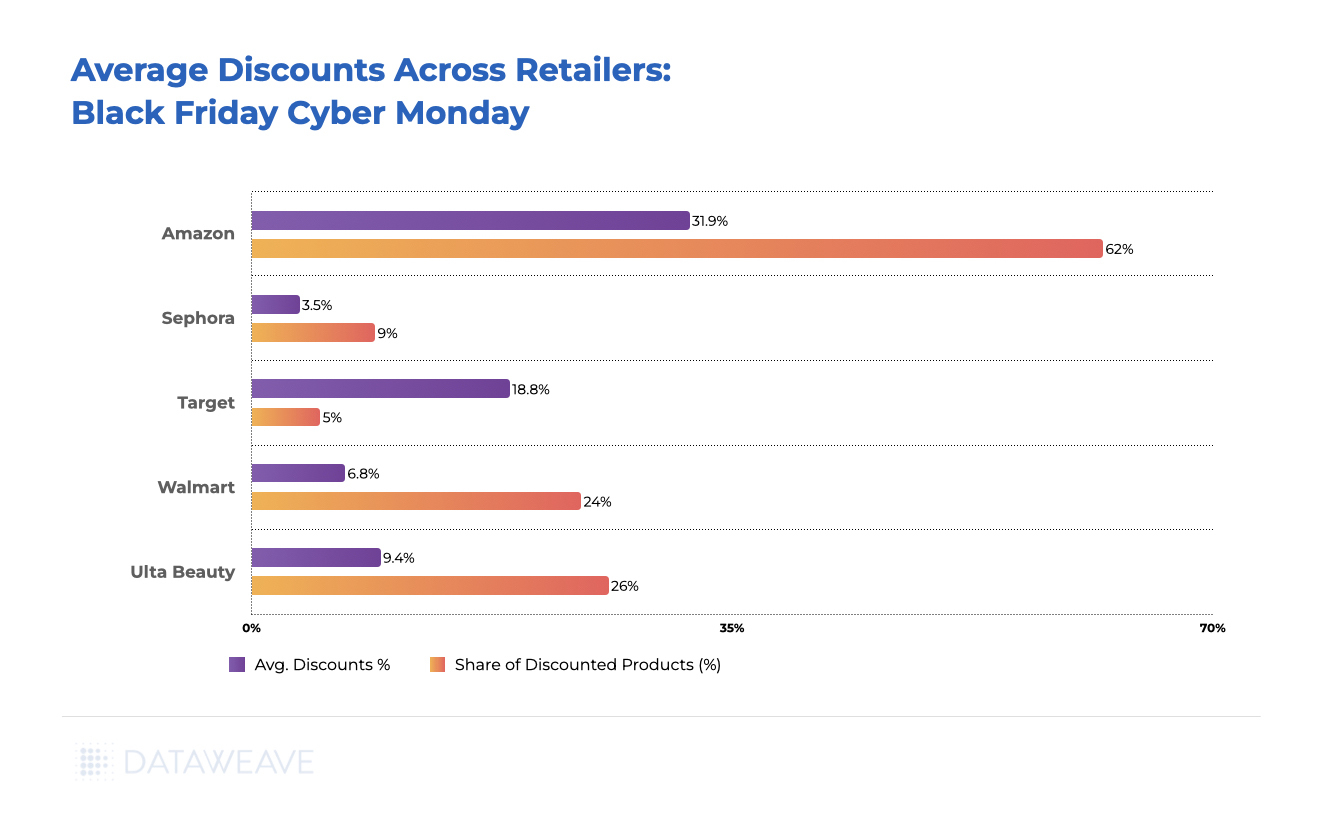

Black Friday has evolved from a purely Western retail phenomenon into a global shopping event. India is no exception. While the country celebrates its own mega sale events like the Great Indian Festival and Big Billion Days, Black Friday has carved out its own space in the Indian retail calendar. E-commerce in India is expected to reach $325 billion by 2030, with festive shopping seasons driving significant portions of that growth.

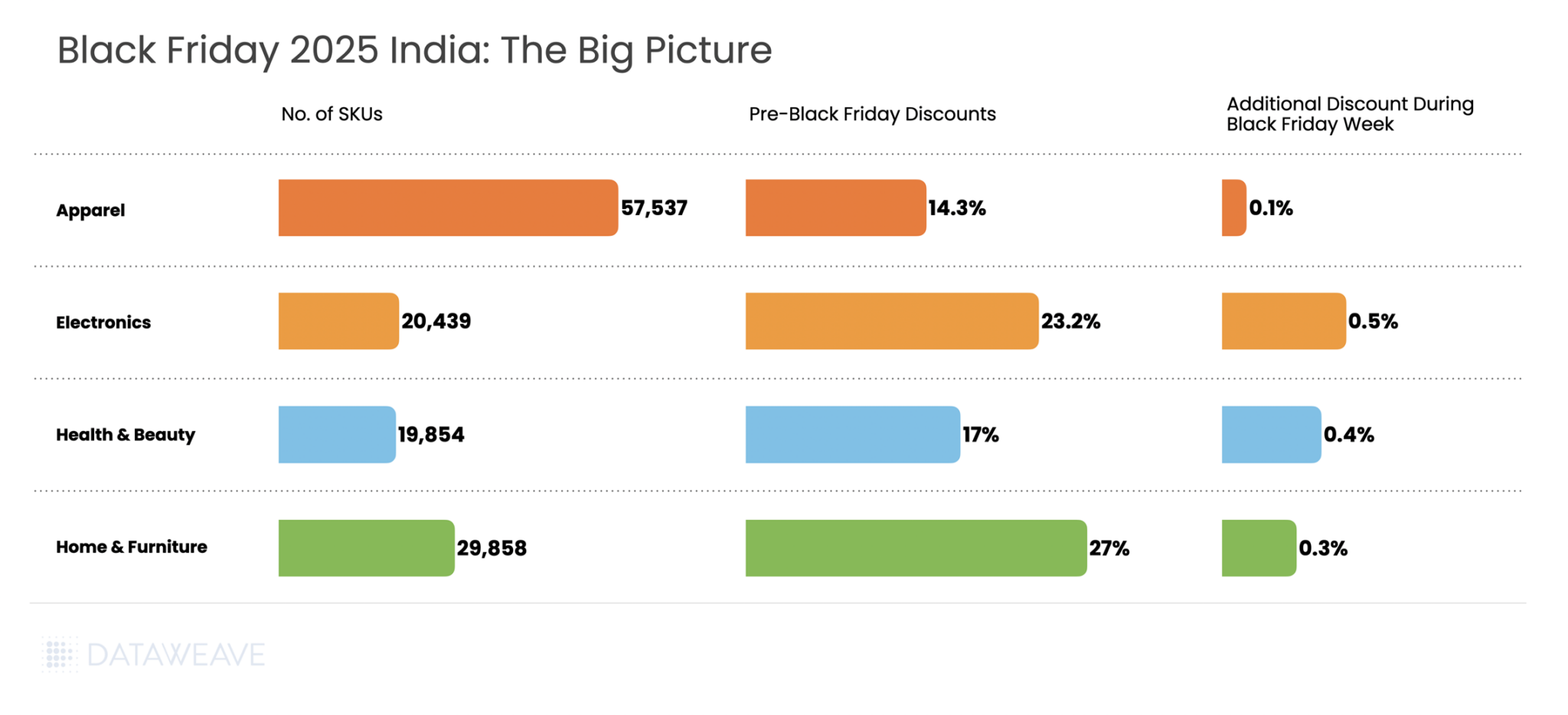

So how did Indian retailers and brands navigate Black Friday 2025? At DataWeave, we analyzed pricing trends across four major categories: Consumer Electronics, Home & Furniture, Health & Beauty, and Apparel. Our AI-powered retail intelligence platform tracked nearly 128,000 SKUs across leading platforms including Amazon India, Flipkart, Myntra, and others, revealing how the Indian market approached discounting and brand visibility during this high-stakes shopping period.

Our Methodology

DataWeave monitored average discount percentages across major Indian e-commerce platforms during two distinct periods:

Pre-Black Friday: Up to November 23, 2025 – capturing early promotional activity and baseline pricing

Black Friday Week: November 24 – December 1,2025 – spanning Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

We analyzed top-ranked products across subcategories on major retail sites, alongside Share of Search data, a metric that measures brand visibility by tracking which brand names appear in the top 20 search results for high-intent keywords.

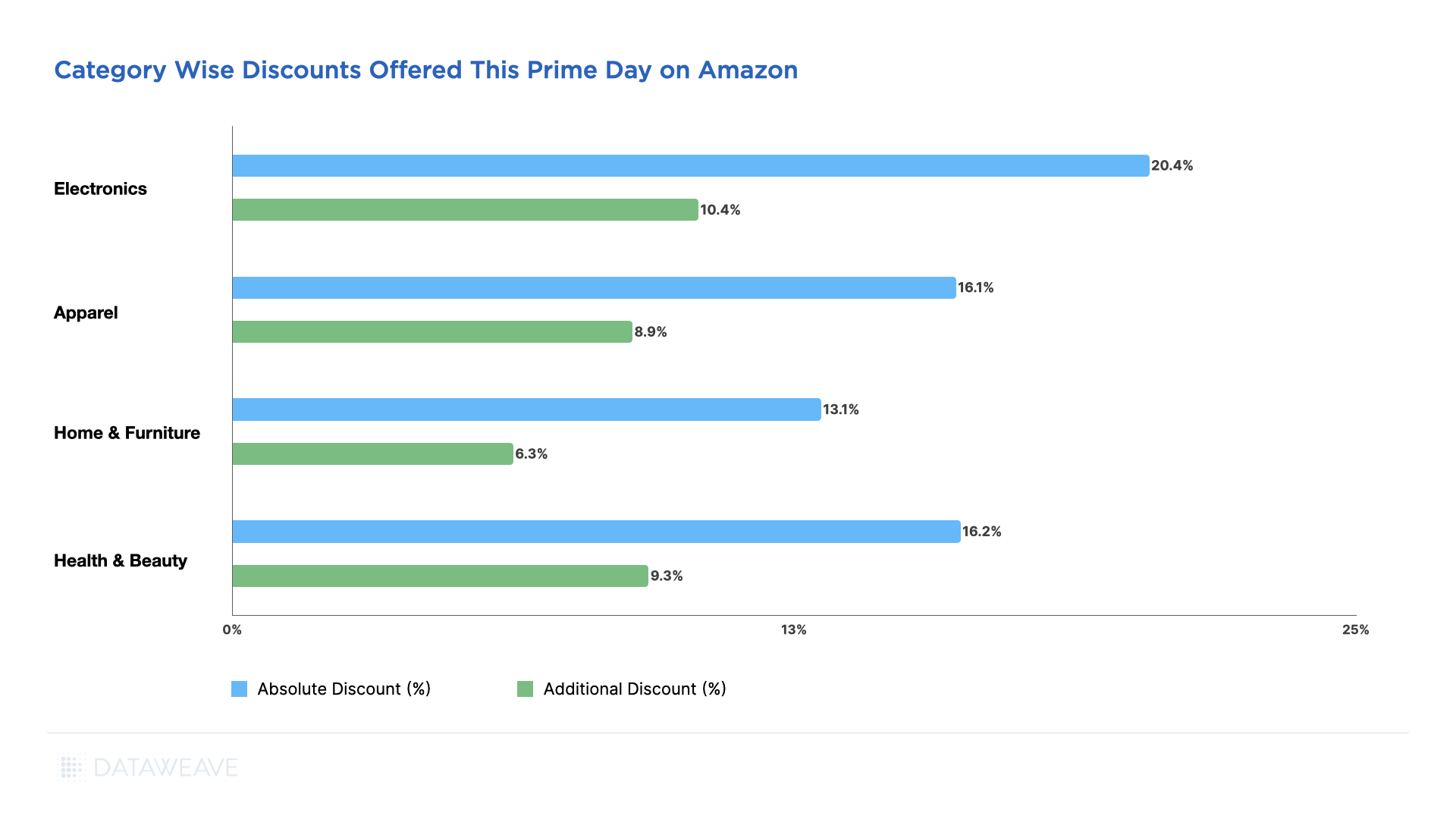

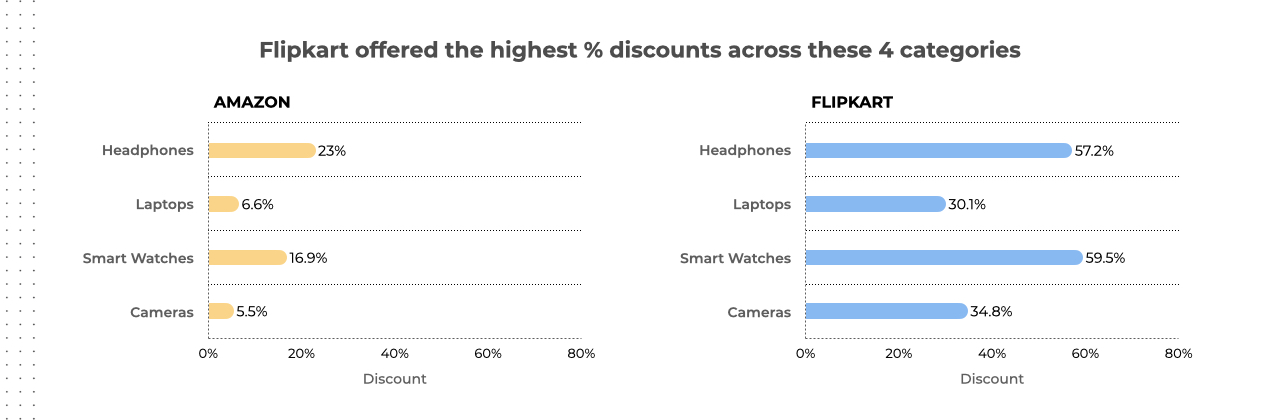

Here’s a quick look at the overall discounts this Black Friday in India:

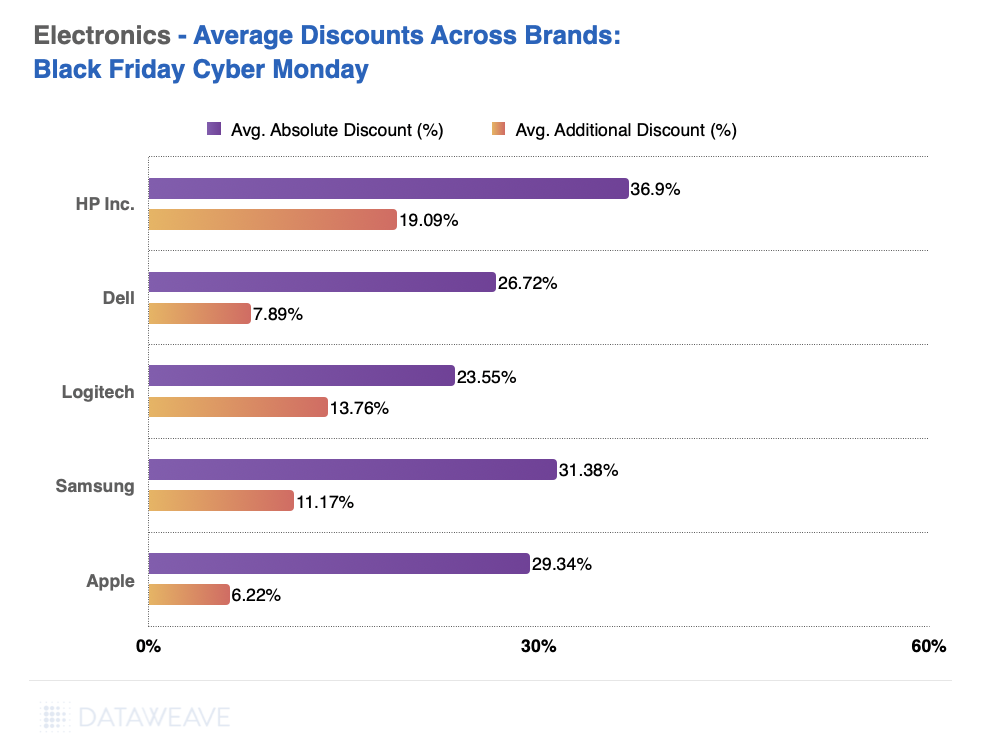

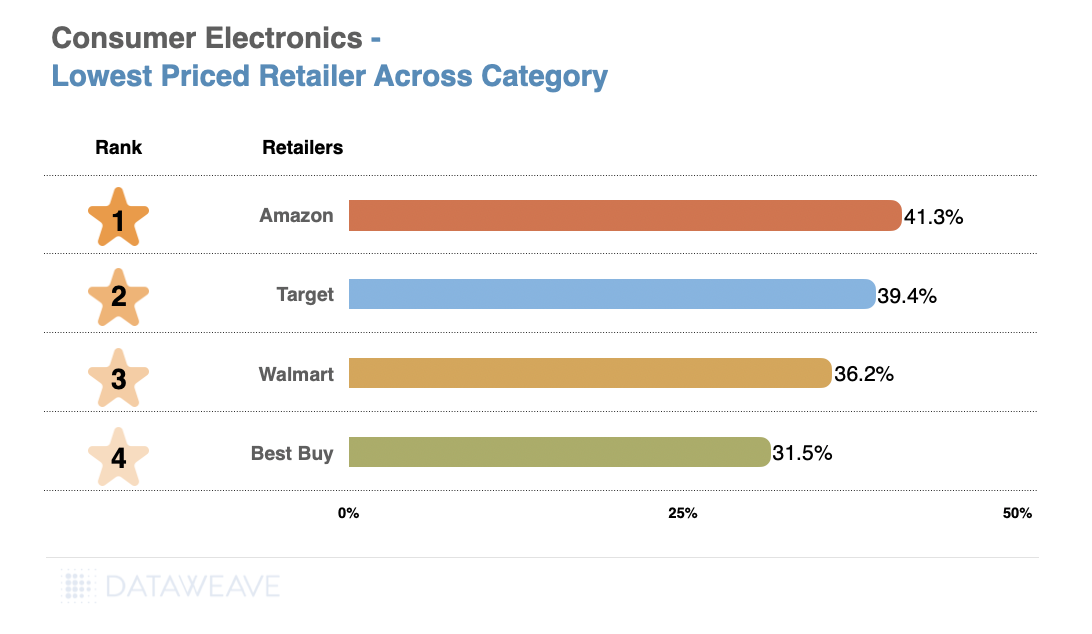

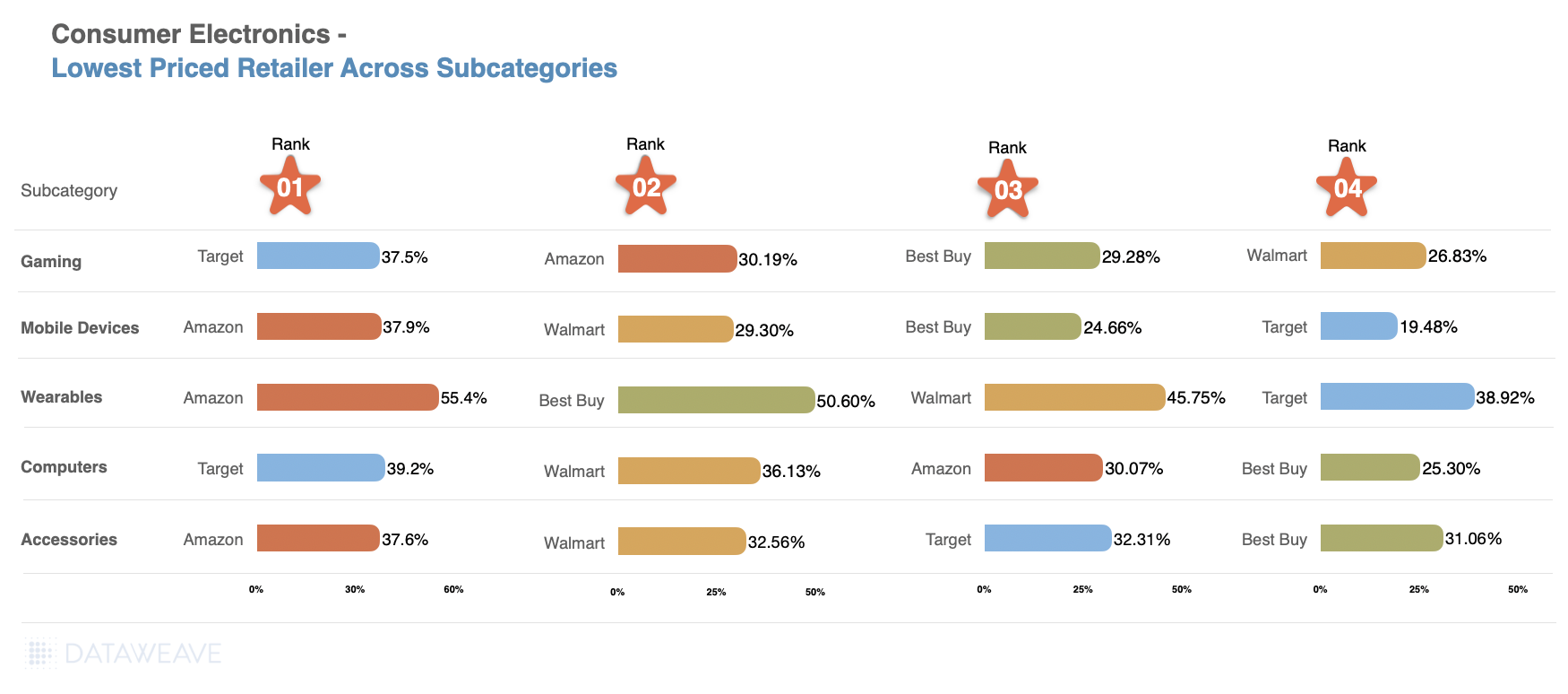

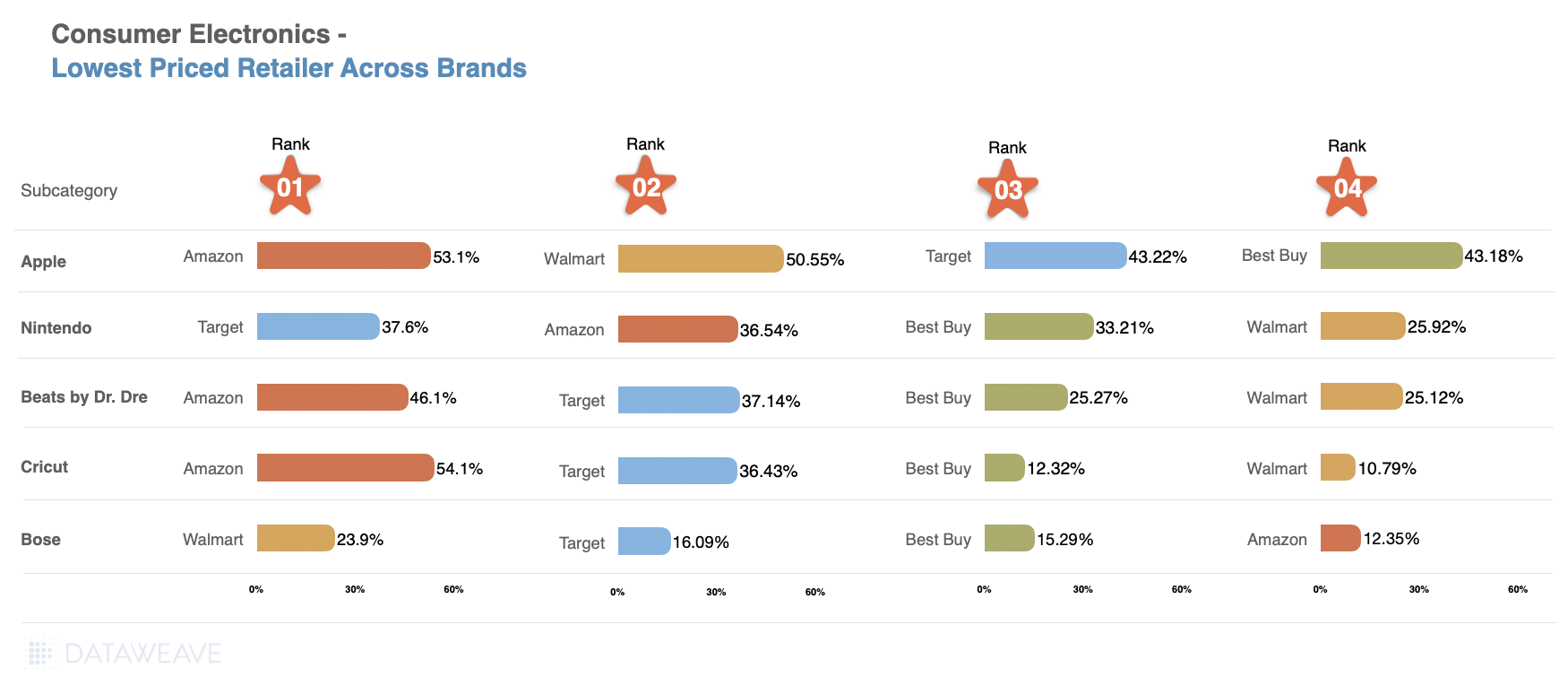

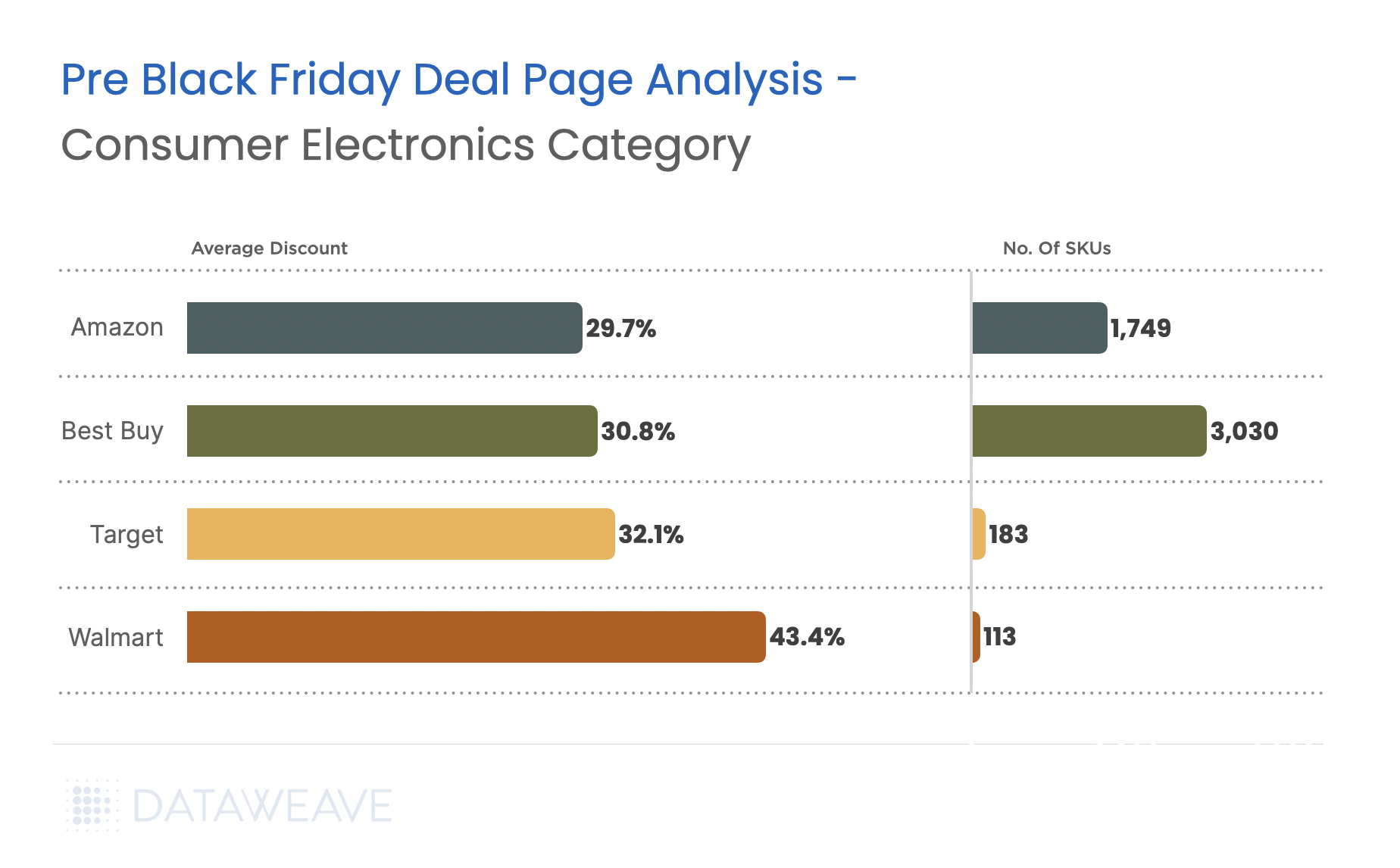

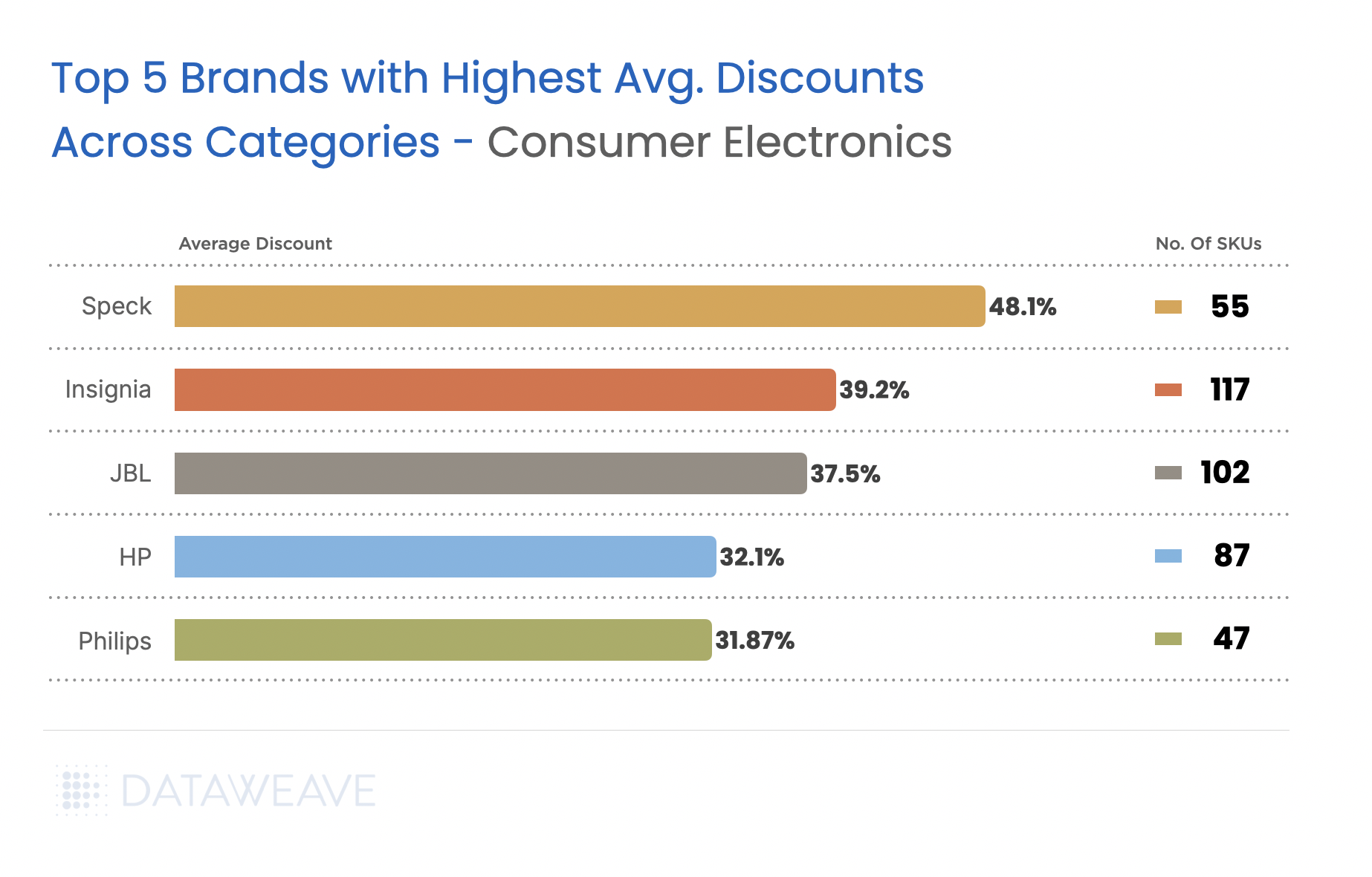

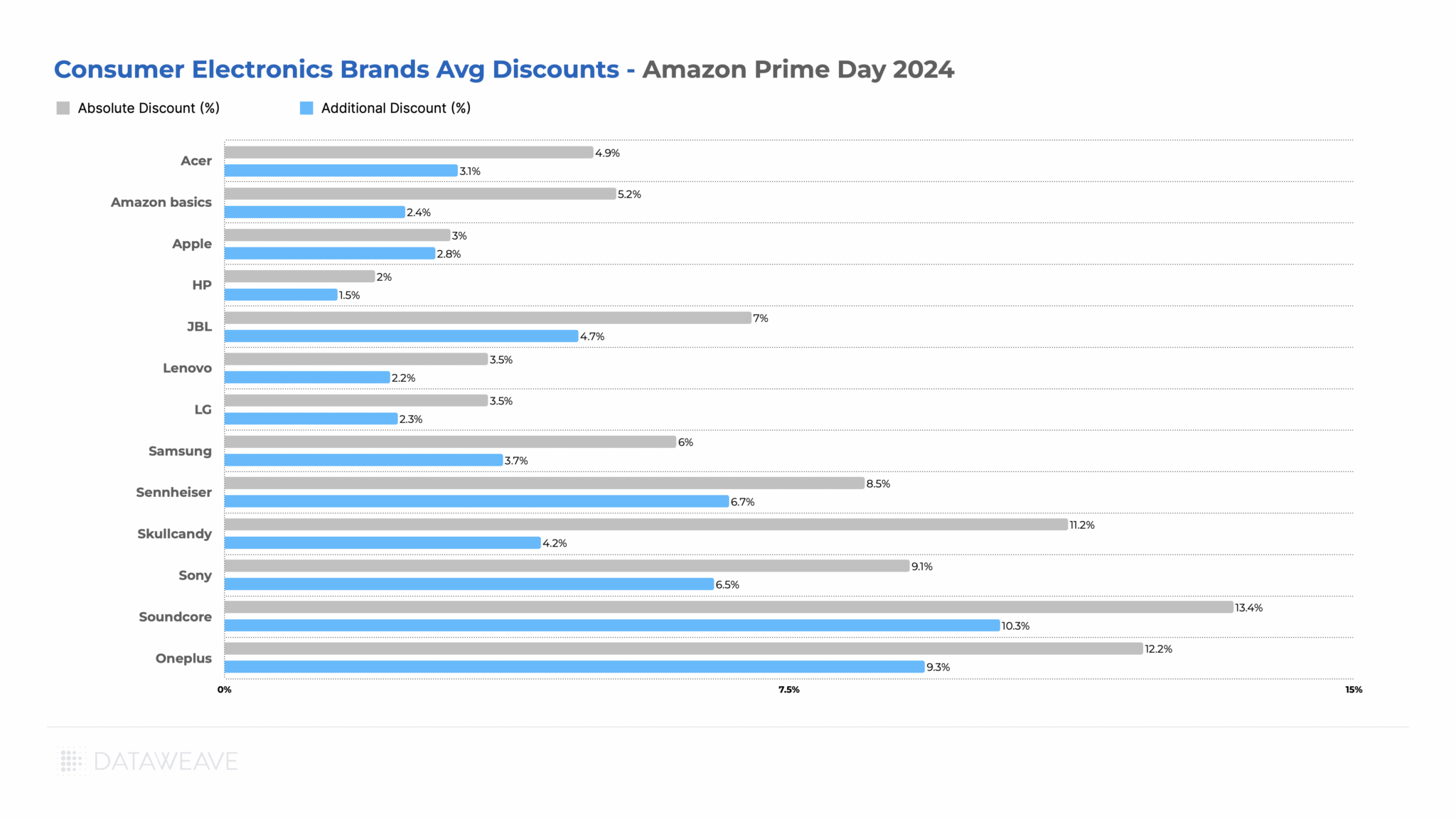

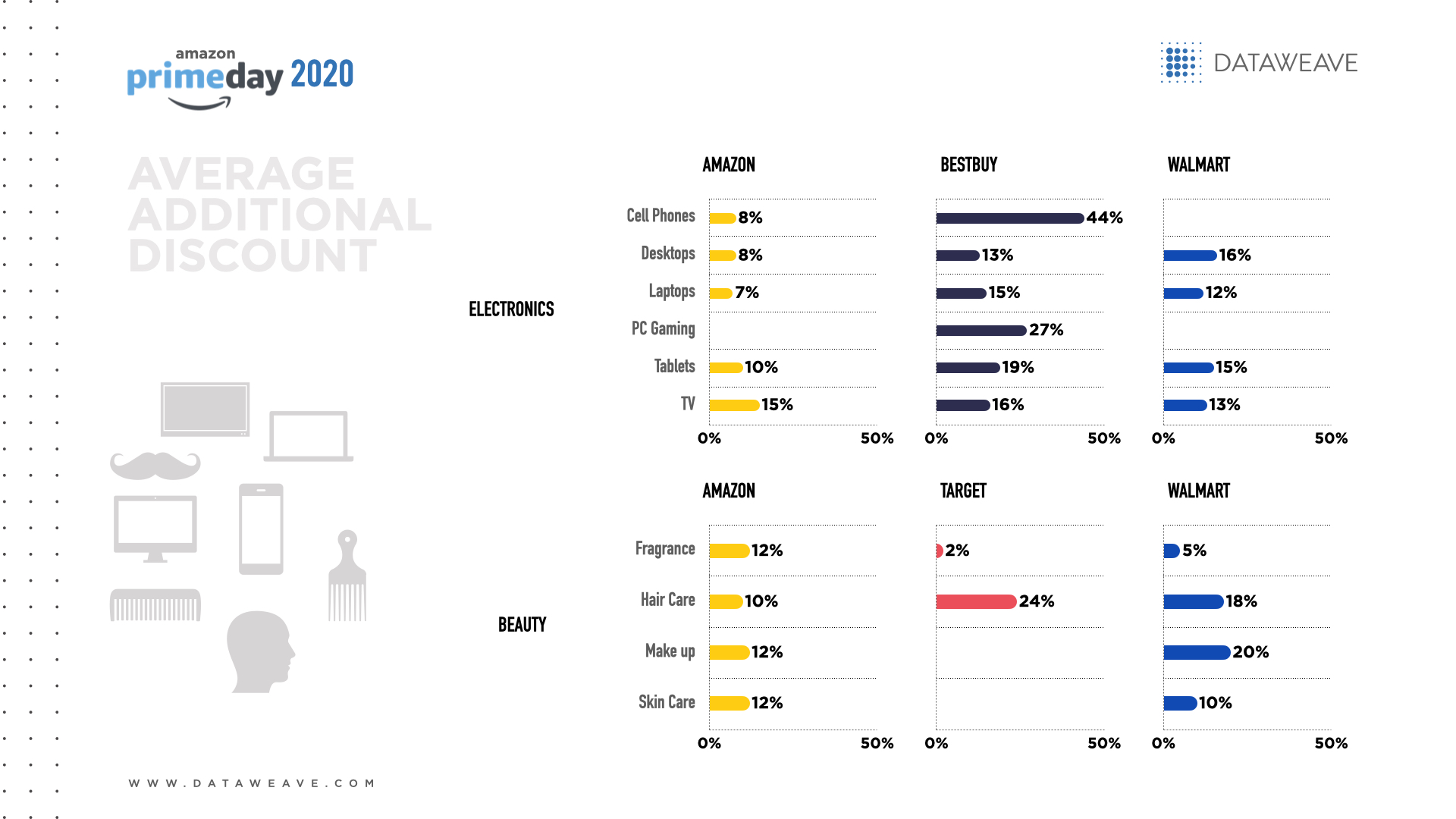

Consumer Electronics

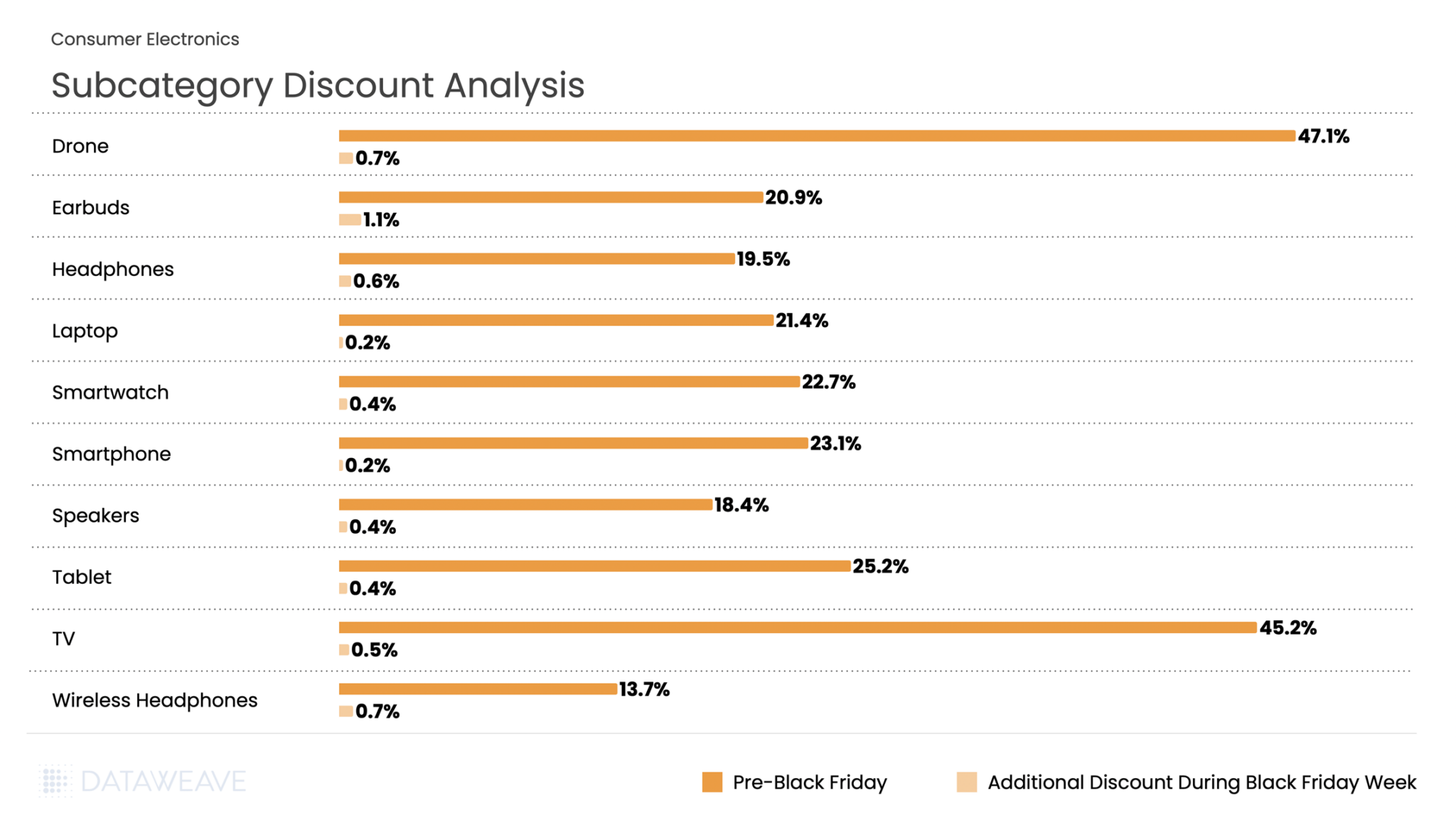

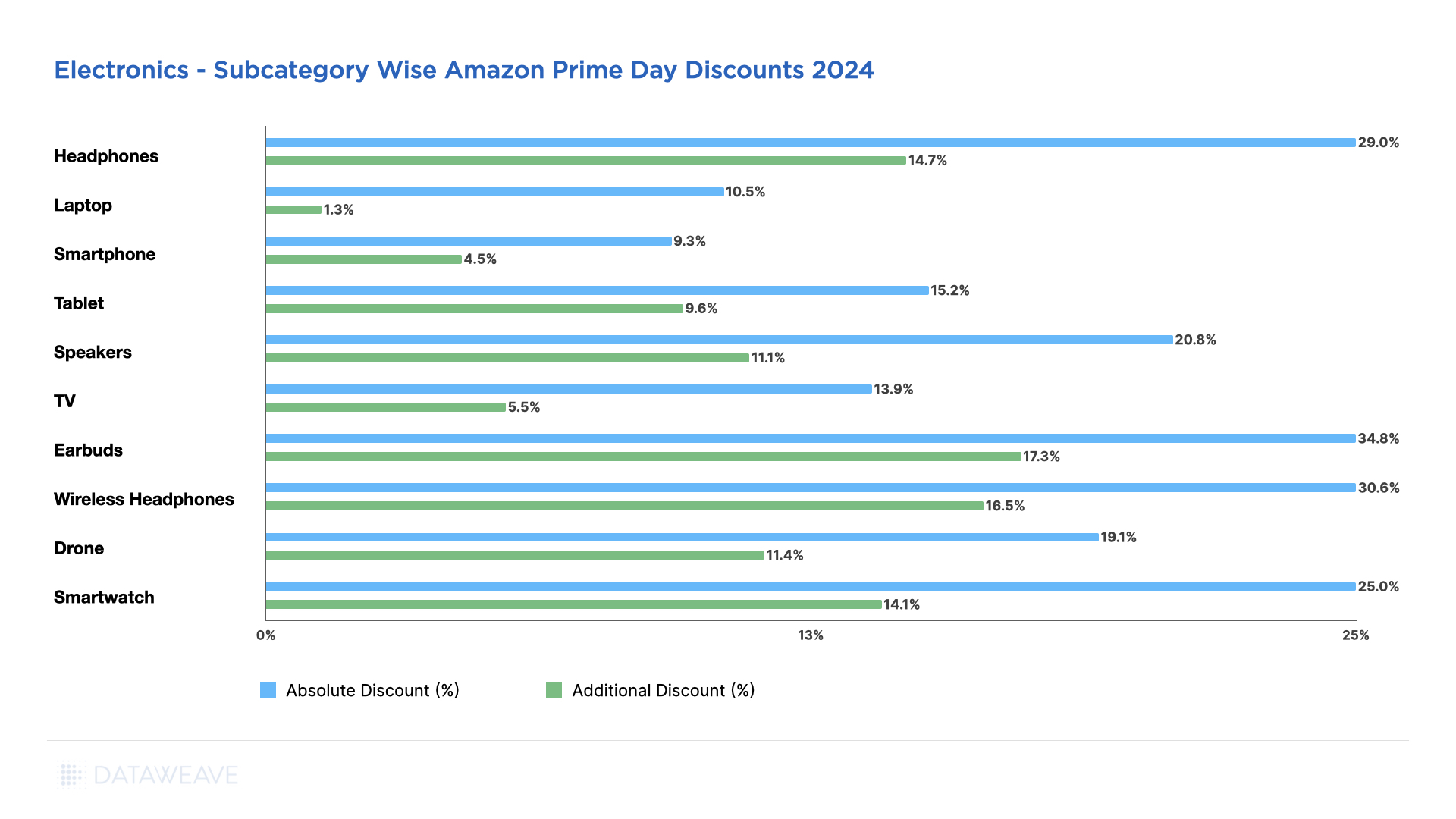

Consumer electronics remain a cornerstone of Black Friday shopping in India, with smartphones and laptops driving significant online sales. Our analysis of 20,439 SKUs reveals distinctive discount patterns across subcategories.

Subcategory Discount Analysis

The category averaged 23.2% pre-Black Friday discounts with an additional 0.5% during Black Friday Week. Drones and TVs led pre-sale discounting at 47.1% and 45.2% respectively, suggesting retailers wanted to clear high-ticket inventory ahead of the main event. Tablets (25.2%) also saw aggressive pre-sale pricing. During Black Friday Week, Earbuds saw the most substantial additional discounts at 1.1%, while categories like Laptops and Smartphones, already heavily discounted, had minimal incremental price cuts at 0.2%.

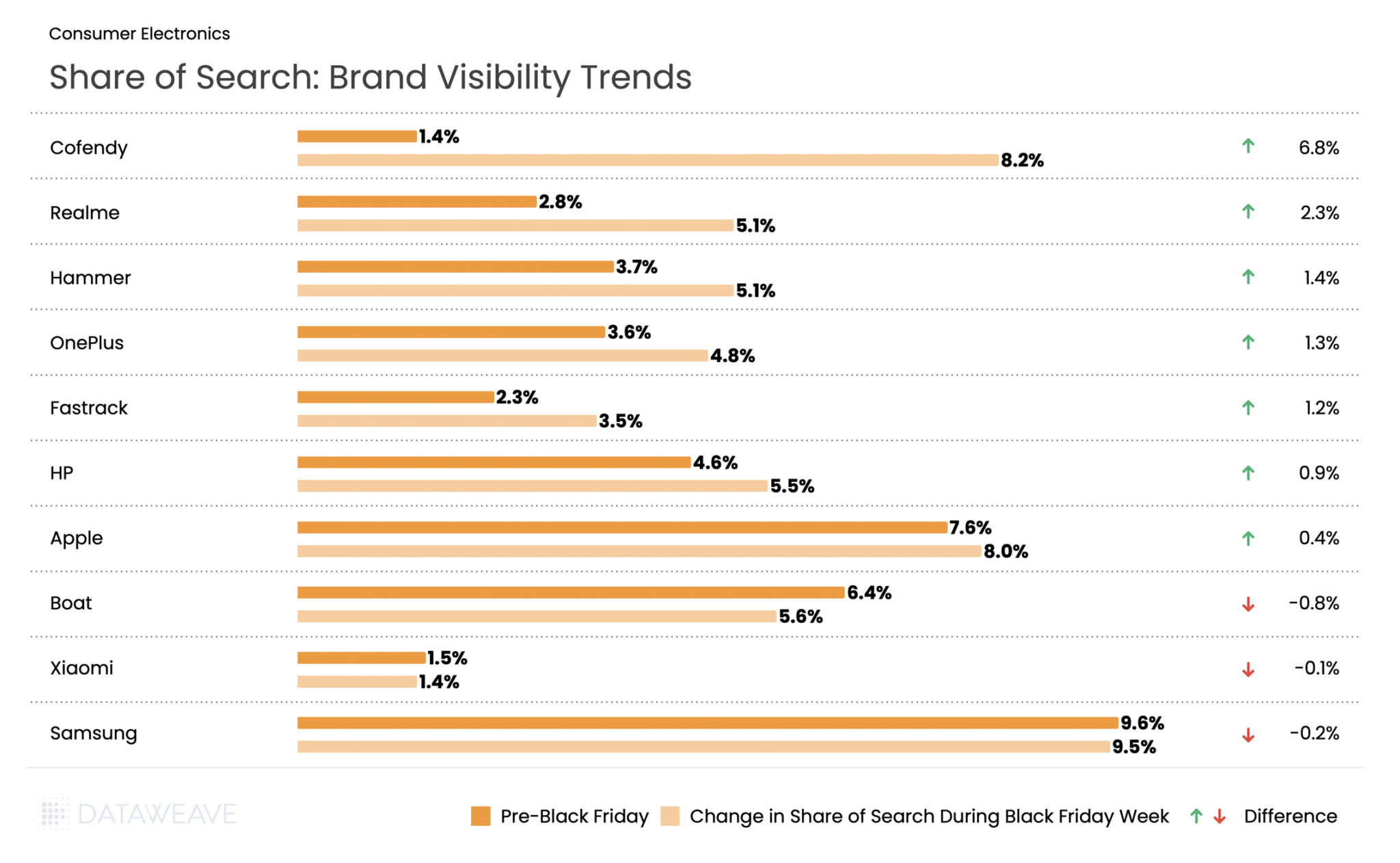

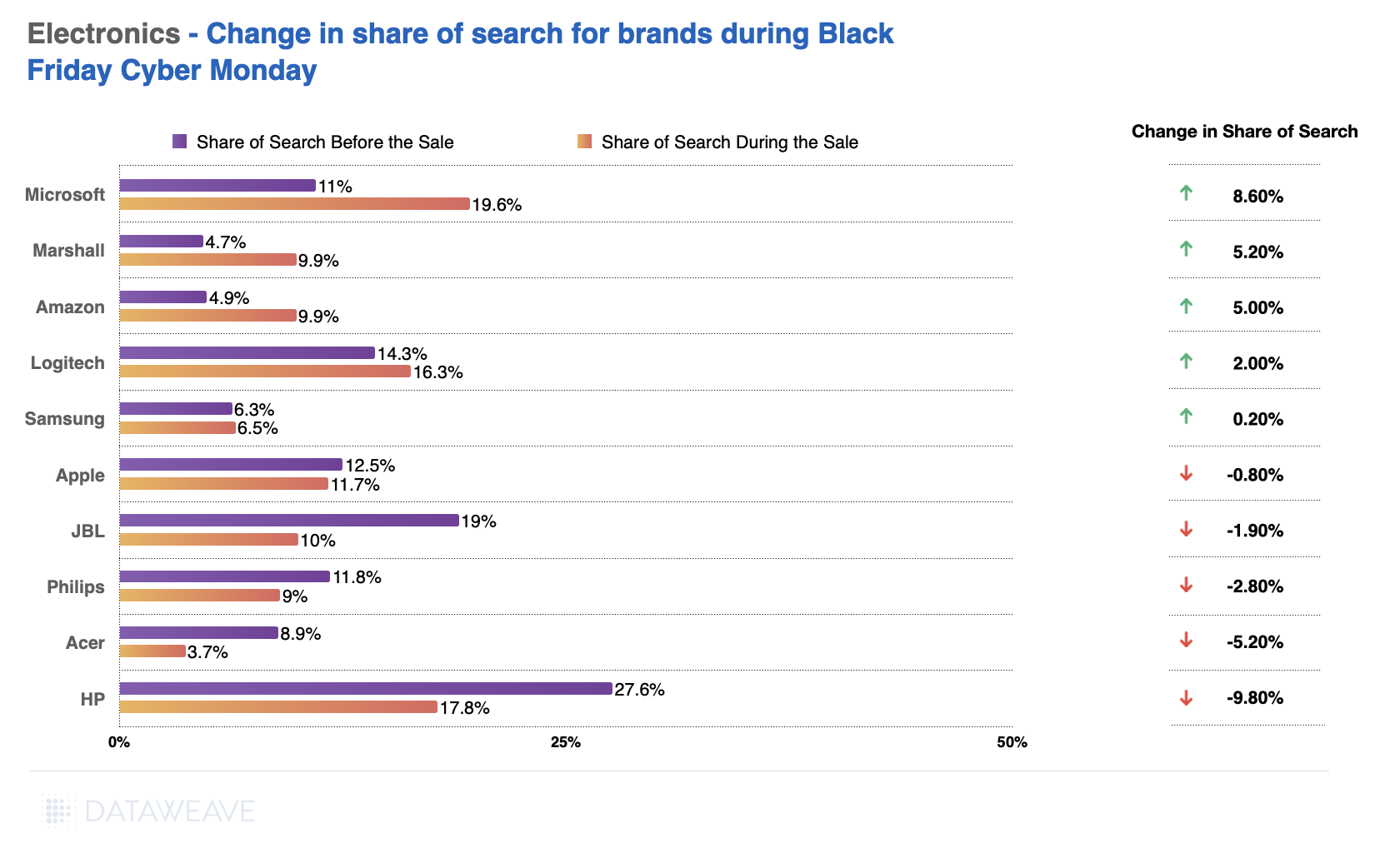

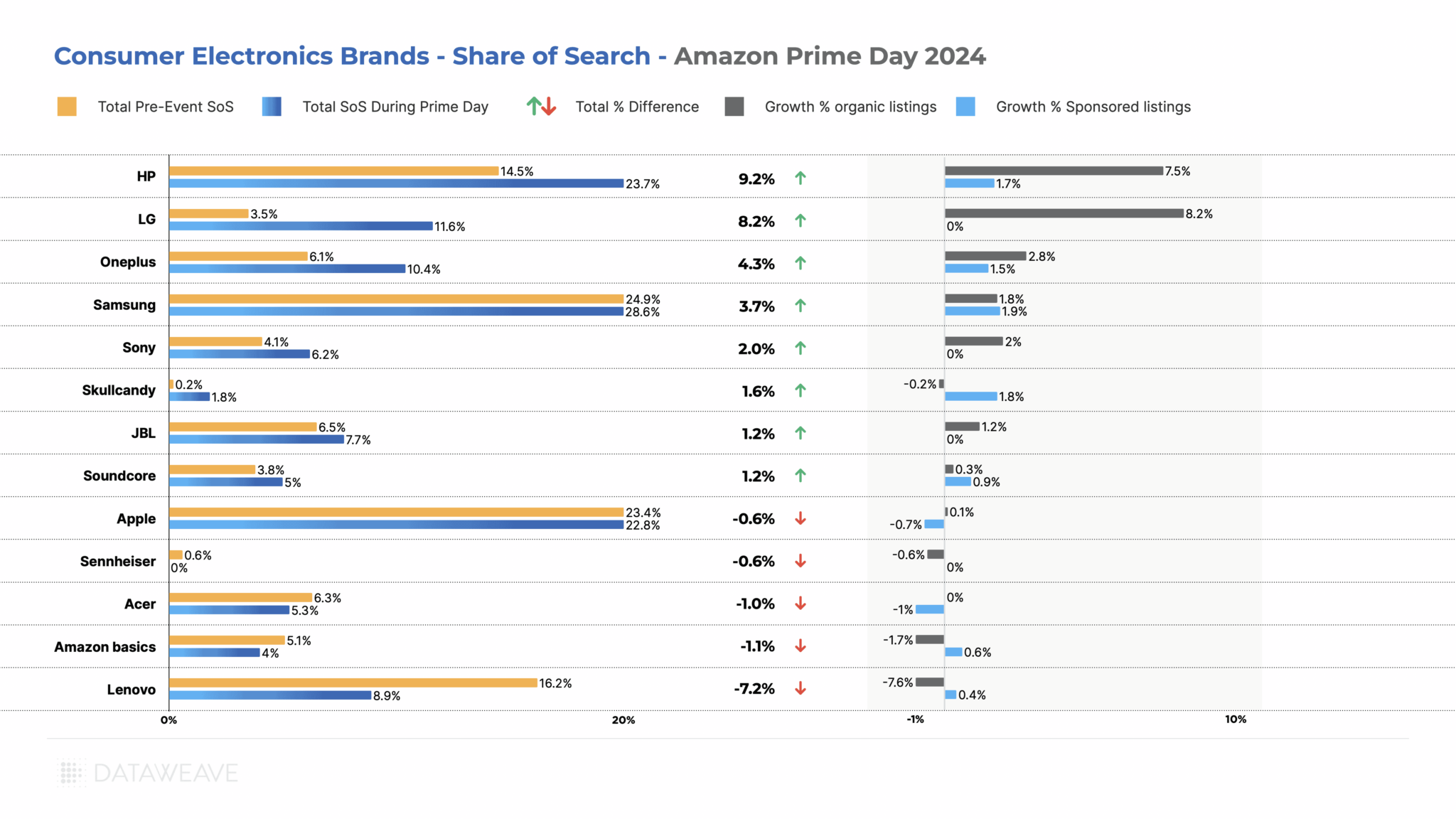

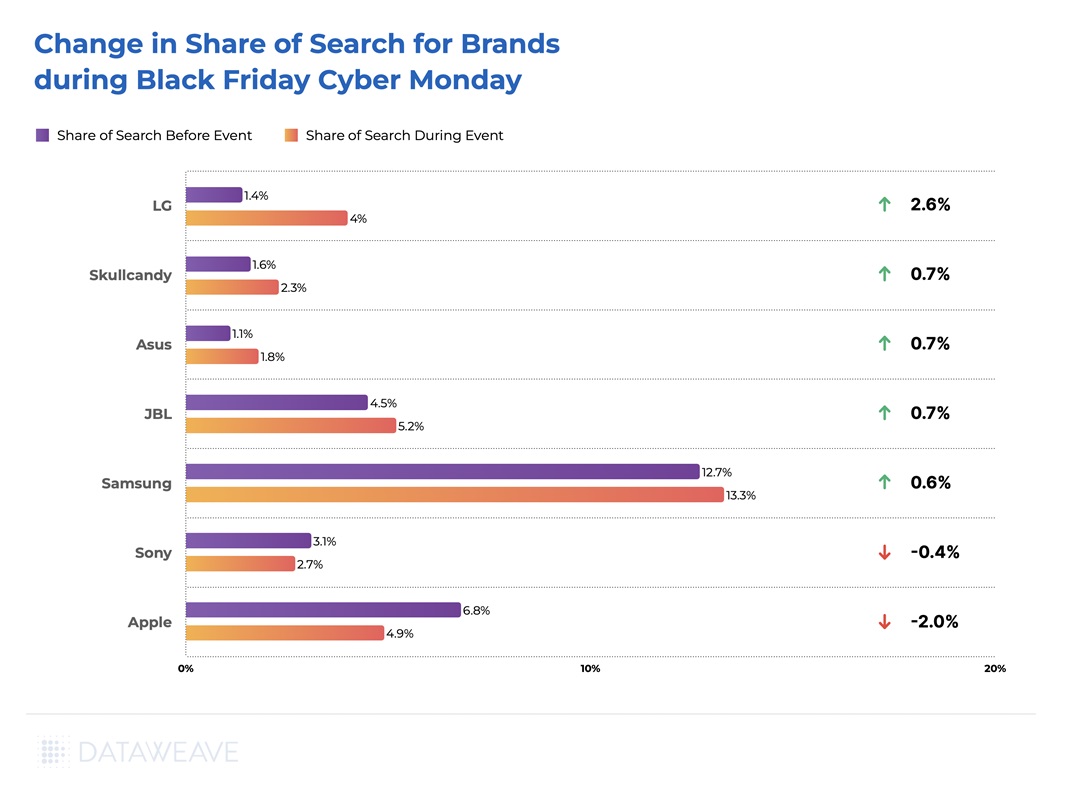

Share of Search: Brand Visibility Trends

The most notable is Cofendy, electronics accessories and speaker brand, that saw the share of search rise from 1.4% pre Black Friday to 8.2% during the event. Realme followed with a solid 2.3% gain, reinforcing its position as a rising smartphone brand. Smart gadget brand Hammer also saw visibility increase by 1.4% at par with OnePlus, Fastrack, HP and Asus.

Samsung saw the highest brand visibility with share of search at 9.6% pre-event and 9.5% during Black Friday week, despite seeing a small drop in visibility. Audio brand Boat saw a visibility drop by 0.8%, while Xiaomi saw the share of search drop by 0.1%. This shift suggests that Indian consumers were drawn to newer brands and compelling deals across computing and mobile devices during the sale period.

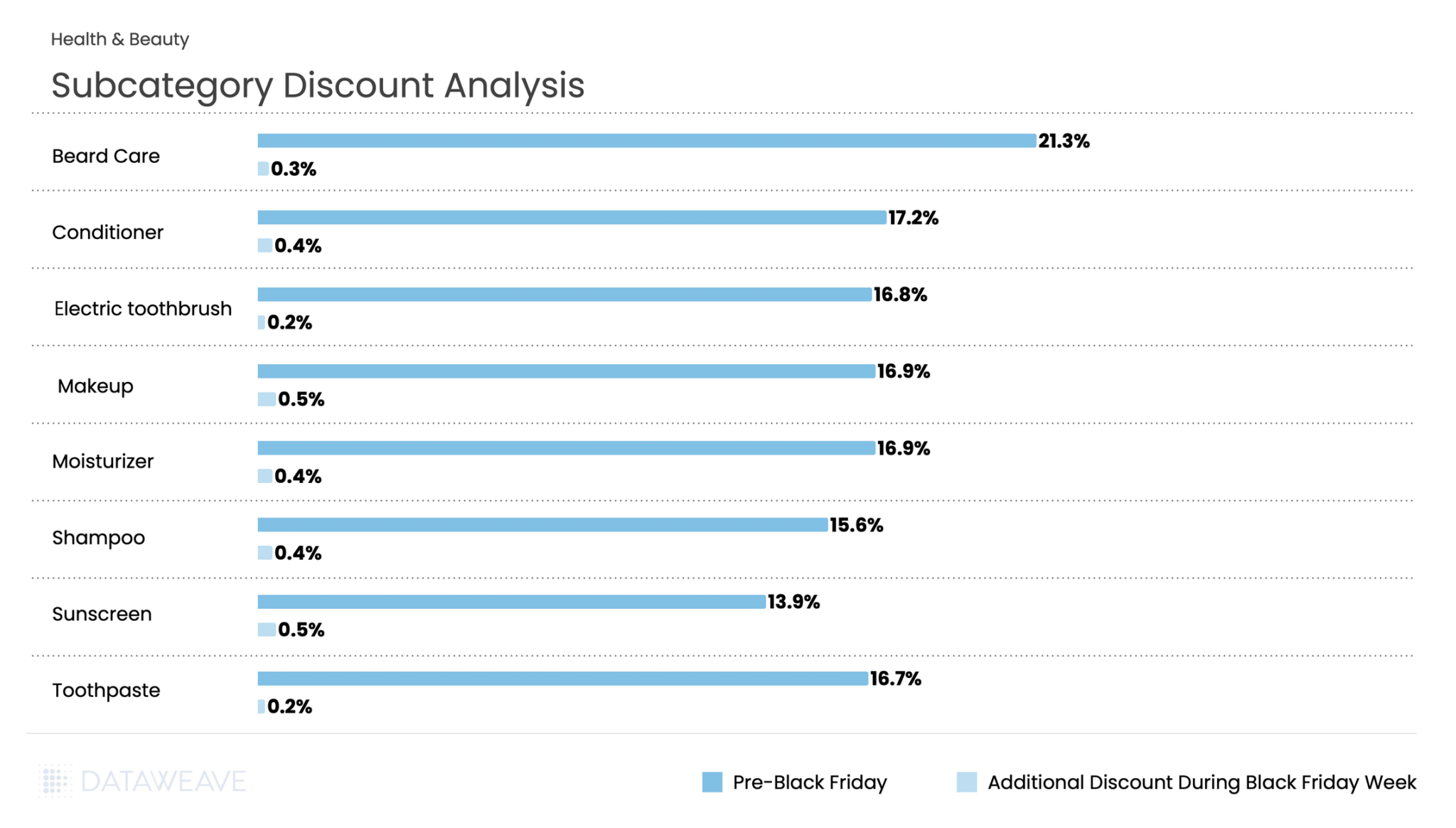

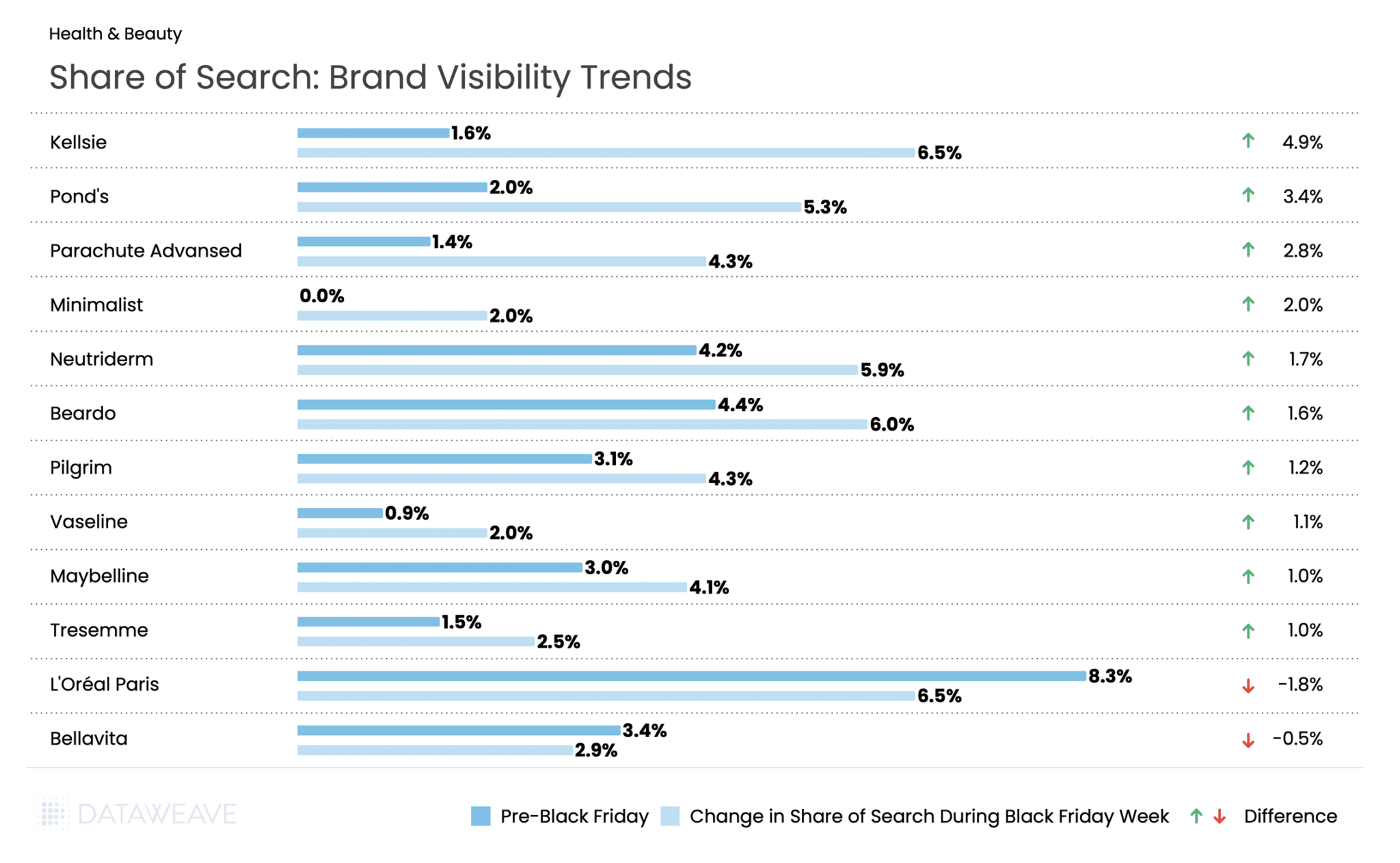

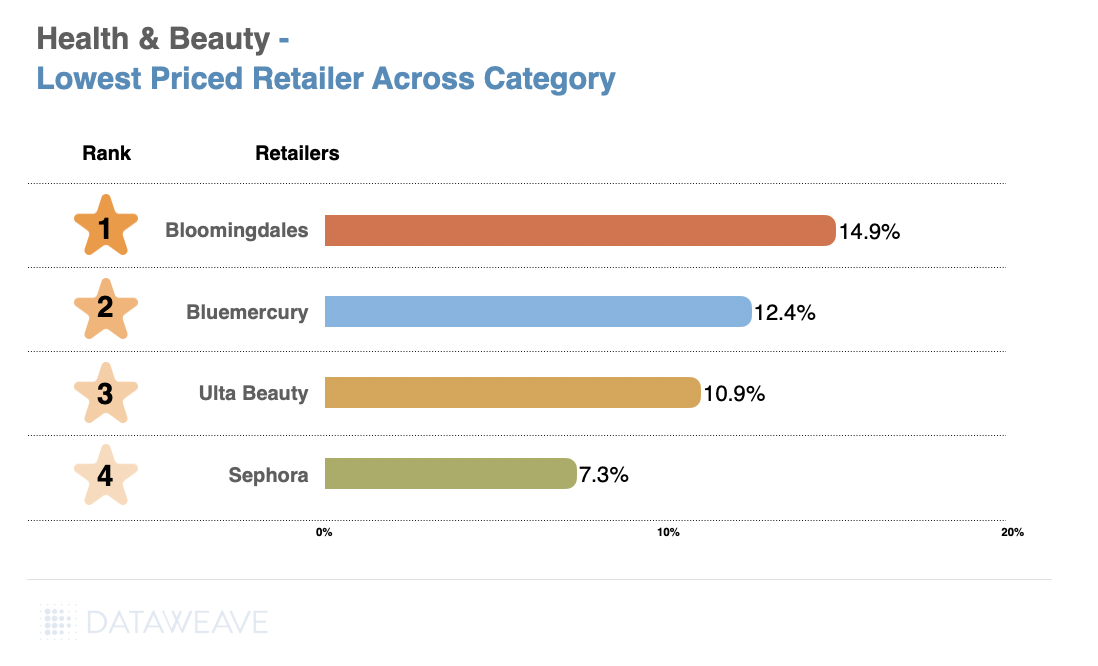

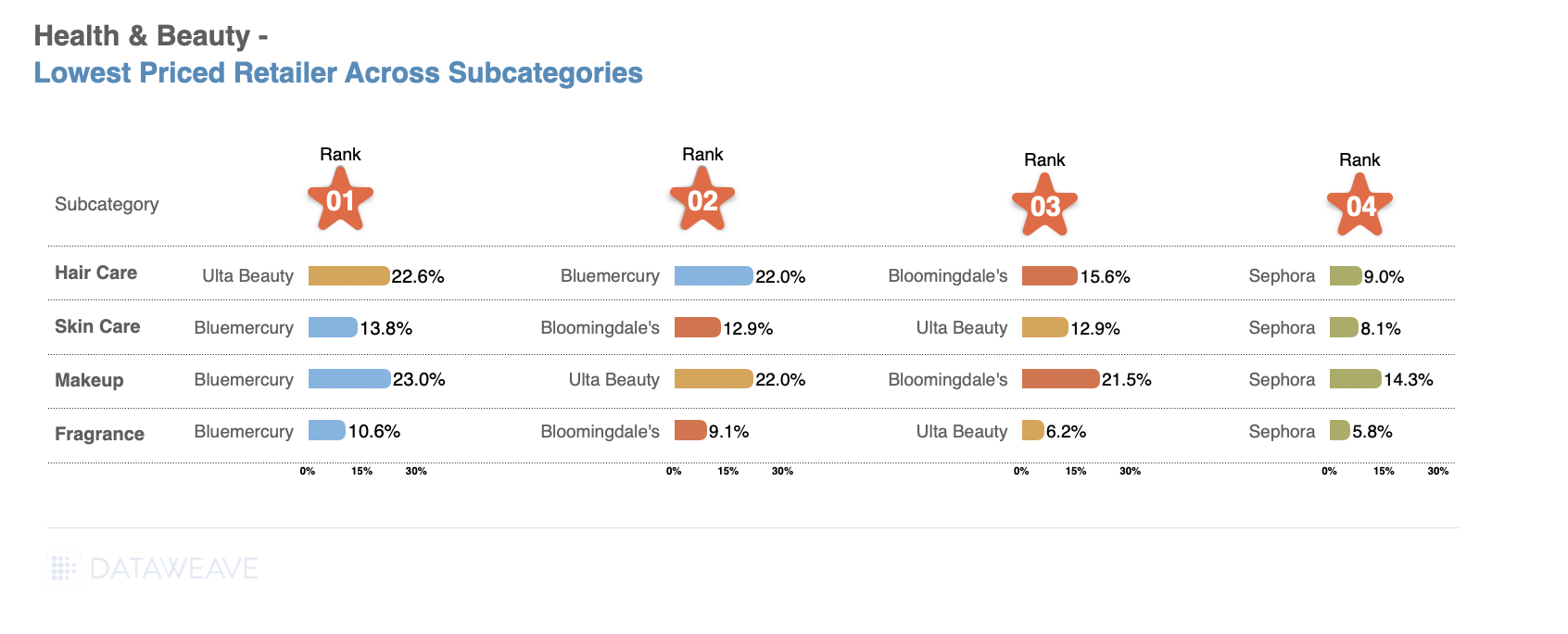

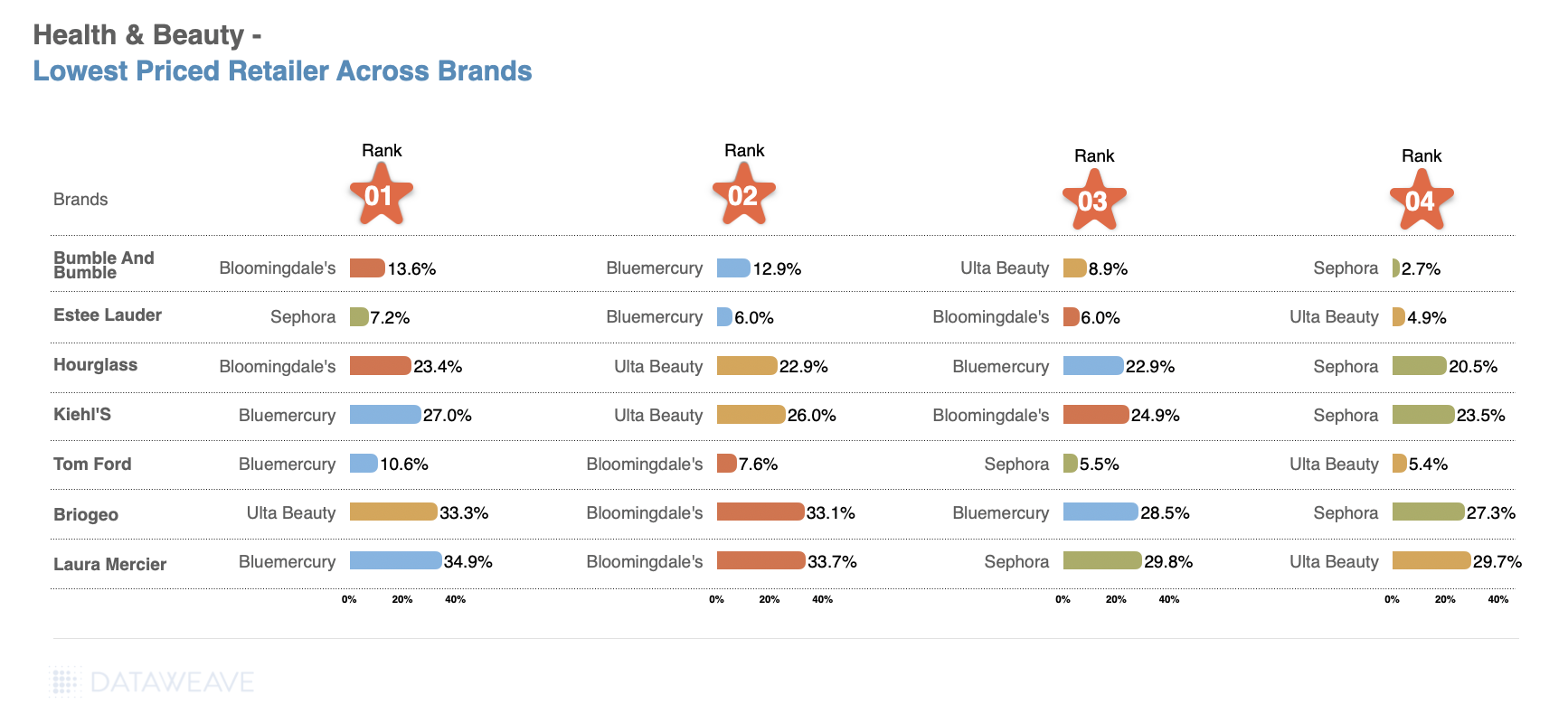

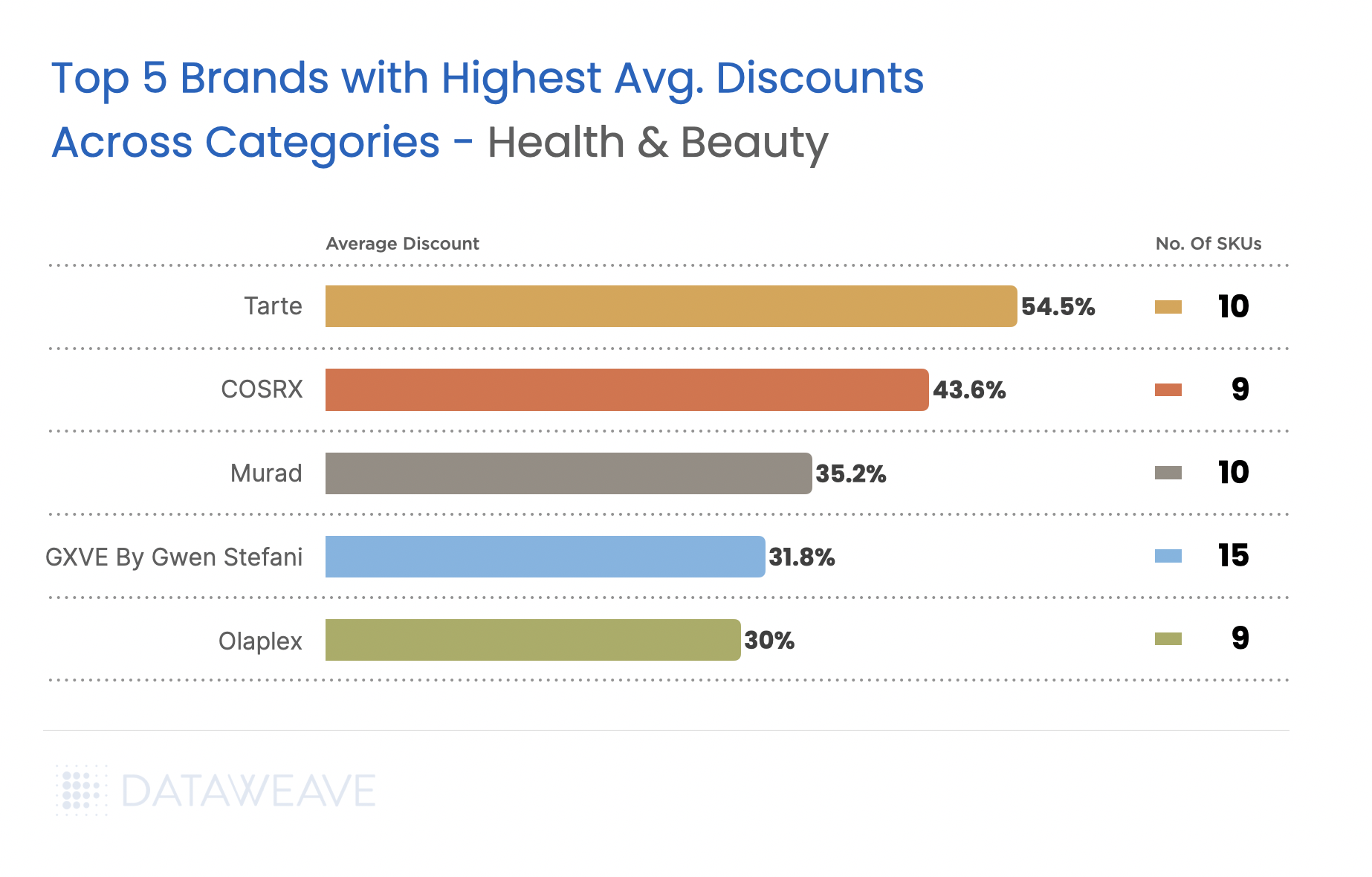

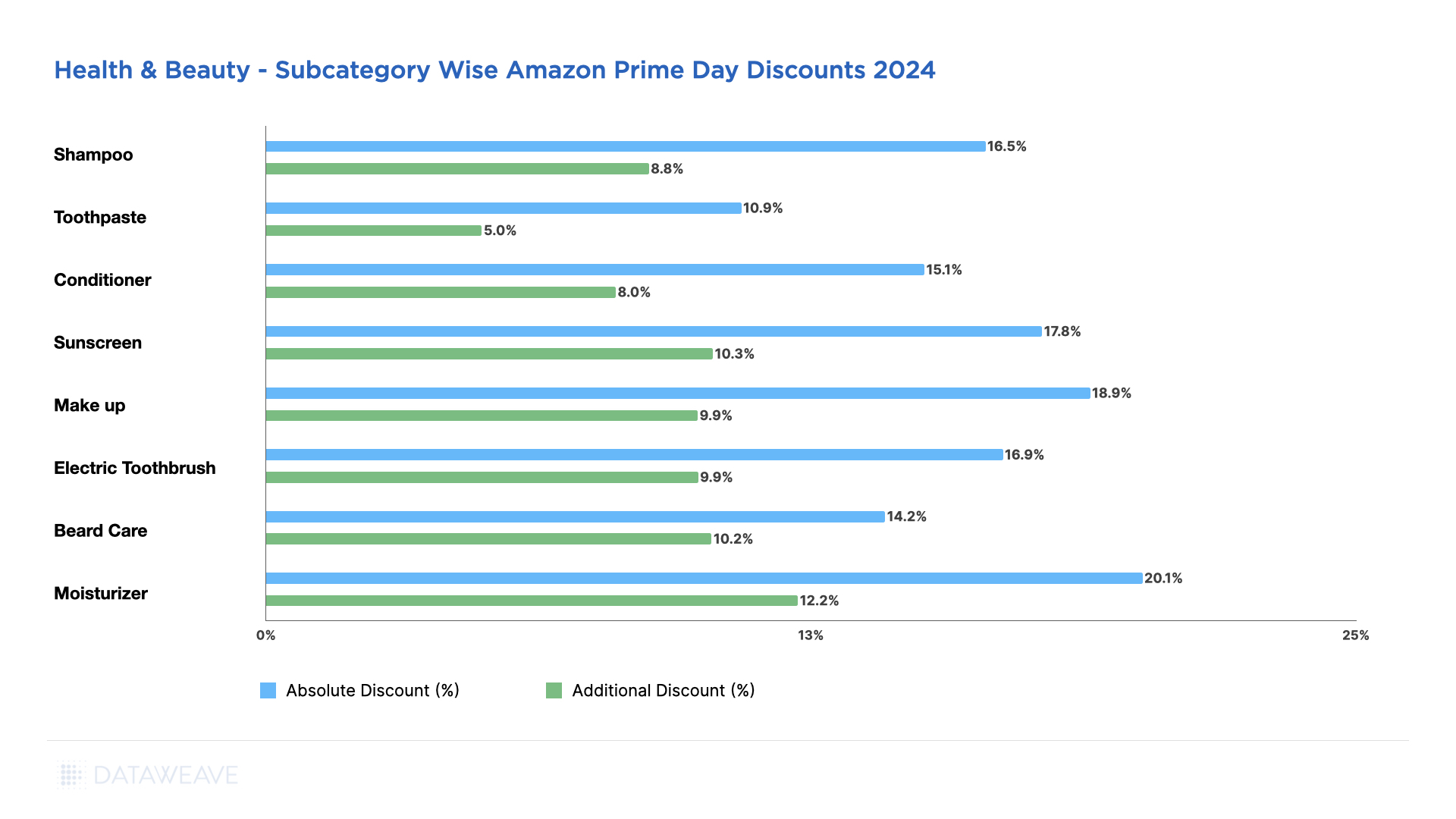

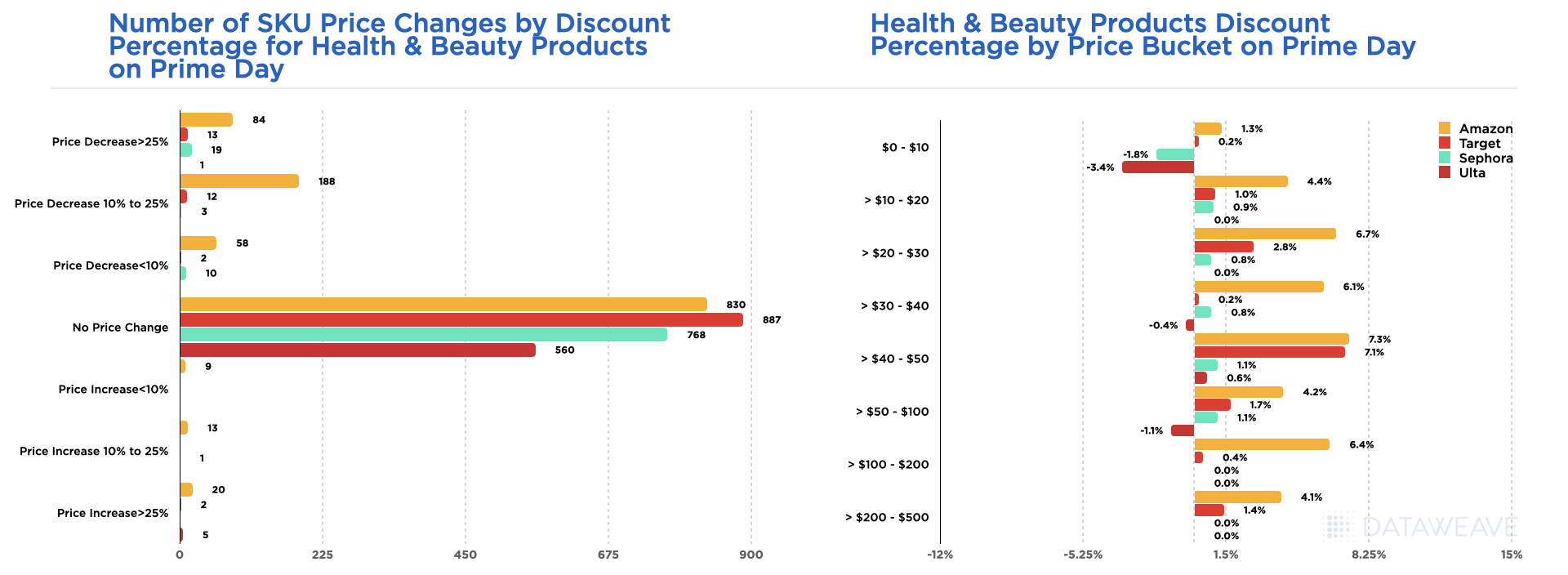

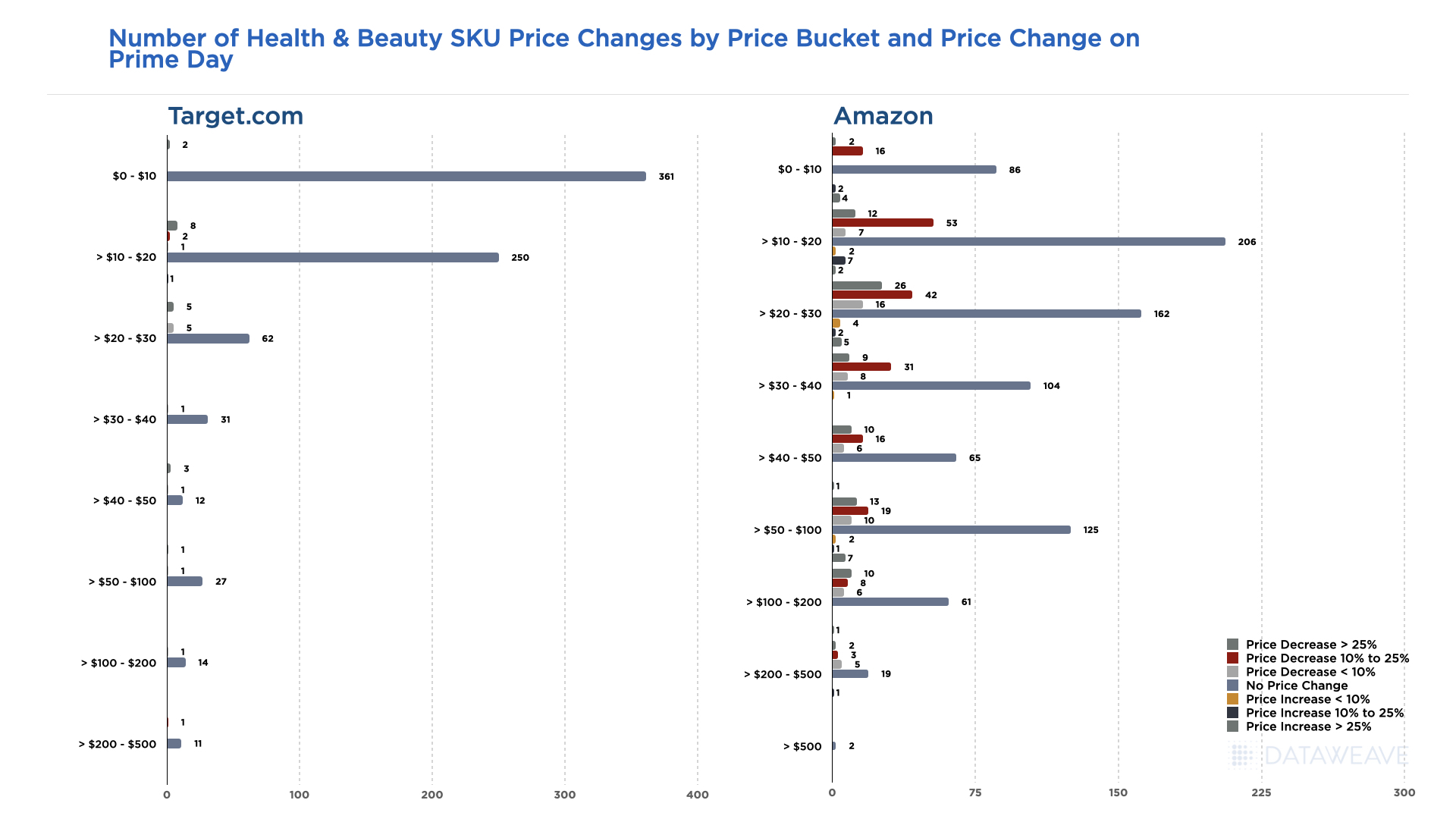

Health & Beauty

The Indian beauty and personal care market is experiencing rapid growth, expected to reach $30 billion by 2027. Black Friday has become an important sales window for beauty brands and retailers. Our analysis of 19,854 SKUs reveals distinct patterns.

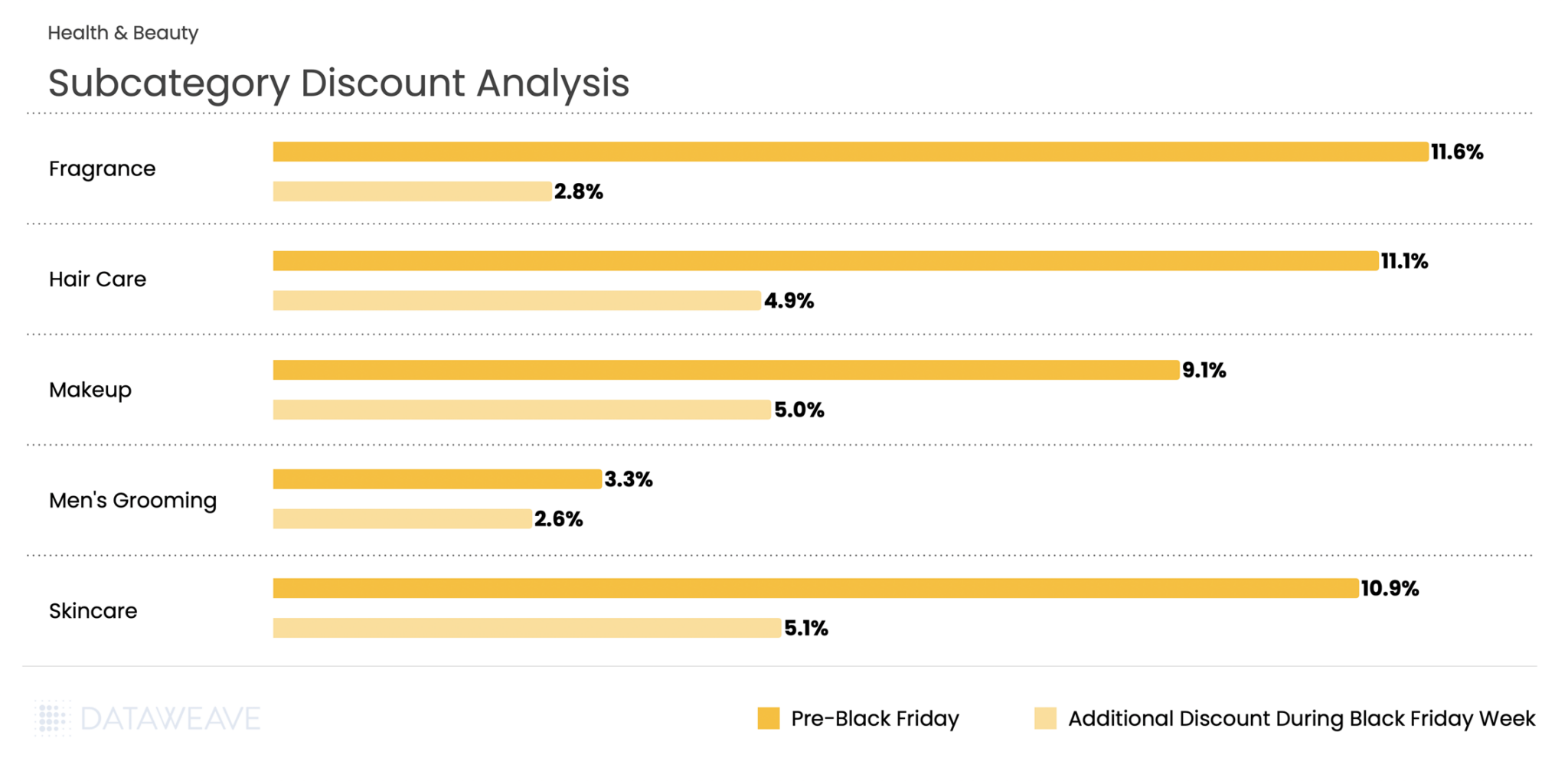

Subcategory Discount Analysis

The category averaged 17% pre-Black Friday discounts with an additional 0.4% during Black Friday Week. Beard Care led early discounting at 21.3%, reflecting strong pre-sale positioning in men’s grooming. Conditioner (17.2%), Makeup (16.9%), and Moisturizer (16.9%) also saw solid baseline promotions. During Black Friday Week, Makeup and Sunscreen saw the highest additional discounts at 0.5% each, while Electric Toothbrush and Toothpaste maintained modest incremental discounts at 0.2%.

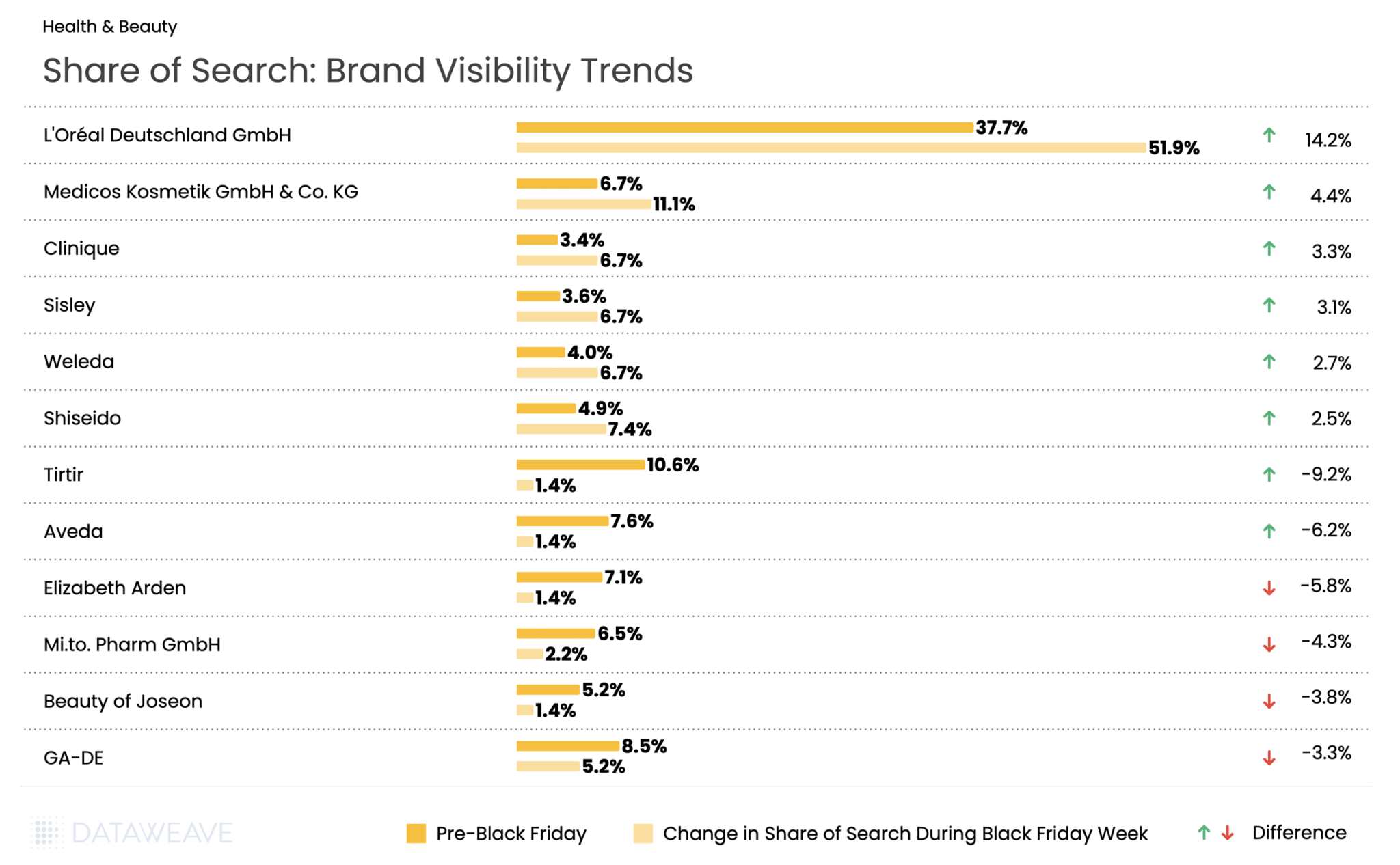

Share of Search: Brand Visibility Trends

Affordable and emerging beauty brands dominated during Black Friday in India. Kellsie (beauty tools brand) surged from 1.6% to 6.5%. Classic mass-market brands like Pond’s (+3.4%) and Parachute Advanced (+2.8%) also performed strongly, alongside men’s grooming favorite Beardo (+1.6%). Other popular brands like Maybelline, Tresemme, Vaseline, all saw share of search and visibility increase during Black Friday.

Skincare brand Minimalist made a notable entry, jumping from 0% to 2.0% visibility. The flip side? Premium international brand L’Oréal Paris dropped from 8.3% to 6.5%, losing visibility during Black Friday.

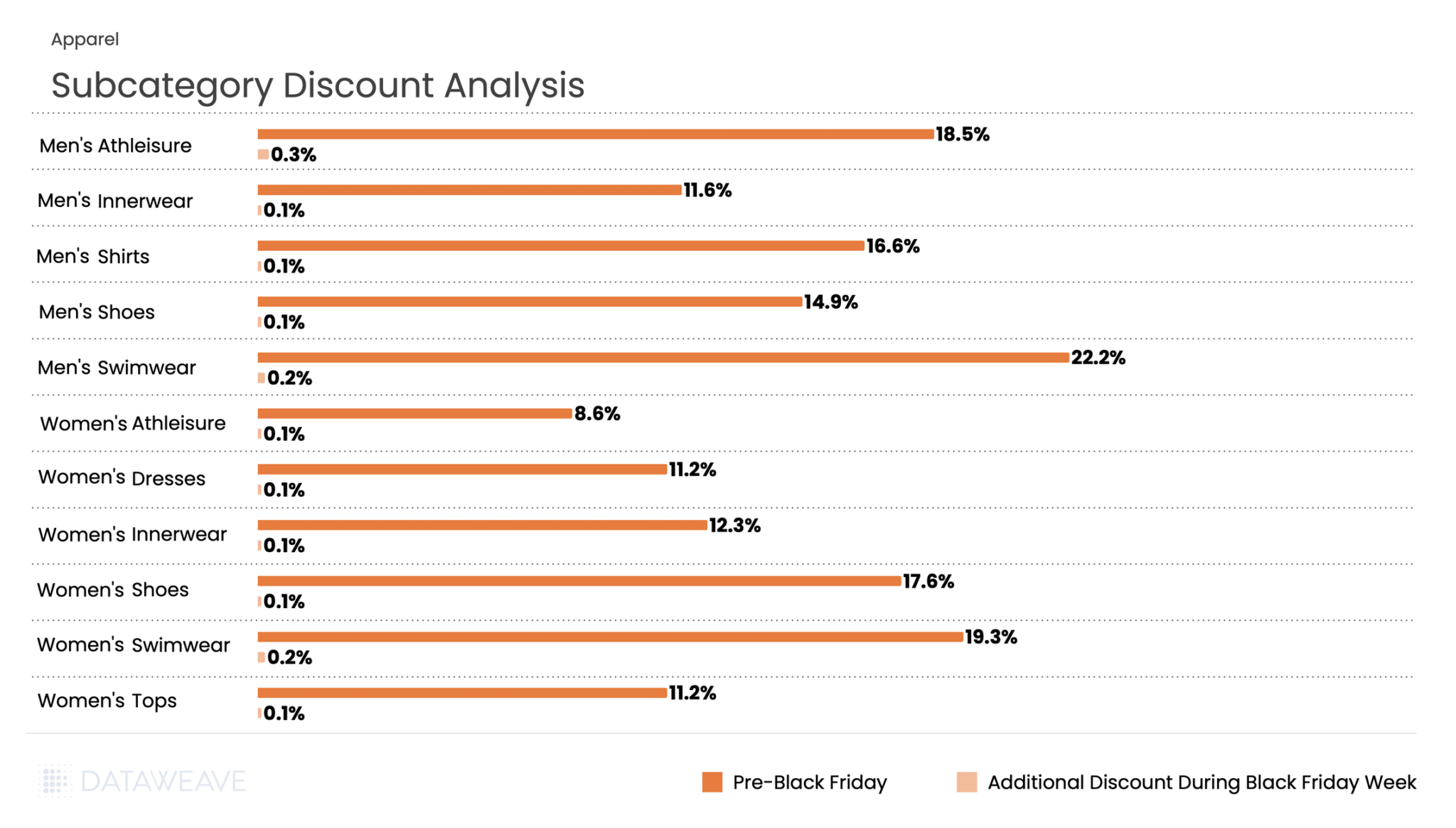

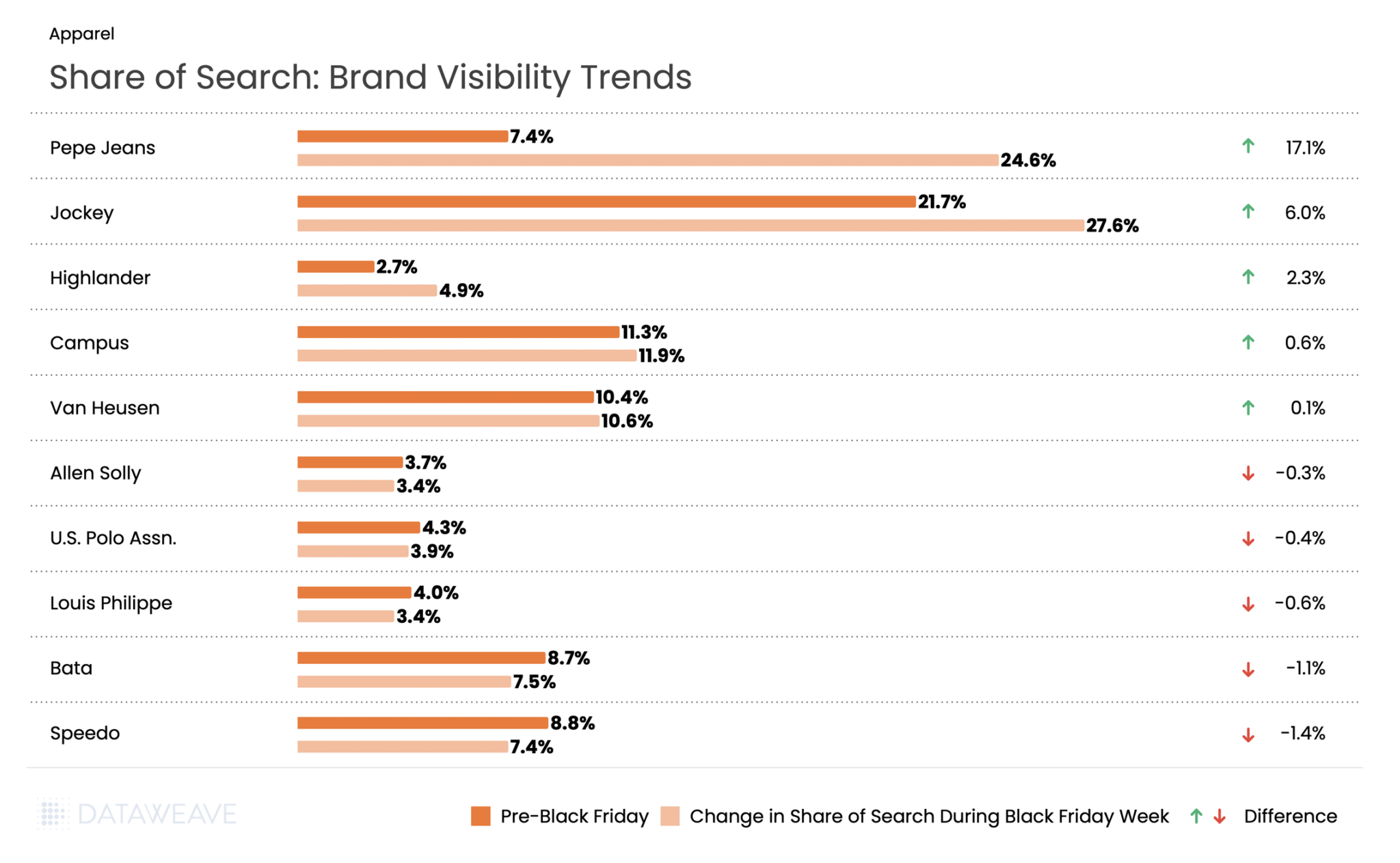

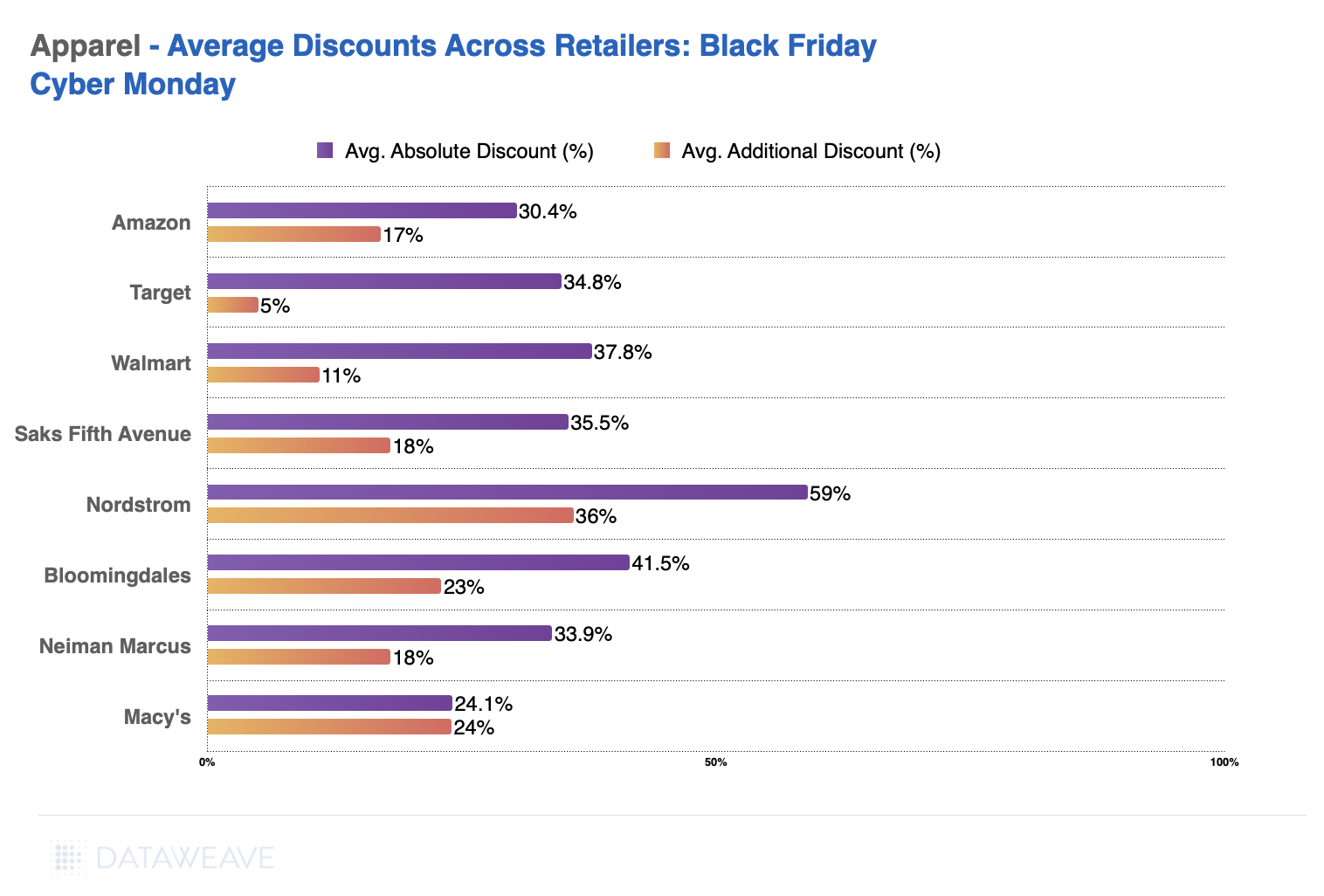

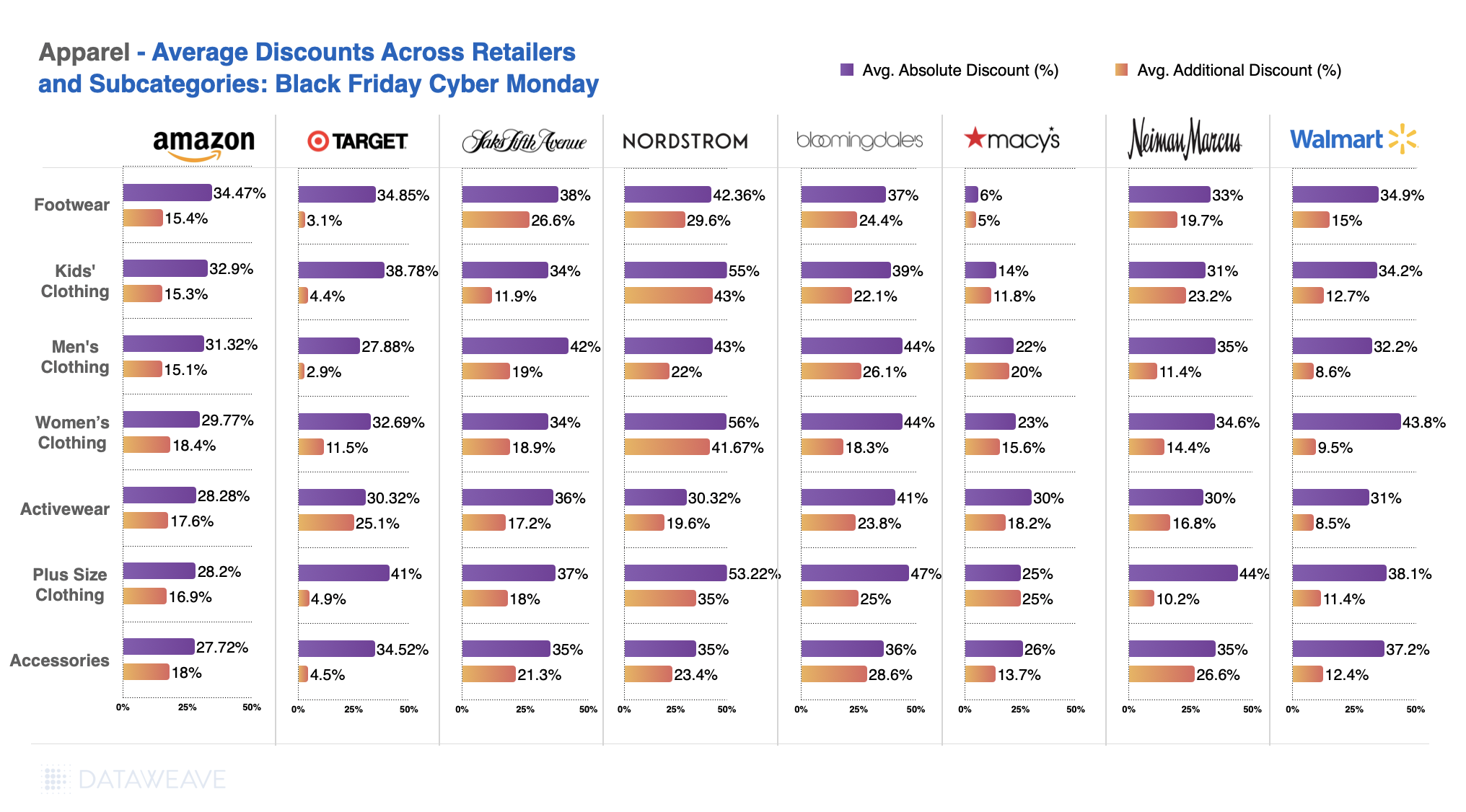

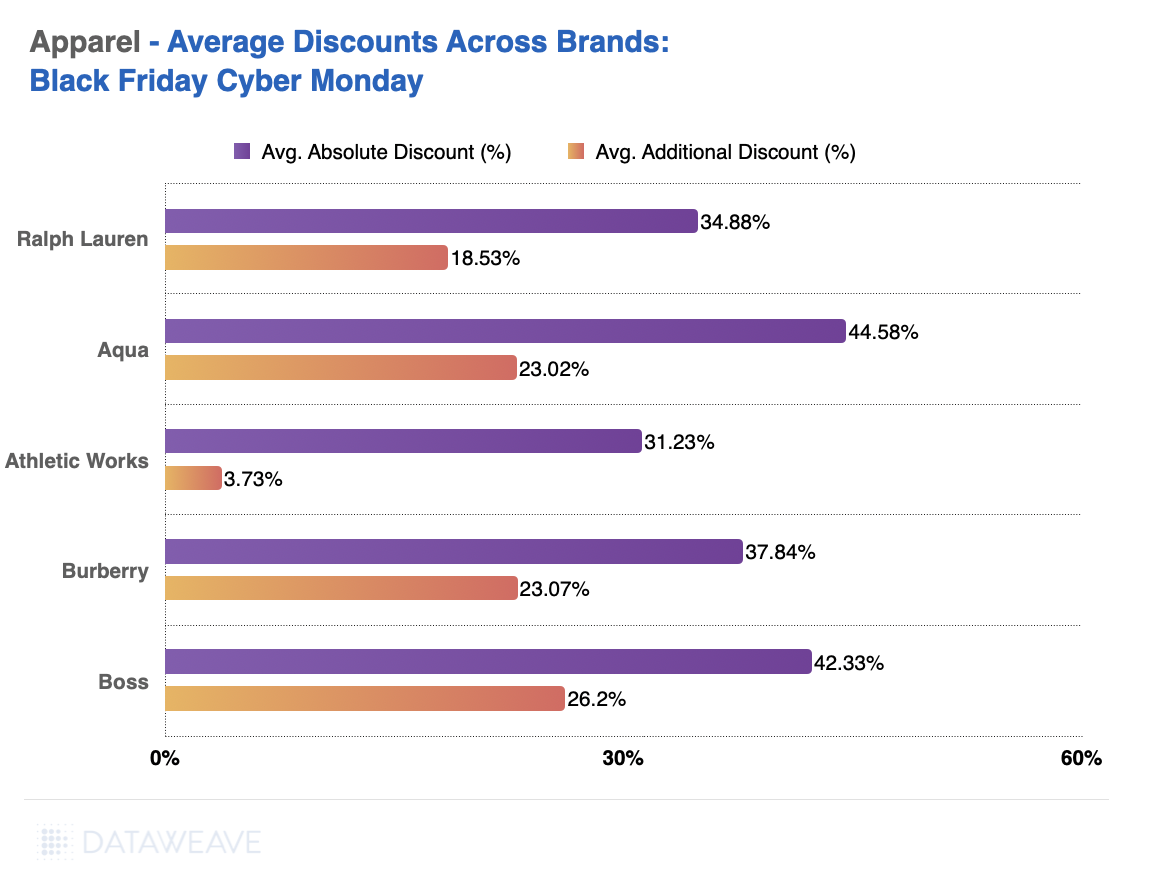

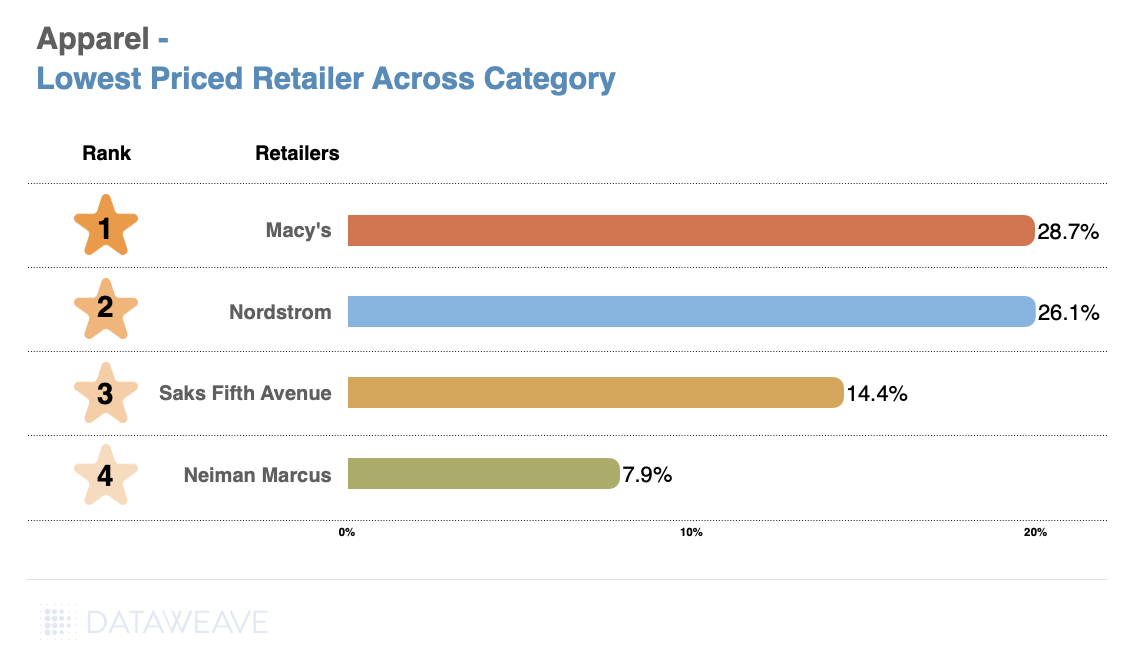

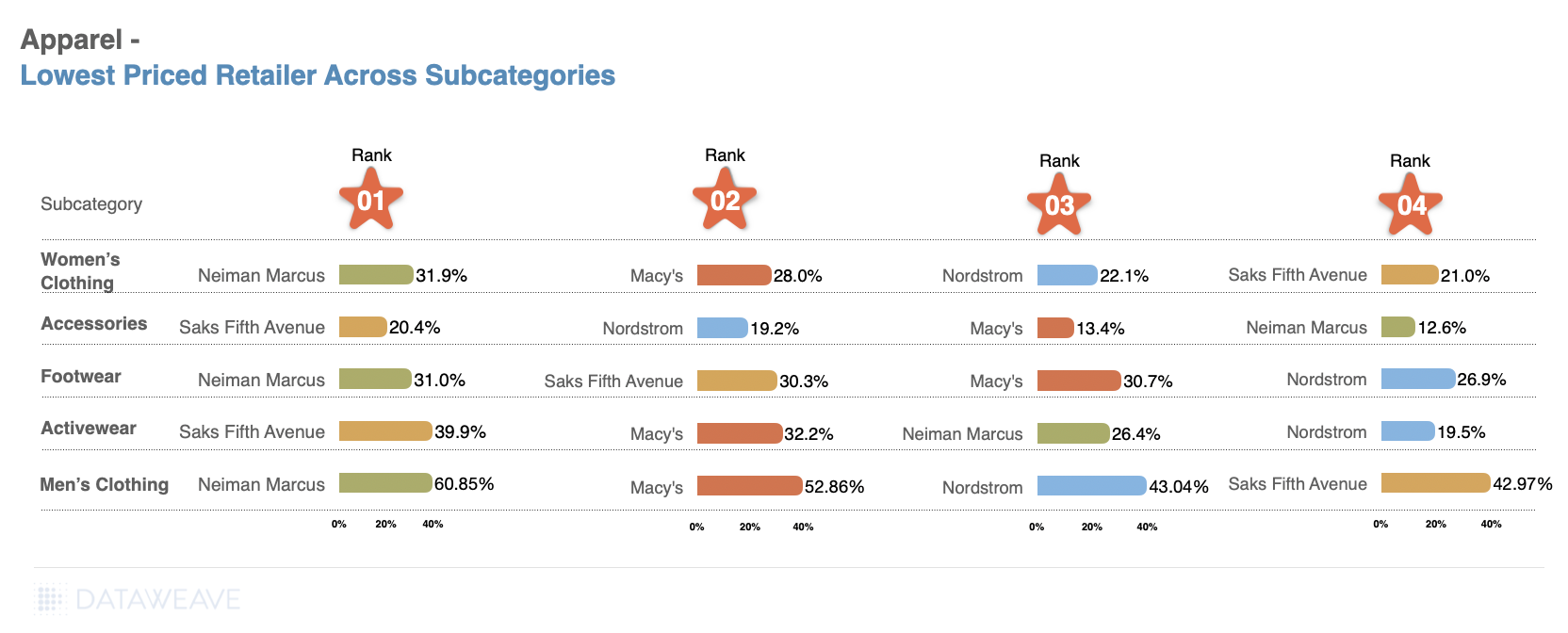

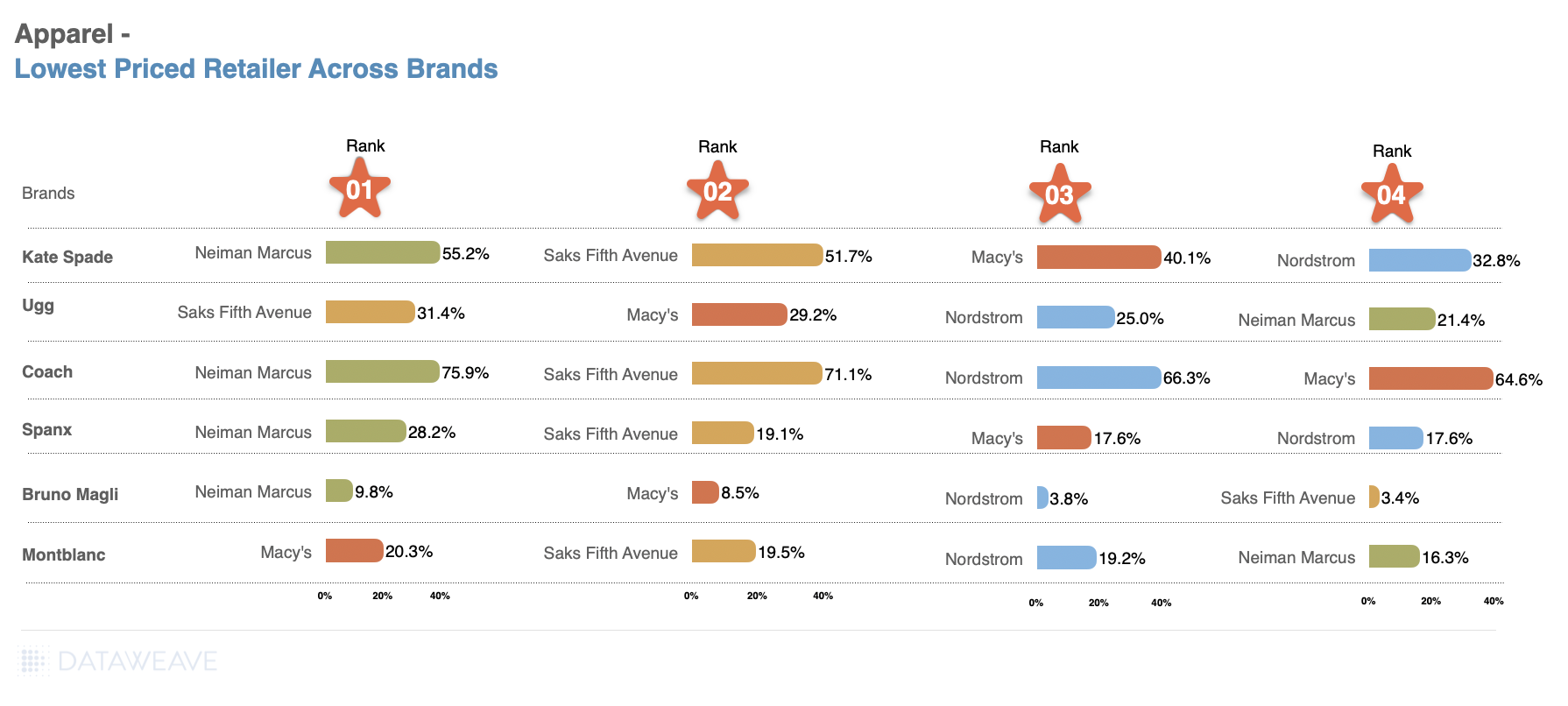

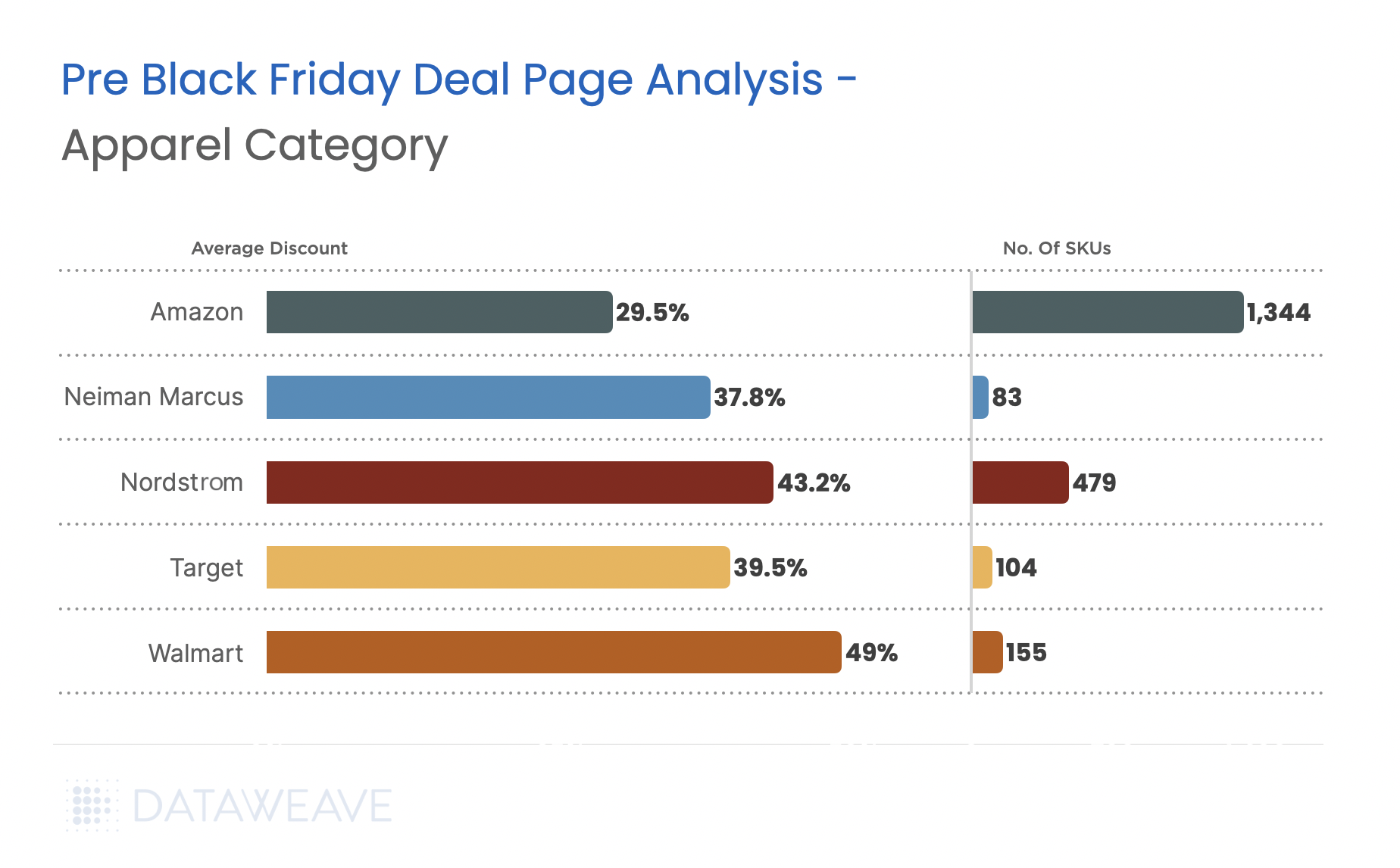

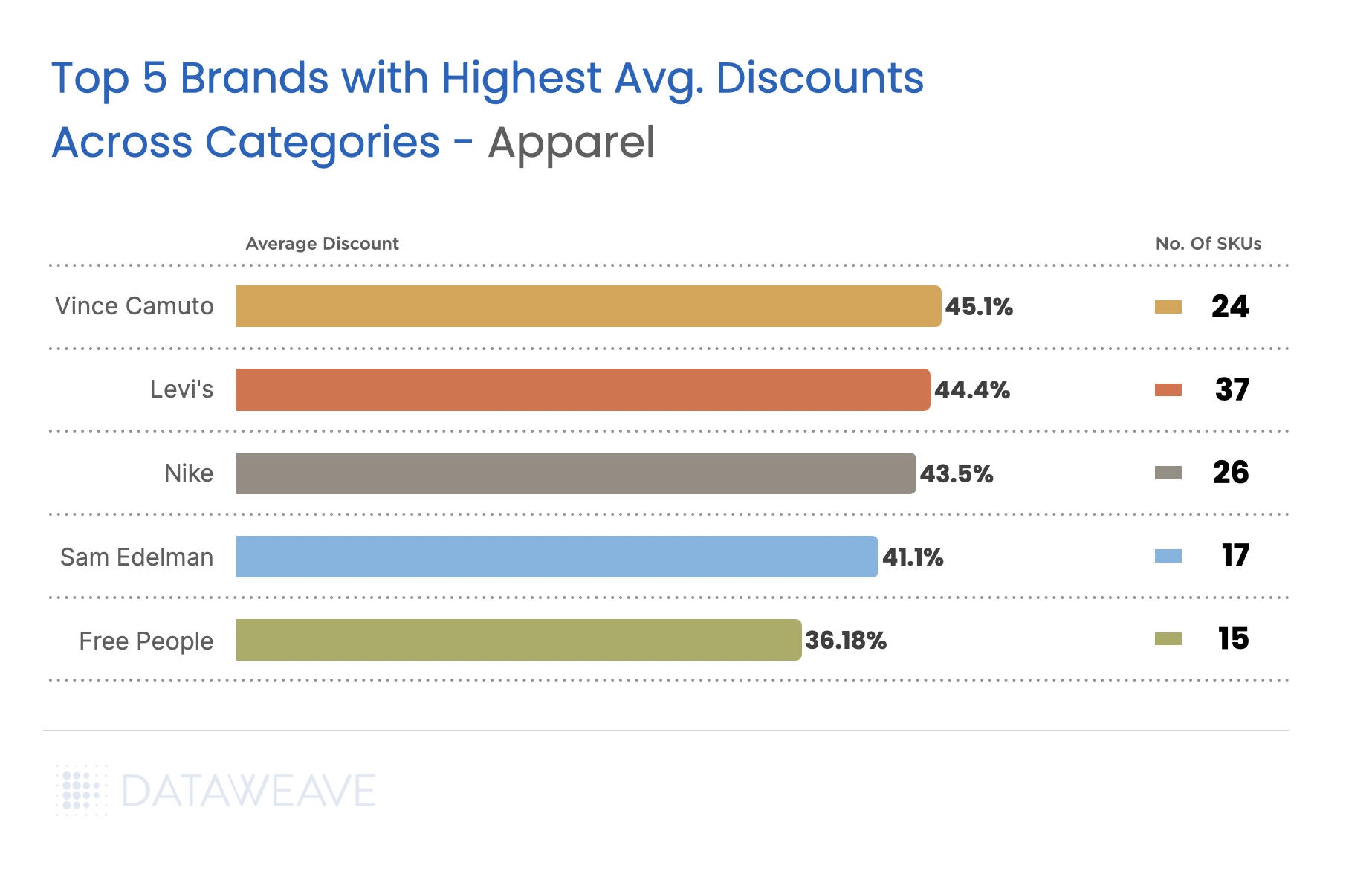

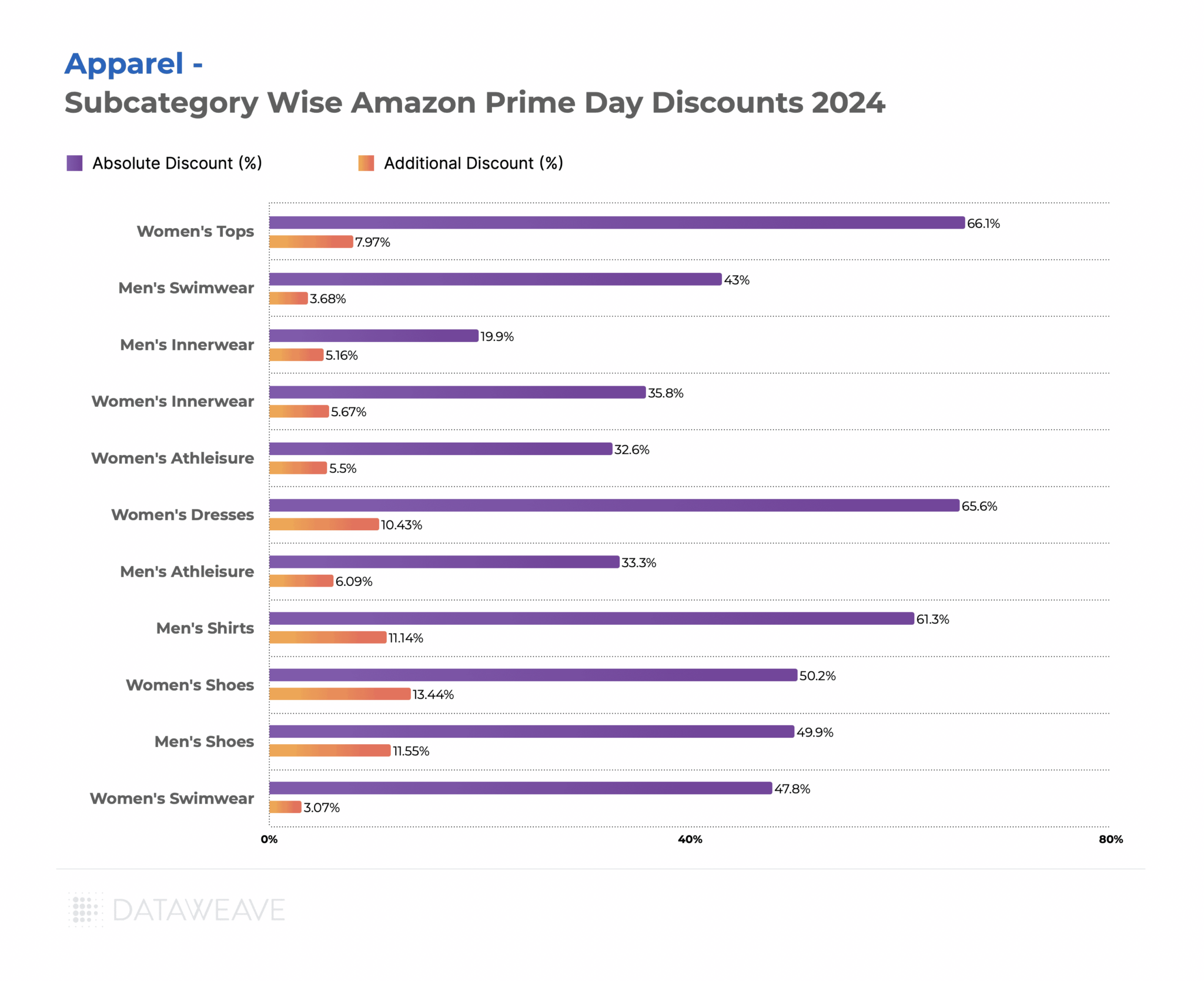

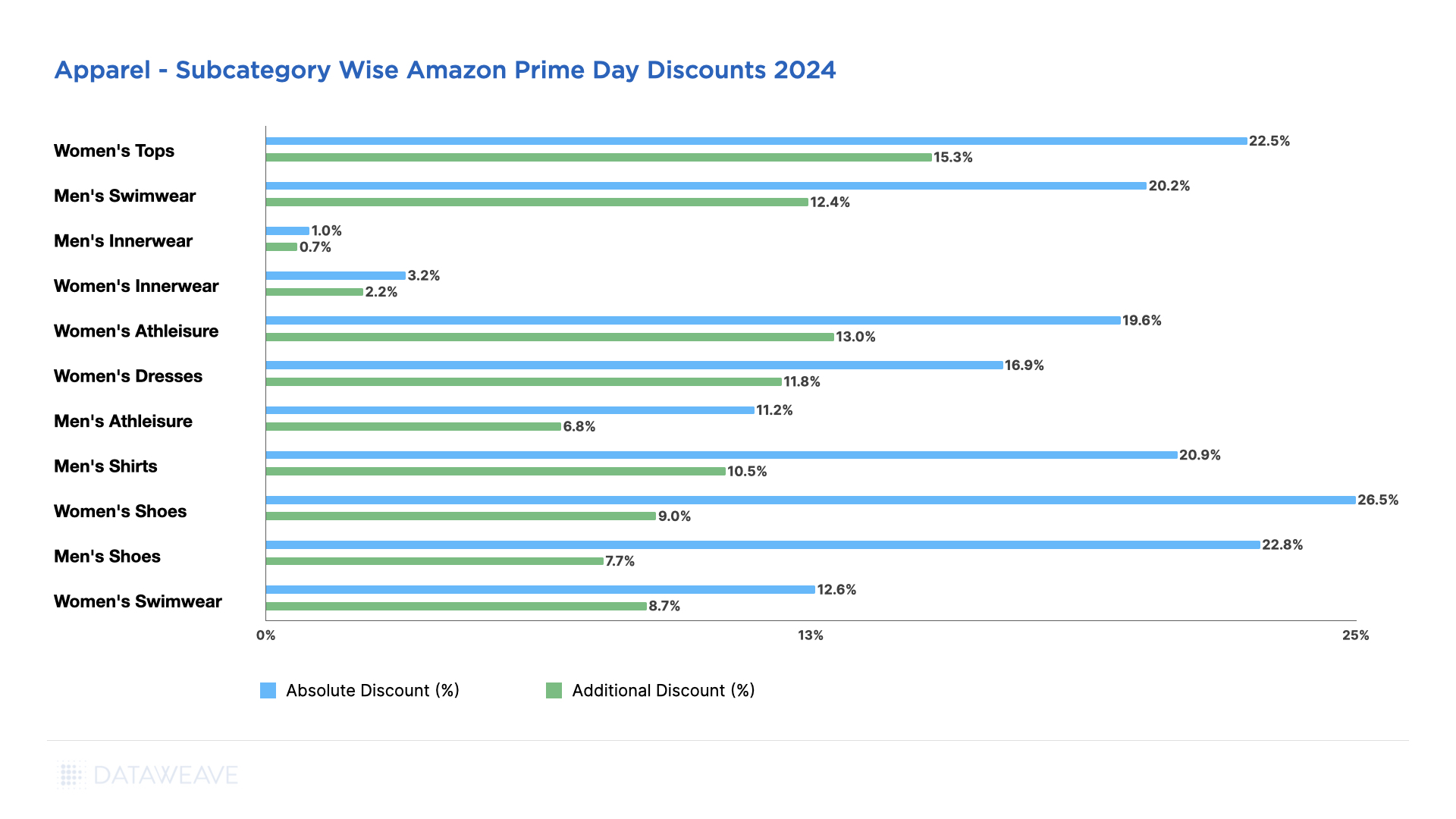

Apparel

Our analysis of 57,537 SKUs reveals interesting discount dynamics.

Subcategory Discount Analysis

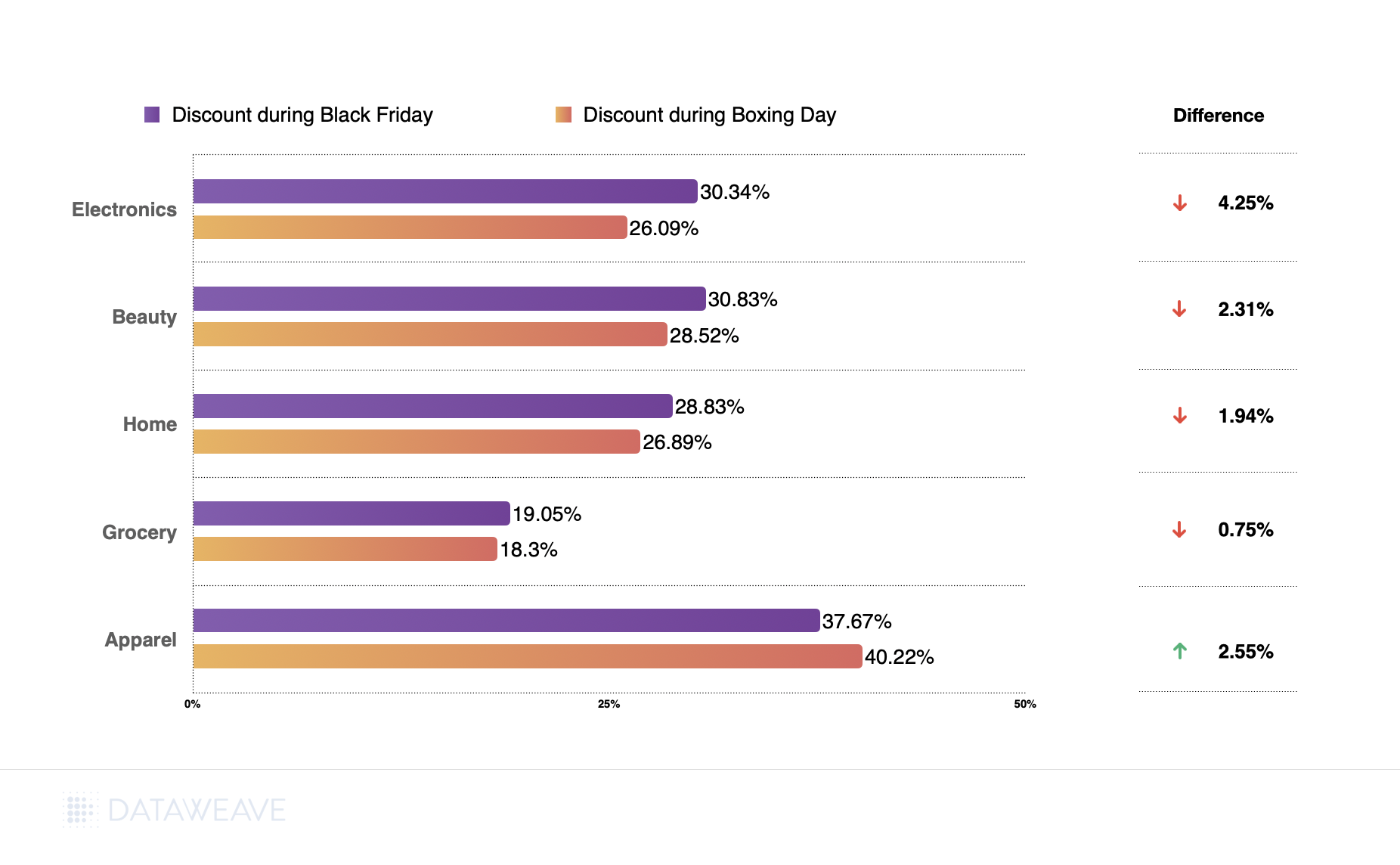

The category averaged 14.3% pre-Black Friday discounts with an additional 0.1% during Black Friday Week. Men’s Swimwear and Men’s Athleisure led pre-sale promotions at 22.2% and 18.5% respectively, while Women’s Swimwear and Women’s Shoes also saw strong pre event discounts at 19.3% and 17.6%.

Black Friday Week saw minimal incremental discounting across all subcategories, with most adding just 0.1-0.3%. The relatively subdued incremental discounting indicates that early birds captured the best deals, or that margins were already stretched from pre-sale promotions.

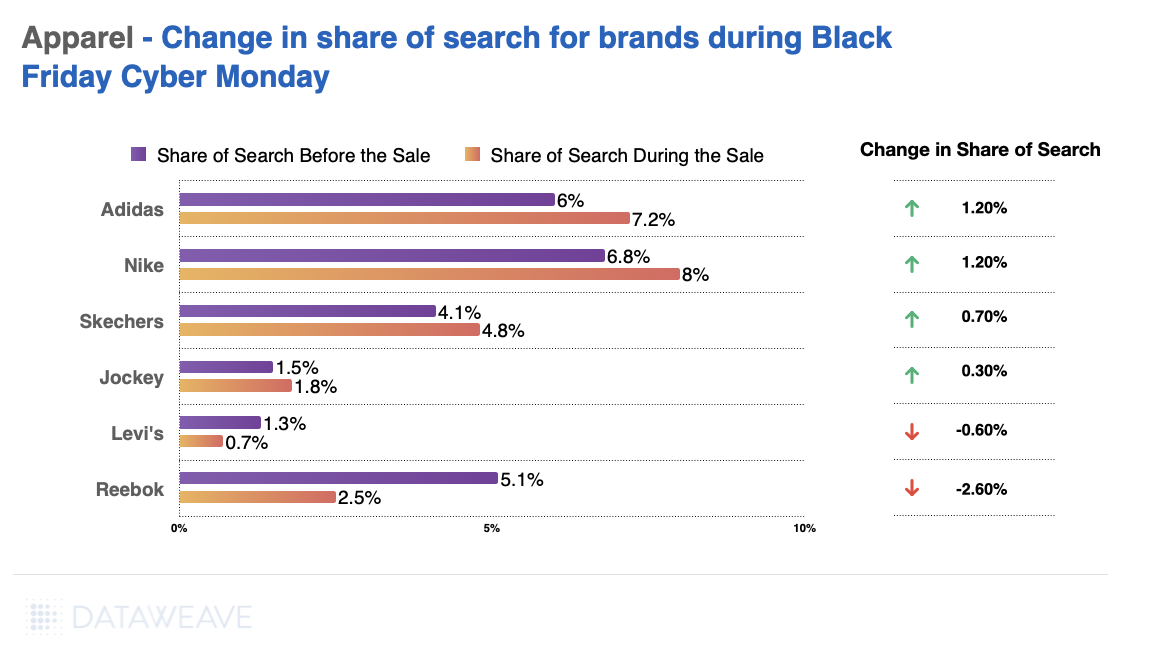

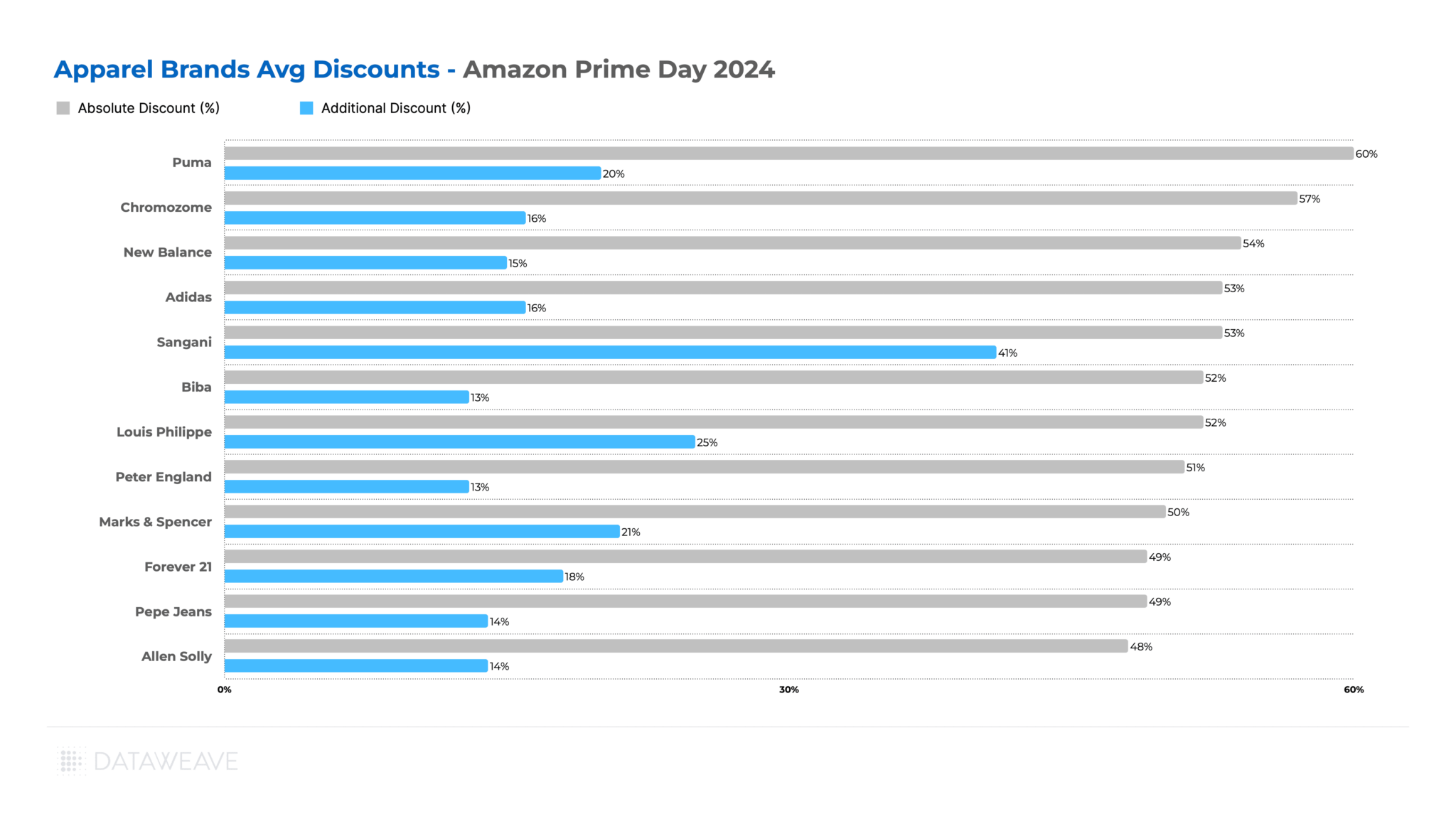

Share of Search: Brand Visibility Trends

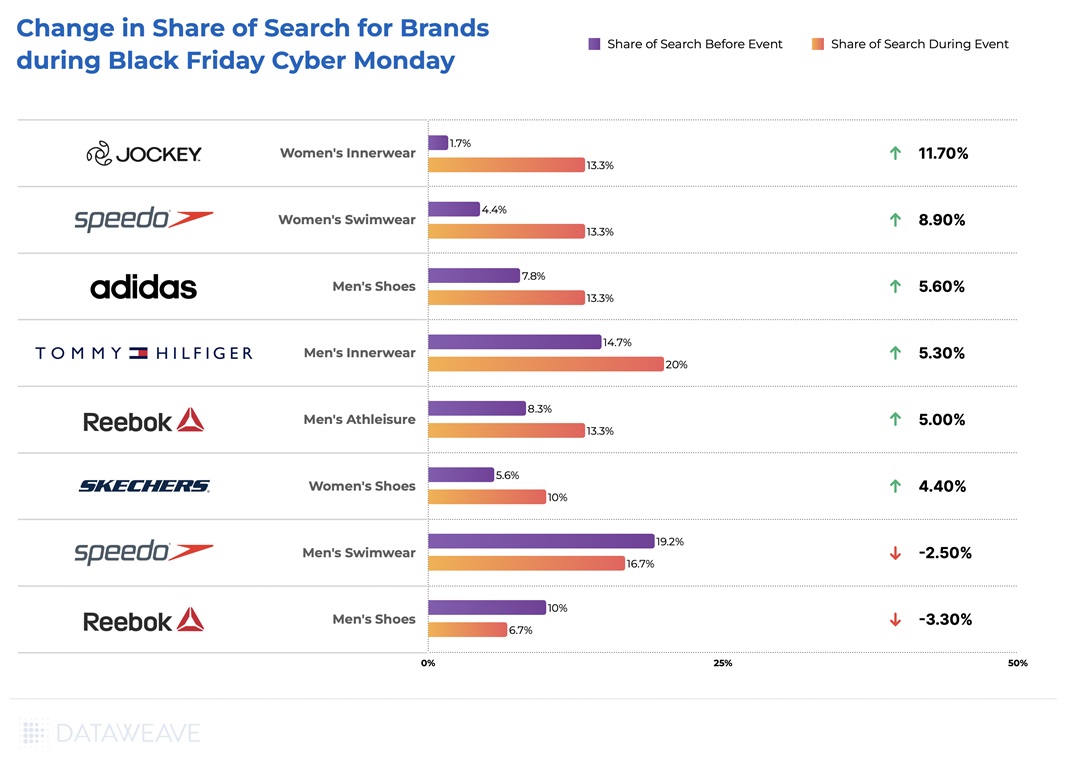

Pepe Jeans dominated visibility, surging from 7.4% to 24.6%, a staggering gain that represents the largest visibility increase across all categories. Jockey also performed strongly with a 6% gain, solidifying its position in innerwear.

On the flip side, athletic and footwear stalwarts faced headwinds: Speedo dropped 1.4% and Bata fell 1.1%. This data suggests that during Black Friday 2025 in India, denim and lifestyle fashion brands invested heavily in promotional visibility, capturing massive mindshare at the expense of traditional athletic and footwear brands.

For brands and retailers navigating India’s increasingly competitive e-commerce landscape, the 2025 Black Friday data reveals a critical insight: pre-sale positioning matters more than Black Friday Week discounting. Early promotional investment and visibility campaigns delivered far greater returns than late-stage price drops, fundamentally reshaping how brands should approach this shopping event.

Want to understand how DataWeave’s retail intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Check out our analysis on Black Friday 2025 Pricing and Discount trends in the USA, Canada, UK, and Germany. Follow our blog for more insights on retail pricing trends, brand visibility analysis, and data-driven commerce intelligence.

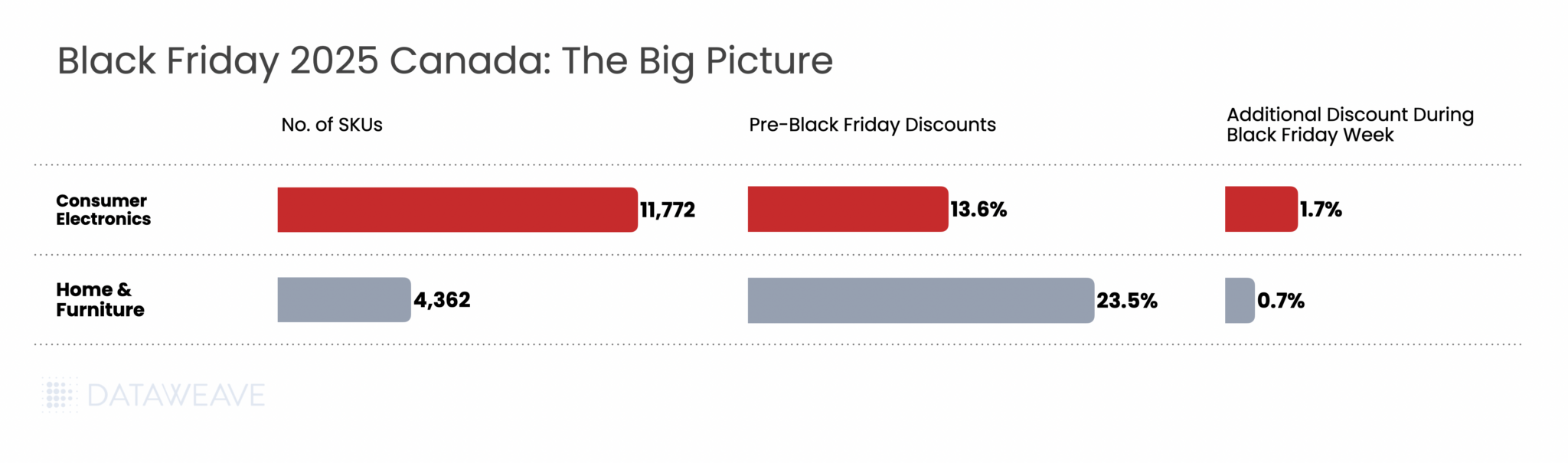

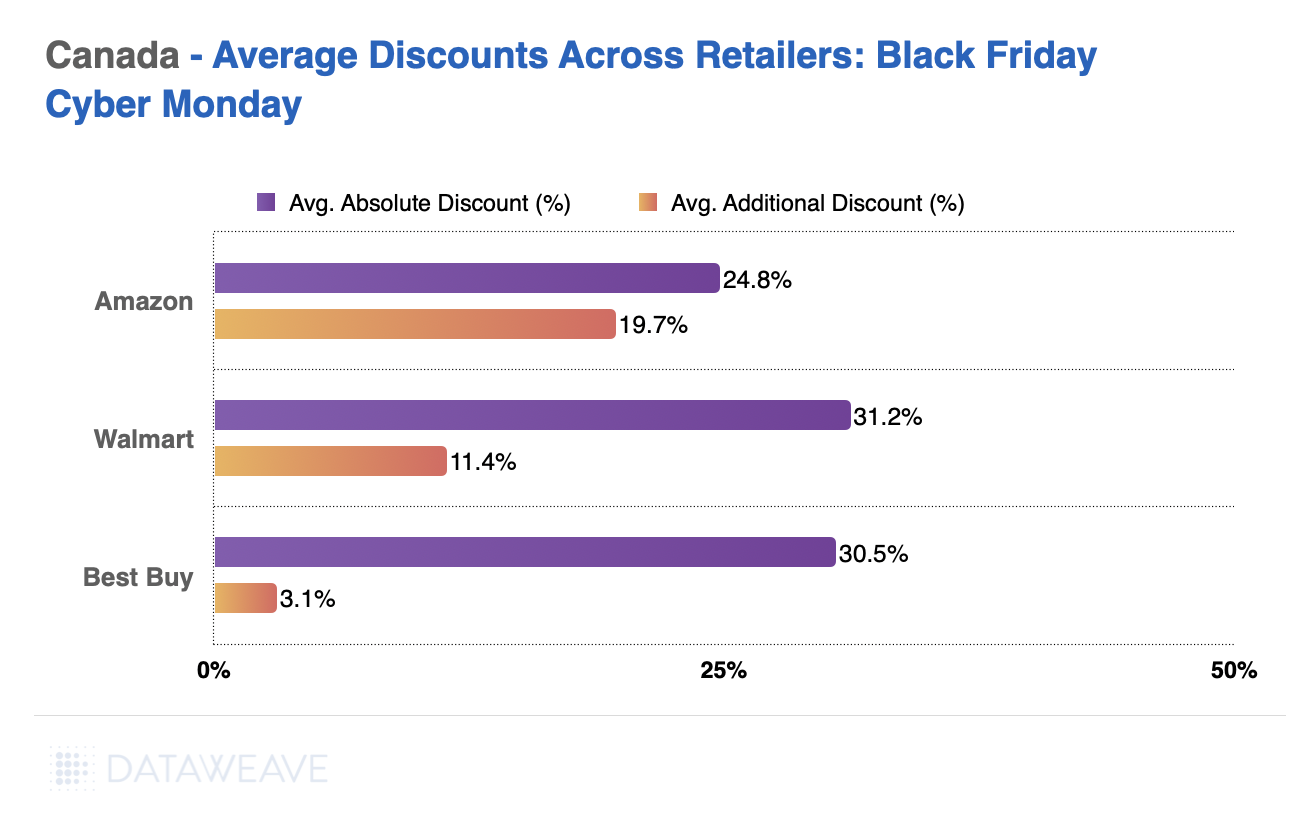

Black Friday 2025 marked another significant shopping event for Canadian consumers, with retailers deploying sophisticated pricing strategies to capture holiday spending. Online and in-store spending on Black Friday reached an estimated $865 million in Canada, which marked a 6% increase compared to last year.

At DataWeave, we analyzed Black Friday 2025 pricing dynamics across two major categories in the Canadian market: Consumer Electronics and Home & Furniture. Our AI-powered pricing intelligence platform tracked approximately 16,000 SKUs across leading Canadian retailers like Target, Walmart, Wayfair, Home Depot, Amazon, Best Buy, Loblaws, Metro and more, uncovering distinct patterns in how brands and retailers structured their promotional calendars this year.

Our Methodology

DataWeave monitored pricing and discount trends across Canadian retailers during two key timeframes:

Pre-Black Friday Period: Up to November 23, 2025 – establishing baseline promotional activity and early holiday deals

Black Friday Week: November 24 – December 1, 2025 – spanning Thanksgiving through Black Friday (November 28) and Cyber Monday (December 1)

Our dataset included top-performing products across multiple subcategories on major Canadian retail platforms. We also tracked Share of Search metrics, measuring brand prominence by analyzing which brand names appeared in the top 20 search results for high-value keywords during each period.

Black Friday 2025 Canada: Overview

Here’s how average discounts compared between the Pre-Black Friday period and Black Friday Week:

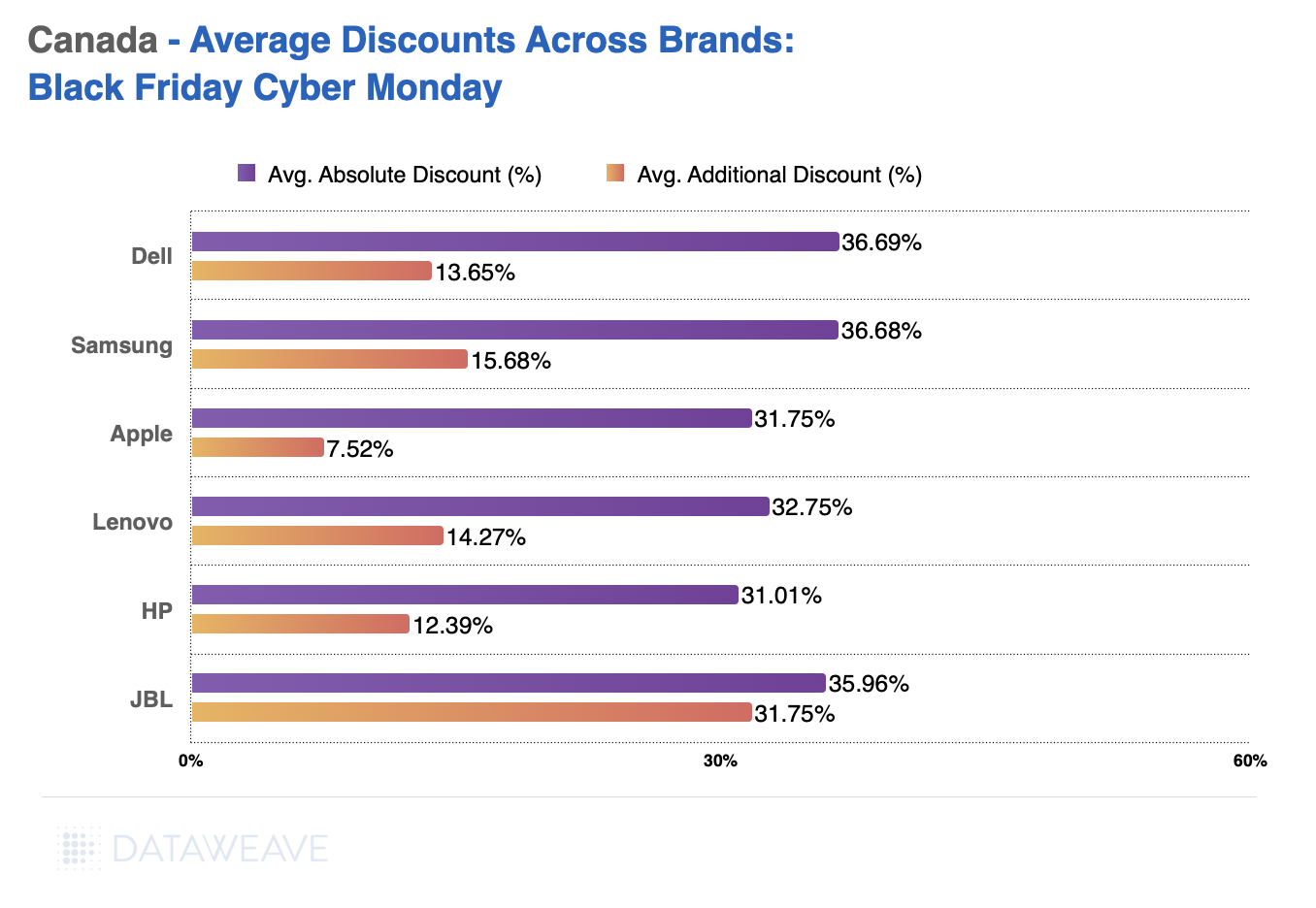

Key Finding: Canadian retailers front-loaded their promotional strategy significantly, with Pre-Black Friday discounts averaging 16.3% across categories. The additional lift during Black Friday Week was modest at 1.4%.

Consumer Electronics

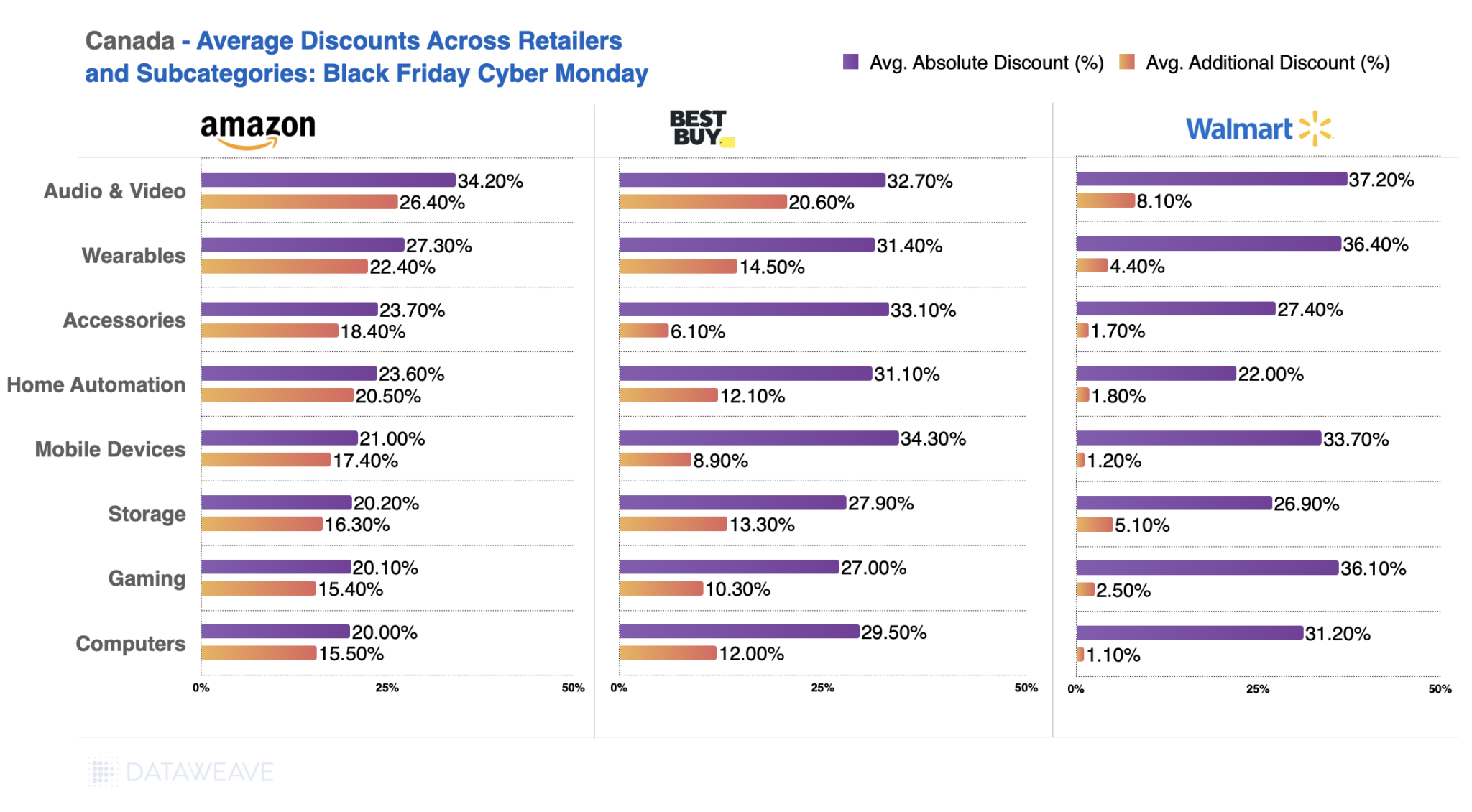

Consumer electronics consistently drives Black Friday traffic, and Canadian retailers delivered compelling early-season value. Our analysis of 11,772 SKUs reveals nuanced subcategory performance.

Subcategory Discount Breakdown

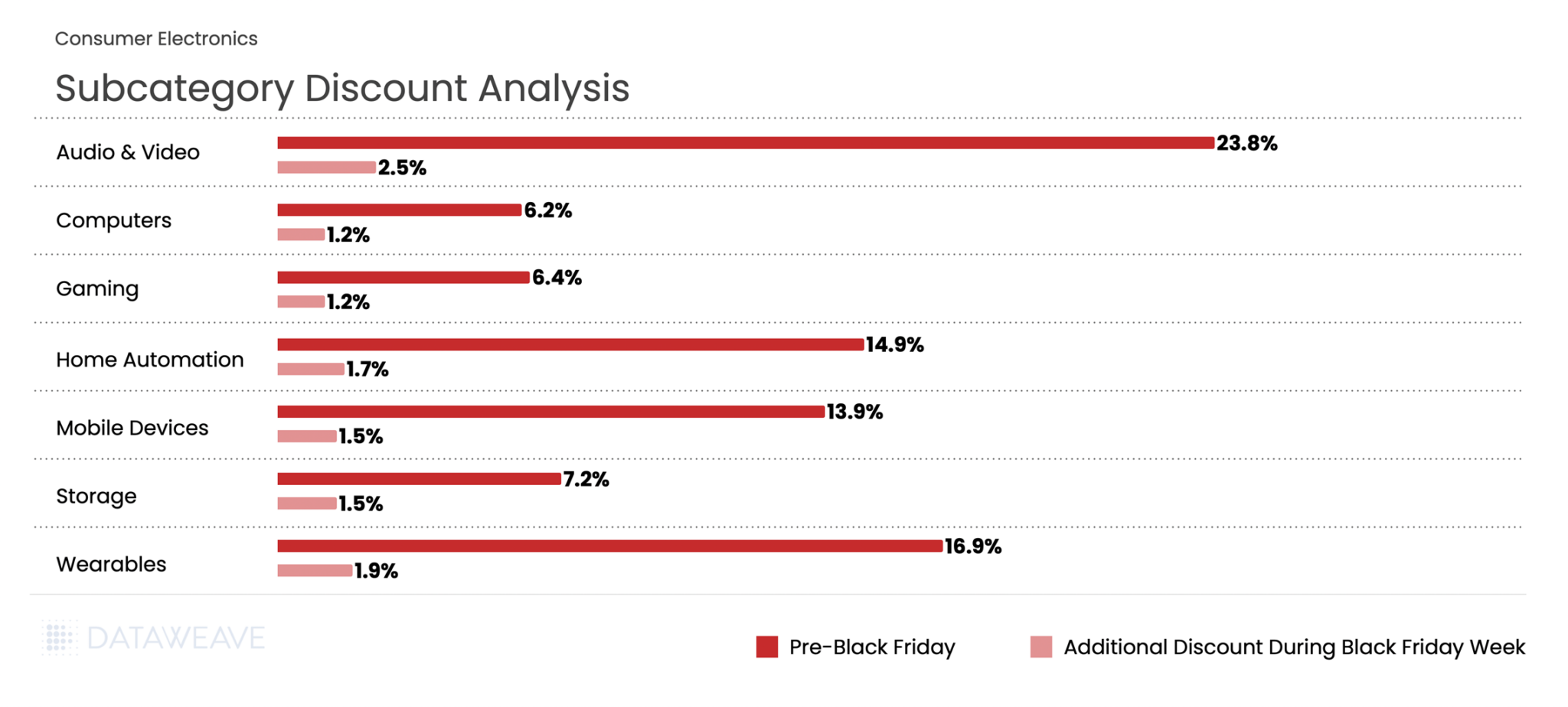

Consumer Electronics averaged 13.6% discounts in the Pre-Black Friday period, with Black Friday Week adding 1.7%. Audio & Video dominated early promotional activity at 23.8%, signalling retailers’ intent to clear inventory ahead of the main event. Wearables followed at 16.9%, likely timed to capture gift-buying momentum.

During Black Friday Week, Audio & Video maintained leadership with an additional 2.5% discount, the highest incremental lift in the category. Meanwhile, Computers and Gaming, already positioned at modest pre-sale discounts of 6.2% and 6.4%, saw minimal additional movement, suggesting constrained inventory or deliberate pricing discipline in these segments.

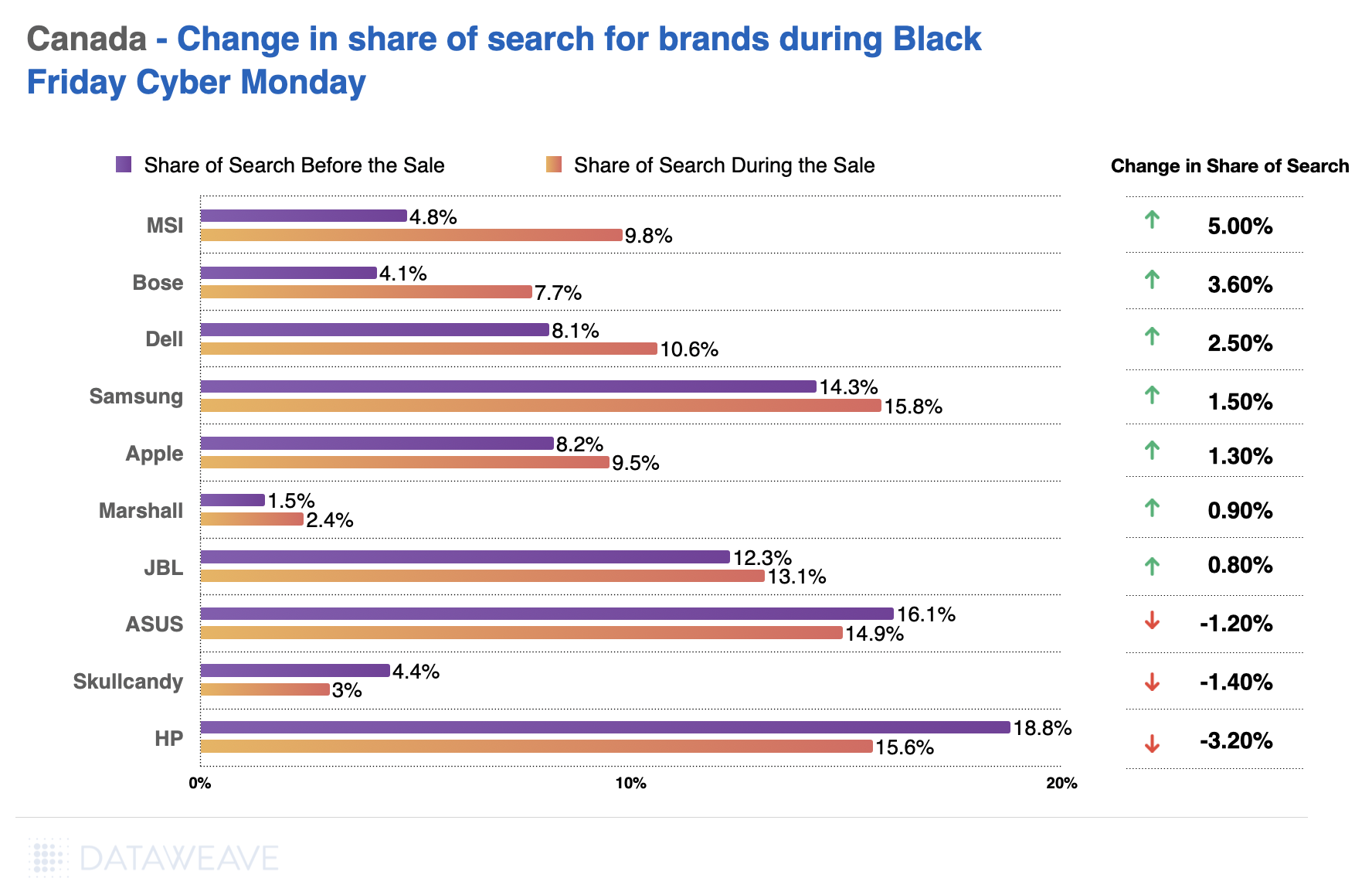

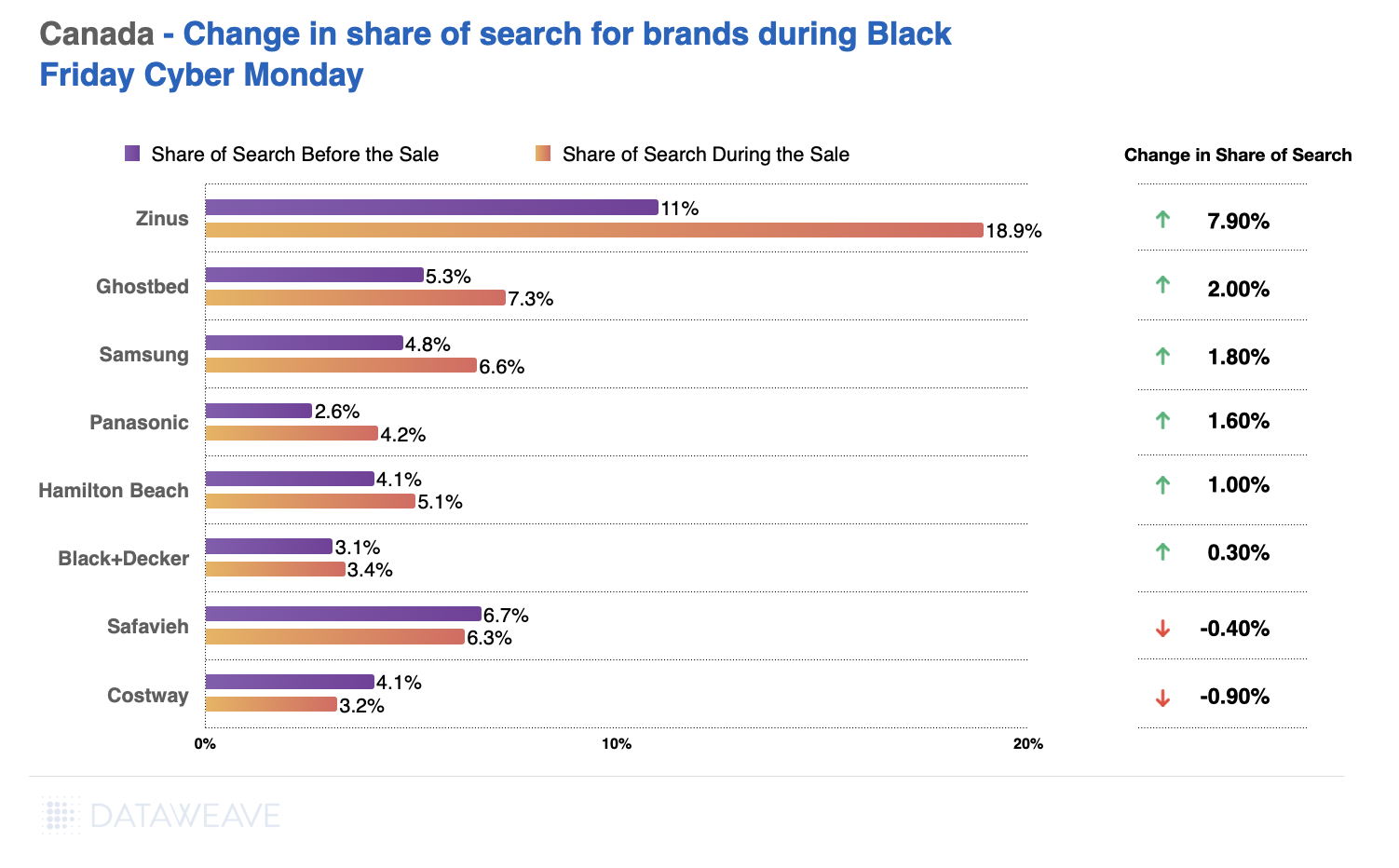

Share of Search: Brand Visibility Trends

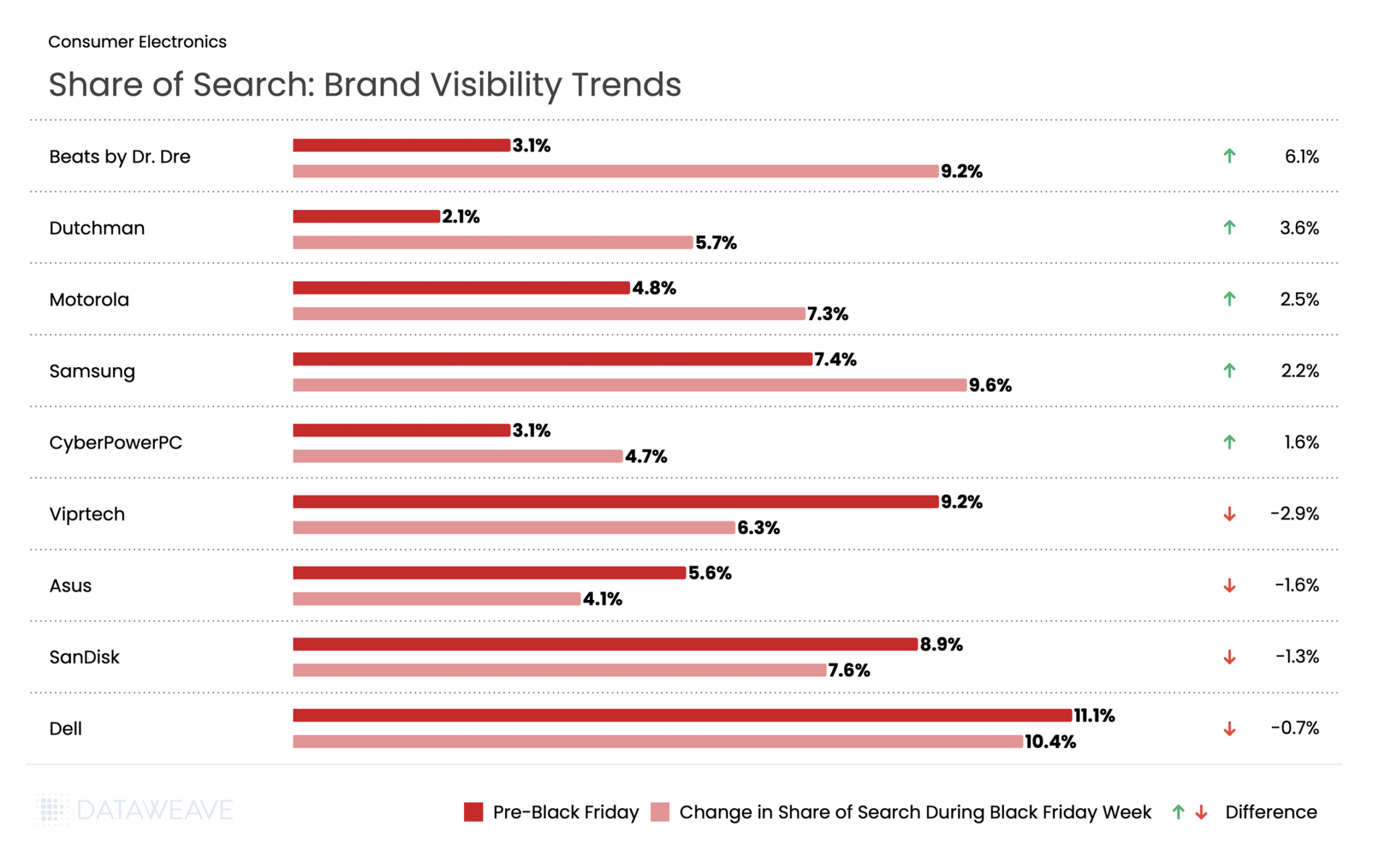

Our Share of Search data reveals which brands gained or lost prominence during Black Friday Week:

Audio brands dominated visibility gains during Black Friday Week. Beats by Dr. Dre nearly tripled its Share of Search from 3.1% to 9.2%, showing the strongest gains. Visibility for Dutchman climbed 3.6%. Motorola and Samsung also captured increased search prominence with gains of 2.5% and 2.2% respectively.

Conversely, some established tech brands experienced visibility declines. Gaming brand Viprtech by 2.9%. Asus declined by 1.6%, and SanDisk dropped by 1.3%.

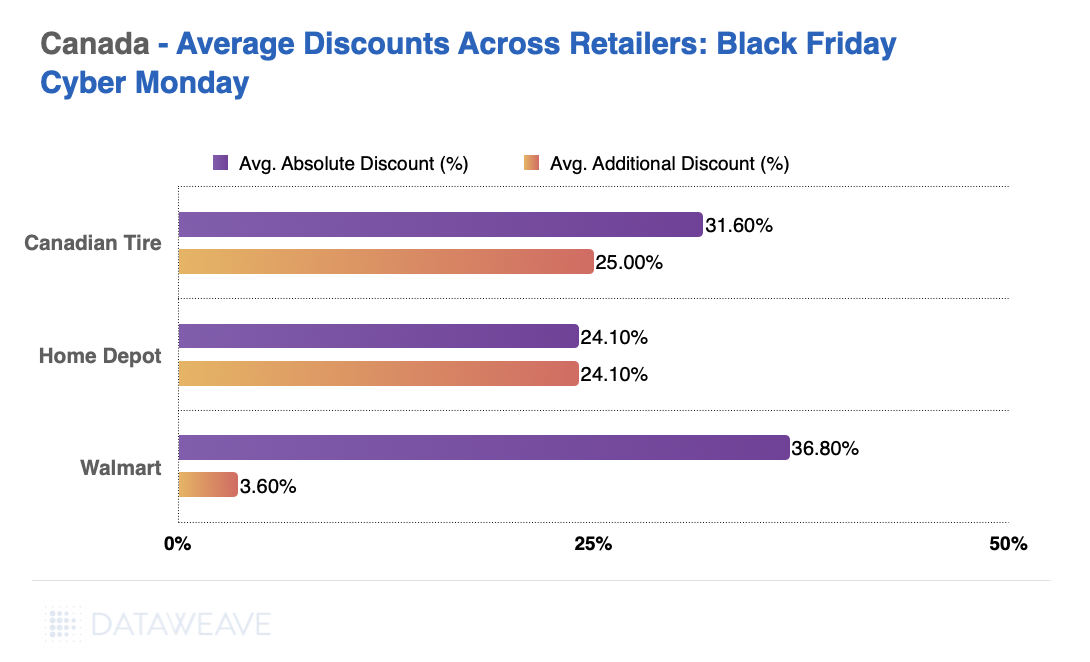

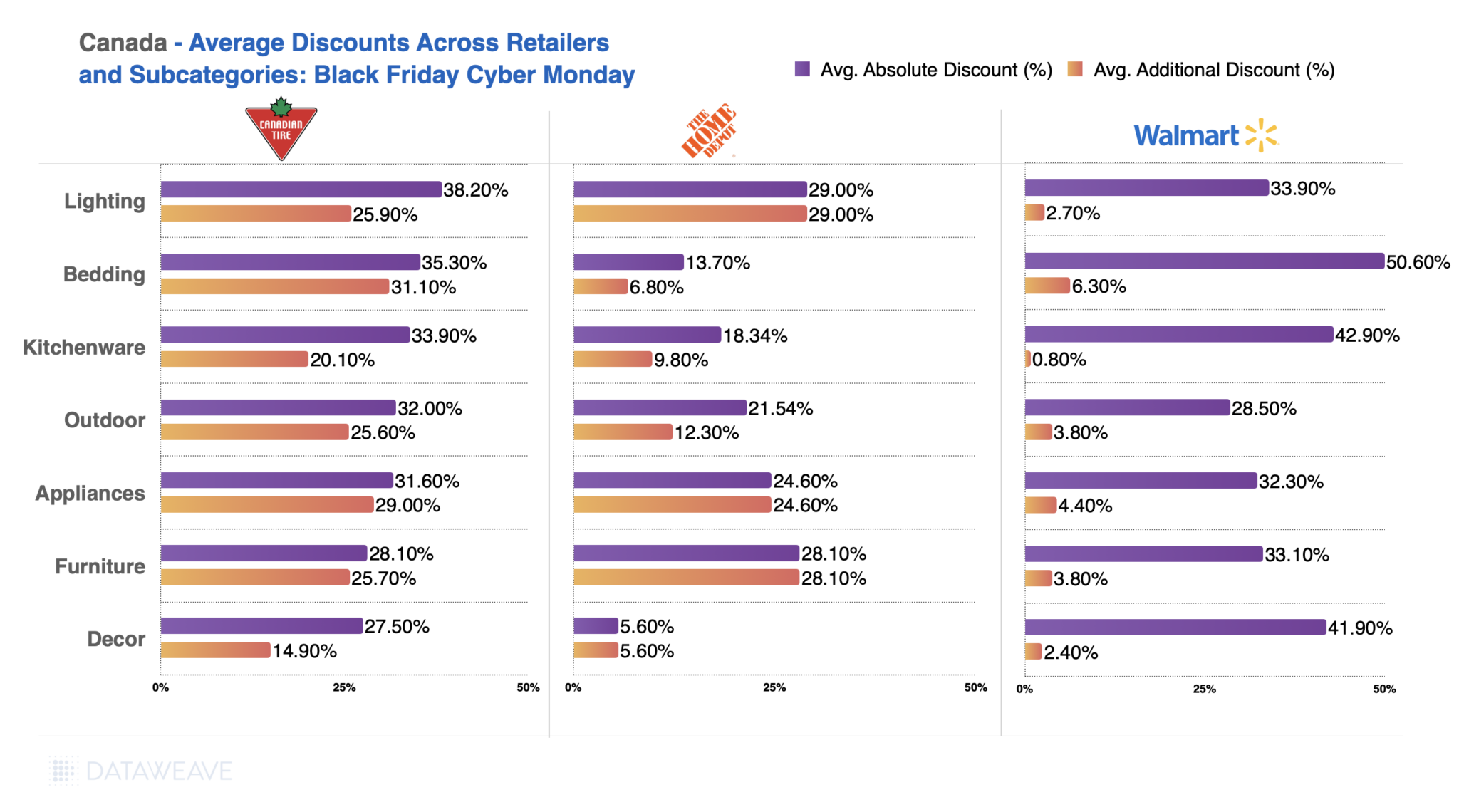

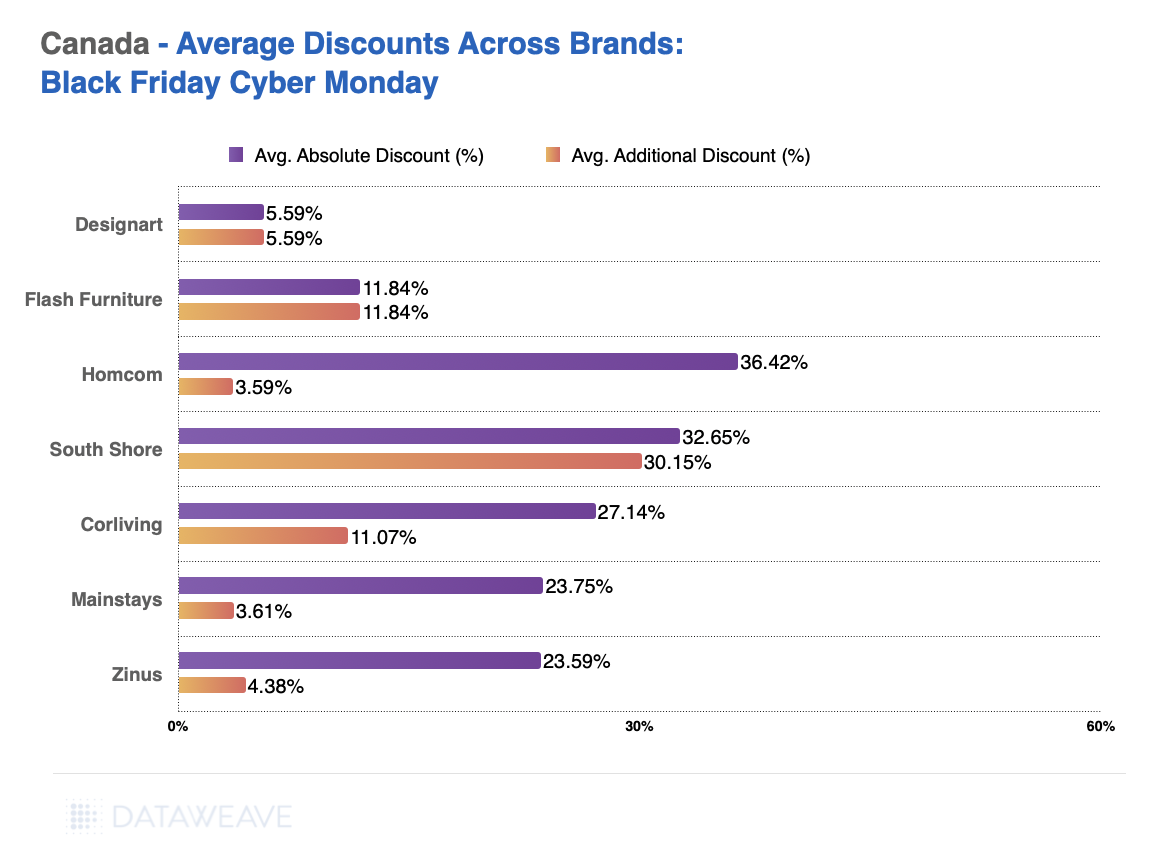

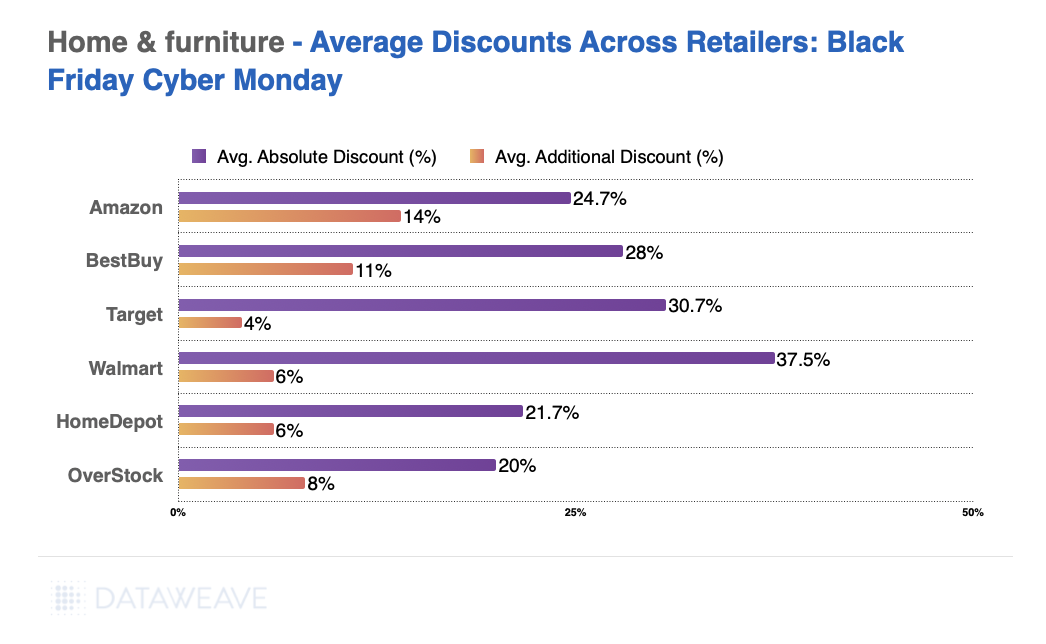

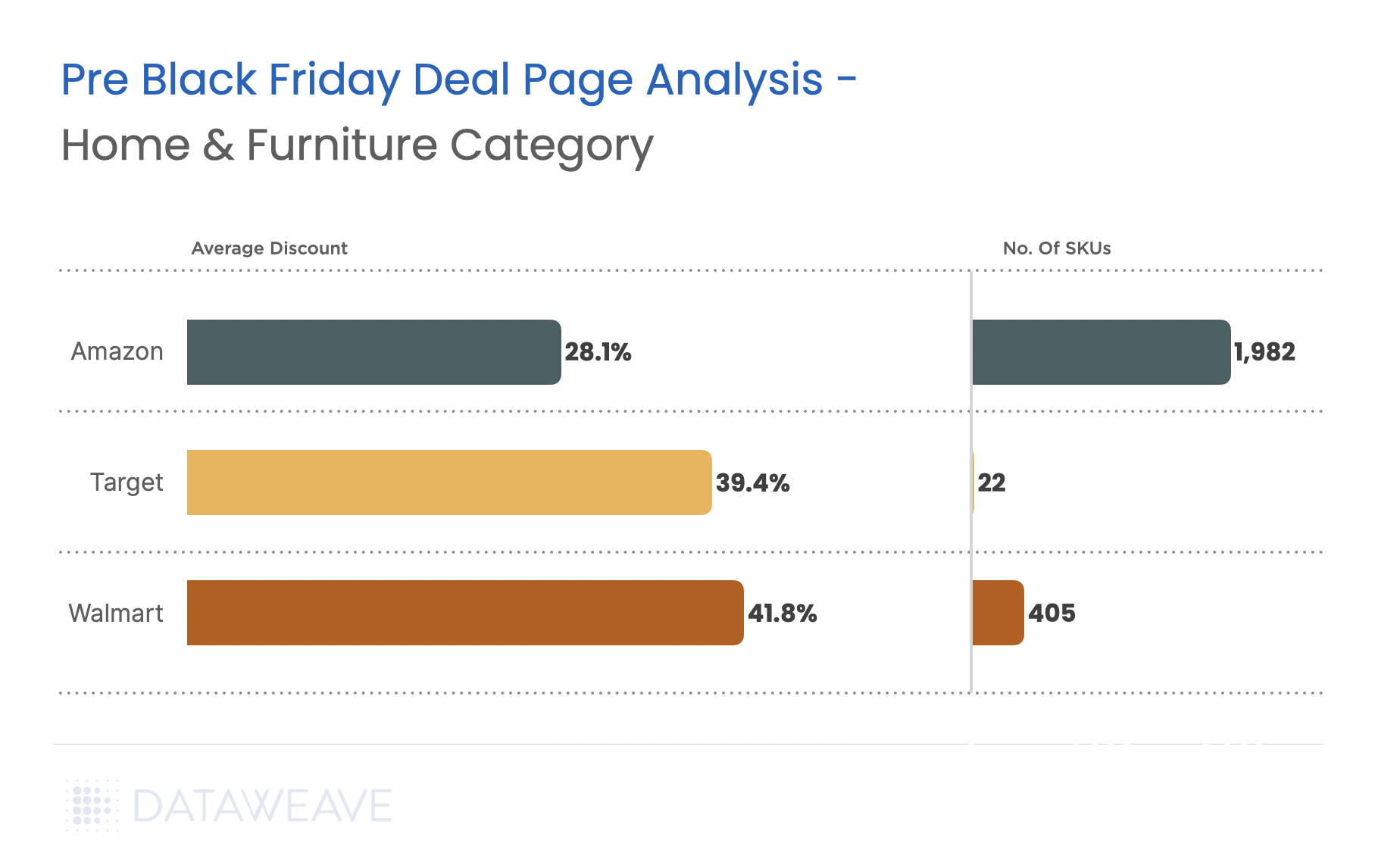

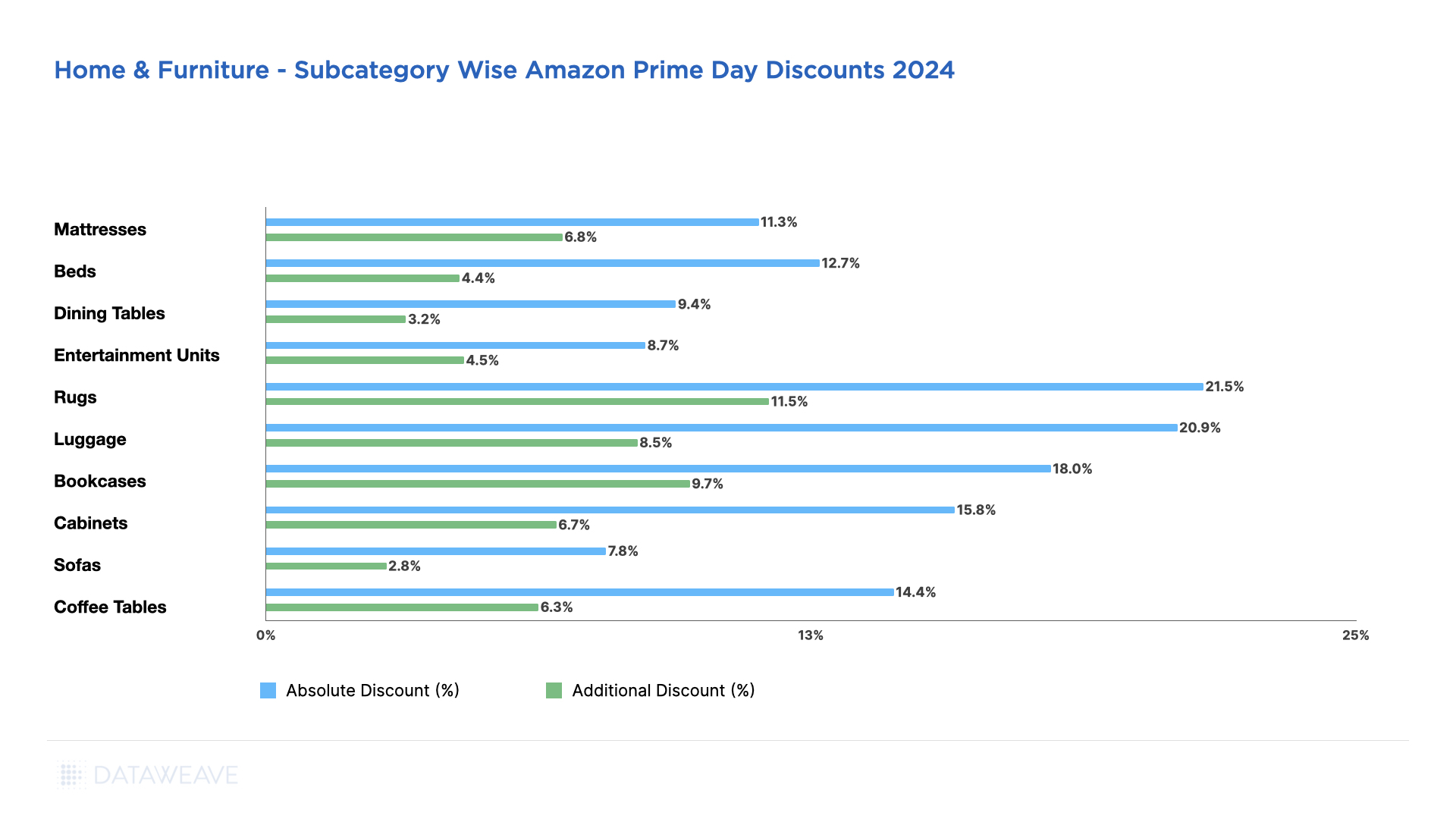

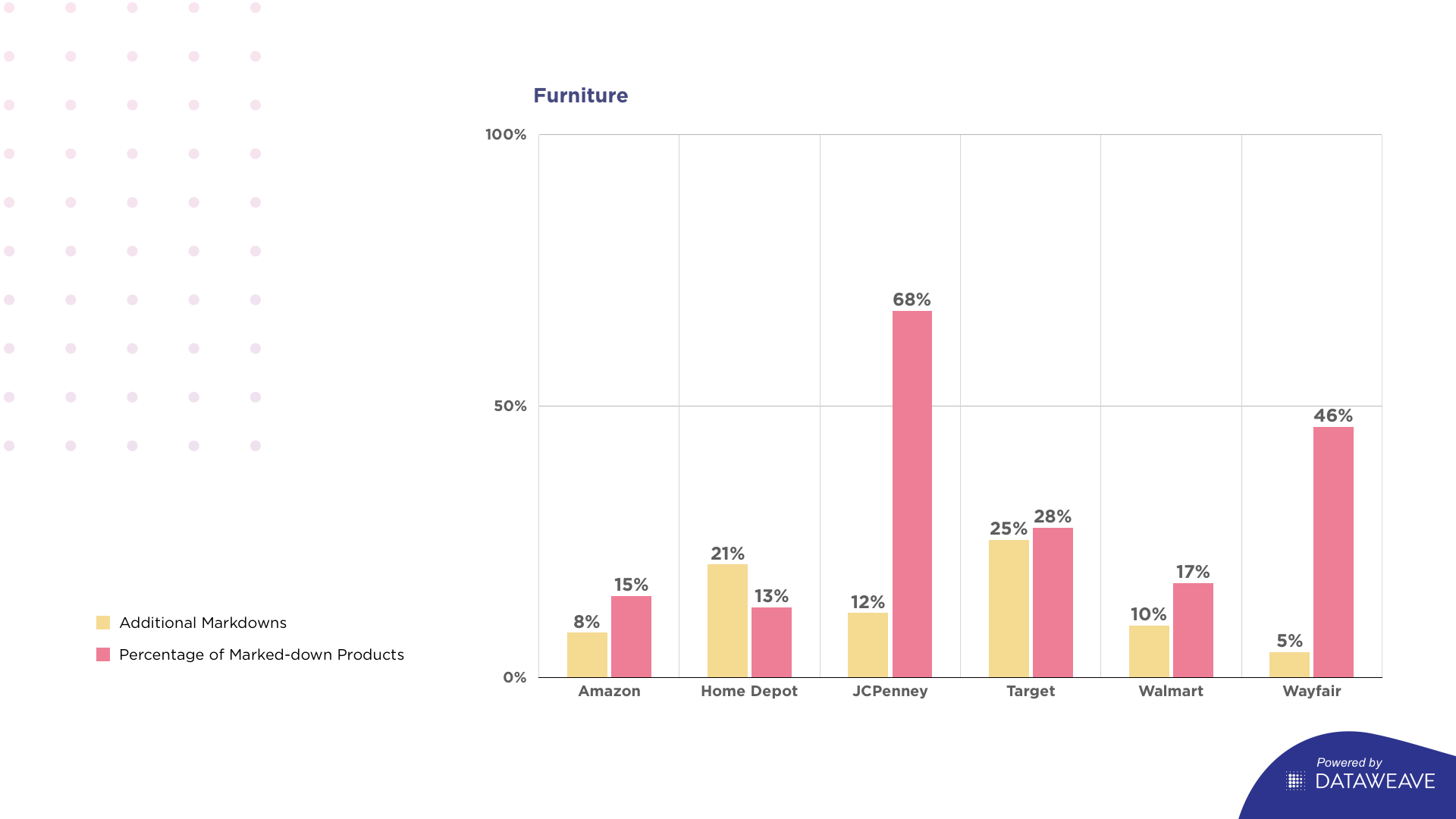

Home & Furniture

Home & Furniture showed the most aggressive early discounting of any category in our Canadian analysis. Tracking 4,362 SKUs, we found retailers heavily promoted home goods well before Black Friday weekend.

Subcategory Discount Breakdown

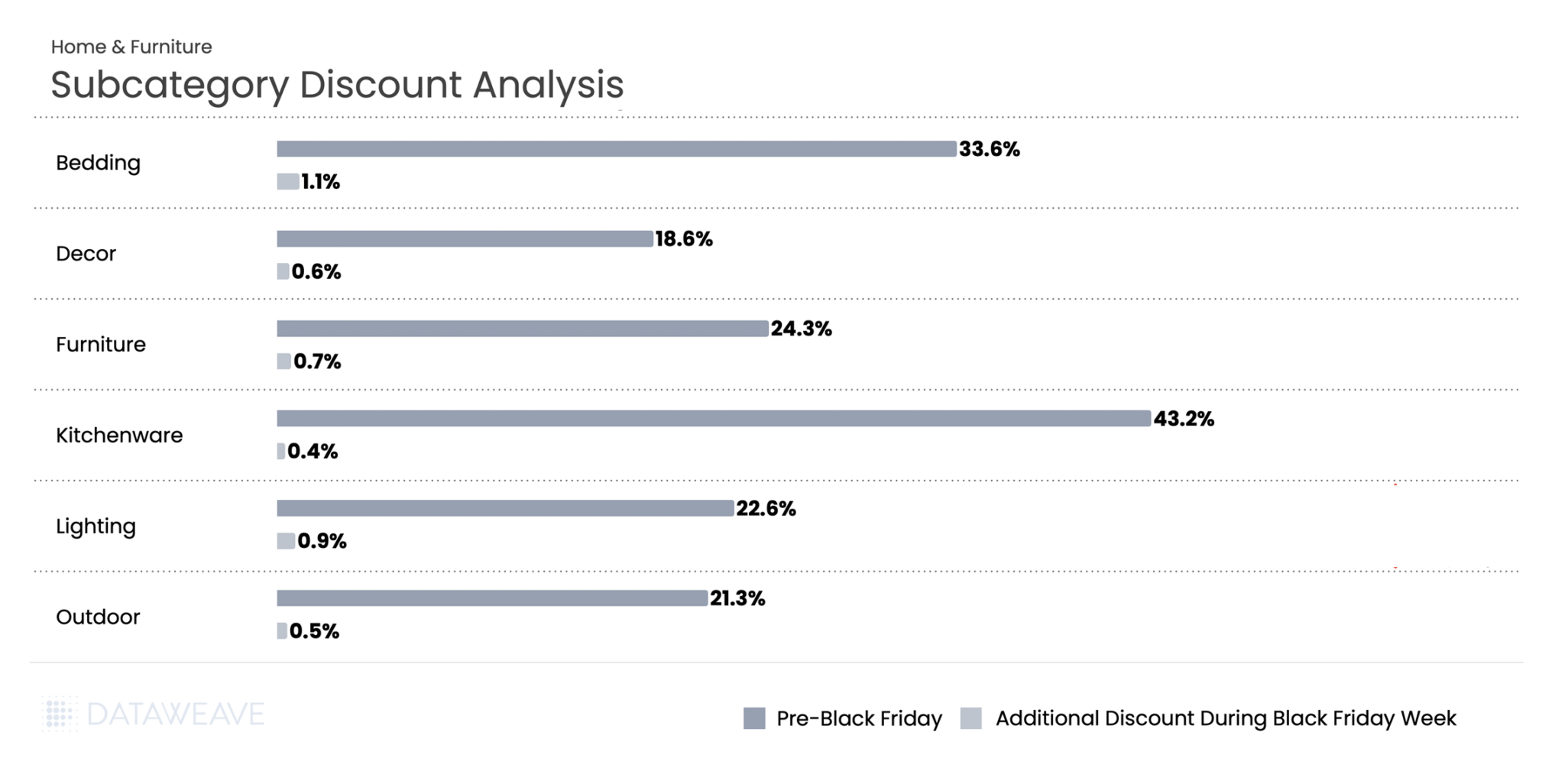

Home & Furniture led all categories with Pre-Black Friday discounts averaging 23.5%, but Black Friday Week added only 0.7%, the smallest incremental discount in our entire study. Kitchenware saw extraordinary pre-sale discounts of 43.2%, the highest in any subcategory we tracked. Bedding followed at 33.6%, while Furniture reached 24.3%. These deep early discounts likely aimed to drive early conversions and manage bulky inventory ahead of peak logistics constraints.

During Black Friday Week, additional discounting remained minimal across the board. Bedding posted the highest lift at 1.1%, while Kitchenware saw just 0.4%. The data suggests Canadian home goods retailers viewed the pre-sale period as their primary promotional window, with Black Friday serving more to sustain momentum than deliver new value.

Share of Search: Brand Visibility Trends

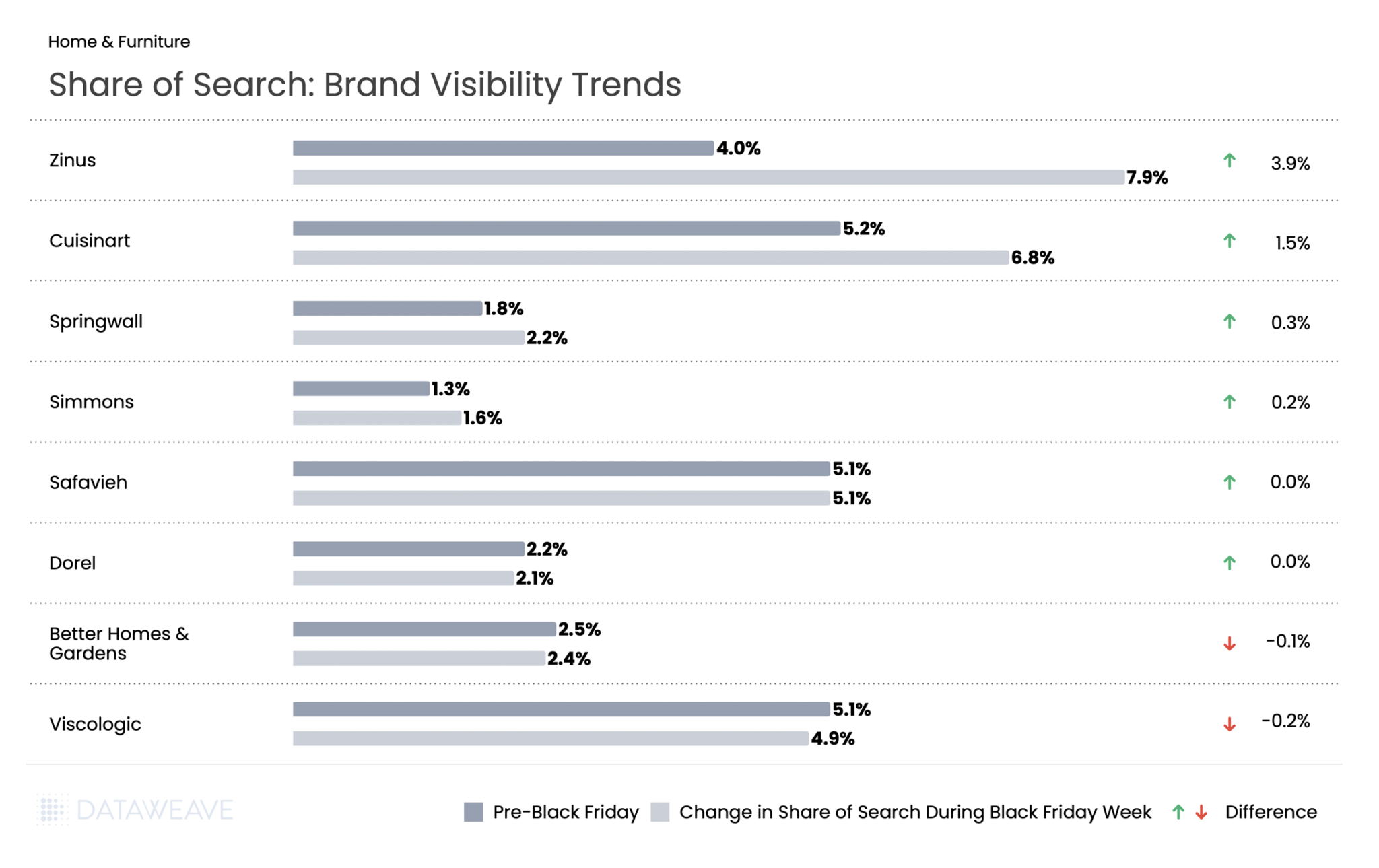

Mattress brand Zinus led gains with a 3.9% increase, positioning itself as a value-focused furniture leader during the sale period. Cuisinart climbed by 1.5%, suggesting strategic amplification of this established kitchenware brand.

Most home brands maintained relatively stable visibility throughout the sale period. Safavieh and Dorel showed essentially no change, while Better Homes & Gardens and Viscologic experienced only minor declines of 0.1% and 0.2% respectively.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Check out our coverage on Black Friday 2025 across US, UK, and Germany. Follow our blog for more insights on retail pricing trends, brand visibility analysis, and data-driven commerce intelligence.

Black Friday 2025 solidified its position as a major retail event in the German market. German consumers demonstrated an average Black Friday budget of €317, the highest among select European countries.

The German market, however, exhibited unique consumer behavior patterns during Black Friday 2025. Rather than meticulous planning, 59% of German shoppers allowed deals to inspire their purchases, compared to just 32% who shopped with predetermined lists and budgets. This spontaneous yet budget-conscious approach distinguishes German consumers from other markets, where FOMO-driven purchasing tends to dominate.

Against this backdrop of rational deal-seeking and regional diversity, how did retailers and brands perform across key categories this Black Friday?

At DataWeave, we conducted a comprehensive analysis of Black Friday 2025 discounting trends across five major categories in the German market: Consumer Electronics, Home & Furniture, Health & Beauty, Grocery, and Apparel. Our AI-powered pricing intelligence platform monitored over 16,000+ SKUs across leading German retailers like Amazon, Aldi, Douglas, Nutritienda, Carethy, Bofrost, and more, revealing fascinating patterns in how retailers and brands approached this year’s sale season.

Our Methodology

For this analysis, DataWeave monitored average discounts across leading German retailers during two distinct periods:

Pre-Black Friday: November 6 – November 23, 2025 – capturing early holiday deals and baseline pricing

Additional Discounts During Black Friday Week: November 24 – December 1, 2025 – covering Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

Our sample encompassed the top-ranked products across subcategories on major retail sites. We also analyzed Share of Search data, which measures brand visibility by monitoring which brand names appear in the top 20 search results for critical keywords.

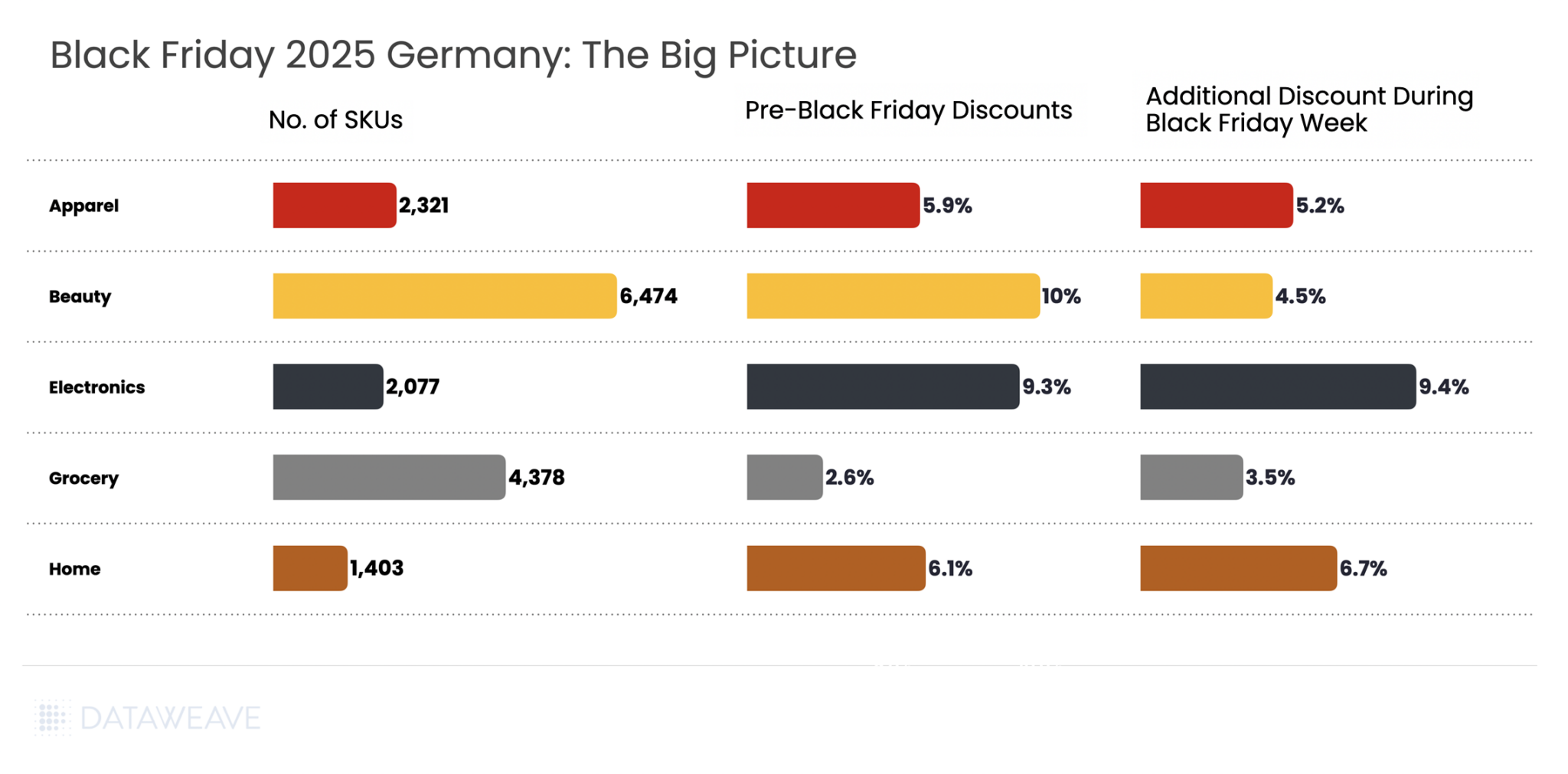

Black Friday 2025 Germany: The Big Picture

Our analysis covered 16,653 SKUs across five major categories. Here’s the snapshot of average discounts during the Pre-Black Friday period compared to Black Friday Week:

Key Insight: The German market presented a notably different discounting pattern compared to other markets. Pre-Black Friday discounts averaged 7% across all categories, with Black Friday Week adding 5.1% on average. Unlike the UK and US markets where retailers front-loaded promotions heavily, German retailers took a more balanced approach, with several categories actually seeing higher discounts during the main Black Friday Week.

Beauty led pre-sale discounts at 10%, followed by Electronics at 9.3%. Consumer electronics stood out with the highest Black Friday Week discounts at 9.4%, slightly exceeding even the pre-sale period at 9.3%.

Shopping Behavior Patterns: The relatively modest discount levels reflect the rational, value-oriented approach of German consumers. With the majority of shoppers setting budgets between €100-€299 and prioritizing wish fulfillment over impulse purchases, German retailers focused on strategic discounting rather than aggressive margin erosion.

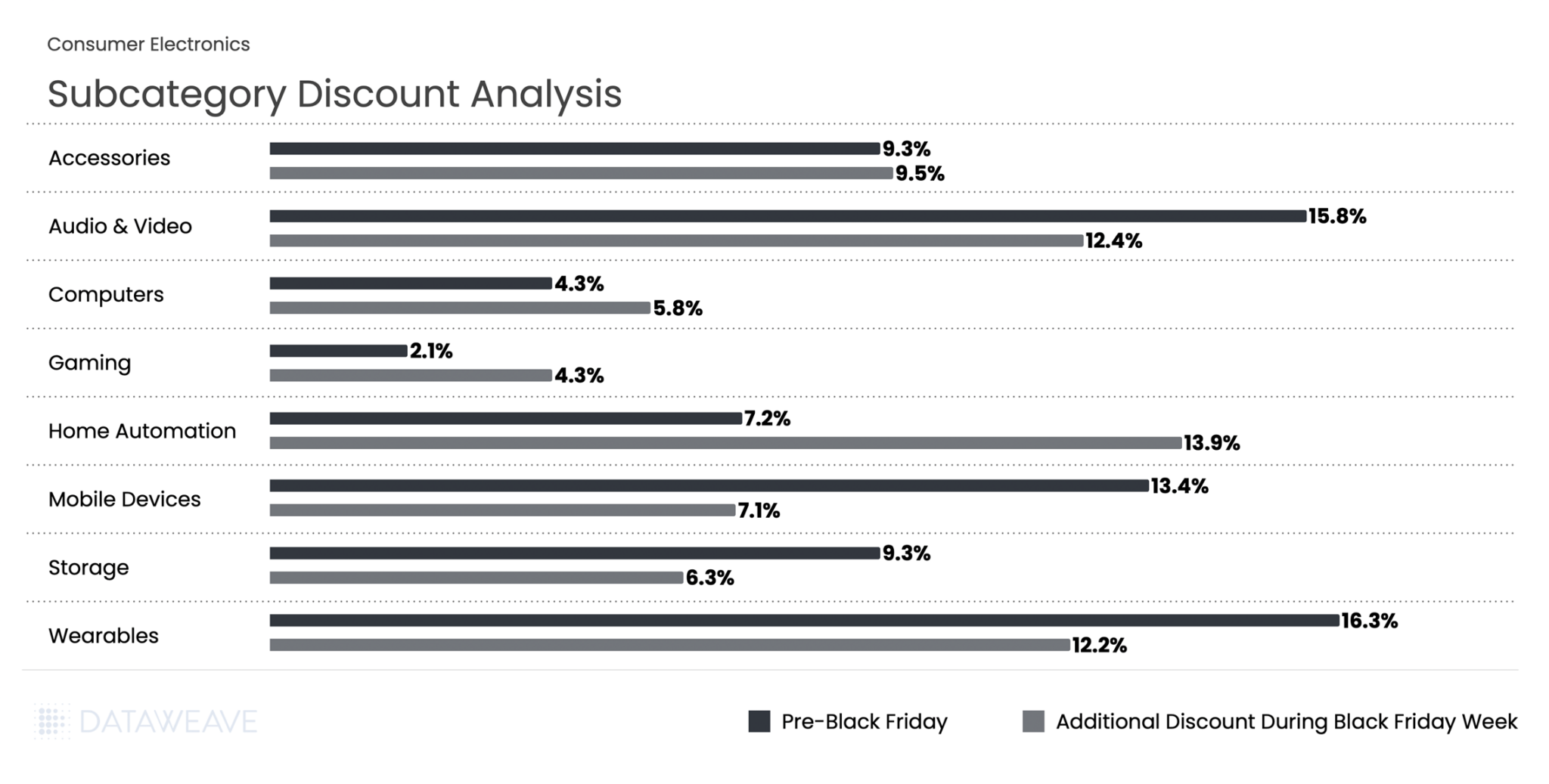

Consumer Electronics

Consumer electronics dominated German Black Friday interest, with 77% of German shoppers most interested in electronics deals, making it the most anticipated category during the sales period. Our analysis of 2,077 SKUs reveals how discounts varied across subcategories and which brands dominated search visibility in this highly competitive category.

Subcategory Discount Analysis

This was one of the few categories where Black Friday Week discounts matched or exceeded pre-sale levels. Wearables led pre-sale discounting at 16.3%, followed closely by Audio & Video at 15.8%. During Black Friday Week, these categories saw additional discounts of 12.2% and 12.4% respectively.

The standout performer was Home Automation, which nearly doubled its additional discount from 7.2% to 13.9% during Black Friday Week. Mobile Devices saw additional discounts dropping from 13.4% pre-sale to 7.1% during Black Friday Week. Meanwhile Gaming doubled additional discounting from 2.1% to 4.3%.

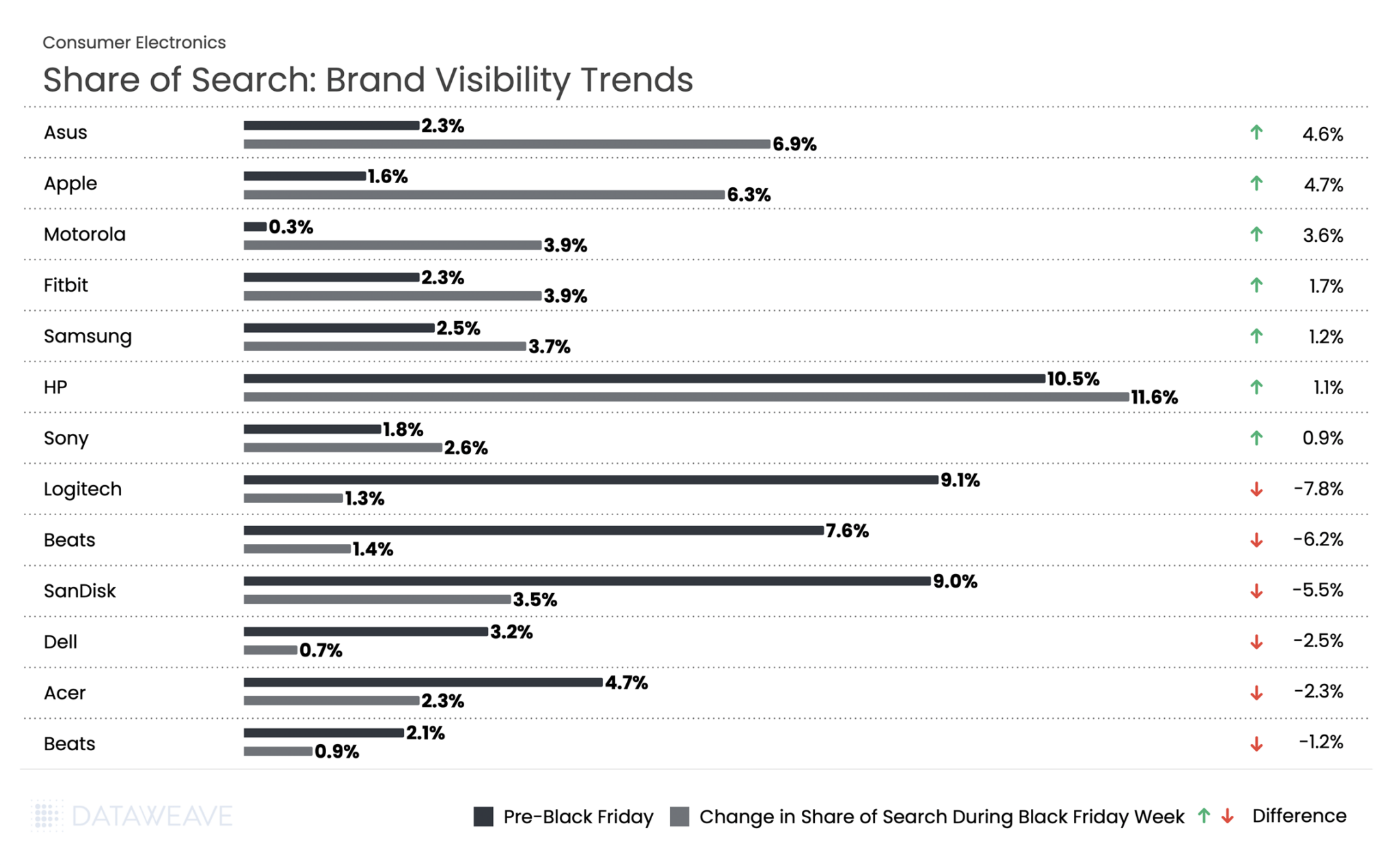

Share of Search: Brand Visibility Trends

Our Share of Search analysis reveals significant shifts in brand visibility during Black Friday Week:

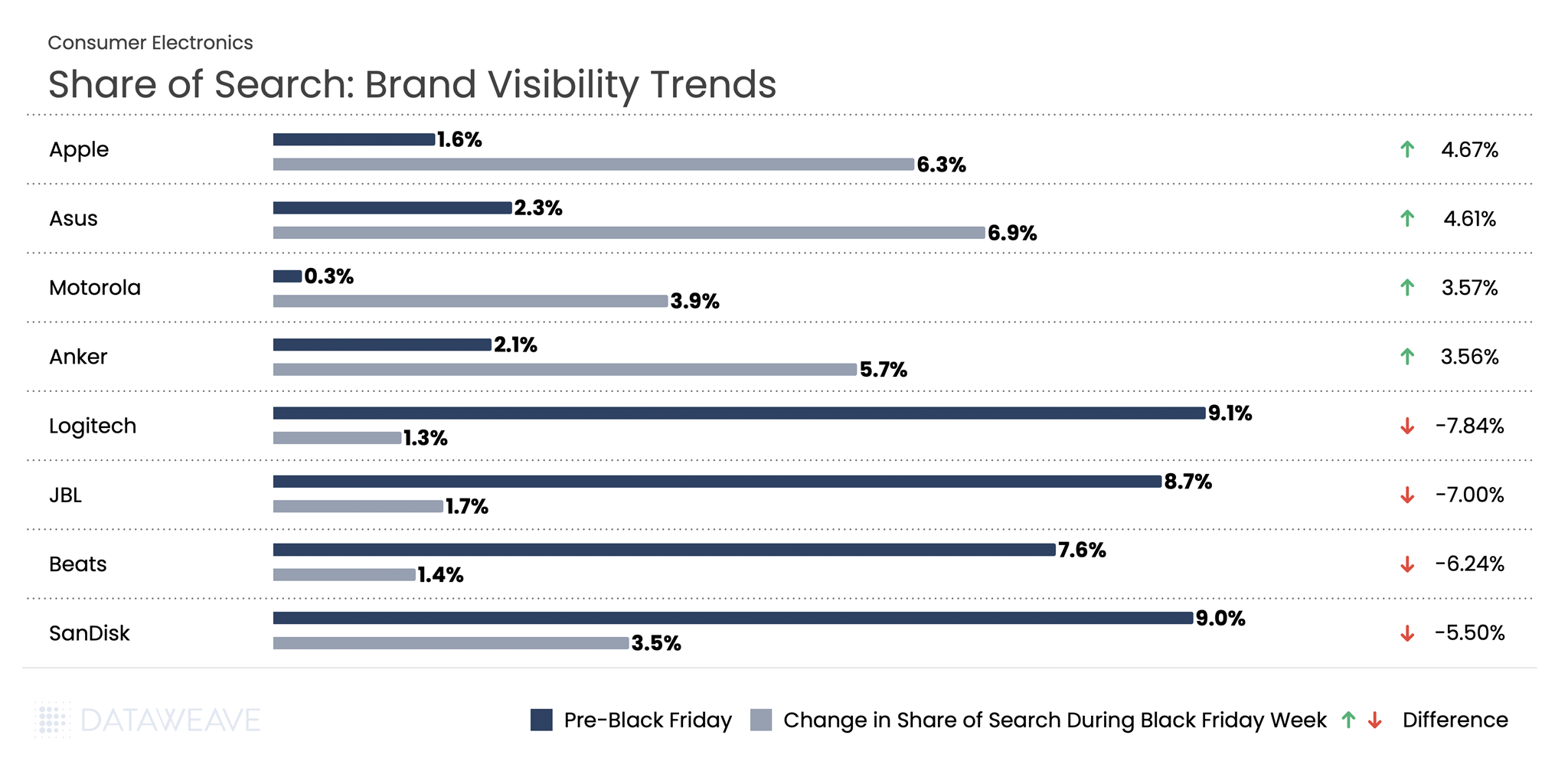

HP saw the highest share of search across Black Friday at 10.5% pre event and 11.6% during the event. Apple led with a 4.7% increase in visibility, jumping from 1.6% to 6.3%. Asus followed at 4.6%. Motorola surged 3.6 %, while wearables brand Fitbit gained 1.7%.

In stark contrast, Logitech dropped by 7.8 %, Beats fell 6.2 %, and SanDisk declined 5.5 %. Computer manufacturers Dell and Acer also struggled, falling 2.5 and 2.3 % respectively.

Home & Furniture

The Home & Furniture category in Germany showed unique discounting behavior compared to other markets, with additional Black Friday Week discounts (6.7%) actually exceeding Pre-Black Friday levels (6.1%). Our analysis of 1,403 SKUs shows how discounts were distributed across subcategories.

Subcategory Discount Analysis

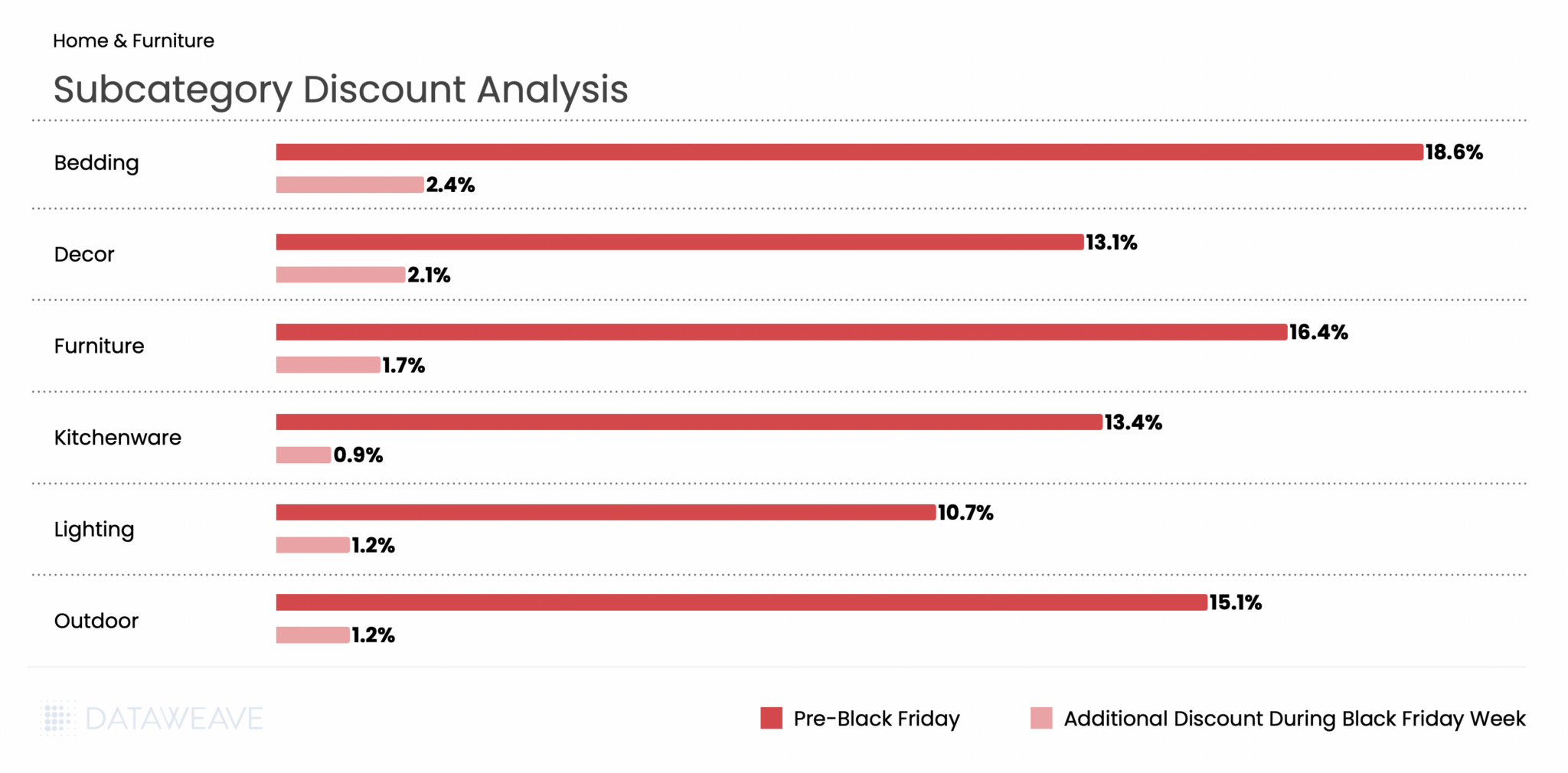

Kitchenware led pre-sale discounts at 8.7%. Decor surged from 5% to 7.5%, lighting jumped from 5% to 6.9%, and bedding more than doubled from 3.2% to 6.6%. These substantial increases suggest strategic timing to capture consumer attention during peak shopping days.

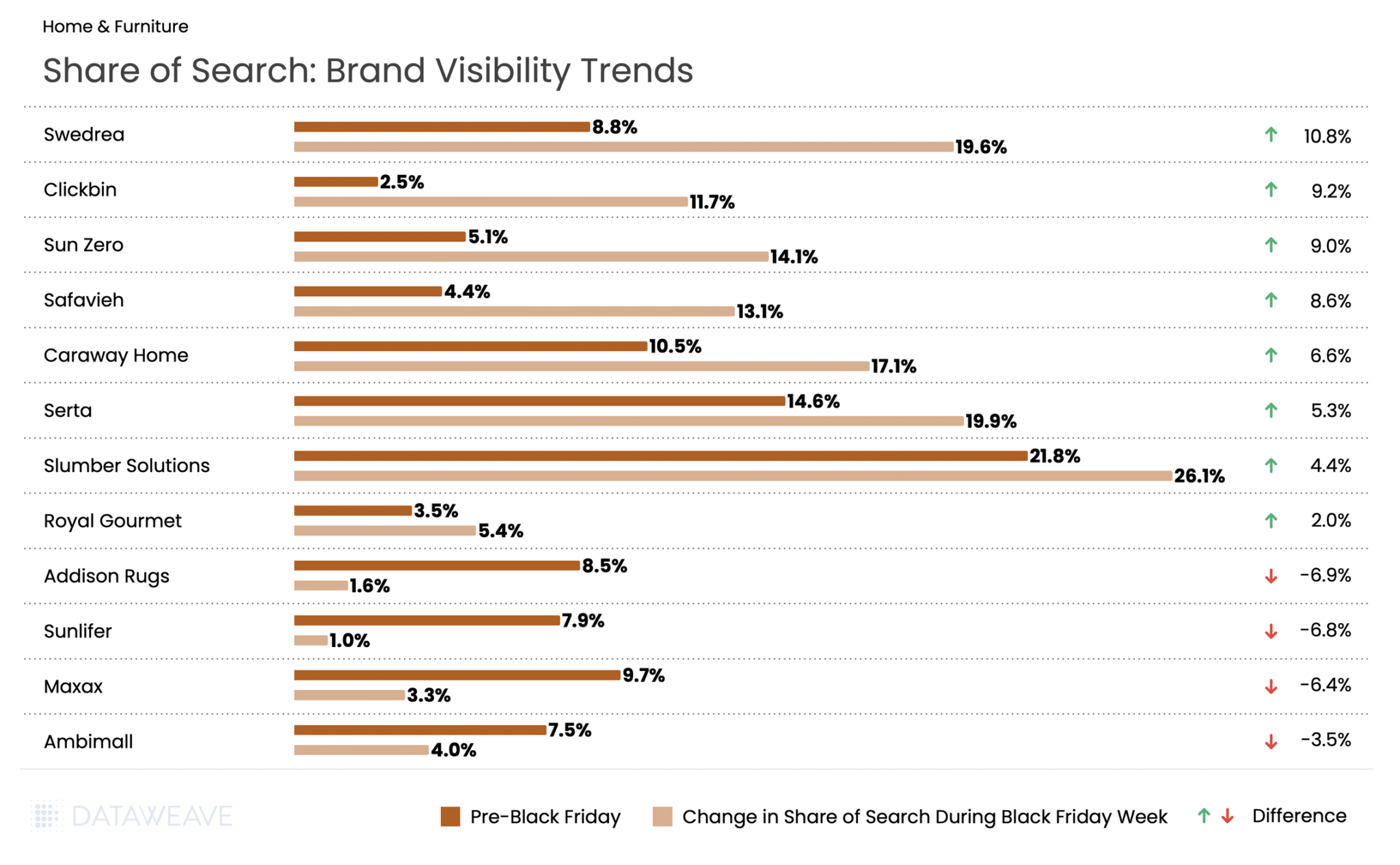

Share of Search: Brand Visibility Trends

Mattress brand Slumber Solutions saw the highest share of search at 21.8% pre event and 26.1% during Black Friday week. Meanwhile, another mattress brand Swedrea led all brands with a remarkable 10.8% surge in visibility, jumping from 8.8% to 19.6%. Budget-friendly furniture brand Clickbin gained 9.2%, while window treatment brand Sun Zero increased 9% and home textiles brand Safavieh surged 8.6%.

Premium and established brands also performed well: Caraway Home (cookware) rose 6.6%, mattress brand Serta gained 5.3%, and Slumber Solutions added 4.4%. Royal Gourmet, specializing in outdoor cooking equipment, gained 2.0%.

However, several mid-tier brands faced steep declines. Addison Rugs dropped 6.9% from 8.5% to just 1.6%, while Sunlifer fell 6.8 % and Maxax declined 6.4 %.

Health & Beauty

Our analysis of 6,474 SKUs reveals subcategory-level insights and dramatic brand visibility shifts that highlight the evolving German beauty landscape.

Subcategory Discount Analysis

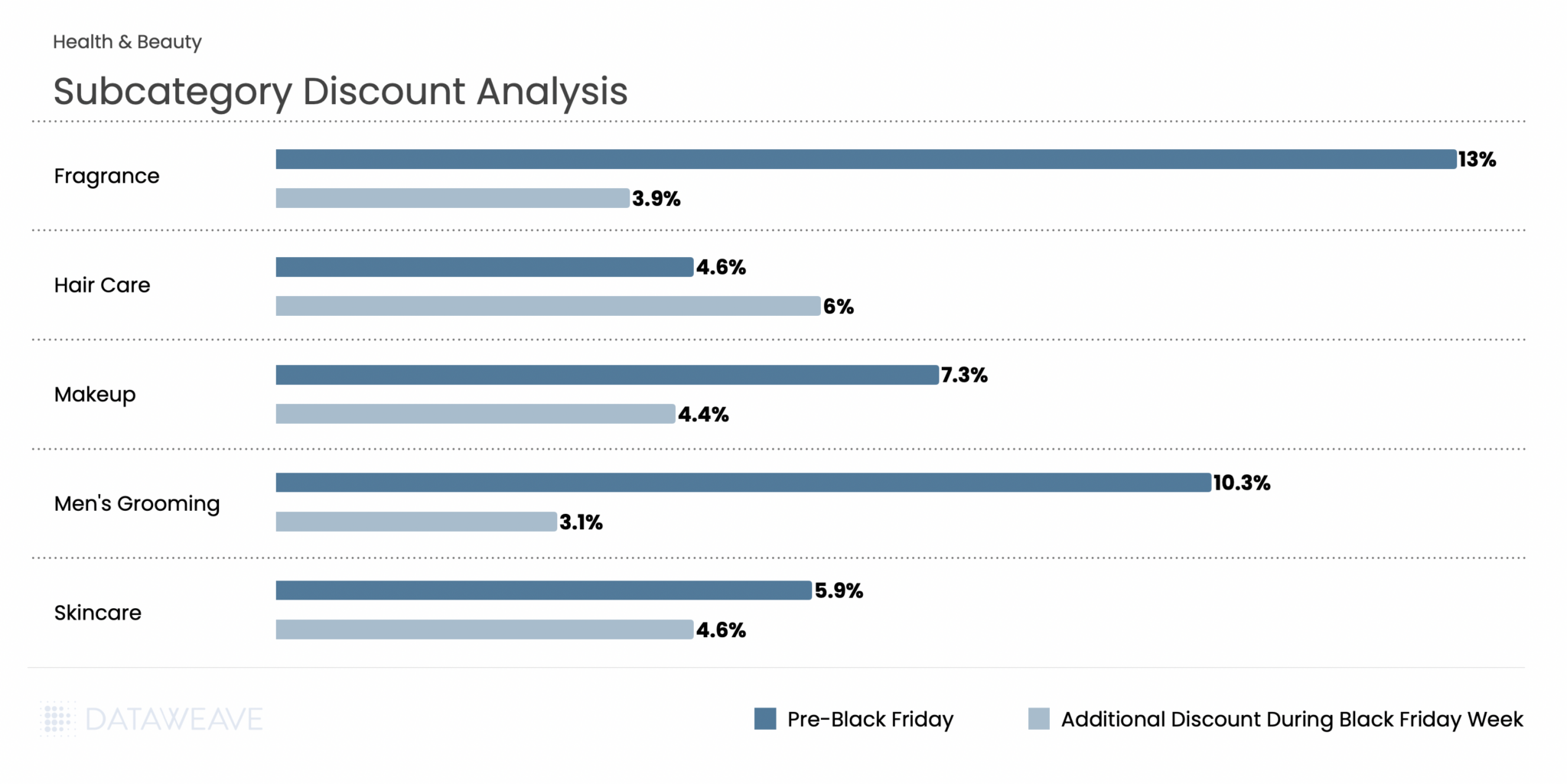

Pre-Black Friday discounts averaged 10%, with Black Friday Week adding 4.5% on average. Fragrance led pre-sale discounting at 11.6%, positioning perfumes and colognes as attractive early holiday purchases. However, Fragrance saw the smallest Black Friday Week addition at just 2.8%.

Hair Care and Skincare both showed strong performance across both periods, with Hair Care at 11.1% pre-sale and 4.9% during Black Friday Week, while Skincare registered 10.9% and 5.1% respectively. Skincare’s 5.1% Black Friday Week discount was the highest in the category.

Men’s Grooming stood apart with notably lower discounts at 3.3% pre-sale and 2.6% during Black Friday Week, suggesting either tighter margins in this subcategory or strategic positioning at different price points.

Share of Search: Brand Visibility Trends

L’Oréal Deutschland GmbH emerged as the most visible brand, surging from 37.7% to 51.9%, (+14.2). German pharmaceutical cosmetics company Medicos Kosmetik GmbH & Co. KG gained 4.4 %. Clinique gained 3.3 %, and French luxury brand Sisley added 3.1 %, German natural cosmetics brand Weleda rose 2.7 %, and Japanese prestige brand Shiseido gained 2.5 %.

The flip side? K-beauty brands and some international names faced significant challenges. Viral make-up brand Tirtir experienced the steepest decline visibility, dropping by 9.2 %. Aveda fell 6.2 %, Elizabeth Arden dropped 5.8 %, and Beauty of Joseon declined 3.8 %. German pharmacy brand Mi.to. Pharm GmbH lost 4.3 %, while Israeli makeup brand GA-DE fell 3.3 %.

The data reveals a clear German preference for European beauty heritage, pharmaceutical-grade cosmetics, and established prestige brands during Black Friday, rather than trendy K-beauty products or mid-tier international brands.

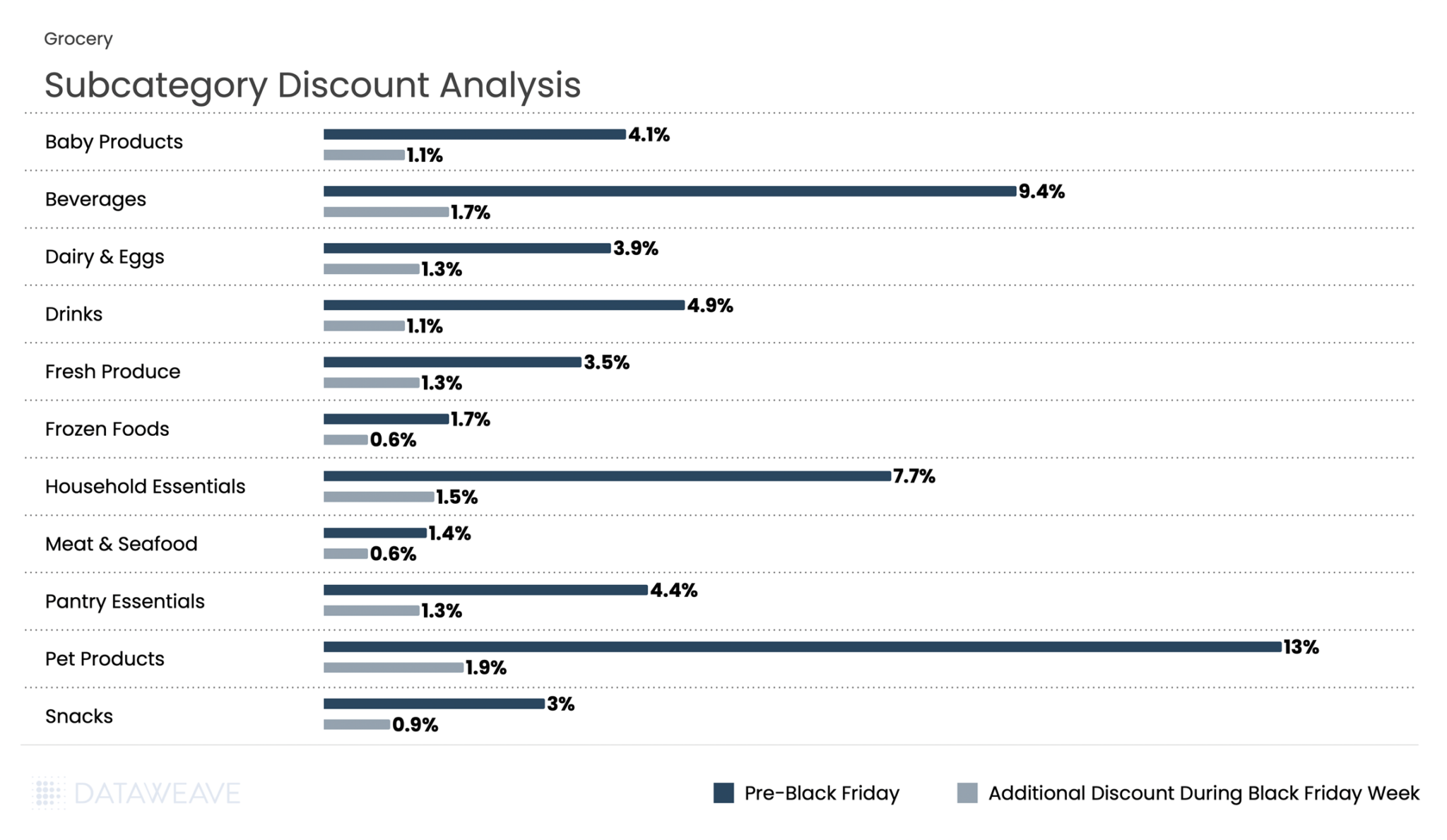

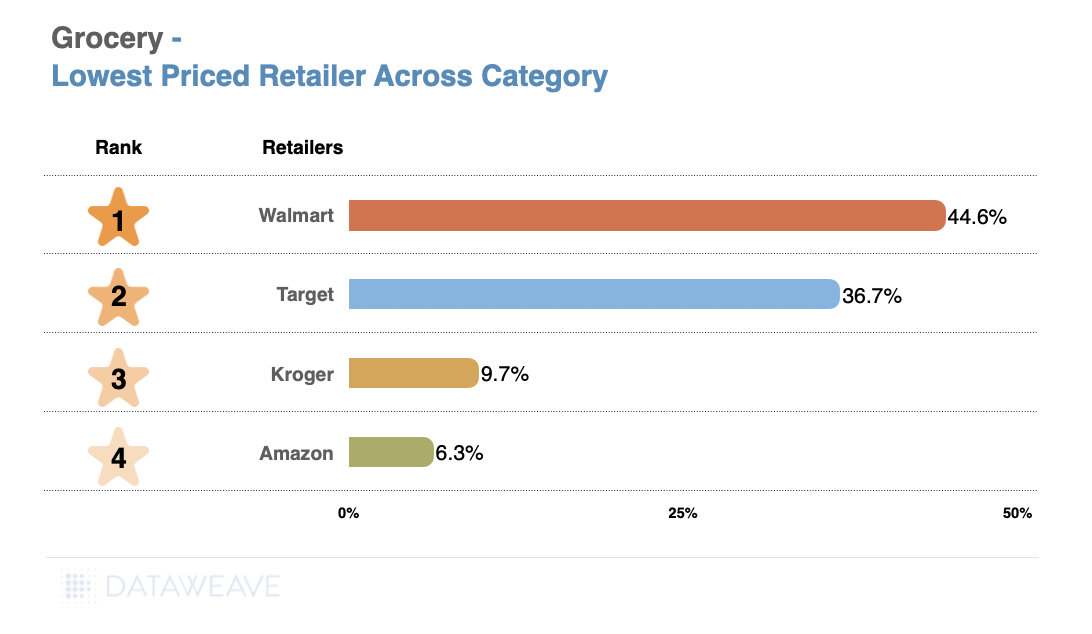

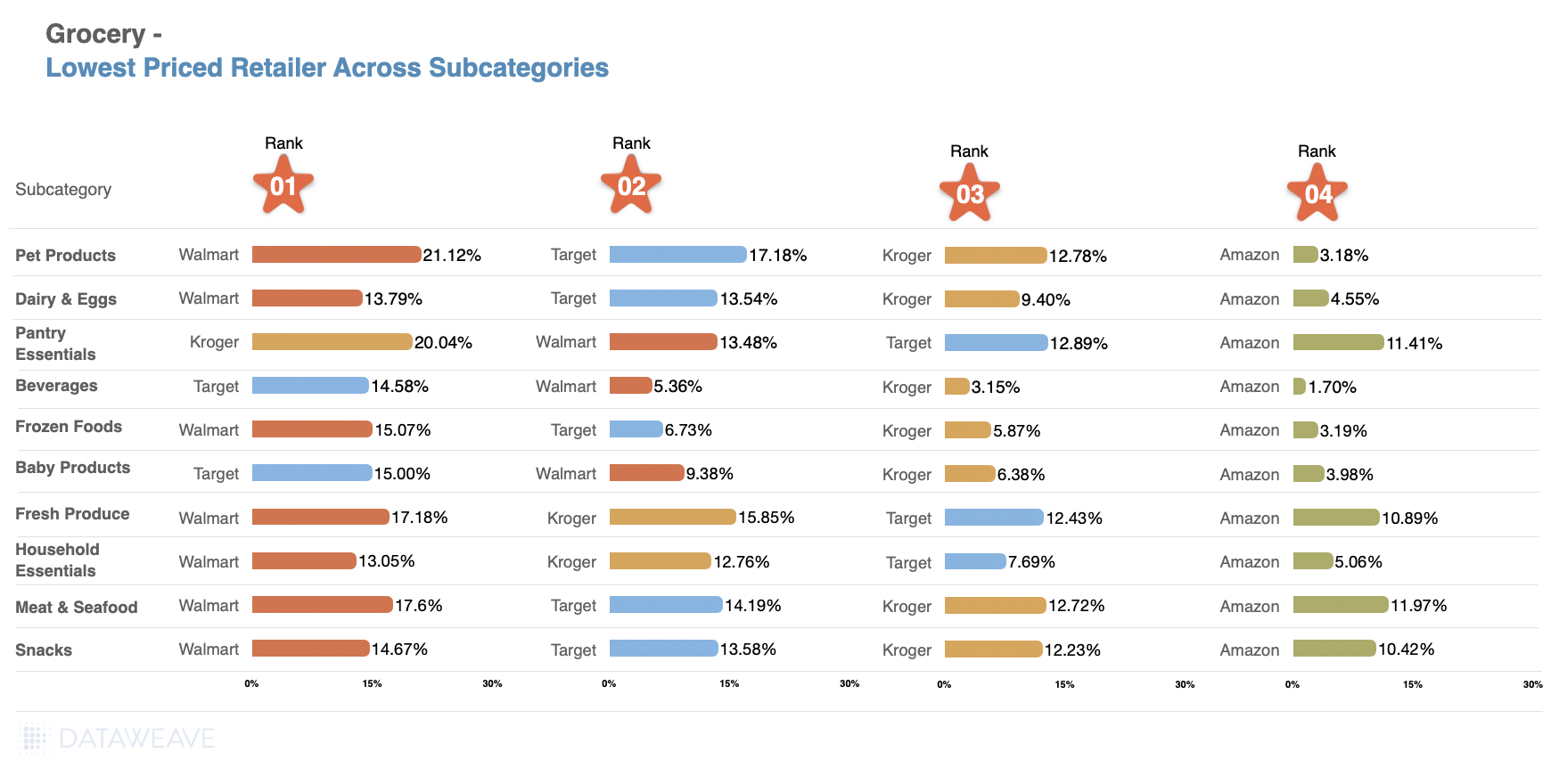

Grocery

While Grocery typically sees more modest discounts compared to discretionary categories, the German market showed interesting patterns with Black Friday Week discounts (3.5%) actually exceeding Pre-Black Friday levels (2.6%). Our analysis of 4,378 SKUs shows how German retailers approached promotions across essential and indulgent subcategories.

Subcategory Discount Analysis

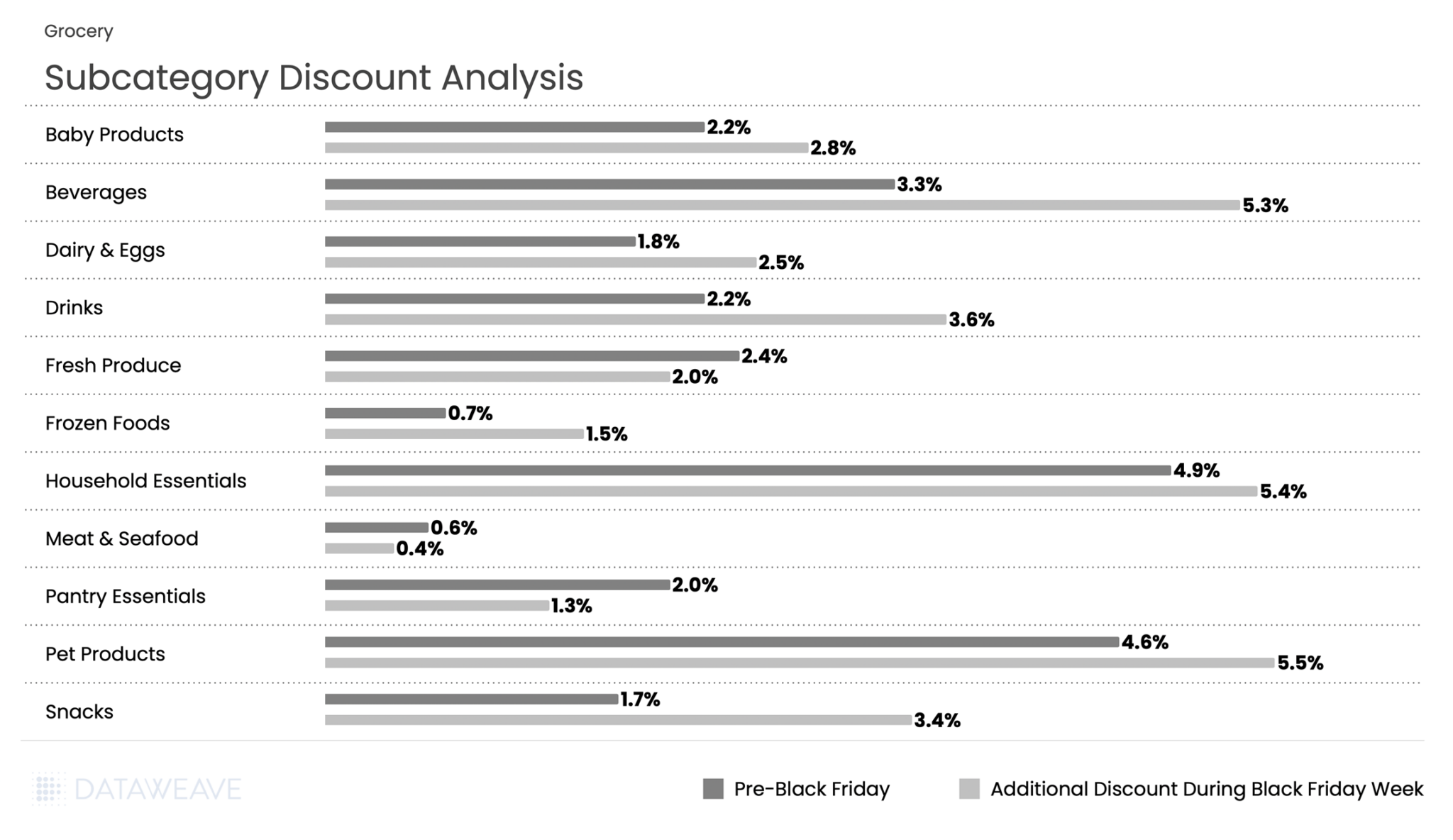

Pre-Black Friday discounts averaged just 2.6% in grocery. But Black Friday Week saw this surging to 3.5%, an increase that represents the highest proportional jump among all categories.

Pet Products and Household Essentials led discounting, with Pet Products at 4.6% pre-sale and an additional 5.5% during Black Friday Week. Meanwhile Household Essentials registered 4.9% and 5.4% respectively.

Beverages showed particularly strong Black Friday Week performance, jumping from 3.3% to 5.3%, while snacks doubled from 1.7% to 3.4%. Fresh categories maintained minimal promotional activity consistent with perishable inventory constraints: Meat & Seafood saw negligible discounts (0.6% pre-sale, 0.4% Black Friday Week), while Fresh Produce actually decreased from 2.4% to 2% during the main event.

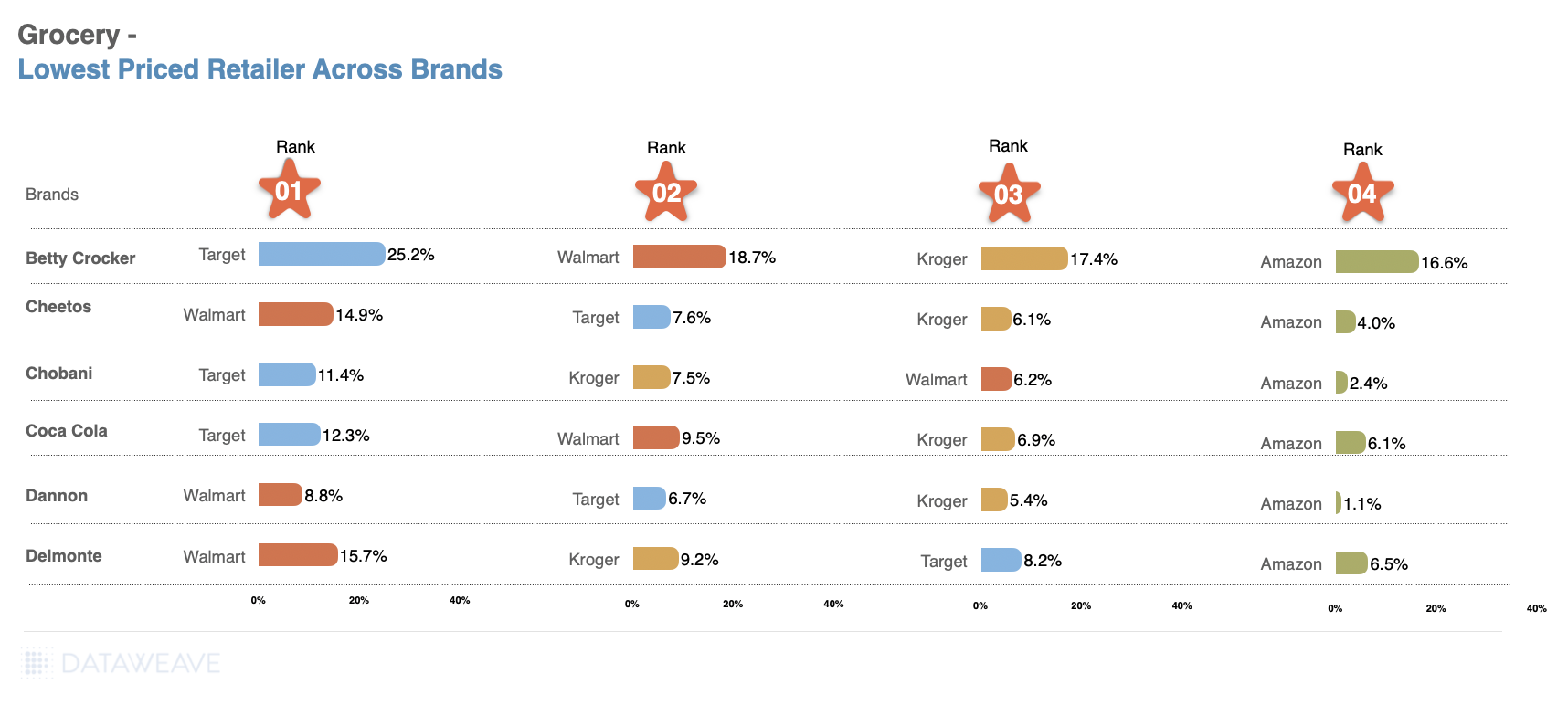

Share of Search: Brand Visibility Trends

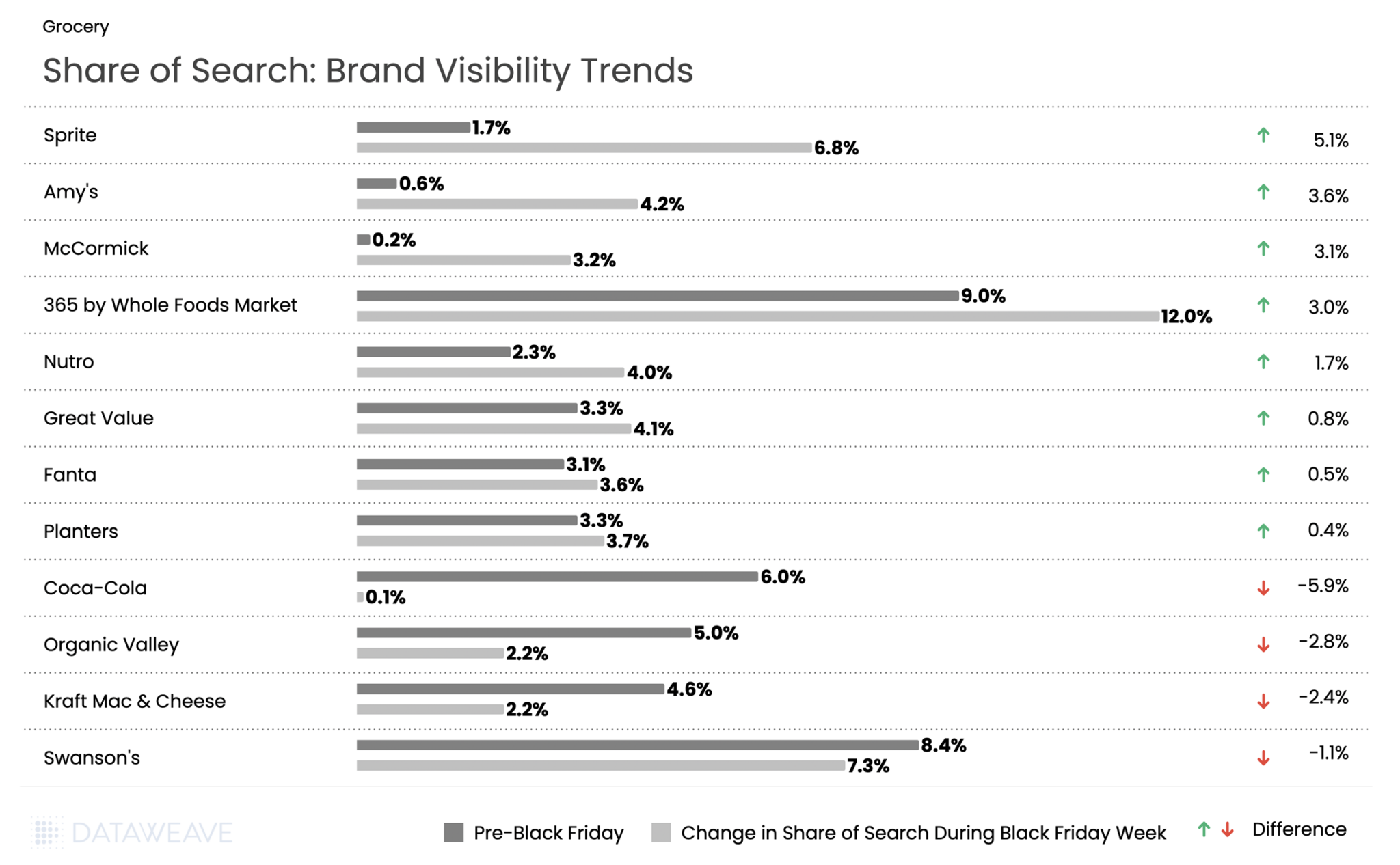

365 by Whole Foods saw the highest share of search at 9% pre event and 12% during Black Friday week. But Sprite led all brands with a 5.1% surge in share of search. Meanwhile, sister brand Coca-Cola experienced one of the steepest declines in our analysis, with visibility plummeting from 6.0% to just 0.1%. Fanta maintained modest search growth at 0.5 %. This stark divergence between two brands from the same parent company suggests vastly different promotional strategies during Black Friday Week.

Specialty and organic food brands performed well: Amy’s (organic/natural foods) gained 3.6 %, while spice brand McCormick surged 3.1 %. Pet food brand Nutro gained 1.7 %, while value-oriented Great Value added 0.8 %.

Snack brand Planters gained 0.4 %. On the decline side, Organic Valley dropped 2.8 %, Kraft Mac & Cheese fell 2.4 %, and Swanson’s declined 1.1 %.

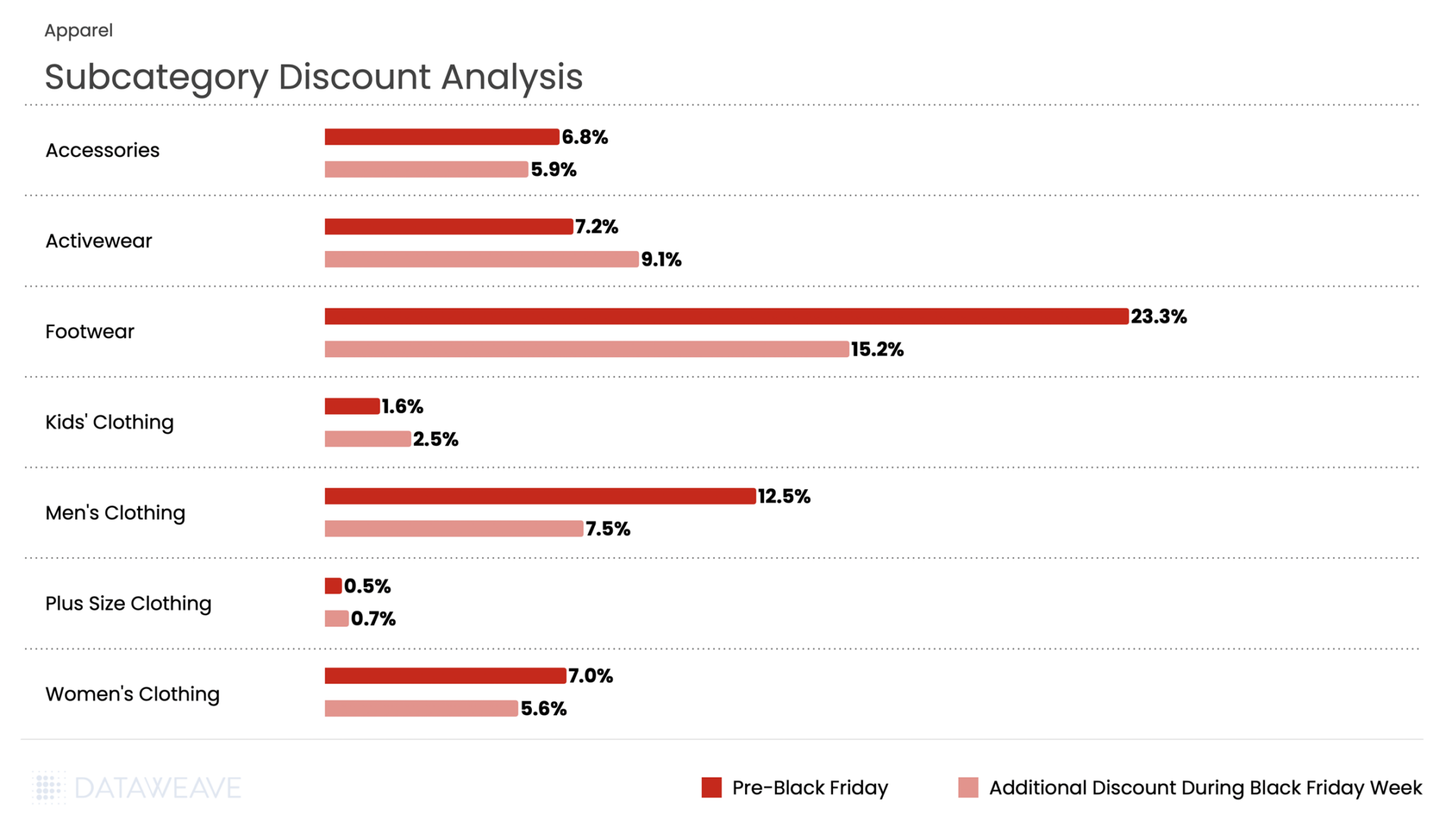

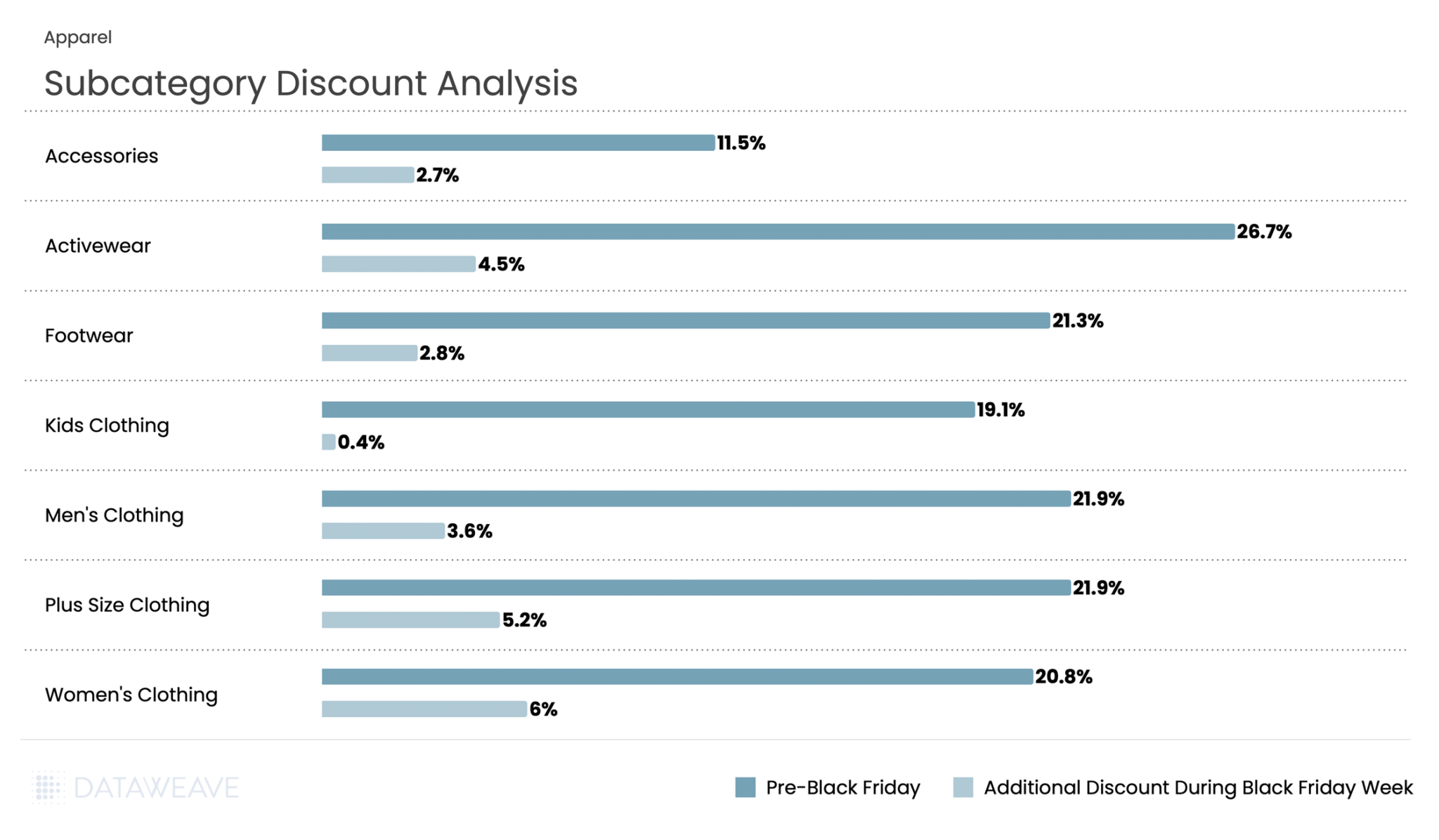

Apparel

Apparel in the German market showed modest promotional activity compared to other markets, with Pre-Black Friday discounts averaging 5.9% and Black Friday Week at 5.2%. Our analysis of 2,321 SKUs reveals interesting patterns across fashion segments in the German market.

Subcategory Discount Analysis

Footwear dominated discounting in both periods, with an impressive 23.3% pre-sale discount, and 15% additional discount during Black Friday Week. Men’s Clothing followed at 12.5% pre-sale, with additional 7.5% during Black Friday Week.

Activewear presented a unique pattern, with discounts increasing from 7.2% pre-event to additional 9.1% during Black Friday Week: one of the few subcategories to show higher discounts during the main event. Plus Size Clothing saw minimal promotional activity at 0.5% pre-sale and 0.7% during Black Friday Week, the lowest discounts in the entire category.

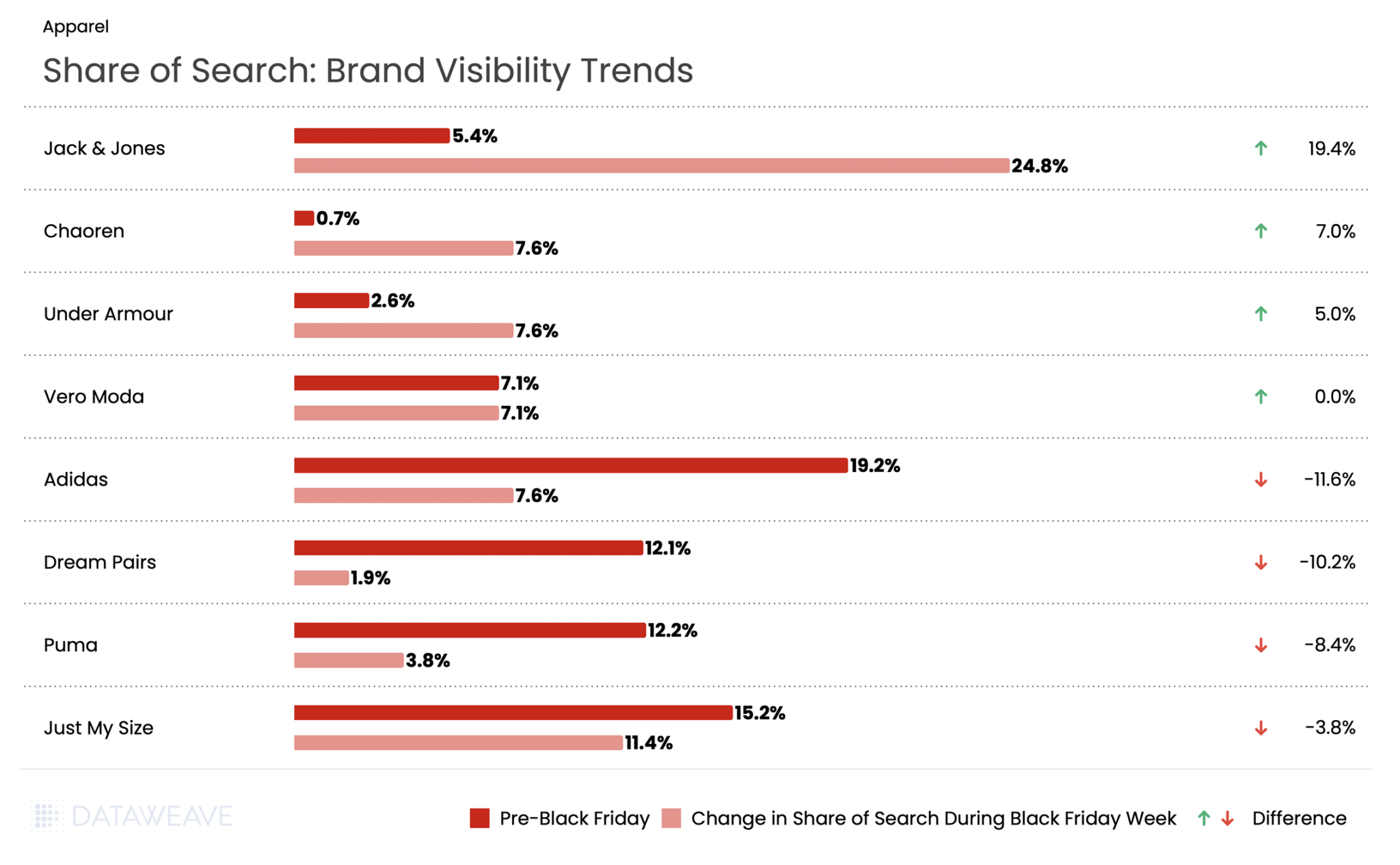

Share of Search: Brand Visibility Trends

Danish fashion brand Jack & Jones experienced an unprecedented surge with a staggering 19.4% gain in visibility. Sister brand Vero Moda (also owned by Jack & Jones’ parent company Bestseller) maintained flat visibility at 7.1%. Footwear brand Chaoren gained 7%. Meanwhile activewear giant Under Armour rose by 5%.

However, established sportswear giants suffered dramatic visibility losses. Adidas experienced an 11.6% decline in share of search. Dream Pairs saw visibility drop by 10.2%, Puma fell 8.4%, and plus-size brand Just My Size declined by 3.8 %.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Check out our analysis on Black Friday Pricing and Discount trends in the USA and UK. Follow our blog for more insights on retail pricing trends, brand visibility analysis, and data-driven commerce intelligence.

Black Friday 2025 saw British shoppers spend an average of £430 each this year representing a £91 increase from last year and totaling over £10.2 billion across the sales period.

The 2025 sales event arrived at a pivotal moment for UK retail. Retail sales fell 1.1% in October 2025 as consumers held back spending in anticipation of Black Friday promotions, according to the Office for National Statistics. Over 2 in 5 UK adults participated in Black Friday shopping, with 45% planning to pick up Christmas gifts at a discount, according to a Barclays study.

Against this backdrop of cautious optimism and strategic consumer behavior, how did retailers and brands perform across key categories this Black Friday? At DataWeave, we conducted a comprehensive analysis of Black Friday 2025 discounting trends across five major categories in the UK market: Consumer Electronics, Home & Furniture, Health & Beauty, Grocery, and Apparel. Our AI-powered pricing intelligence platform monitored over 71K SKUs across leading UK retailers like Costco, Selfridges, Boots, Debenham’s, Carethy, Argos, John Lewis, Amazon, and more, revealing fascinating patterns in how retailers and brands approached this year’s sale season.

Our Methodology

For this analysis, DataWeave monitored average discounts across leading UK retailers during two distinct periods:

Pre-Black Friday: November 6 – November 23, 2025 – capturing early holiday deals and baseline pricing

Additional Discounts During Black Friday Week: November 24 – December 1, 2025 – covering Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

Our sample encompassed the top-ranked products across subcategories on major retail sites. We also analyzed Share of Search data, which measures brand visibility by monitoring which brand names appear in the top 20 search results for critical keywords.

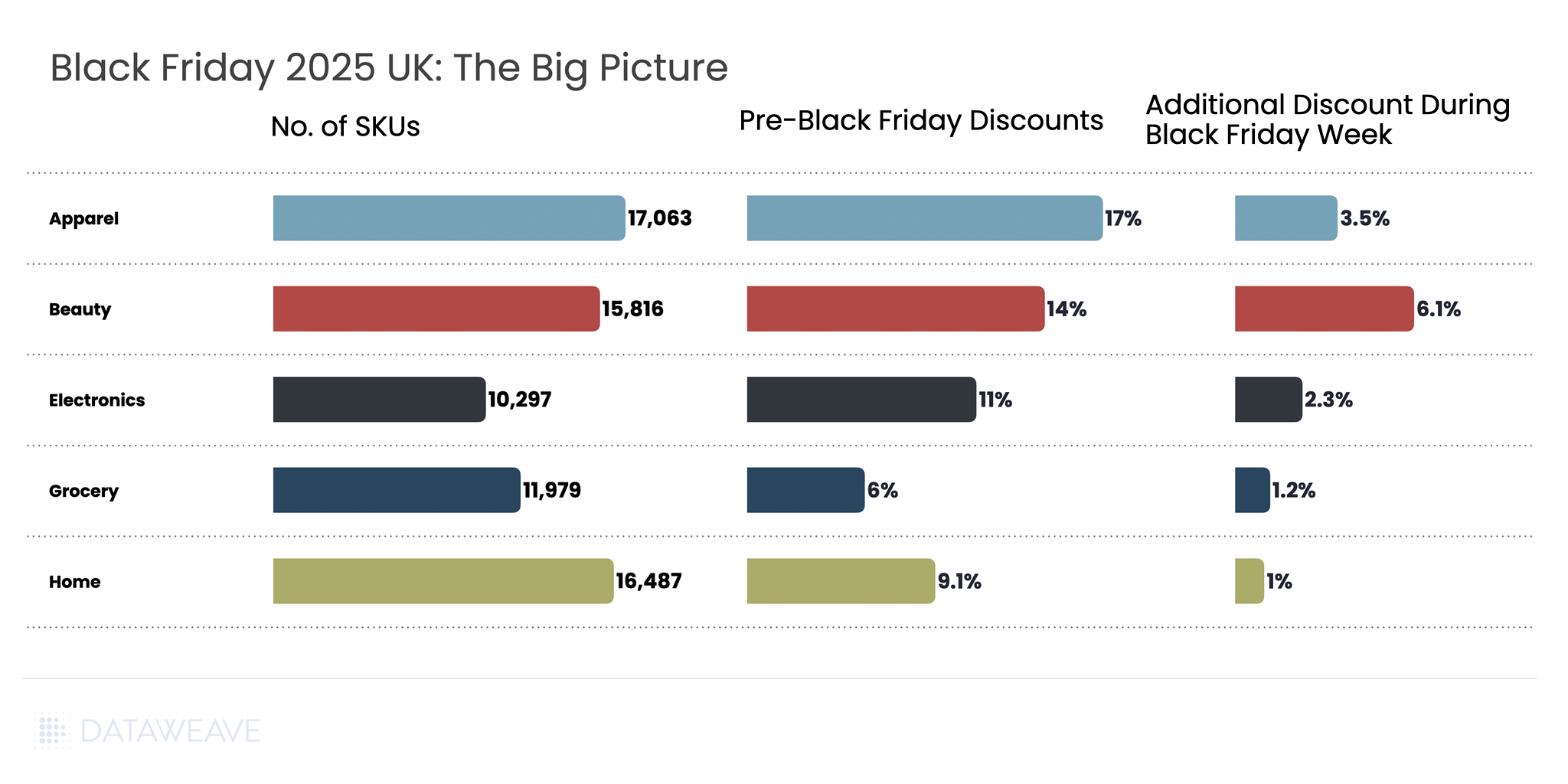

Black Friday 2025 UK: The Big Picture

Our analysis covered 71,642 SKUs across five major categories. Here’s the snapshot of average discounts during the Pre-Black Friday period compared to Black Friday Week:

Key Insight: Pre-Black Friday discounts were substantial across all categories. This suggests UK retailers front-loaded their promotions to capture early holiday shoppers, with additional discounts during Black Friday Week adding to the baseline discounts already in place. The extended promotional period transformed Black Friday from a single-day event into a month-long campaign, with 60% of UK shoppers beginning their deal searches as early as October.

Consumer Electronics

Consumer electronics remains a cornerstone of Black Friday shopping in the UK, with technology accounting for 48% of planned consumer spending during the sales period, according to PwC.

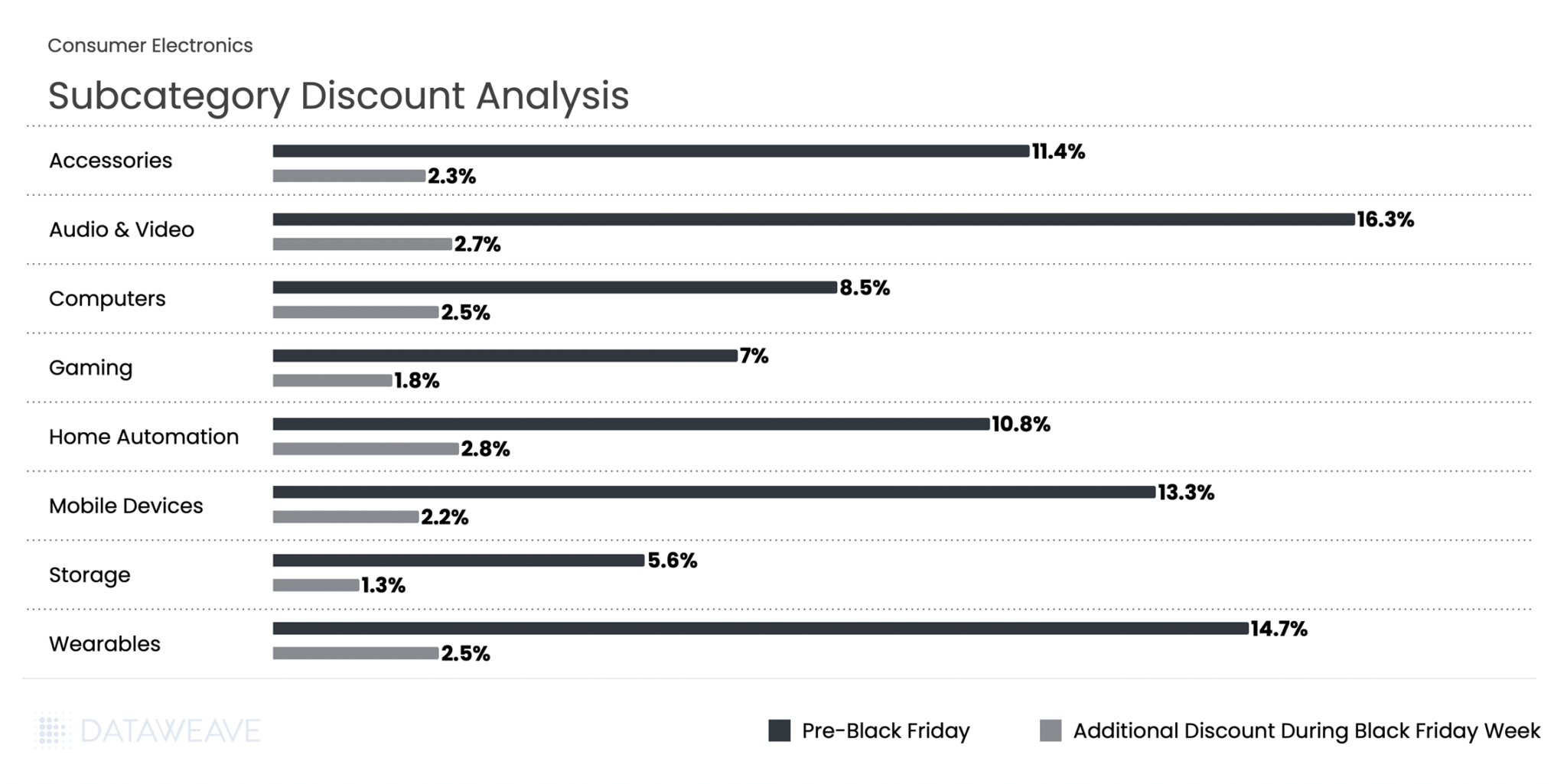

AI is transforming how consumers shop for electronics, with AI-driven traffic to retail sites expected to rise 410% year-on-year during the 2025 holiday season. Younger shoppers particularly embraced AI tools, with 17% of Gen Z consumers using AI platforms like Chat GPT and Gemini to source and compare deals. Our analysis of 10,297 SKUs reveals how discounts varied across subcategories and which brands dominated search visibility.

Subcategory Discount Analysis

Pre-Black Friday discounts averaged 11.1% across subcategories, while Black Friday Week saw an additional 2.3% discount on average. Audio & Video products led the pre-sale discounting at 16.3%, indicating retailers were eager to move inventory early in the season.

During Black Friday Week, Home Automation saw the highest additional discount at 2.8%. Wearables and Computers both saw solid 2.5% additional discounts, making them attractive categories during the peak shopping period.

Share of Search: Brand Visibility Trends

Our Share of Search analysis reveals significant shifts in brand visibility during Black Friday Week:

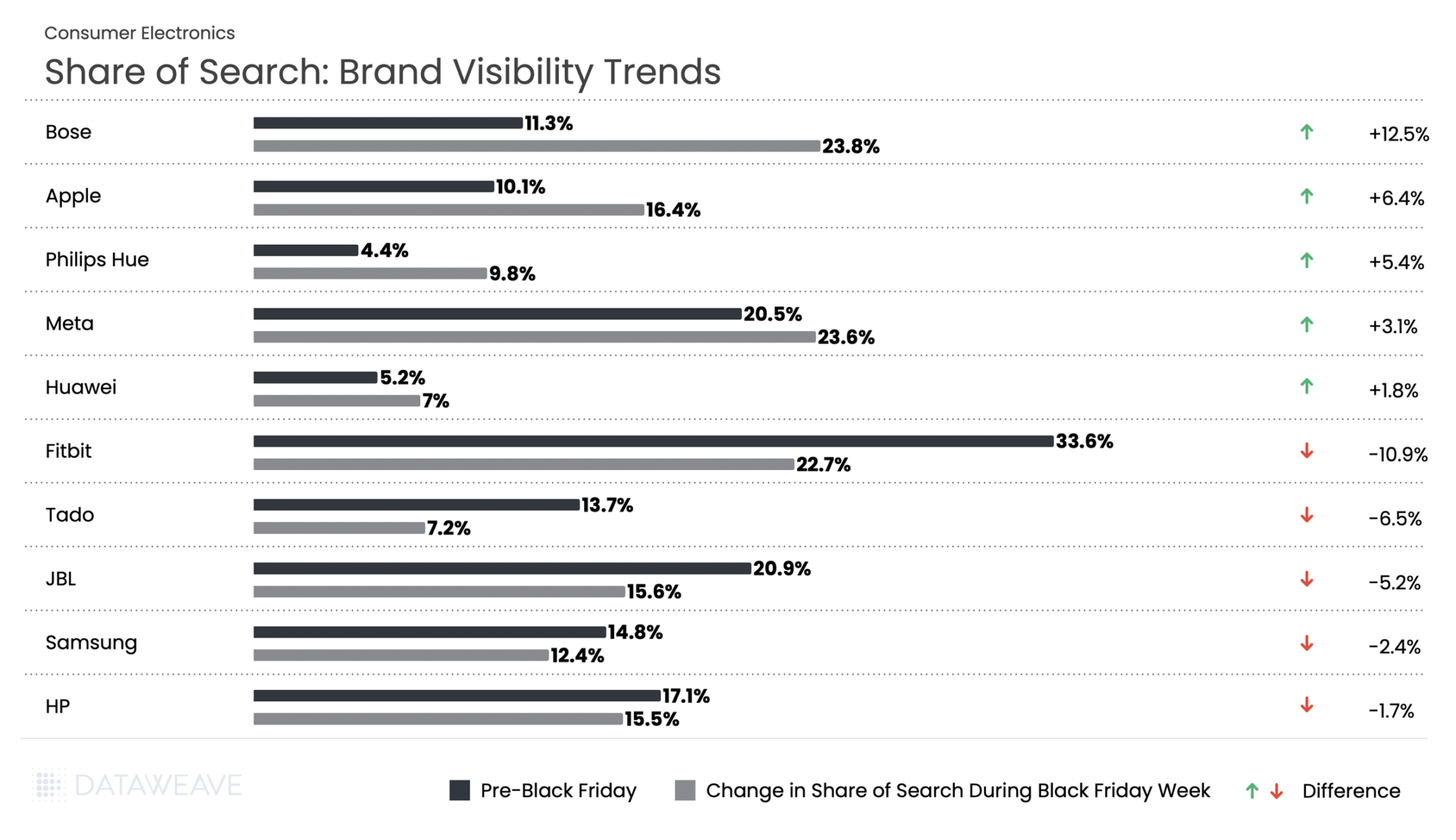

Bose dominated with its Share of Search more than doubling from 11.3% to 23.8%, a remarkable +12.5% gain. Lighting brand Philips Hue followed, gaining by +5.4% in share of search during Black Friday week. Notably, Meta, with it’s range of wearables, stands out for a +3.1% increase in visibility.

Apple’s Share of Search jumped from 10.1% to 16.4%, a gain of 6.4%. At the same time, Fitbit’s share dropped nearly 11%, the steepest decline in the entire electronics category. Meanwhile, Samsung and HP also lost on visibility this Black Friday in the UK.

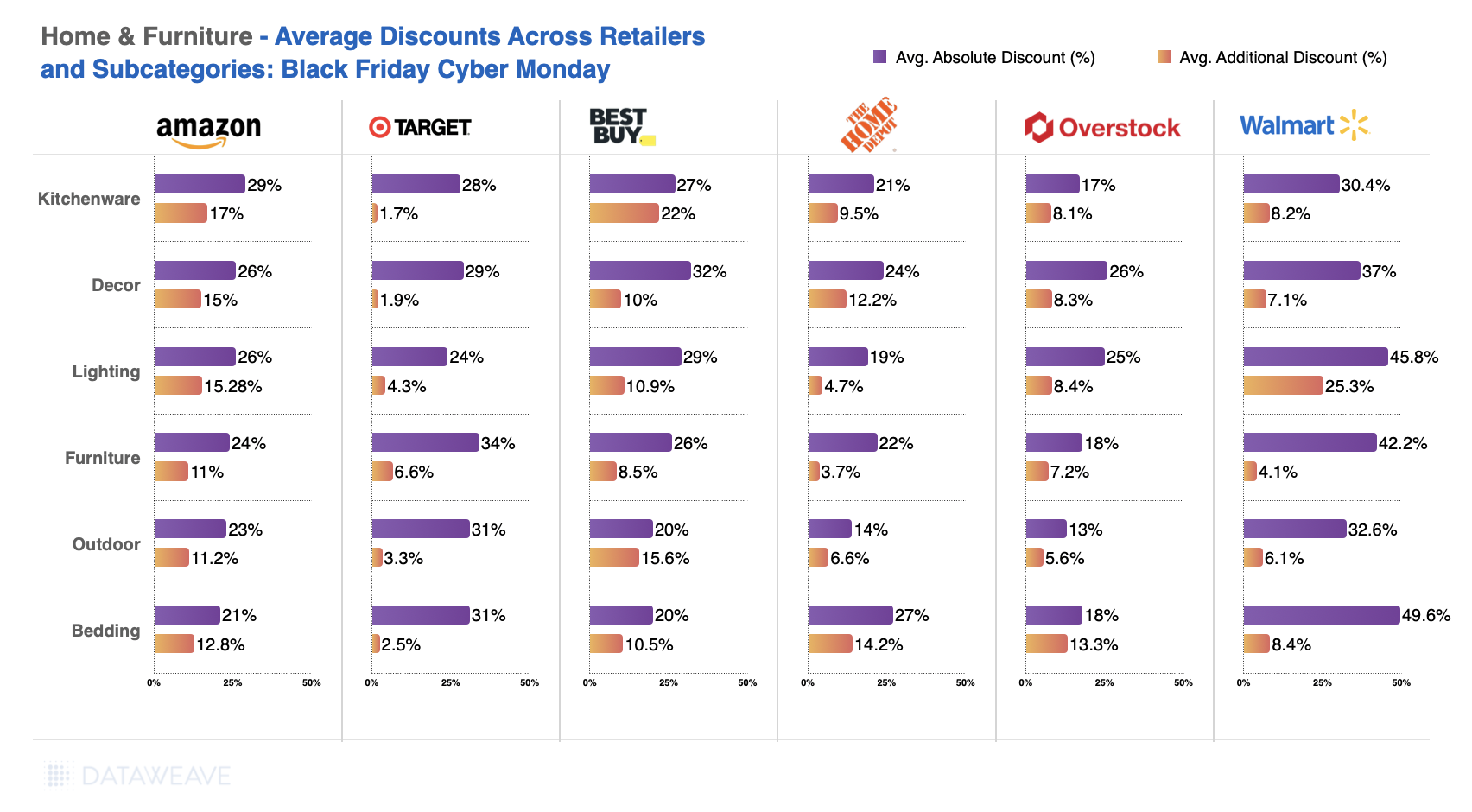

Home & Furniture

The Home & Furniture category continues to attract UK consumers during Black Friday, though with a more measured discounting approach compared to other categories. Our analysis of 16,487 SKUs shows how discounts were distributed across subcategories.

Subcategory Discount Analysis

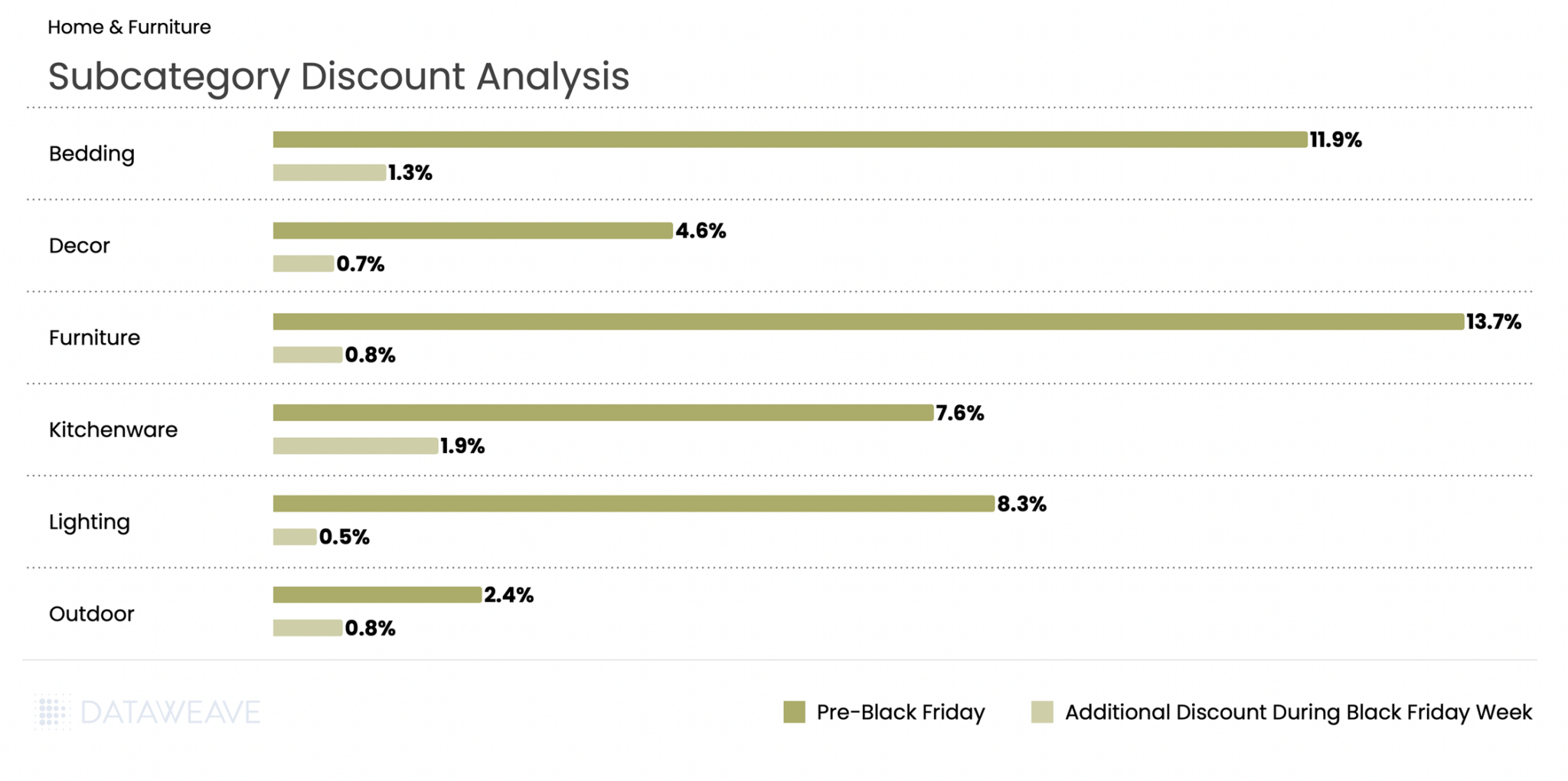

Home & Furniture saw Pre-Black Friday discounts averaging 9.1%, with Black Friday Week adding just 1% on average, the lowest additional discount among all categories. Furniture led pre-sale discounts at 13.7%, followed by Bedding at 11.9%. This suggests retailers aggressively promoted larger home goods early in the season to capture deal-seekers.

During Black Friday Week, Kitchenware saw the highest additional discount at 1.9%, making it attractive for holiday cooking and gifting needs. Conversely, Lighting saw minimal additional promotion at just 0.5%.

Share of Search: Brand Visibility Trends

Made.com, the contemporary furniture brand, saw visibility surge during Black Friday with an impressive 8.9% increase. Similarly, emerging mattress brand Vesgantti gained 5.4%. Rug specialist Gooch Oriental also made significant gains with a 4.9% increase.

On the flip side, British heritage brands faced challenges. Both Laura Ashley and Julian Bowen saw share of search drop 2.2%. Premium mattress maker Vispring also declined 2.1%, while French cookware brand Le Creuset fell 1.9%.

Health & Beauty

Health & Beauty has emerged as a growth engine during Black Friday in the UK. The beauty industry is projected to grow 5% annually through 2030 according to a McKinsey survey. The category continues to demonstrate resilience even as consumers show caution in other discretionary categories. Our analysis of 15,816 SKUs reveals fascinating subcategory-level insights and dramatic brand visibility shifts that highlight evolving consumer preferences in the beauty space.

Subcategory Discount Analysis

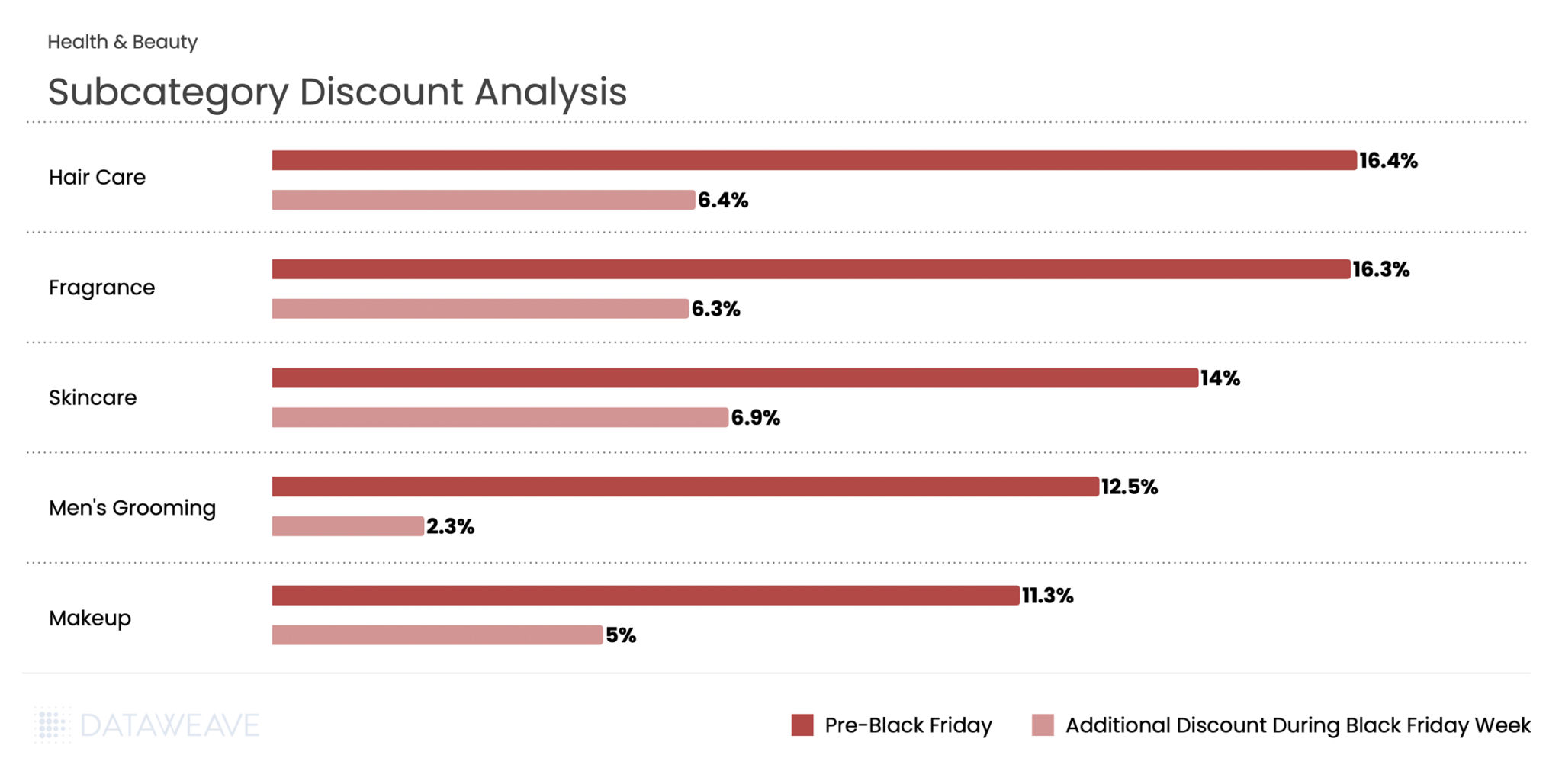

Health & Beauty presented a unique discounting pattern compared to other categories. Pre-Black Friday discounts averaged 14.4%, the second-highest among all categories. But Black Friday Week discounts were also robust at 6.1%, the highest additional discount increase.

Hair Care led both periods with 16.4% pre-sale discounts and an additional 6.4% during Black Friday Week. Skincare saw the highest Black Friday Week discount at 6.9%, suggesting retailers strategically saved their best skincare promotions for the main event when consumers are actively seeking holiday gift sets. Men’s Grooming stood apart with strong pre-sale discounts of 12.5% but more modest Black Friday Week additions of just 2.3%.

Share of Search: Brand Visibility Trends

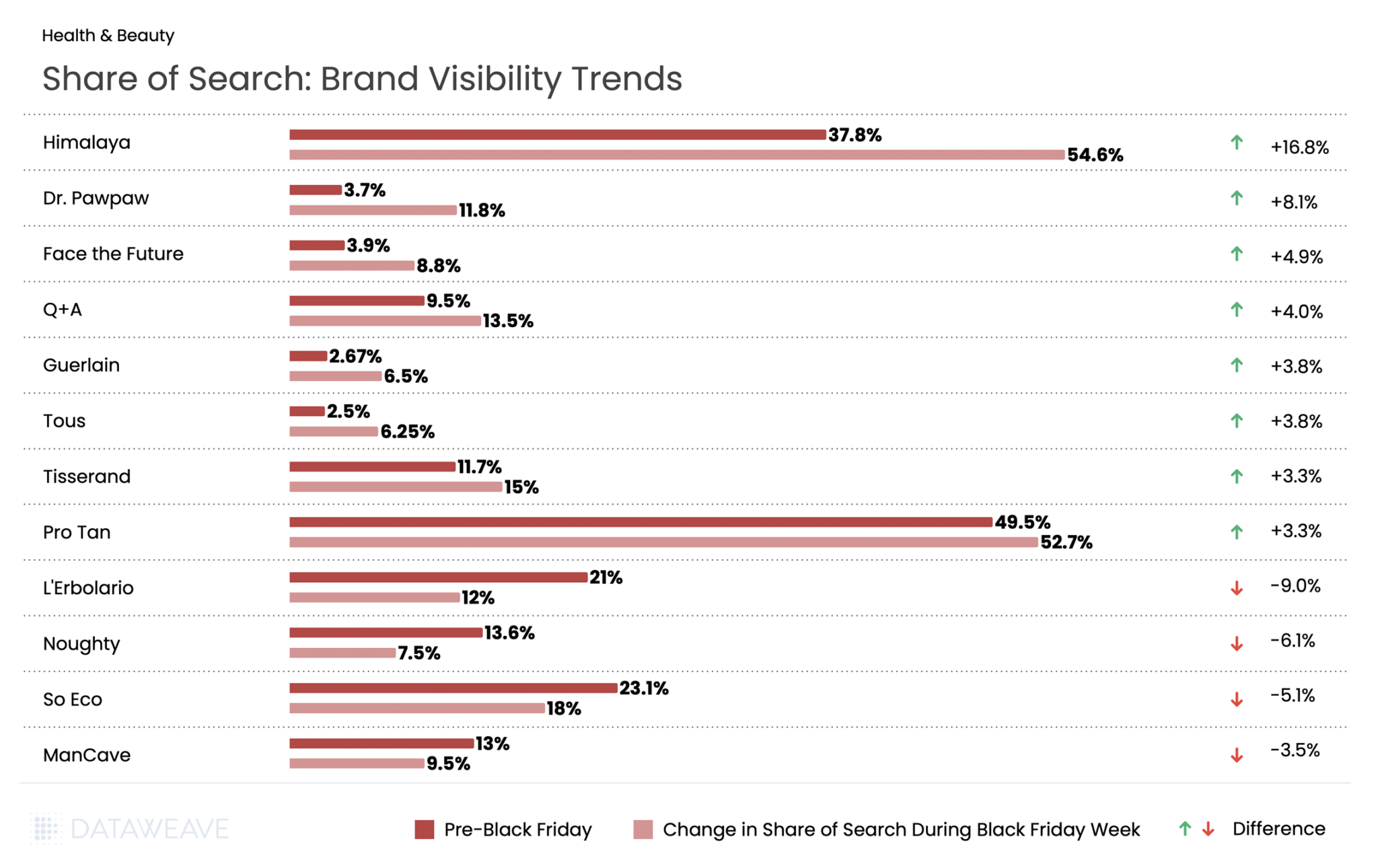

The UK Beauty category saw some of the most dramatic Share of Search swings in our analysis.

Himalaya, the Ayurvedic skincare brand, dominated the category with a stunning 16.8% gain. British cult favorite Dr. Pawpaw exploded from 3.7% to 11.8%, a gain that reflects the brand’s growing mainstream appeal. Face the Future, the skincare specialist, also gained significant ground with a 4.9% increase.

Budget-friendly British brand Q+A continued its momentum, rising 4%, while prestige names like Guerlain and Tous each gained 3.8%.

Italian natural beauty brand L’Erbolario saw the steepest decline, with visibility dropping by 9%. Haircare brand Noughty fell 6.1%, and eco-beauty brand So Eco declined by 5.1%.

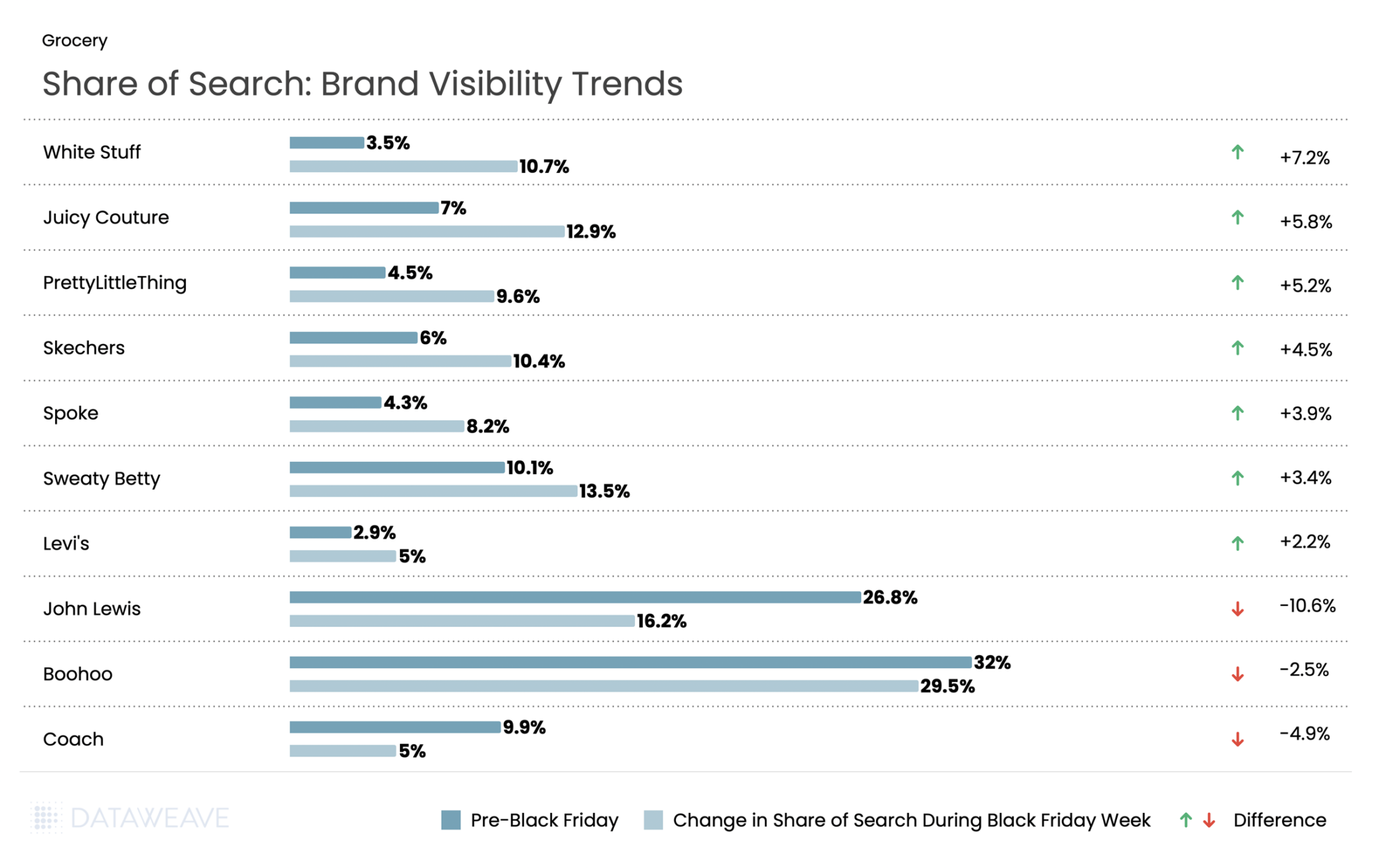

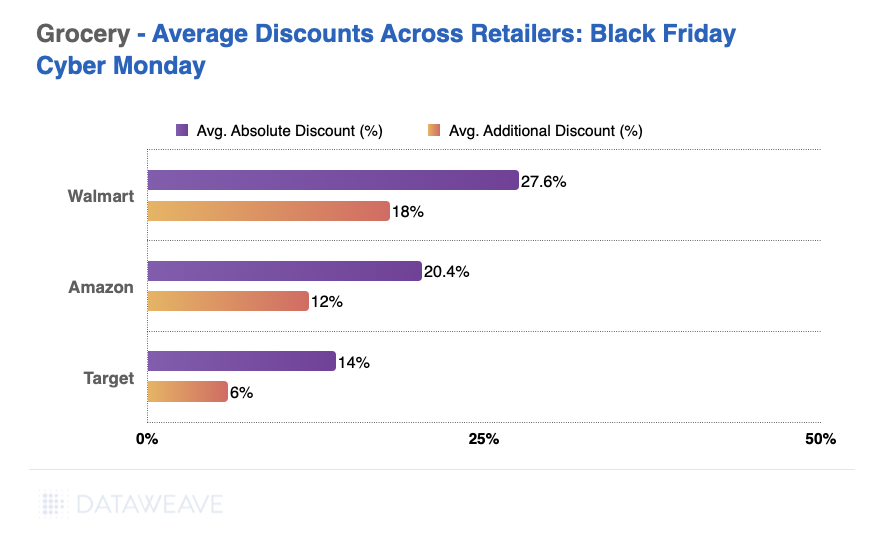

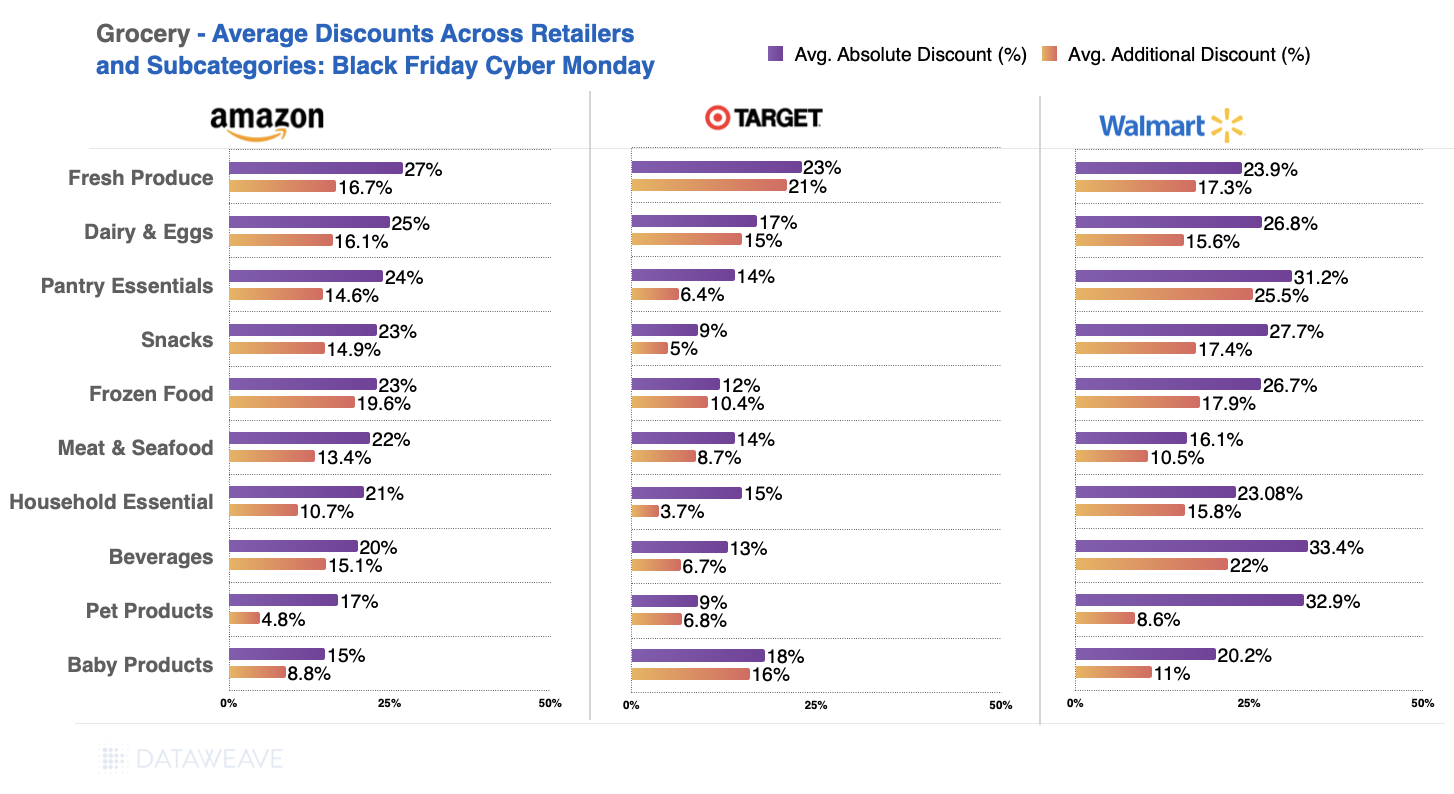

Grocery

While Grocery typically sees more modest discounts compared to discretionary categories, the sector remains a critical part of Black Friday shopping in the UK, particularly as consumers prepare for holiday entertaining and gifting. Our analysis of 11,979 SKUs shows how UK retailers approached promotions across essential and indulgent subcategories.

Subcategory Discount Analysis

Grocery had the lowest discounts across all categories, reflecting the already-thin margins in food retail. Pre-Black Friday discounts averaged just 5.7%, with Black Friday Week adding only 1.2%. Pet Products led pre-sale discounts at an impressive 13%, significantly outpacing other grocery subcategories.

Beverages and Household Essentials followed with 9.4% and 7.7% pre-sale discounts respectively, and maintained their lead during Black Friday Week with 1.7% and 1.5% additional discounts each. Fresh categories like Meat & Seafood (1.4% pre-sale, 0.6% Black Friday Week) and Frozen Foods (1.7% pre sale, 0.6% additional discounts during Black Friday week) saw minimal promotional activity, consistent with perishable inventory constraints and tight margins.

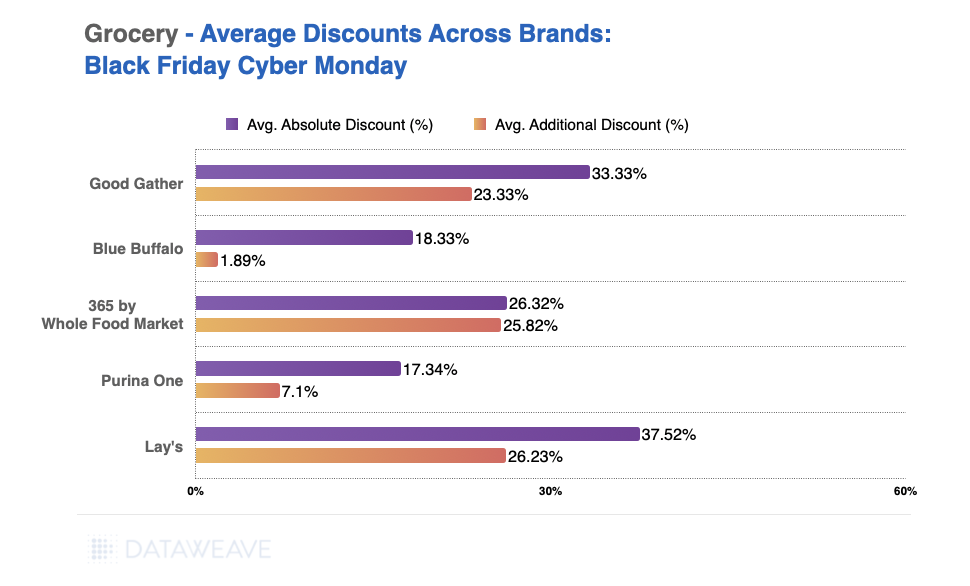

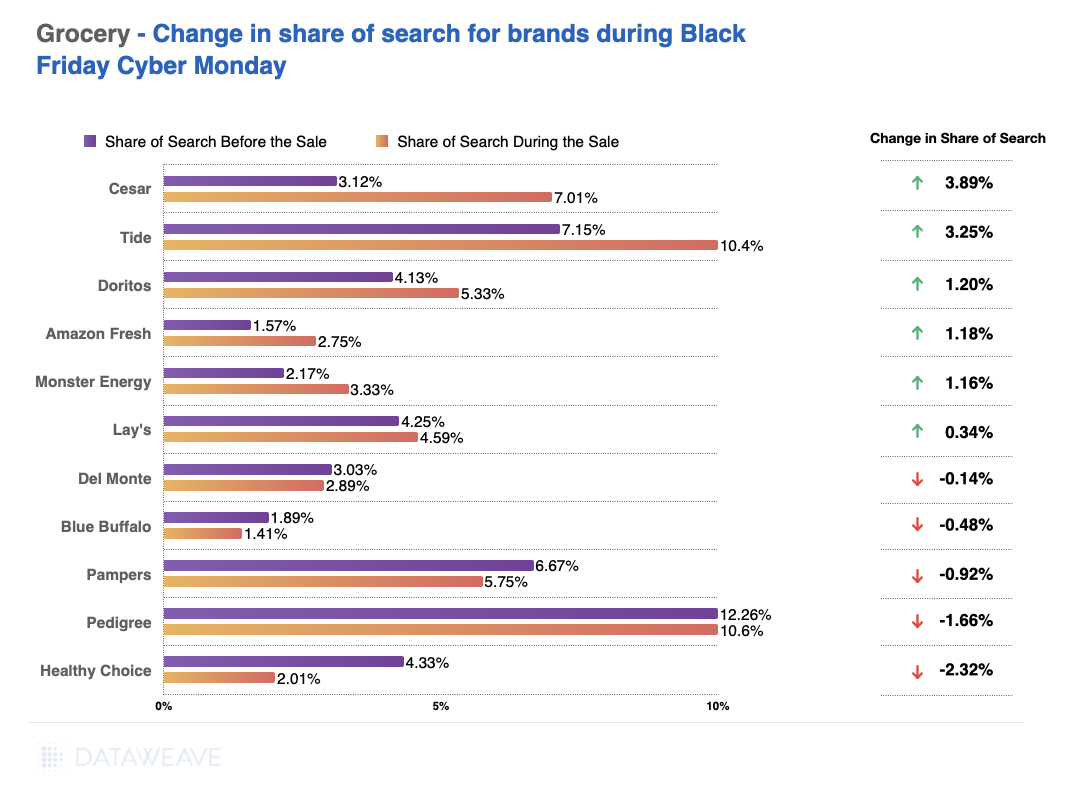

Share of Search: Brand Visibility Trends

Doritos led with a 7.3% surge in visibility. Pepsi delivered an equally impressive performance, rising from 3.6% pre Black Friday to 10.7% during Black Friday week. Fanta too saw 5.2% gain in share of search.

Conversely, Coca-Cola gained more modestly at 1.6%, while its Sprite brand actually declined 0.9%.

Apparel

Apparel remains a Black Friday staple in the UK and is projected to deliver the strongest year-on-year growth of any UK retail segment this festive season. With clothing accounting for 39% of planned Black Friday purchases, the category represents one of the most hotly contested battlegrounds during the sales period.

Our analysis of 17,063 SKUs, the largest category in our study, reveals interesting patterns across fashion segments that demonstrate both the opportunities and competitive intensity in UK apparel retail.

Subcategory Discount Analysis

Apparel showed the strongest discounting activity throughout the BFCM period among all categories. Pre-Black Friday discounts averaged 17.2%, with Black Friday Week adding 3.5%, making it one of the most heavily promoted categories.

Activewear led pre-sale discounts at an impressive 26.7%, with an additional 4.5% discount during Black Friday week. Plus Size Clothing and Men’s Clothing tied for second place in pre-sale discounts at 21.9% each. Notably, Plus Size Clothing saw the highest Black Friday Week discount at 5.4%.

Women’s Clothing saw robust discounts throughout, with 20.8% pre-sale and an additional 6% during Black Friday Week (the highest additional discount in the category).

Share of Search: Brand Visibility Trends

White Stuff, the British lifestyle brand, saw a 7.2% surge in visibility during Black Friday. Y2K fashion made a statement as Juicy Couture jumped 5.8 %. Fast fashion player Pretty Little Thing gained in visibility by 5.2%. Comfort brands performed strongly, with Skechers gaining 4.5% and activewear specialist Sweaty Betty rising 3.4%. Even premium denim brand Levi’s gained ground, increasing share of search by 2.2%.

However, retail giants faced significant visibility challenges. John Lewis saw the steepest decline in the Apparel category, with share of search dropping by 10.6% during Black Friday week. Fast fashion giant Boohoo declined 2.5%. Premium accessory brand Coach’s share fell 4.9%.

The data suggests UK consumers gravitated toward distinctive brands with clear identities during Black Friday, whether heritage British labels, Y2K nostalgia, or comfort-focused specialists, rather than generalist retailers or fast fashion platforms.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

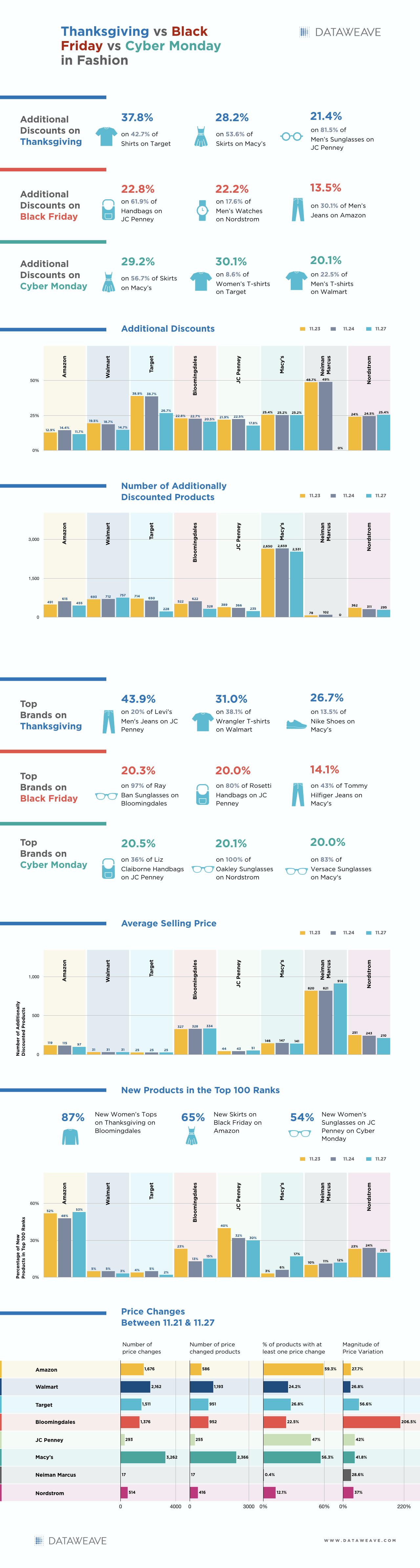

Black Friday 2025 shattered records once again. U.S. consumers spent a record $11.8 billion online on Black Friday, a 9.1% increase from 2024 and the first time online sales exceeded $11 billion. The National Retail Federation (NRF) projects holiday retail sales (November-December) to grow 3.7% to 4.2% over 2024, with total holiday spending expected to surpass $1 trillion for the first time ever. Against this backdrop of robust consumer spending, how did leading retailers and brands perform across key categories this Black Friday?

At DataWeave, we conducted a detailed analysis of Black Friday 2025 pricing trends across five major categories: Consumer Electronics, Home & Furniture, Health & Beauty, Grocery, and Apparel. Our AI-powered pricing intelligence platform monitored nearly 80,000 SKUs across leading U.S. retailers like Amazon, Walmart, Target, Macy’s, Home Depot, Sephora, and more, revealing interesting patterns in how retailers and brands approached this year’s sale season.

Our Methodology

For this analysis, DataWeave monitored average discounts across leading U.S. retailers during two distinct periods:

Pre-Black Friday: Up to November 23, 2025 – capturing early holiday deals and baseline pricing

Additional Discounts During Black Friday Week: November 24 – December 1, 2025 – covering Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

Our sample encompassed the top-ranked products across subcategories on major retail sites. We also analyzed Share of Search data, which measures brand visibility by monitoring which brand names appear in the top 20 search results for critical keywords.

Black Friday 2025: The Big Picture

Here’s the snapshot of average discounts during the Pre-Black Friday period compared to Black Friday Week:

Key Insight: Pre-Black Friday discounts were significant across all categories. This suggests retailers front-loaded their promotions to capture early holiday shoppers, with additional discounts during Black Friday Week adding to the baseline discounts already in place.

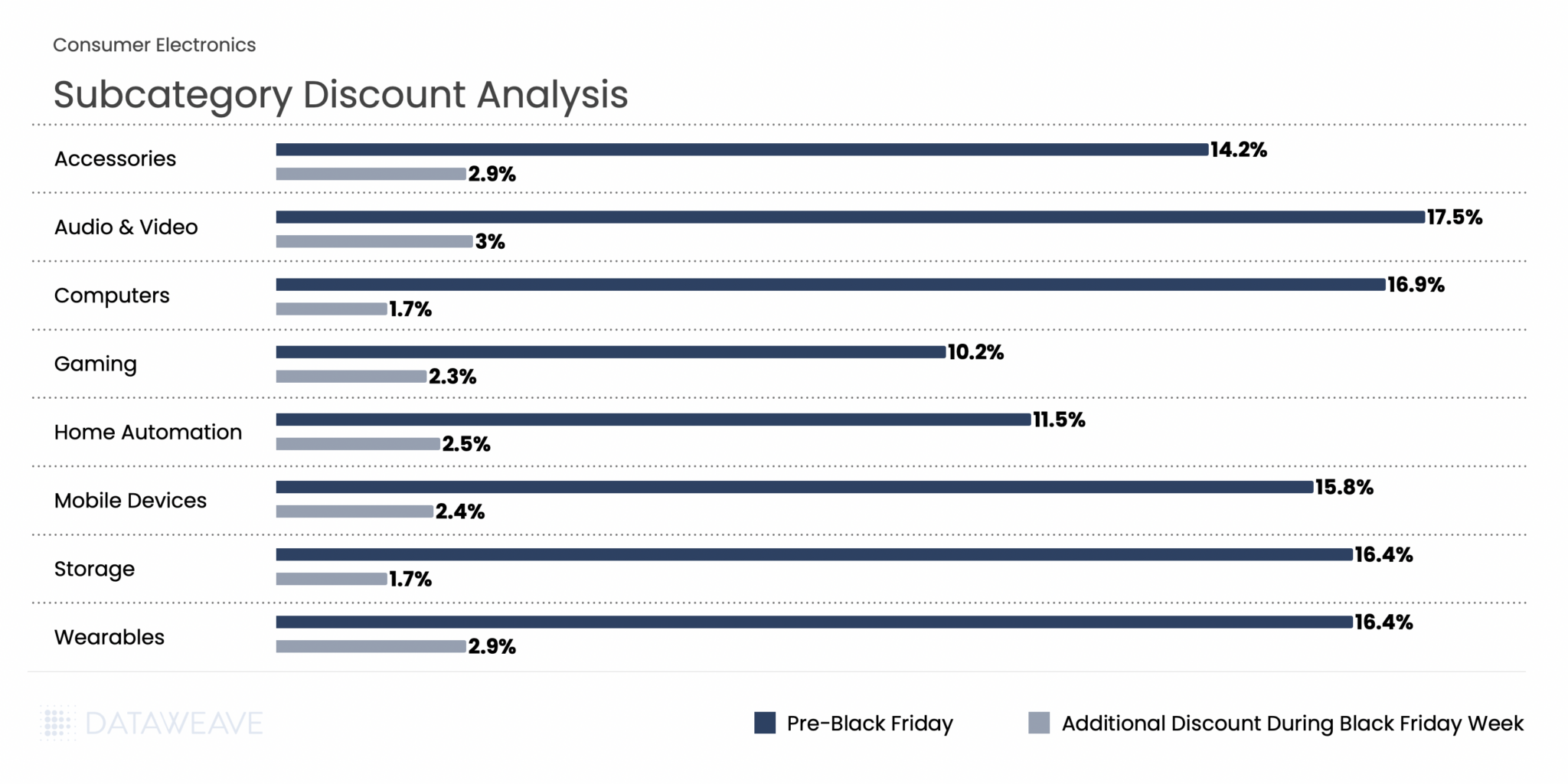

Consumer Electronics

Consumer electronics remain one of the most anticipated categories during Black Friday and Cyber Monday. Notably, AI traffic to retail websites grew 805% year-over-year, with consumers using AI tools most frequently for video games, appliances, and electronics categories. Our analysis of 10,356 SKUs reveals how discounts varied across subcategories.

Subcategory Discount Analysis

In Consumer Electronics, Pre-Black Friday discounts averaged 14.6% across subcategories, while Black Friday Week saw an additional 2.6% discount on average. Audio & Video products led the pre-sale discounting at 17.5%, indicating retailers were eager to move inventory early. During Black Friday Week, Audio & Video, Accessories, and Wearables saw the highest additional discounts (2.9-3 %), while Computers and Storage had already been heavily discounted pre-sale, leaving minimal room for further reductions during the main event.

Share of Search: Brand Visibility Trends

Our Share of Search analysis reveals significant shifts in brand visibility during Black Friday Week:

The Takeaway: Our analysis reveals significant shifts in brand visibility during Black Friday Week compared to the pre-sale period. Computing and mobile-focused brands like Apple and Asus gained substantial ground, while audio brands like Logitech, JBL, and Beats saw their visibility plummet. Apple’s Share of Search jumped from 1.58% to 6.2%, a gain of 4.6%, suggesting strong promotional activity or heightened consumer interest. Meanwhile, Logitech dropped nearly 8%, from 9.9% to just 1.2%.

Home & Furniture

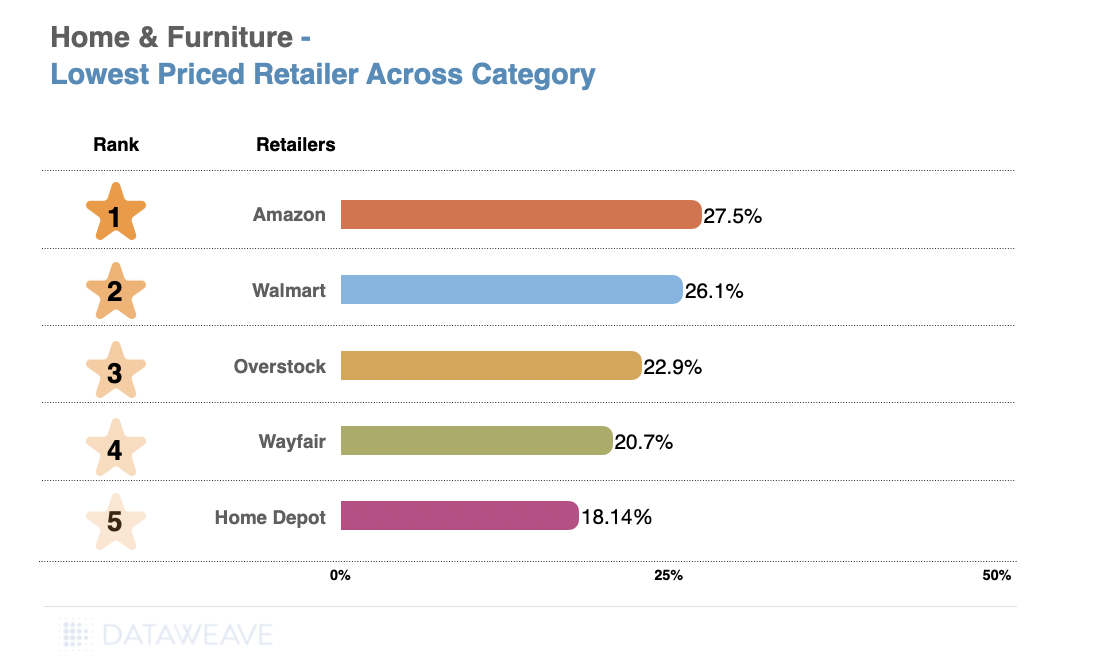

The Home & Furniture category continues to be a consumer favorite during Black Friday. Our analysis of 12,610 SKUs shows how discounts were distributed across subcategories.

Subcategory Discount Analysis

Home & Furniture saw Pre-Black Friday discounts averaging 13.9%, with Black Friday Week adding just 1.7% on average, the second-lowest additional discount among all categories. Bedding led pre-sale discounts at an impressive 18.6%, followed by Furniture at 16.4% and Outdoor at 15.1%. This suggests retailers aggressively promoted home goods early in the season to capture deal-seekers.

During Black Friday Week, Bedding maintained leadership with 2.4% additional discounts, while Kitchenware saw the smallest bump at just 0.9%, indicating early promotions had already captured most of the discount opportunity.

Share of Search: Brand Visibility Trends

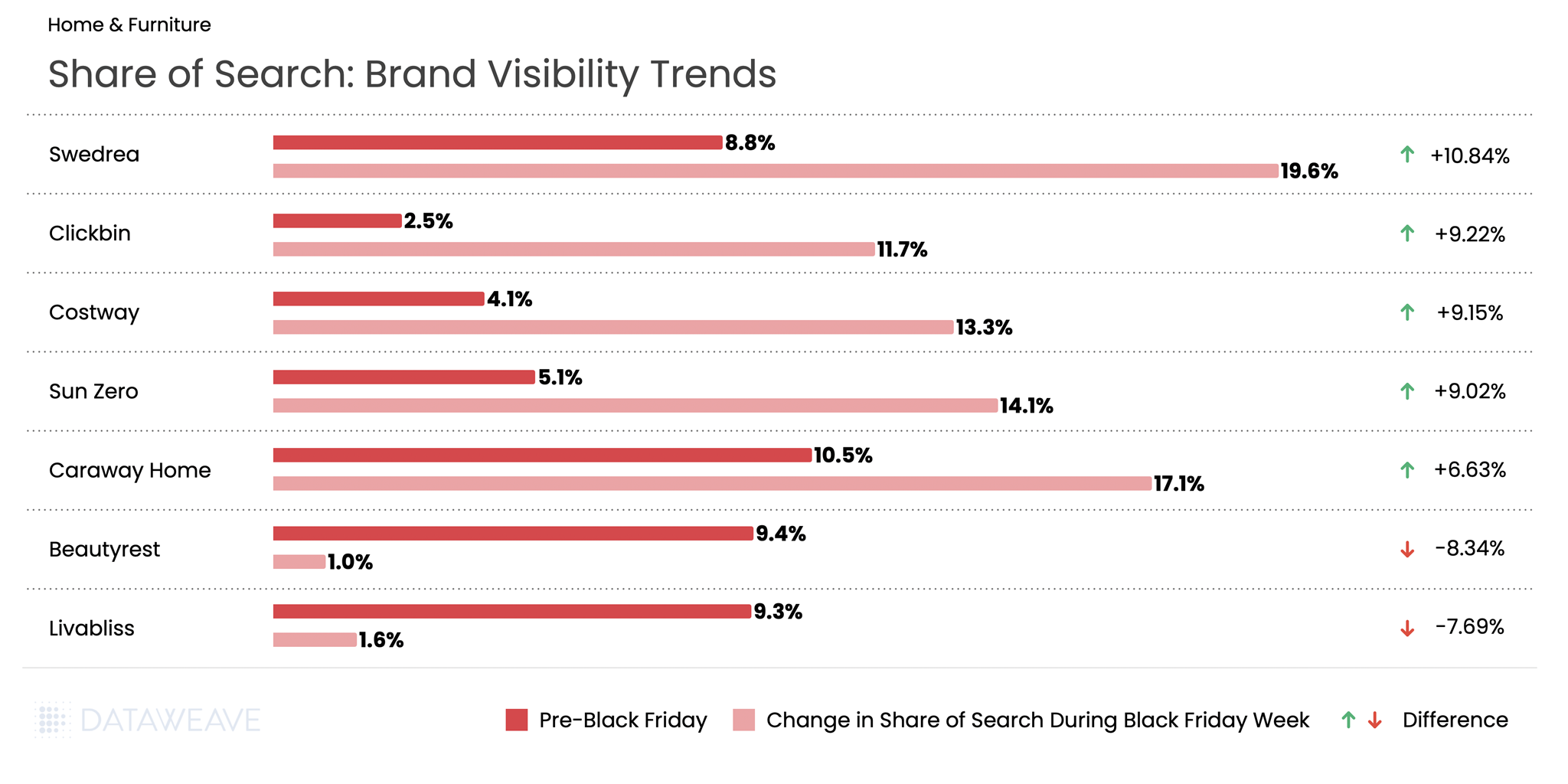

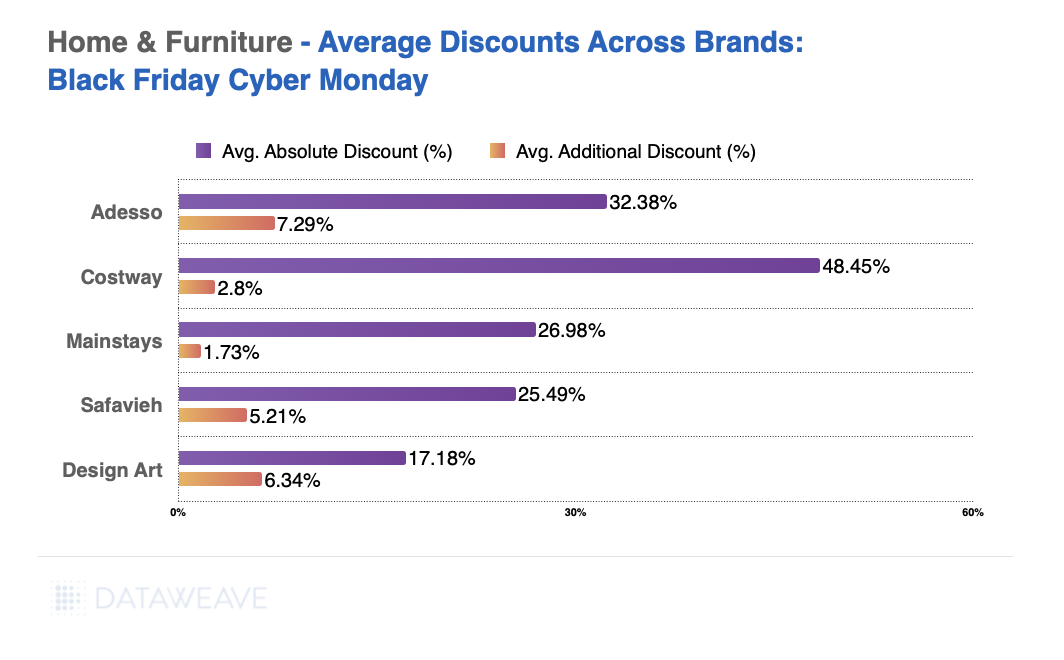

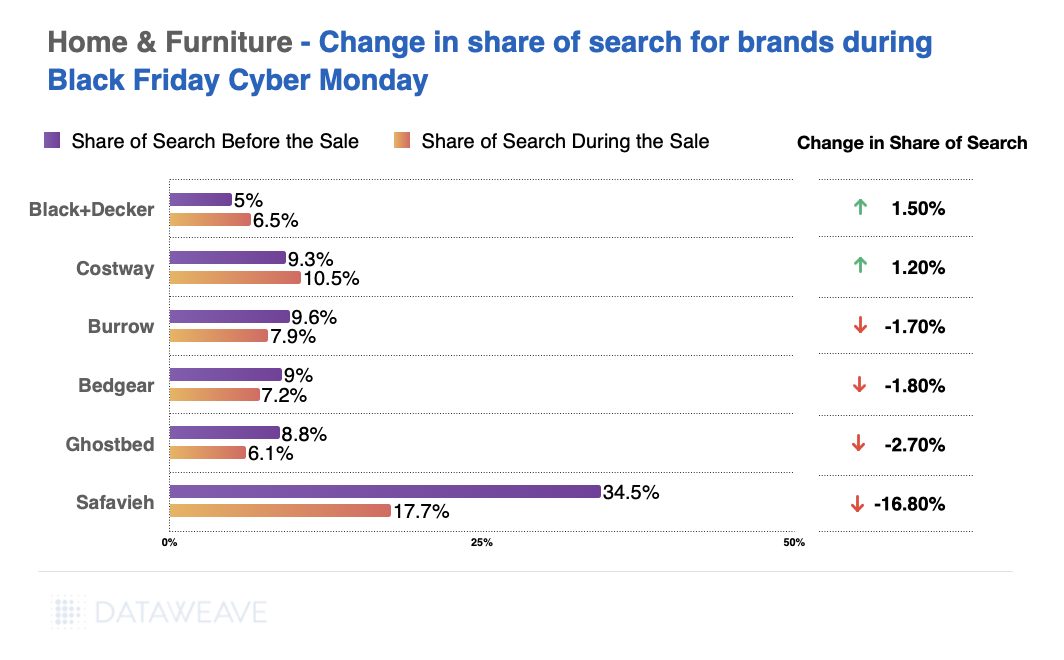

The Takeaway: The Home & Furniture category saw some of the most dramatic Share of Search swings in our entire analysis. Emerging and value-oriented brands dominated the gains, with Swedrea surging from 8.7% to 19.6%, a remarkable 10.8% increase. Similarly, Clickbin and Costway each gained over 9%. On the flip side, established premium brands like Beautyrest and Livabliss saw sharp visibility declines, dropping over 7-8%.

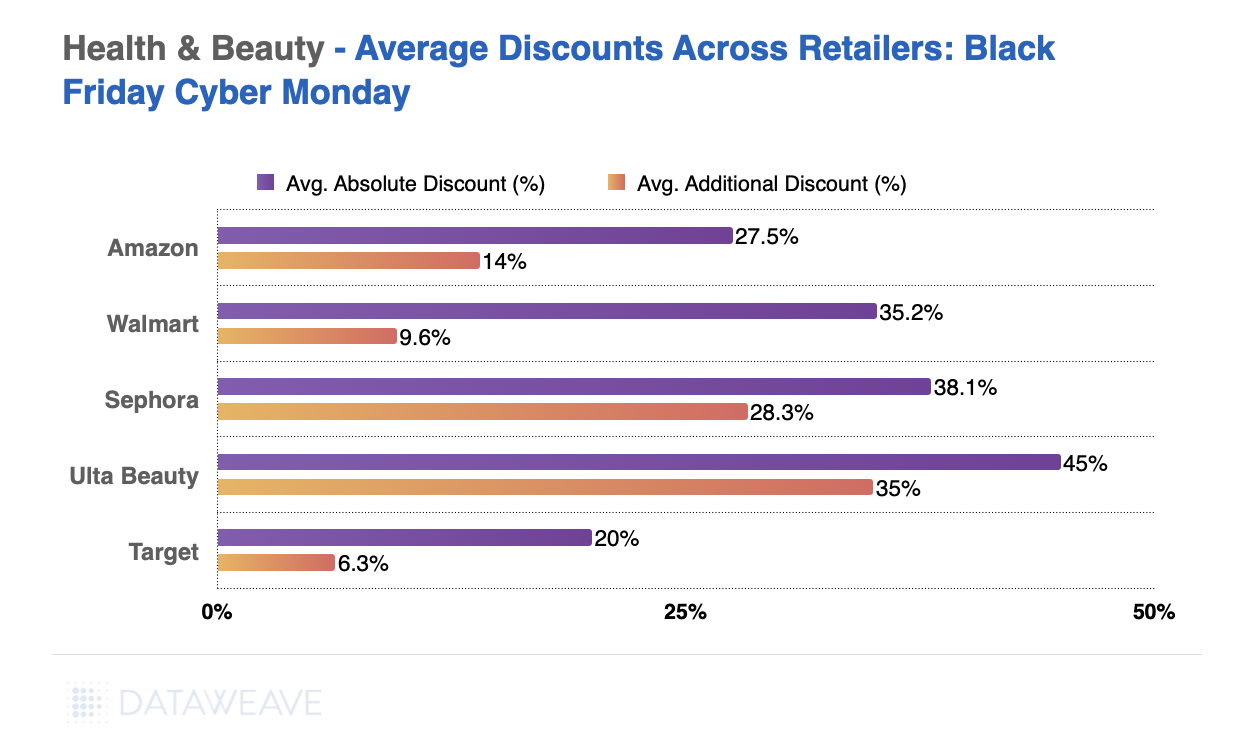

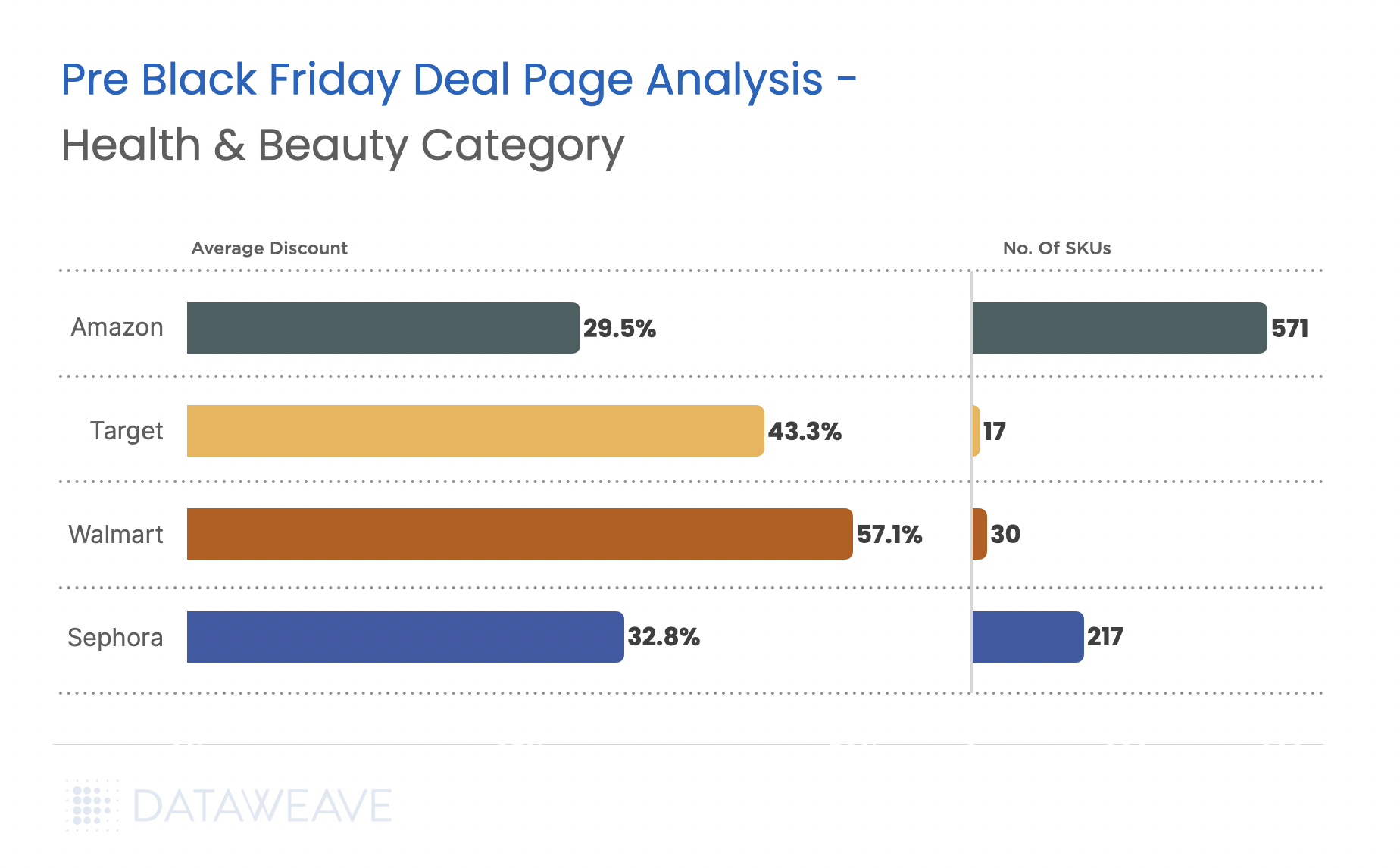

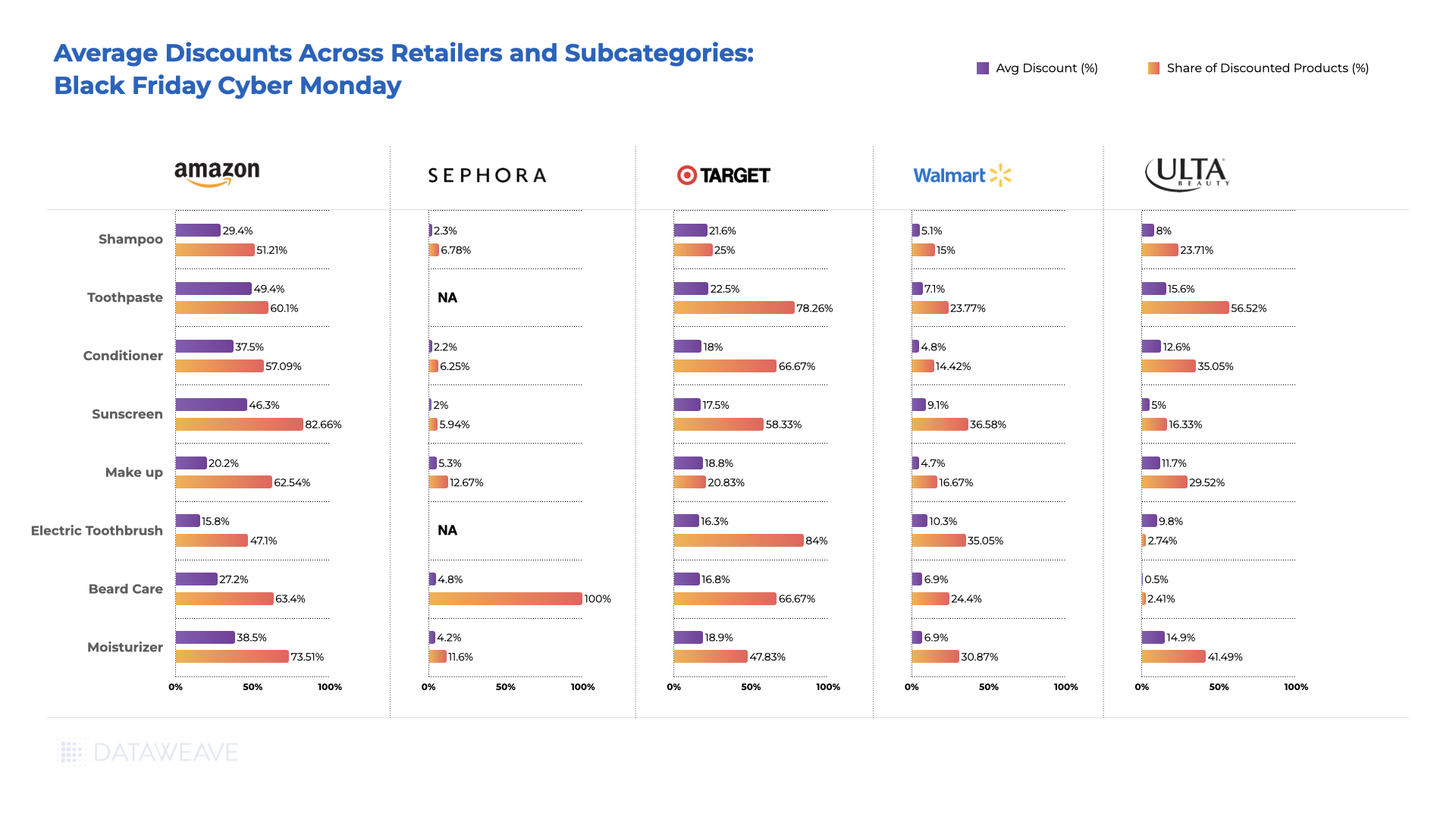

Health & Beauty

Health & Beauty has emerged as a growth engine during Black Friday. The beauty industry is projected to grow 5% annually through 2030 according to a McKinsey survey. Our analysis of 16,141 SKUs reveals subcategory-level insights.

Subcategory Discount Analysis

Notable finding: Health & Beauty presented a unique discounting pattern compared to other categories. Pre-Black Friday discounts averaged just 7.1%, the second-lowest among all categories. But Black Friday Week discounts were relatively strong at 4.8%. This indicates the Beauty category held back more discounts for the main event.

Notably, Hair Care was the only subcategory across our entire analysis where Black Friday Week discounts (6%) exceeded Pre-Black Friday discounts (4.6%), suggesting retailers strategically saved their best hair care promotions for the big weekend. Fragrance led pre-sale discounts at 13%, making it an attractive early shopping category.

Share of Search: Brand Visibility Trends

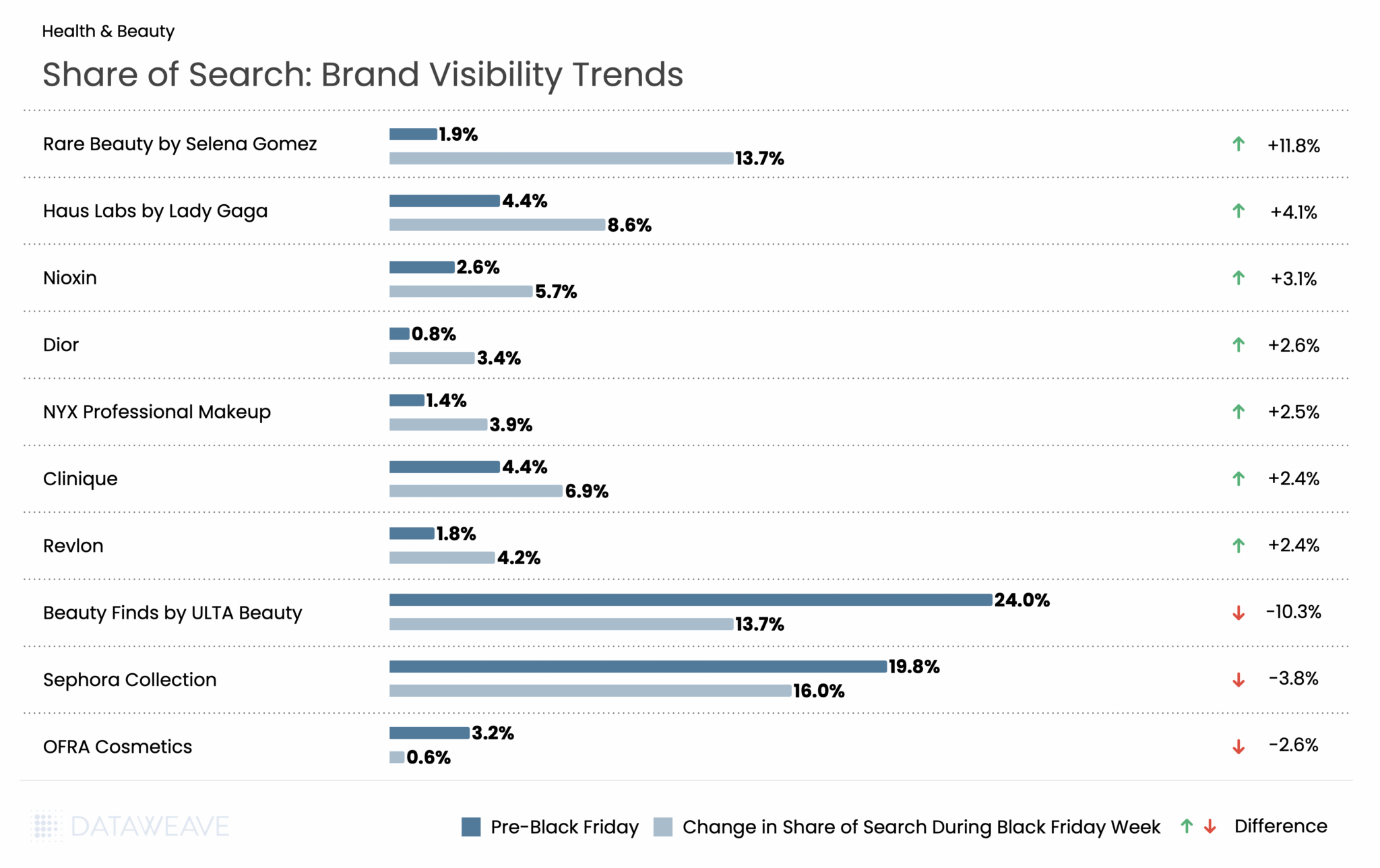

Health & Beauty saw some of the most dramatic Share of Search swings in our analysis, driven largely by celebrity-backed brands. Rare Beauty by Selena Gomez exploded from just 1.9% to 13.7%, a whopping 11.8% gain that made it the biggest winner across all categories. Haus Labs by Lady Gaga also surged (+4.1%), while prestige brands like Dior (+2.6%) and Clinique (+2.4%) gained ground.

The flip side? Retailer private labels took a hit: Beauty Finds by ULTA Beauty collapsed from 24% to 13.7% (-10.3%), and Sephora Collection dropped from 19.8% to 16.0% (-3.8%).

Key Takeaway: The Beauty category tells a compelling story about the power of celebrity brands during Black Friday. The Share of Search shifts appear to reflect how retailers and brands recalibrated their promotional focus for Black Friday. Celebrity-driven lines rose sharply in visibility, suggesting stronger placement, promotion, or search prioritization during the sale period. At the same time, private-label ranges from ULTA and Sephora lost ground, indicating a pivot away from house-brand visibility in favor of more spotlighted national and prestige brands throughout the event.

Grocery

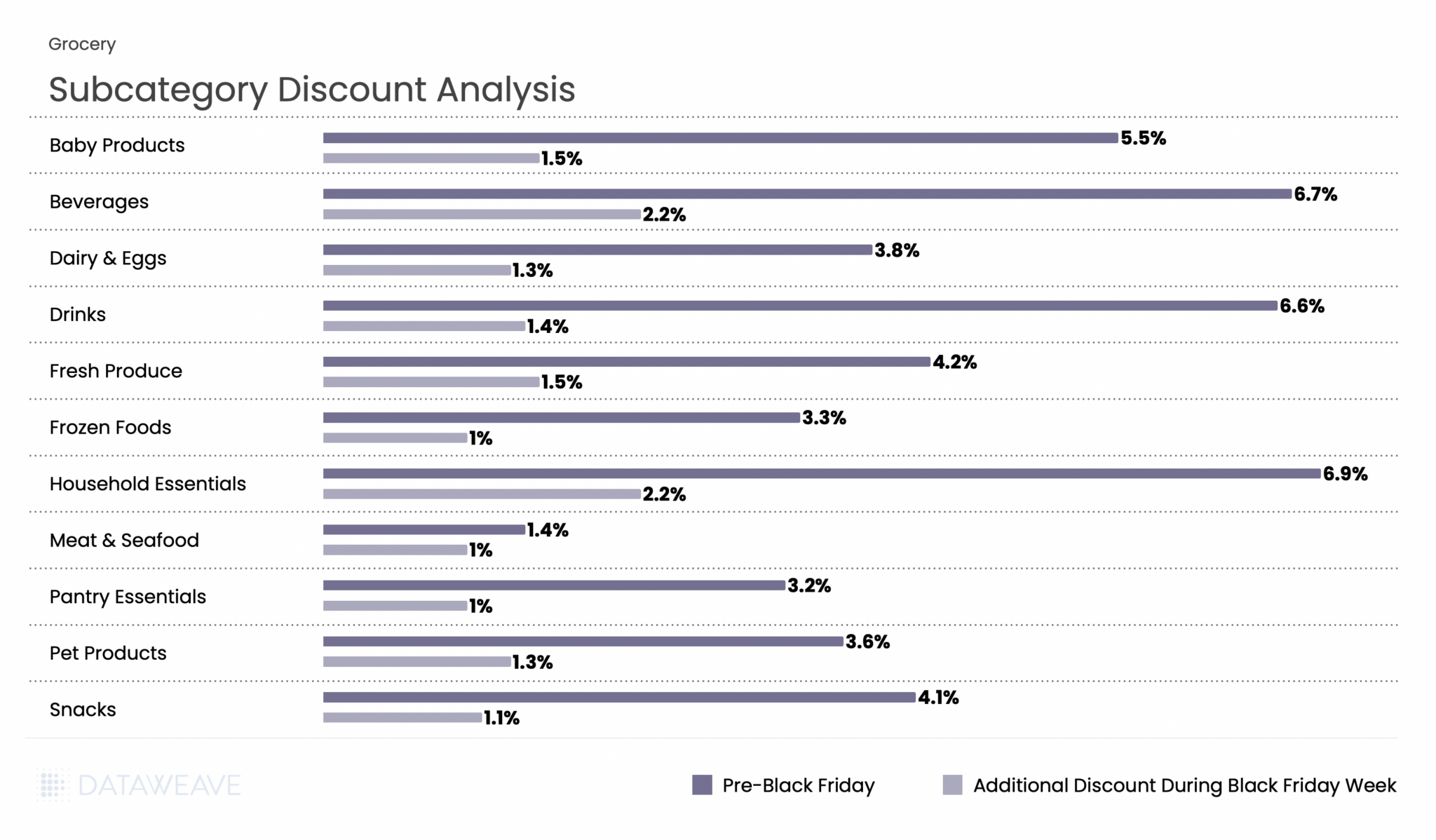

While Grocery typically sees more modest discounts compared to discretionary categories, the sector remains a critical part of Thanksgiving weekend shopping. According to the National Retail Federation, grocery stores and supermarkets ranked as the third most popular shopping destination during Thanksgiving weekend, with 40% of consumers making purchases there. Our analysis of 18,823 SKUs shows how retailers approached promotions across essential and indulgent subcategories.

Subcategory Discount Analysis

Grocery had the lowest discounts across all categories, reflecting the already-thin margins in food retail. Pre-Black Friday discounts averaged just 5.2%, with Black Friday Week adding only 1.5%. Household Essentials and Beverages led pre-sale discounts at 6.9% and 6.7% respectively, and maintained their lead during Black Friday Week with 2.2% additional discounts each. Fresh categories like Meat & Seafood (1.4% pre-sale, 1% Black Friday Week) and Frozen Foods (3.3%, 1%) saw minimal promotional activity, consistent with perishable inventory constraints and tight margins.

Key Takeaway: Grocery discounting remains conservative, with shelf-stable and household items seeing the most promotional activity. The Beverages and Household Essentials subcategories, which have longer shelf life and higher margins, were the primary battleground for grocery promotions during BFCM 2025.

Share of Search: Brand Visibility Trends

The Grocery category saw some surprising Share of Search swings during Black Friday Week. Most notably, there was a dramatic divergence between beverage giants: Sprite surged from 1.7% to 6.8% (+5.1%), while Coca-Cola collapsed from 6% to just 0.1% (-5.9%). This stark contrast suggests vastly different promotional strategies or algorithmic visibility changes between the two brands. Private label 365 by Whole Foods Market continued its steady rise, gaining 3%, reflecting ongoing consumer interest in store brands as shoppers seek value.

The Sprite vs. Coca-Cola divergence is one of the most striking findings in our analysis. Additionally, brands like Amy’s (organic/natural foods) and McCormick (spices/seasonings) gained significant visibility.

Apparel

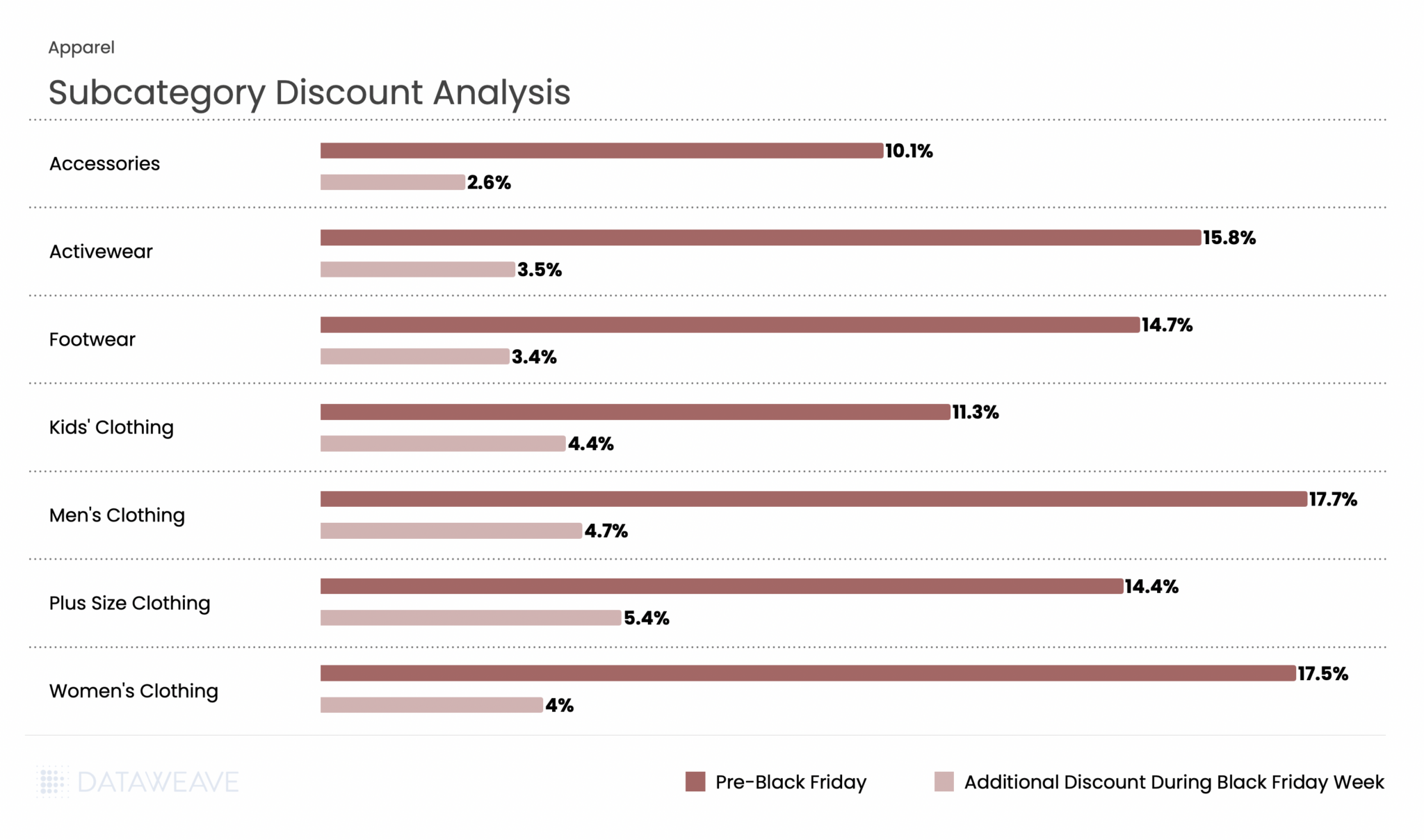

Apparel remains a Black Friday staple and performed strongly this year. Our analysis of 21,749 SKUs (the largest category in our study) reveals interesting patterns.

Subcategory Discount Analysis

Apparel showed strong discounting activity throughout the BFCM period. Pre-Black Friday discounts averaged 13.8%, with Black Friday Week adding 3.8%, the highest additional discount among all five categories. Men’s Clothing and Women’s Clothing led pre-sale discounts at 17.7% and 17.5% respectively, reflecting aggressive early promotions on core apparel. Interestingly, Plus Size Clothing saw the highest Black Friday Week discount at 5.4%, suggesting retailers pushed harder during the main event to drive conversions in this segment. Kids’ Clothing also saw strong Black Friday Week discounts at 4.4%.

Share of Search: Brand Visibility Trends

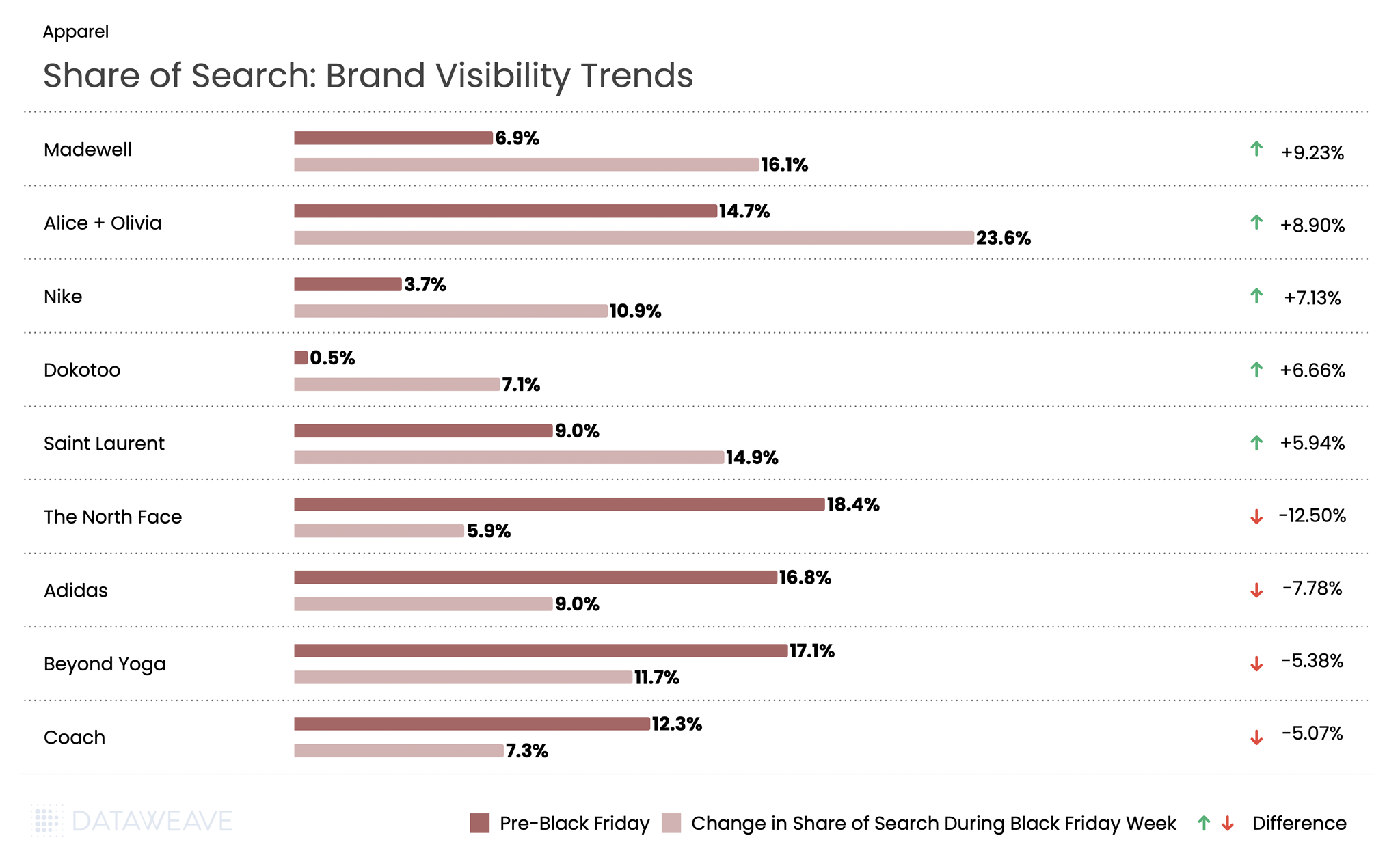

Apparel saw dramatic Share of Search movements during Black Friday Week. Fashion-forward brands dominated the gains: Madewell surged from 6.9% to 16.1% (+9.2%), while Alice + Olivia jumped from 14.7% to 23.6% (+8.9%). Nike also performed strongly with a 7.1% gain. Conversely, outdoor and athletic brands faced steep declines: The North Face dropped from 18.4% to 5.9%, a massive 12.5% decline, the largest in our entire analysis. Adidas fell 7.7%, Beyond Yoga declined 5.3%, and luxury brand Coach by 5%.

Key Takeaway: The data suggests fashion-forward and lifestyle brands (Madewell, Alice + Olivia, Saint Laurent) gained visibility at the expense of outdoor/athletic brands (The North Face, Adidas, Beyond Yoga). This could indicate that fashion brands invested more heavily in promotional visibility during the sale period.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Follow our blog for more insights on retail pricing trends, brand visibility analysis, and data-driven commerce intelligence.

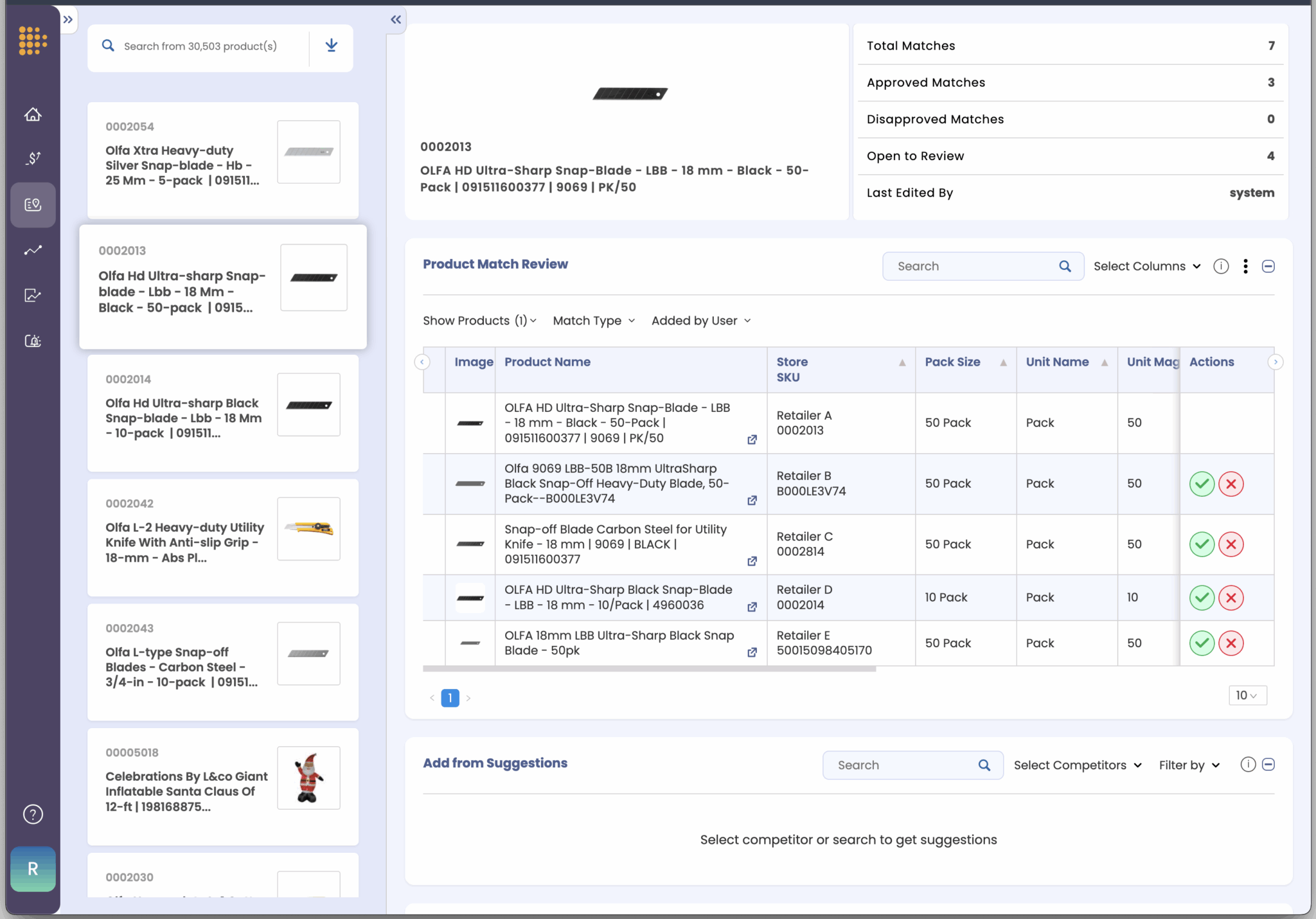

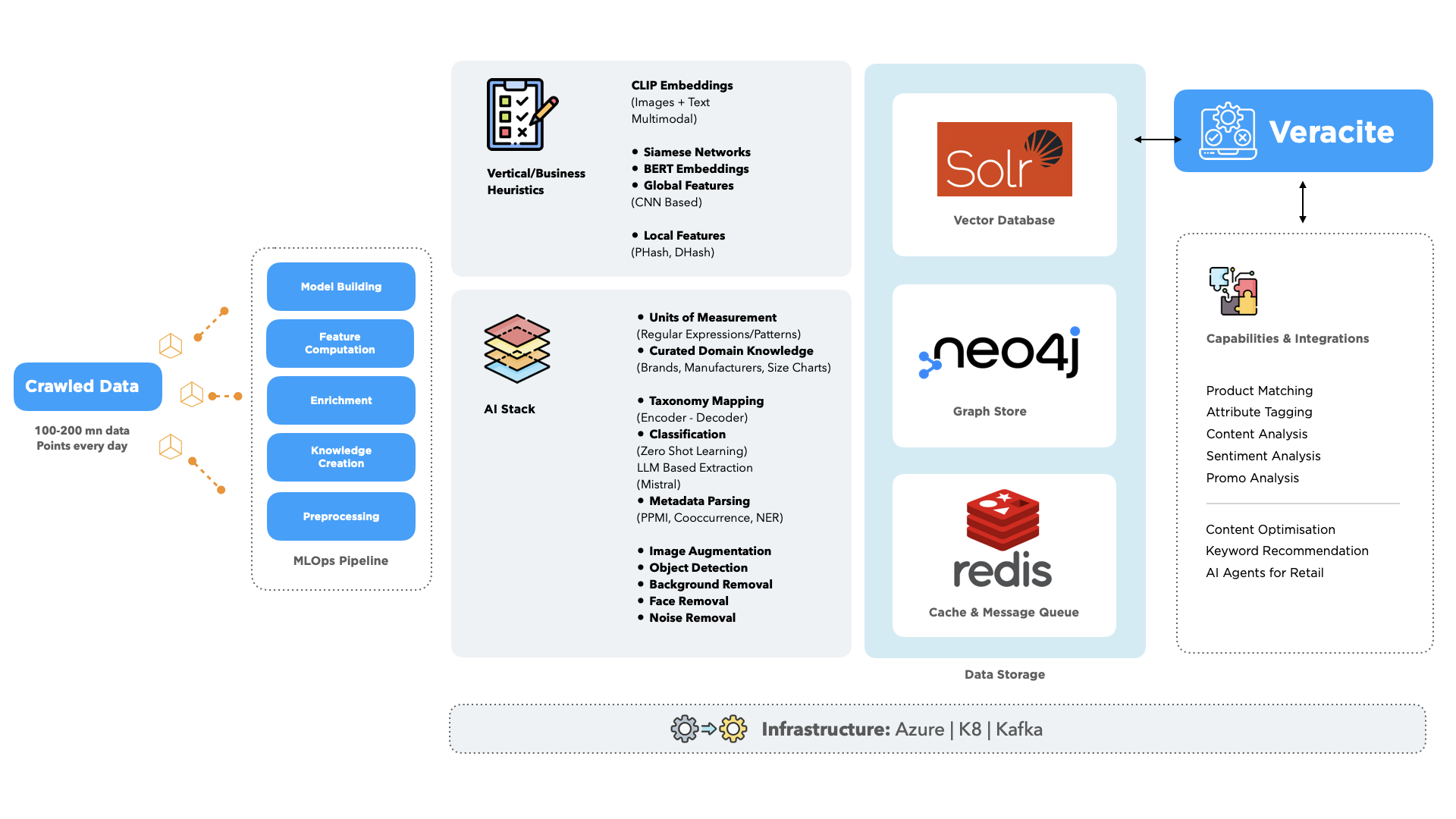

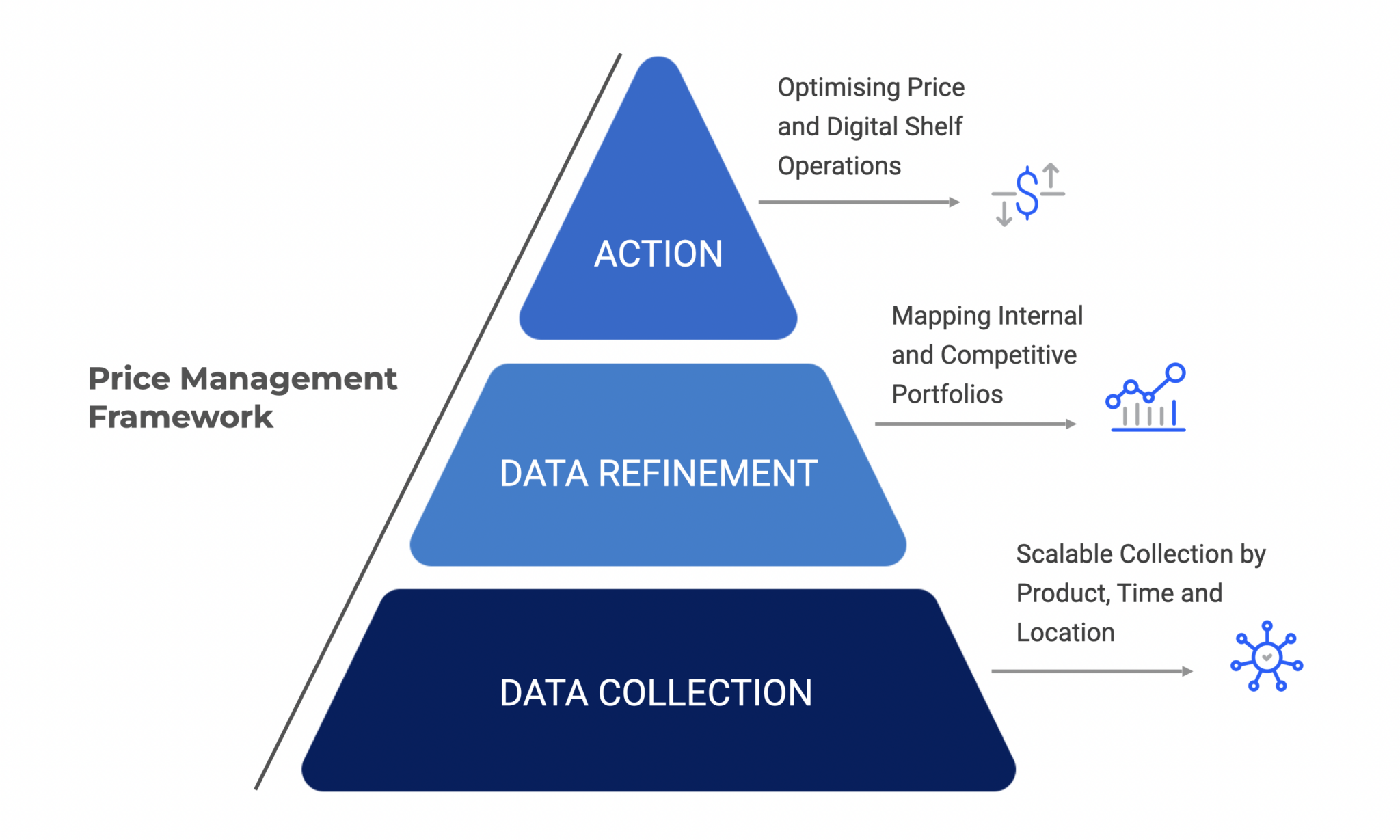

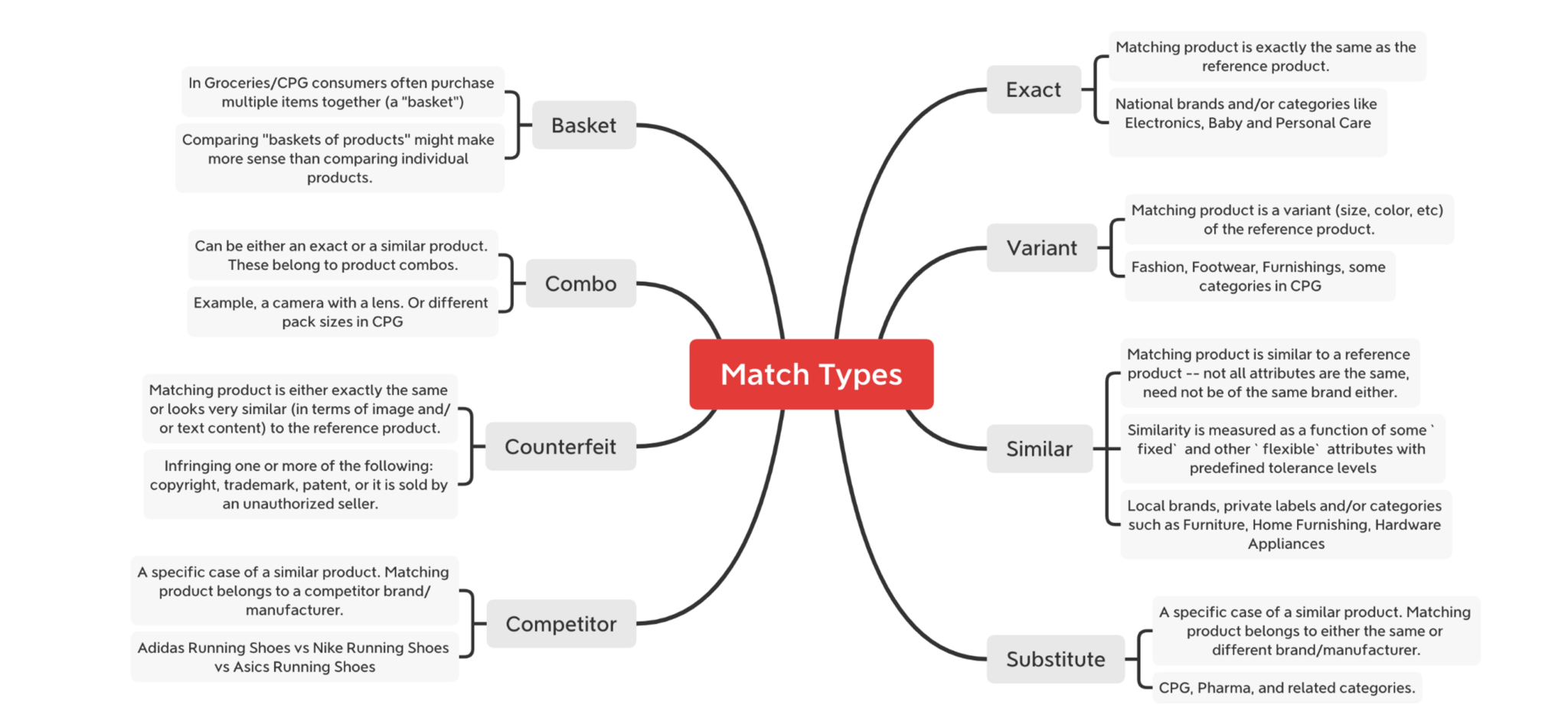

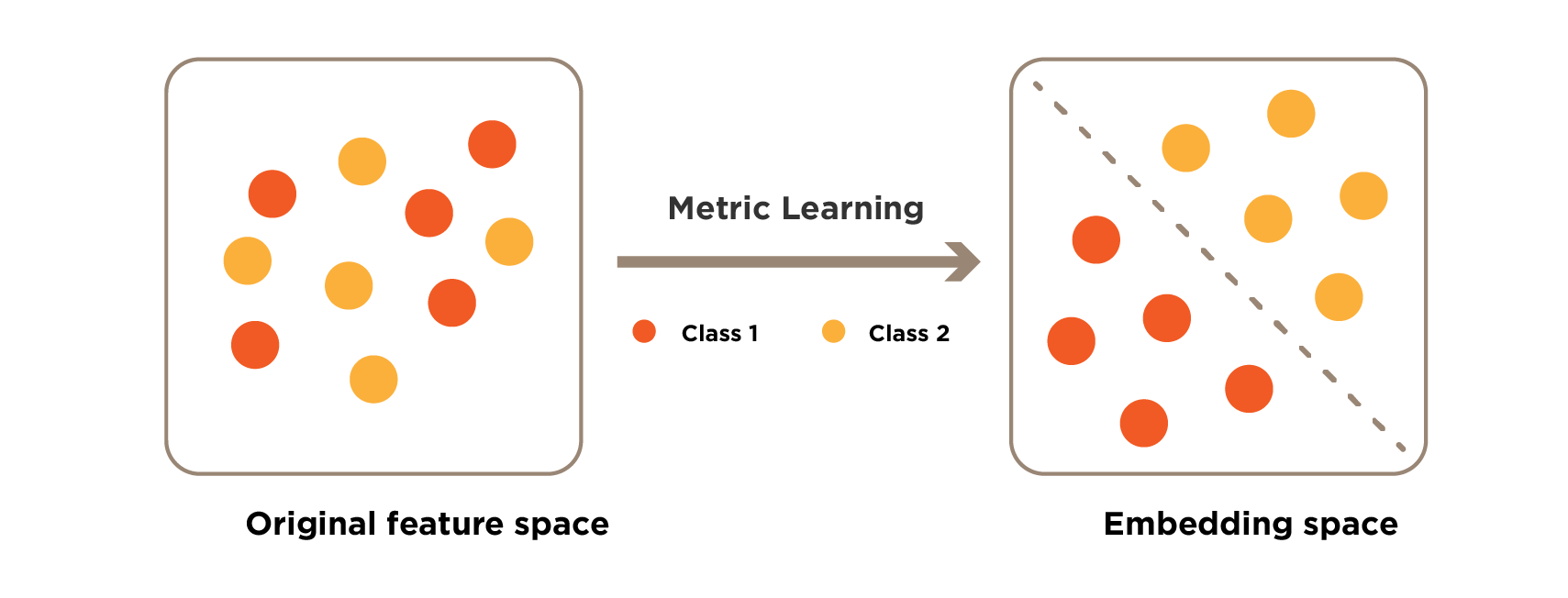

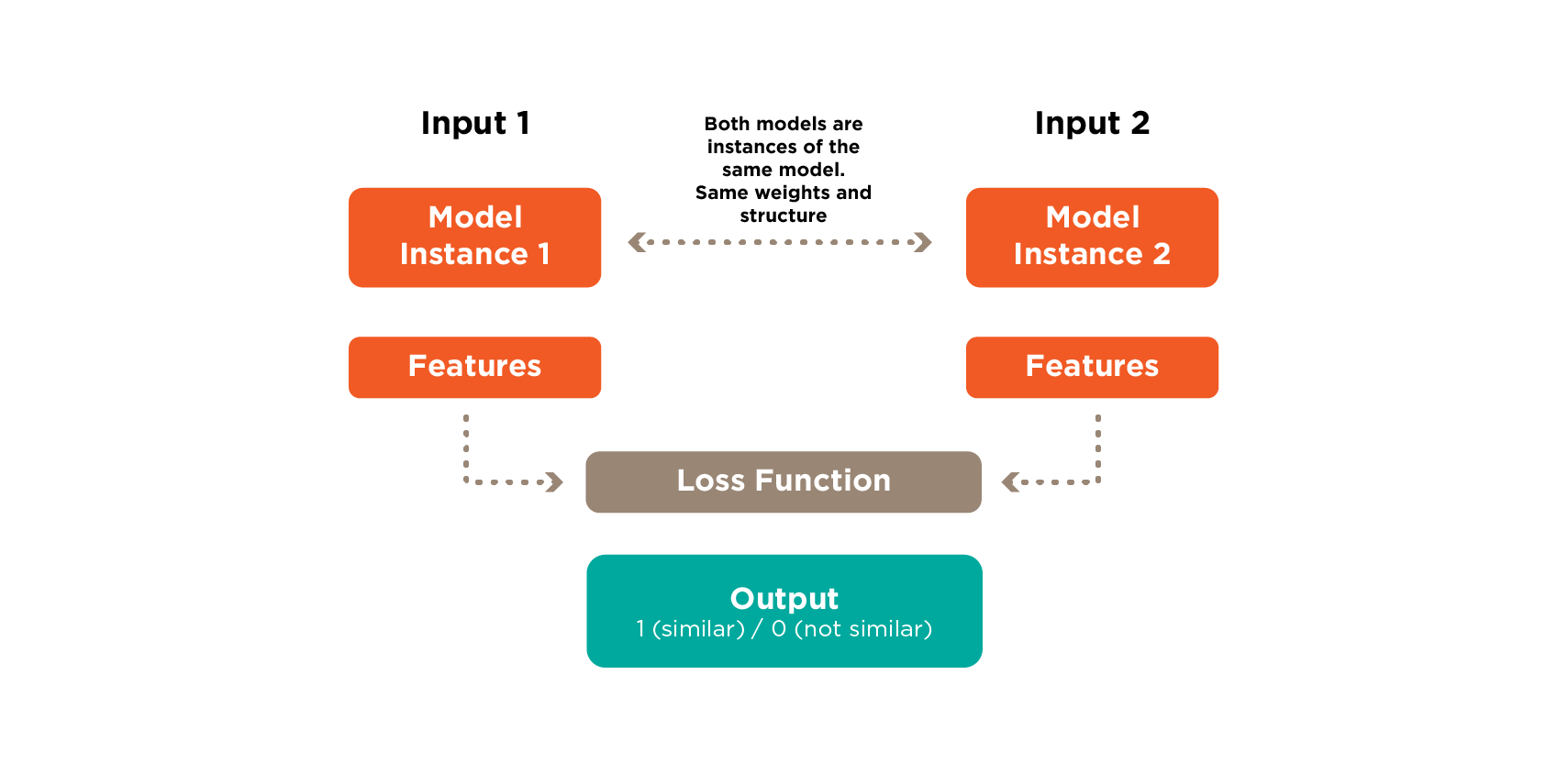

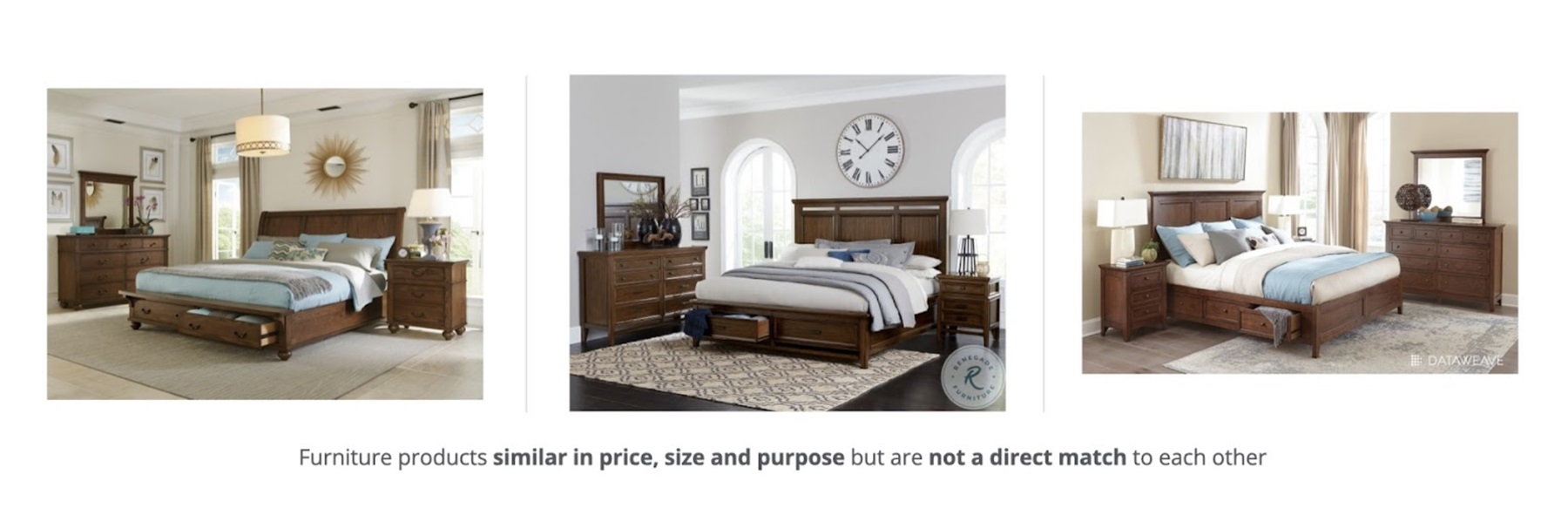

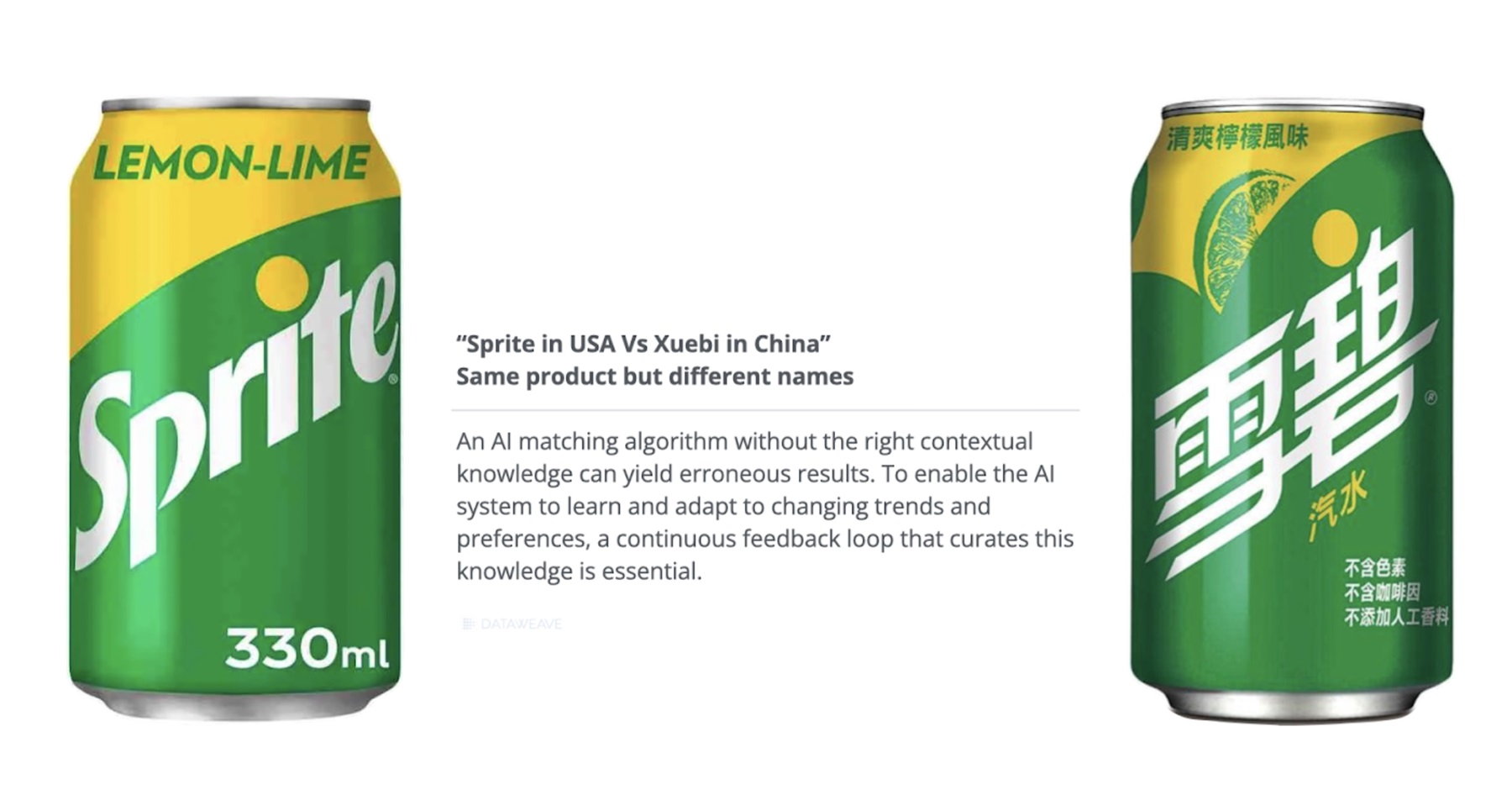

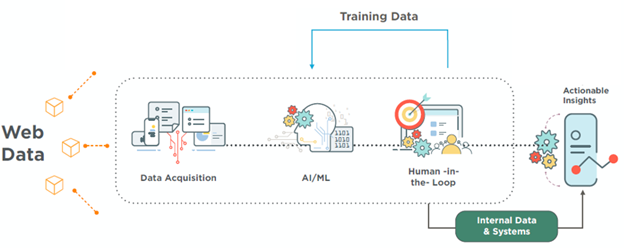

AI-powered product matching is the backbone of competitive pricing intelligence. Accurate matches help you compare prices correctly, identify meaningful assortment gaps, and optimize product content. Inaccurate matches distort every one of these insights. In some categories, a single mismatch can cause millions of dollars of lost revenue.

Retailers and brands know this problem well. Product catalogs are vast. Competitor assortments shift daily. Titles are inconsistent. Product codes are missing. Images vary by region or packaging. Basically, context matters, and AI alone often misses that context.

This is why a human-in-the-loop approach is essential. It allows product matches to be verified consistently, at scale, and with the context that only people can provide. Many retailers have also told us they want to take this a step further. They want the ability to control and define their own product matches.

Sometimes that is because they need to fix inevitable errors quickly. Other times, it is because their teams have deeper category knowledge and can make the right judgment calls when AI falls short.

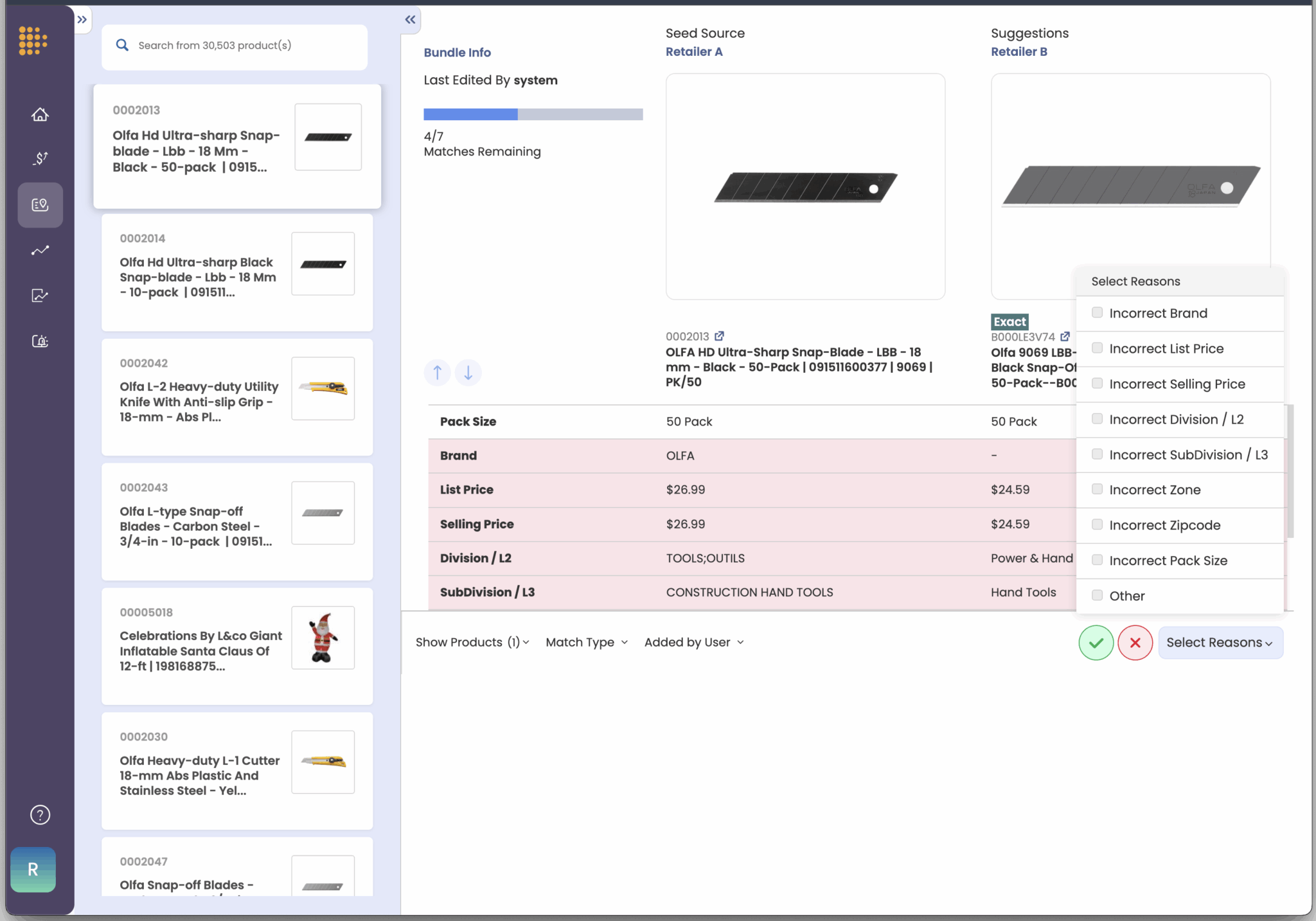

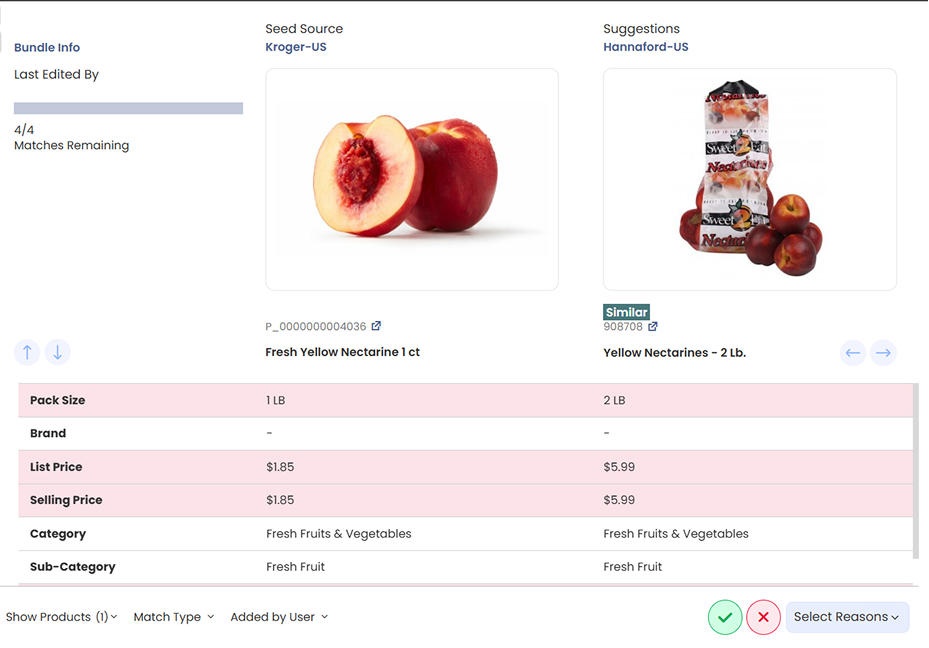

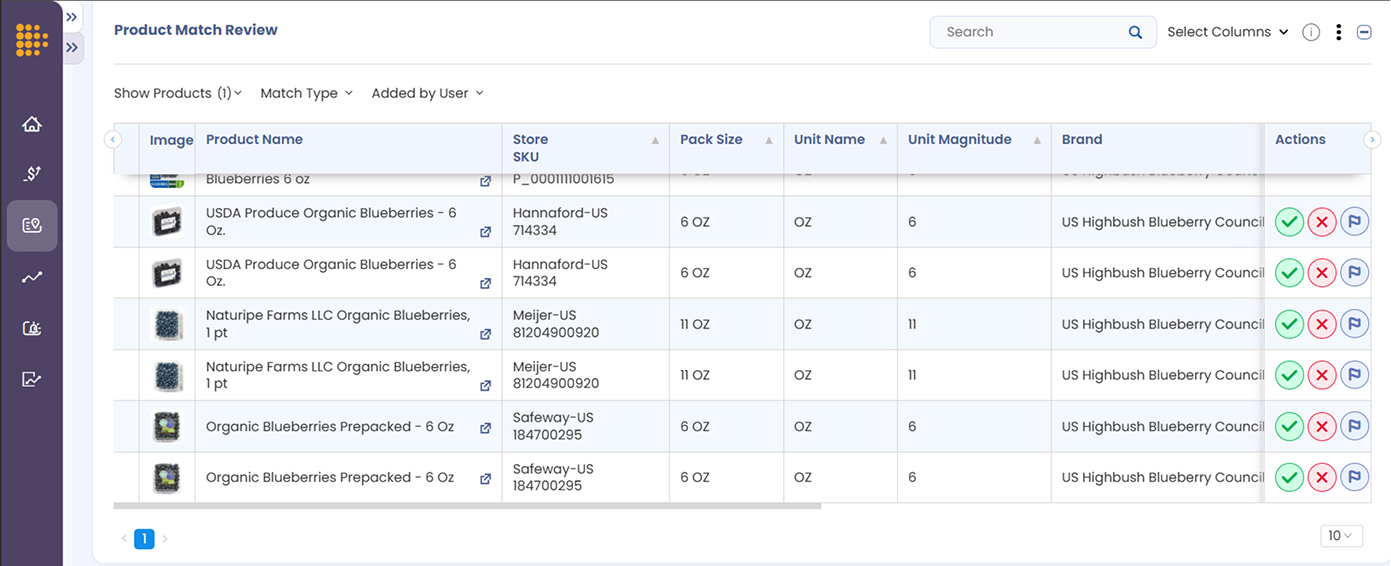

To make that possible,DataWeave introduced User-Led Match Management. It combines the scale of AI with the judgment of experts within retail organizations. The platform does not just suggest matches. It gives your teams the tools to approve, reject, or refine them. This ensures your competitive intelligence reflects both machine precision and your unique business logic.

Why AI Matching Alone Falls Short

AI has changed the speed and scale of product matching. Algorithms can process millions of SKUs quickly. They can detect similarities in text, images, and metadata. But in retail, the stakes are too high to rely on AI alone.

Here is where AI sometimes falls short:

Category complexity: Matching rules that work in electronics may fail in fashion or grocery. An electronics SKU may depend on a model number. A fashion SKU may depend on seasonality. A grocery SKU may depend on pack size or whether it is a private label.

Data inconsistency: Titles vary. Images differ across regions. These gaps, when large, trip up algorithms.

Business context: Should a premium product ever be compared against a budget line? Should seasonal products match year-round items? AI may not know these boundaries.

Scale vs. accuracy: Automated systems optimize for coverage. That speed often limits accuracy for a small set of SKUs. Even a 1% error rate across millions of SKUs creates thousands of bad comparisons.

AI is critical for scale. But accuracy requires human input. DataWeave’s human-in-the-loop framework addresses this by allowing expert reviewers to validate and improve AI outputs. Our user-led match management takes this further by putting control directly into the hands of your business teams.

What DataWeave’s User-Led Match Management Delivers

With User-Led Match Management, your team is not a passive reviewer. They become active participants in shaping the accuracy of your competitive intelligence.

Your teams can:

Approve, reject, or flag AI-suggested matches. Every suggestion comes with full visibility into why it was made. Your team can validate matches quickly, fix errors, and improve the dataset in real time.

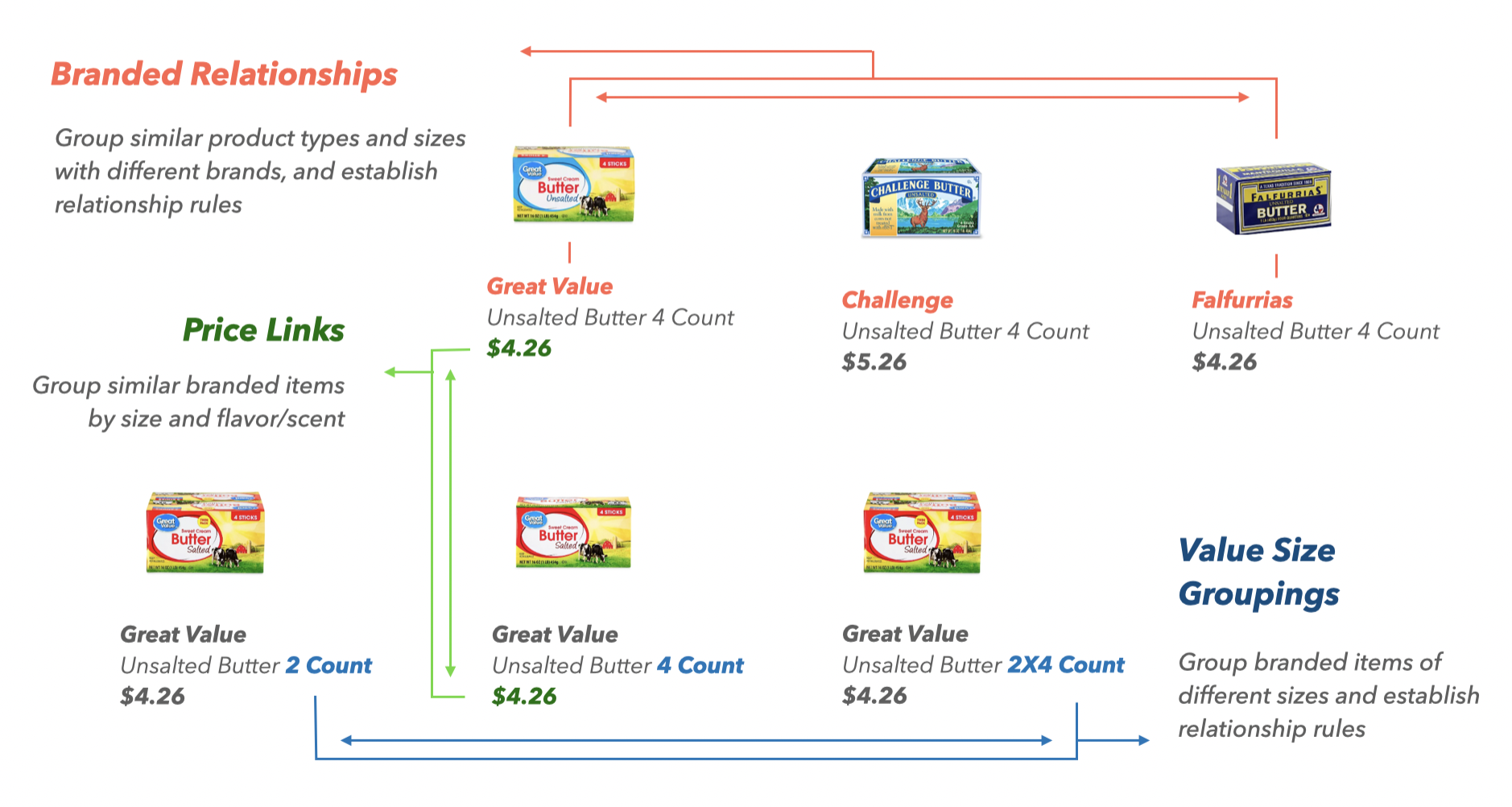

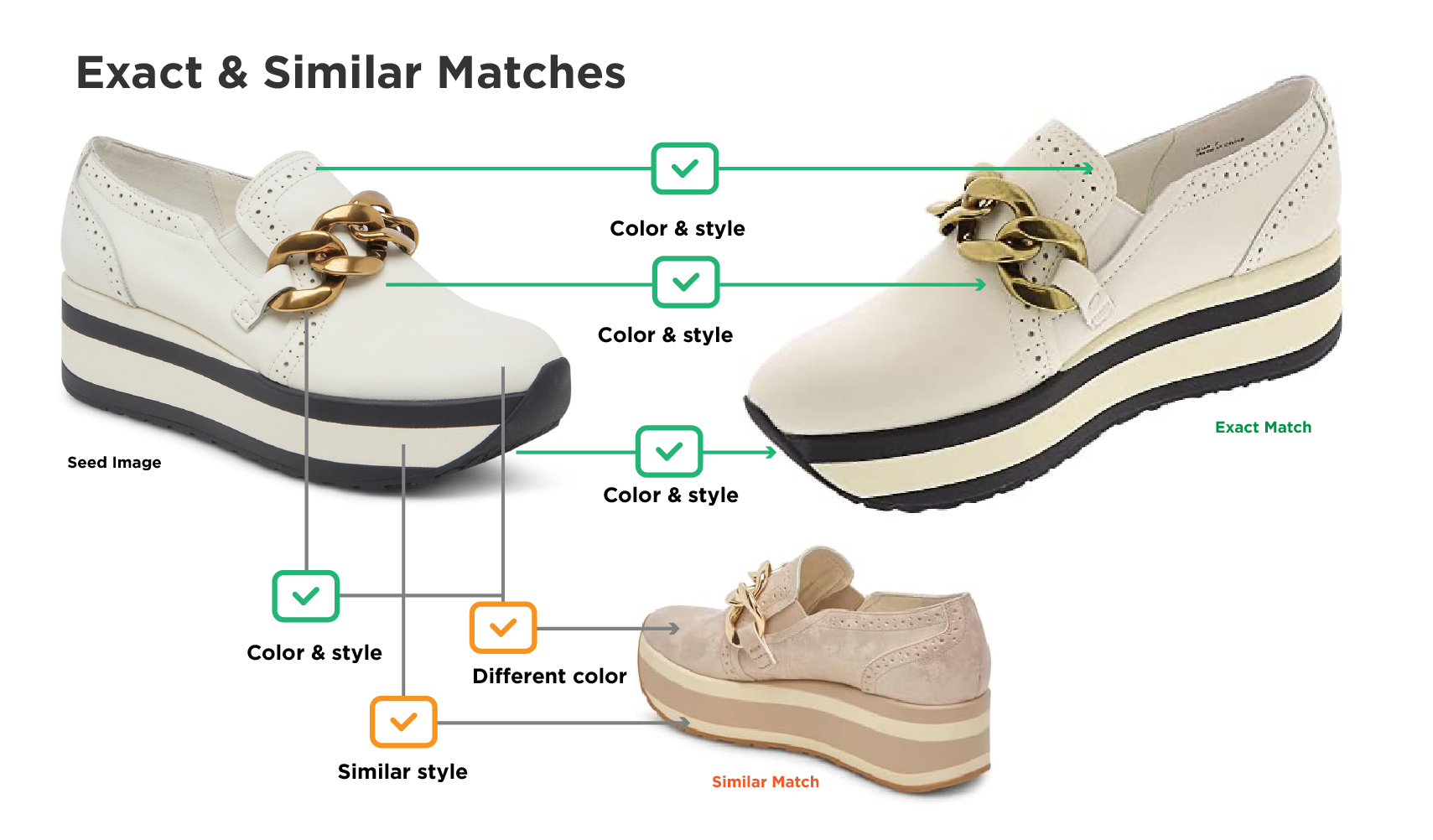

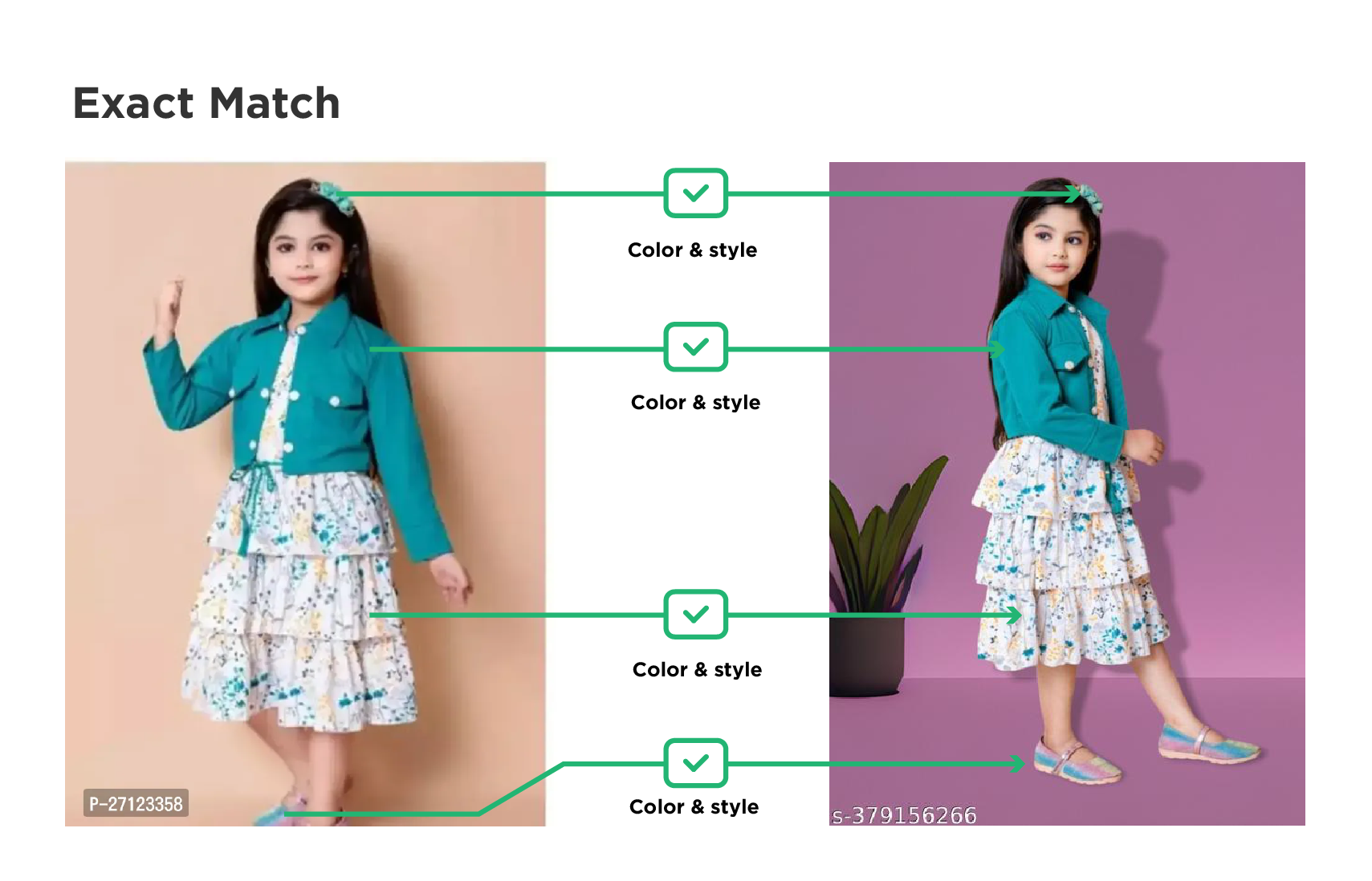

Define what “similar” means for your business. A retailer may want to compare multipacks against single packs. A brand may only care about comparing premium products to other premium products. With User-Led Match Management, your team sets tolerance levels that match your strategy.

Manually add or refine matches. When AI misses edge cases, your team can add them. This ensures coverage is complete and reflects the true competitive landscape.

This approach creates a loop where AI, complemented by DataWeave’s human-in-the-loop framework does the heavy lifting, and your teams can fine-tune the results. The outcome is both scale and accuracy.

Key Features

DataWeave designed User-Led Match Management to be simple, intuitive, and scalable:

Expert-Led Decision Making forms the heart of the system. Rather than trusting AI suggestions blindly, teams gain full visibility into matching logic and can leverage their contextual knowledge of products, categories, and retailers. When the system suggests matching a premium product against a basic alternative, human experts can reject the match and flag it for different criteria. This expertise is particularly valuable for new product launches, seasonal items, or products with complex positioning strategies.

Business Logic Integration: Teams can define matching parameters that reflect their specific strategic needs. A premium brand might establish rules that prevent matches against budget alternatives, while a value retailer might specifically seek those comparisons. Category managers can create different matching criteria for different product lines, ensuring that seasonal items, limited editions, and promotional products are handled appropriately.

Transparent Decision Making: Every match decision creates an audit trail capturing who made the decision, when it occurred, and the reasoning behind it. This transparency is crucial for enterprise environments where pricing decisions need to be defensible and strategies need to be consistent across teams and time periods.

Scalable Validation: User-Led systems provide bulk operations for efficiency while maintaining oversight. Teams can upload thousands of matches for validation, use filtered views to focus on high-priority items, and leverage automated alerts for matches that fall outside established tolerance levels.

Each of these features reduces the friction between AI outputs and business-ready insights.

Technical Foundation

The AI foundation behind User-Led Match Management is built for precision and scale.

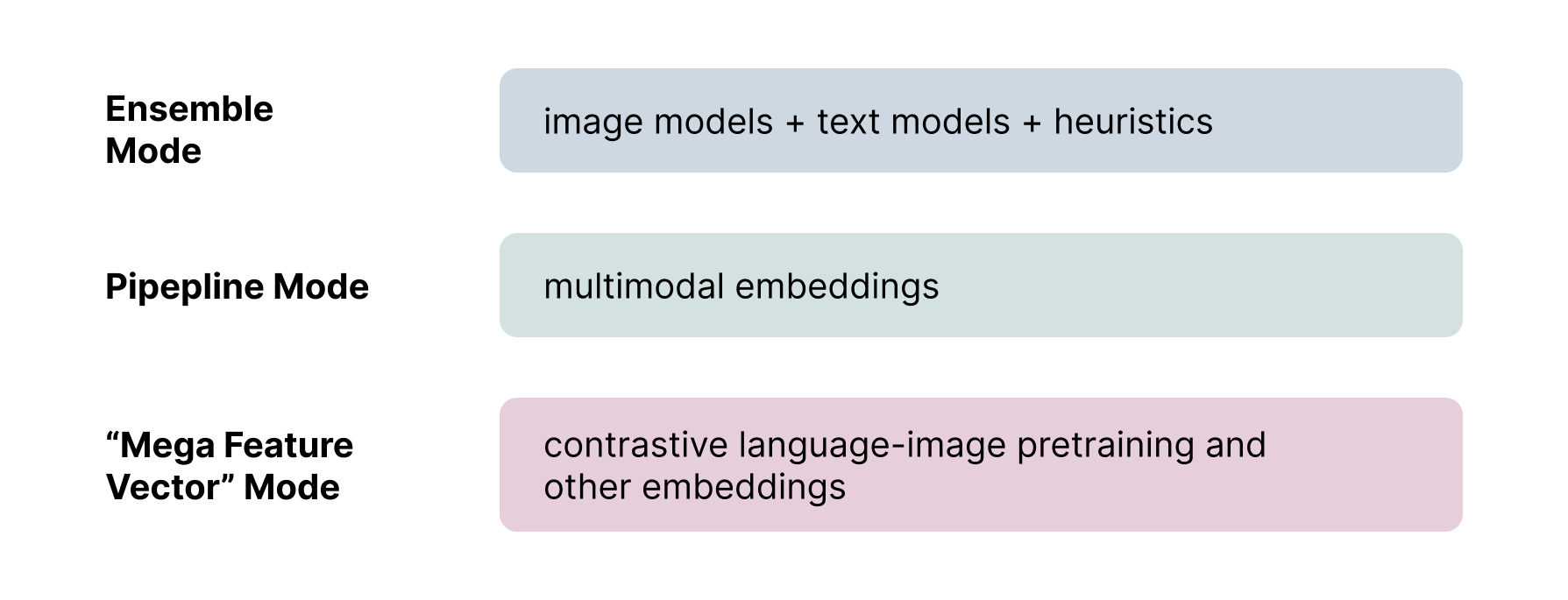

It uses multimodal AI that combines text, image, and metadata analysis to identify matches even when products are described or displayed differently across retailers.

Domain heuristics apply retail-specific logic, recognizing that “Large” means something different in apparel than in beverages, and that seasonal items require unique treatment.

Knowledge graphs link products across brands, categories, and regions to reveal true relationships even when surface attributes vary.

Through continuous learning, every human correction improves future AI suggestions, making the system smarter and more accurate over time.

With DataWeave, accurate and reliable product matching is the standard. Advanced algorithms and built-in quality checks deliver consistently high accuracy, reducing the risk of mismatched products and unreliable insights.

In the few cases where a match needs review, User-Led Match Management gives your team the ability to validate it quickly and easily. You get full visibility and control, while DataWeave ensures the integrity of the overall matching framework.

The outcome is true apples-to-apples price comparisons that protect margins, strengthen pricing strategies, and build trust in every decision.

Assortment Analytics

Gaps and overlaps only matter when matches are accurate. To understand your true competitive landscape, you need to eliminate false gaps and phantom overlaps that distort assortment insights.

DataWeave’s advanced Match Management ensures precise product alignment across retailers, categories, and regions, giving you a clear view of your position in the market. At the same time, user-led oversight adds transparent validation, allowing your teams to confirm or refine matches based on their category knowledge.

The result is a complete and trustworthy view of category coverage that reflects reality, not noise. It helps you identify real opportunities to expand assortments, close gaps, and respond quickly to market changes.

Content Optimization

Digital shelf audits only deliver value when the comparisons are accurate. DataWeave ensures that every product is benchmarked against its true competitors so that your insights reflect the real dynamics of your category. For example, a luxury serum is never compared to a basic moisturizer, and a premium electronic device is never matched with an entry-level model.

With user-led control, your teams have transparent oversight of every match. They can review, validate, or adjust comparisons to make sure each audit aligns with your business standards. The result is a more reliable and actionable view of your digital shelf performance, helping you fine-tune content, optimize visibility, and strengthen conversion across channels.

Trust and Accountability

Leadership teams need complete confidence in the data they use to make decisions. User-Led Match Management delivers that confidence by combining the scale of AI with the assurance of human validation. Every match decision is transparent and traceable, giving teams clear visibility into how and why a product was matched.

This approach builds trust across departments, from analysts to executives. It ensures that every pricing, assortment, and content decision is backed by data that is both accurate and accountable.

Your Market, Your Rules, Your Insights

Retailers and brands today need more than fast data. They need data they can trust, shape, and act on with confidence. User-Led Match Management gives them that control. It turns product matching from a static, automated process into a dynamic, collaborative workflow that adapts to how real teams operate.

Category managers can fine-tune match rules instead of waiting on system updates. Pricing teams can validate critical SKUs in minutes, not days. Digital shelf teams can ensure their audits reflect real competitors, not algorithmic guesses. Executives gain visibility into decisions they can stand behind, supported by transparent data trails and measurable accuracy.

In short, User-Led Match Management puts control back where it belongs – in your hands. It helps every team move faster, compete smarter, and make decisions powered by data they can truly believe in.

Every major shift in commerce has been driven by data. A century ago, shopkeepers relied on ledgers to track sales. In the supermarket era, loyalty cards and barcodes turned transactions into insights. With the rise of eCommerce, clickstream data and online analytics reshaped how products were merchandised and sold.

Now, we are entering the next chapter: agentic commerce.

In this new paradigm, autonomous AI agents will handle the tasks that once required teams of analysts, merchandisers, and pricing specialists. Imagine an agent that monitors competitor prices across dozens of retailers, recommends adjustments, and pushes updates to a dynamic pricing engine, all in real time. Picture a shopper’s digital assistant scanning marketplaces for the right mix of price, delivery time, and customer reviews before making a purchase on their behalf.

These aren’t distant scenarios. They’re unfolding now. Industry analysts estimate the enterprise AI market at $24 billion in 2024, projected to grow to $155 billion by 2030 at nearly 38% CAGR . Meanwhile, 65% of organizations already use web data for AI and machine learning projects, and 93% plan to increase their budgets for it in 2024. The trajectory is undeniable: the next era of commerce will be built on AI-driven decision-making.

And what fuels those AI-driven decisions? Data. Reliable, structured, timely, and compliant data.

The Data Problem No One Can Ignore

Here’s the paradox: just as data has become most critical, it has also become harder to acquire.

For data and engineering leaders, the challenges are painfully familiar:

Old school scrapers that collapse whenever a site changes its HTML or introduces new interactivity.

Constant maintenance cycles, with engineering teams spending 20-40 hours a week debugging, rerunning, and patching scripts.

Low success rates, with in-house approaches succeeding just 60-70% of the time.

Complex infrastructure, from managing proxies to retry logic, pulls attention away from higher-value work.

But the costs go far beyond engineering frustration.

For retailers, broken pipelines mean competitive blind spots. A pricing team without reliable visibility into competitor moves can’t respond fast enough, risking lost margin or missed sales. Merchandising teams trying to optimize assortments are left with incomplete data, making poor stocking decisions inevitable.

For brands, unreliable data disrupts visibility into the digital shelf. Products might be misplaced in search rankings, content could be outdated or incomplete, and reviews could signal issues, but without continuous monitoring, those signals are missed until it’s too late.

For AI and ML teams, poor-quality training data means underperforming models. Without clean, consistent, and large-scale inputs, even the most sophisticated algorithms produce flawed predictions.

Finally for consulting firms and research providers, fragile collection systems can compromise credibility. Clients expect robust, evidence-backed recommendations. Data gaps erode trust.

The reality is stark: fragile pipelines don’t just waste engineering hours. They undermine competitive agility, customer experience, and business growth.

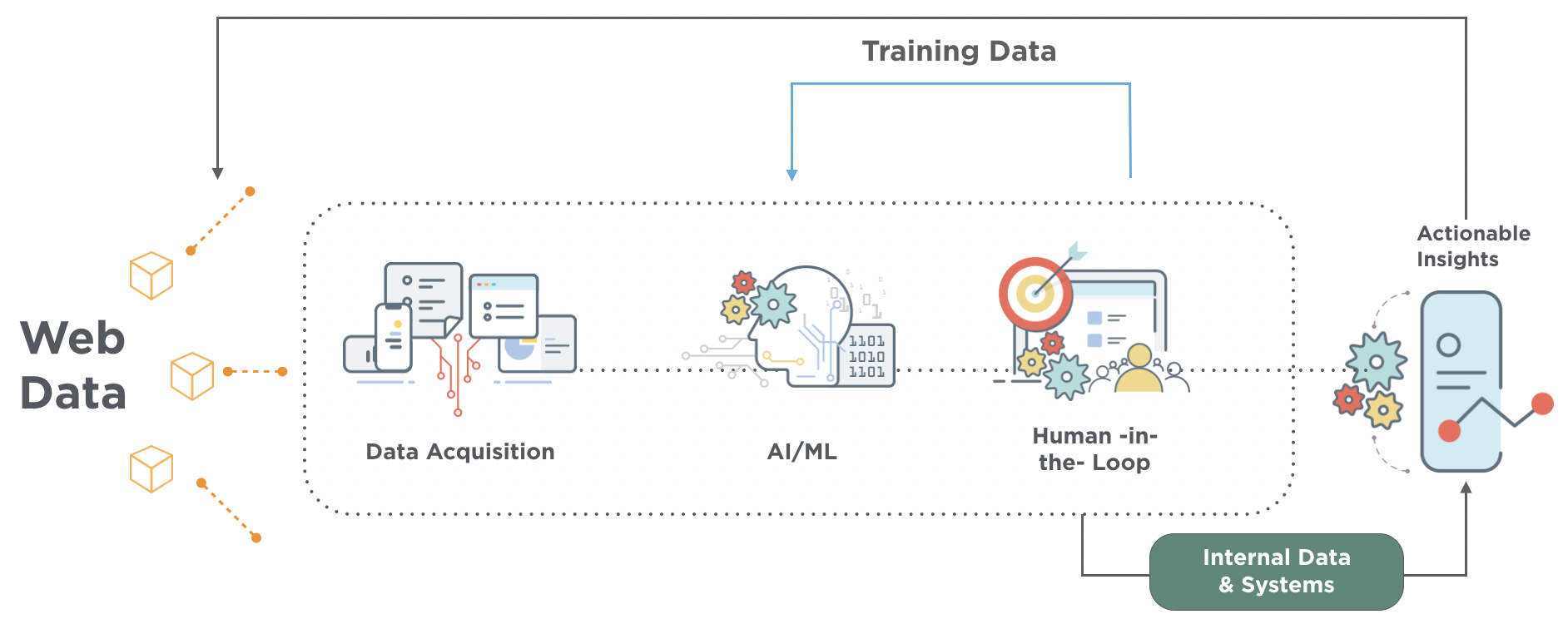

Enter the Data Collection API

DataWeave’s Data Collection API is a self-serve, enterprise-scale platform designed to deliver the data foundation today’s enterprises need, and tomorrow’s agentic AI systems will demand.

At its core, the API replaces brittle scrapers and ad hoc tools with a resilient, adaptive, and compliant data acquisition layer. It combines enterprise reliability with retail-specific intelligence to ensure that structured data is always available, accurate, and ready to power critical workflows.

Here’s what makes it different:

Enterprise-scale throughput: The API can process thousands of URLs in a single batch or handle continuous, high-frequency scrape. Whether you need daily pulses or near real-time monitoring, it scales with you.

Flexible access modes: Technical teams can integrate directly into internal workflows via API, while business users can configure jobs through a no-code interface. Everyone gets what they need without bottlenecks.

Adaptive resilience: As websites evolve, the API adapts automatically. No frantic patching, no firefighting.

Structured outputs, your way: Clean JSON, CSV, or WARC formats are delivered directly into your environment – AWS S3, Snowflake, GCP, or wherever your data stack lives.

Built-in monitoring and self-healing: Automated retries, real-time logs, and usage dashboards keep teams in control without manual oversight.

Compliance by design: WARC-based archiving and SOC2 alignment ensure data pipelines are auditable, trustworthy, and enterprise-ready.

This isn’t about scraping pages. It’s about creating a reliable data utility, a system that transforms raw web inputs into structured, actionable data streams that enterprises can trust and scale on.

Who It’s Built For (And How They Use It)

The Data Collection API isn’t limited to one role or industry. It’s been designed with multiple stakeholders in mind, each of whom can apply it to solve pressing challenges:

Retailers and Consumer Brands

Retailers live and die by competitive awareness. With the API, pricing teams can monitor SKU-level prices and promotions across channels, ensuring they don’t leave margin on the table. Merchandising leaders can track assortment coverage, identifying gaps relative to competitors. Digital shelf teams can measure search rankings, share of voice, and content completeness. The result is faster responses, stronger category performance, and fewer blind spots in shopper experience.

AI & Machine Learning Teams

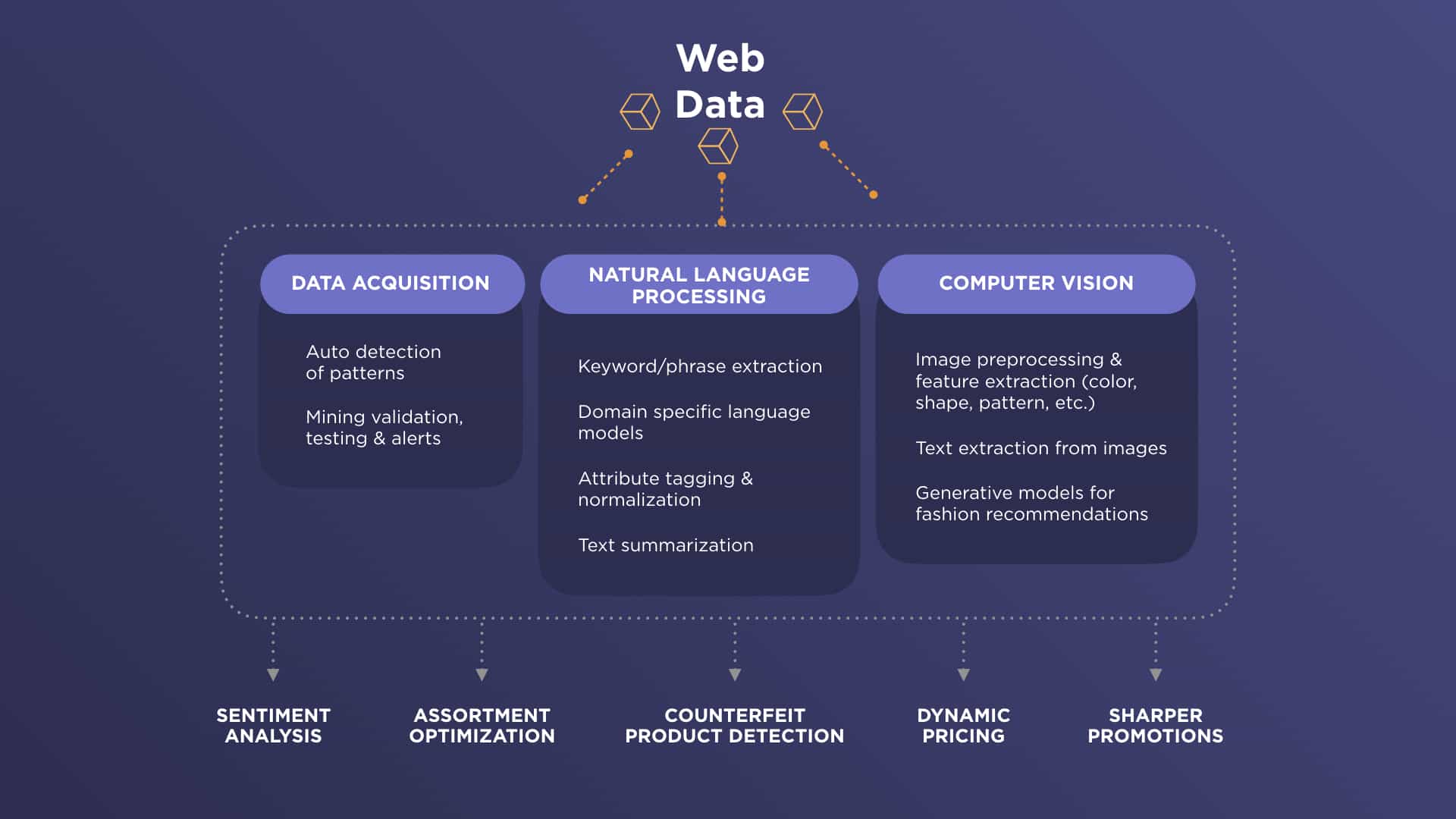

AI teams depend on data at scale. Whether training a natural language model to understand product descriptions or a computer vision system to analyze images, the Data Collection API delivers the structured, high-quality inputs they need. Reviews, ratings, attributes, and product images can all be captured and delivered at scale. For teams building predictive models, from demand forecasting to personalization, the difference between mediocre and world-class often comes down to input quality. This API ensures AI systems are always learning from the best data available.

Retail Intelligence & Pricing Platforms

Technology providers serving retailers and brands face unforgiving client expectations. Missed SLAs on data delivery can mean churn. By using the Data Collection API as their acquisition layer, platform providers gain enterprise reliability without rebuilding infrastructure from scratch. They can scale seamlessly with client needs while maintaining the integrity of the insights their customers rely on.

Marketing & Advertising Teams

For marketing leaders, competition is visible every time a shopper searches. The API enables teams to track keyword rankings, ad placements, and competitor promotions with consistency. Instead of anecdotal data or partial coverage, marketers get a full picture of their brand’s digital presence and the strategies competitors are using to capture share of voice.

Consulting Firms & Research Providers

Consultancies and market research agencies deliver strategy. But a strategy without evidence is just opinion. The API allows these firms to back every recommendation with structured, large-scale data. Whether advising on pricing, benchmarking performance, or publishing analyst research, firms can deliver trustworthy insights without taking on the cost or distraction of building fragile data pipelines.

The diversity of these use cases demonstrates why the API is a platform for collaboration across industries, ensuring every stakeholder, from engineers to strategists, has the reliable data foundation they need.

Why DataWeave, Why It Matters

Many vendors claim to deliver web data. Few can deliver it at enterprise scale, with commerce-specific expertise, and with proven ROI.

What sets DataWeave apart isn’t just that we provide data; it’s the way we do it, and the outcomes we enable.

Commerce expertise baked in: With 14+ years of experience powering the world’s leading retailers and brands, DataWeave brings domain-specific intelligence that generic scraping vendors simply can’t. Our schemas are designed for commerce. Our defaults are smarter because they’re informed by retail realities.

Adaptability without firefighting: Most tools break when websites evolve. Our API adapts automatically, minimizing the need for engineering intervention. Teams stay focused on innovation, not maintenance.

Accessible to everyone: Whether you’re a senior data engineer automating workflows or a business analyst configuring a quick scrape, the API meets you where you are with both API and no-code interfaces.

Enterprise-grade trust: Reliability and compliance are built in, not bolted on. With SLA-backed delivery, SOC2 alignment, and audit-ready archiving, the API is trusted by enterprises that can’t afford uncertainty.

This combination makes the Data Collection API not just a technical solution but a strategic partner for enterprises preparing for the age of agentic commerce.

A Foundation for the Future

The Data Collection API is more than an answer to today’s frustrating data problems. It represents a strategic foundation for tomorrow’s growth, designed to scale alongside the increasingly complex demands of commerce in the AI era.

At the heart of DataWeave’s vision is the Unified Commerce Intelligence Cloud, a layered ecosystem that transforms raw digital signals into strategic insights. The Data Collection API is the entry point, the essential first layer that ensures enterprises have a reliable supply of the most important raw material of the digital economy: data.

Collection: Enterprise-grade acquisition of web data at scale. From product pages and search results to reviews and promotions, enterprises can finally count on continuous, structured inputs without worrying about fragility or failure.

Processing: Once collected, data is normalized, enriched, and matched across sources. What was once noisy and inconsistent becomes clean, comparable, and immediately actionable.

Intelligence: On top of this foundation sits advanced analytics, solutions for pricing optimization, assortment planning, promotion tracking, and digital shelf visibility, enabling sharper decisions at the speed of the market.

This progression means enterprises don’t have to transform overnight. Many start small, solving urgent challenges like competitive price tracking or digital shelf monitoring. From there, they can expand naturally into richer intelligence capabilities, knowing that their data foundation is already strong enough to support more ambitious use cases.

And as agentic AI systems begin to take on a larger share of decision-making, the importance of that foundation grows exponentially. These autonomous systems cannot operate effectively without clean, continuous, and contextual data. Without it, even the most sophisticated AI will falter, making poor predictions or incomplete recommendations. With it, they can operate at full capacity, powering dynamic pricing, real-time demand forecasting, and personalized shopping experiences at scale.

The Data Collection API isn’t just about reducing engineering pain today. It’s about preparing enterprises to compete and win in an AI-driven marketplace that never sleeps.

Getting Started

For teams tired of fragile scrapers, this is a chance to reset. For enterprises preparing for the next era of commerce, it’s a chance to build a foundation that can scale with them.

If your teams are still struggling with generic and inflexible data scrapers, request a demo now to see the DataWeave’s Data Collection API in action.

Back in the day, pricing strategies were a lot easier. These days, not only do teams need to have robust standard price reporting workflows, but they also need to have the know-how and tools to gain and act on competitive intelligence. Retail leaders should prioritize automation and strategic thinking and ensure their teams have the tools, processes, and methodologies required to monitor the competition at scale and over the long term.

Retail leaders who recognize the distinction between standard reporting and competitive intelligence are more likely to gain team buy-in, especially when developing pricing strategies that drive results. You can’t be everywhere at once, but you can optimize pricing strategies to stay ahead of the competition.

This article has everything you need to know about the differences between standard reporting and competitive intelligence and how to use both to make your teams more effective than ever!

Understanding the Distinction

Standard price reporting is much like checking the weather to see if it’s stormy before grabbing a raincoat or sunhat. You need to do it to make essential, everyday choices, but it will not help you predict when the next storm is coming. Standard price reporting deals more with the short-term and immediate actions needed as opposed to long-term strategy.

Don’t get us wrong, standard price reporting is still an essential responsibility of a pricing team’s function—but there’s more to it. It is also lower-tech than a competitive intelligence strategy and can rely on route heuristics.

Think of it as data-in, data-out. It deals with pricing operations like:

Weekly price movements: Seeing which competitors, product categories, and individual items had pricing shifts in the short-term

Basic price indices: Outlining benchmarks to watch how your own, and your competitors’, products are trending in the market

Price competitiveness metrics: Setting thresholds that show whether your products are priced below, above, or equal to your competition for general trend reporting

Standard price reporting is fundamental for operational teams that manage price adjustments in the short term. It can also help teams remain agile and reactive to market condition changes.

It’s likely that your team already has standard reporting strategies or tools to help them with tactical execution. But are they harnessing competitive intelligence correctly with your help?

Characteristics of Competitive Intelligence

While standard price reporting is like checking the weather, competitive intelligence is like being a meteorologist who measures atmospheric changes, predicts storms, and scientifically analyzes weather patterns to keep everyone informed and in the know.

Competitive intelligence goes well beyond simply tracking price movements and benchmarking them against a single set of standards. Competitive intelligence helps steer teams in a strategic direction based on insights from the market. It can drive long-term business success and is one of your best tools to ‘steer the ship’ as a retail leader.

Here are some of the essential elements of competitive intelligence:

Strategic insights: Including but not limited to understanding your competitors’ pricing strategy, promotions, and product positioning

Market-wide patterns: Identifying trends based on geography, product category, or individual SKU across retailers to inform broader strategies

Long-term trends: Taking historical market and competitor data and combining it with real-time retail data to predict future price movements as shifts in consumer behavior to inform pricing strategies

The pricing team serves as a critical strategic partner to senior leadership, delivering the cross-functional insights and market analysis needed to inform C-suite decision-making. By equipping executives with a holistic view of the competitive landscape, pricing gaps, and emerging trends, the team empowers leadership to align pricing strategies with broader business objectives.

This partnership enables senior leaders to guide day-to-day pricing operations with confidence—ensuring tactical execution aligns with corporate goals, monitoring strategy effectiveness, and maintaining competitive agility. Through ongoing market intelligence and scenario modeling, the pricing function helps leadership proactively position the brand, capitalize on untapped opportunities, and future-proof revenue streams.

Different Audiences, Different Needs

As mentioned, there is a place for both standard price reporting and competitive intelligence. They have different roles to play, and different teams find them valuable. Since standard reporting mainly focuses on day-to-day shifts and being able to react to real-time changes, operational teams find it most useful.

On the other hand, competitive intelligence is a tool that leadership can use to shape overarching pricing strategies. The insights from competitive intelligence drive operational activities over months and quarters, whereas standard reporting drives actions daily.

To succeed in pricing, you need to rely on a combination of tactical standard reporting and competitive intelligence for long-term planning. With both, you can successfully navigate the ever-fluctuating retail market.

Price Reporting for Operational Teams

Your operational team is responsible for making pricing adjustments that directly impact sales volume. Automated data aggregation and AI-powered analytics can make this process faster and more accurate by eliminating the need for manual intervention.

Instead of spending hours identifying changes, standard reporting tools surface the most critical areas that need attention and recommend adjustments. This helps operational teams react fast to shifting market conditions.

Key functions of standard price reporting include:

Daily/weekly pricing decisions: Frequent price adjustments based on market trends will help your company remain competitive across entire product categories. With automated, real-time dashboards, your pricing team can monitor broad category-level pricing shifts and make necessary adjustments accordingly.

Individual SKU management: Not all pricing changes happen at the category level. Standard reporting also allows teams to view price and promotion changes on individual SKUs down to the zip code. It’s important to have targeted, granular insights when a change occurs even on a single SKU, especially because these individual changes are easy to miss. Advanced product matching algorithms can tie together exact products across retailers to monitor items conjointly. By incorporating similar product matching technologies beyond standard reporting, your teams can monitor individual price changes on comparable products.

Immediate action items: The best standard reporting tools alert pricing teams when there has been a change in competitor pricing and give them recommendations for what to change. If a competitor launches a flash sale or an aggressive discount program, your team should know as fast as possible which product to adjust. Without this functionality, teams can miss important changes or experience a delay in action that results in lost sales or customer perception.

Competitive Intelligence for Leadership

For Senior Retail Executives, Category Directors, and Pricing Strategy Leaders, pricing cannot only be about reacting to individual competitor price changes. Instead, you must proactively think about your market positioning and brand perception. Doing this without a complete competitive intelligence strategy can feel like throwing darts while blindfolded. Sometimes, you’ll hit the target, but mostly, you’ll miss or only come close. Competitive intelligence tools can help you hit that target every time. They leverage big data, artificial intelligence (AI), and predictive modeling to help you derive holistic insights to understand your current positioning relative to the current and future pricing landscape.

Core strategic functions of competitive intelligence include:

Strategic planning: Competitive intelligence tools can help you forecast competitor behavior, economic shifts, and category-specific patterns you’d otherwise overlook (ex, price drops before new releases, subscription or bundling trends, or seasonable price cycles). Instead of reacting to a change, your team can already have made changes or at least know what playbook to implement.