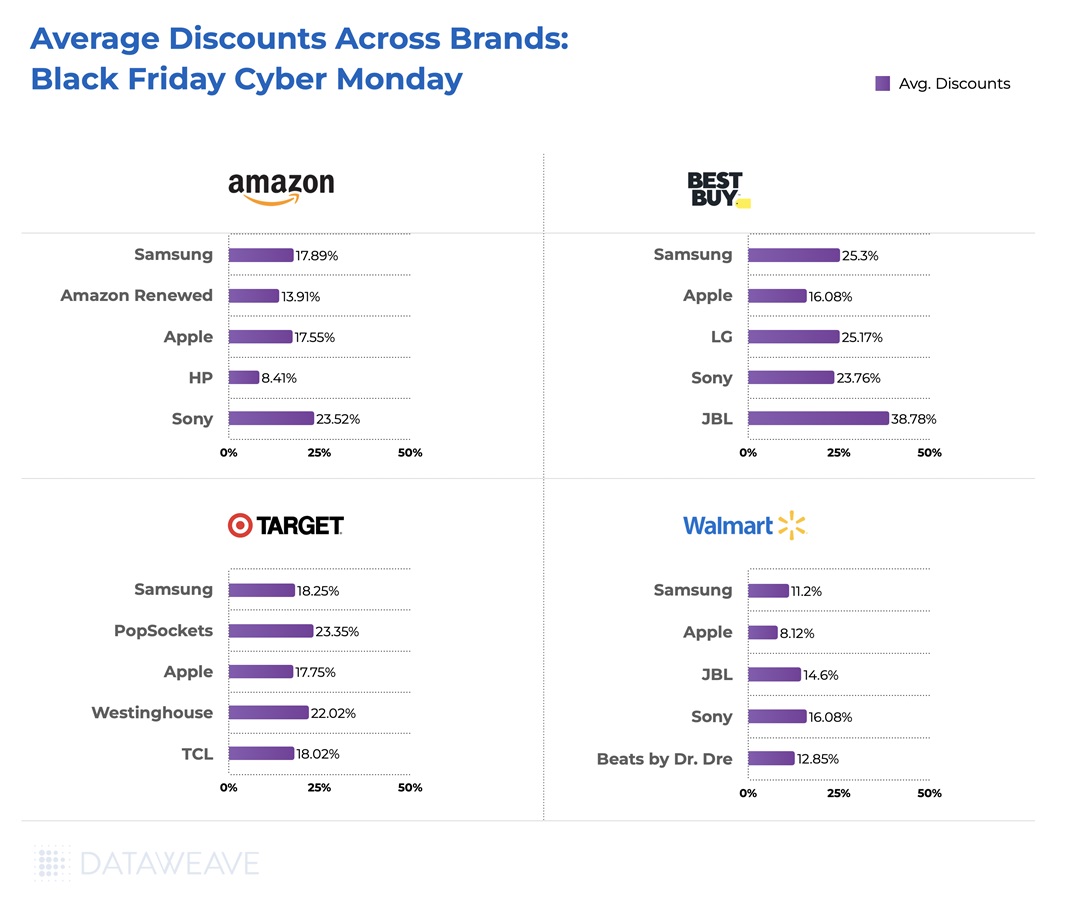

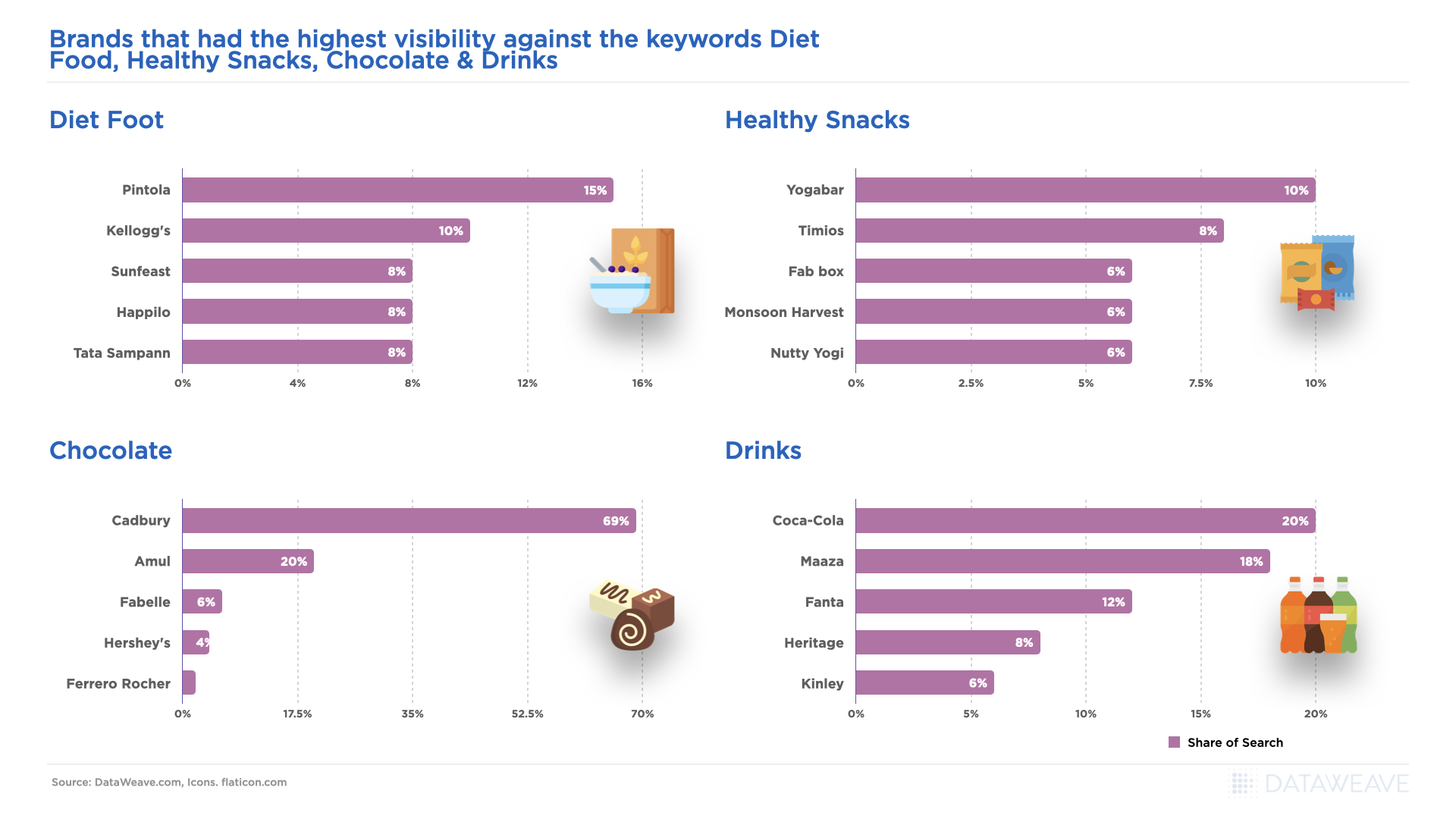

Black Friday has evolved from a purely Western retail phenomenon into a global shopping event. India is no exception. While the country celebrates its own mega sale events like the Great Indian Festival and Big Billion Days, Black Friday has carved out its own space in the Indian retail calendar. E-commerce in India is expected to reach $325 billion by 2030, with festive shopping seasons driving significant portions of that growth.

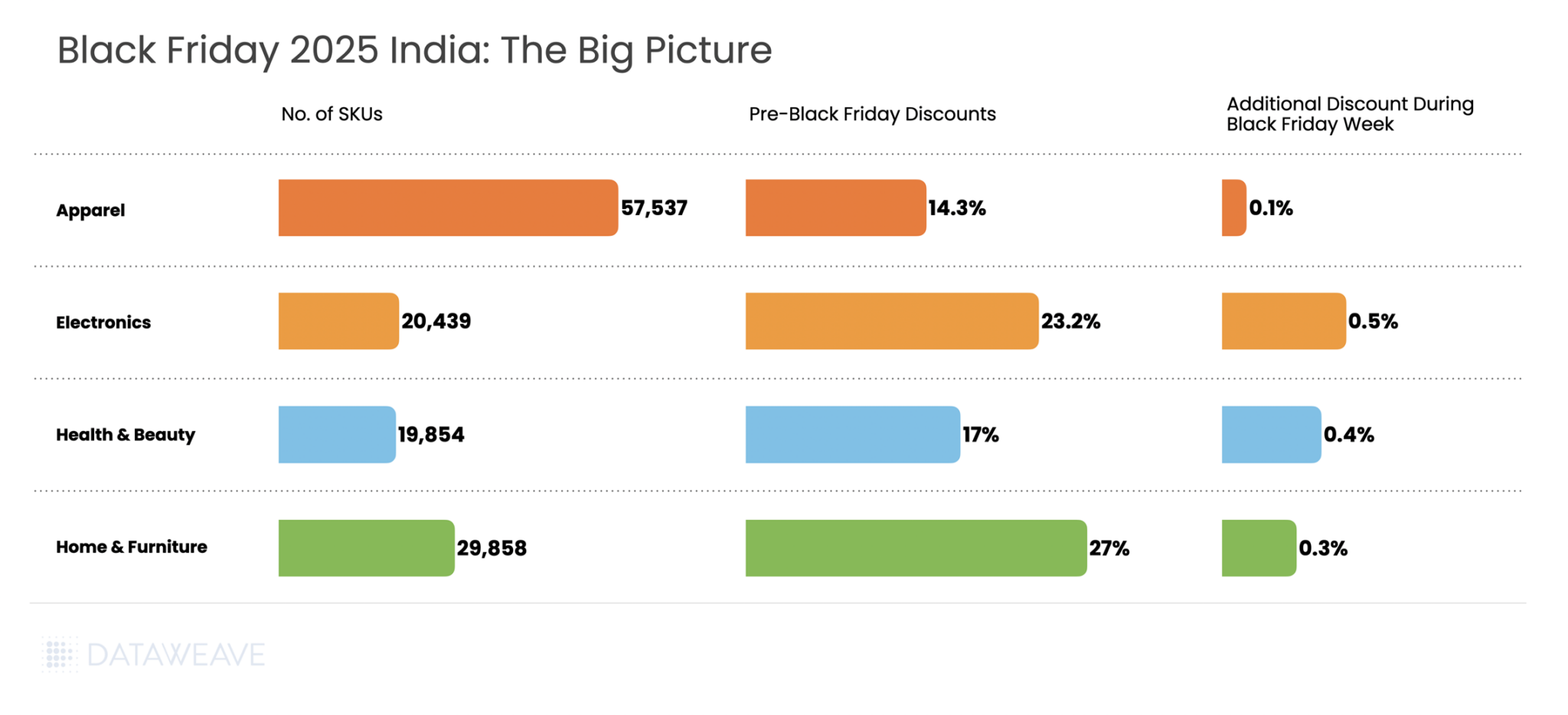

So how did Indian retailers and brands navigate Black Friday 2025? At DataWeave, we analyzed pricing trends across four major categories: Consumer Electronics, Home & Furniture, Health & Beauty, and Apparel. Our AI-powered retail intelligence platform tracked nearly 128,000 SKUs across leading platforms including Amazon India, Flipkart, Myntra, and others, revealing how the Indian market approached discounting and brand visibility during this high-stakes shopping period.

Our Methodology

DataWeave monitored average discount percentages across major Indian e-commerce platforms during two distinct periods:

Pre-Black Friday: Up to November 23, 2025 – capturing early promotional activity and baseline pricing

Black Friday Week: November 24 – December 1,2025 – spanning Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

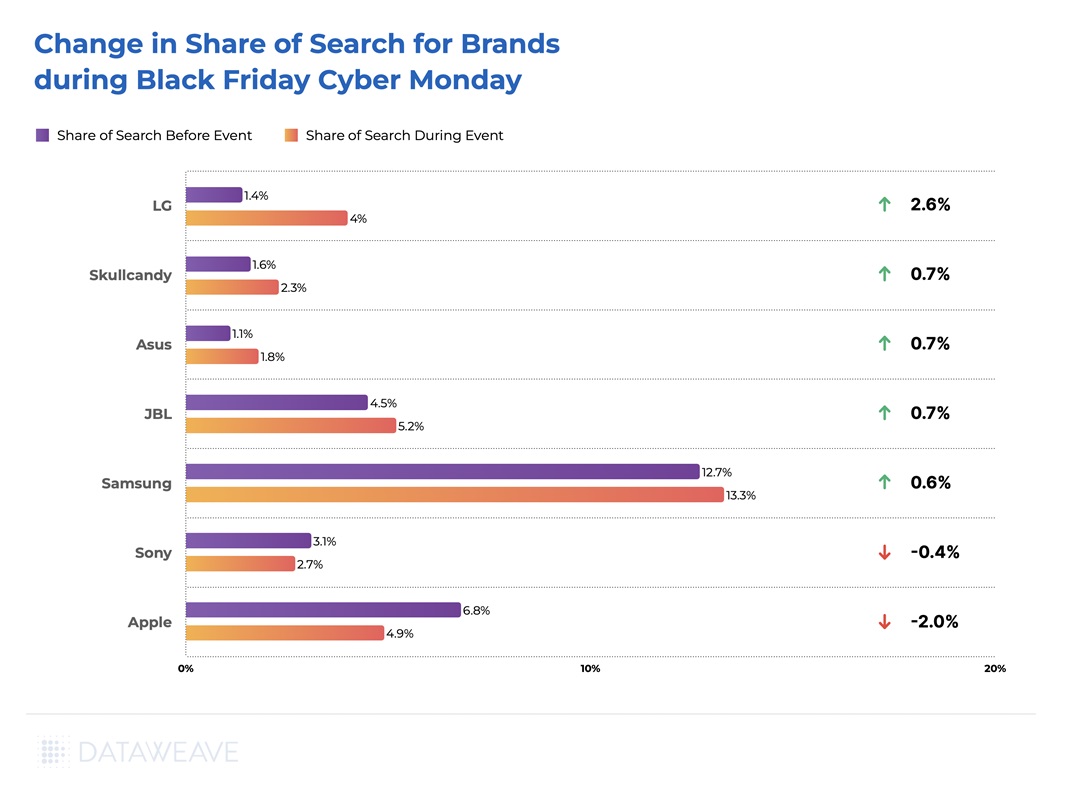

We analyzed top-ranked products across subcategories on major retail sites, alongside Share of Search data, a metric that measures brand visibility by tracking which brand names appear in the top 20 search results for high-intent keywords.

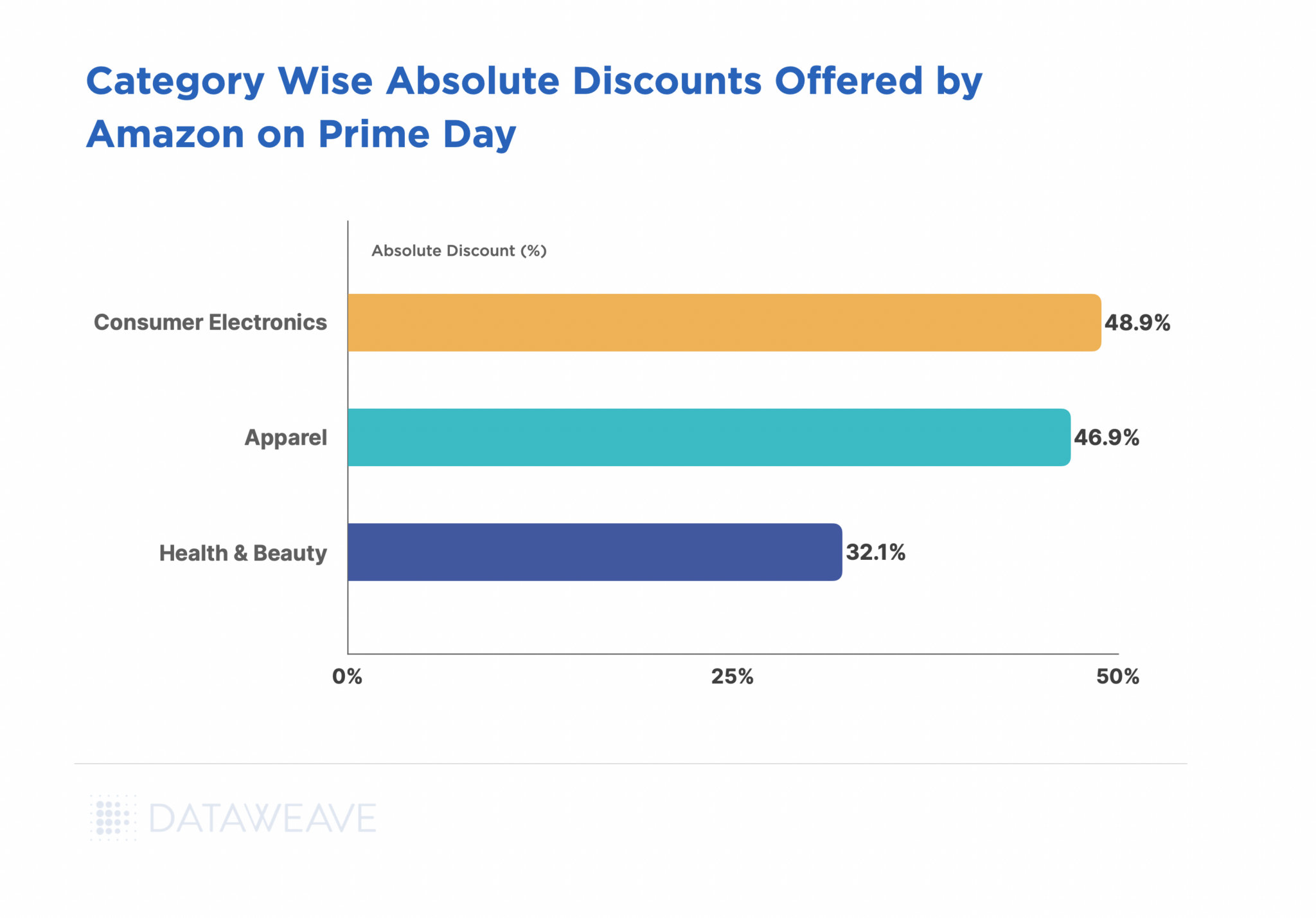

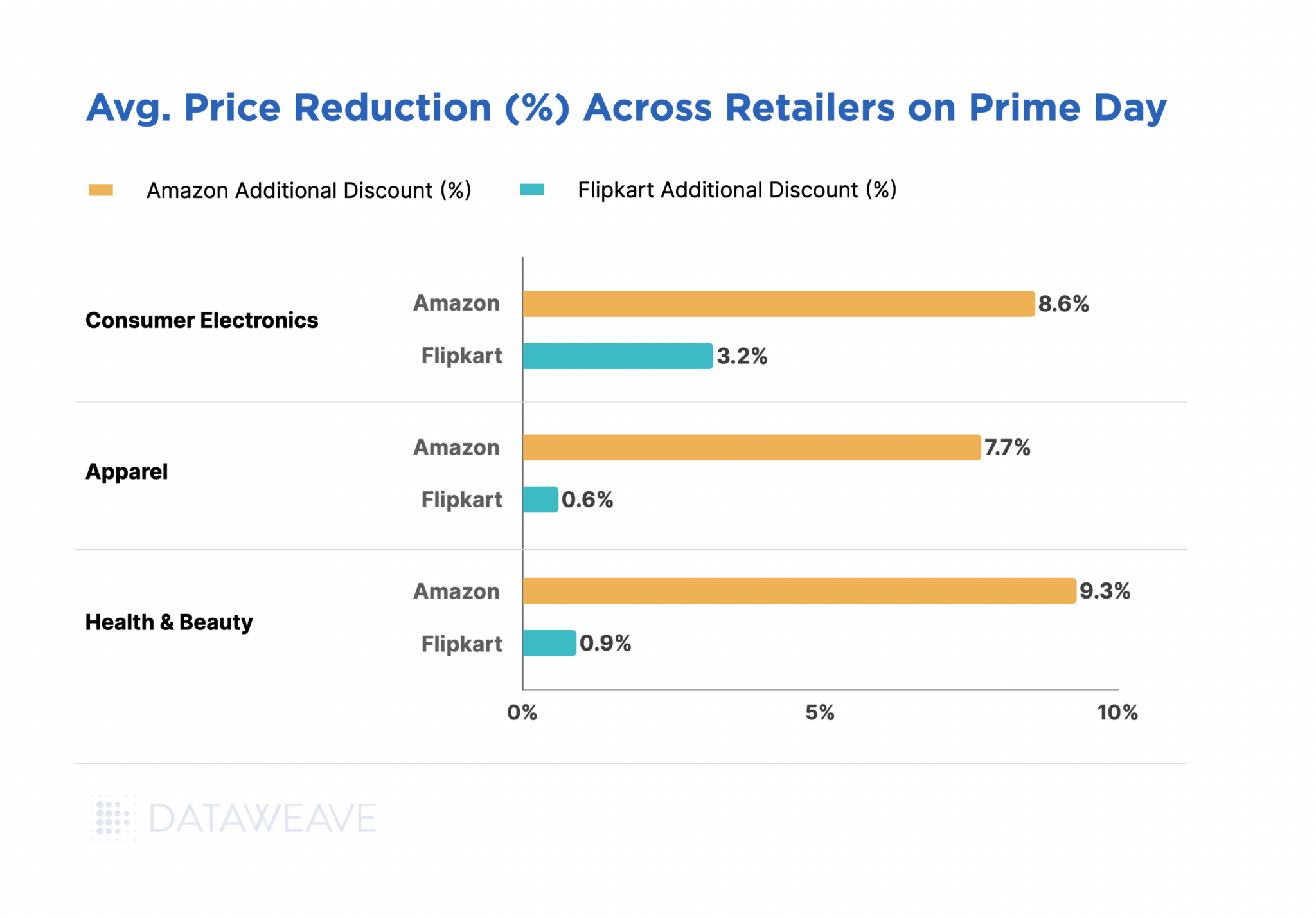

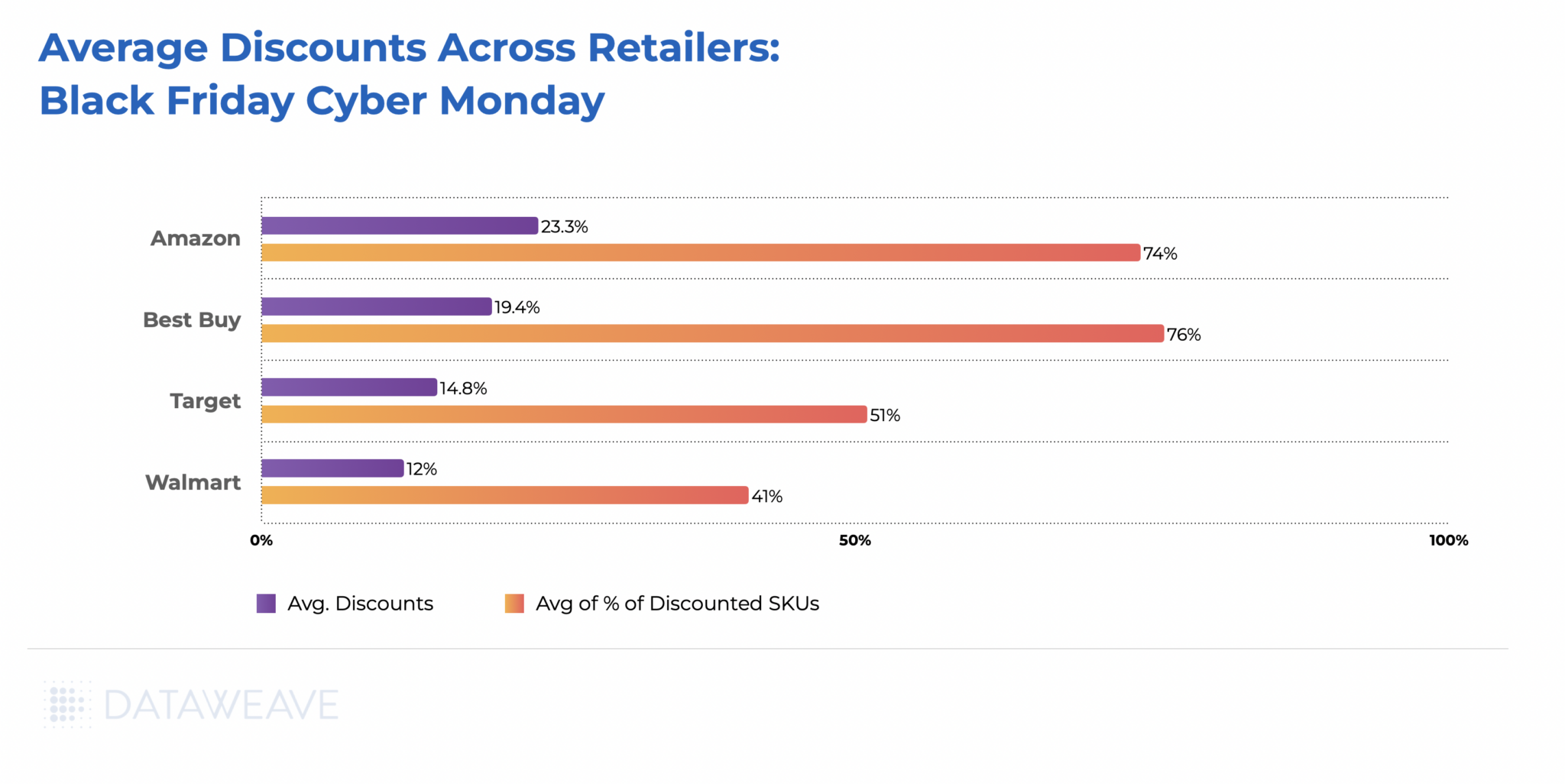

Here’s a quick look at the overall discounts this Black Friday in India:

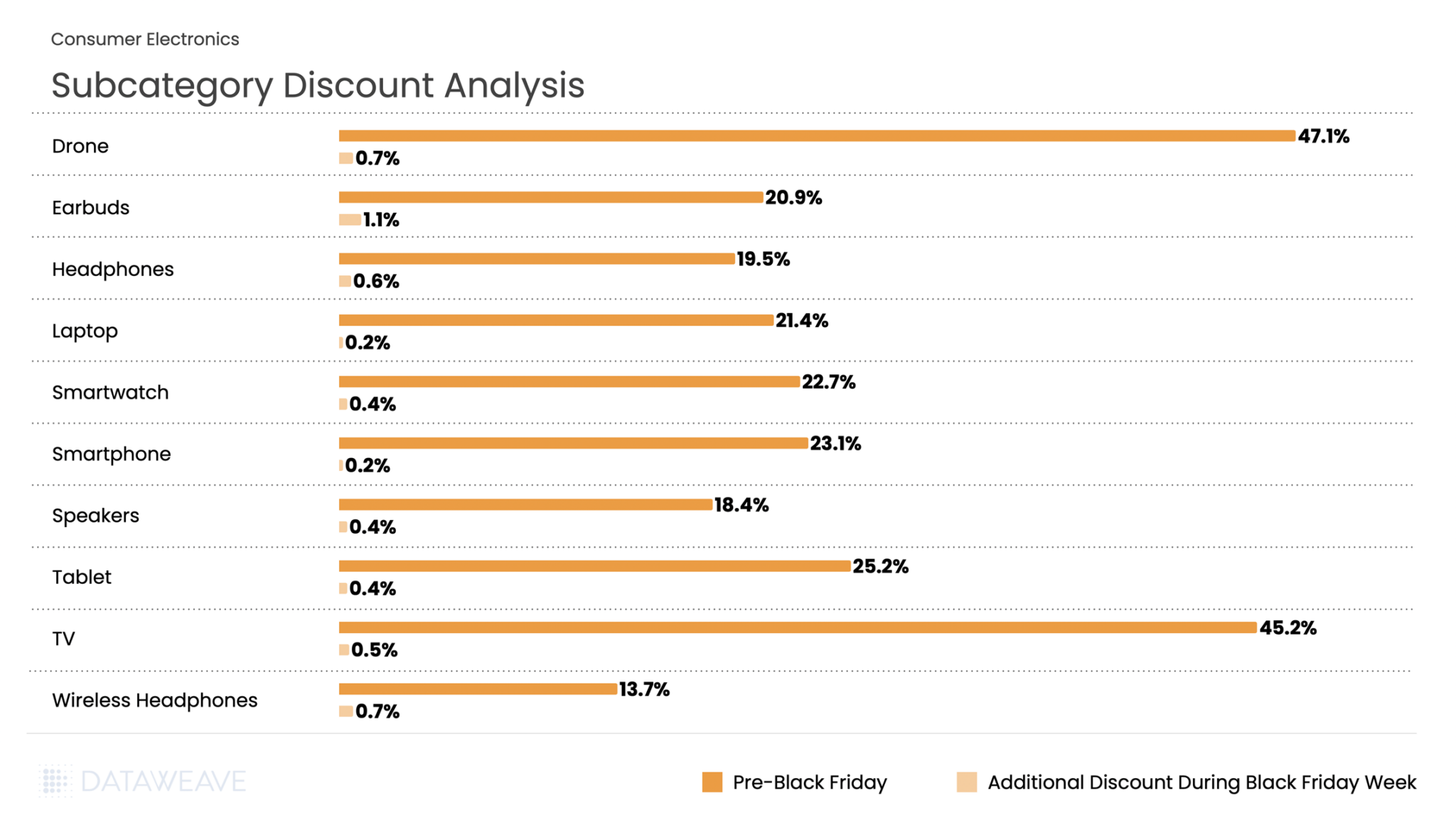

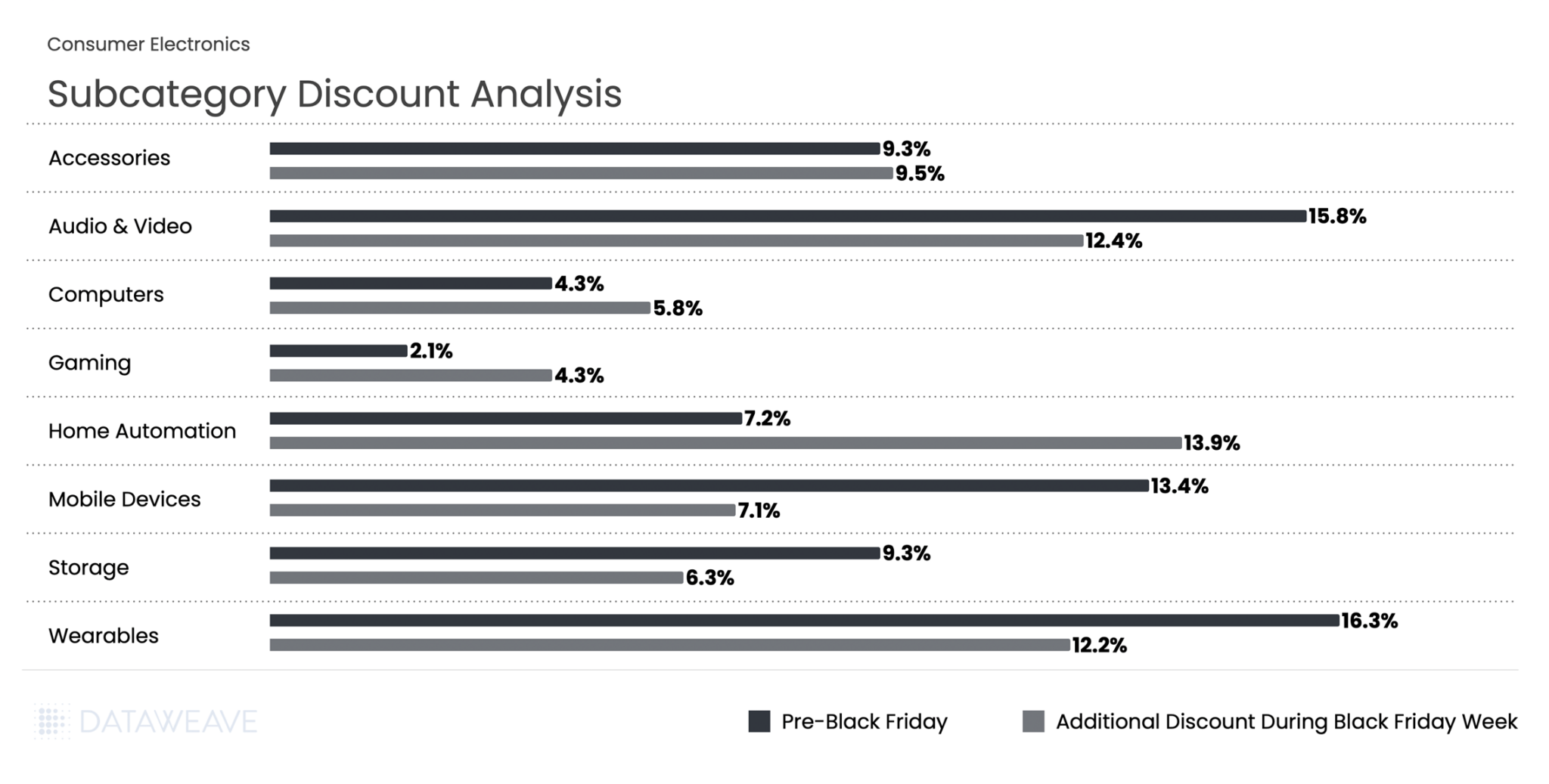

Consumer Electronics

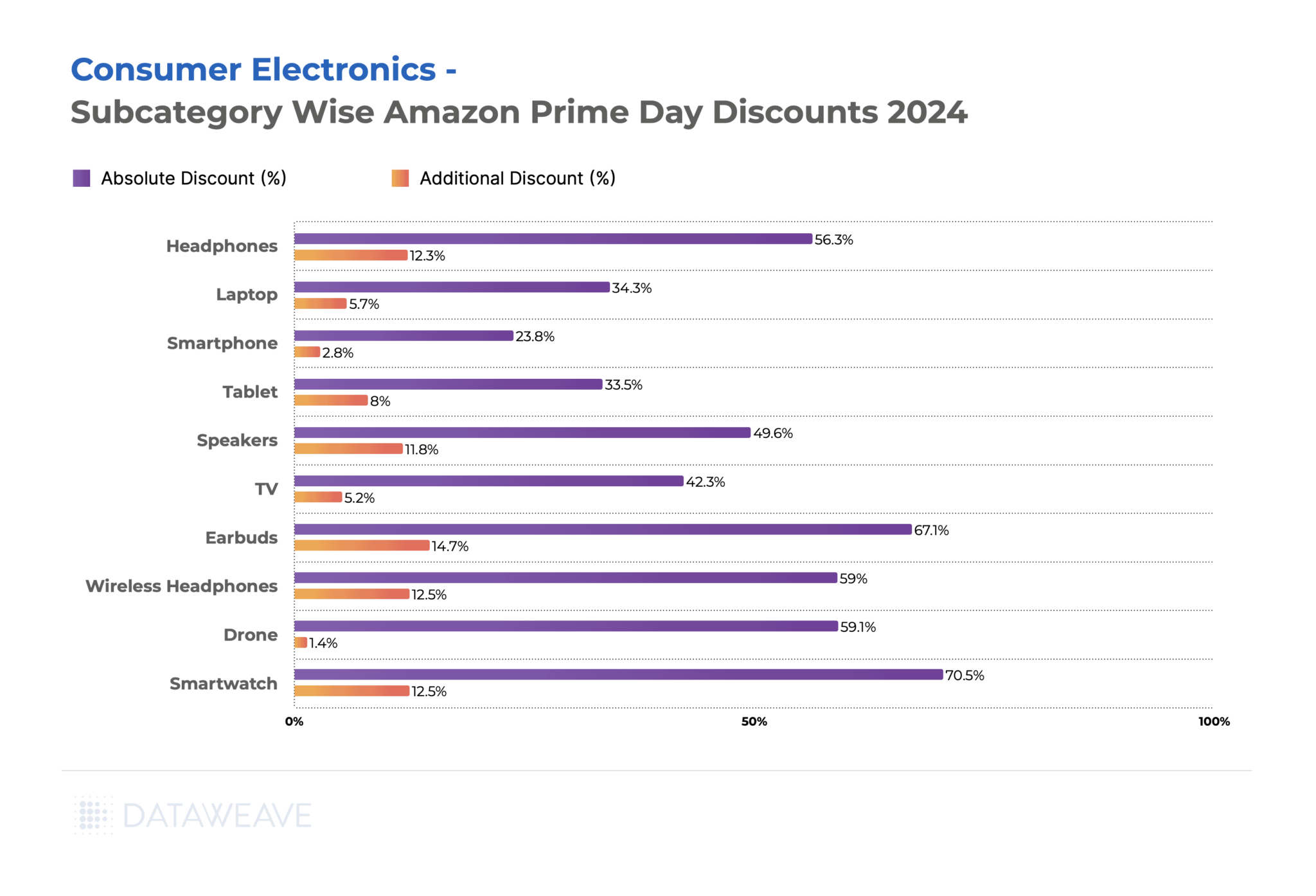

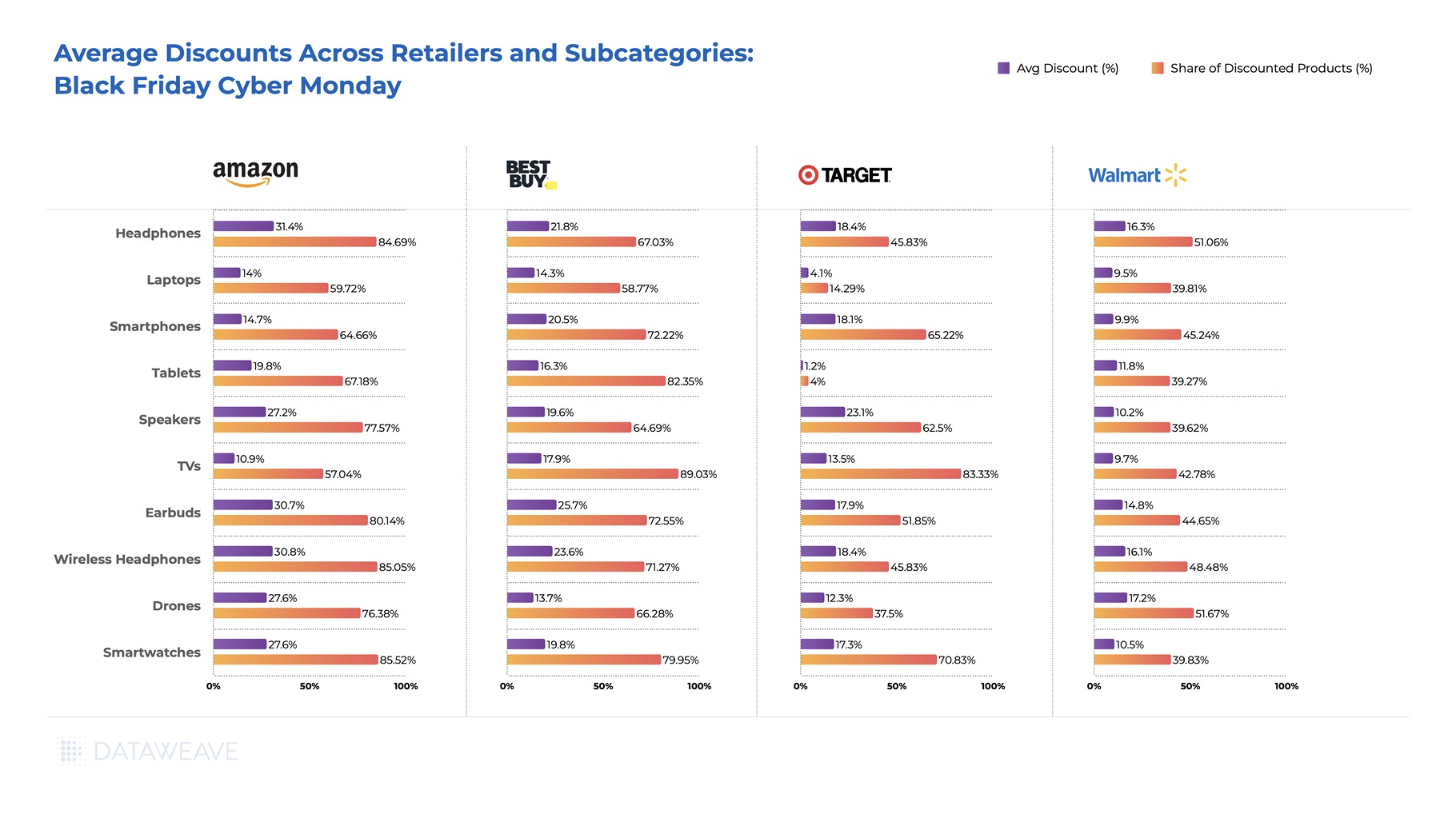

Consumer electronics remain a cornerstone of Black Friday shopping in India, with smartphones and laptops driving significant online sales. Our analysis of 20,439 SKUs reveals distinctive discount patterns across subcategories.

Subcategory Discount Analysis

The category averaged 23.2% pre-Black Friday discounts with an additional 0.5% during Black Friday Week. Drones and TVs led pre-sale discounting at 47.1% and 45.2% respectively, suggesting retailers wanted to clear high-ticket inventory ahead of the main event. Tablets (25.2%) also saw aggressive pre-sale pricing. During Black Friday Week, Earbuds saw the most substantial additional discounts at 1.1%, while categories like Laptops and Smartphones, already heavily discounted, had minimal incremental price cuts at 0.2%.

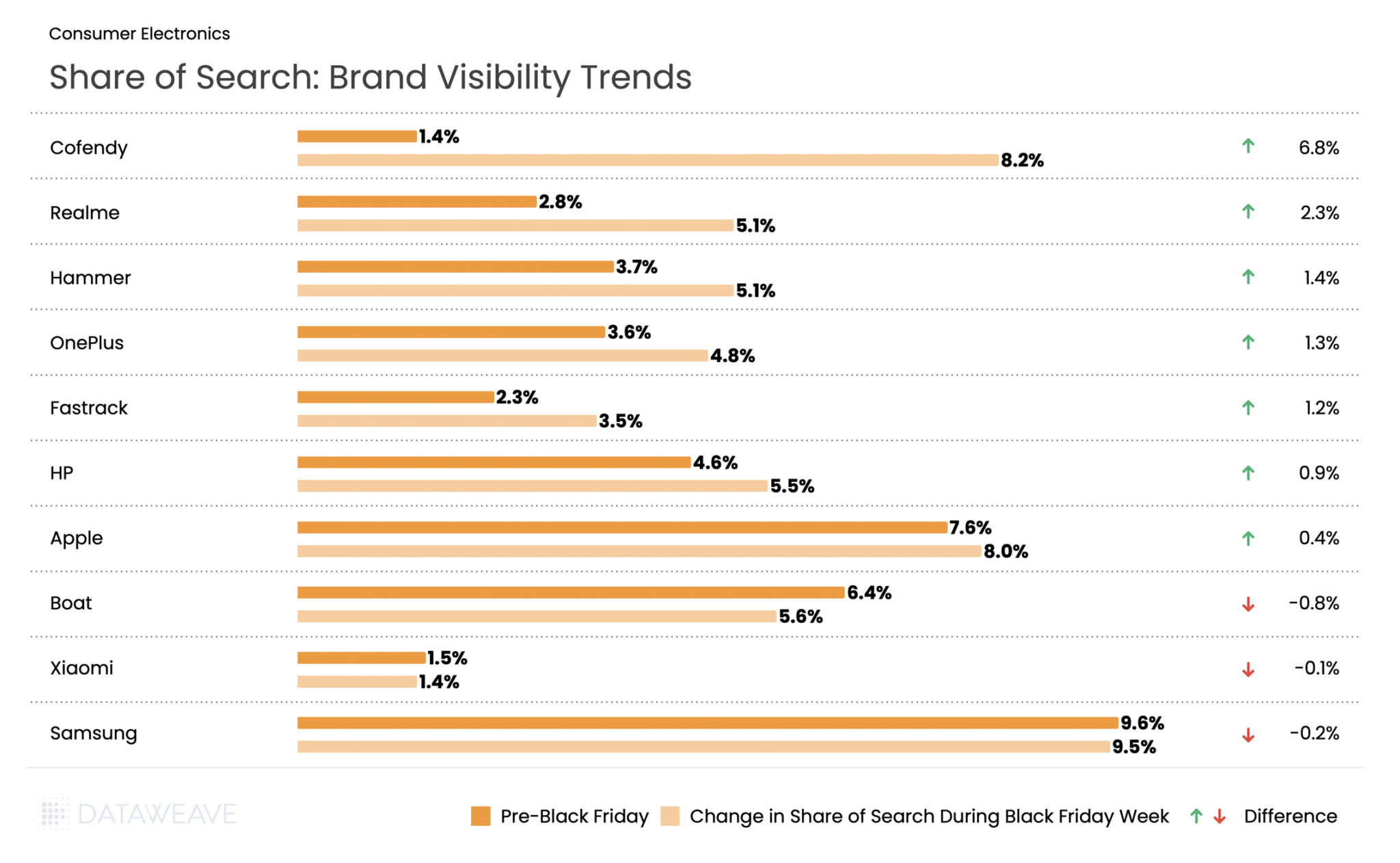

Share of Search: Brand Visibility Trends

The most notable is Cofendy, electronics accessories and speaker brand, that saw the share of search rise from 1.4% pre Black Friday to 8.2% during the event. Realme followed with a solid 2.3% gain, reinforcing its position as a rising smartphone brand. Smart gadget brand Hammer also saw visibility increase by 1.4% at par with OnePlus, Fastrack, HP and Asus.

Samsung saw the highest brand visibility with share of search at 9.6% pre-event and 9.5% during Black Friday week, despite seeing a small drop in visibility. Audio brand Boat saw a visibility drop by 0.8%, while Xiaomi saw the share of search drop by 0.1%. This shift suggests that Indian consumers were drawn to newer brands and compelling deals across computing and mobile devices during the sale period.

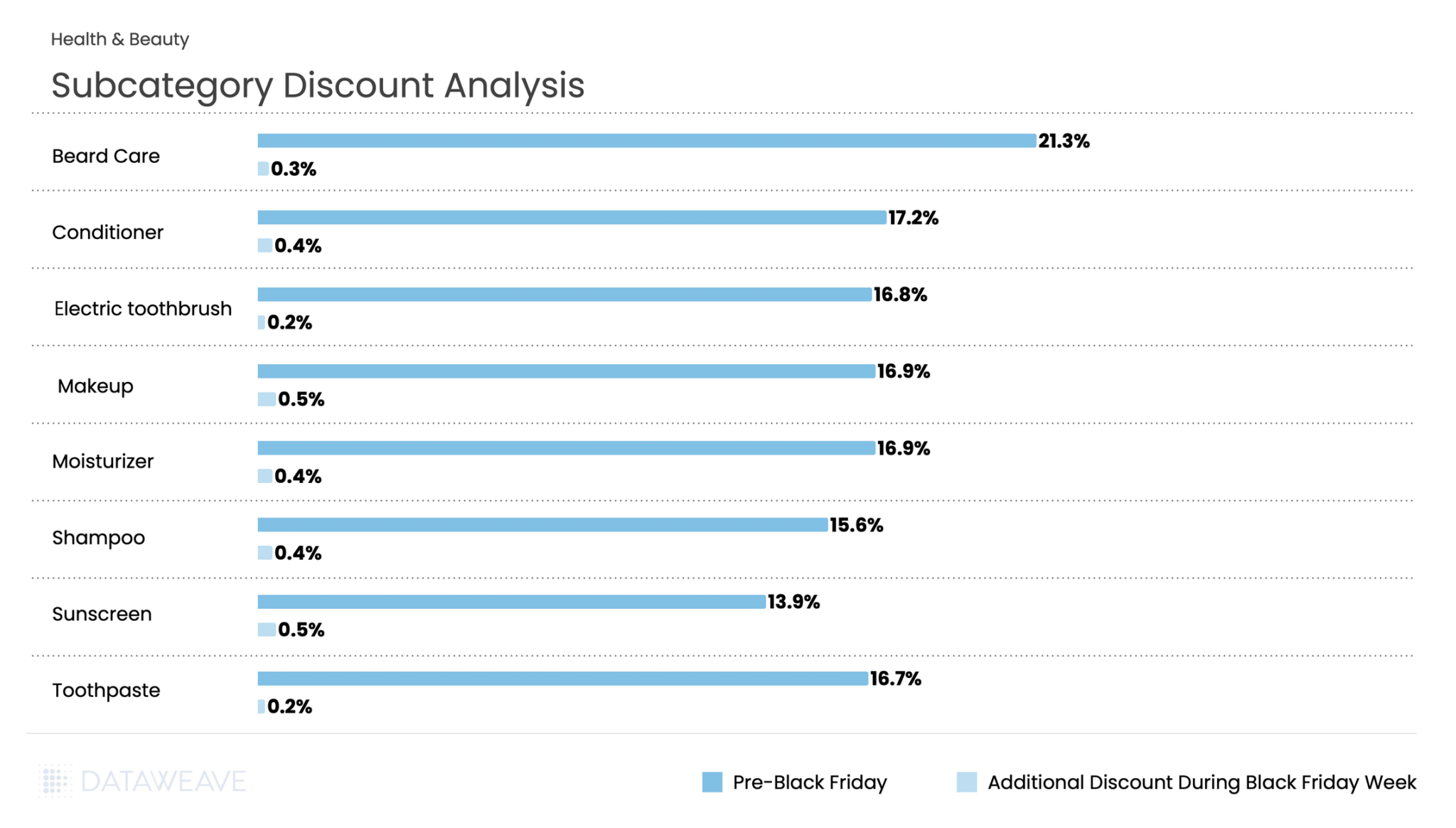

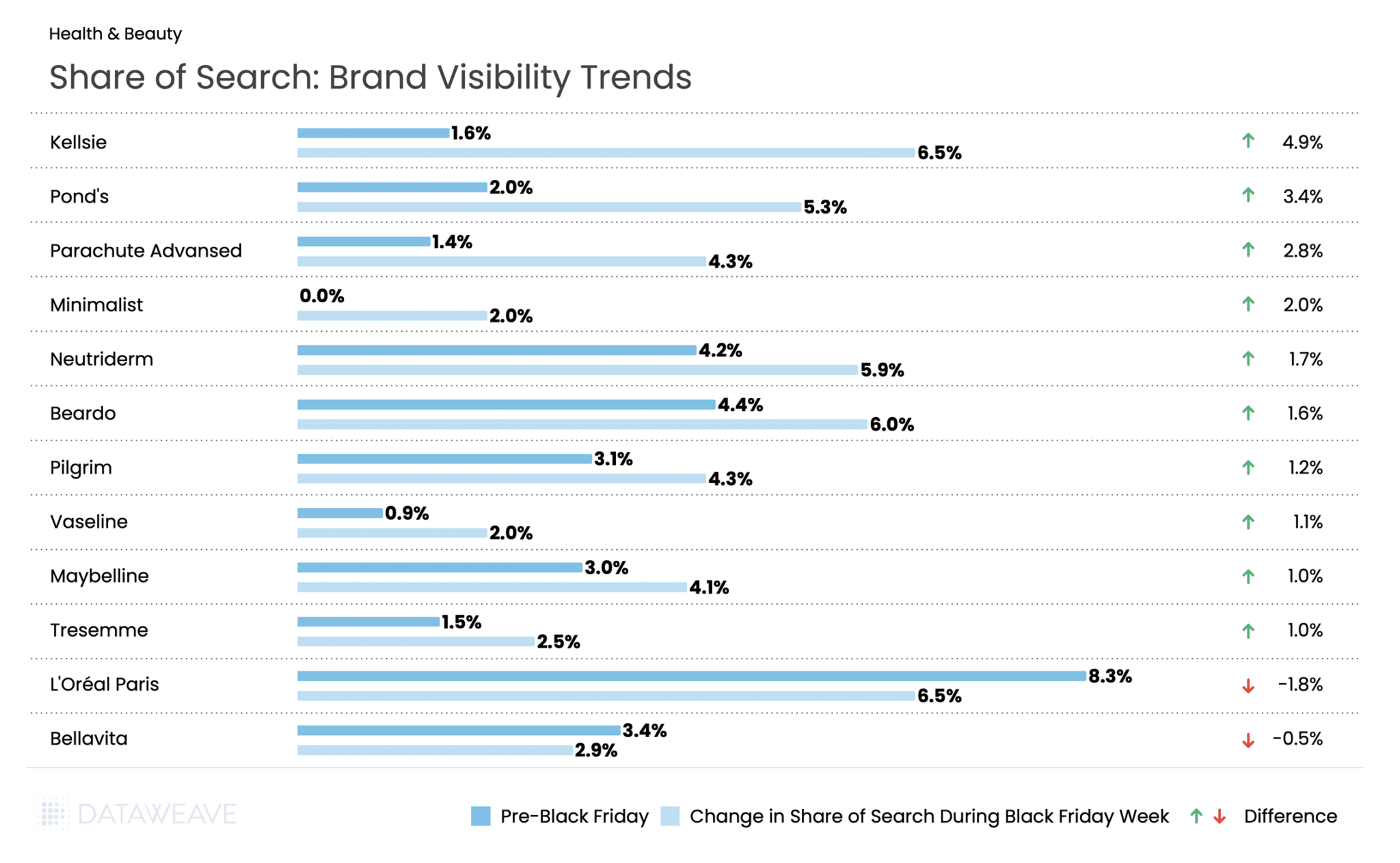

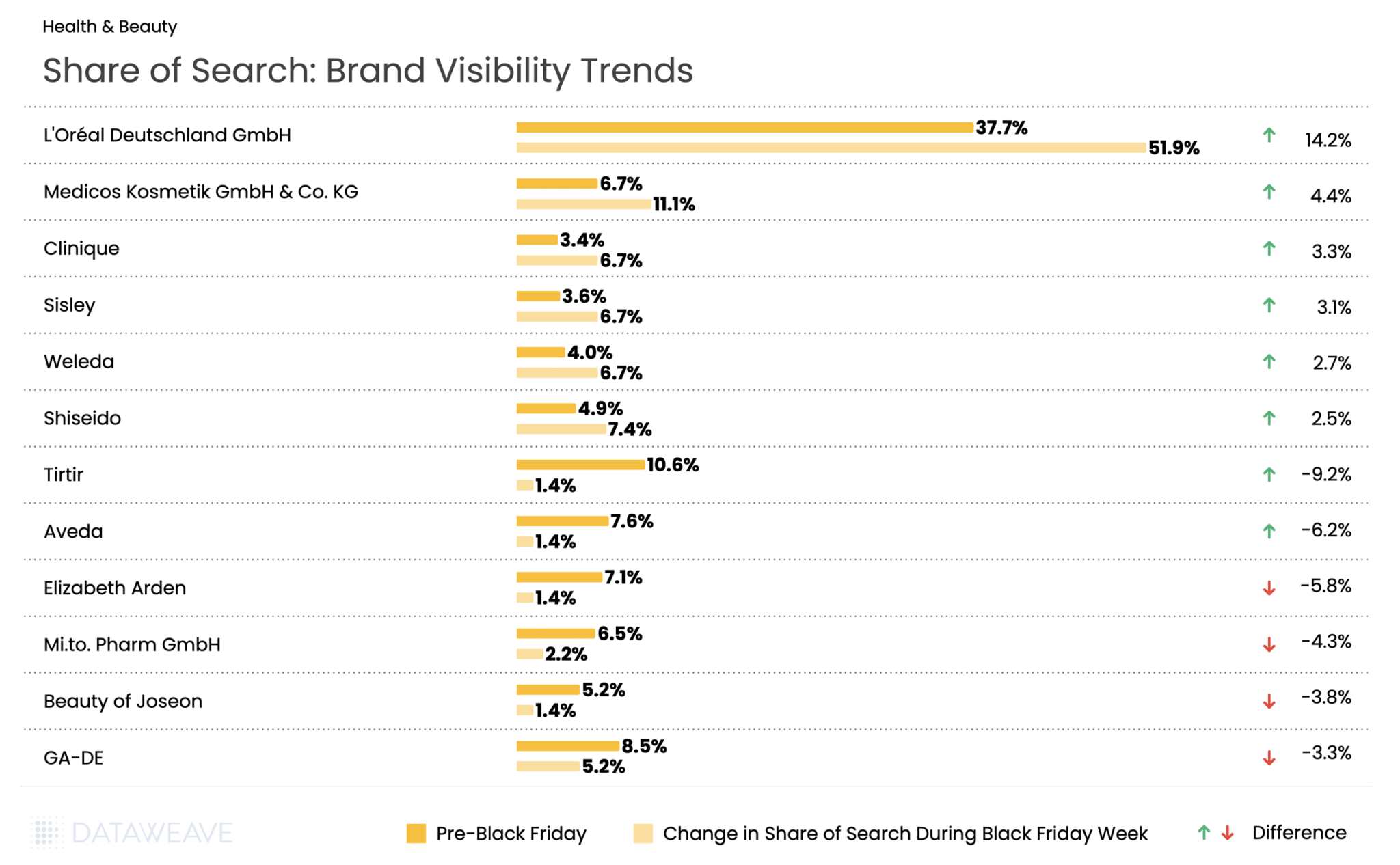

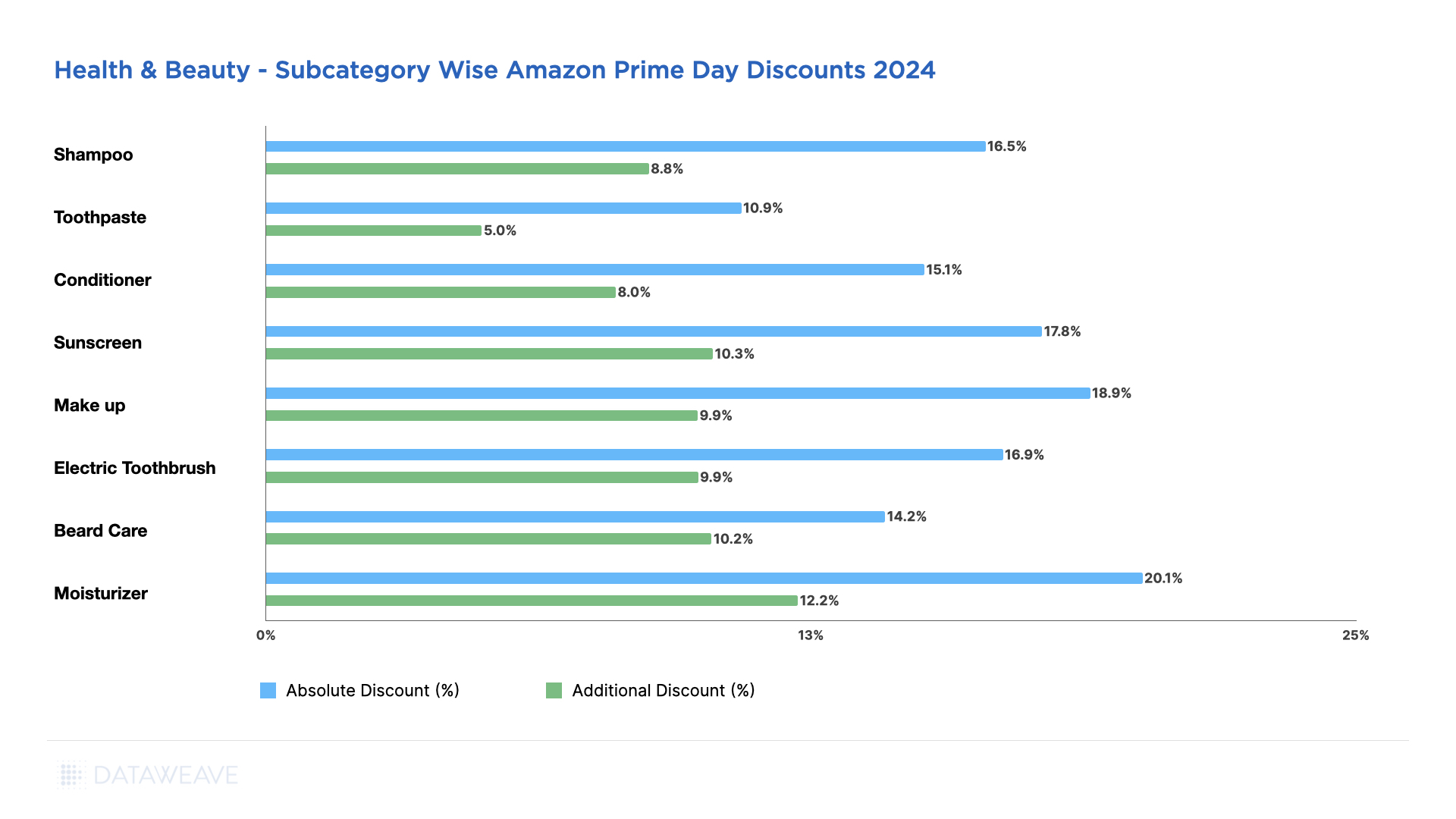

Health & Beauty

The Indian beauty and personal care market is experiencing rapid growth, expected to reach $30 billion by 2027. Black Friday has become an important sales window for beauty brands and retailers. Our analysis of 19,854 SKUs reveals distinct patterns.

Subcategory Discount Analysis

The category averaged 17% pre-Black Friday discounts with an additional 0.4% during Black Friday Week. Beard Care led early discounting at 21.3%, reflecting strong pre-sale positioning in men’s grooming. Conditioner (17.2%), Makeup (16.9%), and Moisturizer (16.9%) also saw solid baseline promotions. During Black Friday Week, Makeup and Sunscreen saw the highest additional discounts at 0.5% each, while Electric Toothbrush and Toothpaste maintained modest incremental discounts at 0.2%.

Share of Search: Brand Visibility Trends

Affordable and emerging beauty brands dominated during Black Friday in India. Kellsie (beauty tools brand) surged from 1.6% to 6.5%. Classic mass-market brands like Pond’s (+3.4%) and Parachute Advanced (+2.8%) also performed strongly, alongside men’s grooming favorite Beardo (+1.6%). Other popular brands like Maybelline, Tresemme, Vaseline, all saw share of search and visibility increase during Black Friday.

Skincare brand Minimalist made a notable entry, jumping from 0% to 2.0% visibility. The flip side? Premium international brand L’Oréal Paris dropped from 8.3% to 6.5%, losing visibility during Black Friday.

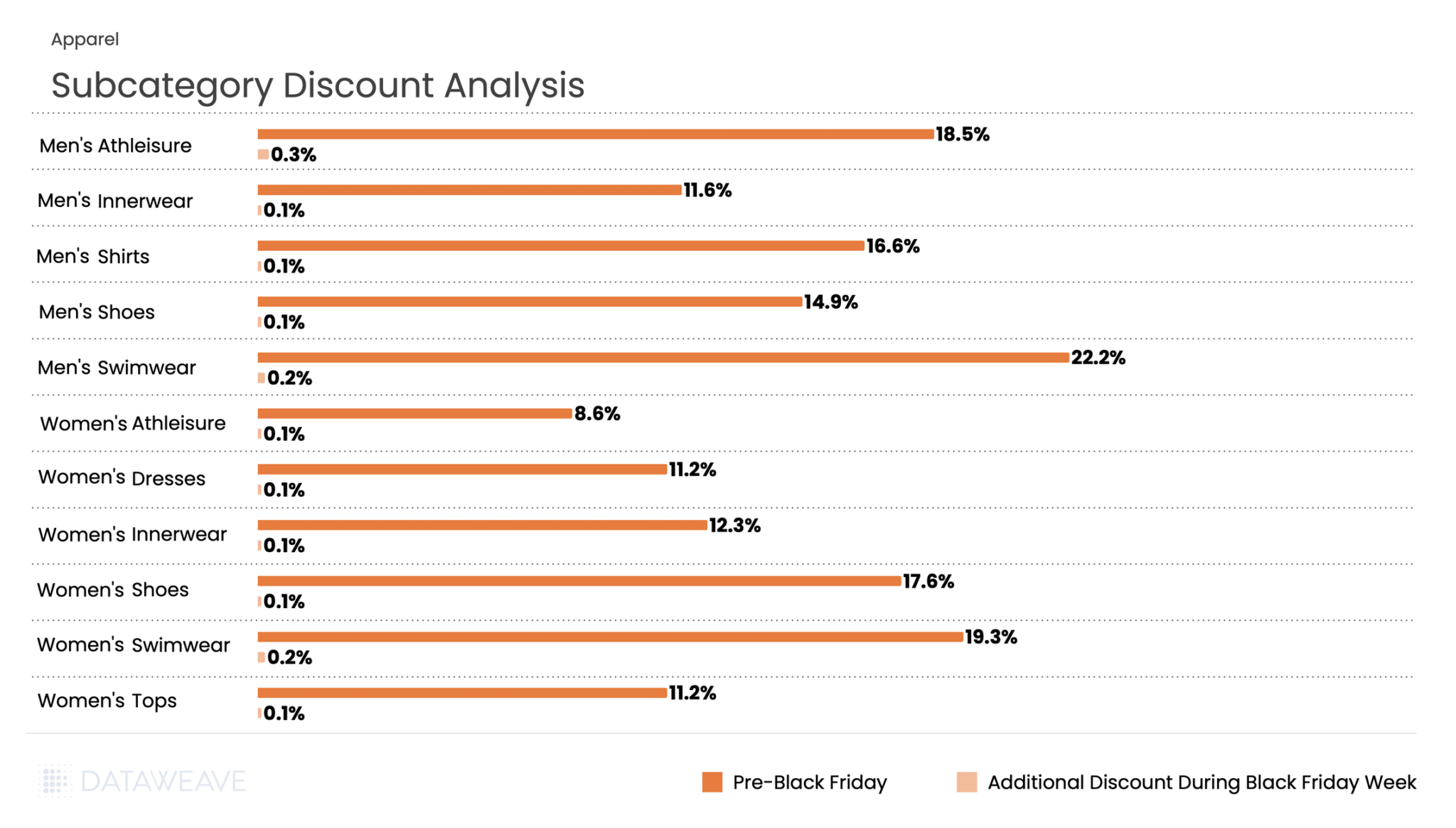

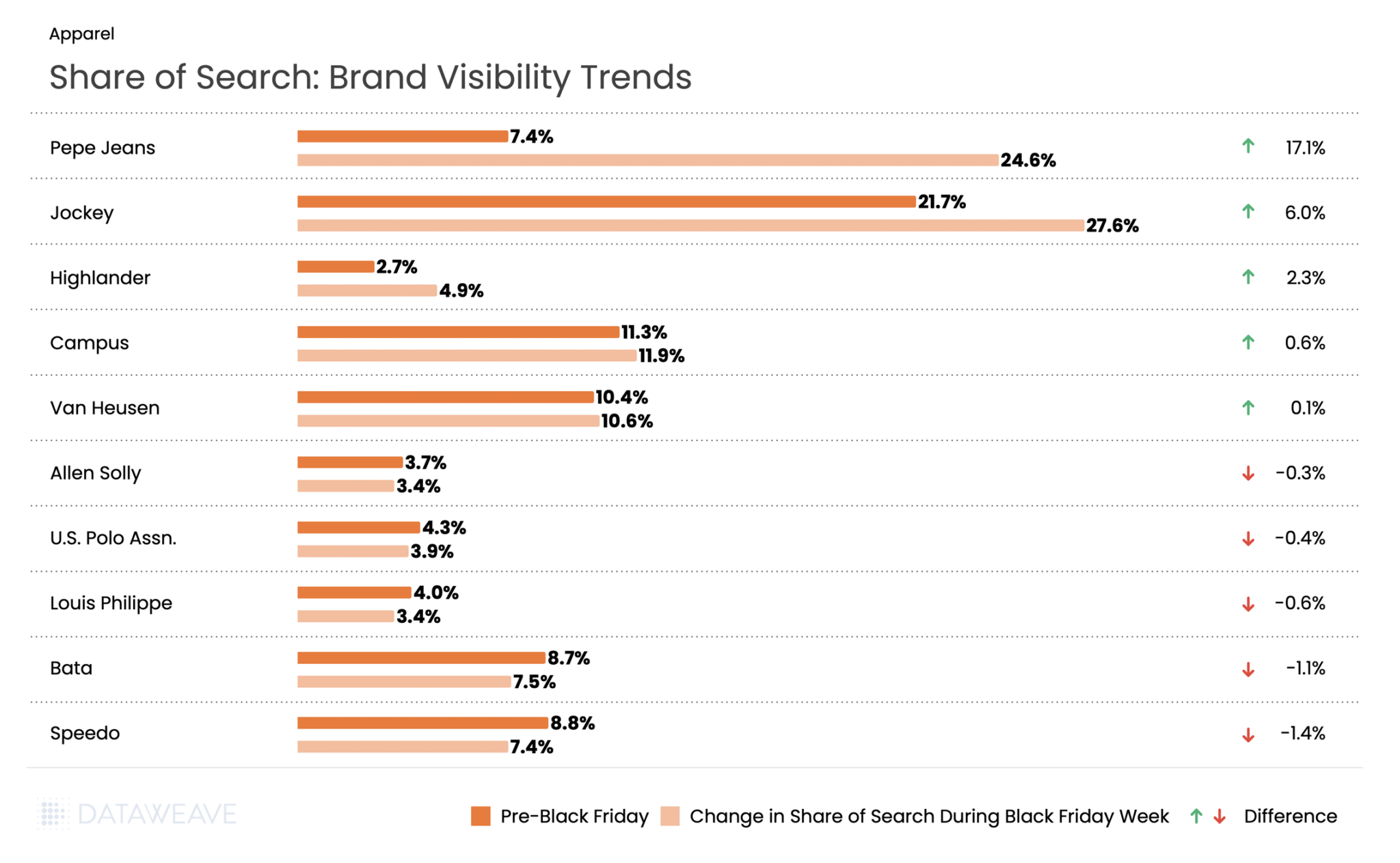

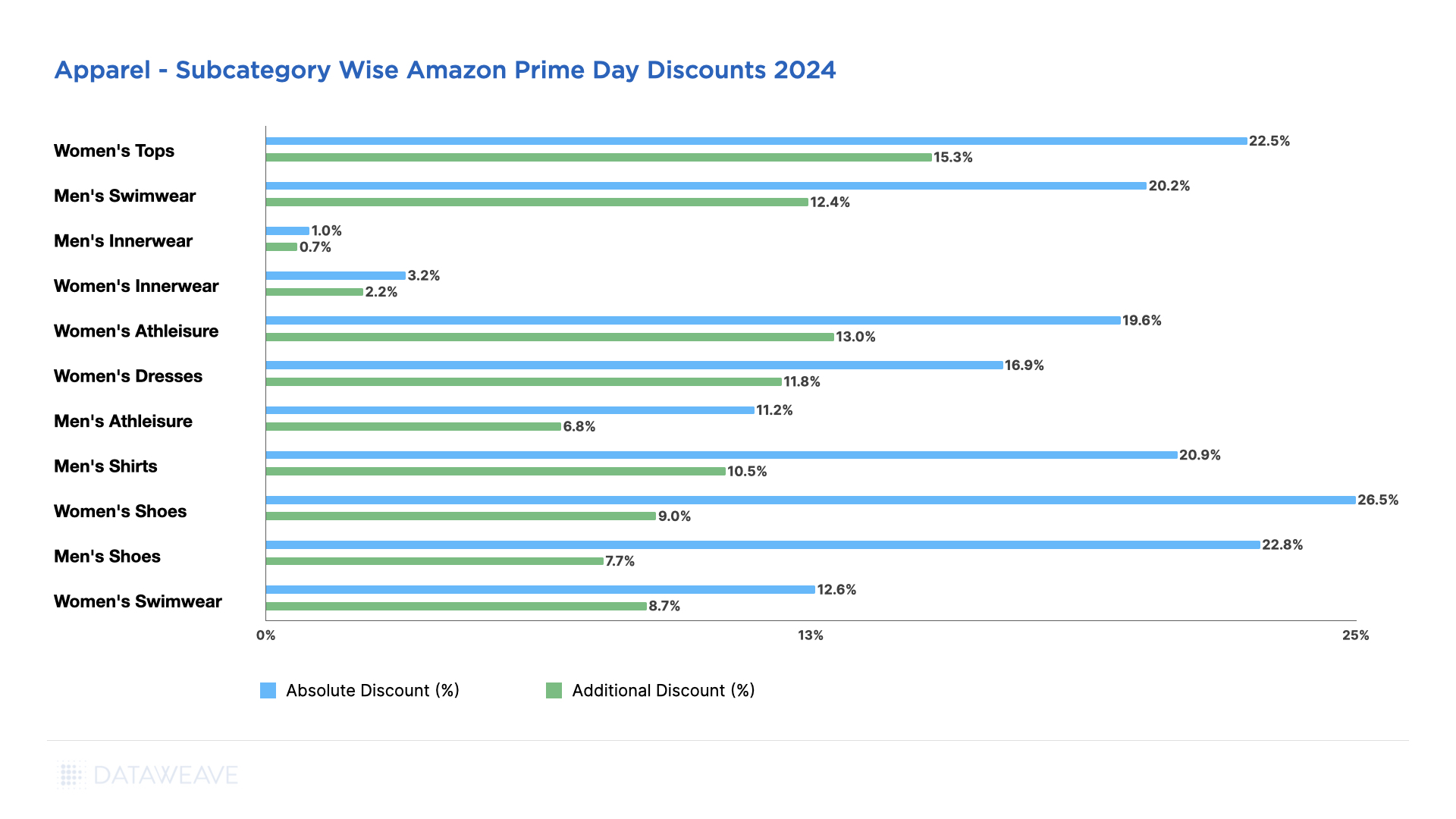

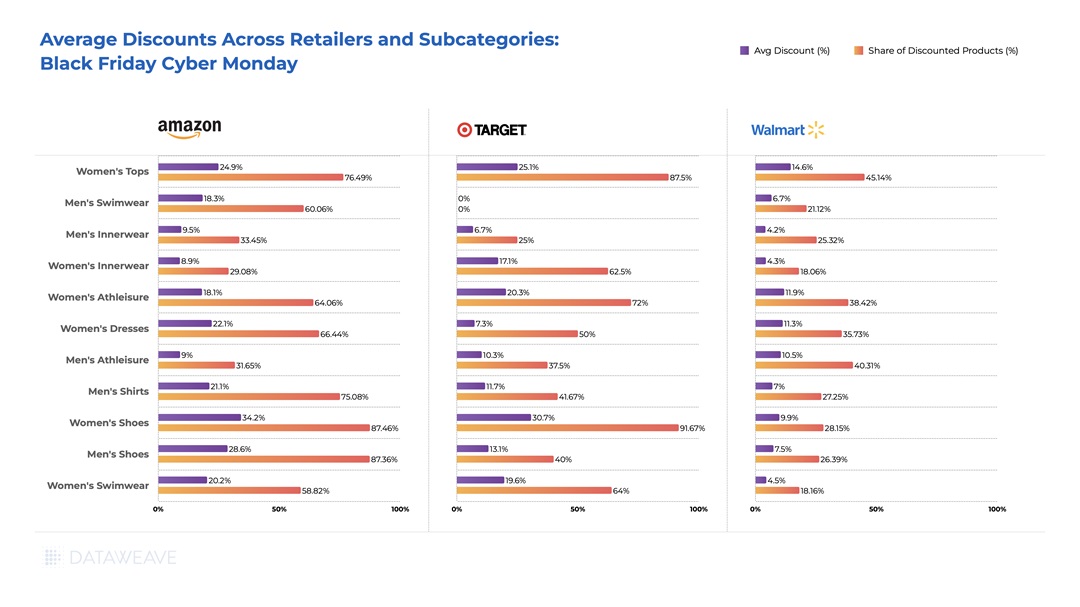

Apparel

Our analysis of 57,537 SKUs reveals interesting discount dynamics.

Subcategory Discount Analysis

The category averaged 14.3% pre-Black Friday discounts with an additional 0.1% during Black Friday Week. Men’s Swimwear and Men’s Athleisure led pre-sale promotions at 22.2% and 18.5% respectively, while Women’s Swimwear and Women’s Shoes also saw strong pre event discounts at 19.3% and 17.6%.

Black Friday Week saw minimal incremental discounting across all subcategories, with most adding just 0.1-0.3%. The relatively subdued incremental discounting indicates that early birds captured the best deals, or that margins were already stretched from pre-sale promotions.

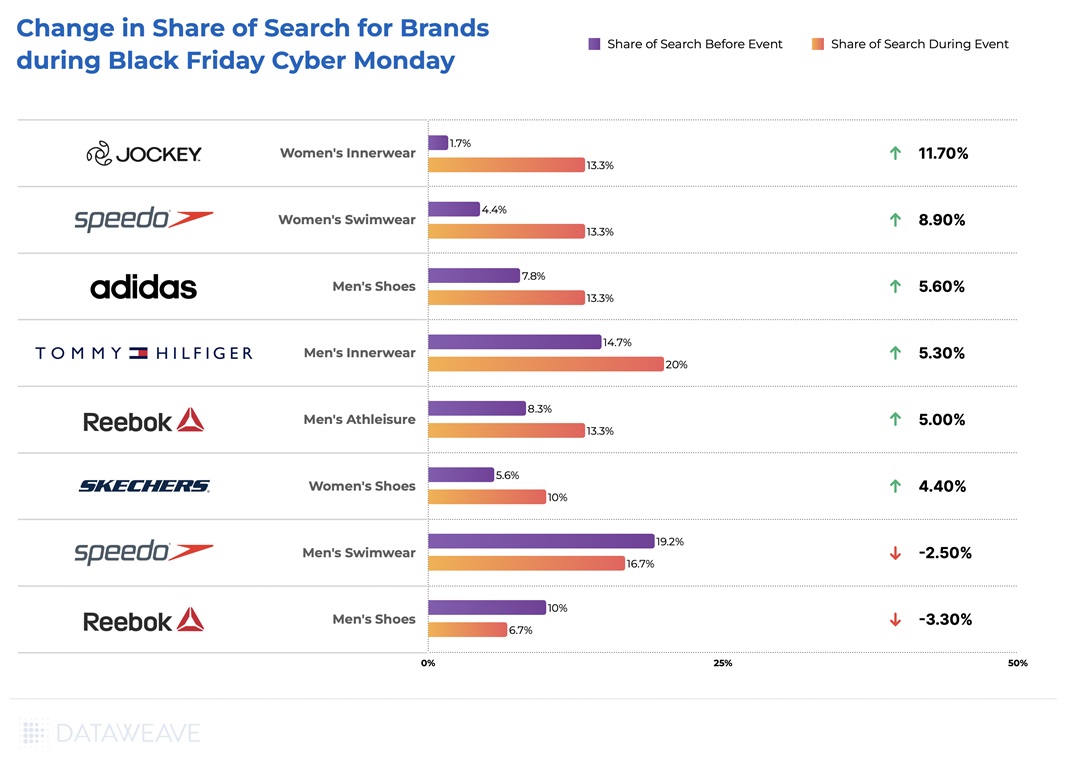

Share of Search: Brand Visibility Trends

Pepe Jeans dominated visibility, surging from 7.4% to 24.6%, a staggering gain that represents the largest visibility increase across all categories. Jockey also performed strongly with a 6% gain, solidifying its position in innerwear.

On the flip side, athletic and footwear stalwarts faced headwinds: Speedo dropped 1.4% and Bata fell 1.1%. This data suggests that during Black Friday 2025 in India, denim and lifestyle fashion brands invested heavily in promotional visibility, capturing massive mindshare at the expense of traditional athletic and footwear brands.

For brands and retailers navigating India’s increasingly competitive e-commerce landscape, the 2025 Black Friday data reveals a critical insight: pre-sale positioning matters more than Black Friday Week discounting. Early promotional investment and visibility campaigns delivered far greater returns than late-stage price drops, fundamentally reshaping how brands should approach this shopping event.

Want to understand how DataWeave’s retail intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Check out our analysis on Black Friday 2025 Pricing and Discount trends in the USA, Canada, UK, and Germany. Follow our blog for more insights on retail pricing trends, brand visibility analysis, and data-driven commerce intelligence.

Black Friday 2025 solidified its position as a major retail event in the German market. German consumers demonstrated an average Black Friday budget of €317, the highest among select European countries.

The German market, however, exhibited unique consumer behavior patterns during Black Friday 2025. Rather than meticulous planning, 59% of German shoppers allowed deals to inspire their purchases, compared to just 32% who shopped with predetermined lists and budgets. This spontaneous yet budget-conscious approach distinguishes German consumers from other markets, where FOMO-driven purchasing tends to dominate.

Against this backdrop of rational deal-seeking and regional diversity, how did retailers and brands perform across key categories this Black Friday?

At DataWeave, we conducted a comprehensive analysis of Black Friday 2025 discounting trends across five major categories in the German market: Consumer Electronics, Home & Furniture, Health & Beauty, Grocery, and Apparel. Our AI-powered pricing intelligence platform monitored over 16,000+ SKUs across leading German retailers like Amazon, Aldi, Douglas, Nutritienda, Carethy, Bofrost, and more, revealing fascinating patterns in how retailers and brands approached this year’s sale season.

Our Methodology

For this analysis, DataWeave monitored average discounts across leading German retailers during two distinct periods:

Pre-Black Friday: November 6 – November 23, 2025 – capturing early holiday deals and baseline pricing

Additional Discounts During Black Friday Week: November 24 – December 1, 2025 – covering Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

Our sample encompassed the top-ranked products across subcategories on major retail sites. We also analyzed Share of Search data, which measures brand visibility by monitoring which brand names appear in the top 20 search results for critical keywords.

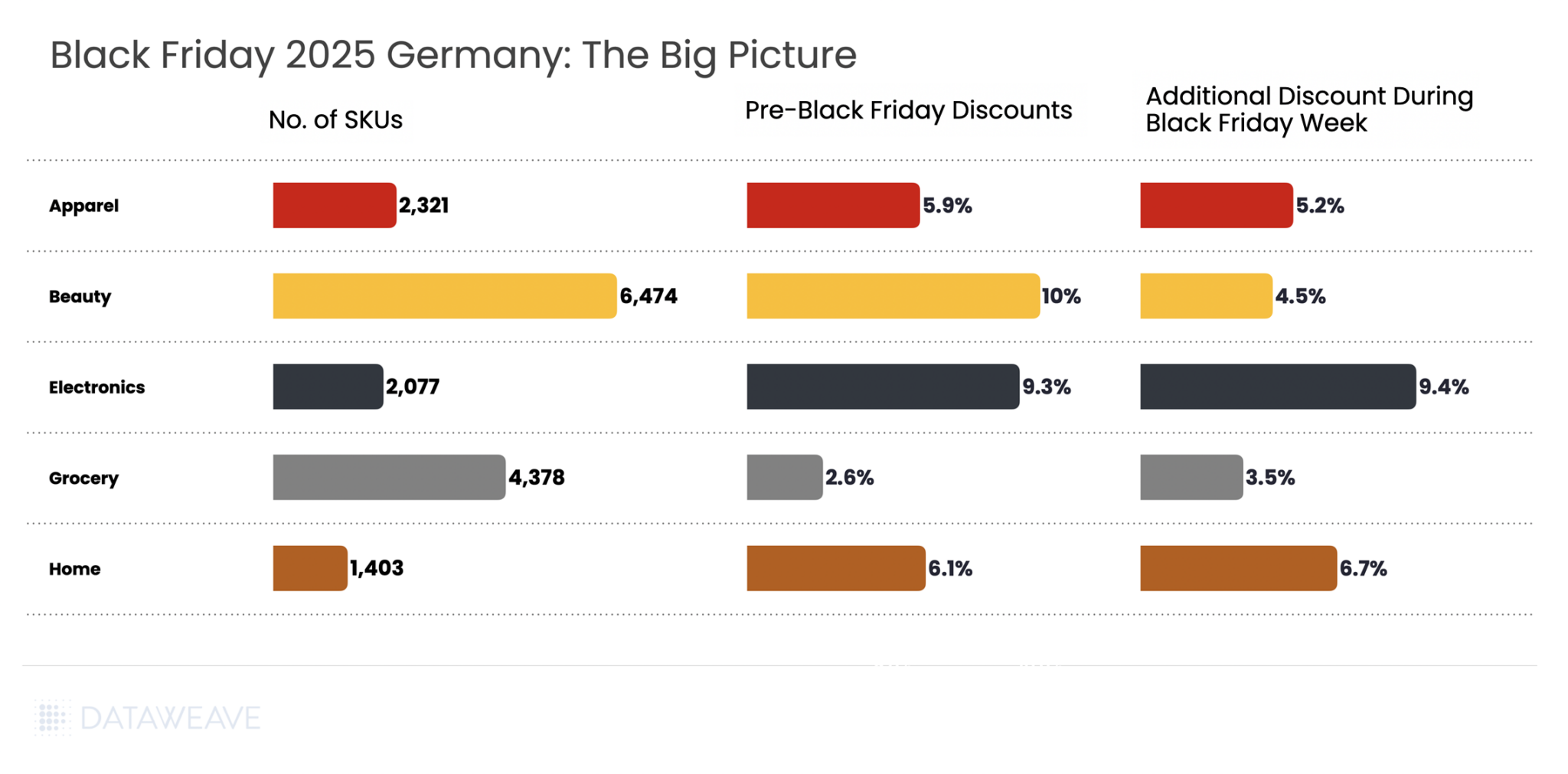

Black Friday 2025 Germany: The Big Picture

Our analysis covered 16,653 SKUs across five major categories. Here’s the snapshot of average discounts during the Pre-Black Friday period compared to Black Friday Week:

Key Insight: The German market presented a notably different discounting pattern compared to other markets. Pre-Black Friday discounts averaged 7% across all categories, with Black Friday Week adding 5.1% on average. Unlike the UK and US markets where retailers front-loaded promotions heavily, German retailers took a more balanced approach, with several categories actually seeing higher discounts during the main Black Friday Week.

Beauty led pre-sale discounts at 10%, followed by Electronics at 9.3%. Consumer electronics stood out with the highest Black Friday Week discounts at 9.4%, slightly exceeding even the pre-sale period at 9.3%.

Shopping Behavior Patterns: The relatively modest discount levels reflect the rational, value-oriented approach of German consumers. With the majority of shoppers setting budgets between €100-€299 and prioritizing wish fulfillment over impulse purchases, German retailers focused on strategic discounting rather than aggressive margin erosion.

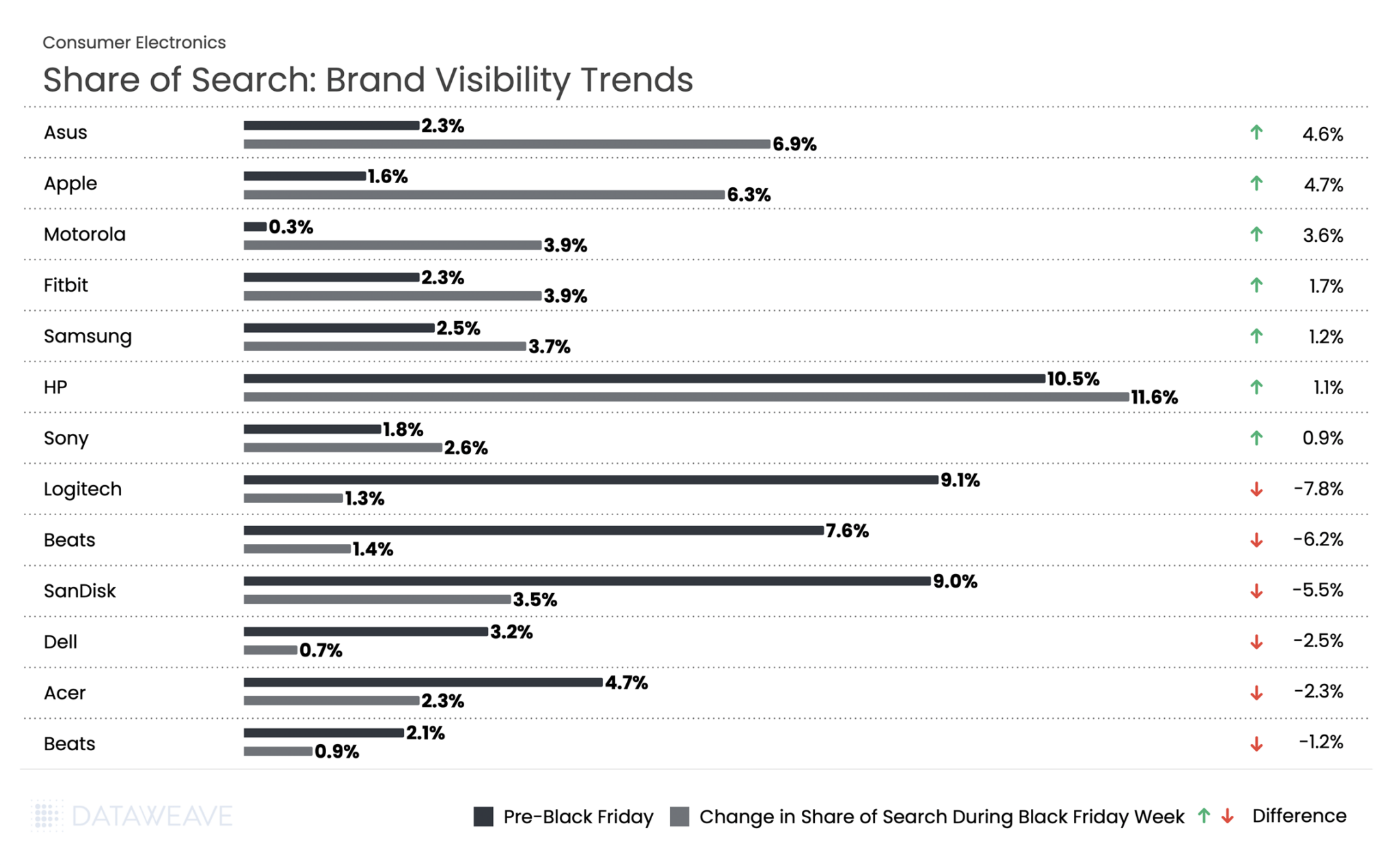

Consumer Electronics

Consumer electronics dominated German Black Friday interest, with 77% of German shoppers most interested in electronics deals, making it the most anticipated category during the sales period. Our analysis of 2,077 SKUs reveals how discounts varied across subcategories and which brands dominated search visibility in this highly competitive category.

Subcategory Discount Analysis

This was one of the few categories where Black Friday Week discounts matched or exceeded pre-sale levels. Wearables led pre-sale discounting at 16.3%, followed closely by Audio & Video at 15.8%. During Black Friday Week, these categories saw additional discounts of 12.2% and 12.4% respectively.

The standout performer was Home Automation, which nearly doubled its additional discount from 7.2% to 13.9% during Black Friday Week. Mobile Devices saw additional discounts dropping from 13.4% pre-sale to 7.1% during Black Friday Week. Meanwhile Gaming doubled additional discounting from 2.1% to 4.3%.

Share of Search: Brand Visibility Trends

Our Share of Search analysis reveals significant shifts in brand visibility during Black Friday Week:

HP saw the highest share of search across Black Friday at 10.5% pre event and 11.6% during the event. Apple led with a 4.7% increase in visibility, jumping from 1.6% to 6.3%. Asus followed at 4.6%. Motorola surged 3.6 %, while wearables brand Fitbit gained 1.7%.

In stark contrast, Logitech dropped by 7.8 %, Beats fell 6.2 %, and SanDisk declined 5.5 %. Computer manufacturers Dell and Acer also struggled, falling 2.5 and 2.3 % respectively.

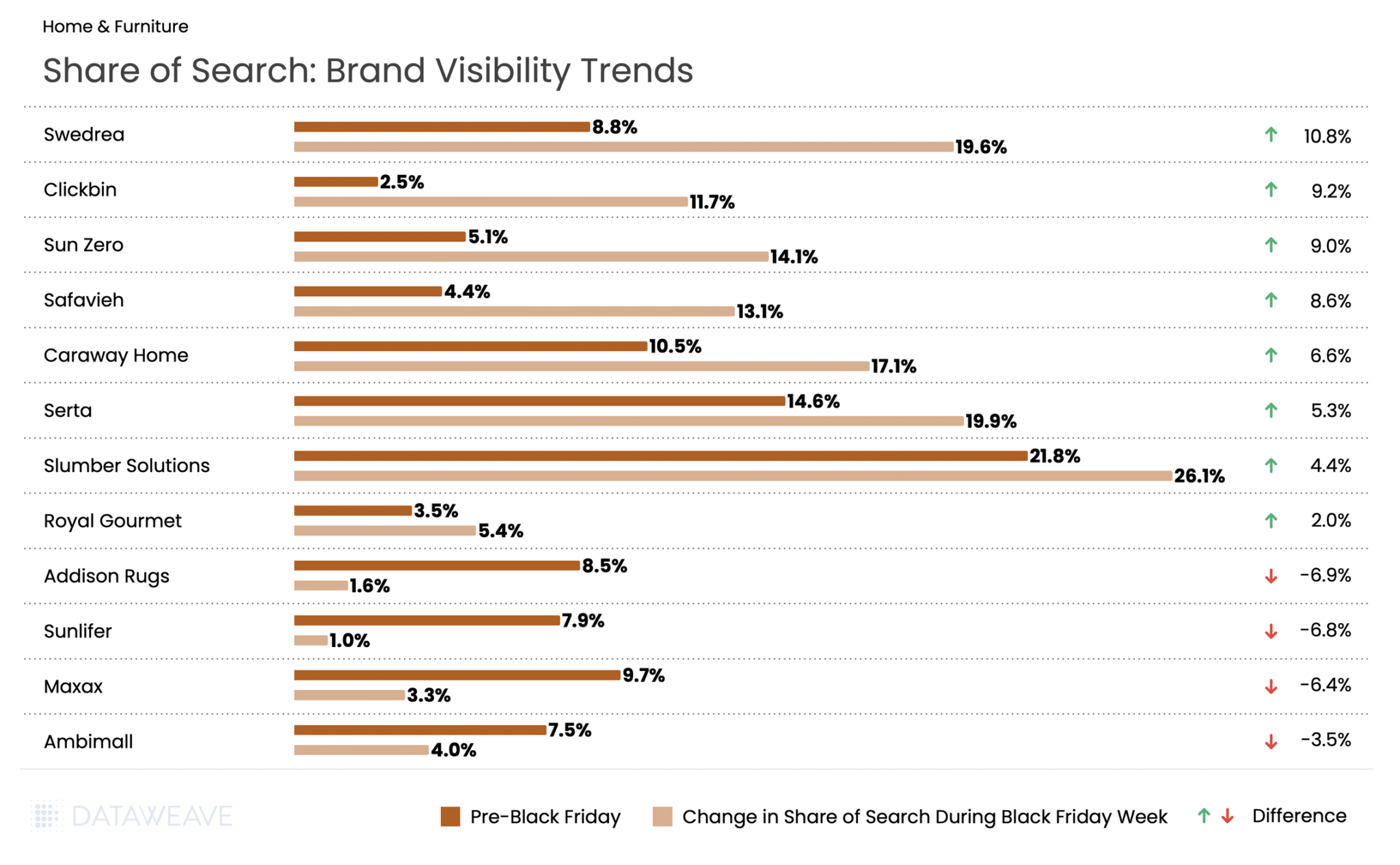

Home & Furniture

The Home & Furniture category in Germany showed unique discounting behavior compared to other markets, with additional Black Friday Week discounts (6.7%) actually exceeding Pre-Black Friday levels (6.1%). Our analysis of 1,403 SKUs shows how discounts were distributed across subcategories.

Subcategory Discount Analysis

Kitchenware led pre-sale discounts at 8.7%. Decor surged from 5% to 7.5%, lighting jumped from 5% to 6.9%, and bedding more than doubled from 3.2% to 6.6%. These substantial increases suggest strategic timing to capture consumer attention during peak shopping days.

Share of Search: Brand Visibility Trends

Mattress brand Slumber Solutions saw the highest share of search at 21.8% pre event and 26.1% during Black Friday week. Meanwhile, another mattress brand Swedrea led all brands with a remarkable 10.8% surge in visibility, jumping from 8.8% to 19.6%. Budget-friendly furniture brand Clickbin gained 9.2%, while window treatment brand Sun Zero increased 9% and home textiles brand Safavieh surged 8.6%.

Premium and established brands also performed well: Caraway Home (cookware) rose 6.6%, mattress brand Serta gained 5.3%, and Slumber Solutions added 4.4%. Royal Gourmet, specializing in outdoor cooking equipment, gained 2.0%.

However, several mid-tier brands faced steep declines. Addison Rugs dropped 6.9% from 8.5% to just 1.6%, while Sunlifer fell 6.8 % and Maxax declined 6.4 %.

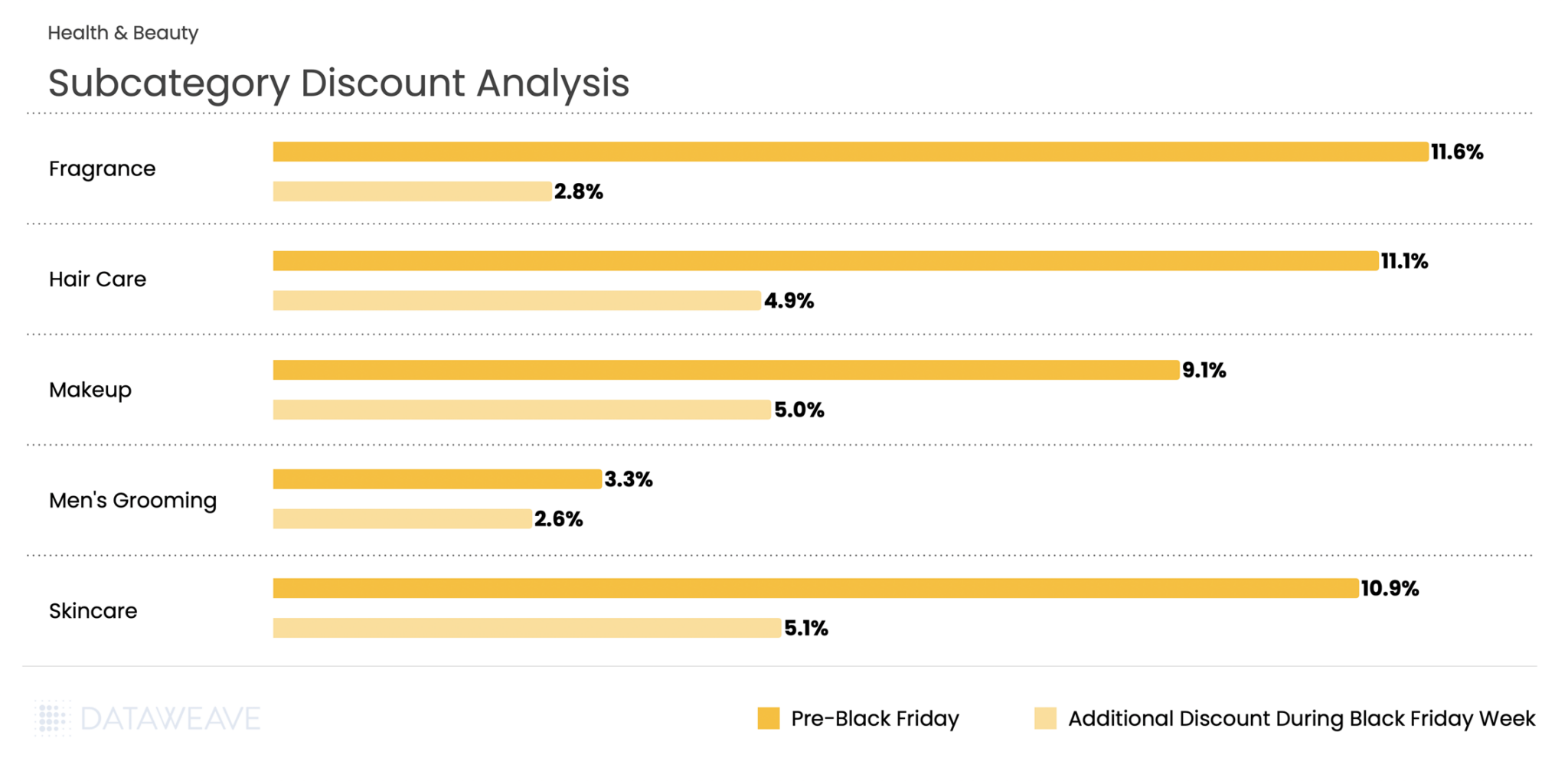

Health & Beauty

Our analysis of 6,474 SKUs reveals subcategory-level insights and dramatic brand visibility shifts that highlight the evolving German beauty landscape.

Subcategory Discount Analysis

Pre-Black Friday discounts averaged 10%, with Black Friday Week adding 4.5% on average. Fragrance led pre-sale discounting at 11.6%, positioning perfumes and colognes as attractive early holiday purchases. However, Fragrance saw the smallest Black Friday Week addition at just 2.8%.

Hair Care and Skincare both showed strong performance across both periods, with Hair Care at 11.1% pre-sale and 4.9% during Black Friday Week, while Skincare registered 10.9% and 5.1% respectively. Skincare’s 5.1% Black Friday Week discount was the highest in the category.

Men’s Grooming stood apart with notably lower discounts at 3.3% pre-sale and 2.6% during Black Friday Week, suggesting either tighter margins in this subcategory or strategic positioning at different price points.

Share of Search: Brand Visibility Trends

L’Oréal Deutschland GmbH emerged as the most visible brand, surging from 37.7% to 51.9%, (+14.2). German pharmaceutical cosmetics company Medicos Kosmetik GmbH & Co. KG gained 4.4 %. Clinique gained 3.3 %, and French luxury brand Sisley added 3.1 %, German natural cosmetics brand Weleda rose 2.7 %, and Japanese prestige brand Shiseido gained 2.5 %.

The flip side? K-beauty brands and some international names faced significant challenges. Viral make-up brand Tirtir experienced the steepest decline visibility, dropping by 9.2 %. Aveda fell 6.2 %, Elizabeth Arden dropped 5.8 %, and Beauty of Joseon declined 3.8 %. German pharmacy brand Mi.to. Pharm GmbH lost 4.3 %, while Israeli makeup brand GA-DE fell 3.3 %.

The data reveals a clear German preference for European beauty heritage, pharmaceutical-grade cosmetics, and established prestige brands during Black Friday, rather than trendy K-beauty products or mid-tier international brands.

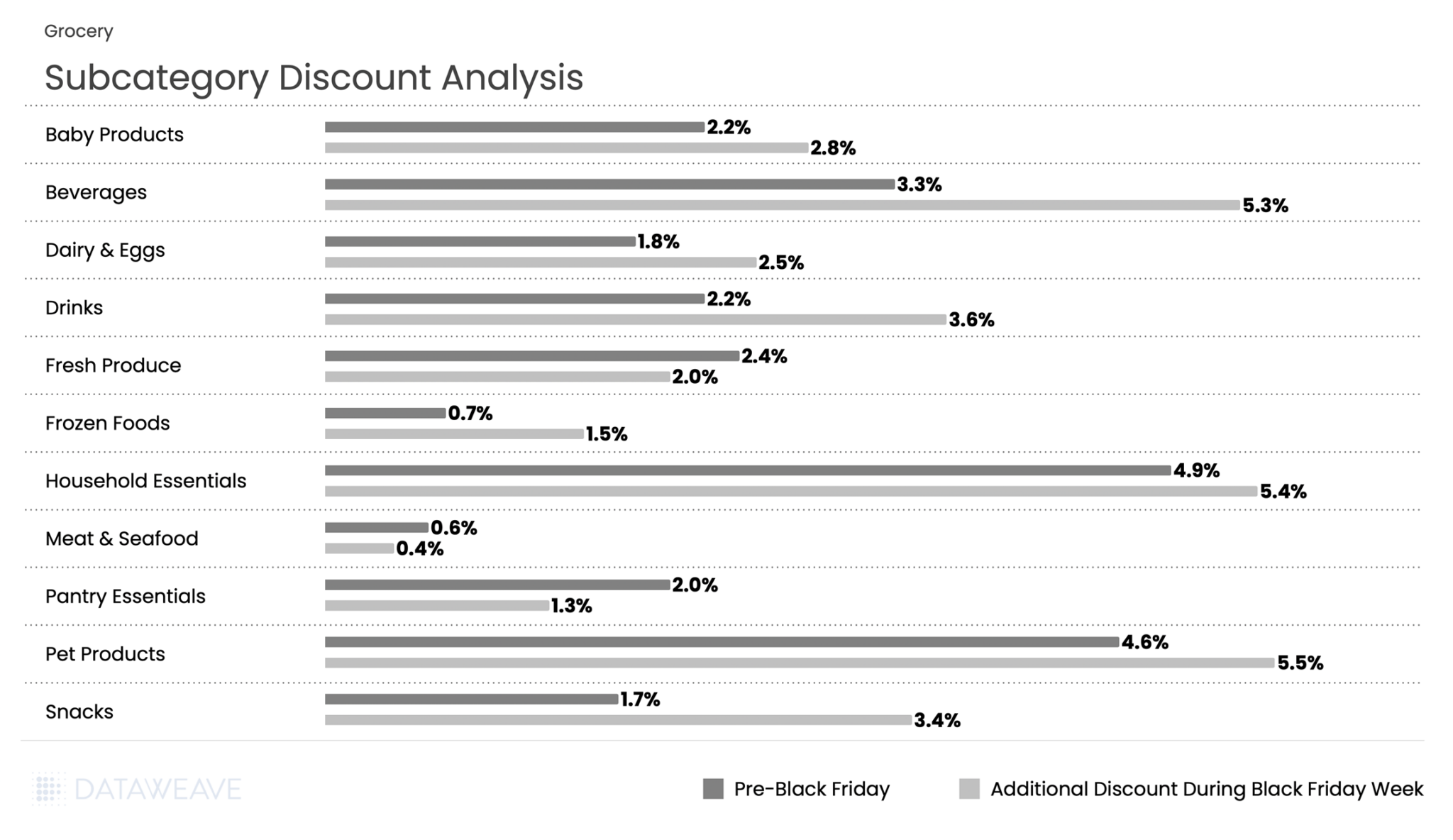

Grocery

While Grocery typically sees more modest discounts compared to discretionary categories, the German market showed interesting patterns with Black Friday Week discounts (3.5%) actually exceeding Pre-Black Friday levels (2.6%). Our analysis of 4,378 SKUs shows how German retailers approached promotions across essential and indulgent subcategories.

Subcategory Discount Analysis

Pre-Black Friday discounts averaged just 2.6% in grocery. But Black Friday Week saw this surging to 3.5%, an increase that represents the highest proportional jump among all categories.

Pet Products and Household Essentials led discounting, with Pet Products at 4.6% pre-sale and an additional 5.5% during Black Friday Week. Meanwhile Household Essentials registered 4.9% and 5.4% respectively.

Beverages showed particularly strong Black Friday Week performance, jumping from 3.3% to 5.3%, while snacks doubled from 1.7% to 3.4%. Fresh categories maintained minimal promotional activity consistent with perishable inventory constraints: Meat & Seafood saw negligible discounts (0.6% pre-sale, 0.4% Black Friday Week), while Fresh Produce actually decreased from 2.4% to 2% during the main event.

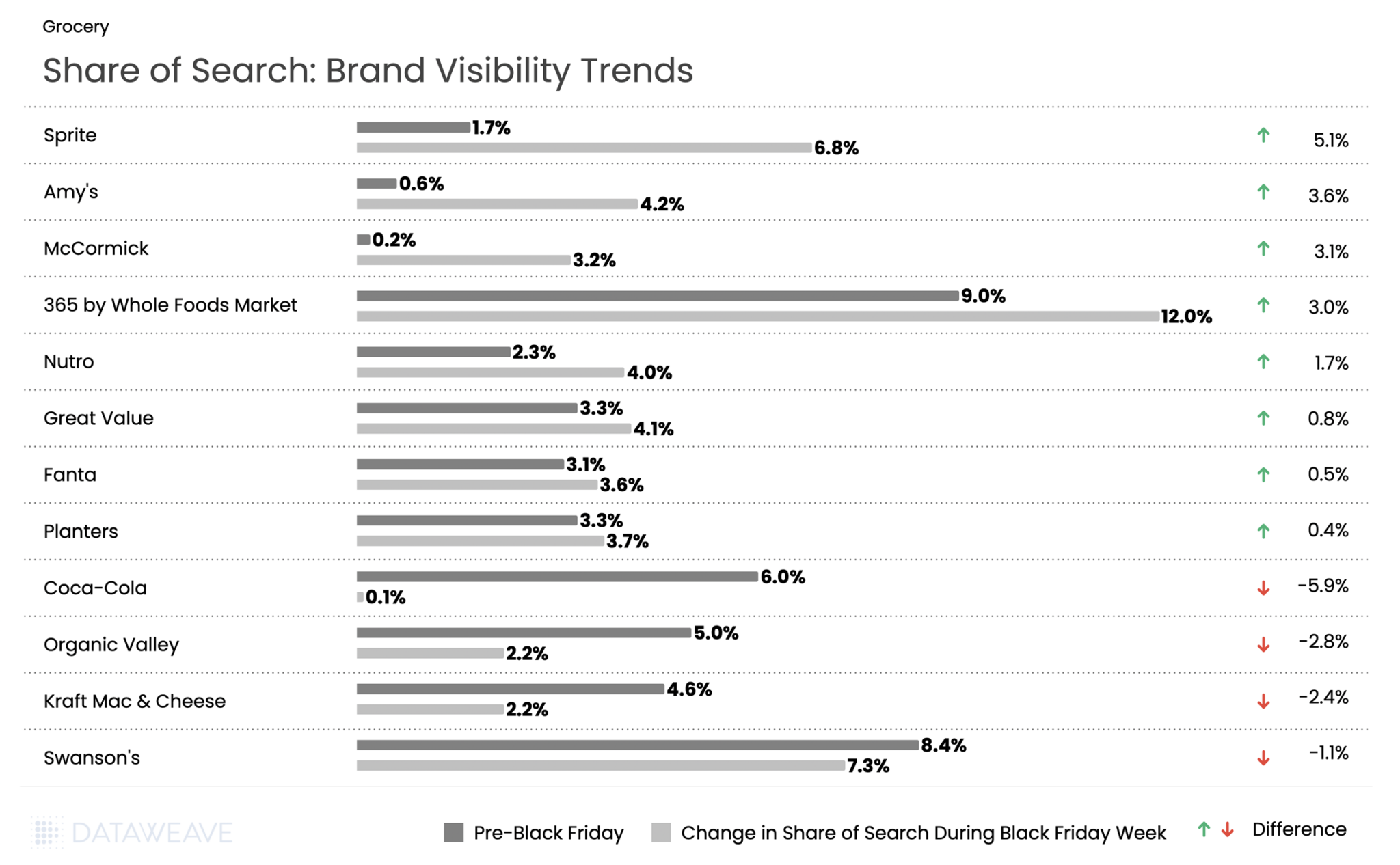

Share of Search: Brand Visibility Trends

365 by Whole Foods saw the highest share of search at 9% pre event and 12% during Black Friday week. But Sprite led all brands with a 5.1% surge in share of search. Meanwhile, sister brand Coca-Cola experienced one of the steepest declines in our analysis, with visibility plummeting from 6.0% to just 0.1%. Fanta maintained modest search growth at 0.5 %. This stark divergence between two brands from the same parent company suggests vastly different promotional strategies during Black Friday Week.

Specialty and organic food brands performed well: Amy’s (organic/natural foods) gained 3.6 %, while spice brand McCormick surged 3.1 %. Pet food brand Nutro gained 1.7 %, while value-oriented Great Value added 0.8 %.

Snack brand Planters gained 0.4 %. On the decline side, Organic Valley dropped 2.8 %, Kraft Mac & Cheese fell 2.4 %, and Swanson’s declined 1.1 %.

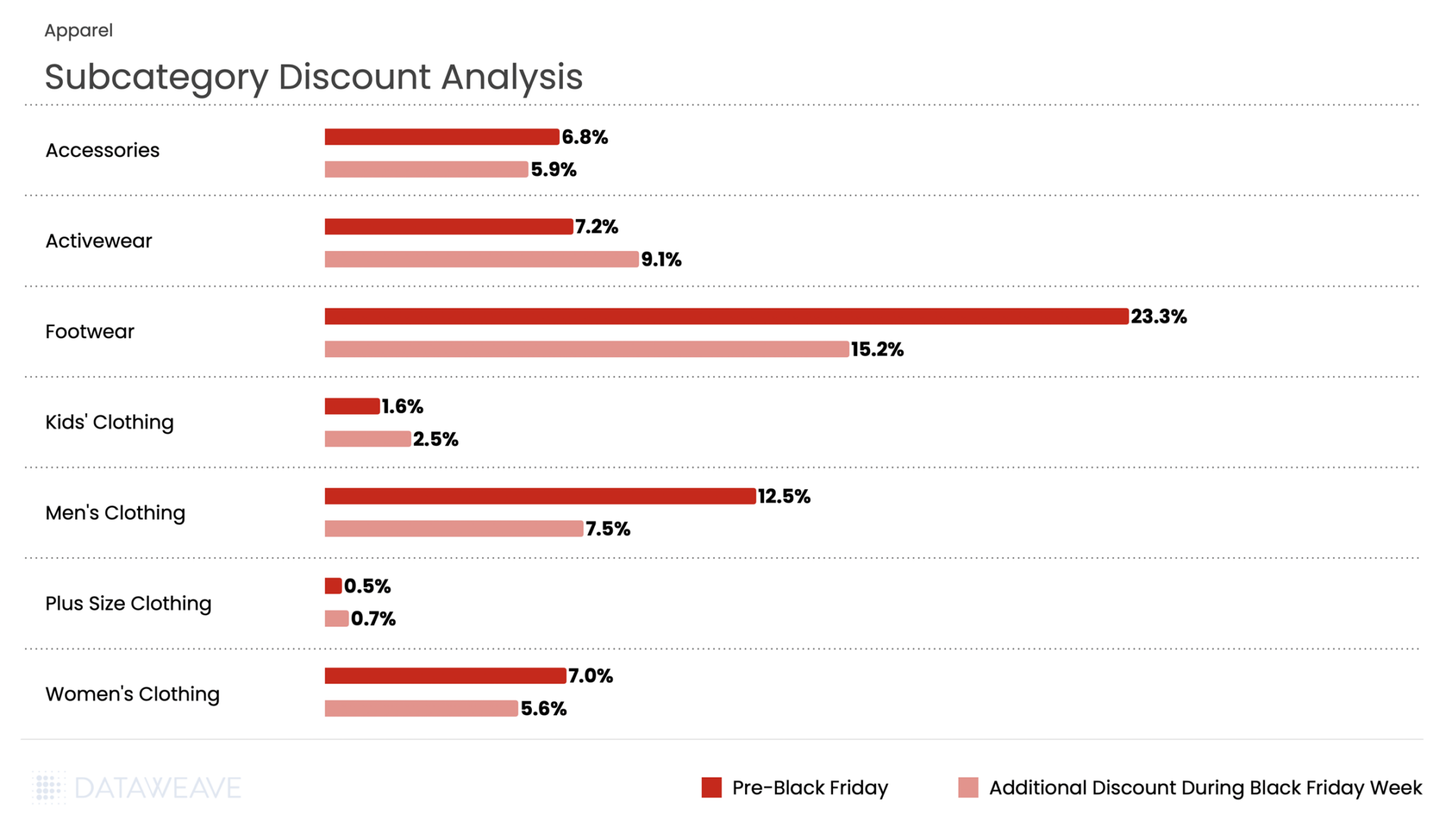

Apparel

Apparel in the German market showed modest promotional activity compared to other markets, with Pre-Black Friday discounts averaging 5.9% and Black Friday Week at 5.2%. Our analysis of 2,321 SKUs reveals interesting patterns across fashion segments in the German market.

Subcategory Discount Analysis

Footwear dominated discounting in both periods, with an impressive 23.3% pre-sale discount, and 15% additional discount during Black Friday Week. Men’s Clothing followed at 12.5% pre-sale, with additional 7.5% during Black Friday Week.

Activewear presented a unique pattern, with discounts increasing from 7.2% pre-event to additional 9.1% during Black Friday Week: one of the few subcategories to show higher discounts during the main event. Plus Size Clothing saw minimal promotional activity at 0.5% pre-sale and 0.7% during Black Friday Week, the lowest discounts in the entire category.

Share of Search: Brand Visibility Trends

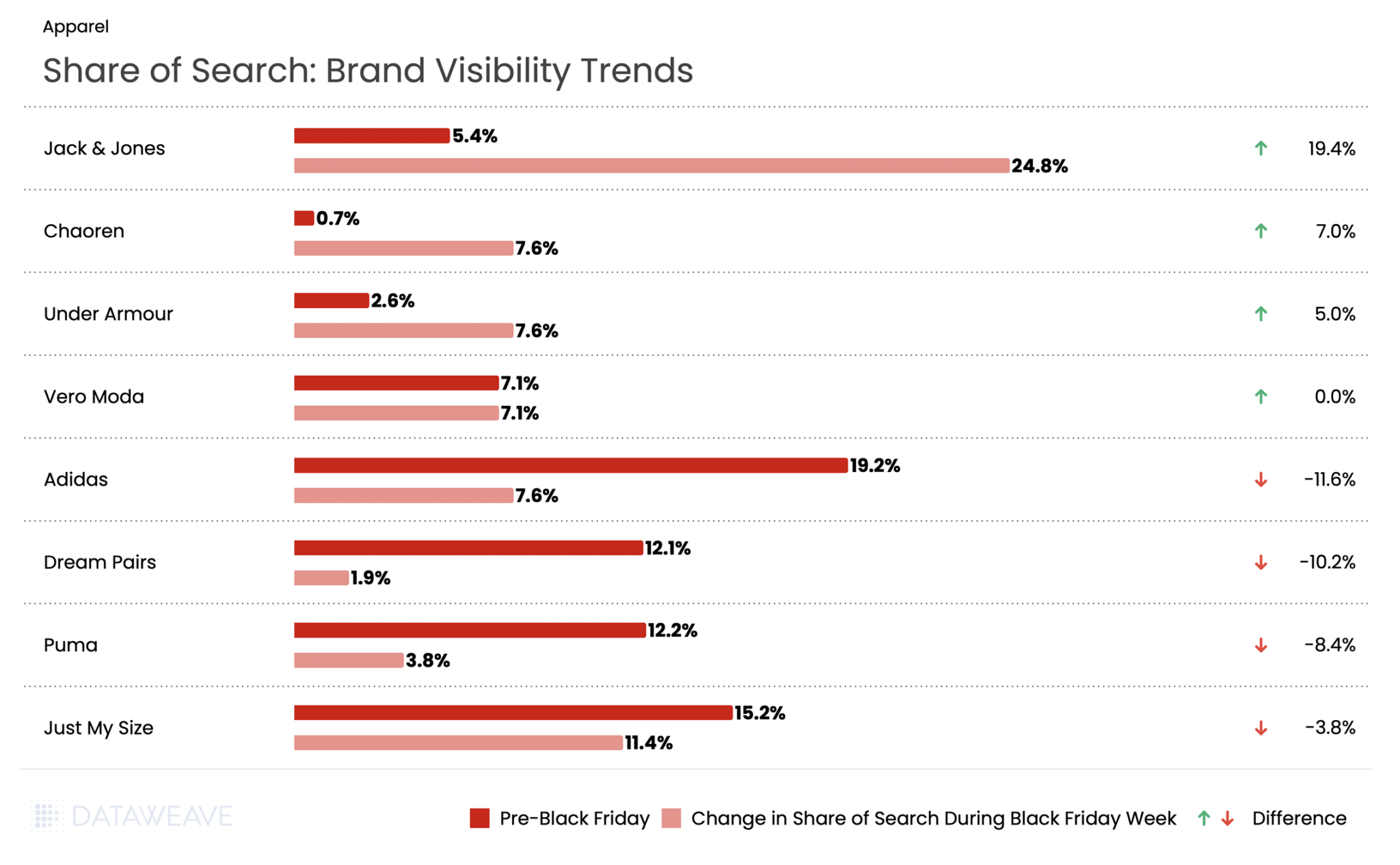

Danish fashion brand Jack & Jones experienced an unprecedented surge with a staggering 19.4% gain in visibility. Sister brand Vero Moda (also owned by Jack & Jones’ parent company Bestseller) maintained flat visibility at 7.1%. Footwear brand Chaoren gained 7%. Meanwhile activewear giant Under Armour rose by 5%.

However, established sportswear giants suffered dramatic visibility losses. Adidas experienced an 11.6% decline in share of search. Dream Pairs saw visibility drop by 10.2%, Puma fell 8.4%, and plus-size brand Just My Size declined by 3.8 %.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Check out our analysis on Black Friday Pricing and Discount trends in the USA and UK. Follow our blog for more insights on retail pricing trends, brand visibility analysis, and data-driven commerce intelligence.

Black Friday 2025 saw British shoppers spend an average of £430 each this year representing a £91 increase from last year and totaling over £10.2 billion across the sales period.

The 2025 sales event arrived at a pivotal moment for UK retail. Retail sales fell 1.1% in October 2025 as consumers held back spending in anticipation of Black Friday promotions, according to the Office for National Statistics. Over 2 in 5 UK adults participated in Black Friday shopping, with 45% planning to pick up Christmas gifts at a discount, according to a Barclays study.

Against this backdrop of cautious optimism and strategic consumer behavior, how did retailers and brands perform across key categories this Black Friday? At DataWeave, we conducted a comprehensive analysis of Black Friday 2025 discounting trends across five major categories in the UK market: Consumer Electronics, Home & Furniture, Health & Beauty, Grocery, and Apparel. Our AI-powered pricing intelligence platform monitored over 71K SKUs across leading UK retailers like Costco, Selfridges, Boots, Debenham’s, Carethy, Argos, John Lewis, Amazon, and more, revealing fascinating patterns in how retailers and brands approached this year’s sale season.

Our Methodology

For this analysis, DataWeave monitored average discounts across leading UK retailers during two distinct periods:

Pre-Black Friday: November 6 – November 23, 2025 – capturing early holiday deals and baseline pricing

Additional Discounts During Black Friday Week: November 24 – December 1, 2025 – covering Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

Our sample encompassed the top-ranked products across subcategories on major retail sites. We also analyzed Share of Search data, which measures brand visibility by monitoring which brand names appear in the top 20 search results for critical keywords.

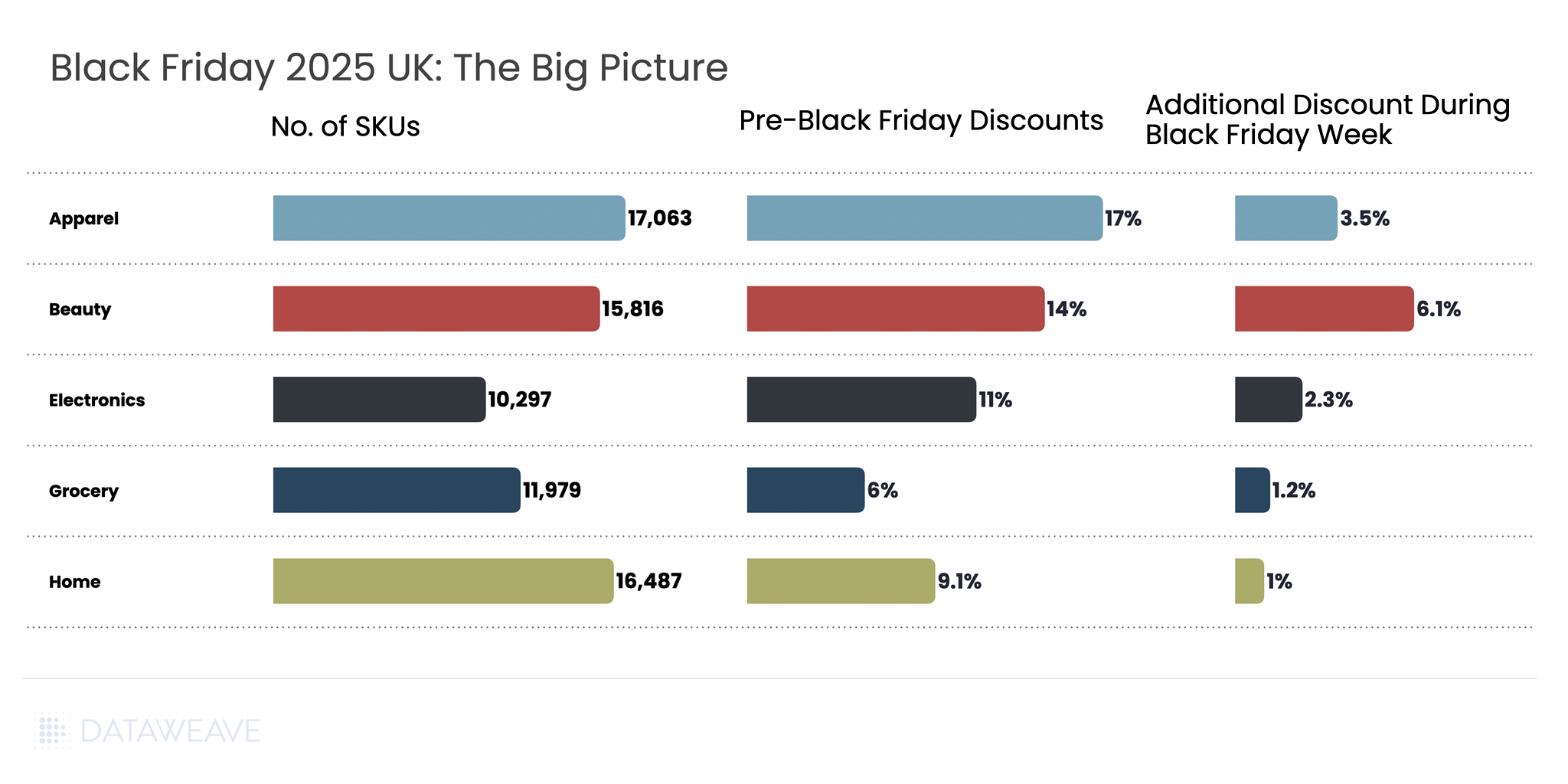

Black Friday 2025 UK: The Big Picture

Our analysis covered 71,642 SKUs across five major categories. Here’s the snapshot of average discounts during the Pre-Black Friday period compared to Black Friday Week:

Key Insight: Pre-Black Friday discounts were substantial across all categories. This suggests UK retailers front-loaded their promotions to capture early holiday shoppers, with additional discounts during Black Friday Week adding to the baseline discounts already in place. The extended promotional period transformed Black Friday from a single-day event into a month-long campaign, with 60% of UK shoppers beginning their deal searches as early as October.

Consumer Electronics

Consumer electronics remains a cornerstone of Black Friday shopping in the UK, with technology accounting for 48% of planned consumer spending during the sales period, according to PwC.

AI is transforming how consumers shop for electronics, with AI-driven traffic to retail sites expected to rise 410% year-on-year during the 2025 holiday season. Younger shoppers particularly embraced AI tools, with 17% of Gen Z consumers using AI platforms like Chat GPT and Gemini to source and compare deals. Our analysis of 10,297 SKUs reveals how discounts varied across subcategories and which brands dominated search visibility.

Subcategory Discount Analysis

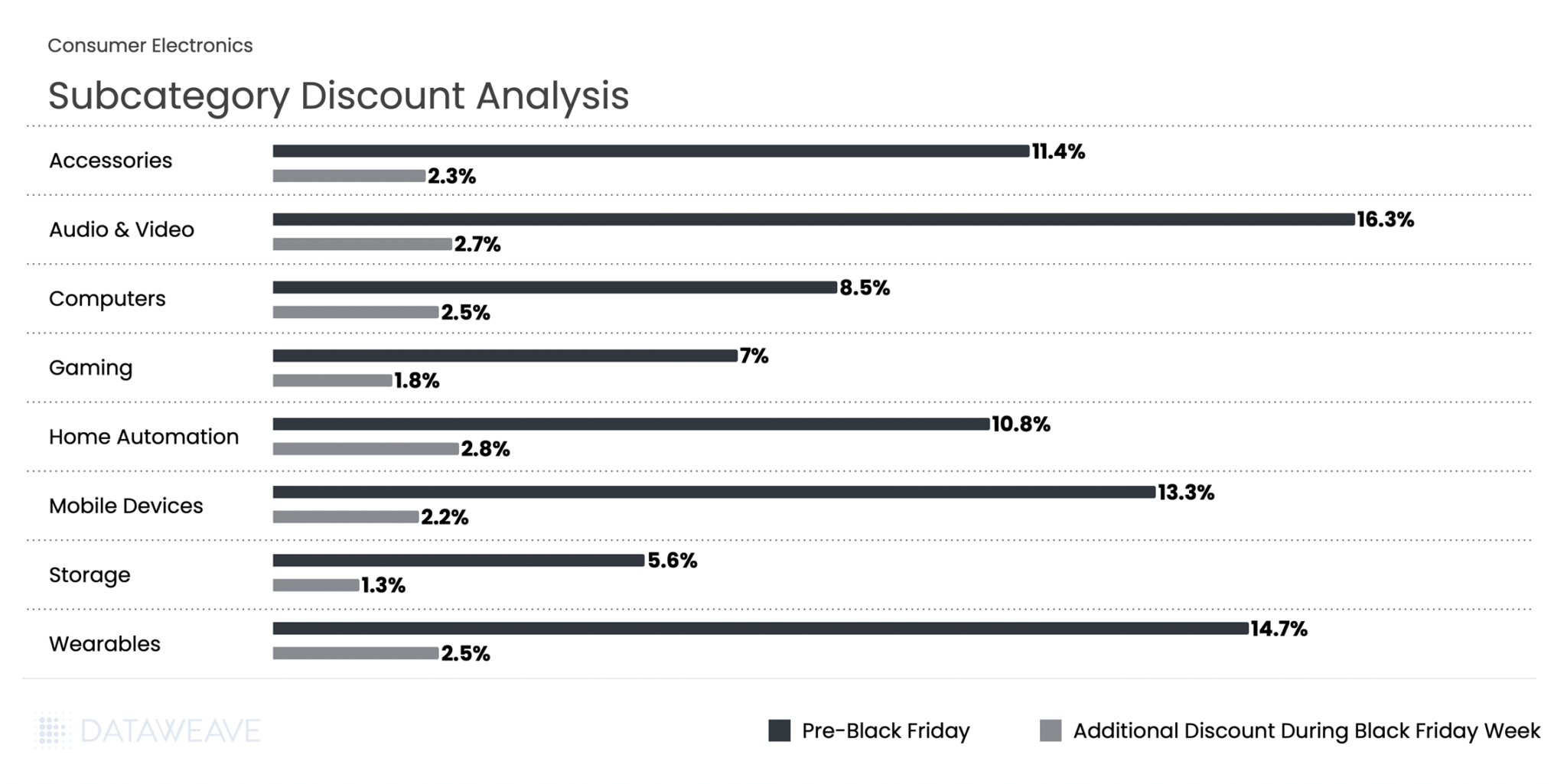

Pre-Black Friday discounts averaged 11.1% across subcategories, while Black Friday Week saw an additional 2.3% discount on average. Audio & Video products led the pre-sale discounting at 16.3%, indicating retailers were eager to move inventory early in the season.

During Black Friday Week, Home Automation saw the highest additional discount at 2.8%. Wearables and Computers both saw solid 2.5% additional discounts, making them attractive categories during the peak shopping period.

Share of Search: Brand Visibility Trends

Our Share of Search analysis reveals significant shifts in brand visibility during Black Friday Week:

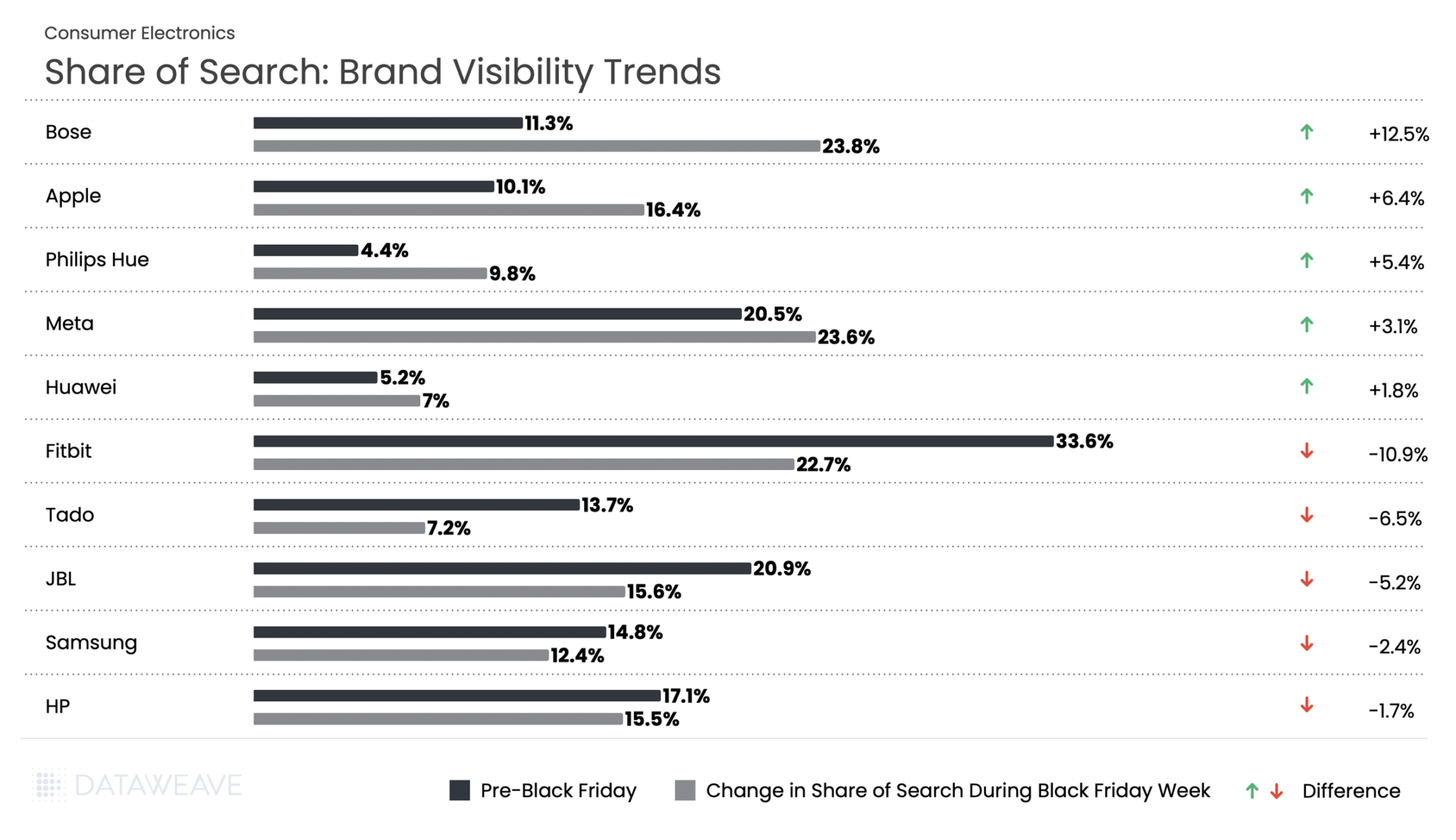

Bose dominated with its Share of Search more than doubling from 11.3% to 23.8%, a remarkable +12.5% gain. Lighting brand Philips Hue followed, gaining by +5.4% in share of search during Black Friday week. Notably, Meta, with it’s range of wearables, stands out for a +3.1% increase in visibility.

Apple’s Share of Search jumped from 10.1% to 16.4%, a gain of 6.4%. At the same time, Fitbit’s share dropped nearly 11%, the steepest decline in the entire electronics category. Meanwhile, Samsung and HP also lost on visibility this Black Friday in the UK.

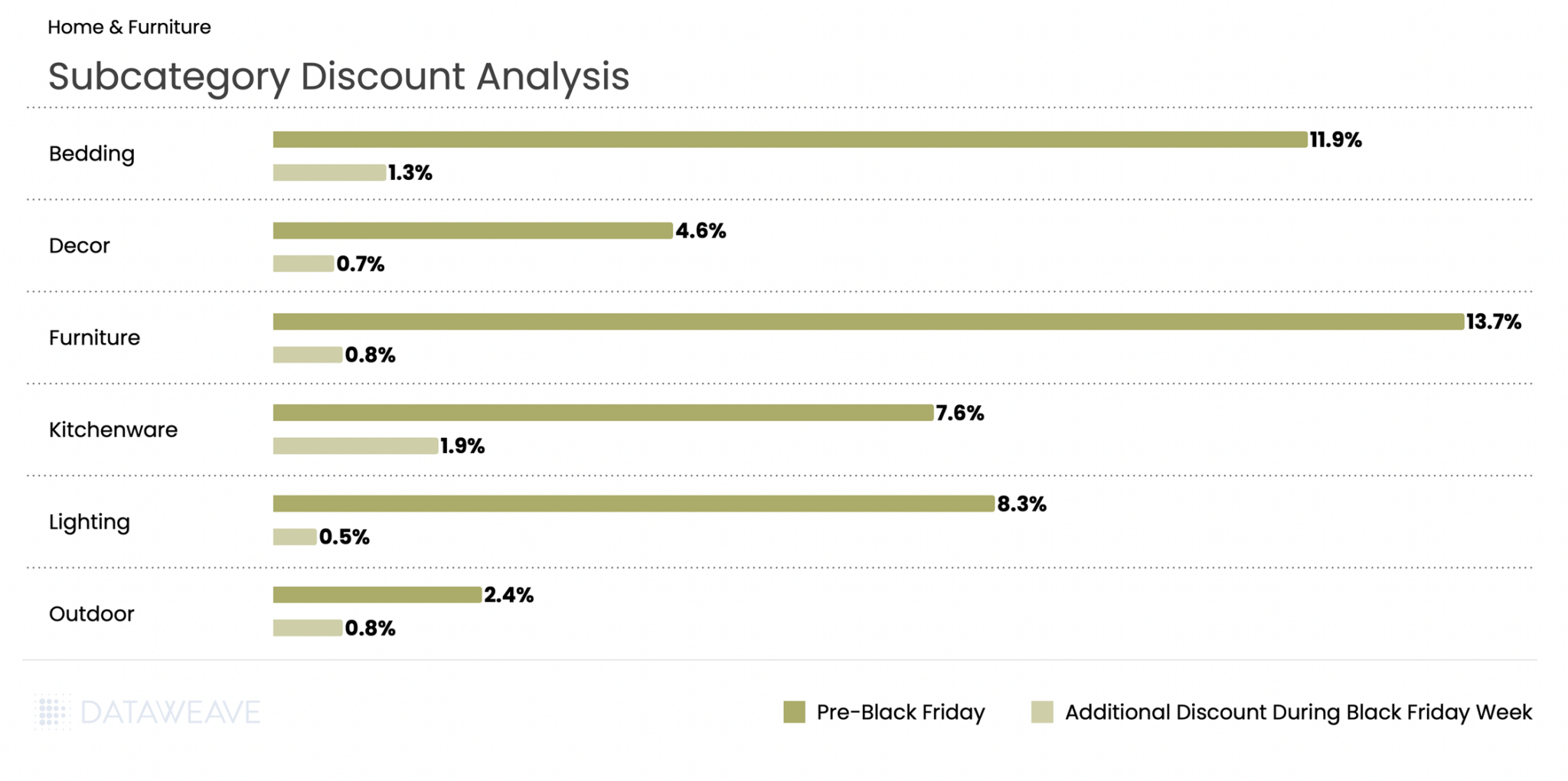

Home & Furniture

The Home & Furniture category continues to attract UK consumers during Black Friday, though with a more measured discounting approach compared to other categories. Our analysis of 16,487 SKUs shows how discounts were distributed across subcategories.

Subcategory Discount Analysis

Home & Furniture saw Pre-Black Friday discounts averaging 9.1%, with Black Friday Week adding just 1% on average, the lowest additional discount among all categories. Furniture led pre-sale discounts at 13.7%, followed by Bedding at 11.9%. This suggests retailers aggressively promoted larger home goods early in the season to capture deal-seekers.

During Black Friday Week, Kitchenware saw the highest additional discount at 1.9%, making it attractive for holiday cooking and gifting needs. Conversely, Lighting saw minimal additional promotion at just 0.5%.

Share of Search: Brand Visibility Trends

Made.com, the contemporary furniture brand, saw visibility surge during Black Friday with an impressive 8.9% increase. Similarly, emerging mattress brand Vesgantti gained 5.4%. Rug specialist Gooch Oriental also made significant gains with a 4.9% increase.

On the flip side, British heritage brands faced challenges. Both Laura Ashley and Julian Bowen saw share of search drop 2.2%. Premium mattress maker Vispring also declined 2.1%, while French cookware brand Le Creuset fell 1.9%.

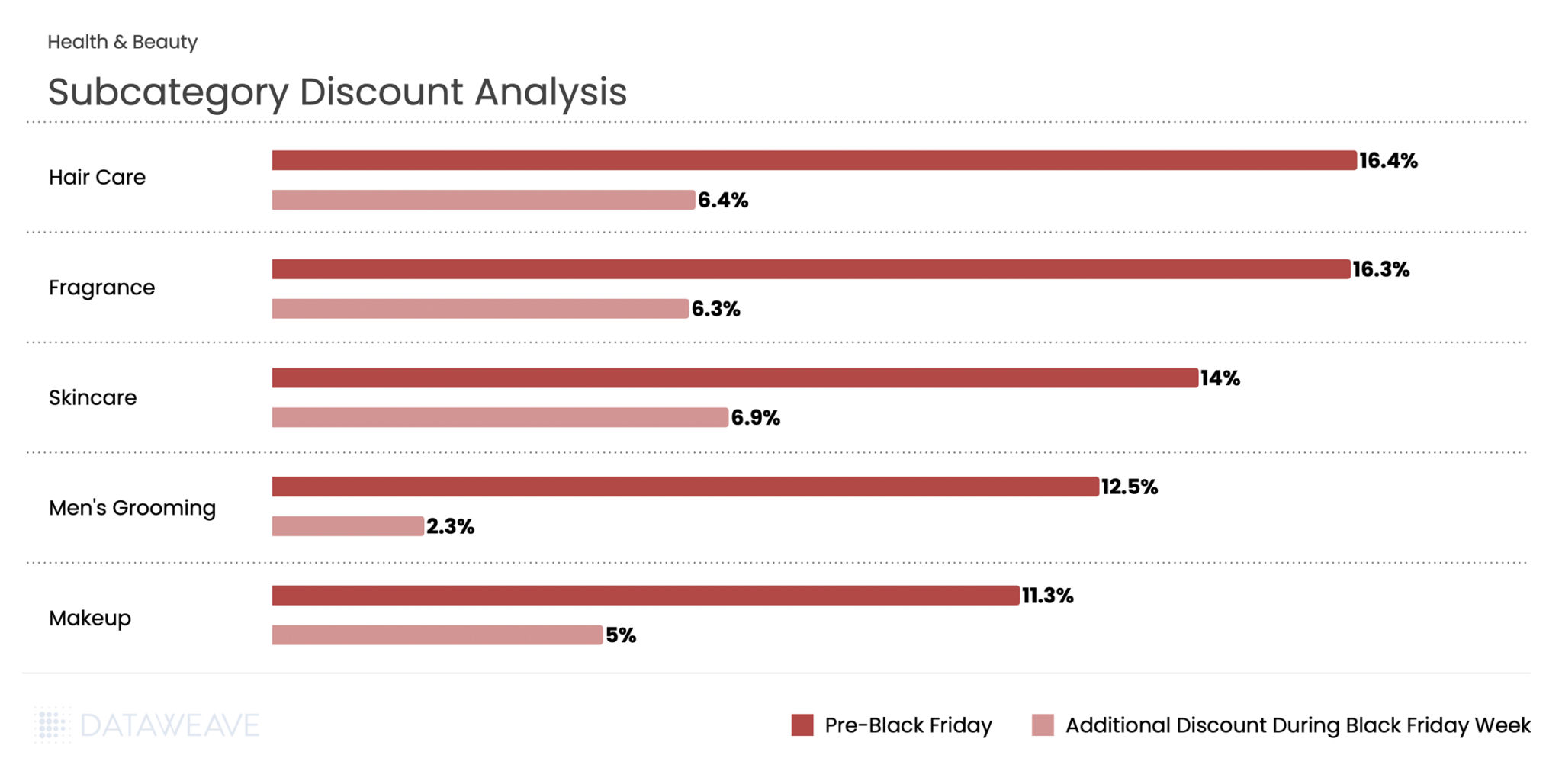

Health & Beauty

Health & Beauty has emerged as a growth engine during Black Friday in the UK. The beauty industry is projected to grow 5% annually through 2030 according to a McKinsey survey. The category continues to demonstrate resilience even as consumers show caution in other discretionary categories. Our analysis of 15,816 SKUs reveals fascinating subcategory-level insights and dramatic brand visibility shifts that highlight evolving consumer preferences in the beauty space.

Subcategory Discount Analysis

Health & Beauty presented a unique discounting pattern compared to other categories. Pre-Black Friday discounts averaged 14.4%, the second-highest among all categories. But Black Friday Week discounts were also robust at 6.1%, the highest additional discount increase.

Hair Care led both periods with 16.4% pre-sale discounts and an additional 6.4% during Black Friday Week. Skincare saw the highest Black Friday Week discount at 6.9%, suggesting retailers strategically saved their best skincare promotions for the main event when consumers are actively seeking holiday gift sets. Men’s Grooming stood apart with strong pre-sale discounts of 12.5% but more modest Black Friday Week additions of just 2.3%.

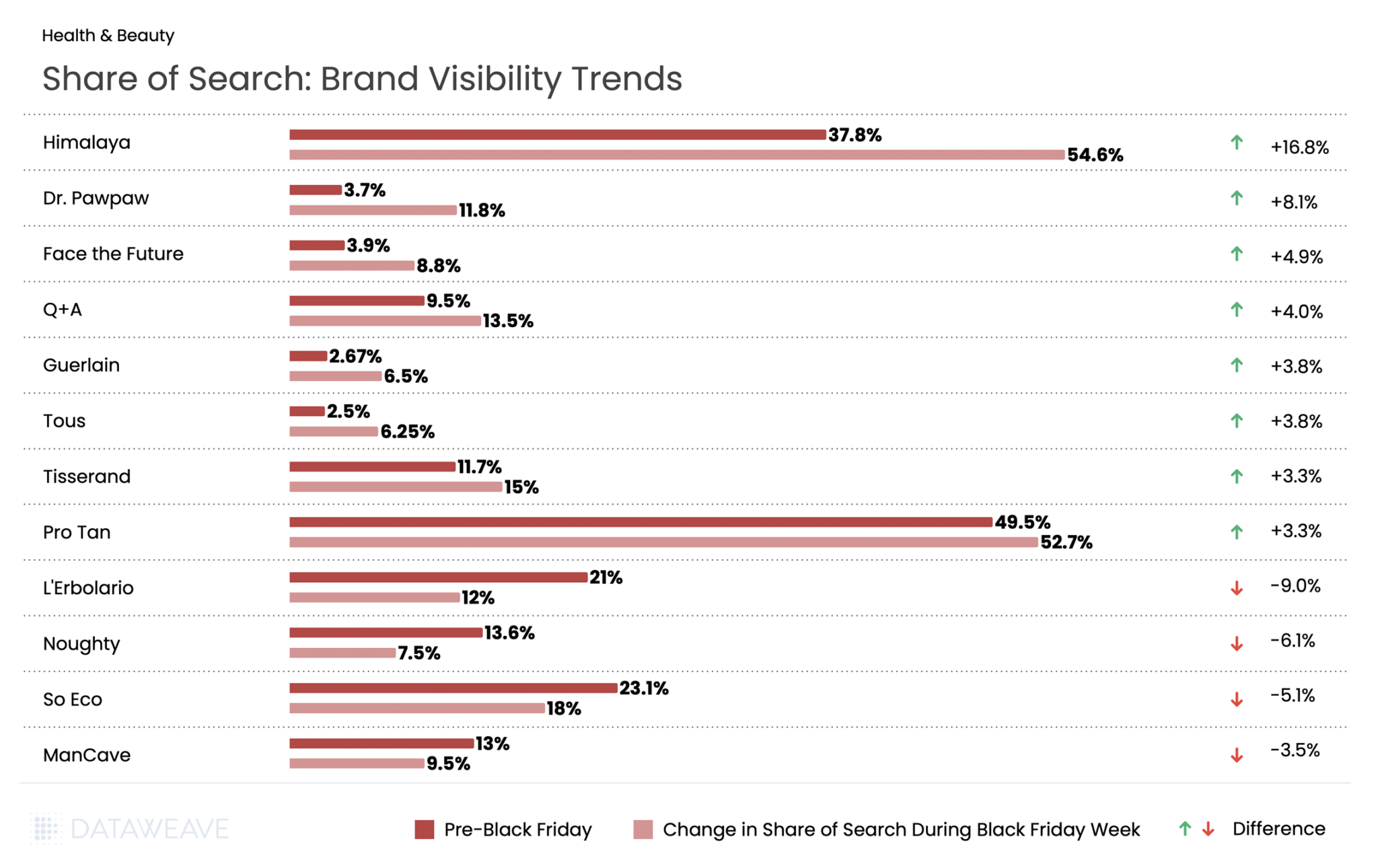

Share of Search: Brand Visibility Trends

The UK Beauty category saw some of the most dramatic Share of Search swings in our analysis.

Himalaya, the Ayurvedic skincare brand, dominated the category with a stunning 16.8% gain. British cult favorite Dr. Pawpaw exploded from 3.7% to 11.8%, a gain that reflects the brand’s growing mainstream appeal. Face the Future, the skincare specialist, also gained significant ground with a 4.9% increase.

Budget-friendly British brand Q+A continued its momentum, rising 4%, while prestige names like Guerlain and Tous each gained 3.8%.

Italian natural beauty brand L’Erbolario saw the steepest decline, with visibility dropping by 9%. Haircare brand Noughty fell 6.1%, and eco-beauty brand So Eco declined by 5.1%.

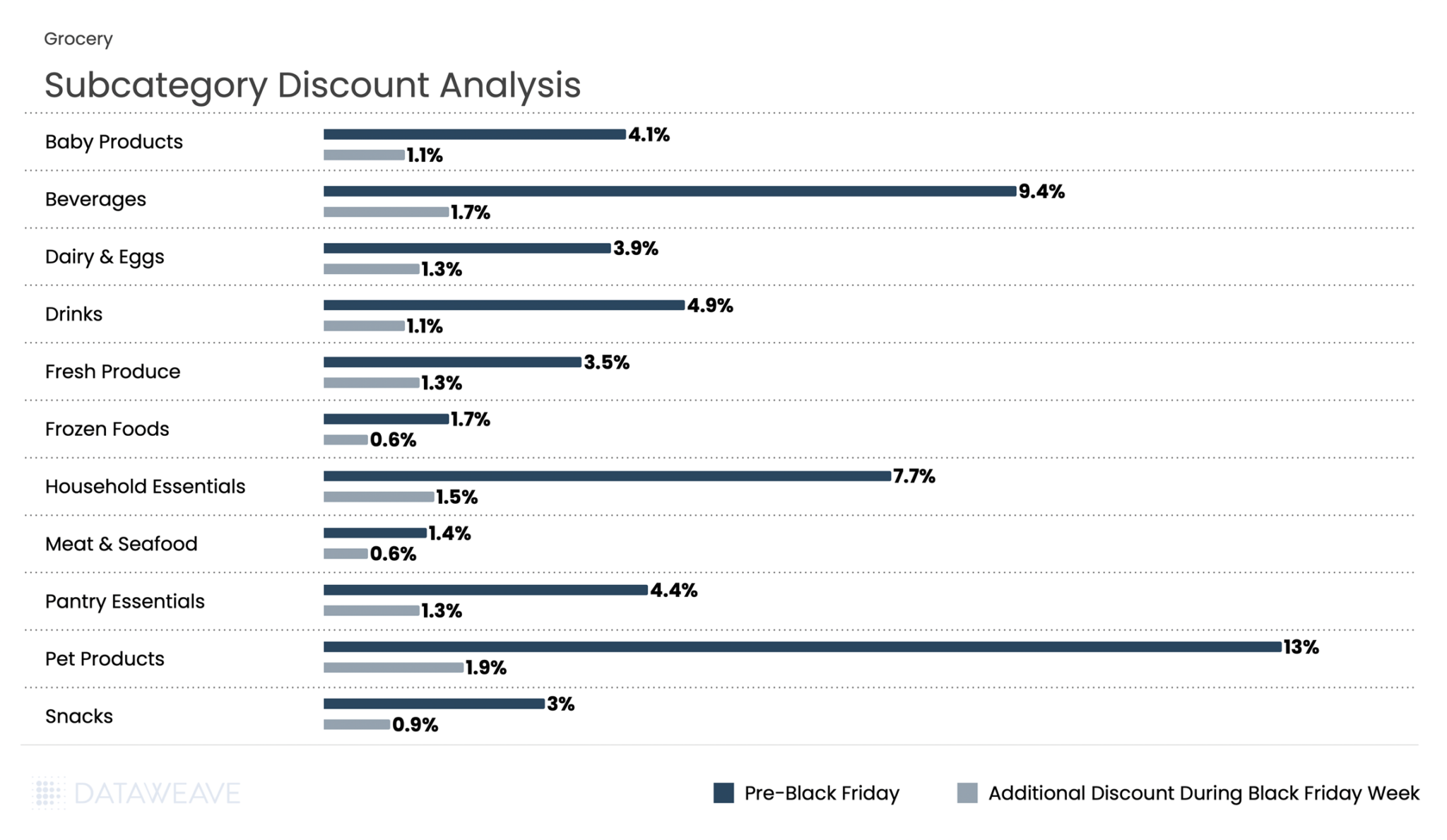

Grocery

While Grocery typically sees more modest discounts compared to discretionary categories, the sector remains a critical part of Black Friday shopping in the UK, particularly as consumers prepare for holiday entertaining and gifting. Our analysis of 11,979 SKUs shows how UK retailers approached promotions across essential and indulgent subcategories.

Subcategory Discount Analysis

Grocery had the lowest discounts across all categories, reflecting the already-thin margins in food retail. Pre-Black Friday discounts averaged just 5.7%, with Black Friday Week adding only 1.2%. Pet Products led pre-sale discounts at an impressive 13%, significantly outpacing other grocery subcategories.

Beverages and Household Essentials followed with 9.4% and 7.7% pre-sale discounts respectively, and maintained their lead during Black Friday Week with 1.7% and 1.5% additional discounts each. Fresh categories like Meat & Seafood (1.4% pre-sale, 0.6% Black Friday Week) and Frozen Foods (1.7% pre sale, 0.6% additional discounts during Black Friday week) saw minimal promotional activity, consistent with perishable inventory constraints and tight margins.

Share of Search: Brand Visibility Trends

Doritos led with a 7.3% surge in visibility. Pepsi delivered an equally impressive performance, rising from 3.6% pre Black Friday to 10.7% during Black Friday week. Fanta too saw 5.2% gain in share of search.

Conversely, Coca-Cola gained more modestly at 1.6%, while its Sprite brand actually declined 0.9%.

Apparel

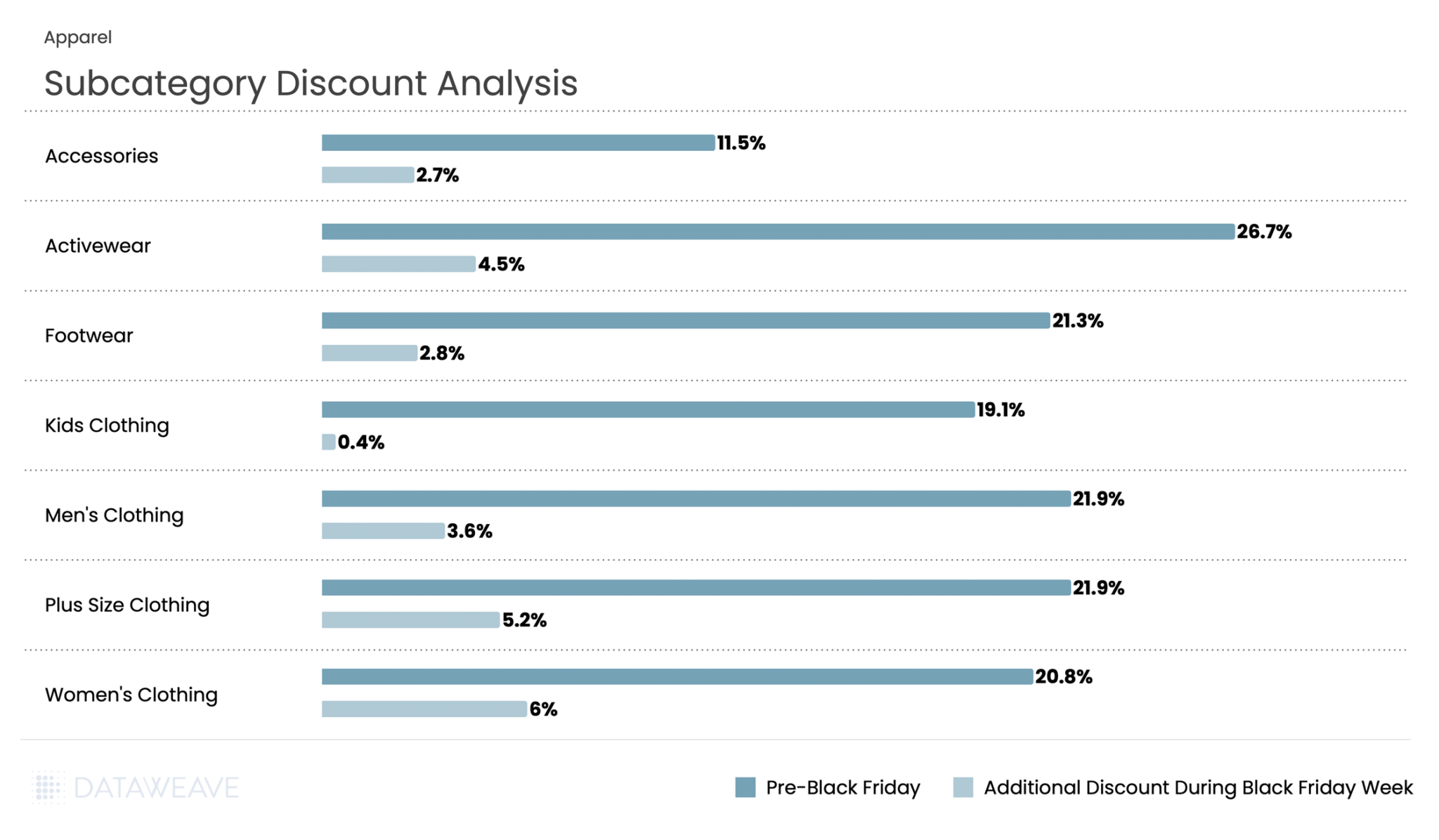

Apparel remains a Black Friday staple in the UK and is projected to deliver the strongest year-on-year growth of any UK retail segment this festive season. With clothing accounting for 39% of planned Black Friday purchases, the category represents one of the most hotly contested battlegrounds during the sales period.

Our analysis of 17,063 SKUs, the largest category in our study, reveals interesting patterns across fashion segments that demonstrate both the opportunities and competitive intensity in UK apparel retail.

Subcategory Discount Analysis

Apparel showed the strongest discounting activity throughout the BFCM period among all categories. Pre-Black Friday discounts averaged 17.2%, with Black Friday Week adding 3.5%, making it one of the most heavily promoted categories.

Activewear led pre-sale discounts at an impressive 26.7%, with an additional 4.5% discount during Black Friday week. Plus Size Clothing and Men’s Clothing tied for second place in pre-sale discounts at 21.9% each. Notably, Plus Size Clothing saw the highest Black Friday Week discount at 5.4%.

Women’s Clothing saw robust discounts throughout, with 20.8% pre-sale and an additional 6% during Black Friday Week (the highest additional discount in the category).

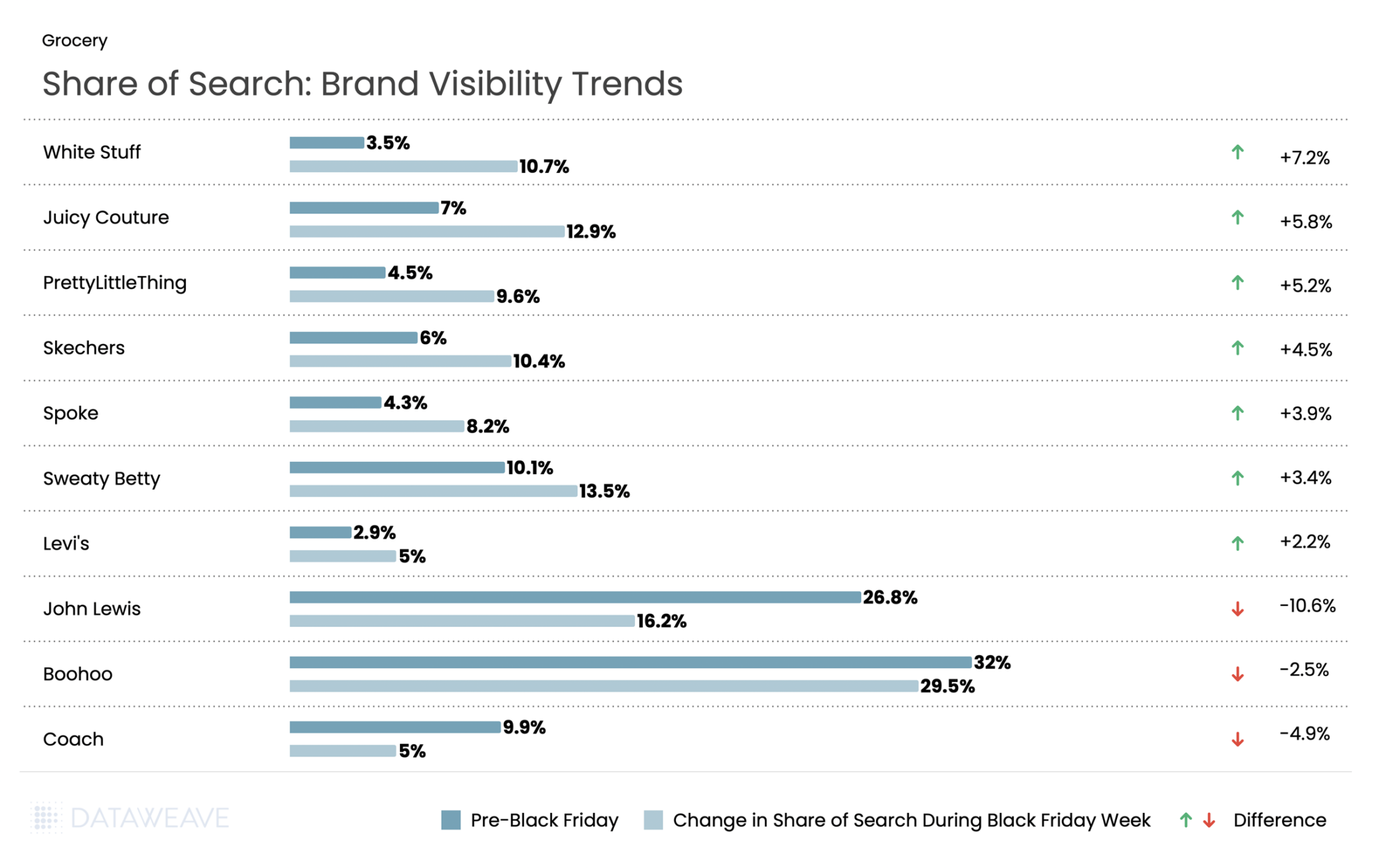

Share of Search: Brand Visibility Trends

White Stuff, the British lifestyle brand, saw a 7.2% surge in visibility during Black Friday. Y2K fashion made a statement as Juicy Couture jumped 5.8 %. Fast fashion player Pretty Little Thing gained in visibility by 5.2%. Comfort brands performed strongly, with Skechers gaining 4.5% and activewear specialist Sweaty Betty rising 3.4%. Even premium denim brand Levi’s gained ground, increasing share of search by 2.2%.

However, retail giants faced significant visibility challenges. John Lewis saw the steepest decline in the Apparel category, with share of search dropping by 10.6% during Black Friday week. Fast fashion giant Boohoo declined 2.5%. Premium accessory brand Coach’s share fell 4.9%.

The data suggests UK consumers gravitated toward distinctive brands with clear identities during Black Friday, whether heritage British labels, Y2K nostalgia, or comfort-focused specialists, rather than generalist retailers or fast fashion platforms.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

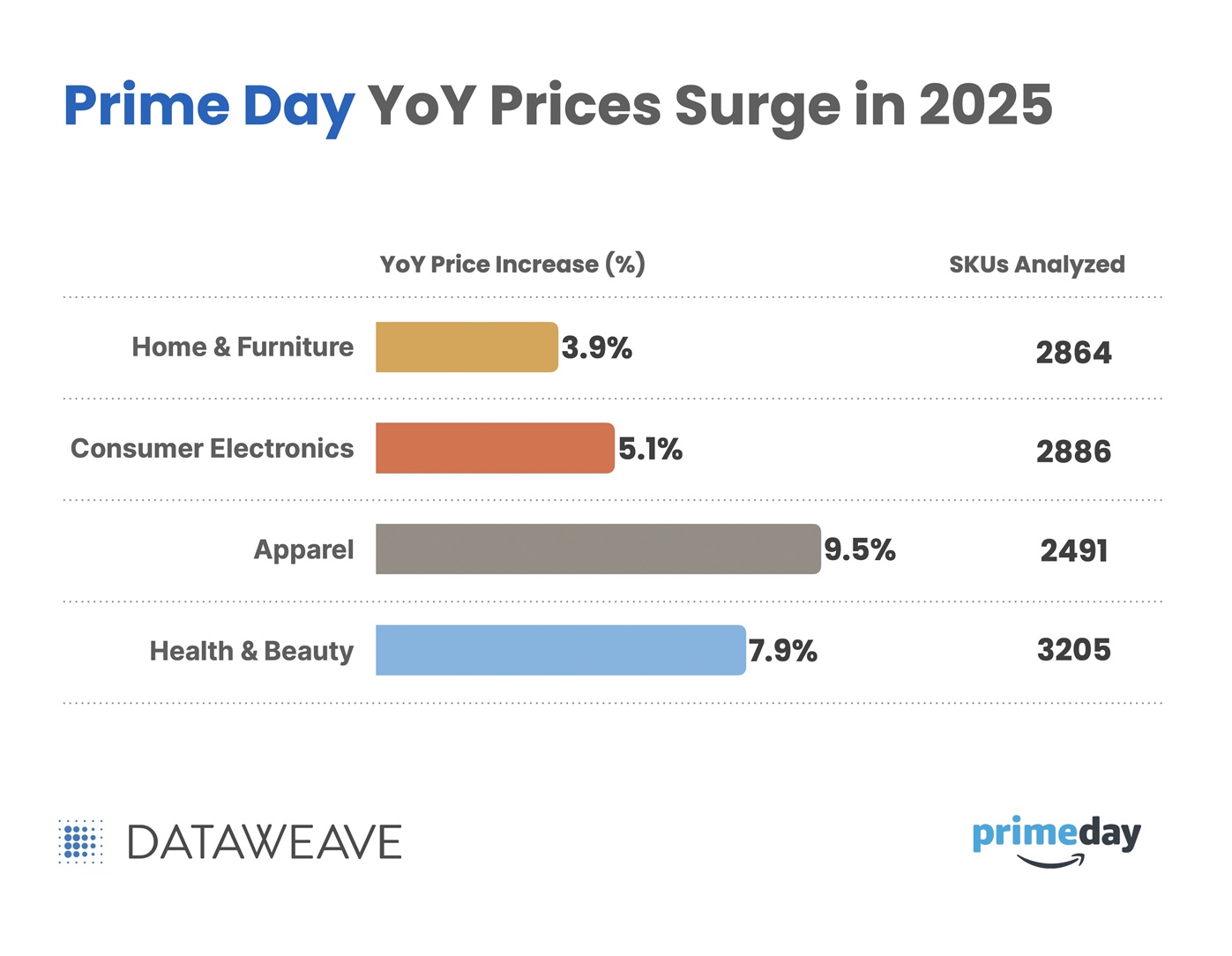

Amazon Prime Day 2025 generated a record-breaking $24.1 billion in US online sales during its extended four-day run (July 8–11, 2025). While the expanded format helped broaden participation, it also diluted the urgency and daily peaks that typically define Prime Day.

Beneath this record-setting performance lies a more complex reality. Persistent inflation, shifting consumer behavior, and rising pricing pressures created a retail environment very different from previous years, one where higher baseline prices often replaced the deep discounts shoppers expected.

To understand these dynamics, DataWeave analyzed pricing and visibility trends across 11,495 products using our proprietary AI platform. The study focused on four major categories – Consumer Electronics, Apparel, Home & Furniture, and Health & Beauty – comparing identical SKUs from Prime Day 2024 and 2025, and tracking changes in both organic and sponsored share of search for leading brands.

The results reveal clear year-over-year price increases: Apparel led with a 9.5% rise, followed by Health & Beauty (7.9%), Consumer Electronics (5.1%), and Home & Furniture (3.9%). In total, 47% of tracked products saw higher prices, indicating that this year’s record sales were achieved in an environment of elevated base pricing rather than deeper discounts.

Multiple converging forces shaped the retail landscape leading into Prime Day 2025, pushing baseline prices higher even before promotions began.

Supply Chain Pressures: Ongoing disruptions and elevated shipping and production costs continue to shape the cost structure across categories.

Trade Policy Factors: Recent tariff measures and trade regulations may be contributing to upward pricing trends in certain categories, particularly those with high import dependence such as electronics and home goods.

Labor and Operating Costs: Rising wages, transportation expenses, and general operating overhead are placing additional pressure on retailer margins and influencing pricing decisions.

Currency Fluctuations: Shifts in exchange rates continue to add variability to the cost of imported goods, especially in globally sourced categories like electronics and apparel.

These combined pressures created a pricing environment where brands had less room for deep discounting, shaping not just how products were priced, but also how aggressively they were promoted.

To better understand the impact, we compared Prime Day 2025 prices to those from Prime Day 2024 for the same SKUs across major categories. This year-over-year view highlights how elevated baseline prices, driven by the factors outlined above, shaped the shopping experience and promotional strategies.

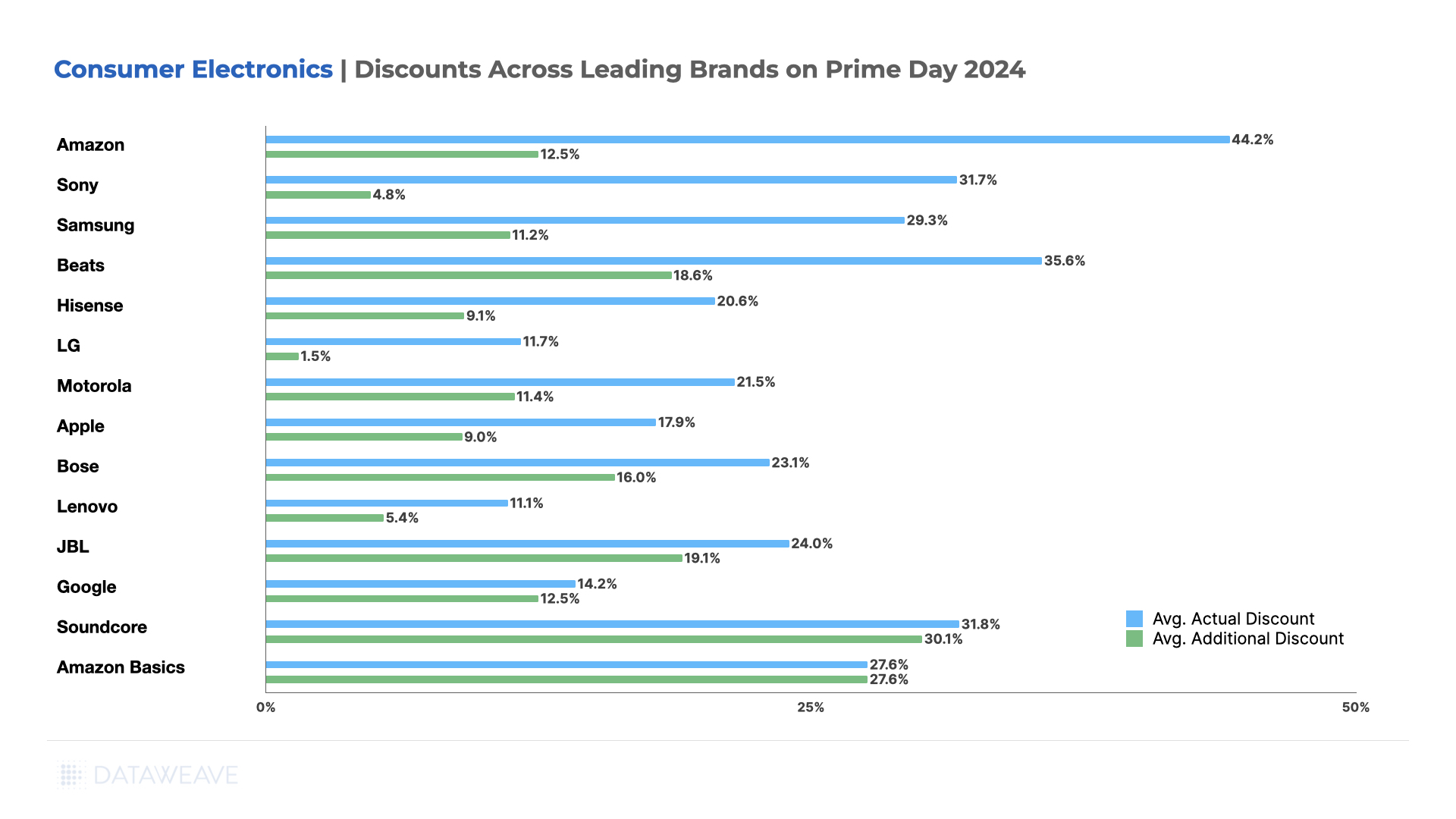

Consumer Electronics

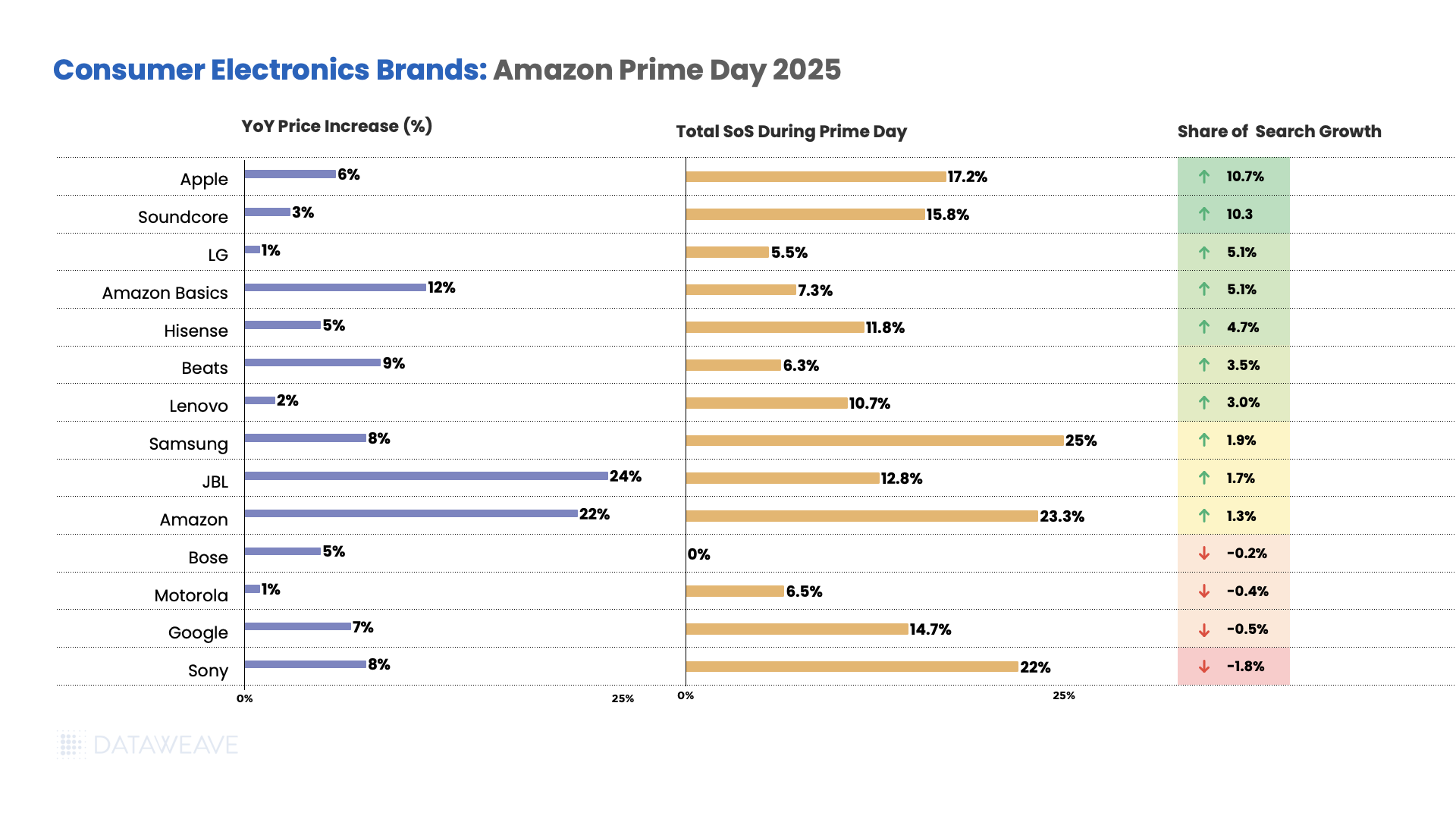

JBL prices increased 24% year-over-year, the highest among major electronics brands.

Amazon’s own brand saw prices increase by 22%.

Beats saw a significant 9% increase, while Sony and Samsung both experienced 8% price increases. Apple prices went up by 6%, and Google saw a 7% increase.

Meanwhile, other established brands like LG and Motorola maintained minimal increases at 1%, Lenovo at 2%, Soundcore at 3%, and Bose and Hisense both at 5%.

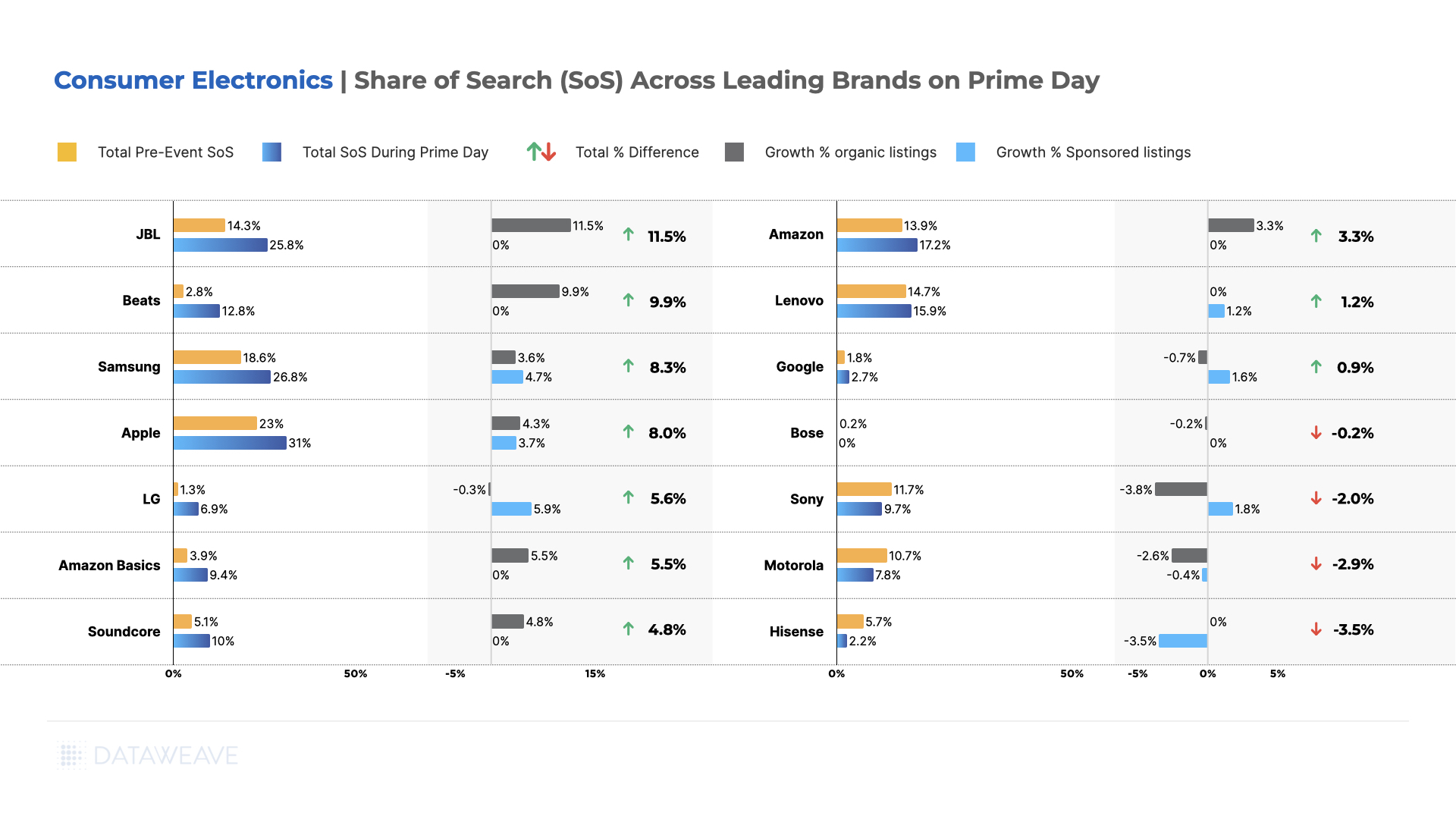

Apple dominated visibility gains, jumping to 17.2% share of search during Prime Day with a 10.7% growth, likely driven by promotional focus on premium devices. Soundcore also saw significant gains of 10.3%, reaching 15.8% share of search.

LG and Amazon Basics both achieved strong 5.1% growth. Hisense gained 4.7% share with 5% price increases. Samsung and Amazon maintained strong positions with modest gains of 1.9% and 1.3% respectively.

However, several brands lost ground, with Sony declining most significantly by 1.8% share despite its strong market position, followed by Google (-0.5%) and Motorola (-0.4%).

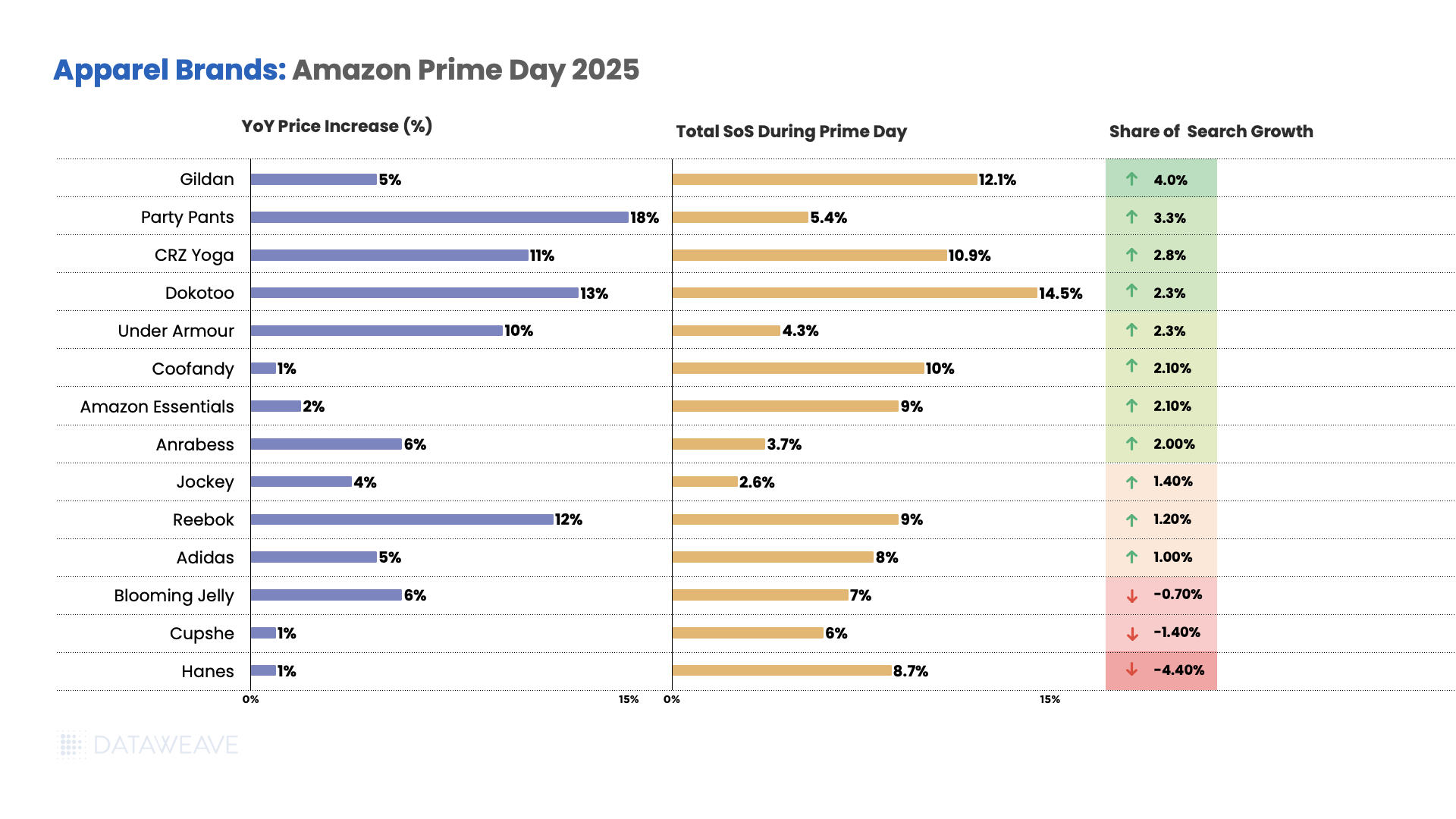

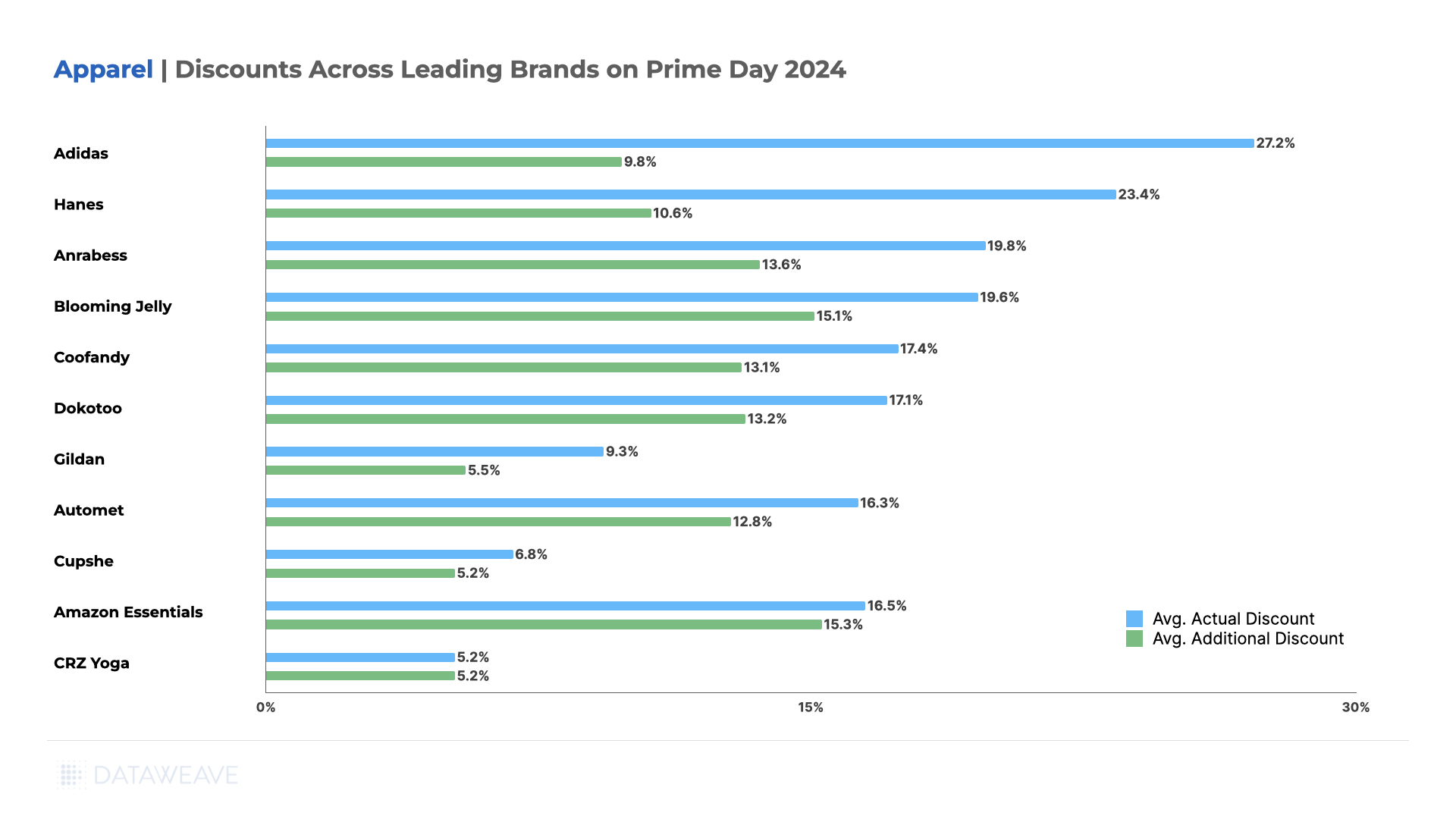

Apparel

Party Pants showed the highest price increases at 18% year-over-year, followed by casual wear brand Dokotoo at 13%.

Athleisure brand CRZ Yoga saw prices increasing by 11%, while Under Armour saw prices rise by 10%.

While Reebok experienced a significant 12% increase, Adidas saw 5% price increase.

Meanwhile, innerwear brands like Hanes and Cupshe saw minimal price increases at 1%, while Coofandy also saw minimal increases of 1%.

Amazon’s own Amazon Essentials maintained minimal price increases of 2%, and Jockey saw modest increases of 4%.

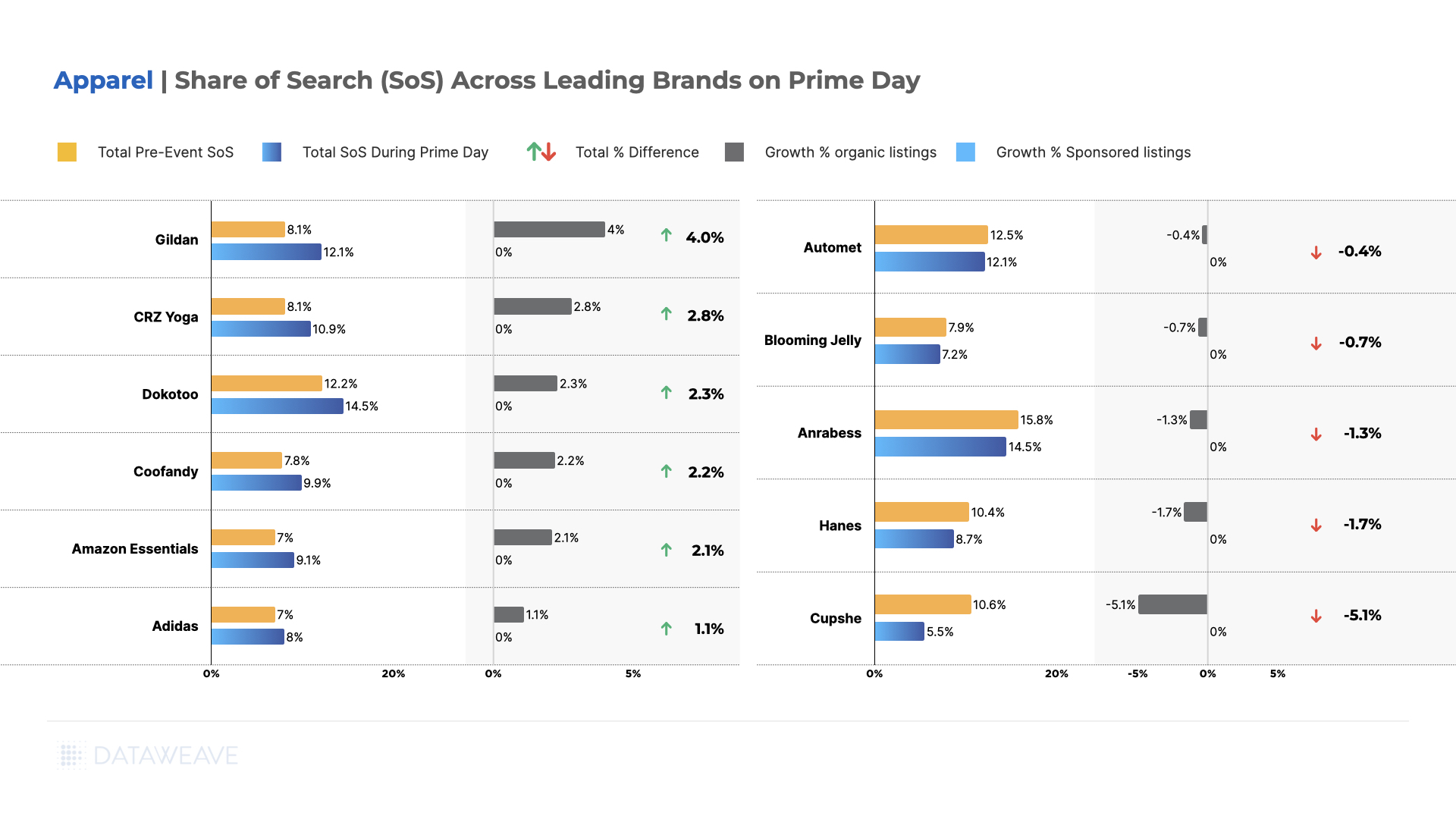

T-shirt brand Gildan led share of search gains with 4.0% growth along with a 5% price increase. Party Pants achieved 3.3% growth with 18% price increases, while CRZ Yoga gained 2.8% share and 11% price increases.

Amazon Essentials and Mens’ apparel brand Coofandy both improved share by 2.1%, with Amazon Essentials keeping price increases to just 2% and Coofandy at 1%. Under Armour gained 2.3% share with 10% price increase.

However, several brands lost ground, with Hanes declining significantly by 4.4% while keeping price increases to just 1%, followed by Cupshe (-1.4%) and Blooming Jelly (-0.7%).

Home & Furniture

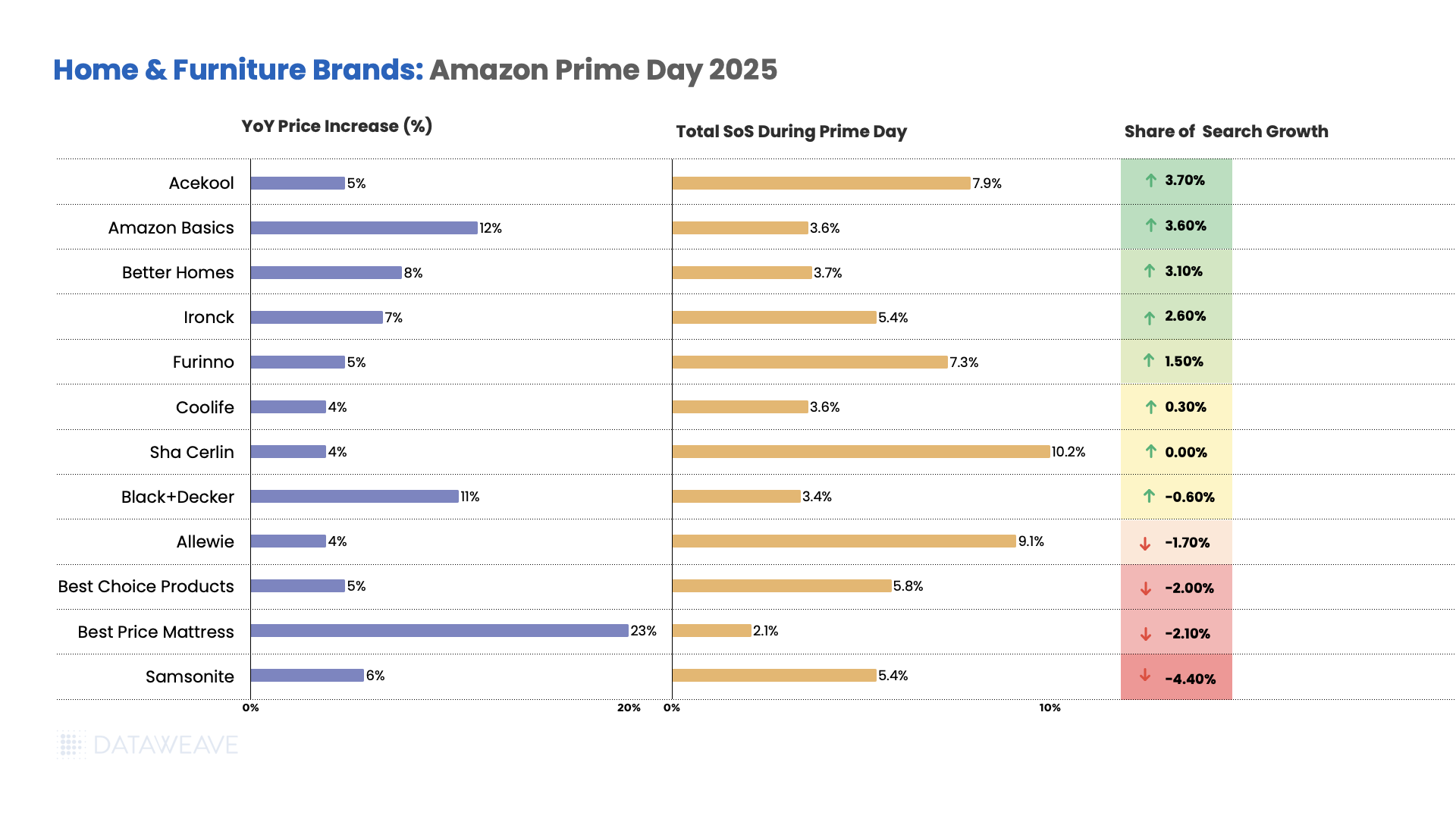

Mattress brand Best Price Mattress increased prices 23% year-over-year, the highest in the category.

Home Improvement and Appliances brand Black+Decker saw a pricing increase of 11%.

Better Homes saw an 8% increase, while most other brands saw price increases between 4-7%.

Appliance brand Acekool led visibility gains with 3.7% growth along with a 5% price increase. Amazon Basics improved significantly with a 3.6% share growth alongside its 12% price increases. Better Homes achieved 3.1% gains with 8% price increases.

Ironck gained 2.6% share with 7% price increases, and furniture brand Furinno improved by 1.5% with 5% price increases. However, several brands lost ground, with Samsonite declining most significantly by 4.4%, Best Price Mattress lost 2.1% share with its massive 23% price increase, and Allewie declined by 1.7% with 4% price increases.

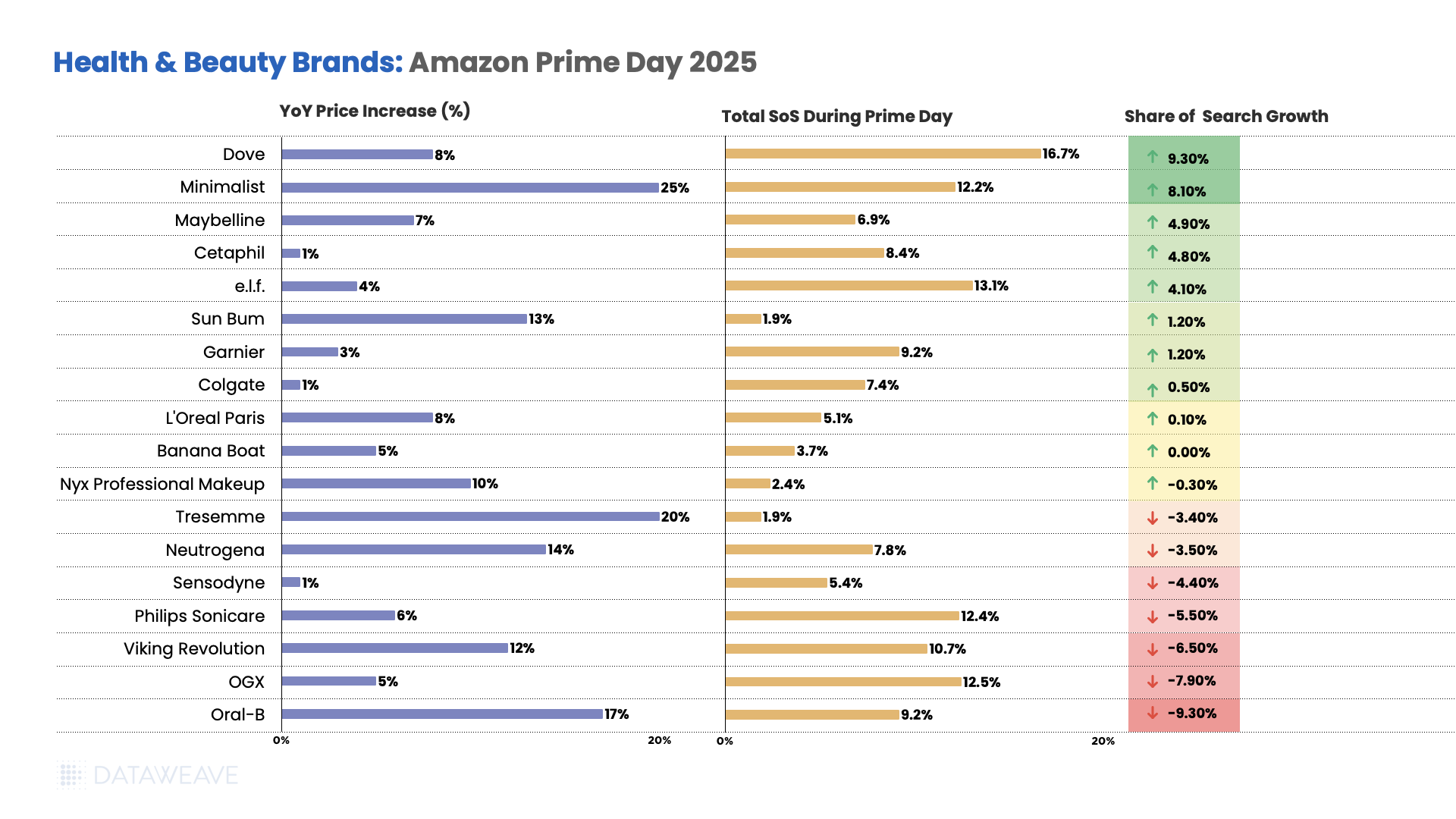

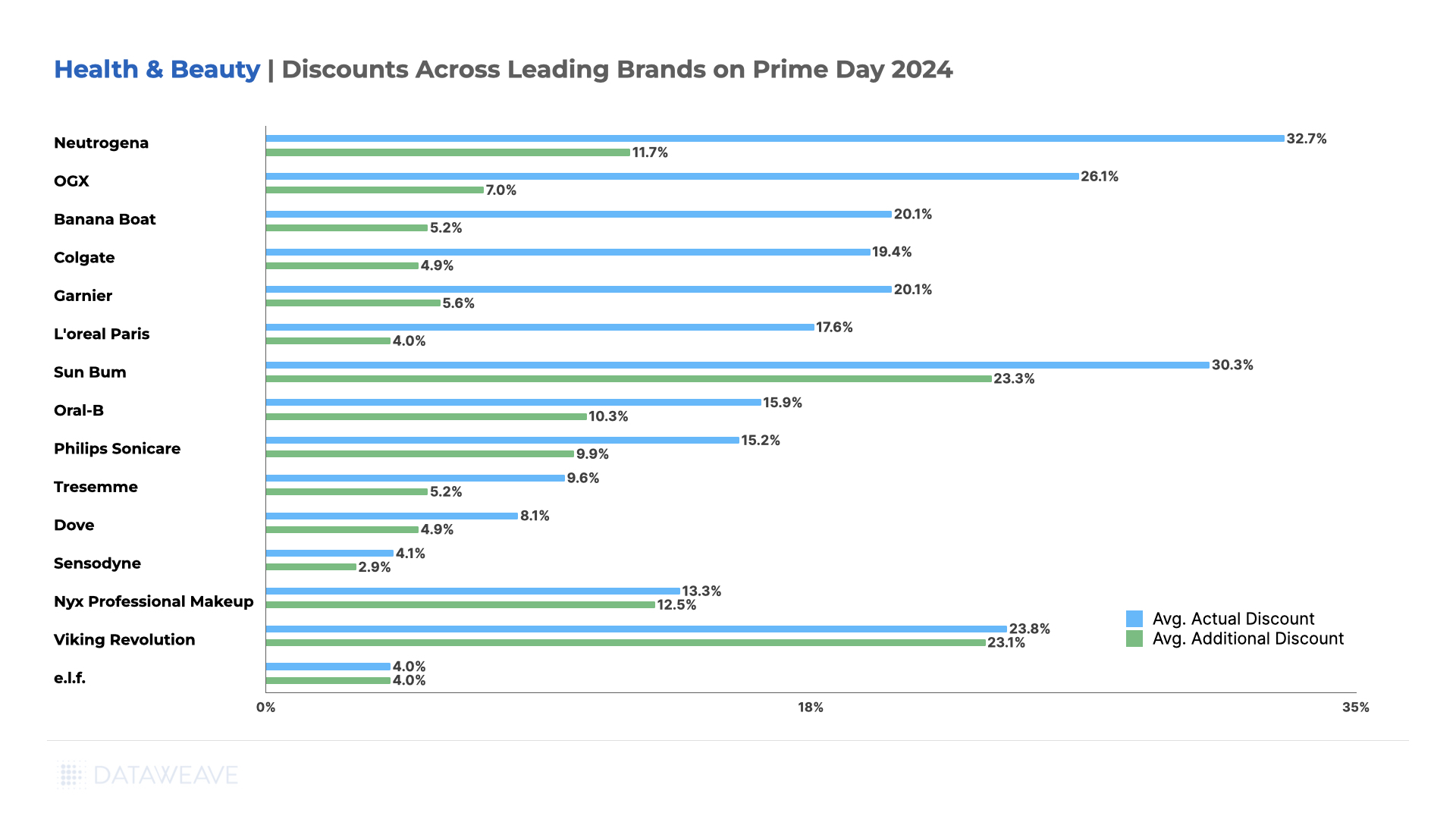

Minimalist saw prices increase 25% year-over-year, the highest in the category, followed by Tresemme at 20% and Oral-B at 17%.

Neutrogena increased pricing by 14%, while Sun Bum rose 13% and Viking Revolution 12%.

Nyx Professional Makeup saw price increases of 10%, Dove and L’Oréal Paris both at 8%, and Maybelline at 7%.

Value-positioned brands saw modest price increases, with Philips Sonicare (6%), OGX and Banana Boat (both 5%), e.l.f. (4%), and Garnier (3%).

Notably, Cetaphil, Colgate, and Sensodyne all kept increases to just 1%.

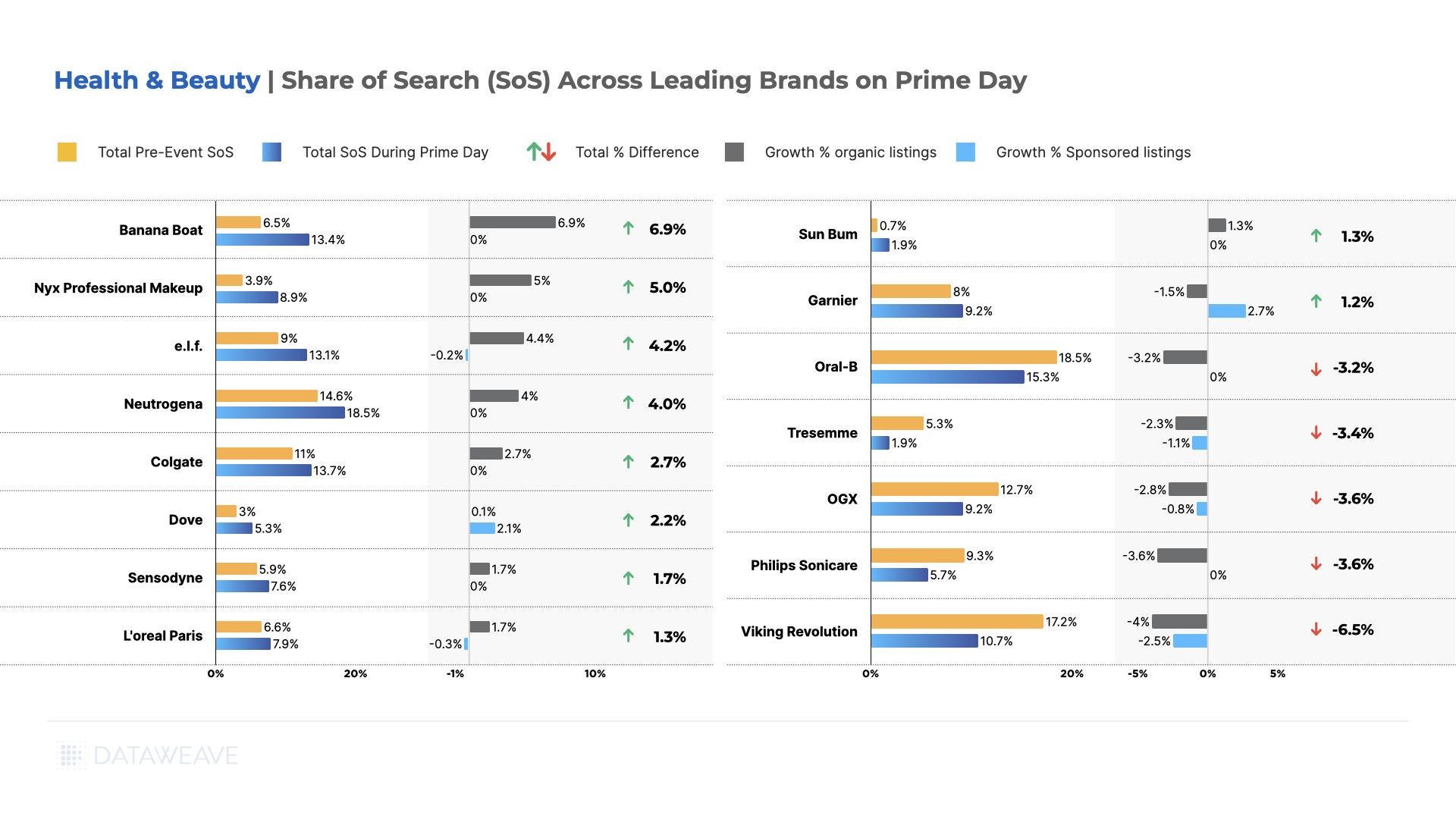

Dove led visibility gains with 9.3% growth along with 8% price increases. Minimalist achieved remarkable 8.1% growth even with the category’s highest 25% price increases, and Maybelline gained 4.9% share with 7% price increases.

Cetaphil improved by 4.8% with minimal 1% price increases, while e.l.f. gained 4.1% share with 4% price increases. However, several established brands lost share, with Oral-B declining most significantly by 9.3% along with 17% price increases, followed by OGX (-7.9%) with 5% price increases, Viking Revolution (-6.5%) with 12% increases, and Philips Sonicare (-5.5%) with 6% price increases.

In Conclusion

Prime Day 2025 underscores the shifting realities of retail, where persistent pricing pressures, evolving consumer behavior, and complex market forces are redefining how promotions are planned and executed. In this environment, success hinges on having the right intelligence at the right time, empowering brands to target promotions strategically, protect margins, and maintain visibility in a crowded marketplace.

As competition intensifies, the ability to anticipate trends and respond with precision will separate market leaders from the rest. At DataWeave, we equip retailers and brands with the insights needed to navigate these changes and make data-backed decisions that drive sustainable growth.

Stay connected to our blog for ongoing analysis of pricing, promotion, and visibility trends or reach out to us today to learn more.

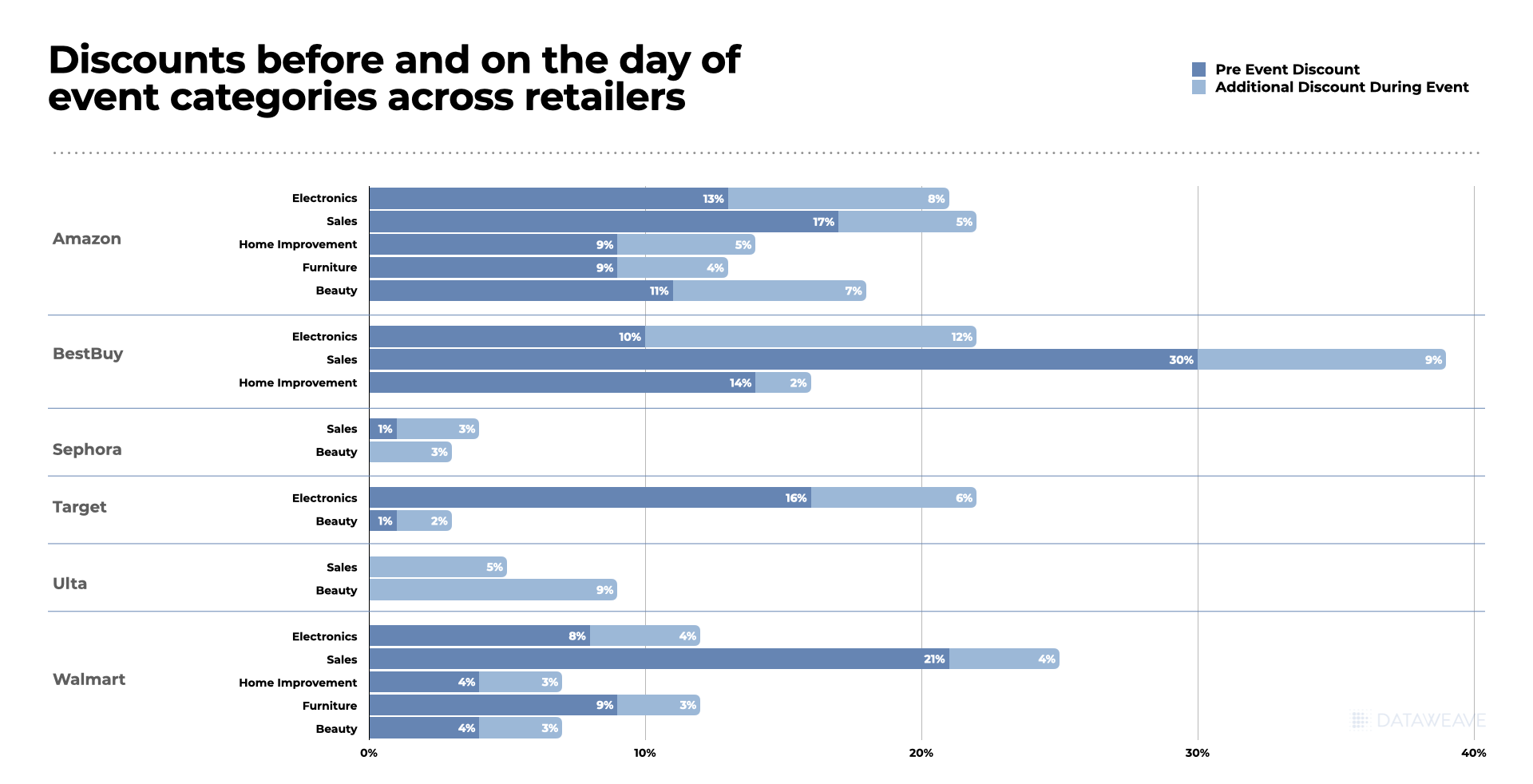

When it comes to shopping events, Black Friday stands out as one of the most anticipated dates for scoring deals. Typically occurring the day after Thanksgiving, the weekend kicks off the holiday shopping season with a frenzy of discounts. But Boxing Day, celebrated on December 26, is also well-known for its post-Christmas clearance sales.

This Black Friday, US eCommerce sales increased by a hefty 14.6% in 2024, according to Mastercard SpendingPulse. While Black Friday leads in overall revenue generation for retailers, Boxing Day presents unique opportunities for clearing post-holiday inventory.

For a consumer, which sale event is likely to offer the most attractive deals?

At DataWeave, we analyzed discounts across retailers and categories to uncover the answer.

Our Methodology

For this analysis, we tracked pricing data across major retailers for Black Friday and Boxing Day. To provide a comprehensive analysis of Black Friday pricing strategies, we explored a matched products dataset, comparing identical 14,000+ SKUs across retailers within key categories.

Categories included: Consumer Electronics, Home & Furniture, Apparel, Health & Beauty, Grocery

Retailers included: Amazon, Target, Walmart, Sephora, Ulta Beauty, Overstock, Home Depot, Best Buy, Saks Fifth Ave, Nordstrom, Macy’s, Bloomingdale’s, Neiman Marcus

Timeline: November 26 (Black Friday), December 26 (Boxing Day)

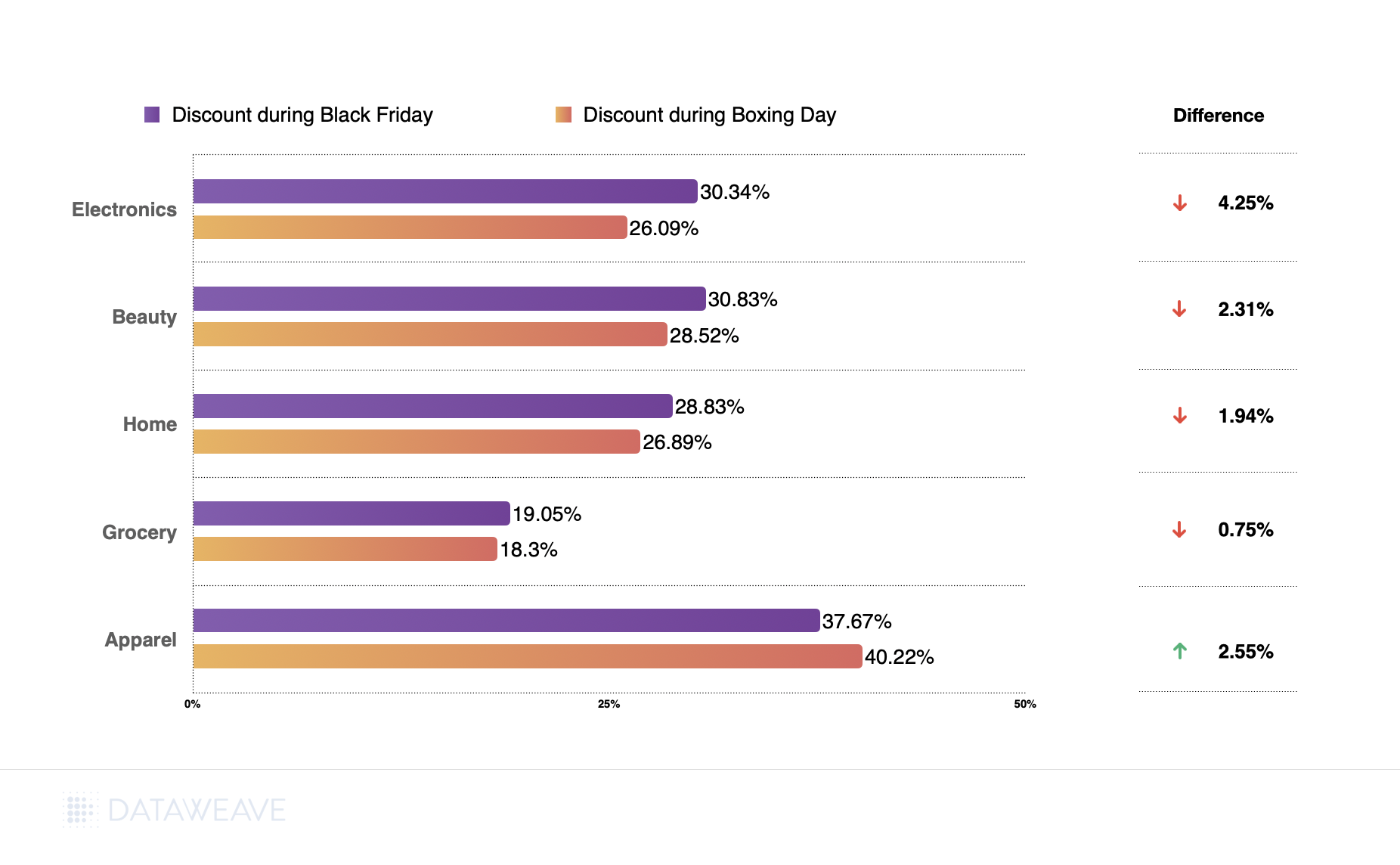

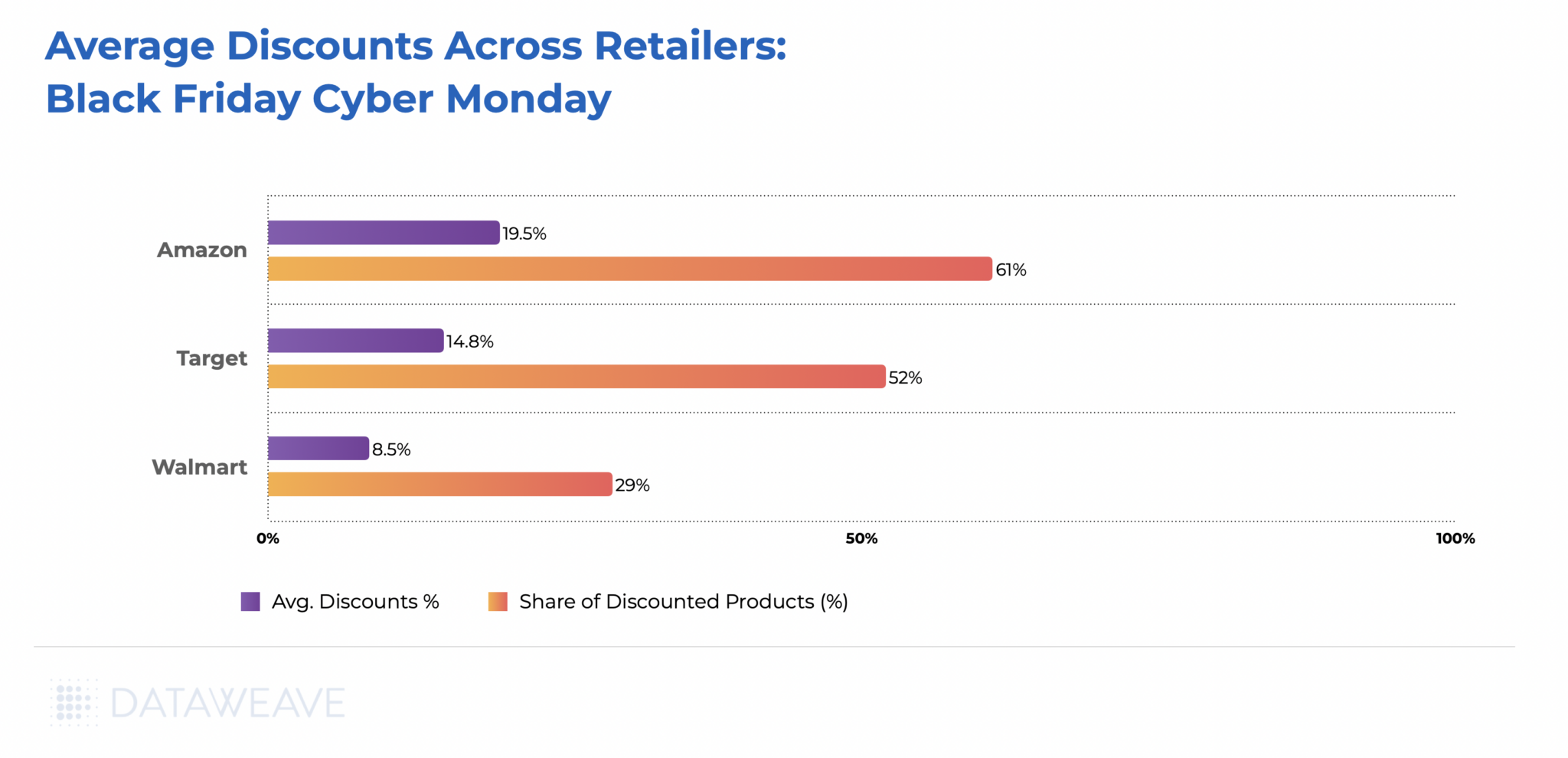

Average Discounts: Black Friday vs Boxing Day

Our analysis reveals that Black Friday generally offered steeper discounts across most categories, although Boxing Day wasn’t far behind. Here’s a breakdown:

While Black Friday led in most categories, Apparel saw a slight edge on Boxing Day, with discounts averaging 40.22% compared to 37.67% on Black Friday. Electronics, Beauty, and Home, however, remained more lucrative during Black Friday.

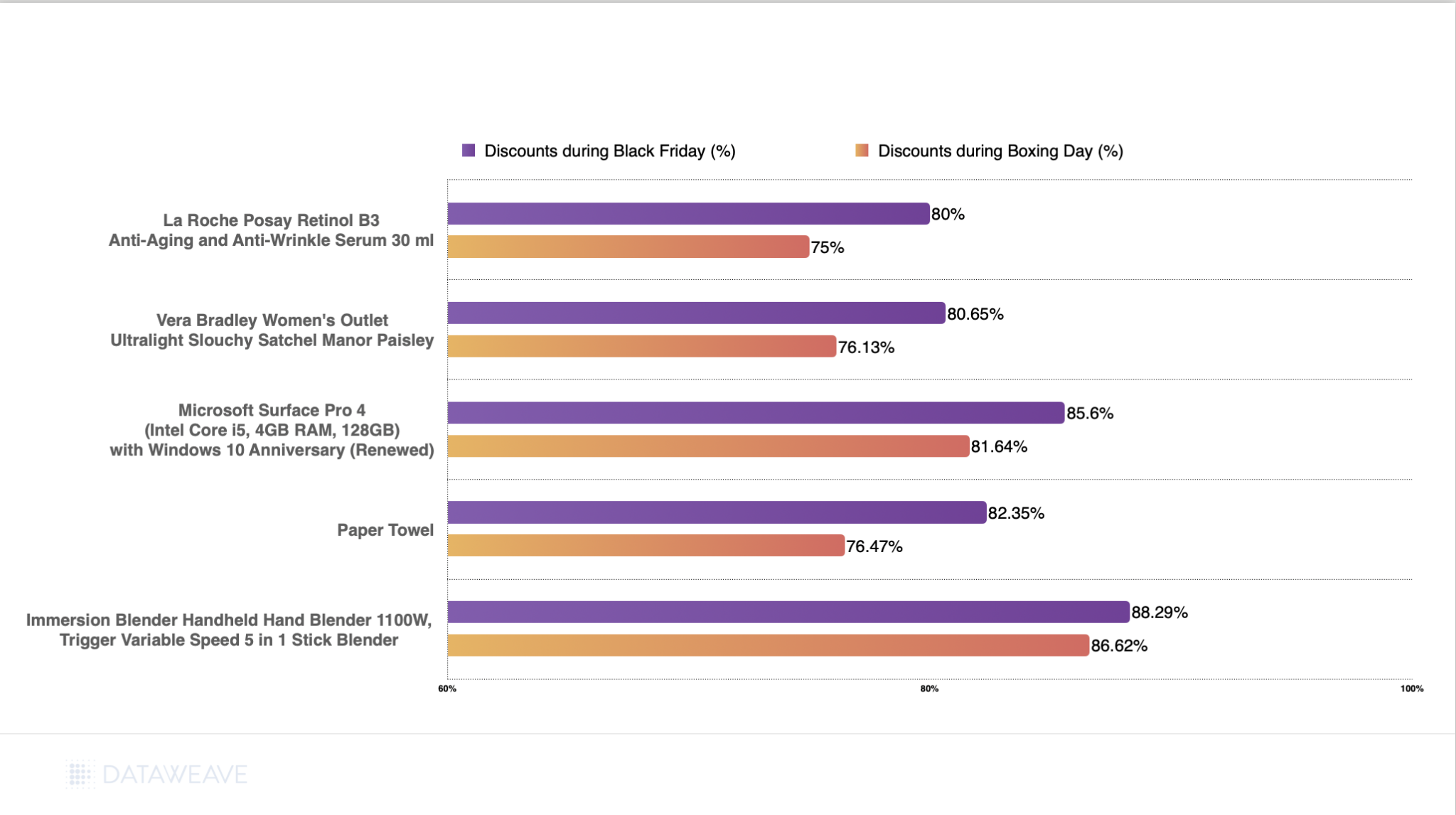

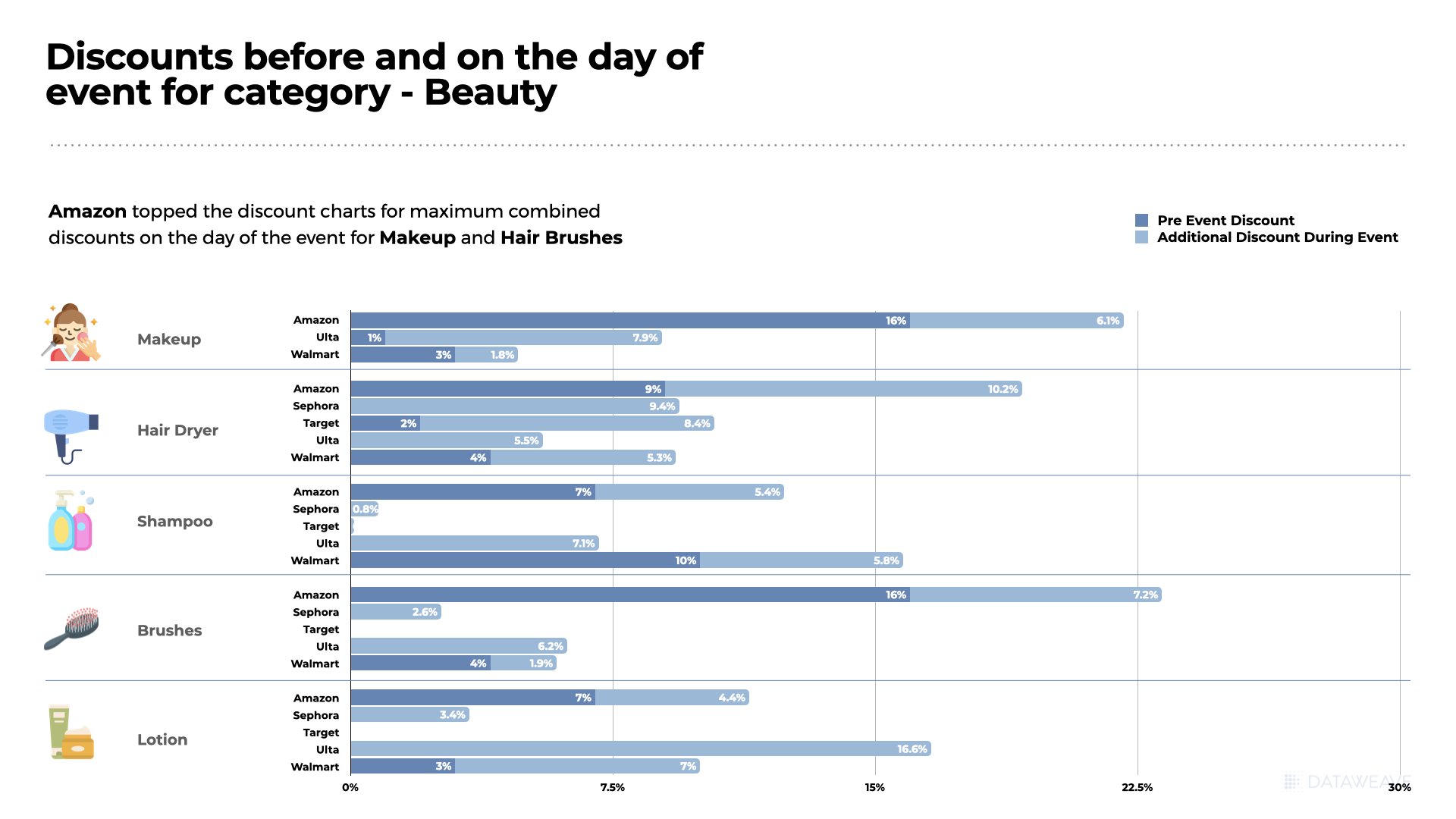

Top 5 Products Higher Discounts on Black Friday

Diving deeper into specific products, here are our top 5 picks offering better discounts during Black Friday.

Appliances like an Immersion blender set offering a discount of 88.29%, significantly higher than its Boxing Day offer of 86.62%.

High-end electronics like the Microsoft Surface Pro 4 also saw substantial markdowns at 84.60%.

In beauty and fashion, both La Roche Posay’s retinol serum and Vera Bradley’s satchel offered discounts above 80%.

Even everyday essentials like paper towels enjoyed generous discounts, with markdowns reaching 82.35% during Black Friday compared to 76.47% on Boxing Day.

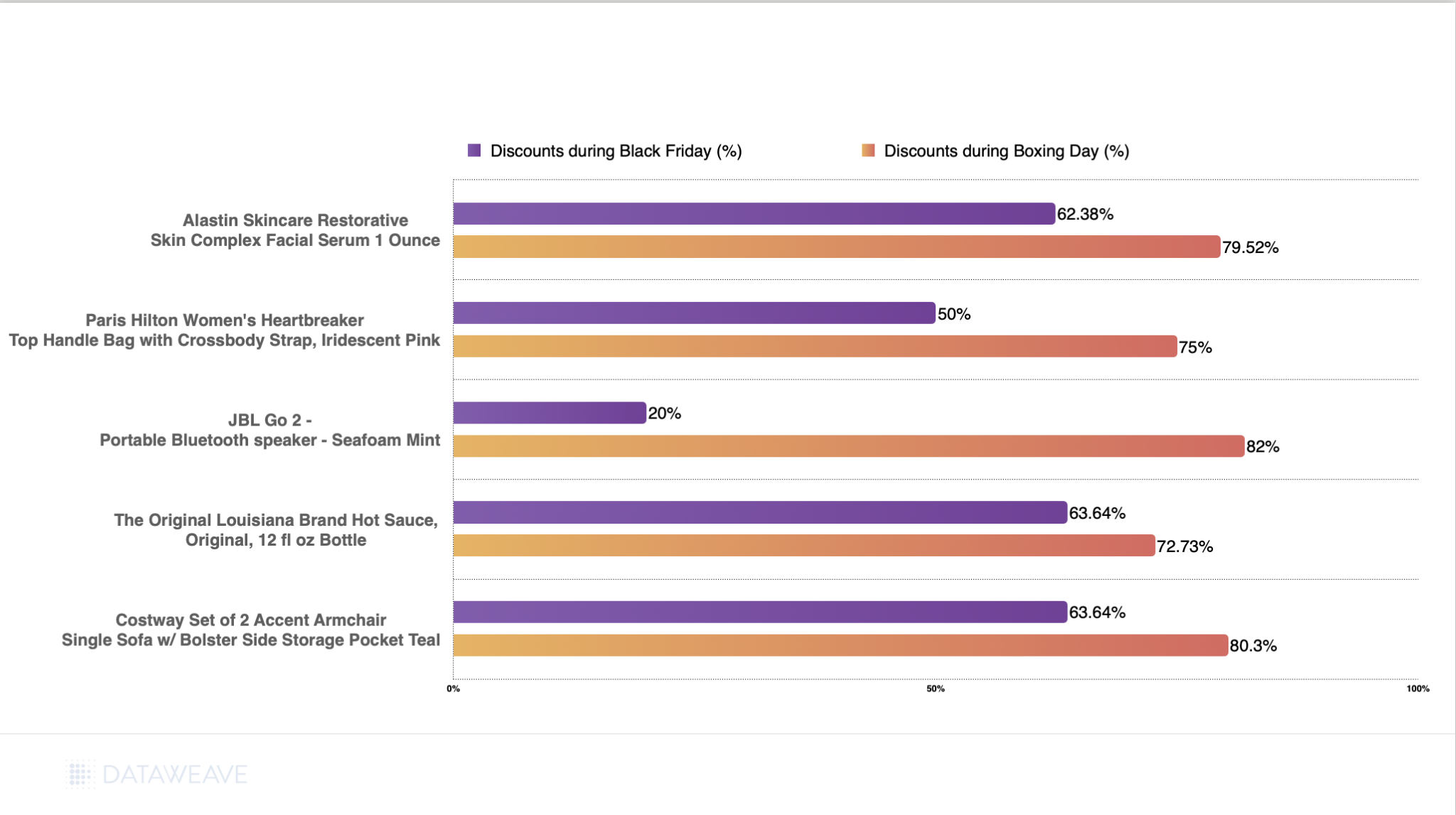

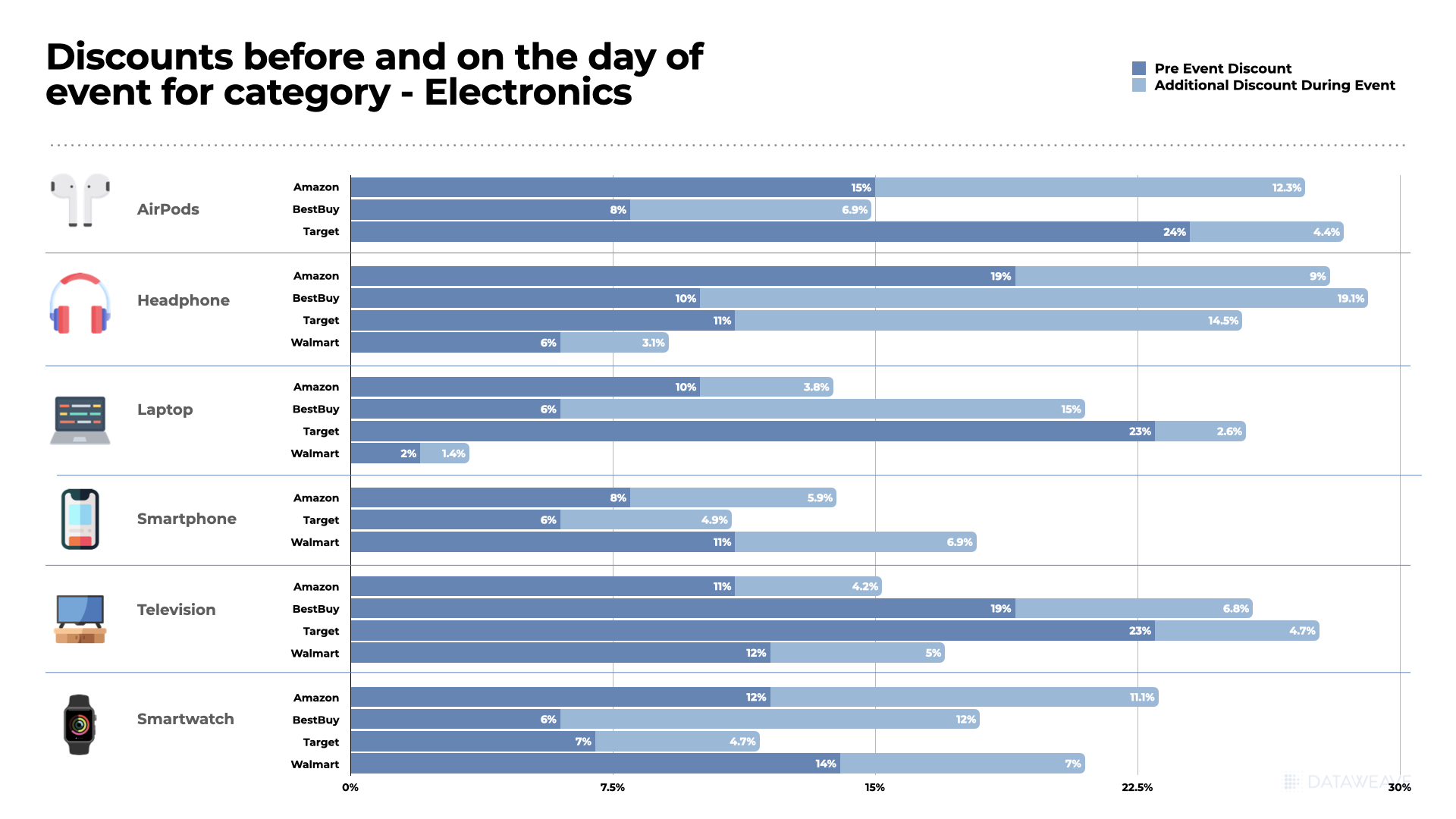

Top 5 Products With Higher Discounts on Boxing Day

Boxing Day revealed some remarkable deals across diverse categories, with certain products offering significantly better value than their Black Friday counterparts.

The JBL Go 2 portable speaker emerged as the standout, with an extraordinary 82% Boxing Day discount compared to just 20% on Black Friday—a dramatic 62% difference.

Home furnishings showed strong Boxing Day performance, with the Costway accent armchair set reaching 80.30% off.

In Conclusion

Black Friday reigns supreme in driving early holiday sales, offering deeper discounts and drawing larger crowds. However, Boxing Day remains critical for retailers to offload surplus inventory and attract post-holiday shoppers.

By combining insights from both events, retailers can refine their strategies to maximize revenue and enhance customer satisfaction. For shoppers, the decision comes down to timing—shop early for better deals or wait to capitalize on clearance markdowns. The products and categories with more attractive offers tend to vary between these two sale events. Hence, as a shopper, it’s a good idea to keep track of prices all through the holiday season to take advantage of the best deals.

For a deeper dive into the world of competitive pricing intelligence and to explore how our solutions can benefit apparel retailers and brands, reach out to us today!

As the holiday shopping season kicked off, savvy shoppers embraced the spirit of the season, drawn by enticing deals. The apparel category is forecasted as the second highest earning category (Source: Statista), expected to generate revenues up to $43.9 billion, closely following consumer electronics. To understand the pricing strategies of top retailers amidst the sale season, DataWeave analyzed the pricing trends for the Apparel category this Black Friday.

We leveraged our AI-powered data platform to analyze the discounting across key retailers. Our analysis focused on the Apparel category, examining how Amazon, Walmart, Target, Saks Fifth Avenue, Nordstrom, Bloomingdales, Neiman Marcus and Macy’s differentiated themselves through their discounts.

For this analysis, we tracked the average discounts of apparel products among leading US retailers during the Thanksgiving weekend sale, including Black Friday. Our sample was chosen to encompass the top 500 ranked products in each product subcategory across during the sale.

Subcategories reported on: Footwear, Kid’s Clothing, Men’s Clothing, Women’s Clothing, Activewear, Plus Size Clothing, Accessories

Timeline of analysis: 10 to 29 November 2024

We focused on the top 500 products ranked for each search keyword on each retail site, using targeted terms aligned with categories like “athleisure” and “plus size clothing”. Our methodology distinguished between standard discounts and Black Friday-specific ‘additional discounts’ or price reductions during the sale compared to the week before, to reveal true consumer value.

Key Findings

This year’s fashion discounts were unprecedented. Let’s take a look.

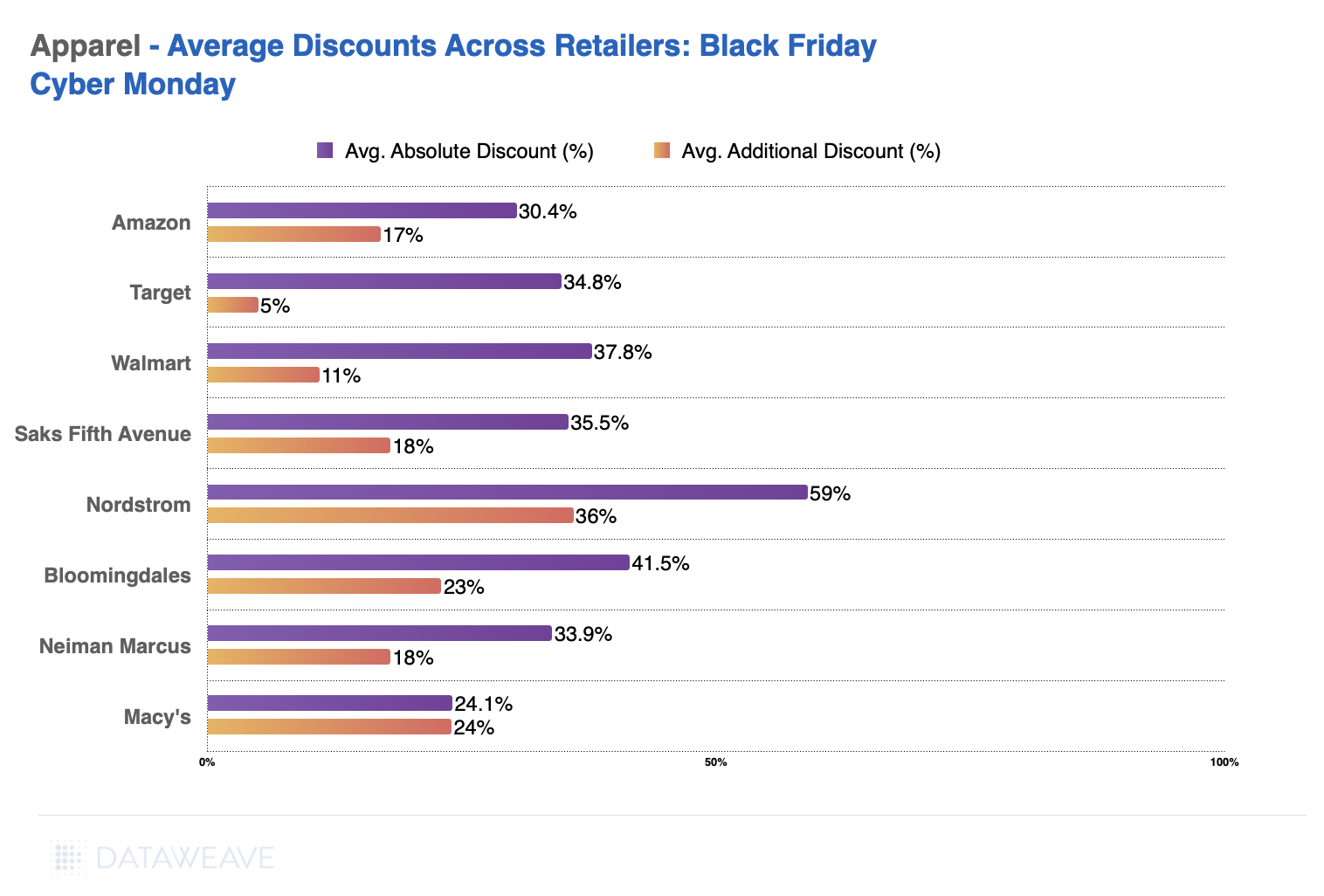

Retailer Level Insights

Nordstrom leads with the highest average absolute discount at 59%, followed by Saks Fifth Avenue at 35.5% and Bloomingdale’s at 41.5%. Macy’s shows the lowest average discount at 24.1%, while Amazon has an average discount of 30.4%.

Amazon ranks lower in both average absolute and additional discounts compared to competitors, indicating a more conservative discounting strategy.

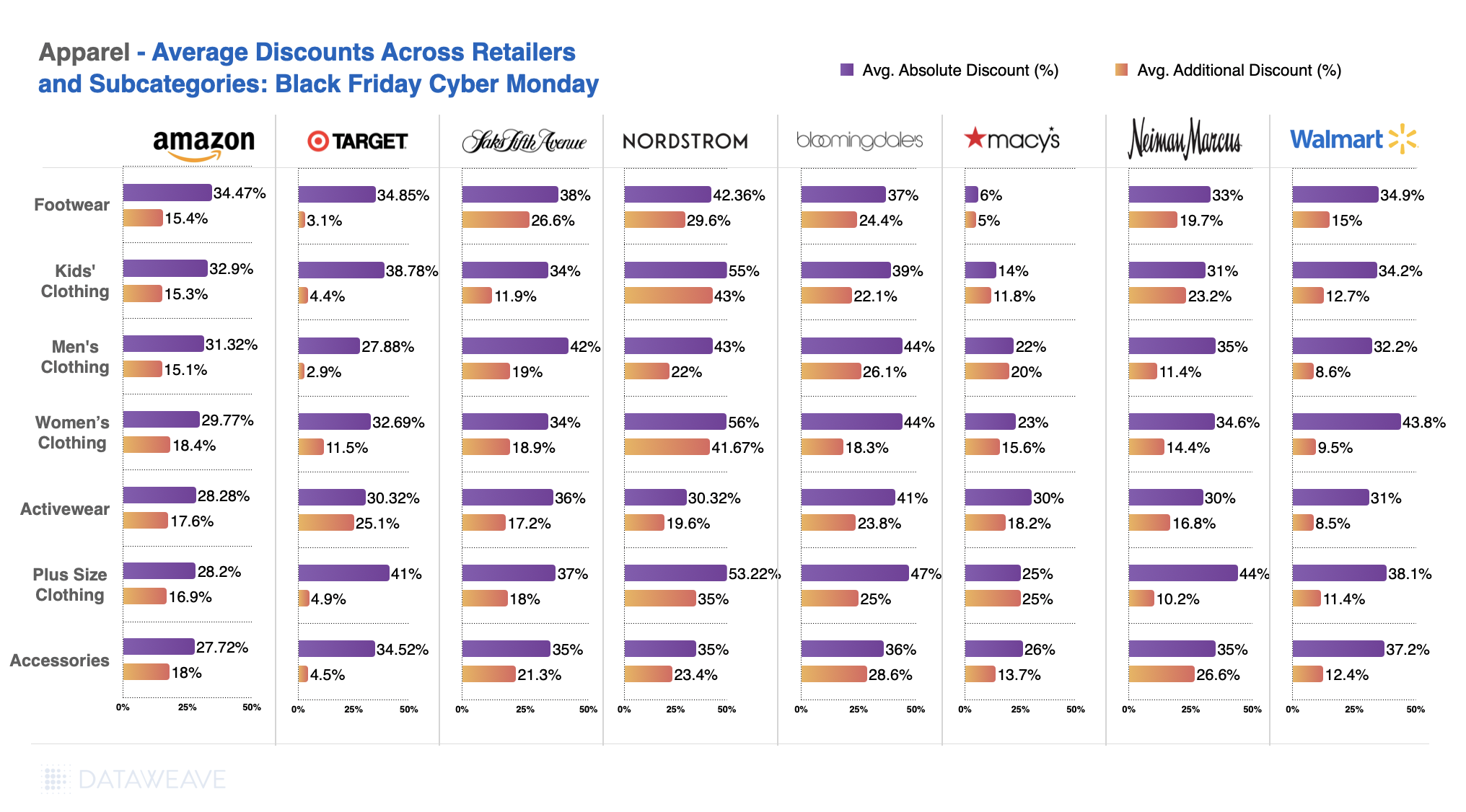

Subcategory Analysis

Kids’ Clothing saw the deep discounts (up to 55% at Nordstrom), reflecting growing pressure on family budgets and heightened competition to attract budget-conscious parents.

Plus-Size Clothing emerged as a major focus, with Nordstrom leading at 53.22% average absolute discounts, signaling that retailers are increasingly prioritizing size inclusivity and appealing to a broader consumer base.

Footwear experienced robust discounting, particularly at Bloomingdale’s with 37% average absolute discounts, showing a competitive approach to attract customers looking for seasonal footwear deals.

Activewear displayed substantial discounts, with Walmart offering up to 41% on average, aligning with the trend of consumers looking for practical and comfortable attire during the winter season.

Brand Level Insights

Apparel brands, meanwhile, also offer telling insights.

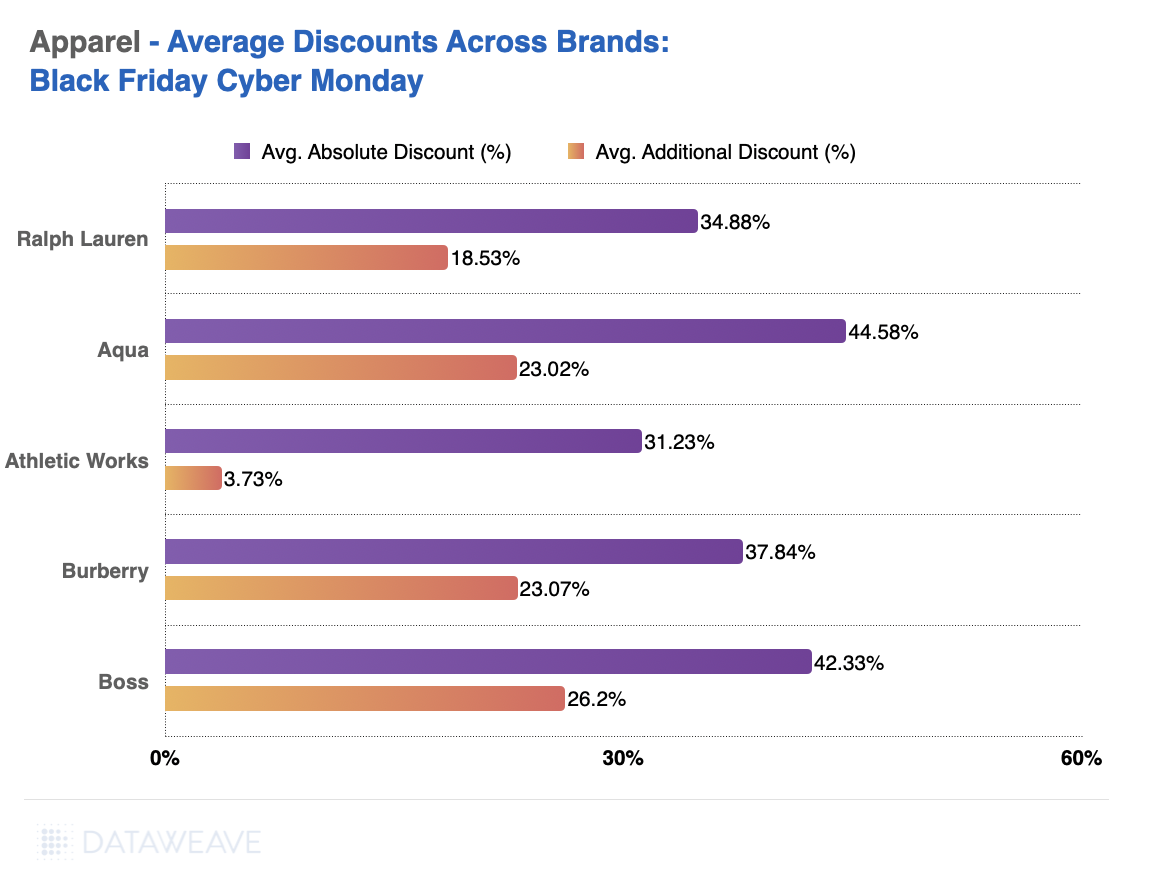

Top Discounting Brands: Aqua leads with an average absolute discount of 44.58%, followed by Boss at 42.33% and Burberry at 37.84%.

Lowest Discounts: Athletic Works shows the lowest average absolute discount at 31.23%, with a minimal additional discount of 3.73%.

Competitive Advantage: Brands like Ralph Lauren and Boss show strong discounts, indicating aggressive marketing during the sale.

Share of Search Insights

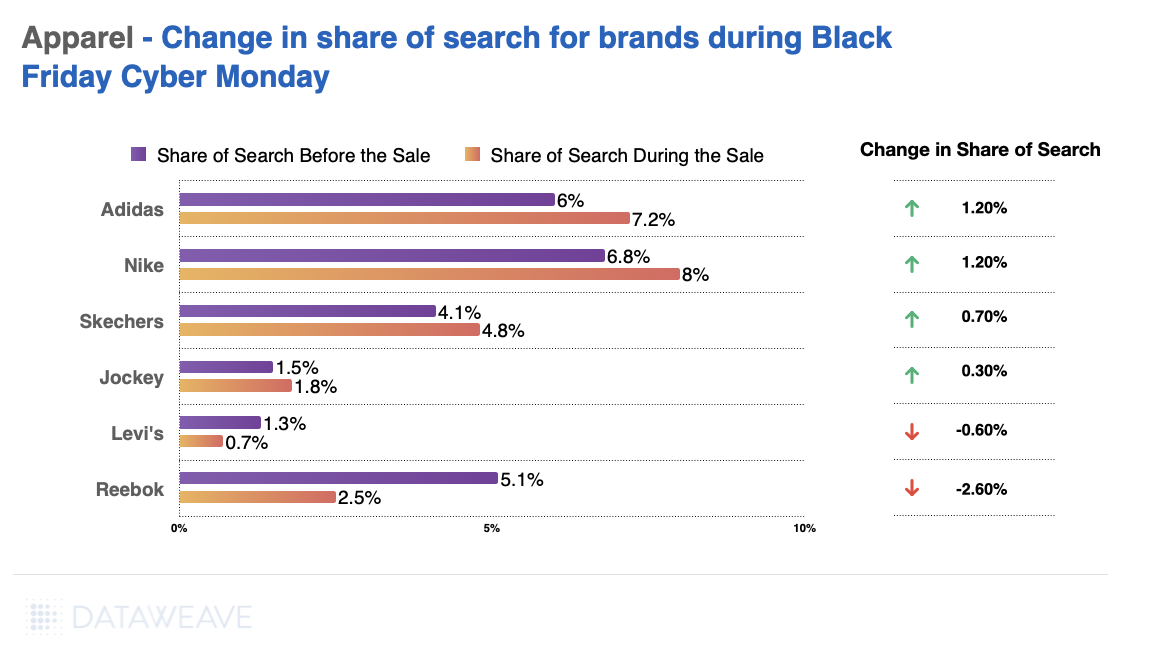

Top Gainers: Adidas and Nike each saw an increase of 1.20% in their share of search during Black Friday/Cyber Monday, highlighting their strong brand presence and consumer interest.

Top Losers: Reebok experienced a sharp decline, losing 2.60% in its share of search, while Levi’s also dropped by 0.60%.

Search Trends: The data suggests a strong consumer preference for activewear brands like Nike and Adidas and a decline in interest for traditional apparel brands like Levi’s.

Who Offered Most Value This Black Friday

In the previous analysis, we focused on the top 500 products within each subcategory for each retailer, showcasing the discount strategies for their highlighted or featured items. However, to identify which retailer offered the lowest or highest prices for the same set of products, it’s necessary to match items across retailers. For this, we analyzed a separate dataset of 418 matched products across Apparel specific retailers to compare their pricing during Black Friday. This approach provides a clearer picture of price leadership and competitiveness across categories.

Here are the key takeaways from this analysis.

Category-Level Analysis

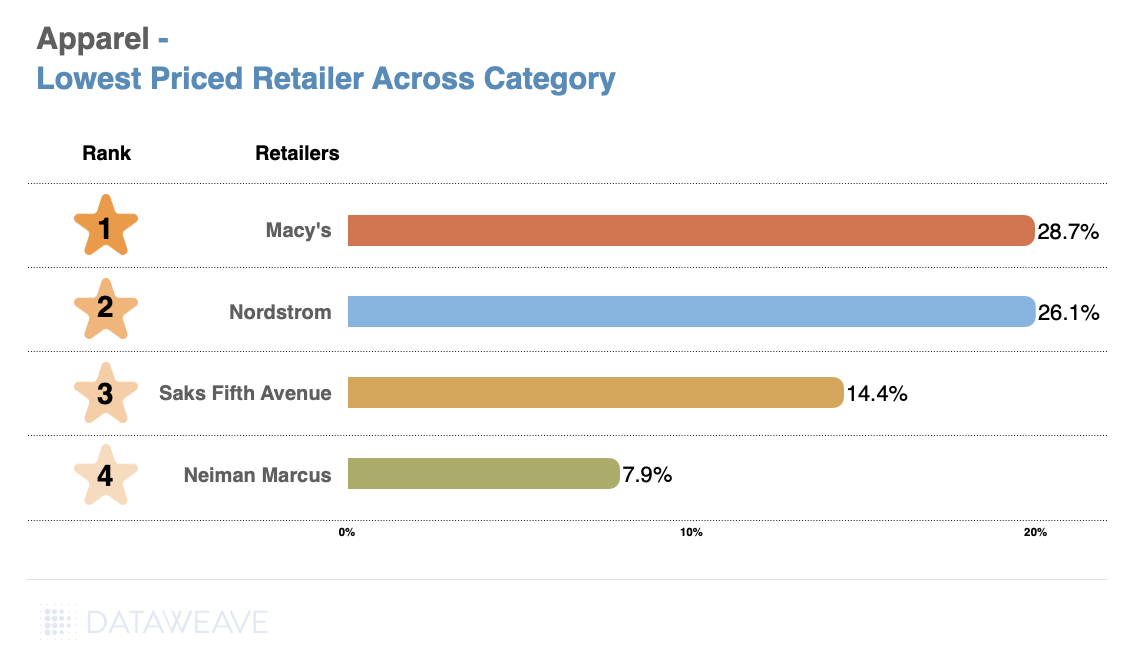

At the overall category level, Macy’s emerged as the lowest-priced retailer, offering the highest average discount of 28.72%, followed closely by Nordstrom (26.06%). The steep decline in average discounts from Saks Fifth Avenue (14.42%) and Neiman Marcus (7.93%) highlights a clear gap in discounting strategies.

Macy’s and Nordstrom are aggressively competitive on pricing in the overall apparel category, likely capturing consumer attention with substantial discounts.

Saks Fifth Avenue and Neiman Marcus may rely more on brand perception and luxury positioning rather than heavy discounting.

Subcategory-Level Analysis

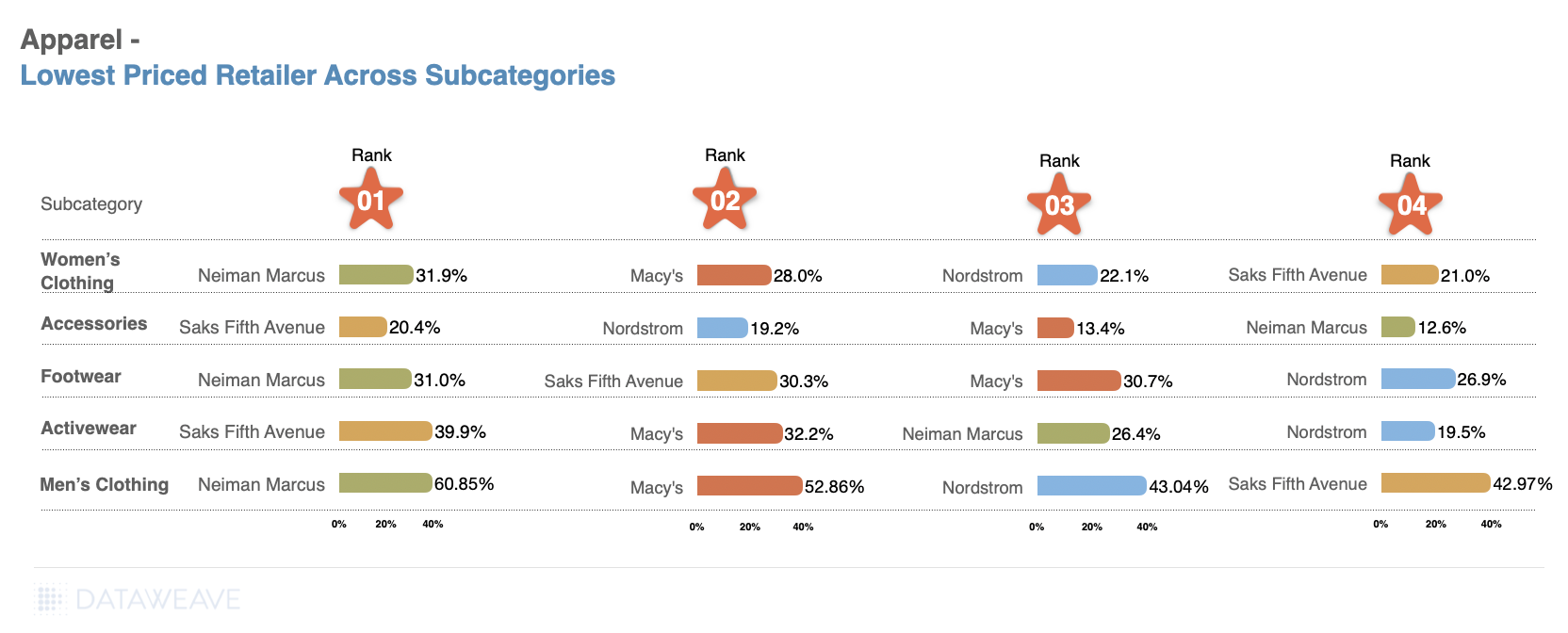

Neiman Marcus tops the ranking with an impressive 60.85% average discount, outperforming Macy’s (52.86%) and Nordstrom (43.04%) for Men’s Clothing. We see a similar trend with Neiman Marcus offering more value across Women’s Clothing as well, compared to other retailers.

The competition in footwear was intense, with Neiman Marcus narrowly securing the top spot at 31.03%, slightly ahead of Saks Fifth Avenue (30.28%) and Macy’s (30.07%).

Saks Fifth Avenue led by a significant margin in the Activewear category, offering 39.89% average discounts, indicating a strong push in this growing segment.

Macy’s followed at 32.16% in Activewear, while Neiman Marcus and Nordstrom had comparatively lower discounts of 26.40% and 19.52%, respectively.

Brand-Level Analysis

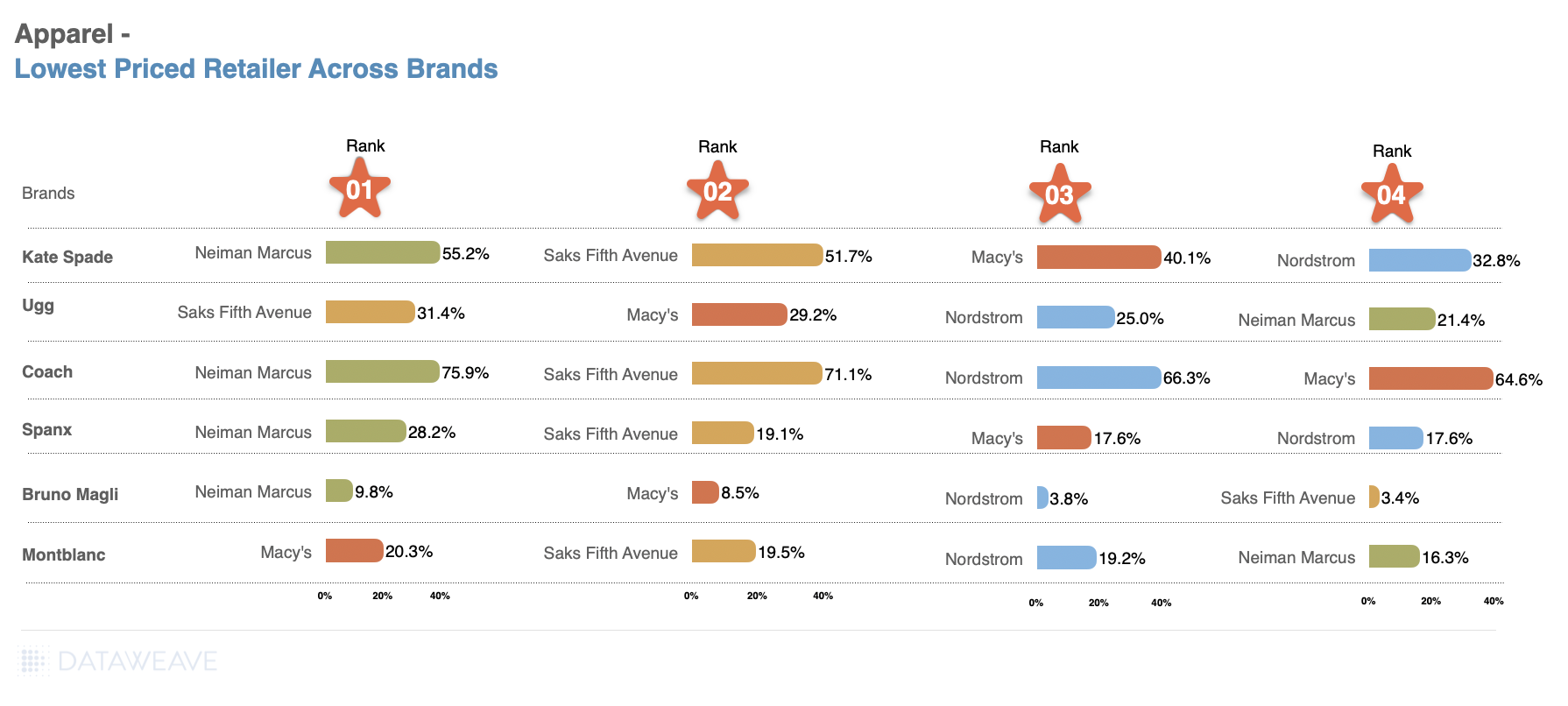

Kate Spade New York: Neiman Marcus leads with the highest discount of 55.23%, reflecting strong price leadership in premium fashion, closely followed by Saks Fifth Avenue at 51.66%.

Coach: Neiman Marcus dominates with a significant 75.85% discount, showcasing an aggressive promotional strategy for this luxury brand.

Spanx: While Neiman Marcus leads with 28.22%, discounts across other retailers like Saks Fifth Avenue, Macy’s, and Nordstrom are clustered within a competitive range of 17–19%.

Montblanc: Macy’s takes the lead with 20.32%, signaling its competitiveness even in high-end accessories, with Saks Fifth Avenue and Nordstrom closely behind.

Ugg: Saks Fifth Avenue leads with 31.42%, focusing on maintaining price leadership for this popular brand, while other retailers remain competitive with discounts around 25–30%.

What’s Next

To win over price-conscious shoppers, retailers need to stay competitive and consistently offer the lowest prices.

For a deeper dive into the world of competitive pricing intelligence and to explore how our solutions can benefit apparel retailers and brands, reach out to us today!

Stay tuned to our blog for more insights on different categories this Black Friday and Cyber Monday.

Black Friday, once confined to a single weekend, has evolved into a shopping season that now stretches well before Thanksgiving. With inflation hovering around 3% and consumer confidence showing signs of recovery, retailers are adapting their promotional calendars to capture early-bird shoppers and maintain a competitive edge.

Major retailers, including Amazon, Walmart, Target, and Best Buy, have capitalized on this trend by launching promotions weeks in advance, signaling the traditional holiday rush is now a month-long event. At DataWeave, we put these deals under a microscope.

Our Methodology

Using DataWeave’s advanced, AI-powered pricing intelligence platform, we tracked early Black Friday deals across Consumer Electronics, Home & Furniture, Health & Beauty, and Apparel categories. We monitored dedicated Black Friday deal pages on Amazon, Walmart, Target, Best Buy, Nordstrom, Neiman Marcus, and Sephora to gather and analyze discount data a week prior to Black Friday weekend.

Who’s Offering the Best Deals Across Categories?

Our pre- Black Friday analysis reveals a clear pattern of premium brands offering deeper discounts across categories ahead of the holiday. Here are some key findings around retail players:

Walmart emerges as the most aggressive discounter across categories, leading in Health & Beauty (57.07%), Apparel (48.97%), and Consumer Electronics (43.35%).

Amazon maintains consistent but lower discounts (28-29%) across categories, suggesting potential deeper cuts ahead.

Best Buy and Sephora, both category specialists, play it conservative compared to mass retail players.

Let’s look at each category more closely to get a detailed snapshot of the deals this Thanksgiving week:

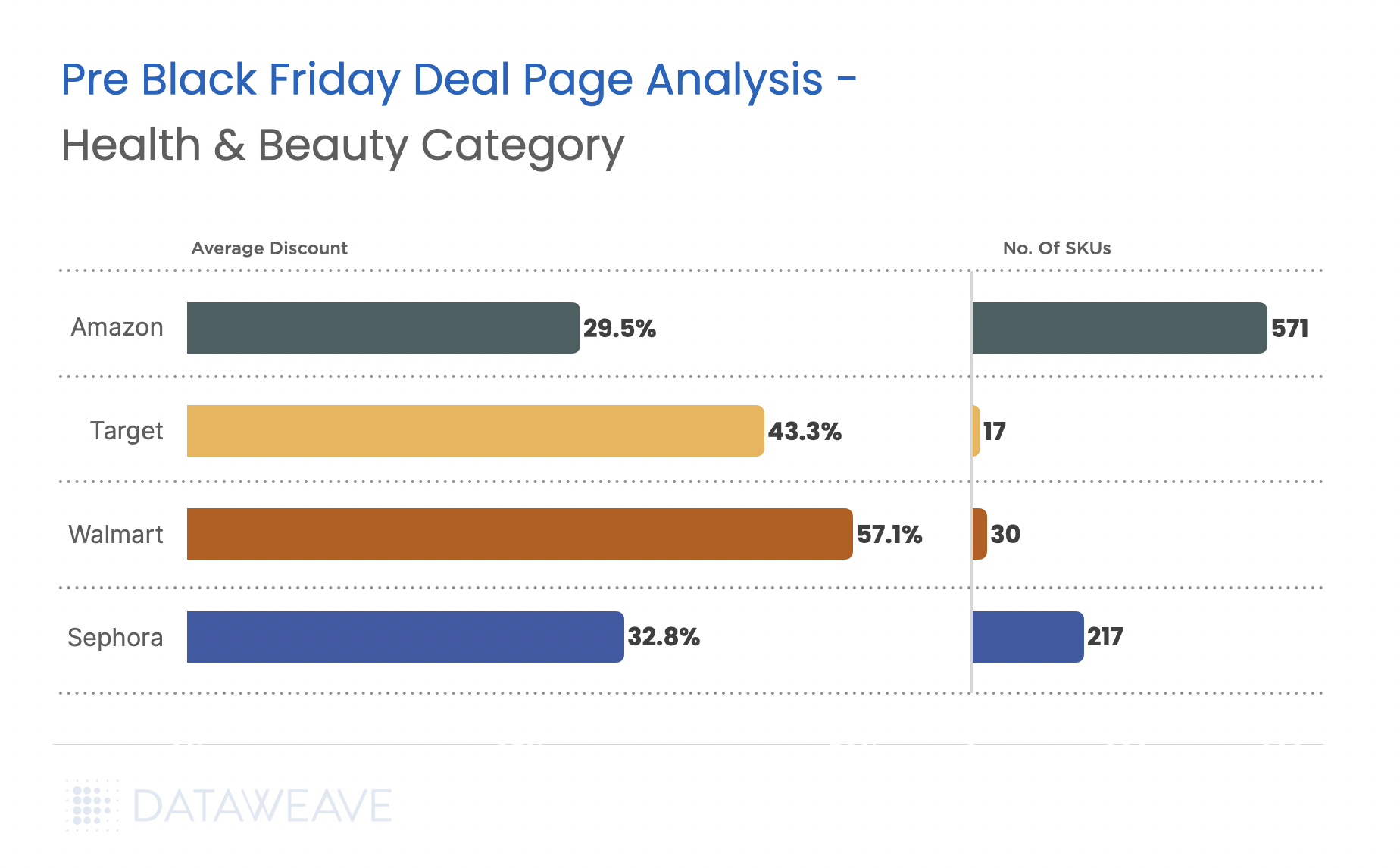

Health & Beauty

Our analysis reveals that it’s not electronics, but the health & beauty category that leads with the widest discount range pre Black Friday, making it the category to watch out for.

Walmart takes the lead with an aggressive 57.1% average discount in this category, capitalizing on its value-oriented reputation.

Beauty specialist Sephora holds modest beauty discounts (32.81%) compared to other retailers.

Amazon offers the broadest range of SKUs (571) in the category.

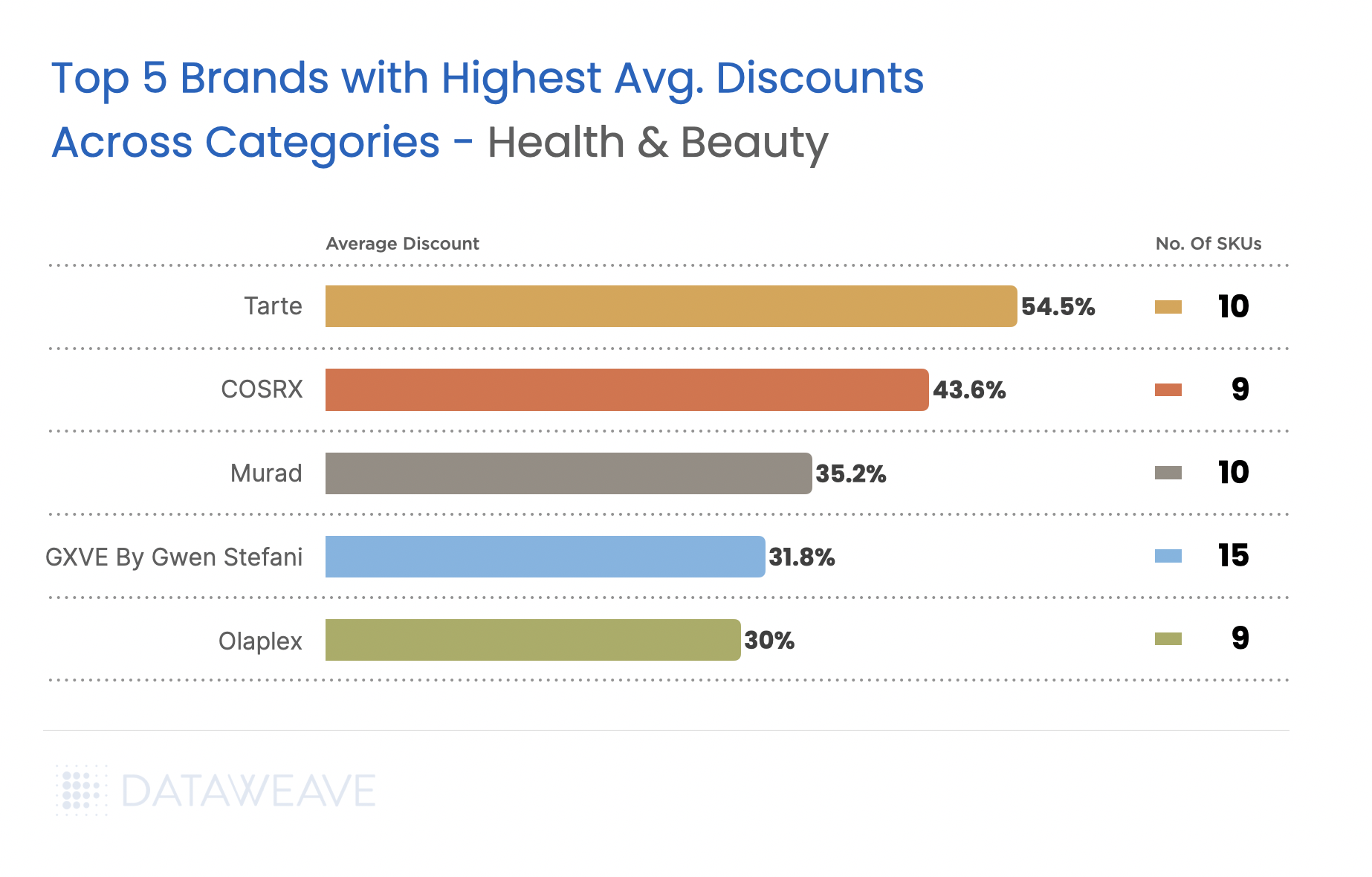

Among the health & beauty brands we analyzed, cosmetics brand Tarte and viral K-Beauty skincare brand COSRX stand out with discounts above 40%, appealing to cost-conscious beauty enthusiasts.

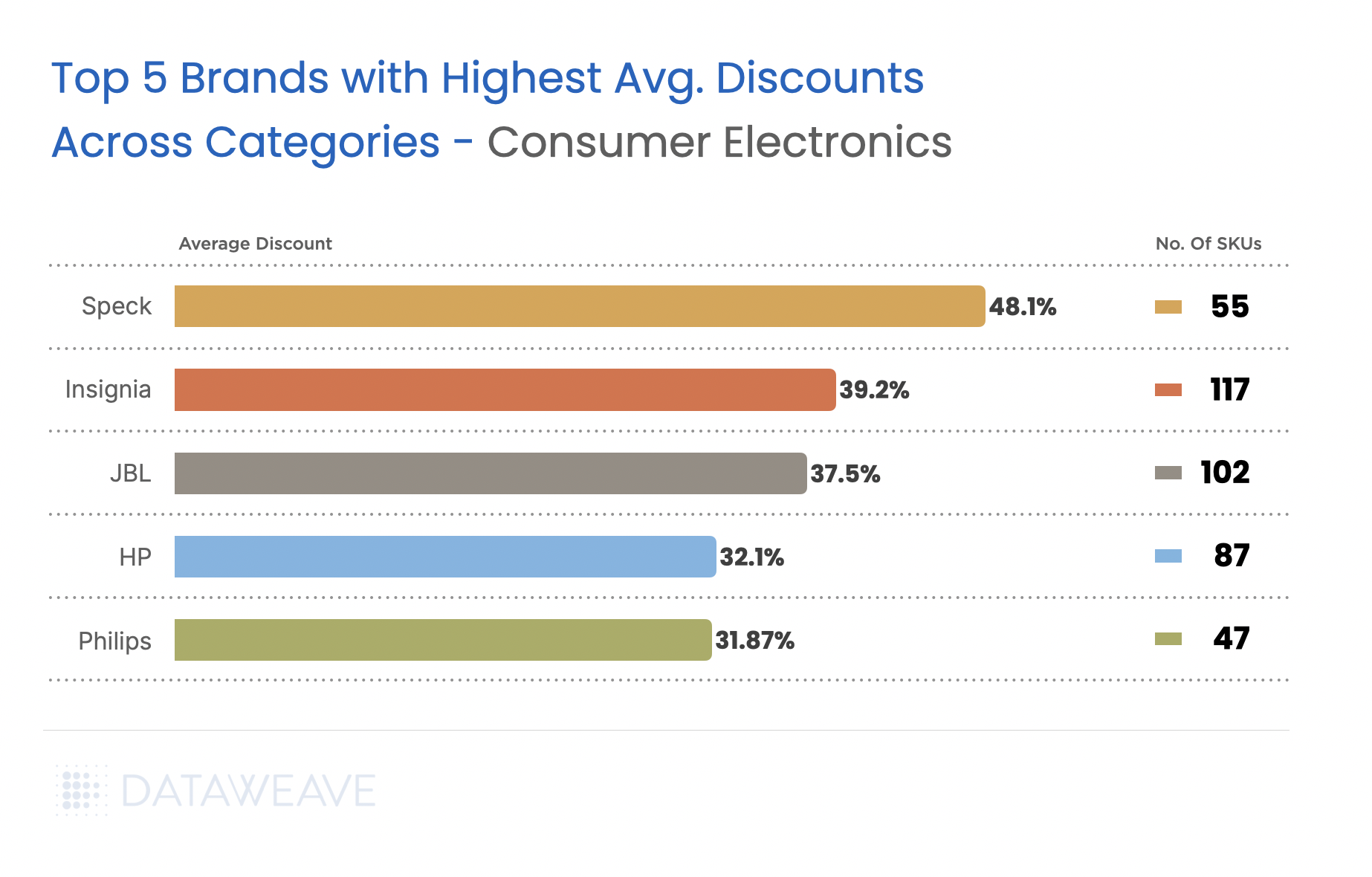

Consumer Electronics

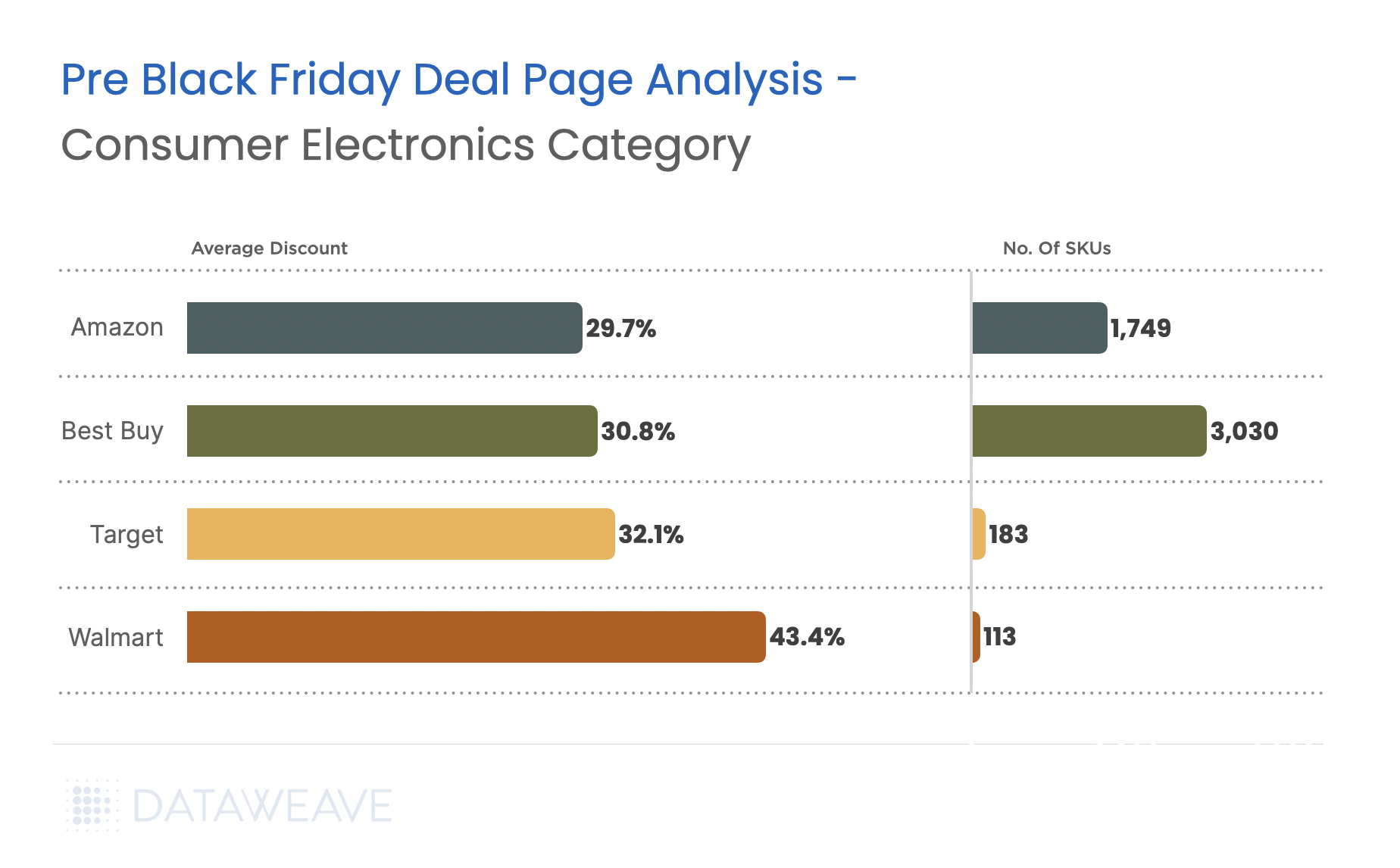

Our pre- Black Friday analysis reveals interesting insights about consumer electronics deals this season.

Walmart, once again, emerges as the frontrunner in the category with 43.4% average discounts.

Best Buy plays it conservative in electronics (30.75%), despite being a category specialist, but offers the most extensive SKU coverage (3030).

Amazon’s consistent 29.7% discount across 1,749 SKUs suggests they’re probably holding back their best deals for Prime members during Black Friday.

Brand-specific data for the category reveals significant deals on Speck (48.07%) and smart TV brand Insignia (39.22%), making accessories and mid-tier electronics attractive for early shoppers. Core computing (HP at 32.14%) and electronics brands maintain more conservative discounts. It remains to be seen if this changes on Black Friday or Cyber Monday.

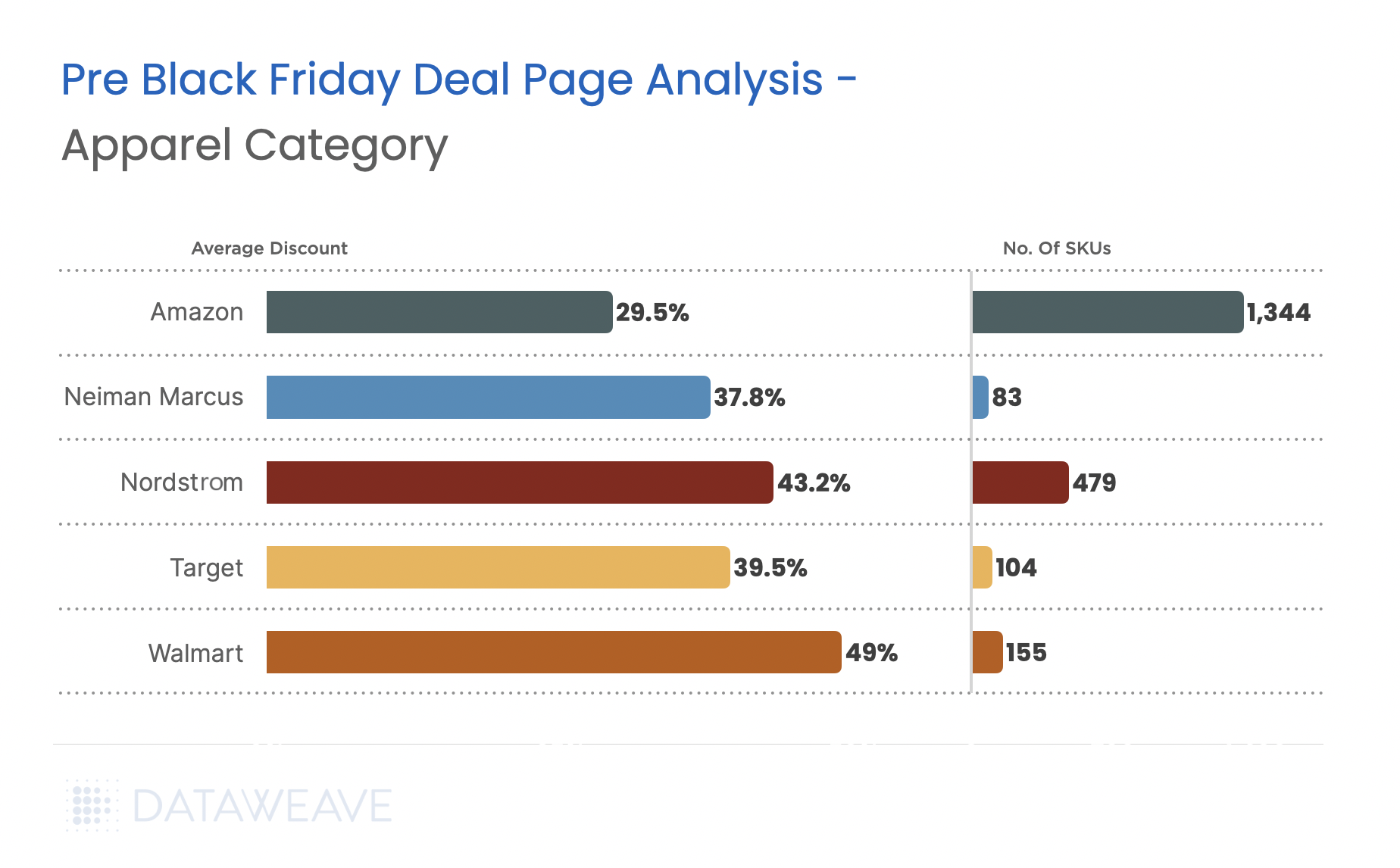

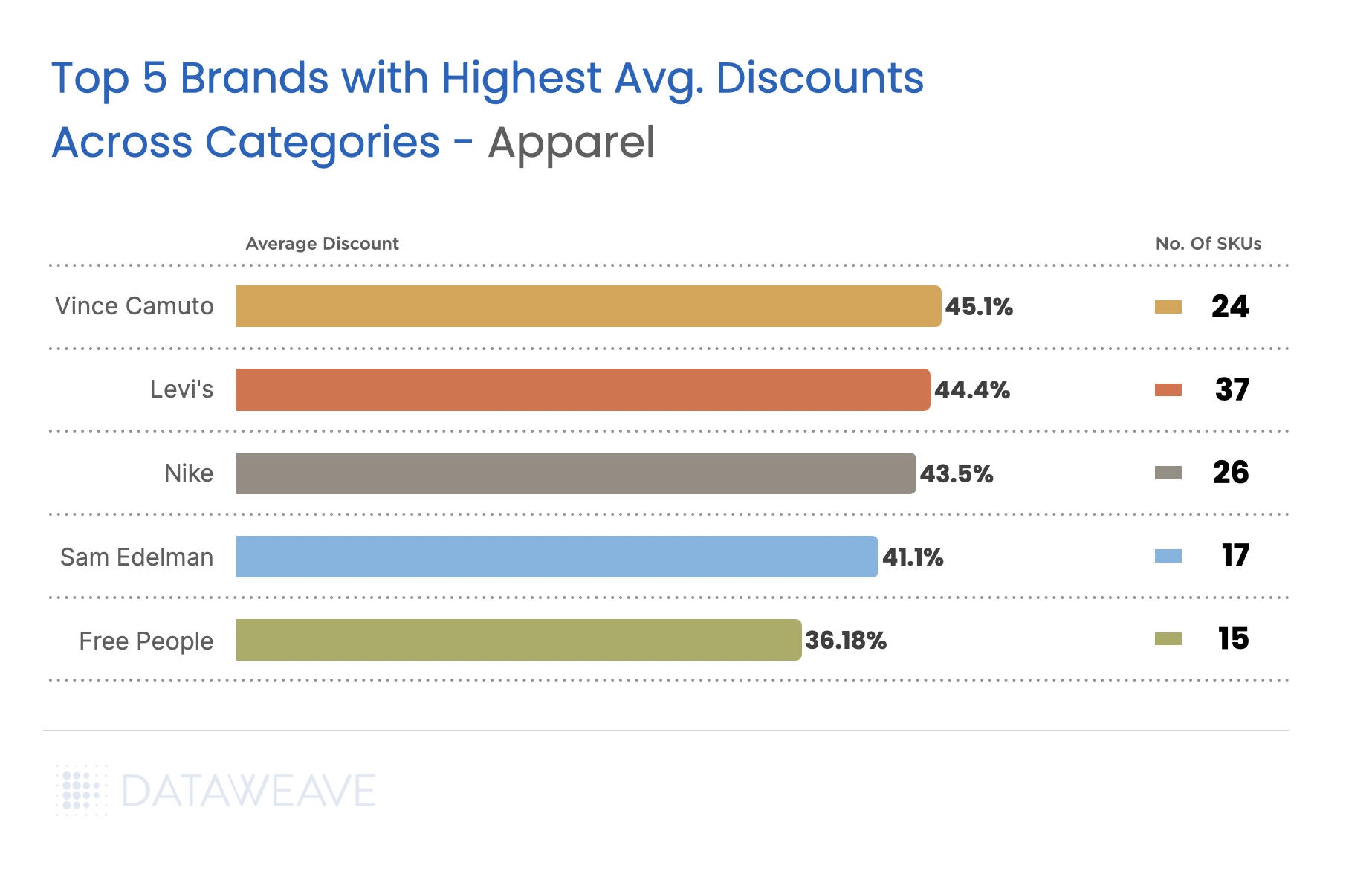

Apparel

Our analysis of the apparel category reveals several highlights:

In the apparel category too, Walmart dominates with an impressive 49% average discount, effectively targeting price-sensitive shoppers in the fashion segment.

Nordstrom and Neiman Marcus, both known for apparel, offer significant discounts at 43.2% and 37.8% respectively.

Amazon’s expansive SKU coverage (1344) is countered by a modest 29.5% discount, showing its focus on variety over depth of discounts.

Premium fashion brands dominate the highest discounts this Black Friday in the apparel category. Vince Camuto leads with over 45.1% average discount. Notably, Levi and Nike’s aggressive 44.43% and 43.50% discounts suggests significant inventory positions or intent to capture market share.

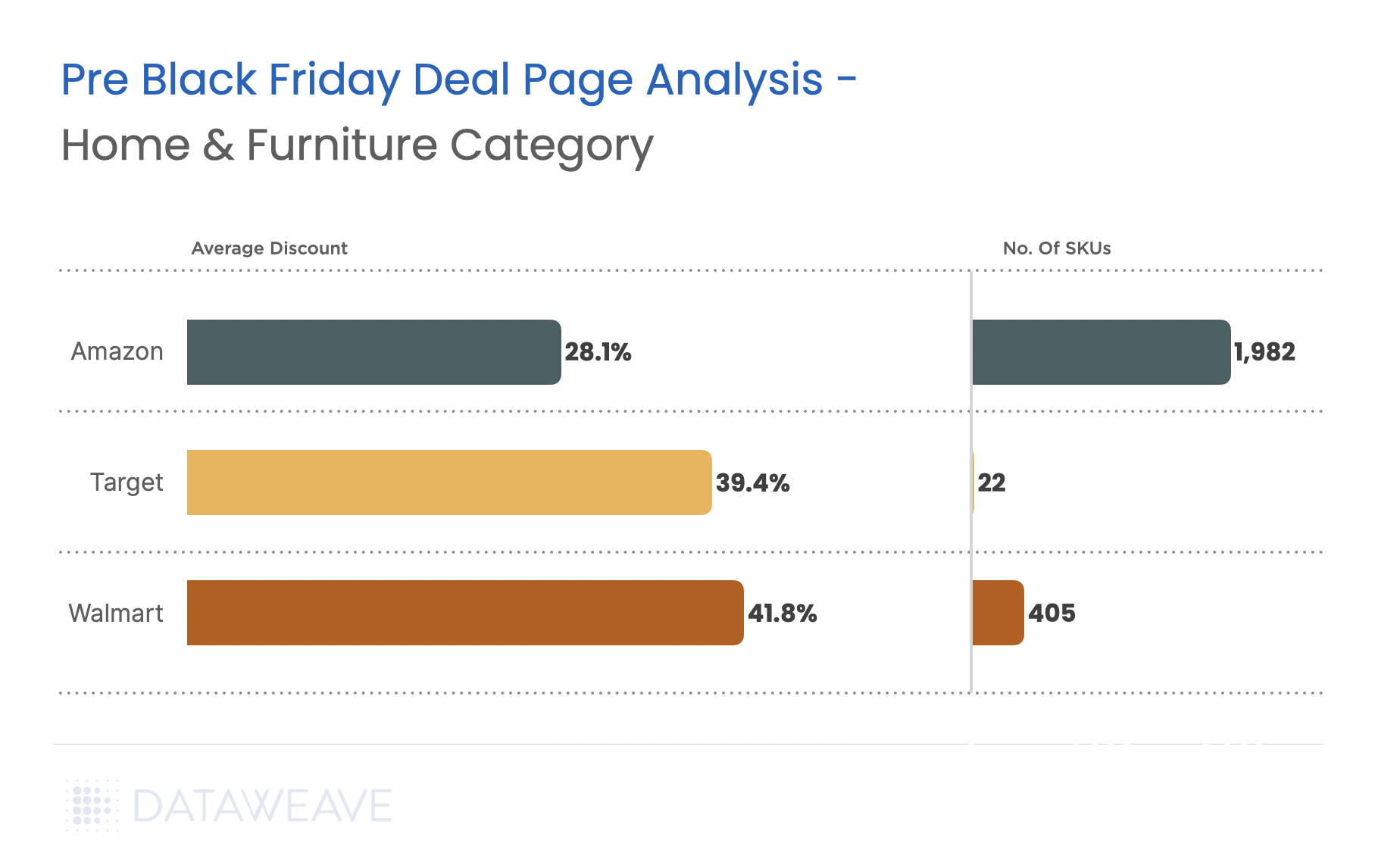

Home & Furniture

Our analysis reveals an interesting trend across the category.

In the home & furniture category too, Walmart leads at 41.8% average discounts. Target follows closely, but with significantly lesser SKUs on offer.

Amazon’s 28.1% discount, though the lowest among major players, spans a substantial 1,982 SKUs, reinforcing its position as a marketplace for diverse needs.

Top 3 Products With the Highest Discounts Across Retailers

To provide a clearer picture of the early Black Friday landscape, we analyzed the top 3 products with the most substantial discounts in consumer electronics and health & beauty categories. These insights highlight how retailers are leveraging strategic discounts on high-value items to attract early shoppers.

Top Discounted Products in Consumer Electronics

Premium TVs dominate the discount scene, with LG’s 83″ OLED offering up to 44.5% off on Amazon, closely followed by a 44.4% discount on Best Buy, showcasing aggressive competition. The same product has much lower discounting on Walmart, but notably, the product is retailed at $3999.9, at least $1000 less than other retailers, highlighting Walmart’s commitment to offering lowest prices.

Gaming consoles, like the PlayStation 5 Slim Bundle, show moderate discounts (ranging from 15% on Walmart and Target to 25% at Best Buy), appealing to tech-savvy shoppers.

Notable competition is evident in price matching across major retailers, particularly in TVs and high-value electronics like the Nikon Z 8 camera, where Walmart offers the deepest discount at 13.75%, edging past Amazon and Best Buy.

Top Discounted Products in Health & Beauty

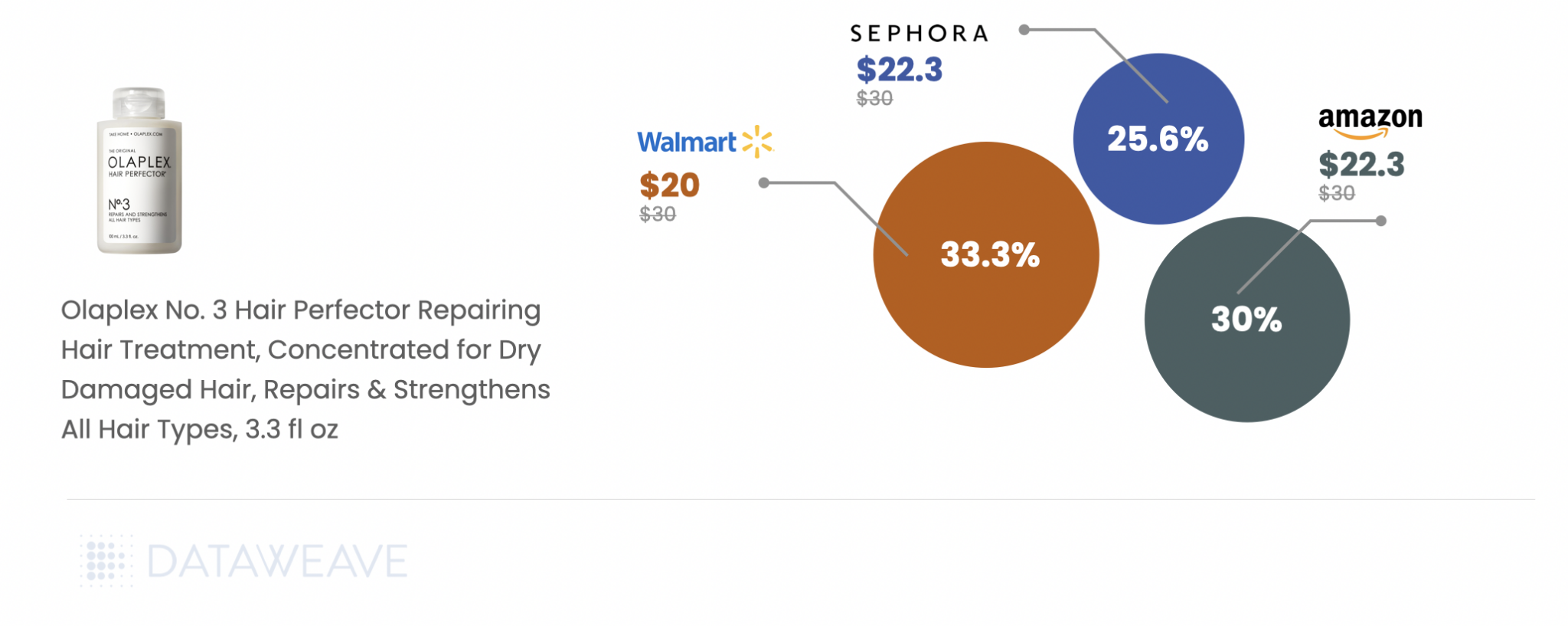

Viral skincare staples like Tatcha’s Water Cream show tight discounting consistency, with Walmart offering 19.47% off compared to Amazon’s 20% and Sephora’s 20.83%.

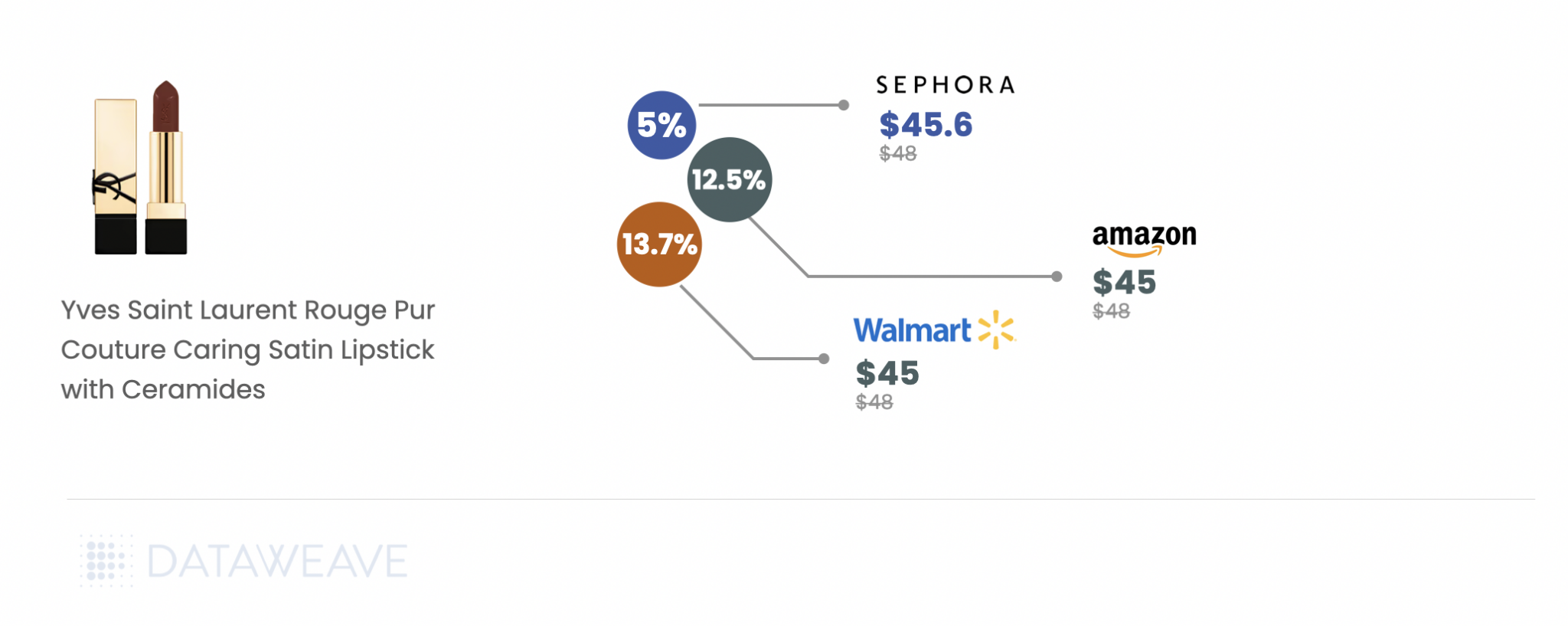

Trending haircare brand Olaplex displays greater disparity, with Walmart leading with a 33.33% discount, surpassing Amazon and Sephora. Luxury brand, Yves Saint Laurent’s Satin Lipstick is one of the highest discounted items across retailers.

Looking Ahead

Our analysis suggests that while some early deals offer genuine value, particularly in premium beauty and high-end electronics, many retailers might be holding their best discounts for Black Friday.

For shoppers, the key is being selective: jump on premium brand discounts now (since they’re likely to remain the same though the weekend), but wait on mid-range electronics and home goods where better deals are likely to emerge on Black Friday or Cyber Monday.

For retailers, the imperative is clear: dynamic pricing intelligence is crucial for maintaining a competitive edge while protecting margins. Competitive insights will be critical as the holiday season progresses to balance market share against profitability.

Stay tuned for our Black Friday Cyber Monday analysis next week, where we’ll track how these early discounts compare to the main event’s deals!

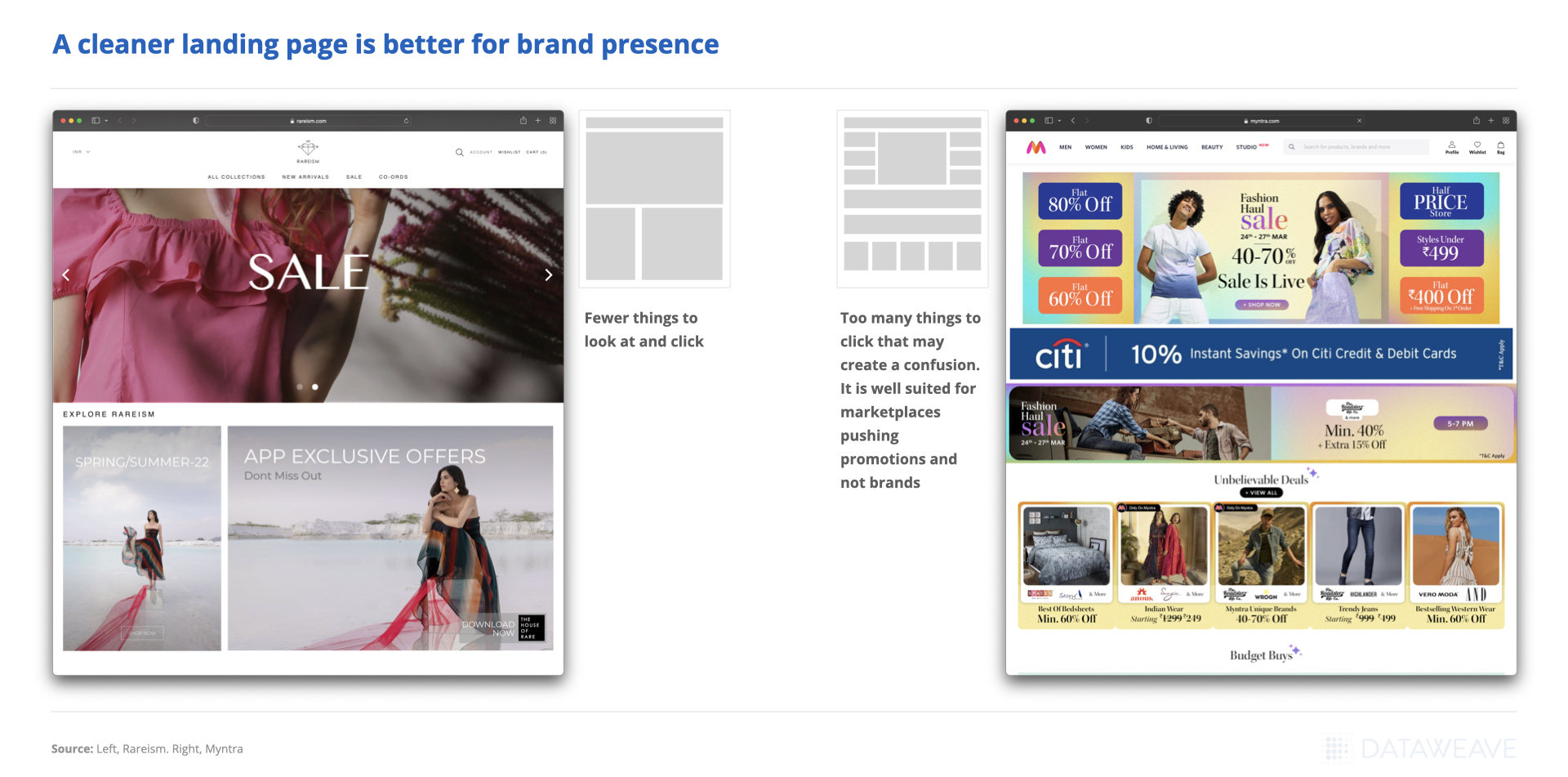

In online retail, success hinges on more than just offering quality products at competitive prices. As eCommerce catalogs expand and consumer expectations soar, businesses face an increasingly complex challenge: How do you effectively organize, categorize, and present your vast product assortments in a way that enhances discoverability and drives sales?

Having complete and correct product catalog data is key. Effective product attribute tagging—a crucial yet frequently undervalued capability—helps in achieving this accuracy and completeness in product catalog data. While traditional methods of tagging product attributes have long struggled with issues of scalability, consistency, accuracy, and speed, a new thinking and fundamentally new ways of addressing these challenges are getting established. These follow from the revolution brought in Large Language Models but they fashion themselves as Small Language Models (SLM) or more precisely as Domain Specific Language Models. These can be potentially considered foundational models as they solve a wide variety of downstream tasks albeit within specific domains. They are a lot more efficient and do a much better job in those tasks compared to an LLM. .

Retail Domain Language Models (RLMs) have the potential to transform the eCommerce customer journey. As always, it’s never a binary choice. In fact, LLMs can be a great starting point since they provide an enhanced semantic understanding of the world at large: they can be used to mine structured information (e.g., product attributes and values) out of unstructured data (e.g., product descriptions), create baseline domain knowledge (e.g, manufacturer-brand mappings), augment information (e.g., image to prompt), and create first cut training datasets.

Powered by cutting-edge Generative AI and RLMs, next-generation attribute tagging solutions are transforming how online retailers manage their product catalog data, optimize their assortment, and deliver superior shopping experiences. As a new paradigm in search emerges – based more on intent and outcome, powered by natural language queries and GenAI based Search Agents – the capability to create complete catalog information and rich semantics becomes increasingly critical.

In this post, we’ll explore the crucial role of attribute tagging in eCommerce, delve into the limitations of conventional tagging methods, and unveil how DataWeave’s innovative AI-driven approach is helping businesses stay ahead in the competitive digital marketplace.

Why Product Attribute Tagging is Important in eCommerce

As the eCommerce landscape continues to evolve, the importance of attribute tagging will only grow, making it a pertinent focus for forward-thinking online retailers. By investing in robust attribute tagging systems, businesses can gain a competitive edge through improved product comparisons, more accurate matching, understanding intent, and enhanced customer search experiences.

Taxonomy Comparison and Assortment Gap Analysis

Products are categorized and organized differently on different retail websites. Comparing taxonomies helps in understanding focus categories and potential gaps in assortment breadth in relation to one’s competitors: missing product categories, sizes, variants or brands. It also gives insights into the navigation patterns and information architecture of one’s competitors. This can help in making search and navigation experience more efficient by fine tuning product descriptions to include more attributes and/or adding additional relevant filters to category listing pages.

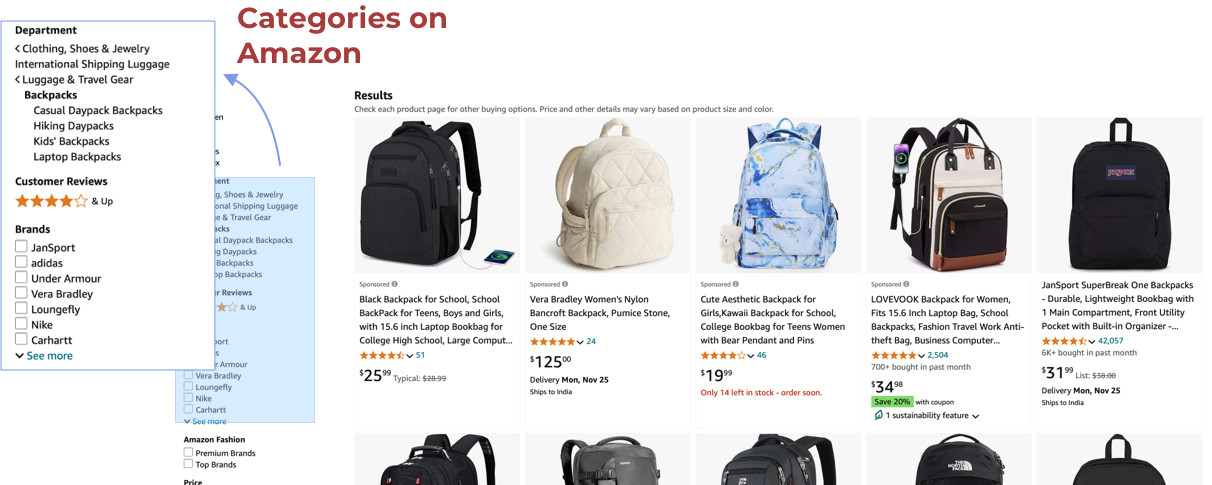

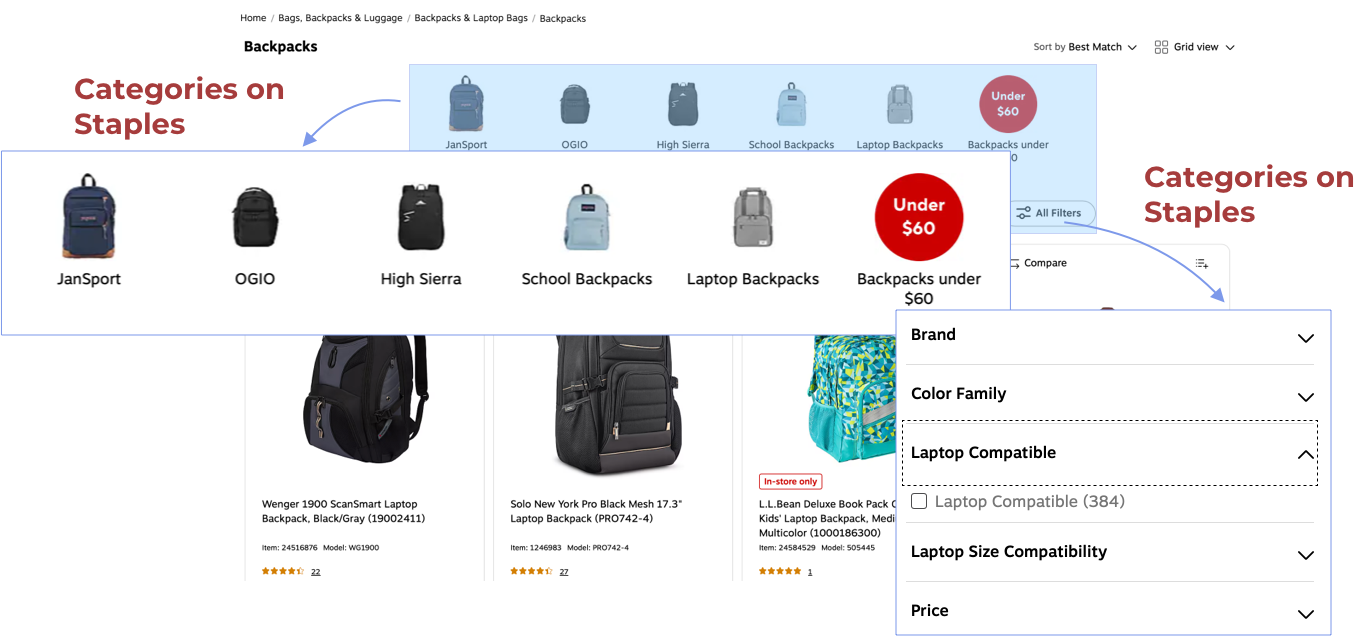

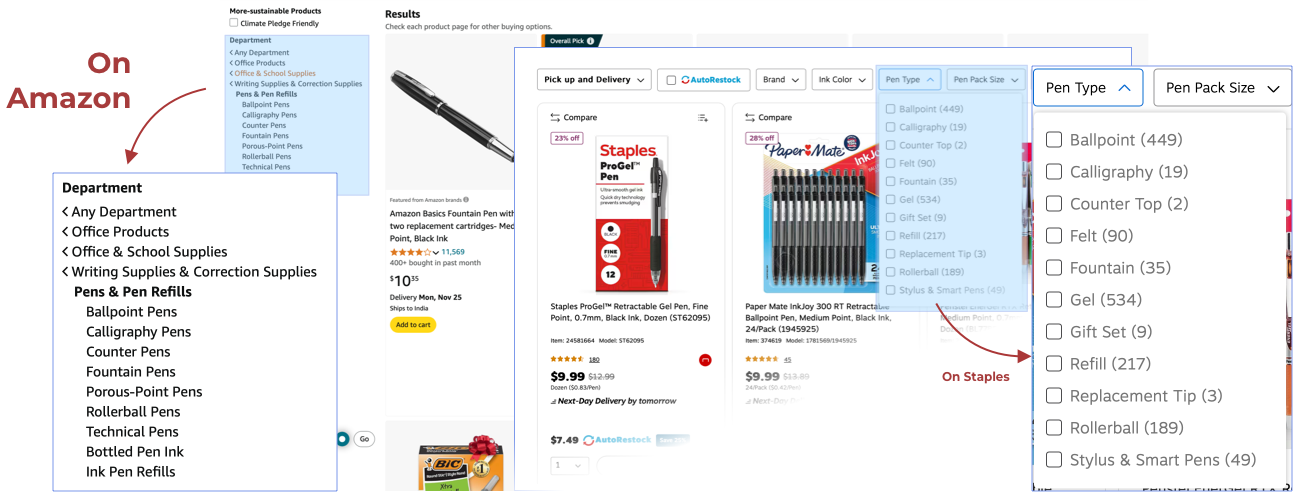

For instance, check out the different Backpack categories on Amazon and Staples in the images below.

Or look at the nomenclature of categories for “Pens” on Amazon (left side of the image) and Staples (right side of the image) in the image below.

Assortment Depth Analysis

Another big challenge in eCommerce is the lack of standardization in retailer taxonomy. This inconsistency makes it difficult to compare the depth of product assortments across different platforms effectively. For instance, to categorize smartphones,

Retailer A might organize it under “Electronics > Mobile Phones > Smartphones”

Retailer B could use “Technology > Phones & Accessories > Cell Phones”

Retailer C might opt for “Consumer Electronics > Smartphones & Tablets”

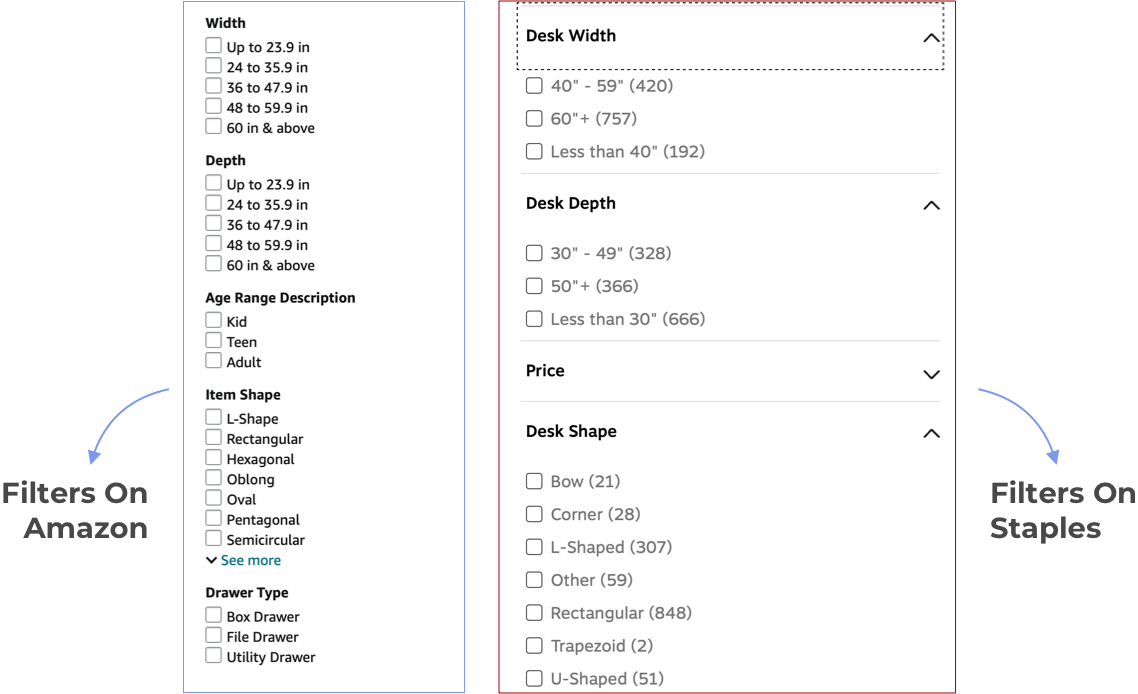

Inconsistent nomenclature and grouping create a significant hurdle for businesses trying to gain a competitive edge through assortment analysis. The challenge is exacerbated if you want to do an in-depth assortment depth analysis for one or more product attributes. For instance, look at the image below to get an idea of the several attribute variations for “Desks” on Amazon and Staples.

Custom categorization through attribute tagging is essential for conducting granular assortment comparisons, allowing companies to accurately assess their product offerings against those of competitors.

Enhancing Product Matching Capabilities

Accurate product matching across different websites is fundamental for competitive pricing intelligence, especially when matching similar and substitute products. Attribute tagging and extraction play a crucial role in this process by narrowing down potential matches more effectively, enabling matching for both exact and similar products, and tagging attributes such as brand, model, color, size, and technical specifications.

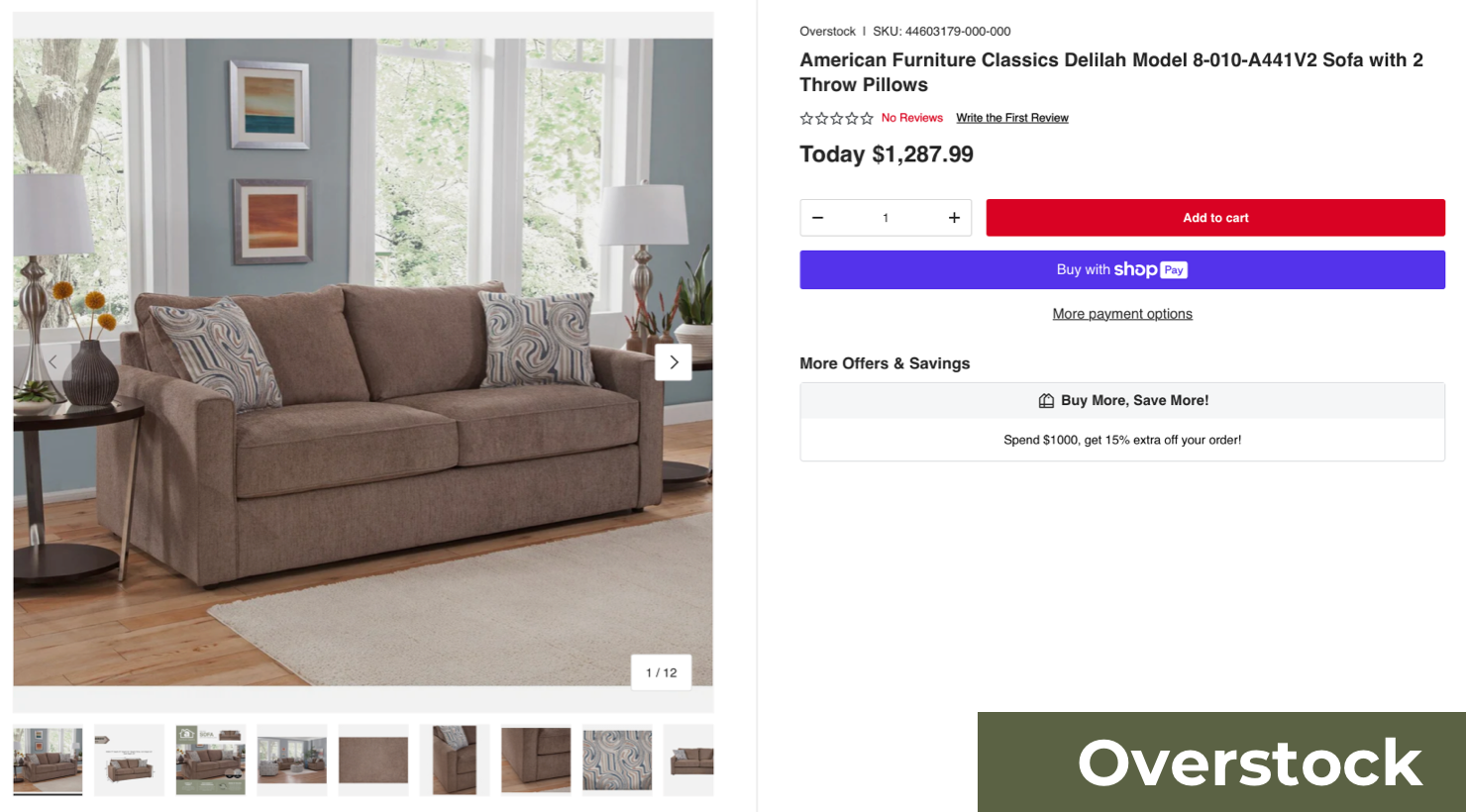

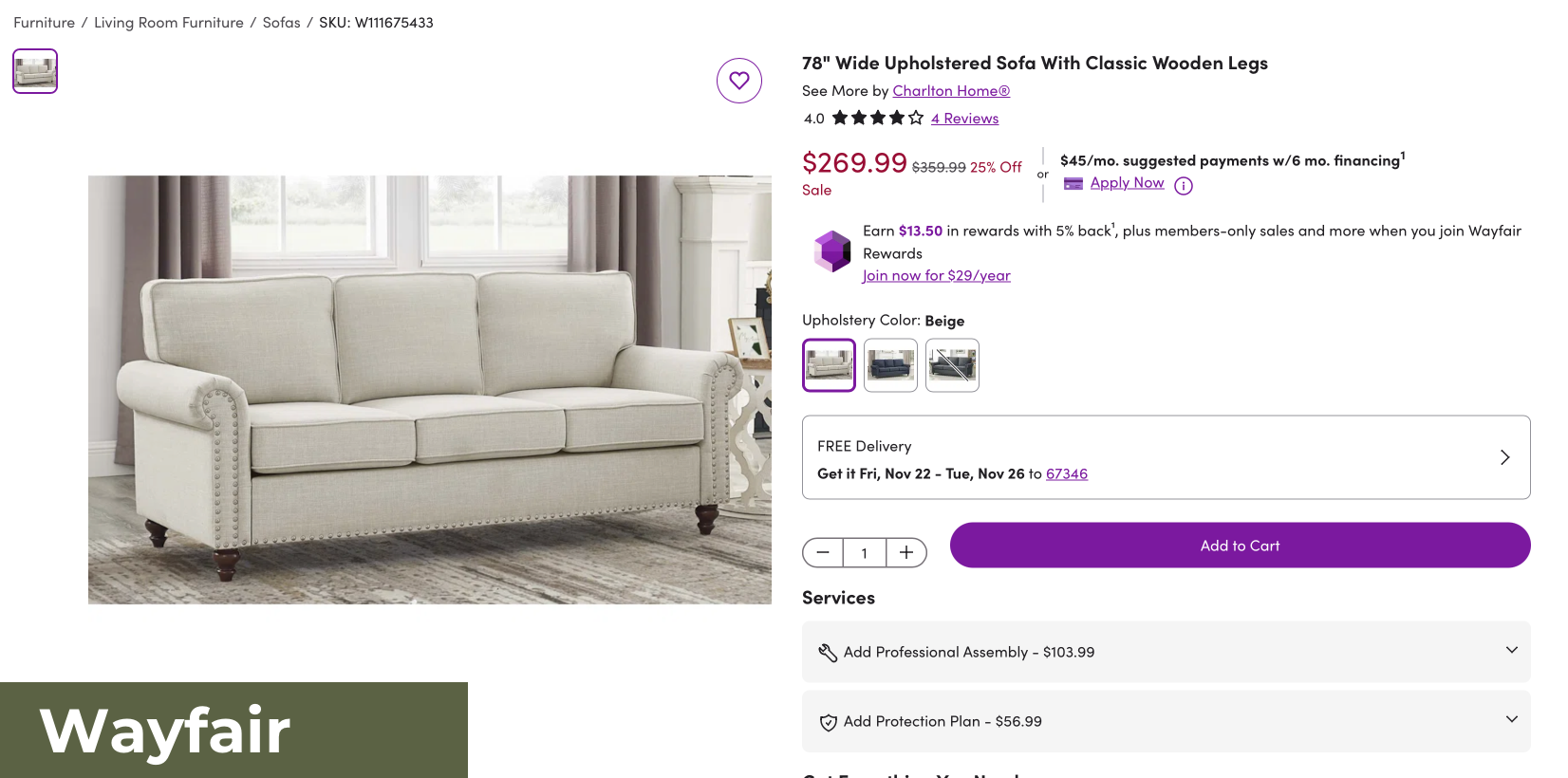

For instance, when choosing to match similar products in the Sofa category for 2-3 seater sofas from Wayfair and Overstock, tagging attributes like brand, color, size, and more is a must for accurate comparisons.

Taking a granular approach not only improves pricing strategies but also helps identify gaps in product offerings and opportunities for expansion.

Fix Content Gaps and improve Product Detail Page (PDP) Content

Attribute tagging plays a vital role in enhancing PDP content by ensuring adherence to brand integrity standards and content compliance guidelines across retail platforms. Tagging attributes allows for benchmarking against competitor content, identifying catalog gaps, and enriching listings with precise details.

This strategic tagging process can highlight missing or incomplete information, enabling targeted optimizations or even complete rewrites of PDP content to improve discoverability and drive conversions. With accurate attribute tagging, businesses can ensure each product page is fully optimized to capture consumer attention and meet retail standards.

Elevating the Search Experience

In today’s online retail marketplace, a superior search experience can be the difference between a sale and a lost customer. Through in-depth attribute tagging, vendors can enable more accurate filtering to improve search result relevance and facilitate easier product discovery for consumers.

By integrating rich product attributes extracted by AI into an in-house search platform, retailers can empower customers with refined and user-friendly search functionality. Enhanced search capabilities not only boost customer satisfaction but also increase the likelihood of conversions by helping shoppers find exactly what they’re looking for more quickly and with minimal effort.

Pitfalls of Conventional Product Tagging Methods

Traditional methods of attribute tagging, such as manual and rule-based systems, have been significantly enhanced by the advent of machine learning. While these approaches may have sufficed in the past, they are increasingly proving inadequate in the face of today’s dynamic and expansive online marketplaces.

Scalability

As eCommerce catalogs expand to include thousands or even millions of products, the limitations of machine learning and rule-based tagging become glaringly apparent. As new product categories emerge, these systems struggle to keep pace, often requiring extensive revisions to existing tagging structures.

Inconsistencies and Errors

Not only is reliance on an entirely human-driven tagging process expensive, but it also introduces a significant margin for error. While machine learning can automate the tagging process, it’s not without its limitations. Errors can occur, particularly when dealing with large and diverse product catalogs.

As inventories grow more complex to handle diverse product ranges, the likelihood of conflicting or erroneous rules increases. These inconsistencies can result in poor search functionality, inaccurate product matching, and ultimately, a frustrating experience for customers, drawing away the benefits of tagging in the first place.

Speed

When product information changes or new attributes need to be added, manually updating tags across a large catalog is a time-consuming process. Slow tagging processes make it difficult for businesses to quickly adapt to emerging market trends causing significant delays in listing new products, potentially missing crucial market opportunities.

How DataWeave’s Advanced AI Capabilities Revolutionize Product Tagging

Advanced solutions leveraging RLMs and Generative AI offer promising alternatives capable of overcoming these challenges and unlocking new levels of efficiency and accuracy in product tagging.

DataWeave automates product tagging to address many of the pitfalls of other conventional methods. We offer a powerful suite of capabilities that empower businesses to take their product tagging to new heights of accuracy and scalability with our unparalleled expertise.

Our sophisticated AI system brings an advanced level of intelligence to the tagging process.

RLMs for Enhanced Semantic Understanding

Semantic Understanding of Product Descriptions

RLMs analyze the meaning and context of product descriptions rather than relying on keyword matching. Example: “Smartphone with a 6.5-inch display” and “Phone with a 6.5-inch screen” are semantically similar, though phrased differently.

Attribute Extraction

RLMs can identify important product attributes (e.g., brand, size, color, model) even from noisy or unstructured data. Example: Extracting “Apple” as a brand, “128GB” as storage, and “Pink” as the color from a mixed description.

Identifying Implicit Relationships

RLMs find implicit relationships between products that traditional rule-based systems miss. Example: Recognizing that “iPhone 12 Pro” and “Apple iPhone 12” are part of the same product family.

Synonym Recognition in Product Descriptions

Synonym Matching with Context

RLMs identify when different words or phrases describe the same product. Examples: “Sneakers” = “Running Shoes”, “Memory” = “RAM” (in electronics) Even subtle differences in wording, like “rose gold” vs “pink” are interpreted correctly.

Overcoming Brand-Specific Terminology

Some brands use their own terminologies (e.g., “Retina Display” for Apple). RLMs can map proprietary terms to more generic ones (e.g., Retina Display = High-Resolution Display).

Dealing with Ambiguities

RLMs analyze surrounding text to resolve ambiguities in product descriptions. Example: Resolving “charger” to mean a “phone charger” when matched with mobile phones.

Contextual Understanding for Improved Accuracy and Precision

By leveraging advanced natural language processing (NLP), DataWeave’s AI can process and understand the context of lengthy product descriptions and customer reviews, minimizing errors that often arise at human touch points. The solution processes and interprets information to extract key information to dramatically improve the overall accuracy of product tags.

It excels at grasping the subtle differences between similar products, sizes, colors and identifying and tagging minute differences between items, ensuring that each product is uniquely and accurately represented in a retailer’s catalog.

This has a major impact on product and similarity-based matching that can even help optimize similar and substitute product matching to enhance consumer search. At the same time, our AI can understand that the same term might have different meanings in various product categories, adapting its tagging approach based on the specific context of each item.

This deep comprehension ensures that even nuanced product attributes are accurately captured and tagged for easy discoverability by consumers.

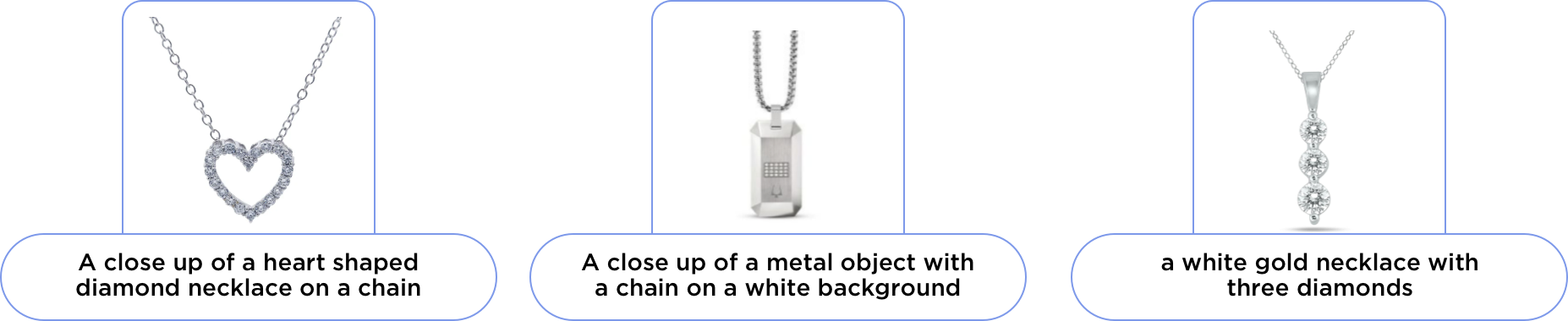

Case Study: Niche Jewelry Attributes

DataWeave’s advanced AI can assist in labeling the subtle attributes of jewelry by analyzing product images and generating prompts to describe the image. In this example, our AI identifies the unique shapes and materials of each item in the prompts.

The RLM can then extract key attributes from the prompt to generate tags. This assists in accurate product matching for searches as well as enhanced product recommendations based on similarities.

This multi-model approach provides the flexibility to adapt as product catalogs expand while remaining consistent with tagging to yield more robust results for consumers.

Unparalleled Scalability

DataWeave can rapidly scale tagging for new categories. The solution is built to handle the demands of even the largest eCommerce catalogs enabling:

Effortless management of extensive product catalogs: We can process and tag millions of products without compromising on speed or accuracy, allowing businesses to scale without limitations.

Automated bulk tagging: New product lines or entire categories can be tagged automatically, significantly reducing the time and resources required for catalog expansion.

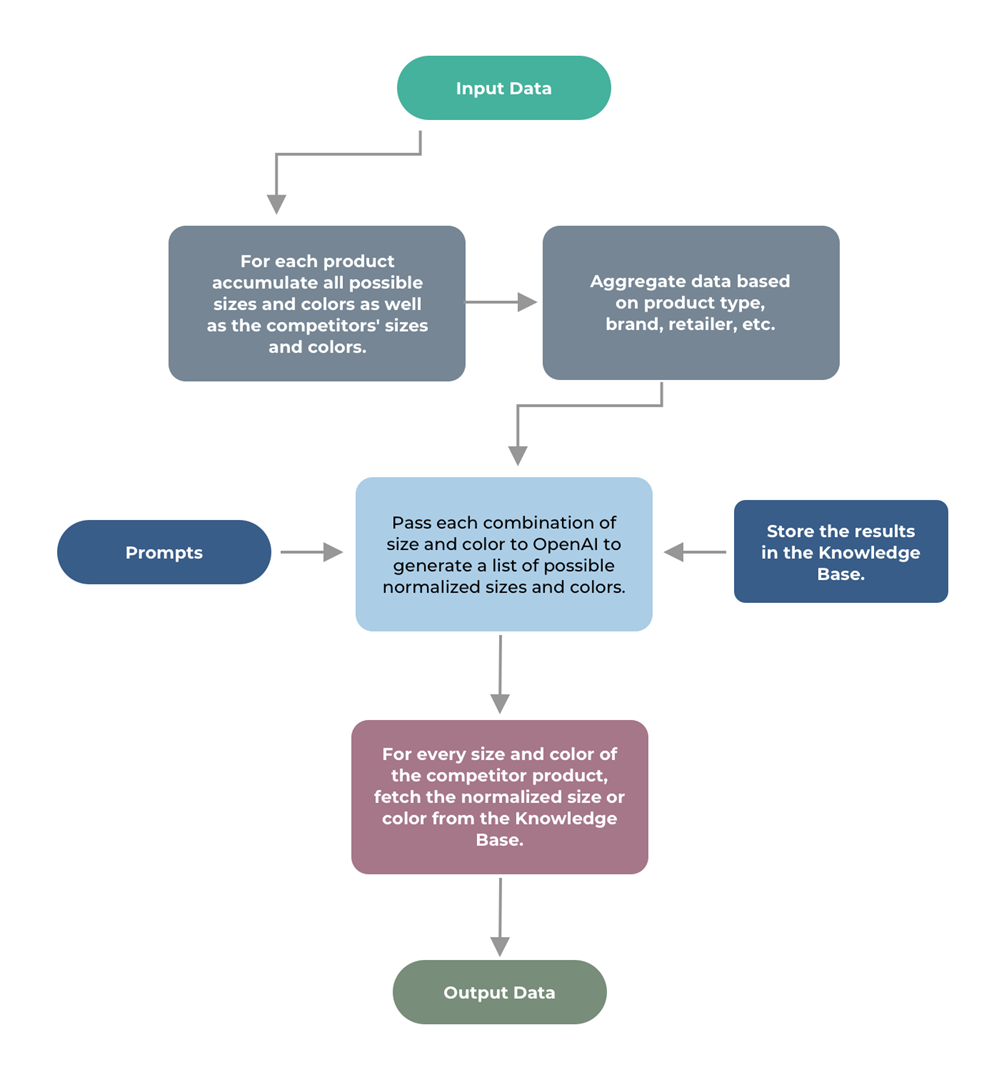

Normalizing Size and Color in Fashion

Style, color, and size are the core attributes in the fashion and apparel categories. Style attributes, which include design, appearance, and overall aesthetics, can be highly specific to individual product categories.

Our product matching engine can easily handle color and sizing complexity via our AI-driven approach combined with human verification. By leveraging advanced technology to identify and normalize identical and similar products from competitors, you can optimize your pricing strategy and product assortment to remain competitive. Using Generative AI in normalizing color and size in fashion is key to powering competitive pricing intelligence at DataWeave.

Continuous Adaptation and Learning

Our solution evolves with your business, improving continuously through feedback and customization for retailers’ specific product categories. The system can be fine-tuned to understand and apply specialized tagging for niche or industry-specific product categories. This ensures that tags remain relevant and accurate across diverse catalogs and as trends emerge.

The AI in our platform also continuously learns from user interactions and feedback, refining its tagging algorithms to improve accuracy over time.

Stay Ahead of the Competition With Accurate Attribute Tagging

In the current landscape, the ability to accurately and consistently tag product attributes is no longer a luxury—it’s essential for staying competitive. With advancements in Generative AI, companies like DataWeave are revolutionizing the way product tagging is handled, ensuring that every item in a retailer’s catalog is presented with precision and depth. As shoppers demand a more intuitive, seamless experience, next-generation tagging solutions are empowering businesses to meet these expectations head-on.

DataWeave’s innovative approach to attribute tagging is more than just a technical improvement; it’s a strategic advantage in an increasingly competitive market. By leveraging AI to scale and automate tagging processes, online retailers can keep pace with expansive product assortments, manage content more effectively, and adapt swiftly to changes in consumer behavior. In doing so, they can maintain a competitive edge.

Fashion is as dynamic a market as any—and more competitive than most others. Consumer trends and customer needs are always evolving, making it challenging for fashion and apparel brands to keep up.

Despite the inherent difficulties fashion and apparel sellers face, this industry is one of the largest grossing markets in the world, estimated at $1.79 trillion in 2024. Global revenue for apparel is expected to grow at an annual rate of about 3.3% over the next four years. That means companies in this space stand to make significant revenue if they can competitively price their products, keep up with the competition, and win customer loyalty with consistent product availability.

There are three main categories in fashion and apparel. These include:

Apparel and clothing (i.e., shirts, pants, dresses, and other apparel)

Footwear (i.e., sneakers, sandals, heels, and other products)

Accessories (i.e., bags, belts, watches, and so on)

If you look at all of these product types across all sorts of retailers, there is a massive amount of overlapping data based on product attributes like style and size that are difficult to normalize.

Fashion Attributes

Style, color, and size are the main attribute categories in fashion and apparel. Style attributes include things like design, look, and overall aesthetics of the product. They’re very dependent on the actual product category of fashion as well. A shirt might have a slim fit attribute associated with it, whereas a belt might have a length. All these different attributes are usually labeled within a product listing and affect the consumer’s decision-making process:

Color (red, blue, sea green, etc.)

Pattern (solid, striped, checked, floral, etc.)

Material (cotton, polyester, leather, denim, silk, etc.)

Fit (regular, slim, relaxed, oversized, tailored, etc.)

Type (casual, formal, sporty, vintage, streetwear)

Color Complexity in Fashion

Color is perhaps the most visually distinctive attribute in fashion, yet it presents unique challenges for retailers. This is because color naming can vary across retailers and marketplaces. There are several major differences in color convention:

A single color can be labeled differently across brands (e.g., “navy,” “midnight blue,” “deep blue”)

Seasonal color names (e.g., “summer sage” vs. “forest green”)

Marketing-driven names (e.g., “sunset coral” vs. “pale orange”)

Size: The Other Critical Dimension

Size in fashion refers to the dimensions or measurements that determine how fashion products fit. Depending on whether the product is a clothing item, shoes, or a hat, there will be different sizing options. Types of sizes include:

Standard sizes (XS, S, M, L, XL, XXL, XXL)

Custom sizes (based on brand, retailer, country, etc.)

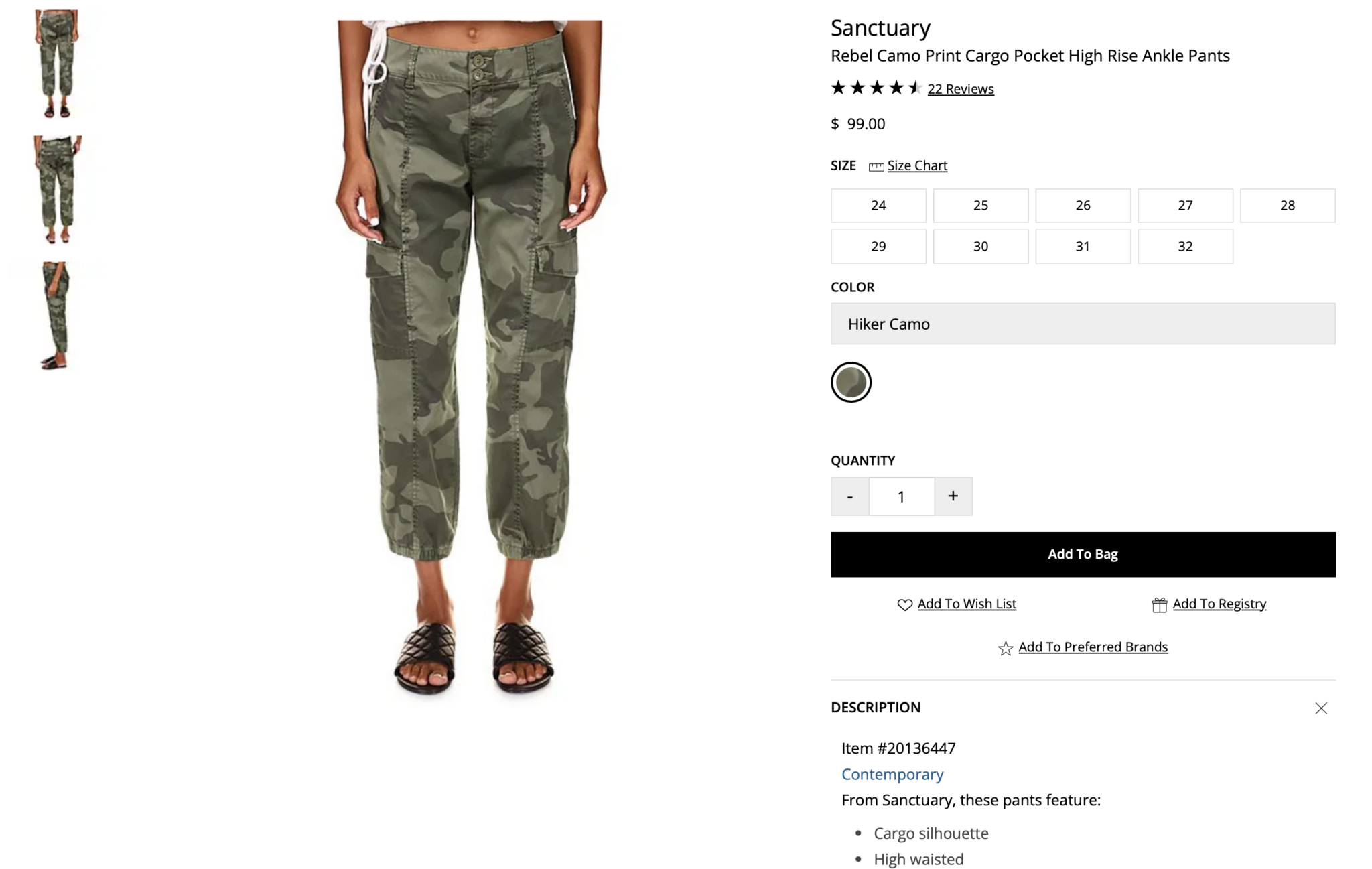

A single type of product may have different sizing labels. For instance, one pants listing may use traditional S, M, L, XL sizing, while another pants listing may use 24, 25, or 26, to refer to the waist measurement.

Size is a dynamic attribute that changes based on current trends. For example, there has recently been a significant shift towards inclusive sizing. Size inclusivity refers to the practice of selling apparel in a wide range of sizes to accommodate people of all body types. Consumers are more aware of this trend and are demanding a broader range of sizing offerings from the brands they shop from.

In the US market, in particular, some 67% of American women wear a size 14 or above and may be interested in purchasing plus-size clothing. There is a growing demand in the plus-size market for more options and a wider selection. Many brands are considering expanding their sizes to accommodate more shoppers and tap into this growing revenue channel.

Pricing Based on Size and Color

Many fashion products are priced differently based on size and color. Let’s take a look at an example of what this can look like.

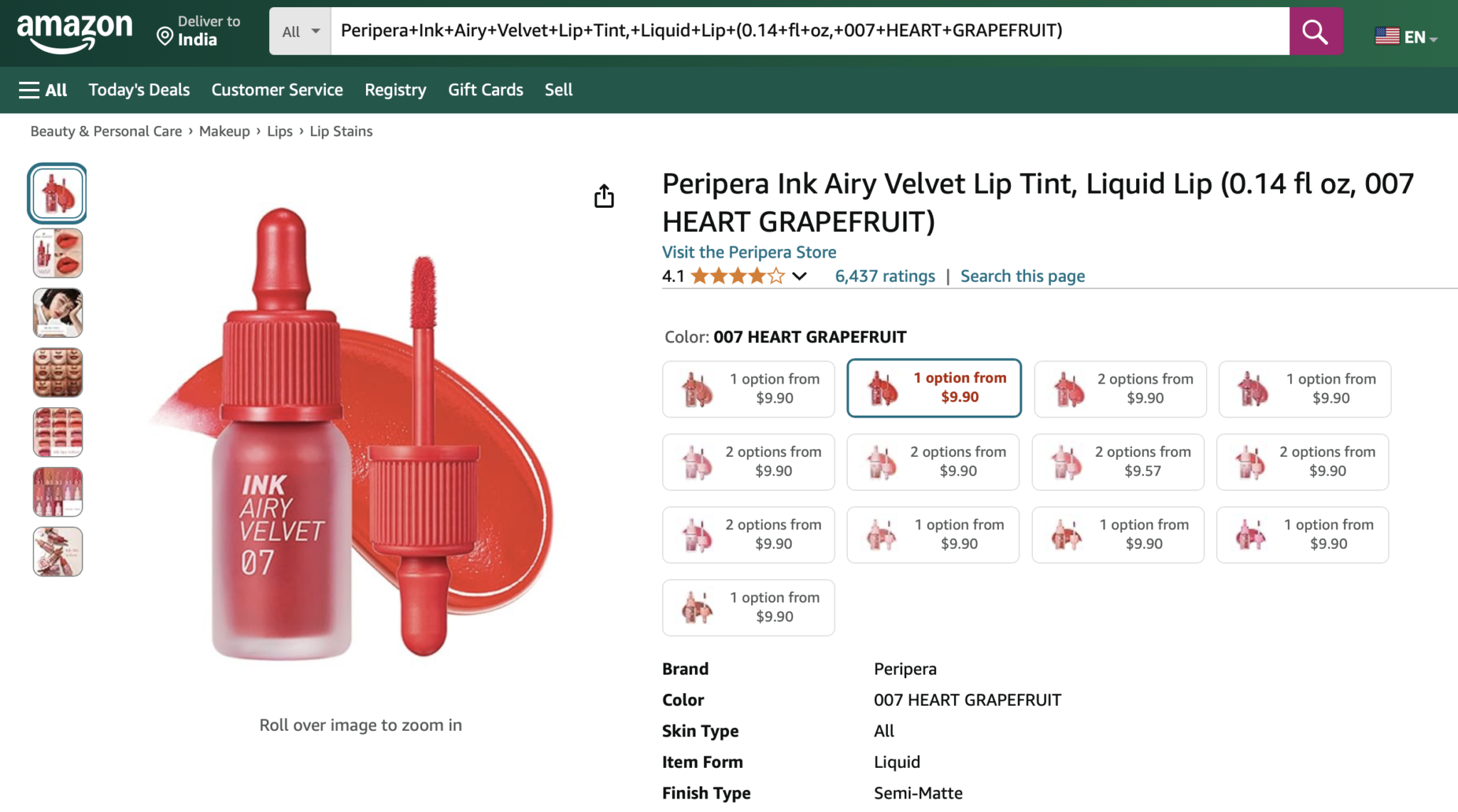

A popular beauty brand (see image) is known for its viral lip tint. While most of the color variants are priced at $9.90 on Amazon, a specific colorway option, featuring less pigmented options, is priced at $9.57. This price differential is driven by both material costs and market demand.

Different colorways (any of a range of combinations of colors in which a style or design is available) of the same product often command different prices also. This is based on:

Dye costs (some colors require more expensive processes)

Seasonal demand (traditional colors vs. trend colors)

Exclusivity (limited edition colors)

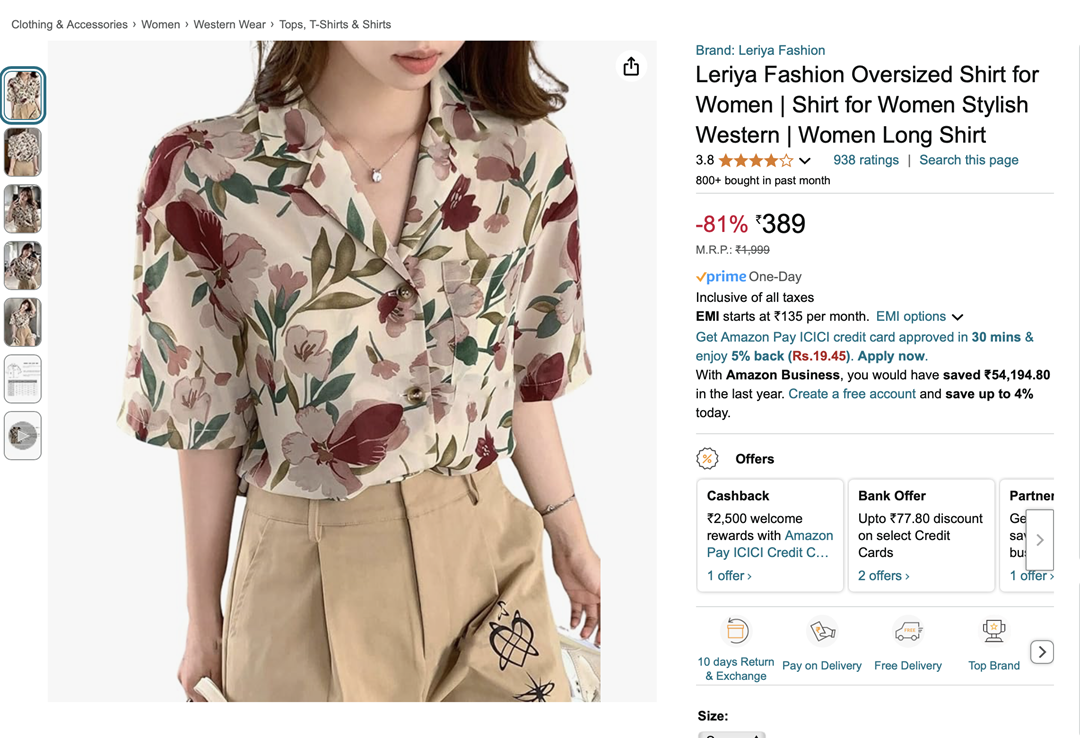

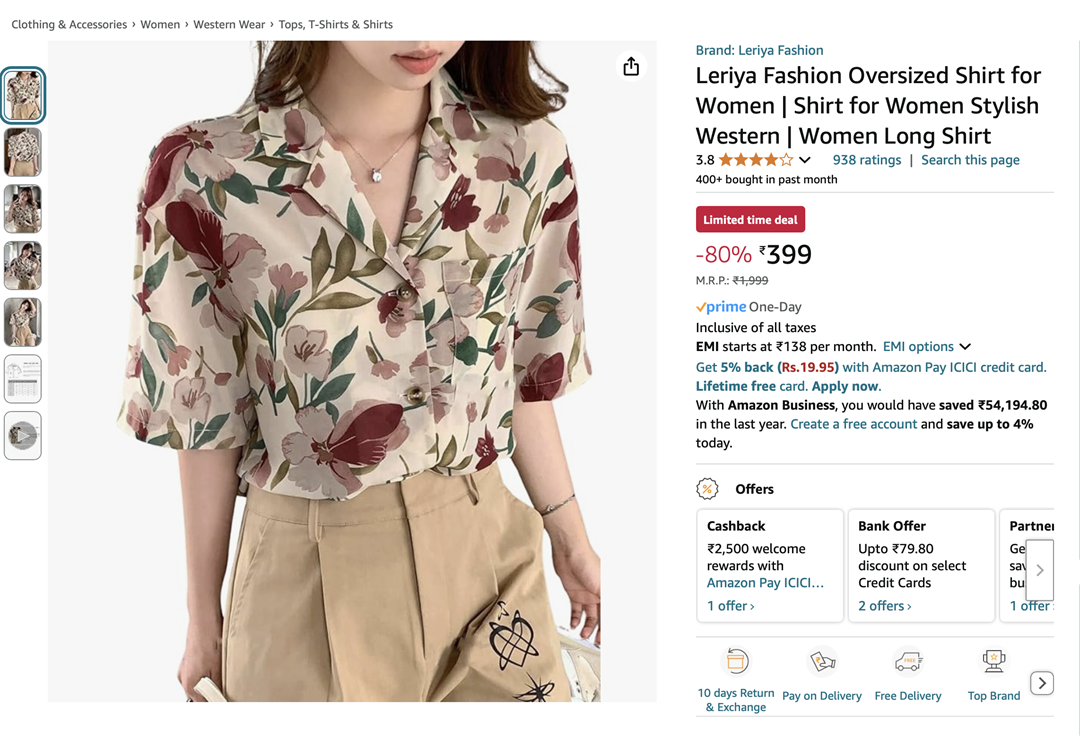

An example of price variations by size is a women’s shirt that is being sold on Amazon as shown below. For this product, there are no style attributes to choose from. The only parameter the shopper has to select is the size they’d like to purchase. They can choose from S to XL. On the top, we can see that the product in size S is ₹389. Below, the size XL version of this same shirt is ₹399. This price increase is correlated to the change in size.

So why are these same products priced differently? In an analysis of One Six, a plus-size clothing brand, several reasons for this difference in plus-size clothing were determined.

Extra material is needed, hence an increase in production costs

Extra stitching costs, hence an increase in production costs