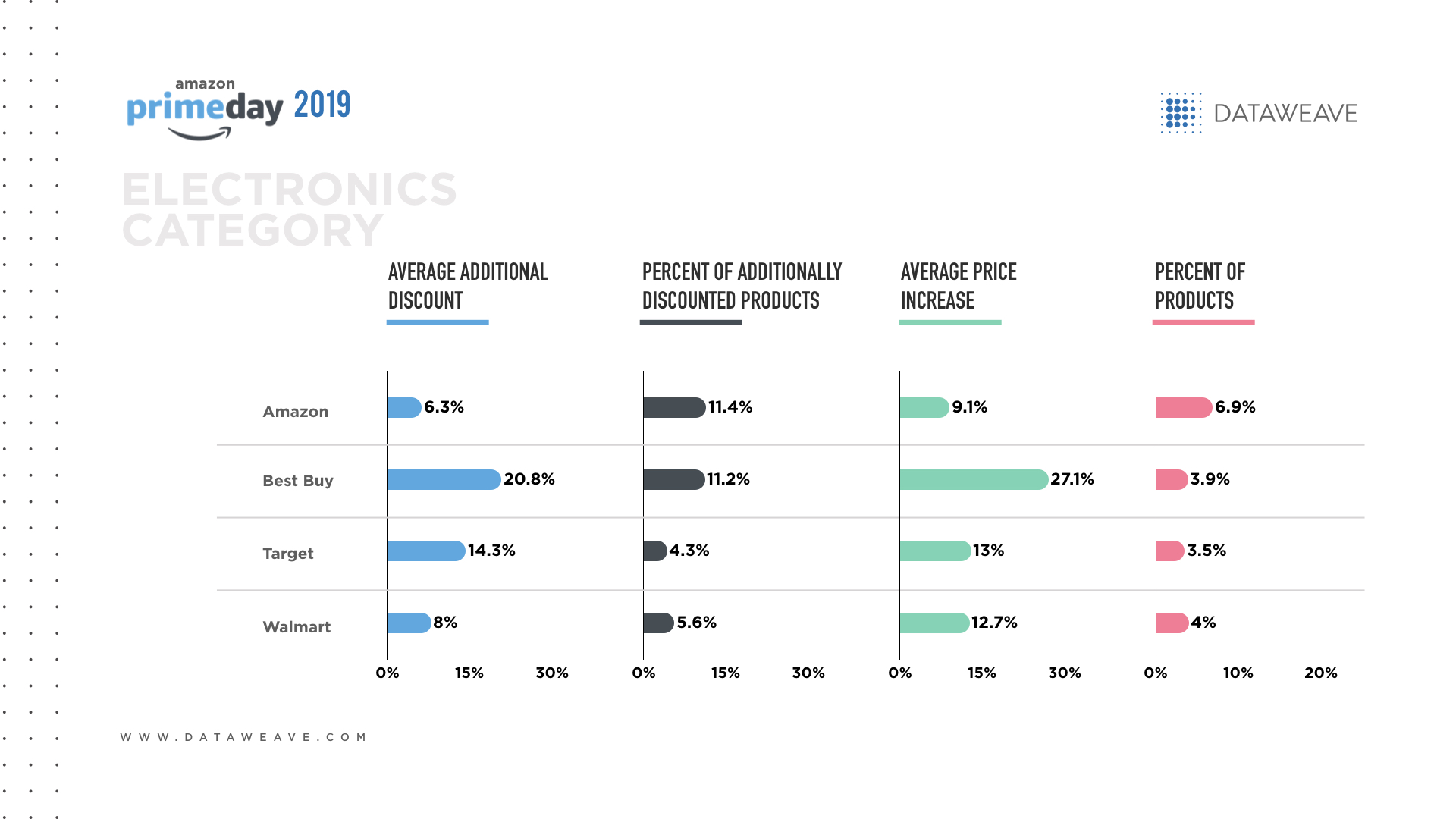

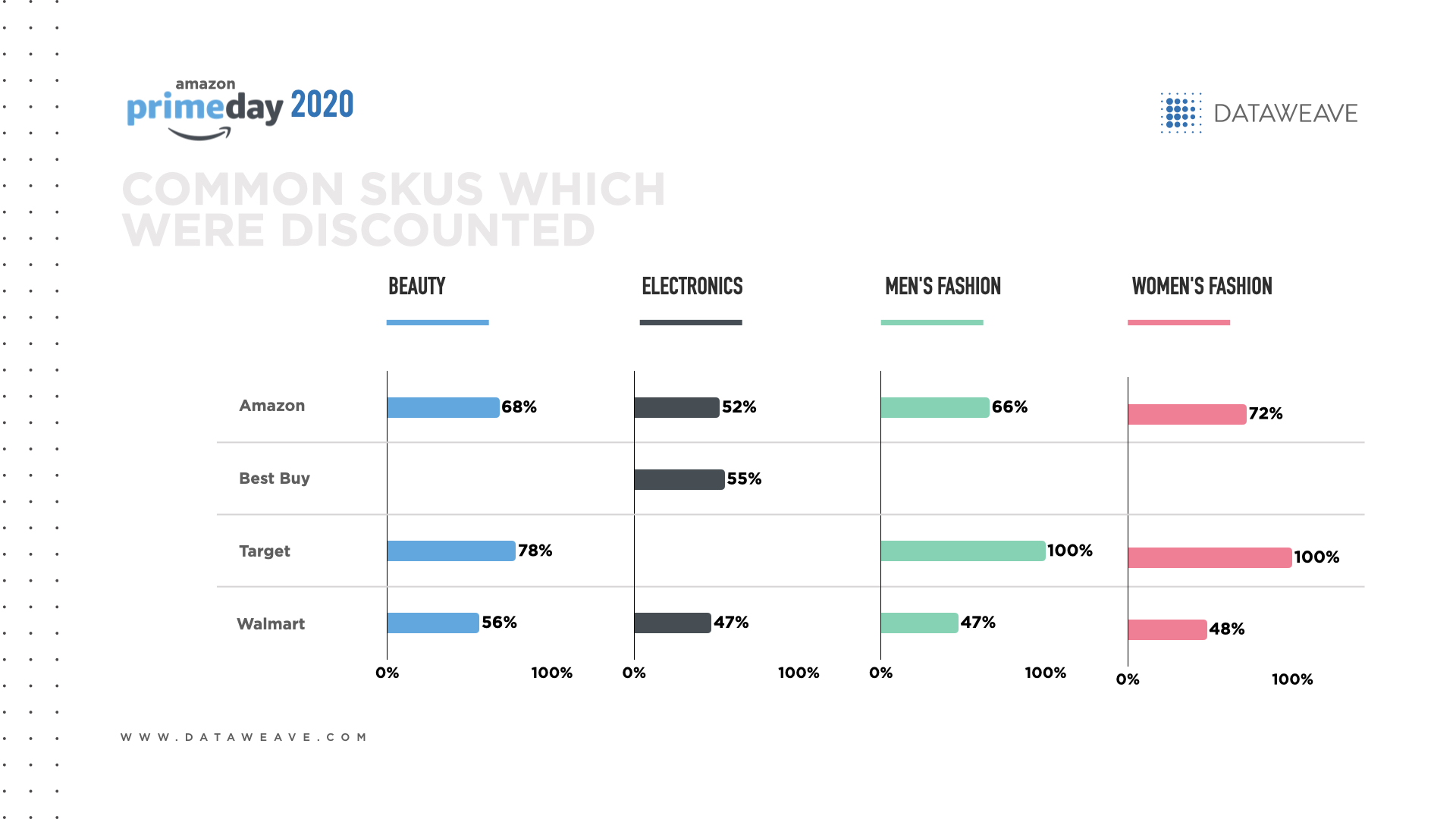

Overall, Amazon reported the lowest price reduction in the Electronics, Beauty and Fashion categories (13.4%), compared to Best Buy (22.5%), Target (21.7%) and Walmart (16.3%). Yet Amazon reported the second-highest percentage of additionally discounted products (12.0% vs. 15.7% for Target).

After Prime Day ended, certain assortments reflected more significant price increases than others. For instance, 97% of Target’s 158 products in Electronics, Beauty and Fashion had a price increase during the post-sale period, compared to 49% of Walmart’s 986 products. This discrepancy makes sense given Walmart’s everyday low price strategy.

These results suggest that although Prime Day generates tremendous media buzz for Amazon, the most generous deals come from its rivals. To stand out and lure shoppers away from Amazon, competitors offered comparatively deeper discounts, especially in categories in which they want to grow their market share. This means online shoppers would be wise to compare prices across retailers’ websites to find the best cross-category deals on Prime Day.

Top product types by additional discount

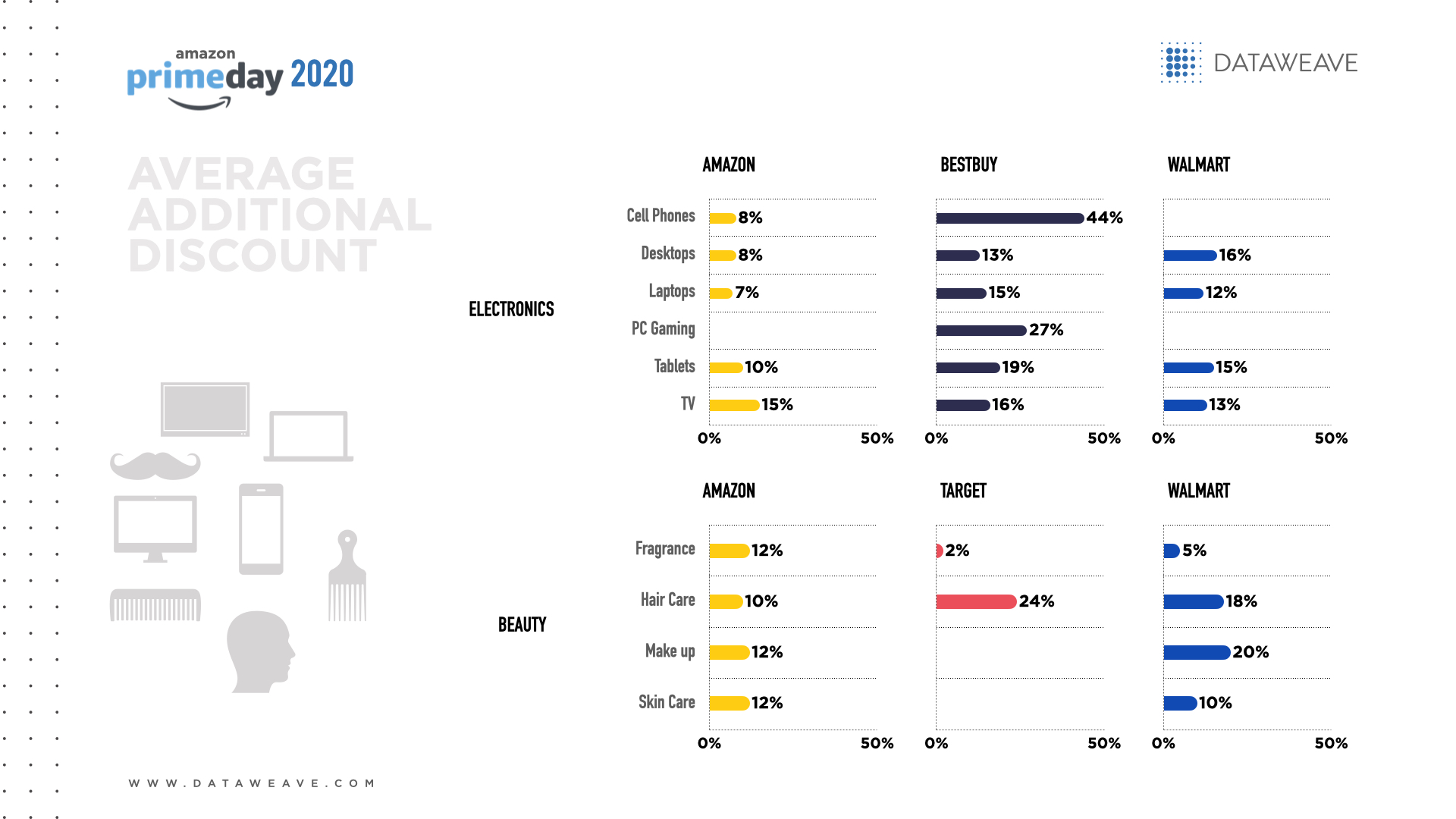

In Electronics, Best Buy offered the biggest average additional discount (22.4%) and Amazon offered the lowest (9.4%). Tablets were a popular product category among Amazon, Best Buy and Walmart, with Best Buy offering the best average additional discount at 19.1%. Other popular product types among rival retailers included TVs, desktops and laptops.

In Beauty, Target (13.2%) and Walmart (13.1%) almost tied for the biggest overall additional discount. Makeup was a popular beauty subcategory, with Walmart offering the highest additional discount at 19.7%. Other popular product types included hair care, skin care and fragrance.

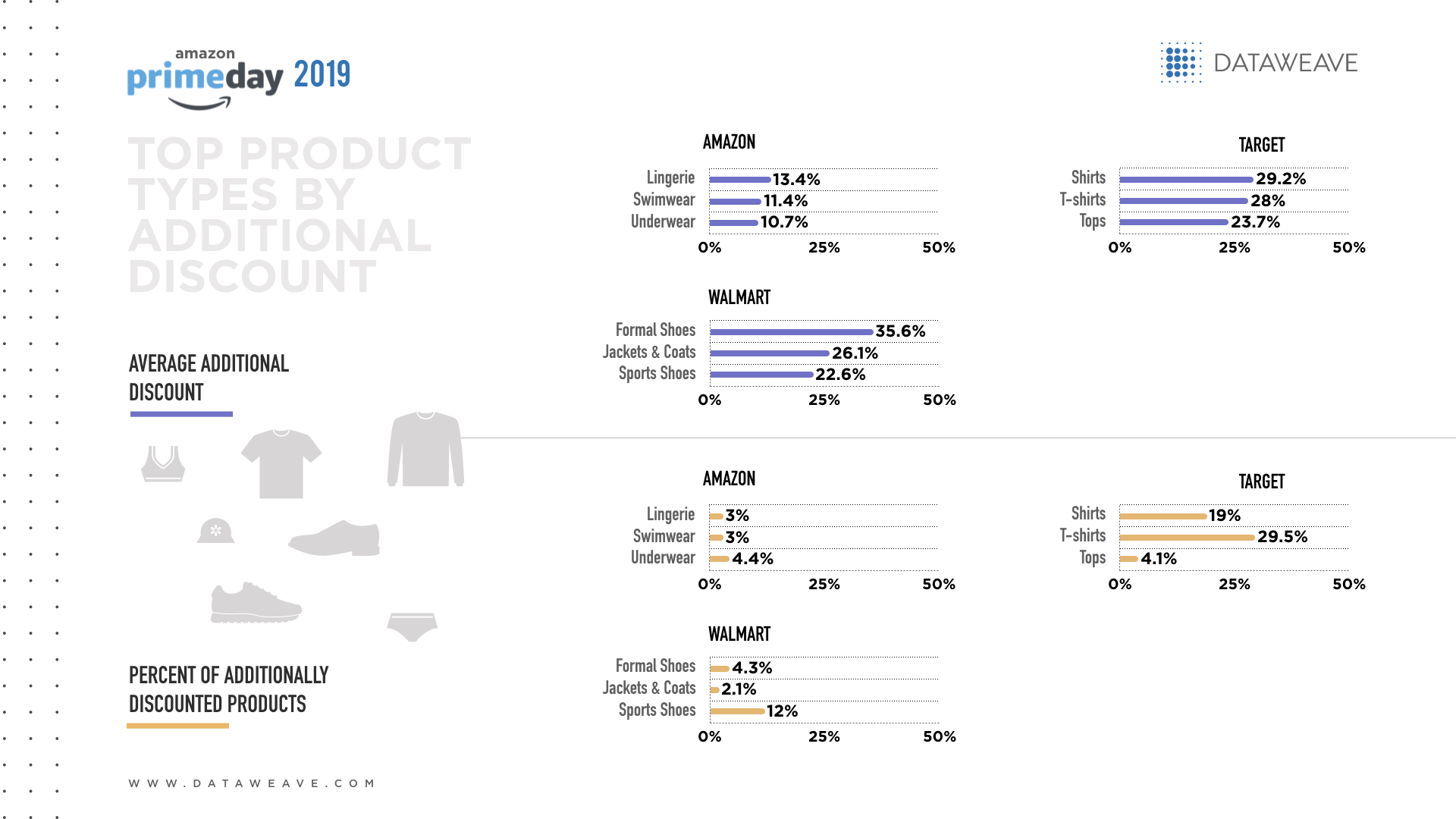

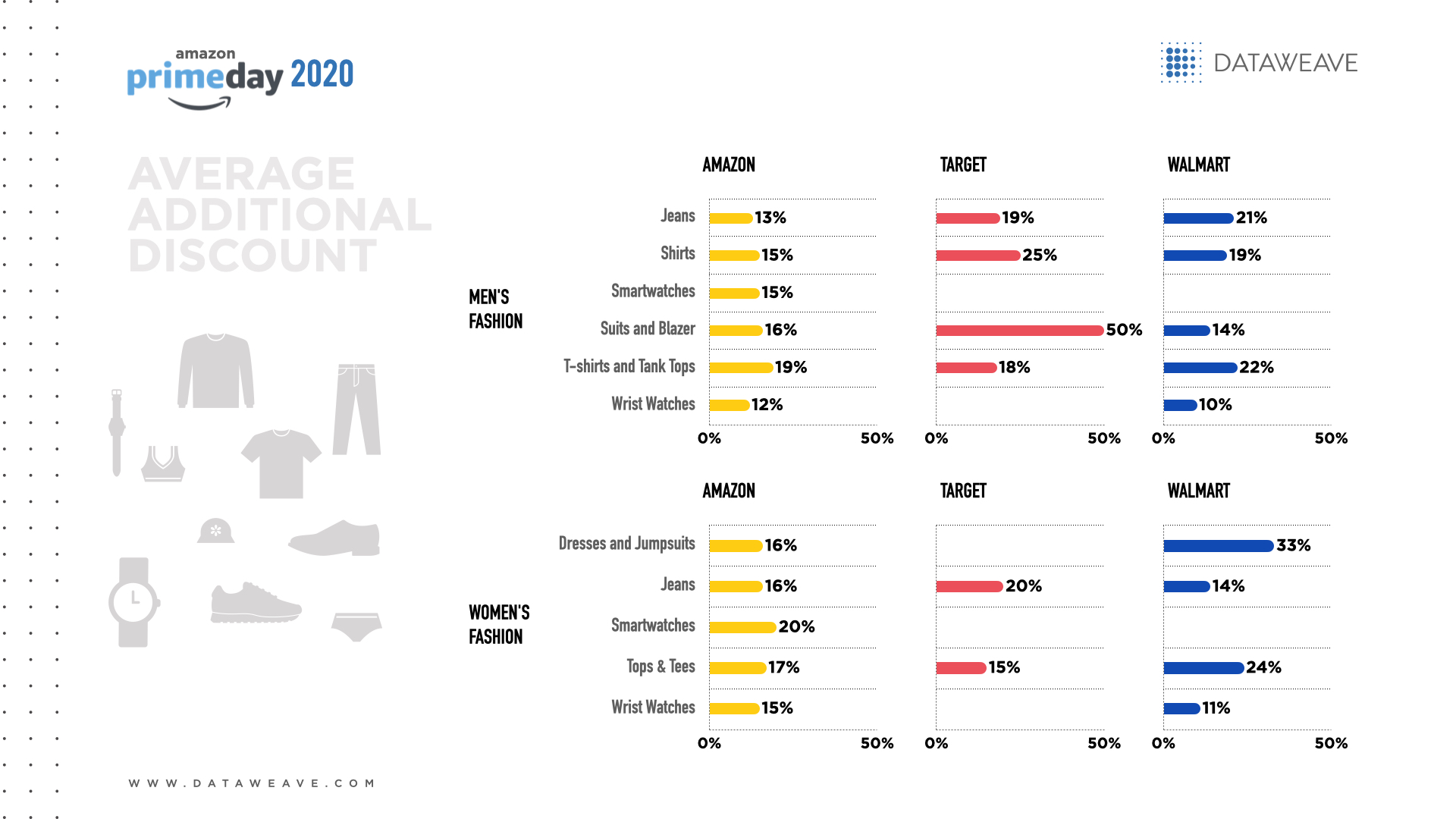

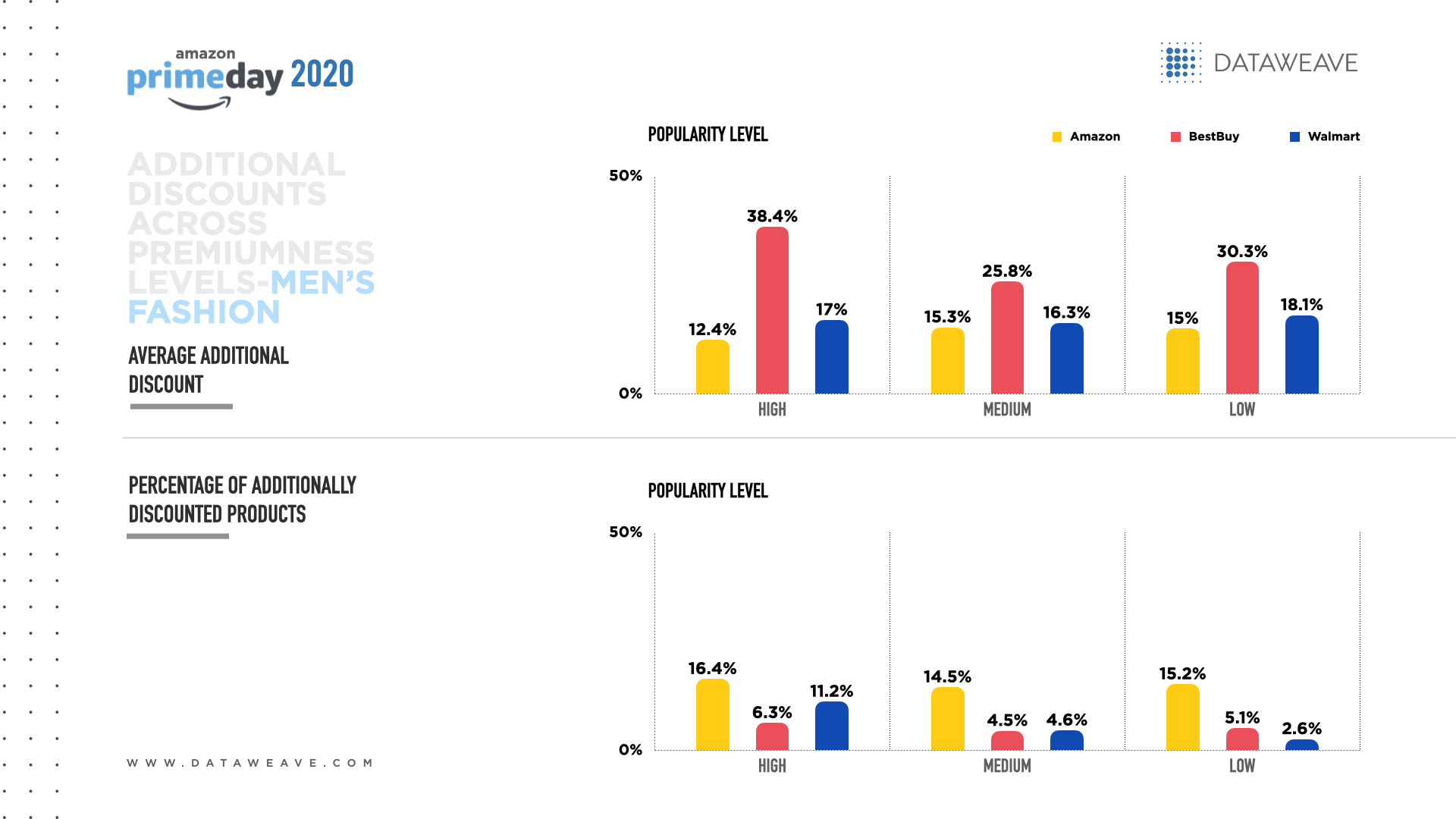

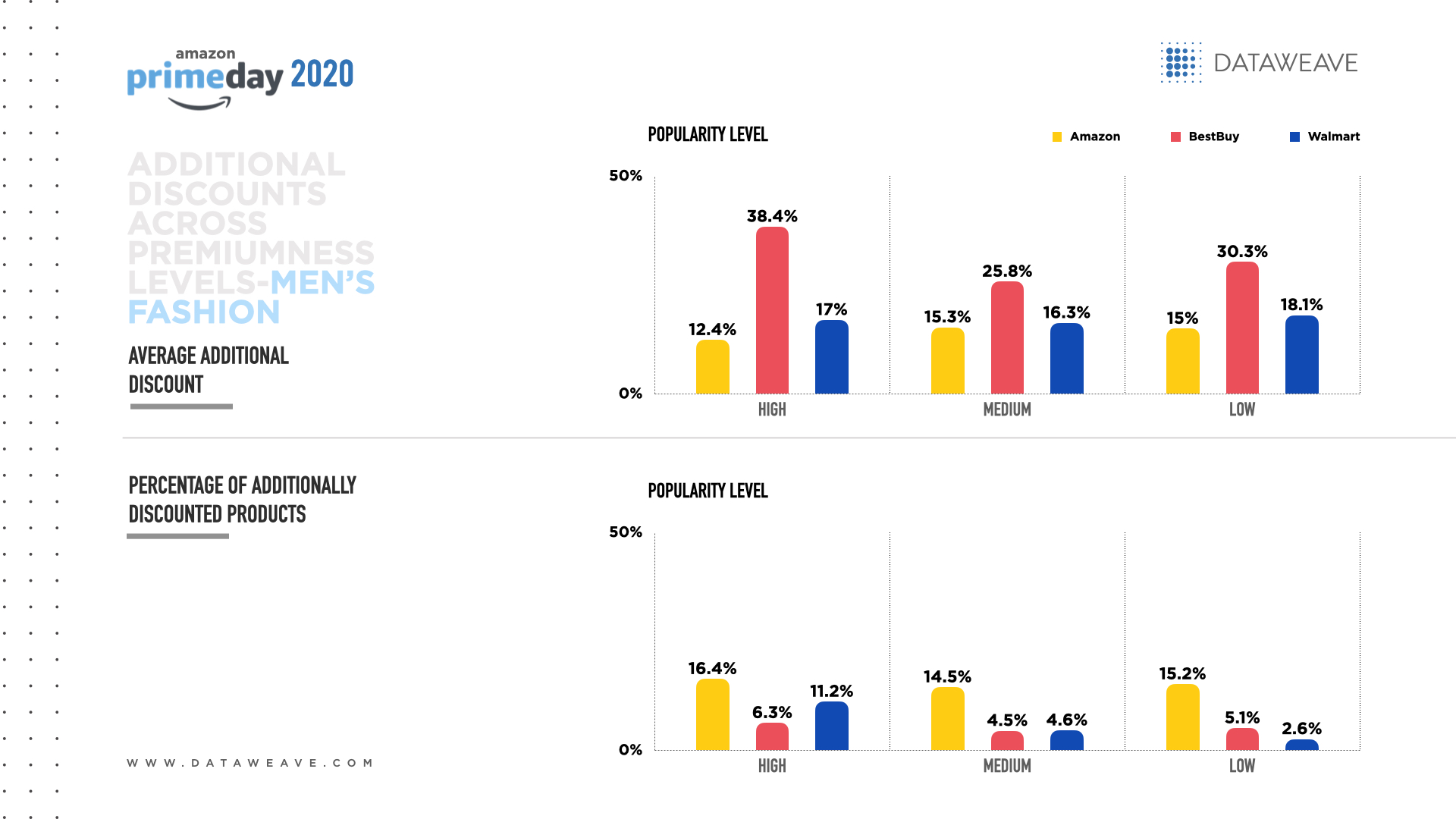

In Men’s Fashion, Target offered the biggest average additional discount of 28.1%. Suits and blazers were a popular fashion subcategory, in which Target offered the highest average additional discount at 50.0%. Other popular product types included T-shirts and tank tops, shirts and jeans.

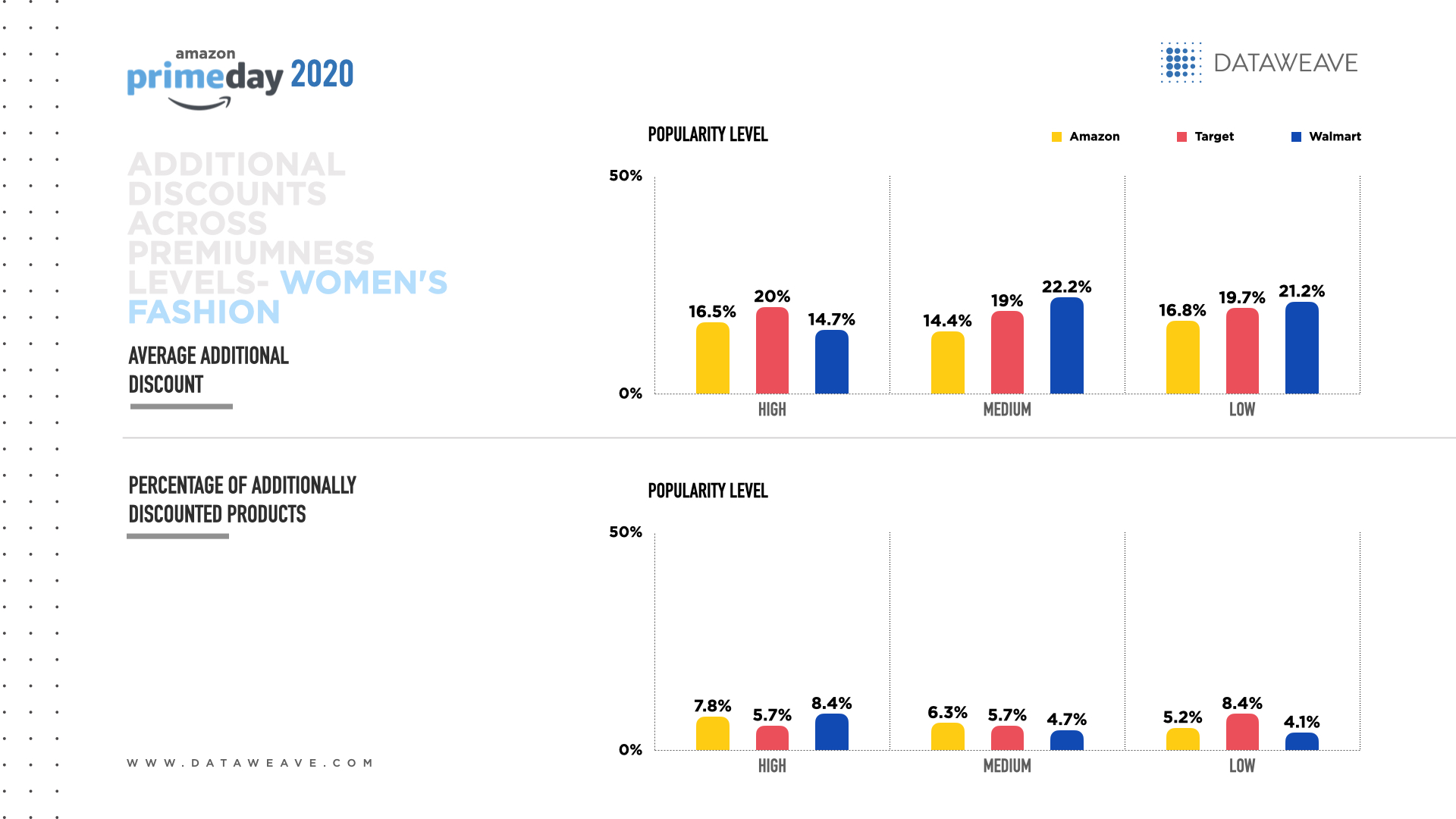

Within the Women’s Fashion category, Walmart offered the biggest average additional discount of 20.5%. Tops and tees were a popular product category across all three fashion rivals, with Walmart offering the best average additional discount at 23.6%. Other popular product types included dresses, jumpsuits and jeans.

Additional discounts across product “premiumness” levels

Premiumness was calculated as the average selling price before the sale event. This was divided into low, medium and high premiumness levels, with high indicating higher selling prices.

In Electronics, Amazon showed a direct relationship between its additional discounts and the level of premiumness; Best Buy and Walmart showed an inverse relationship. Best Buy offered the biggest additional discounts across all levels of premiumness, nearly triple Amazon’s discounts (20.7% vs. 7.0% ) at the low end of the premium spectrum, and more than double Amazon’s discounts (18.5% vs. 7.3%) at the moderate level. Best Buy’s discounting strategy show it’s serious about protecting its competitive position in electronics.

Best Buy and Walmart offered the most additional discounts at the high end of the premiumness spectrum, making both retailers more competitive in the high-ticket electronics category. By contrast, Amazon offered nearly double the additional discounts of its rivals within the low segment, which helps to protect its margins while making products even more affordable and appealing.

In Beauty, Amazon and Walmart offered their biggest additional discounts at the low premium level, possibly to position those products as loss leaders. Meanwhile Target nearly doubled and tripled its rivals’ additional discounts at the high premium level (30.0% vs. 16.0% for Walmart and 11.0% for Amazon) to stand out in this intensely competitive category.

Amazon stood out by discounting the greatest portion of its Beauty offerings at all premiumness levels and Target discounted the least. Amazon and Walmart showed a direct relationship between their distribution of additional discounts and the beauty products’ premiumness level.

Across all levels of premiumness for Men’s Fashion, Target offered the biggest additional discounts, including more than triple Amazon’s discounts at the high end (38.4% vs. 12.4%). Target’s aggressive discounting shows a desire to be more competitive within the most premium segment of Men’s Fashion.

Amazon’s additional discounts accounted for the greatest percentage of its Men’s Fashions across all levels of premiumness, nearly triple Target’s overall average (15.4% vs. 5.3%). This approach shows Amazon’s willingness to give shoppers deals across a broader variety of Men’s Fashion items.

In Women’s Fashion, Target’s and Walmart’s overall additional discounts were comparable, and Amazon’s discounts were consistently the lowest among all levels of premiumness. Walmart offered its most generous discounts at the low and medium level of premiumness, which could reinforce its low-cost leadership image.

While Amazon and Target offered a comparable overall percentage of additional discounts in Women’s Fashions, Amazon applied more discounts to the higher end of the premium spectrum and Target focused on the lower end.

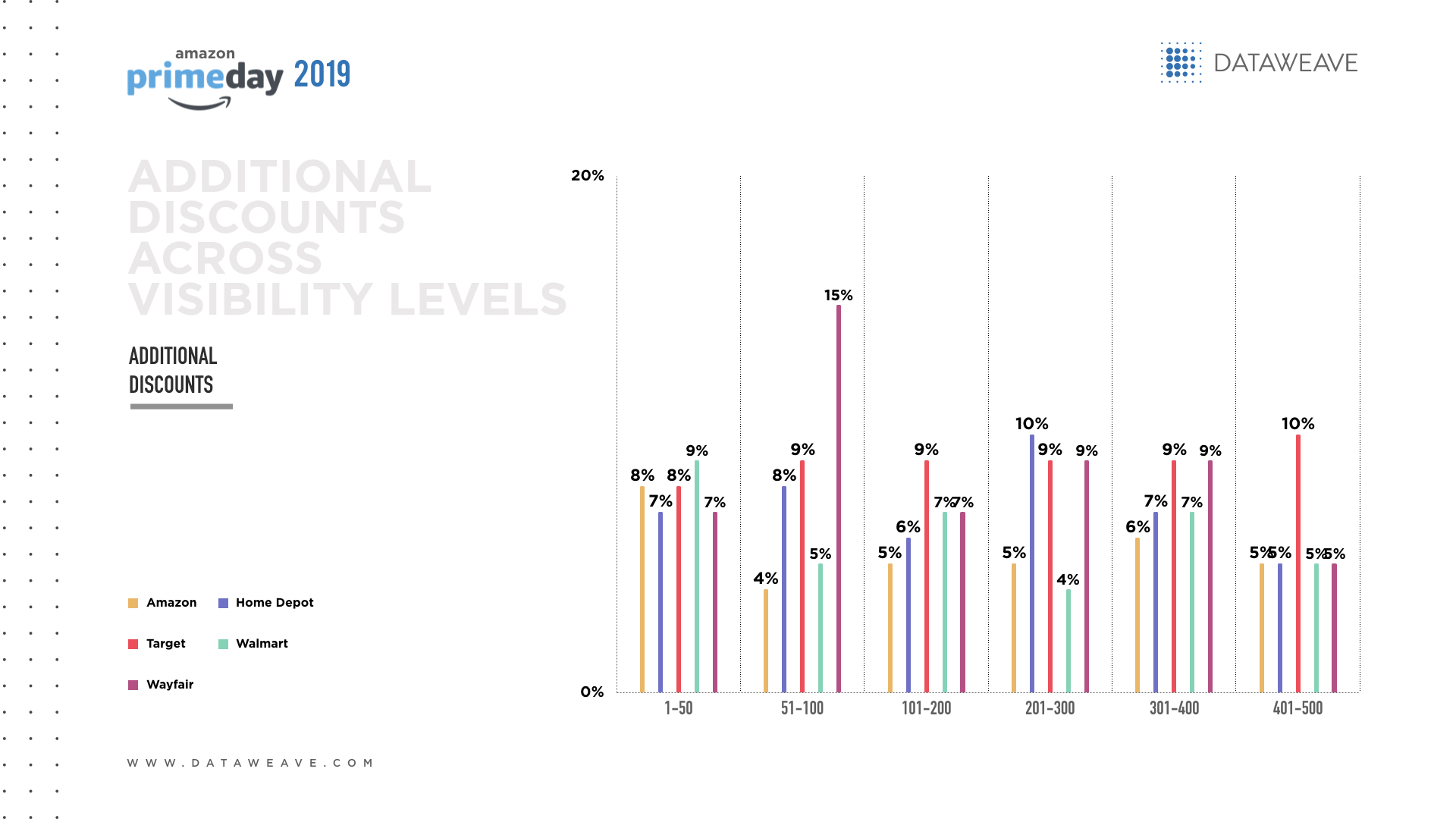

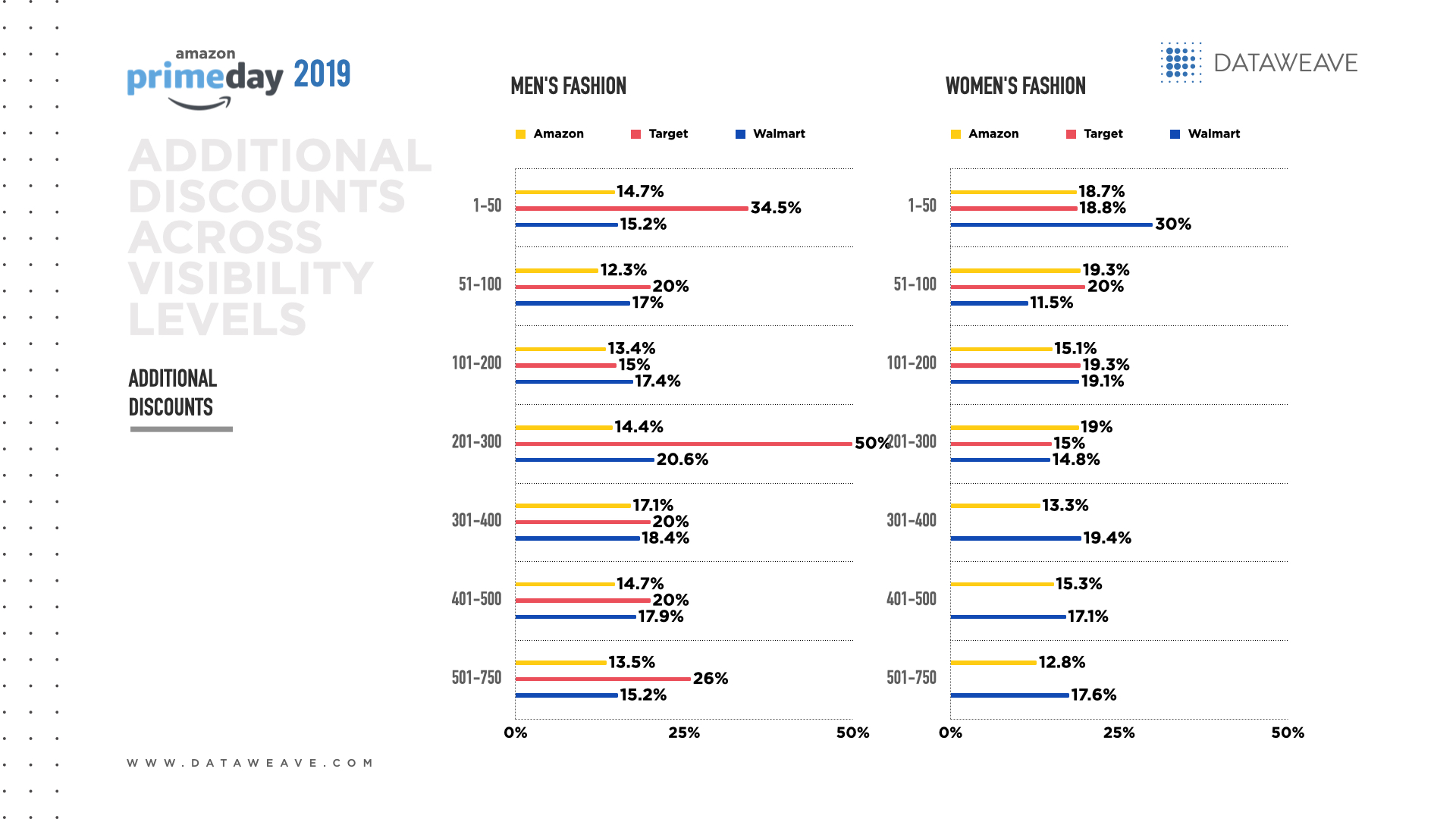

Additional discounts across visibility levels

In Electronics, Amazon offered the lowest average additional discounts across all levels of visibility. Among the most visible electronics, Amazon and Best Buy gave the most visible electronics higher additional discounts to make those items more alluring to help consumers find the items fast and add them to their online baskets.

Among the Beauty category’s most visible items, Amazon and Target offered their highest additional discounts. Yet Target was most aggressive in beauty, offering a 30% additional discount at the most visible end of the spectrum as well as at the least visible. This discount strategy shows Target wants to compete in Beauty, spreading its generosity beyond an exclusive focus on highly visible items.

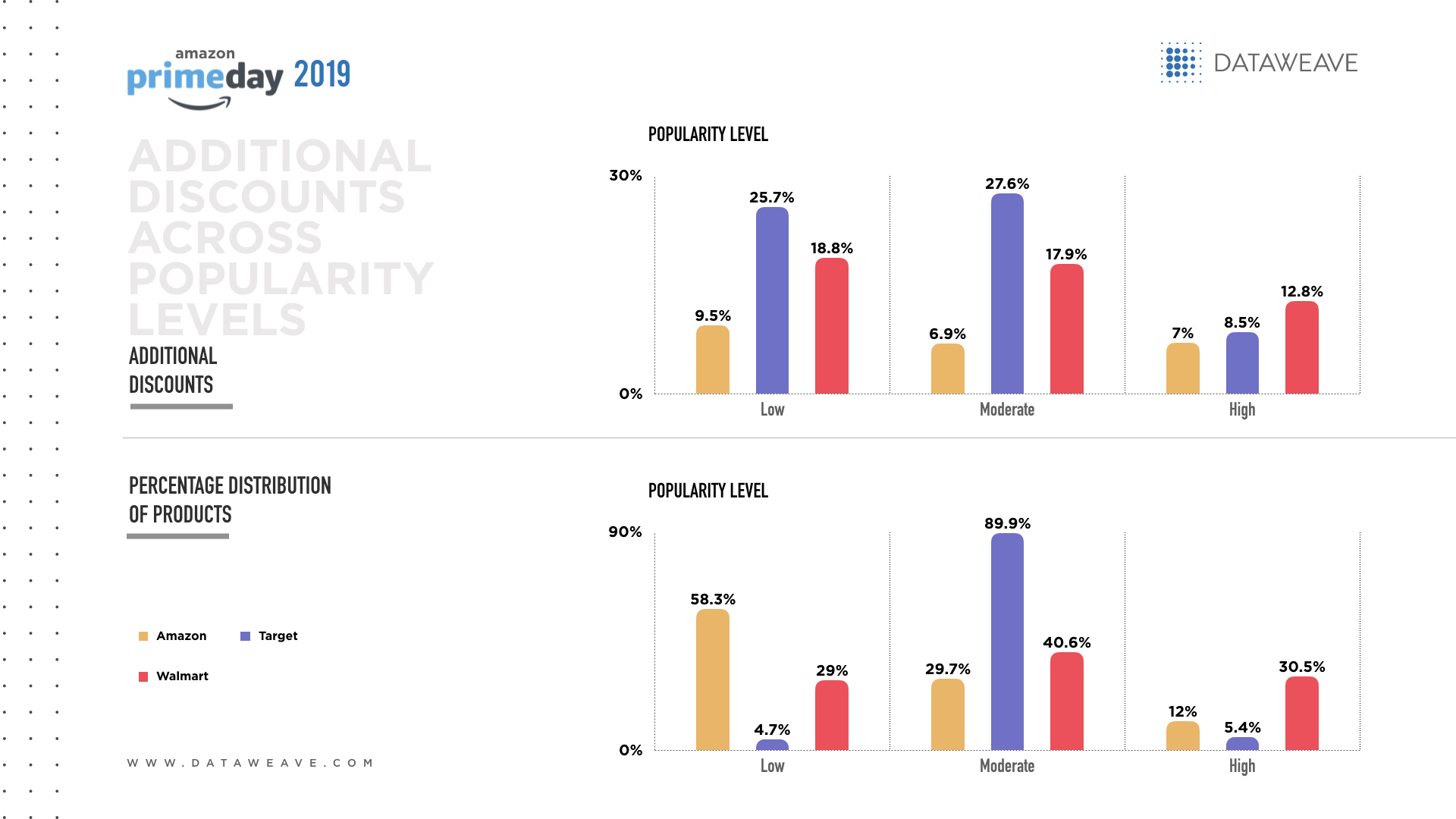

In Men’s Fashion, Amazon consistently offered the lowest additional discounts at all visibility levels. Target was the most aggressive in this category, offering additional discounts of 50% at moderate levels of visibility and 34.5% among the most visible items. Amazon may feel confident that men already choose Amazon for their apparel needs.

In Women’s Fashion, the retailers generally offered the most additional discounts for items at the higher end of the visibility spectrum. Walmart offered the most aggressive additional discounts among the most visible items in Women’s Fashion to try to boost its market share in this category.

Overall, while Prime Day is an effective way for Amazon to boost brand engagement, its rivals overwhelmingly offer higher additional discounts in Electronics, Beauty and Fashion. How about other categories like the booming Home space? Watch this space for more insights!

This year, homebound consumers crave the convenience of food delivery. Growing 20% since 2015, restaurant delivery has sparked intense rivalry to reach consumers’ homes. Although the pandemic led to $165 billion in lost sales industry-wide between March and July, experts predict online food delivery sales will reach $220 billion by 2023, accounting for 40% of total restaurant sales.[1,2]

This massive market opportunity makes food delivery an urgent priority for restaurants to stay competitive and solvent during the pandemic. This year nearly one in six U.S. restaurants have closed either permanently or long-term.[3]

Also, 40% of U.S. operators say they will likely be out of business within six months if economic conditions persist and 60% of Canadian restaurants could close permanently by November.[4,5]

COVID-19 compounds market complexity

Powerful market trends are rattling restaurants. During the pandemic, nearly 70% of operators have added third-party delivery to lift sales.[6]

This year, third-party delivery from food delivery apps like Uber Eats, Grubhub and DoorDash will grow 21% over 2018.[7] The global market for cloud kitchens (also called ghost kitchens or virtual kitchens), commercial kitchens intended for delivery-only orders, will grow from $650 million in 2018 to $2.6 billion by 2026.[8]

To avoid the need to rely on delivery partners, many chains invest in their own last-mile delivery capability to serve their fleet of restaurants. E-grocery sales are poised to surge 40% in 2020 and meal kits have boomeranged back into popularity, nearly doubling 2019 sales.[9, 10]

Consumers demand speed to keep their food fast, fresh and hot. Prompt service matters, as one survey found when consumers face a food delivery issue, 93% want it resolved within 10 minutes.[11]

The recession and job losses mean more consumers now need affordable food options. Meanwhile, restaurants are investing more in technology to modernize operations for efficient omnichannel service.

How restaurants are adapting to 2020’s disruption

Restaurant prices have risen during the pandemic to cover operating costs. Third-party delivery fees have led 41% of consumers to prefer to order food by contacting the restaurant directly (vs. 16% for third-party delivery).[12] To optimize pricing competitiveness, more restaurants now compare their delivery fees and offerings with rivals’ to spot and correct gaps, and keep their prices affordable.

To streamline operational processes and costs during the pandemic, 28% of restaurants shrank their menus.[13]

For clarity on which items to keep, operators now use data insights on restaurant listings and menu items down to the ZIP code level. This information also helps them decide whether to adapt to consumers’ diverse tastes, including vegan, gluten-free and organic, for competitive local assortments.

Outperform rivals: Restaurant operators seek proof of their brand visibility on food delivery apps’ homepages.

Restaurants have discovered consumers welcome reasons to celebrate at home this year. One chain’s weekly virtual happy hours on Facebook Live drew 80,000 participants and a $40,000 sales increase from delivery and takeout orders.[14]

More restaurants now compare their promotional strategies with rivals’ to evaluate marketing performance, including homepage discoverability and visibility ranking, to ensure consumers find their brand online with ease.