As summer winds down, families across the US have been gearing up for the annual back-to-school shopping season. The back-to-school season has always been a significant event in the retail calendar, but its importance has grown in recent years. With inflation still impacting many households, parents and guardians are more discerning than ever about their purchases, seeking the best value for their money.

The National Retail Federation has forecasted that this season could see one of the highest levels of spending in recent years, reaching up to $86.6 billion. As shoppers eagerly stock up on back-to-school and back-to-college essentials, it’s crucial for retailers and brands to refine their pricing strategies in order to capture a larger share of the market.

To understand how retailers are responding to the back-to-school rush this season, our proprietary analysis delves into pricing trends, discount strategies, and brand visibility across major US retailers, including Amazon, Walmart, Kroger, and Target. By examining 1000 exactly matching products in popular back-to-school categories, our analysis provides valuable insights into the pricing strategies adopted by leading retailers and brands this year.

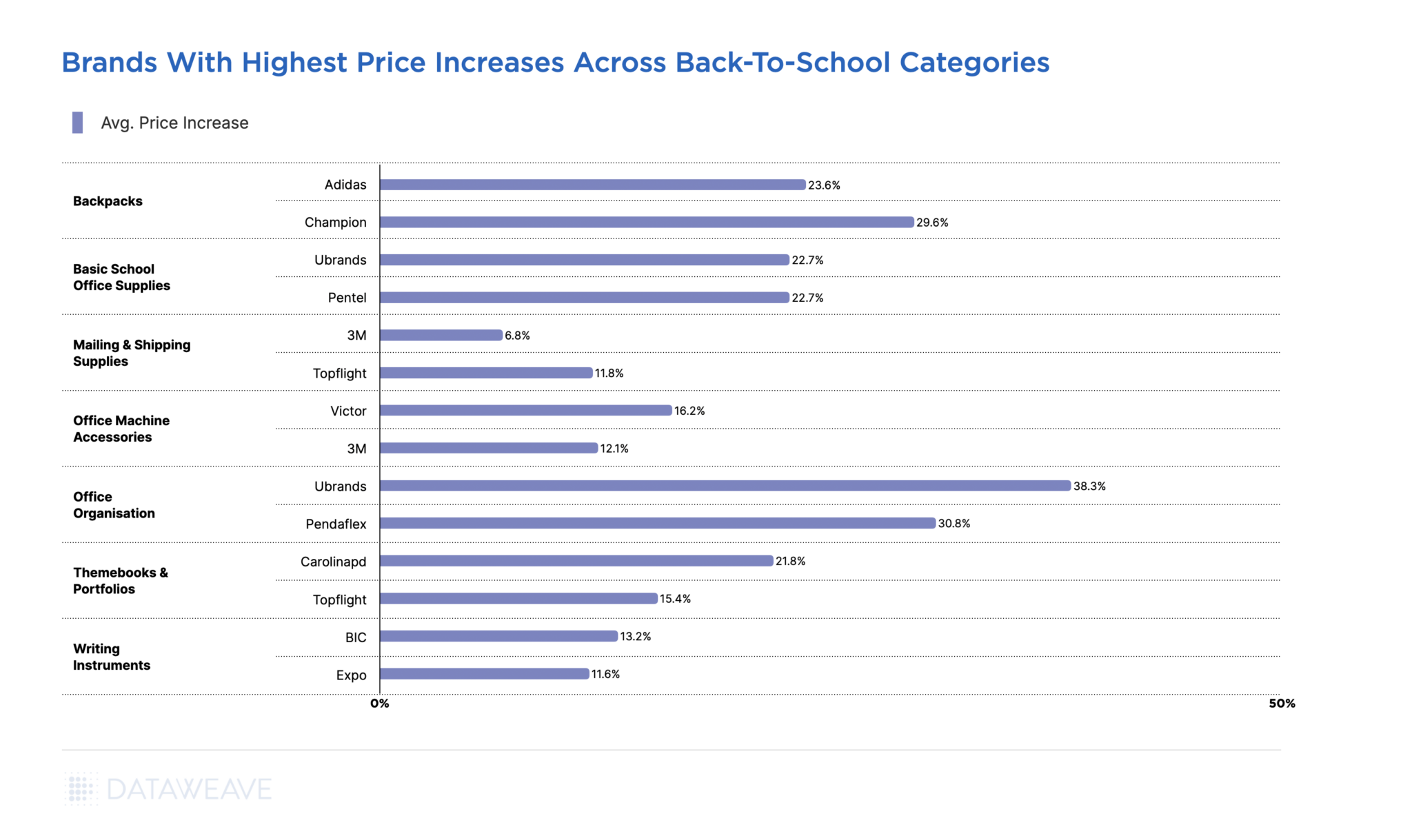

Price Changes: A Tale of Moderation

The most notable trend in our analysis is the much smaller annual price increases this year, in contrast to last year’s sharp price hikes. This shift is a reaction to growing consumer frustration about rising prices. After enduring persistent inflation and steep price growth, which peaked last year, consumers have become increasingly frustrated. As a result, retailers have had to scale back and implement more moderate price increases this year.

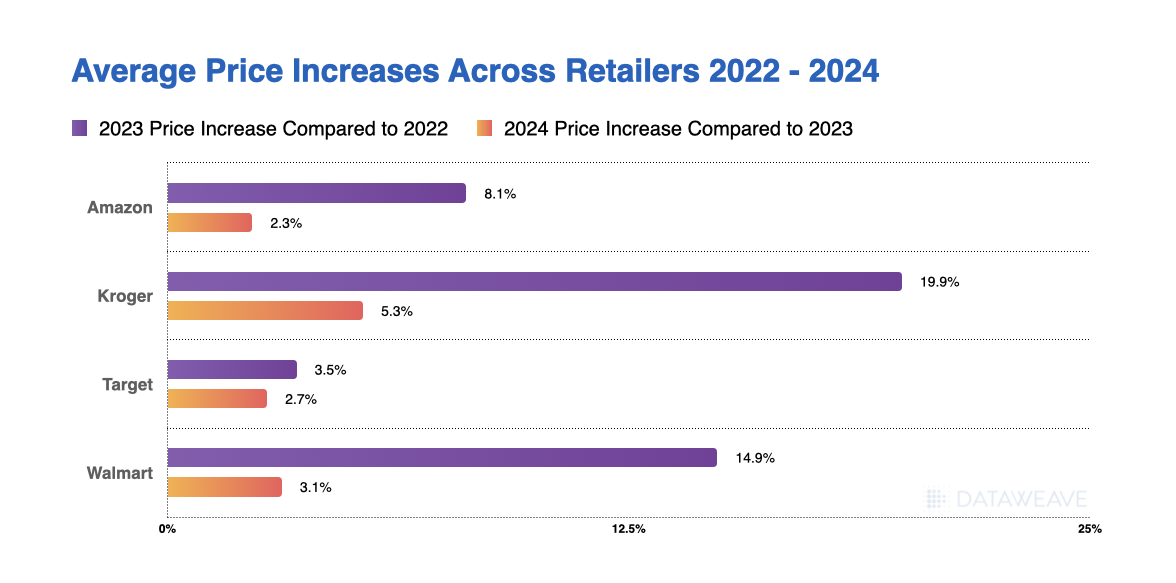

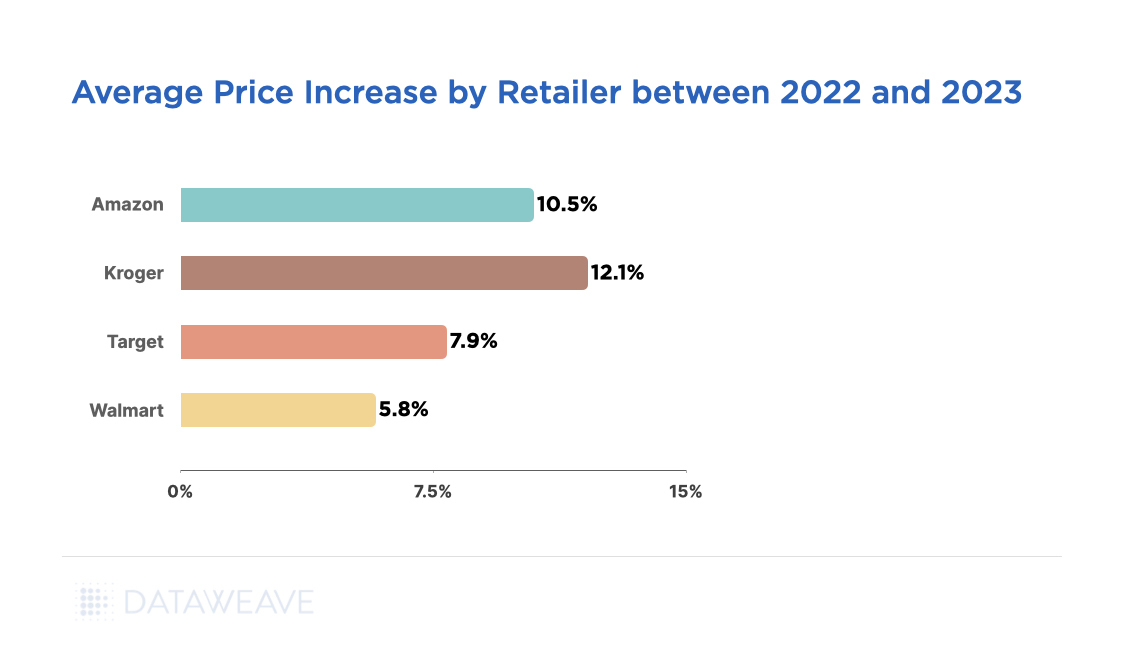

Kroger led the pack with the highest price increases, showing a 5.3% increase this year, which follows a staggering 19.9% rise last year. Walmart’s dramatic price increase of 14.9% is now followed by a muted 3.1% hike. Amazon and Target demonstrated a similar pattern of slowing price hikes, with increases of 2.3% and 2.7% respectively in the latest period. This trend indicates that retailers are still adjusting to increased costs but are also mindful of maintaining customer loyalty in a competitive market.

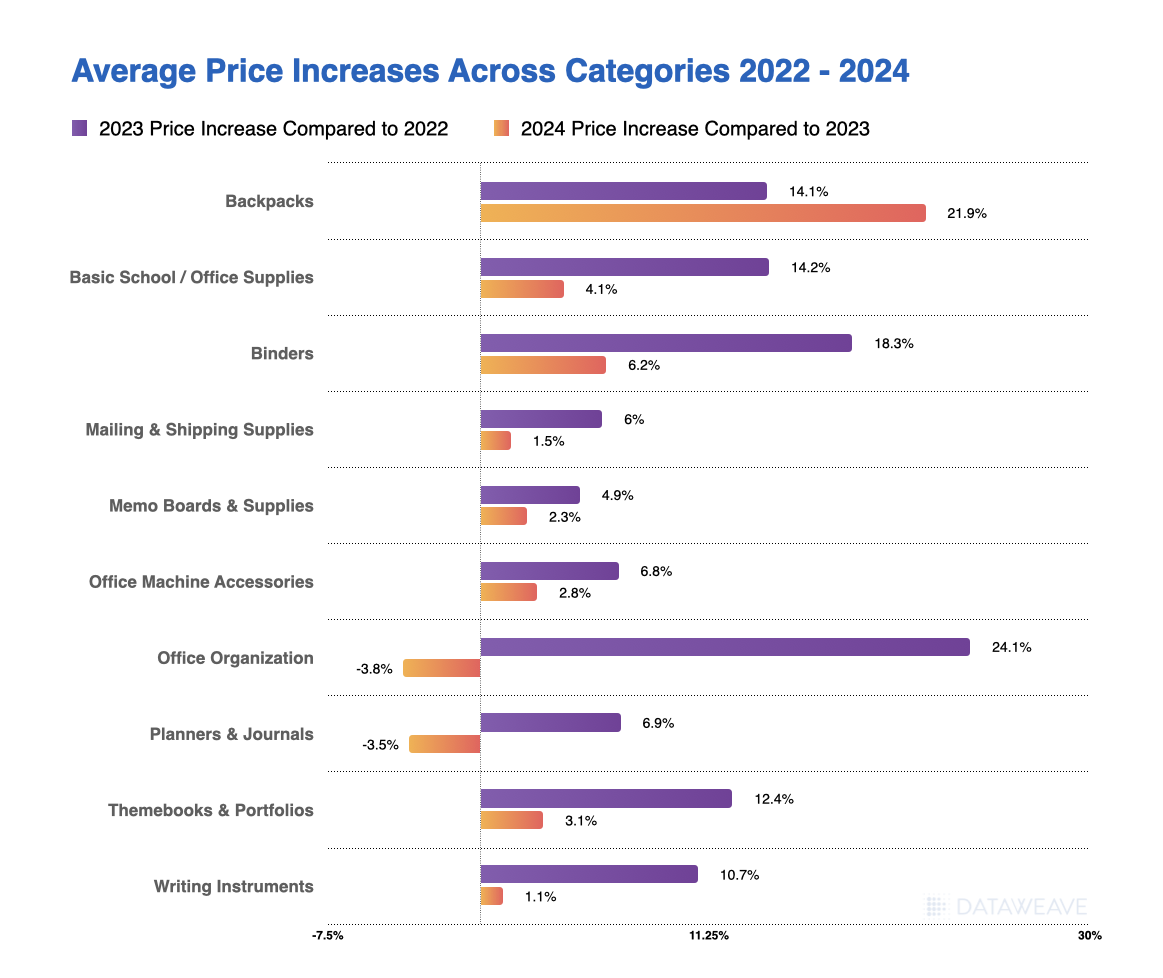

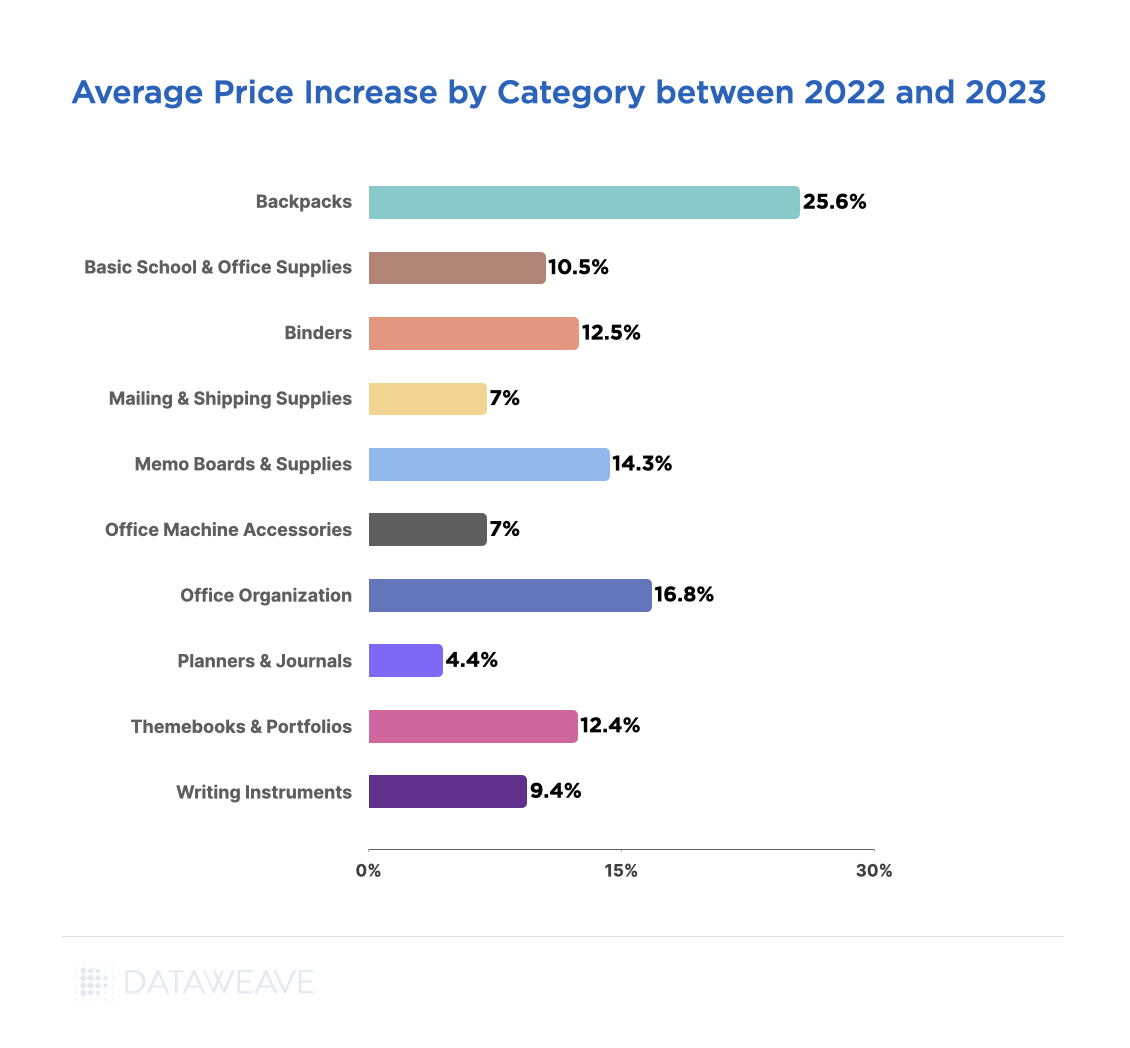

When examining specific product categories, we observe diverse pricing trends. Electronics and apparel saw the largest price increases between 2022 and 2023, likely due to supply chain disruptions and volatile demand. However, the pace of these increases slowed in 2024, indicating a gradual return to more stable market conditions. Notably, backpacks remain an outlier, with prices continuing to rise sharply by 22%.

Interestingly, some categories, such as office organization and planners, experienced a price decline in 2024. This could signal an oversupply or shifting consumer preferences, presenting potential opportunities for both retailers and shoppers.

Brand Visibility: The Search for Prominence

In the digital age, a brand’s visibility in online searches can significantly impact its success during the back-to-school season. Our analysis of the share of search across major retailers provides valuable insights into brand prominence and marketing effectiveness.

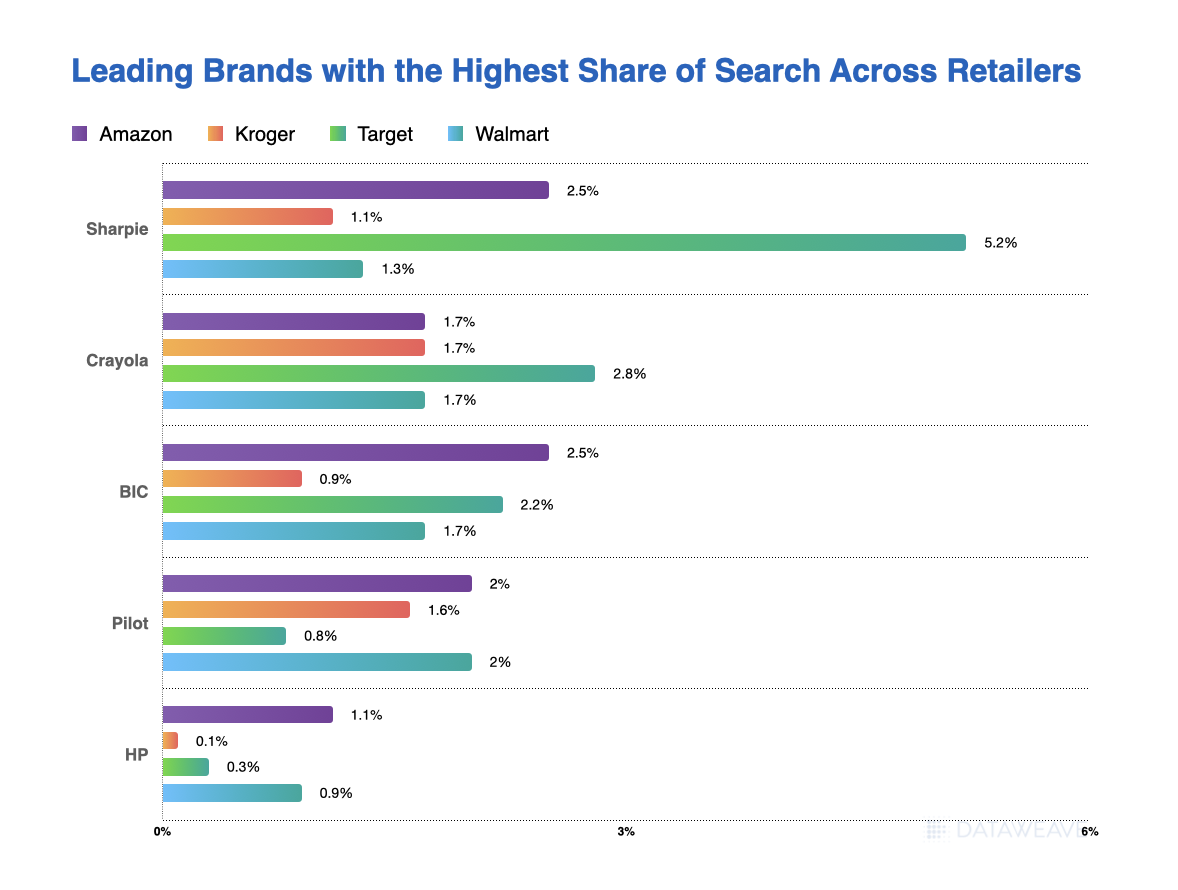

Sharpie and Crayola emerged as the strongest performers overall, with particularly high visibility on Target. This suggests strong consumer recognition and demand for these traditional school supply brands. BIC showed strength on Amazon and Target but lagged on Kroger, while Pilot maintained a more balanced presence across most retailers.

The variation in brand visibility across retailers also hints at potential partnerships or targeted marketing strategies. For instance, Sharpie’s notably high visibility on Target (5.16% share of search) could indicate a specific partnership.

Talk to us to get more insights on the most prominent brands broken down by specific product categories.

Navigating the 2024 Back-to-School Landscape

As we look ahead to the 2024 back-to-school shopping season, several key takeaways emerge for retailers and brands:

Price sensitivity remains high, but the rate of increase is moderating. Retailers should carefully balance the need to cover costs with maintaining competitive pricing.

Strategic discounting can be a powerful tool, especially for lesser-known brands looking to gain market share. However, established brands would need to rely more on quality, visibility, and brand loyalty.

Online visibility is crucial. Brands should invest in strong SEO and retail media strategies, tailored to different retail platforms.

Category-specific strategies are essential. What works for backpacks may not work for writing instruments, so a nuanced approach is key.

Retailers and brands should be prepared for potential shifts in consumer behavior, such as increased demand for value-priced items or changes in category preferences.

By staying attuned to these trends and remaining flexible in their strategies, businesses can position themselves for success in the competitive back-to-school retail landscape of 2024. As always, the key lies in understanding and responding to consumer needs while maintaining a keen eye on market dynamics.

Stay tuned to our blog to know more about how retailers can stay aware of changing pricing trends. Reach out to us today to learn more.

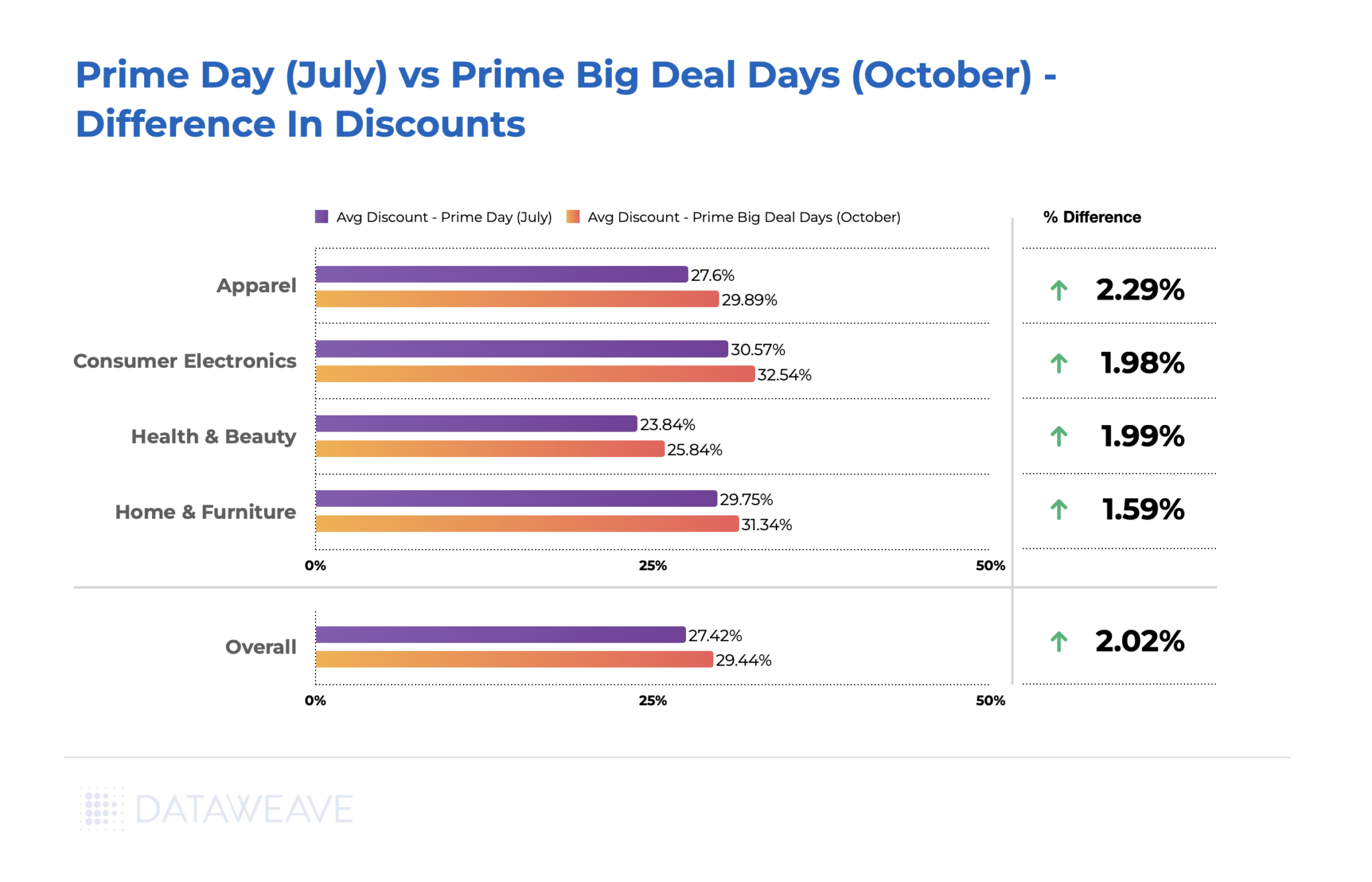

As the retail landscape continues to evolve, events like Amazon Prime Day have become more than just shopping extravaganzas—they’ve transformed into strategic battlegrounds where retailers assert their market positions and brand identities. Prime Day 2024 was no exception, serving as a crucial moment for retailers to showcase their pricing prowess, customer loyalty programs, and category expertise.

In an era where consumer expectations for deals are at an all-time high, the impact of Prime Day extends far beyond Amazon’s ecosystem. Retailers like Walmart, known for its “everyday low prices,” Target with its emphasis on style and value, and Best Buy, the electronics specialist, have all adapted their strategies to compete. These companies didn’t just react to Prime Day; they proactively launched their own pre-emptive sales events, with Target Circle Week, Walmart July Deals and more, effectively extending the shopping bonanza and challenging Amazon’s dominance.

For Prime Day, we analyzed over 47,000 SKUs across major retailers and product categories to publish insights on Amazon’s pricing strategies as well as the performance of leading consumer brands. Here, we go further to delve into the discounts offered (or not offered) by Amazon’s competitors during Prime Day. Our analysis reveals that some retailers chose to compete on price during the sale for certain categories, while others did not.

Below, we highlight our findings for each product category. The Absolute Discount is the total discount offered by each retailer during Prime Day compared to the MSRP. These are the discounts consumers are familiar with, displayed on retail websites prominently during sale events. The Additional Discount, on the other hand, is the reduction in price during Prime Day compared to the week prior to the sale, revealing the level of price markdowns by the retailer specific to a sale event.

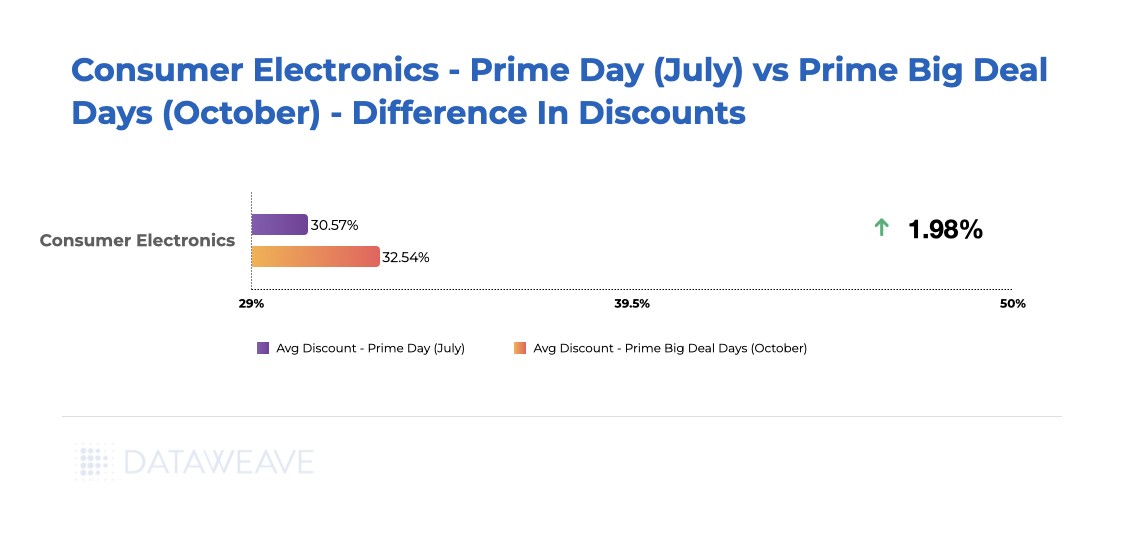

Consumer Electronics

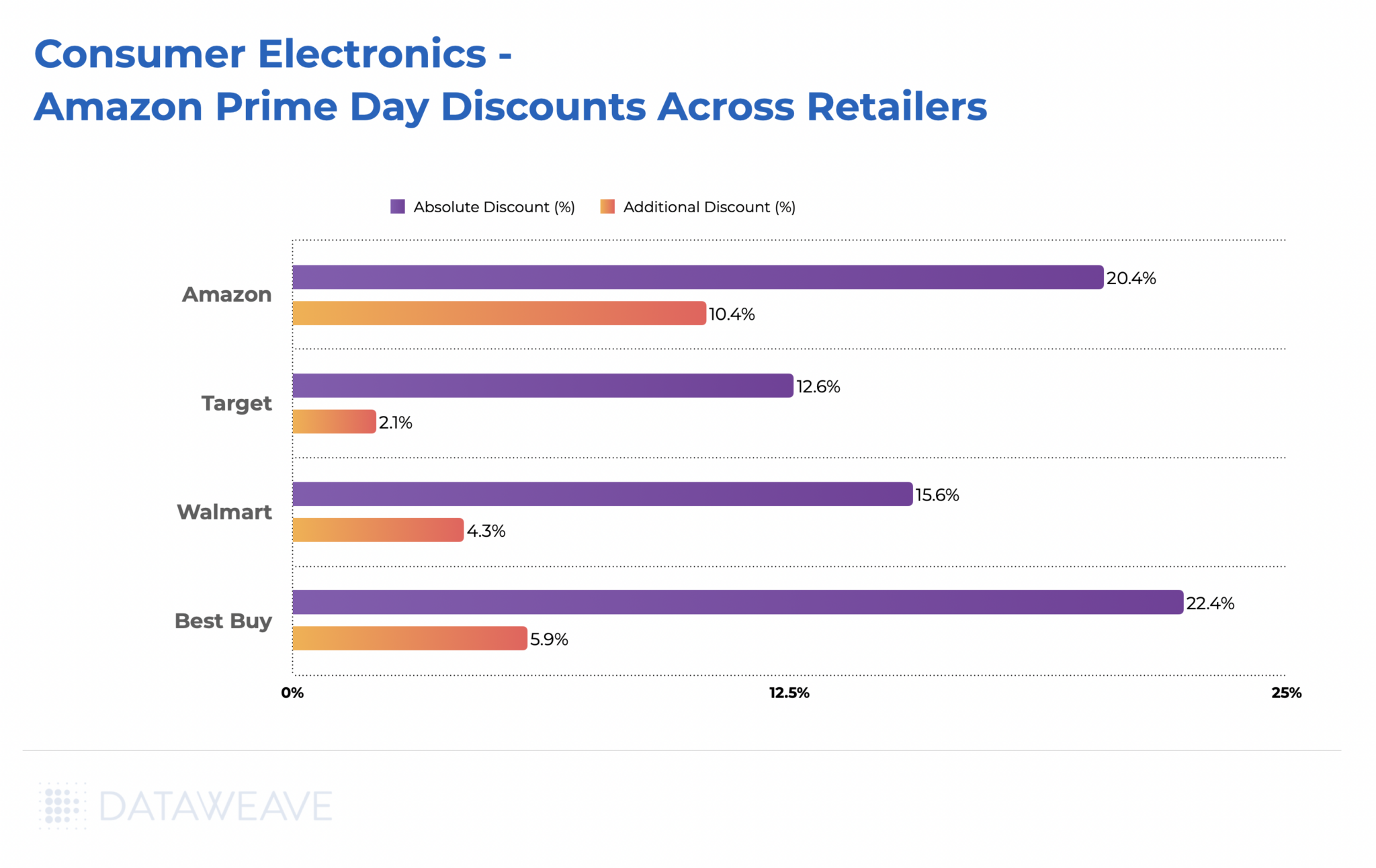

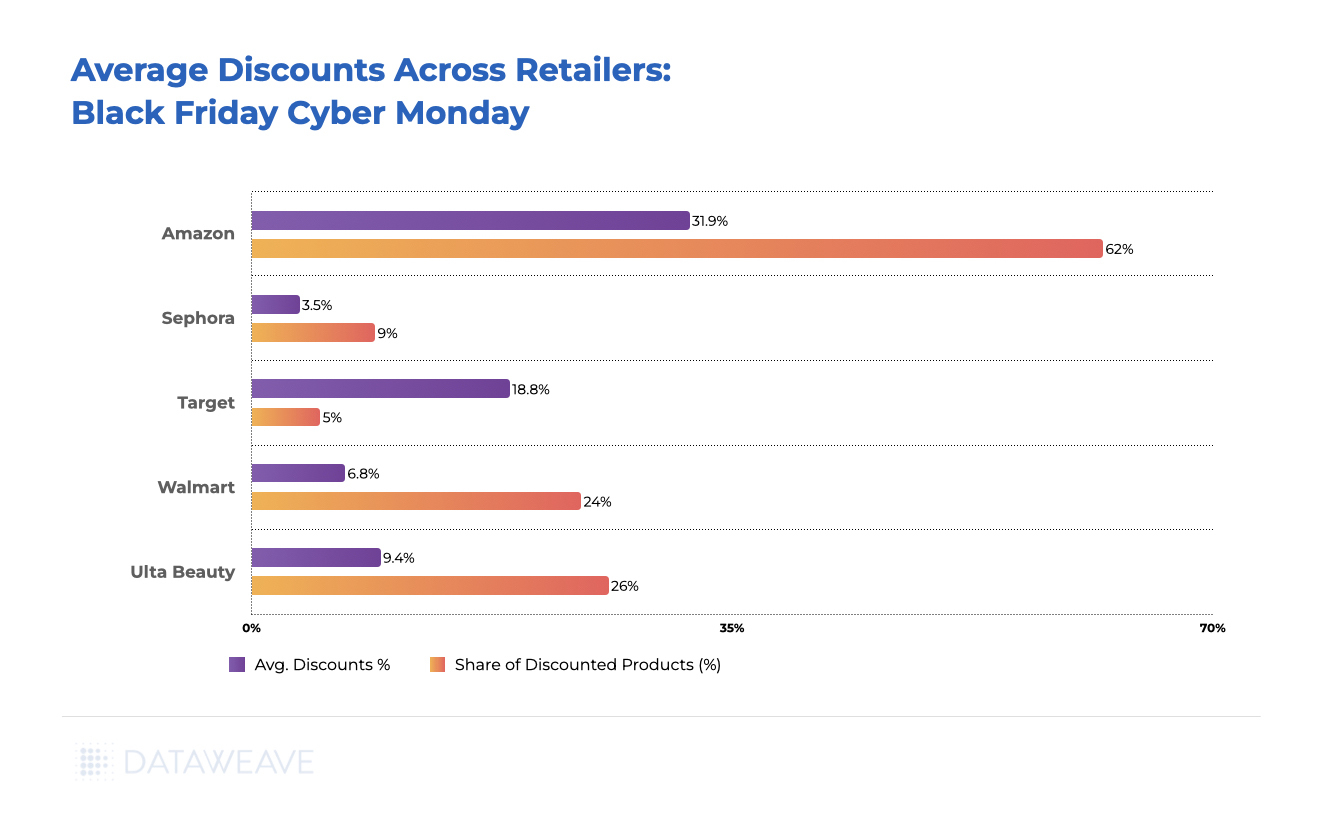

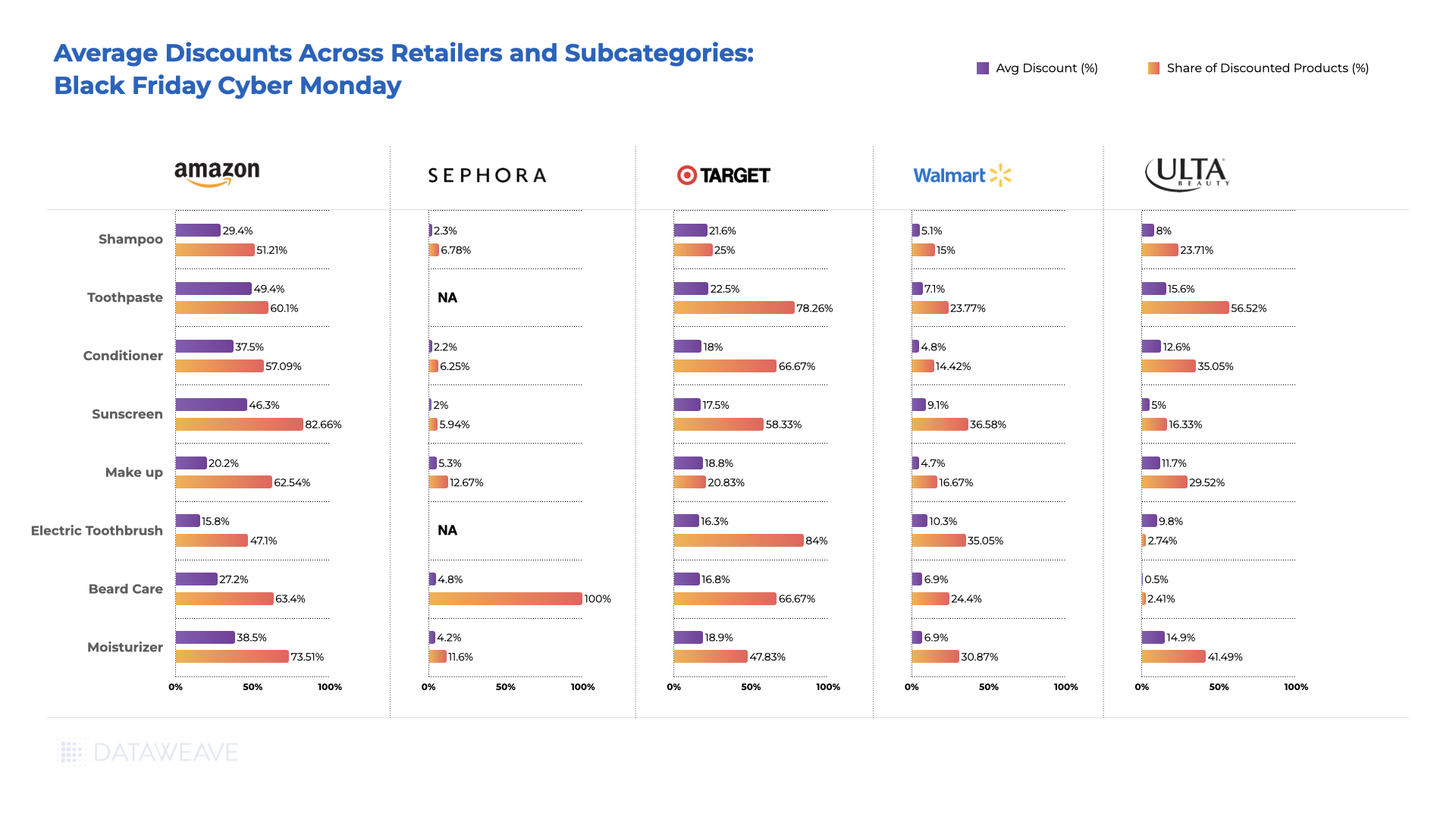

In the Consumer Electronics category, Best Buy stood out as a strong competitor, offering an Additional Discount of 5.9%—the highest among all competitors analyzed. This is unsurprising, as Best Buy is well-known for its focus on consumer electronics and is likely aiming to reinforce its reputation for offering attractive deals in order to maintain its strong consumer perception in the category.

Walmart was a close second with a 4.3% Additional Discount while Target reduced its prices by only 2% during the sale.

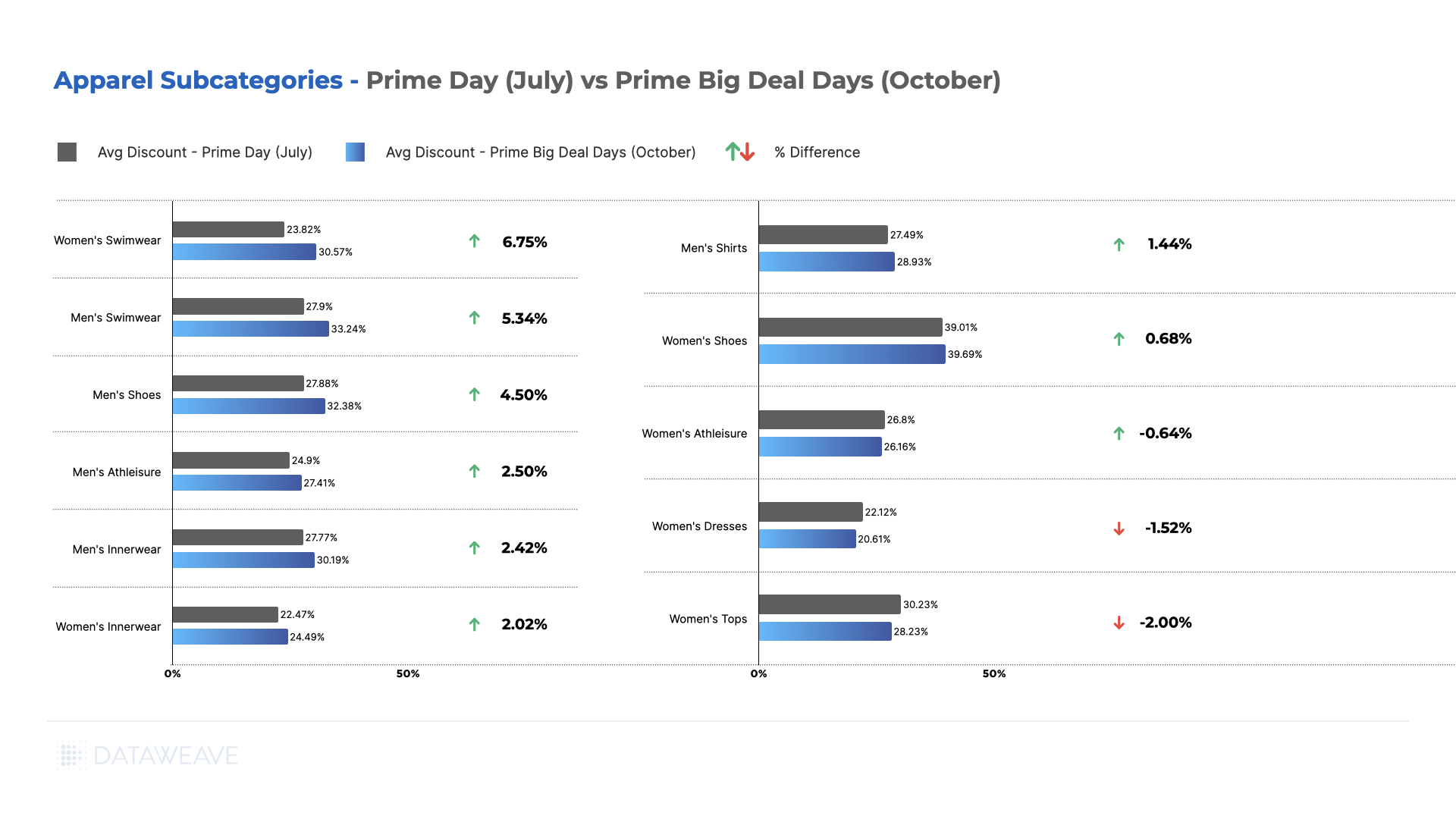

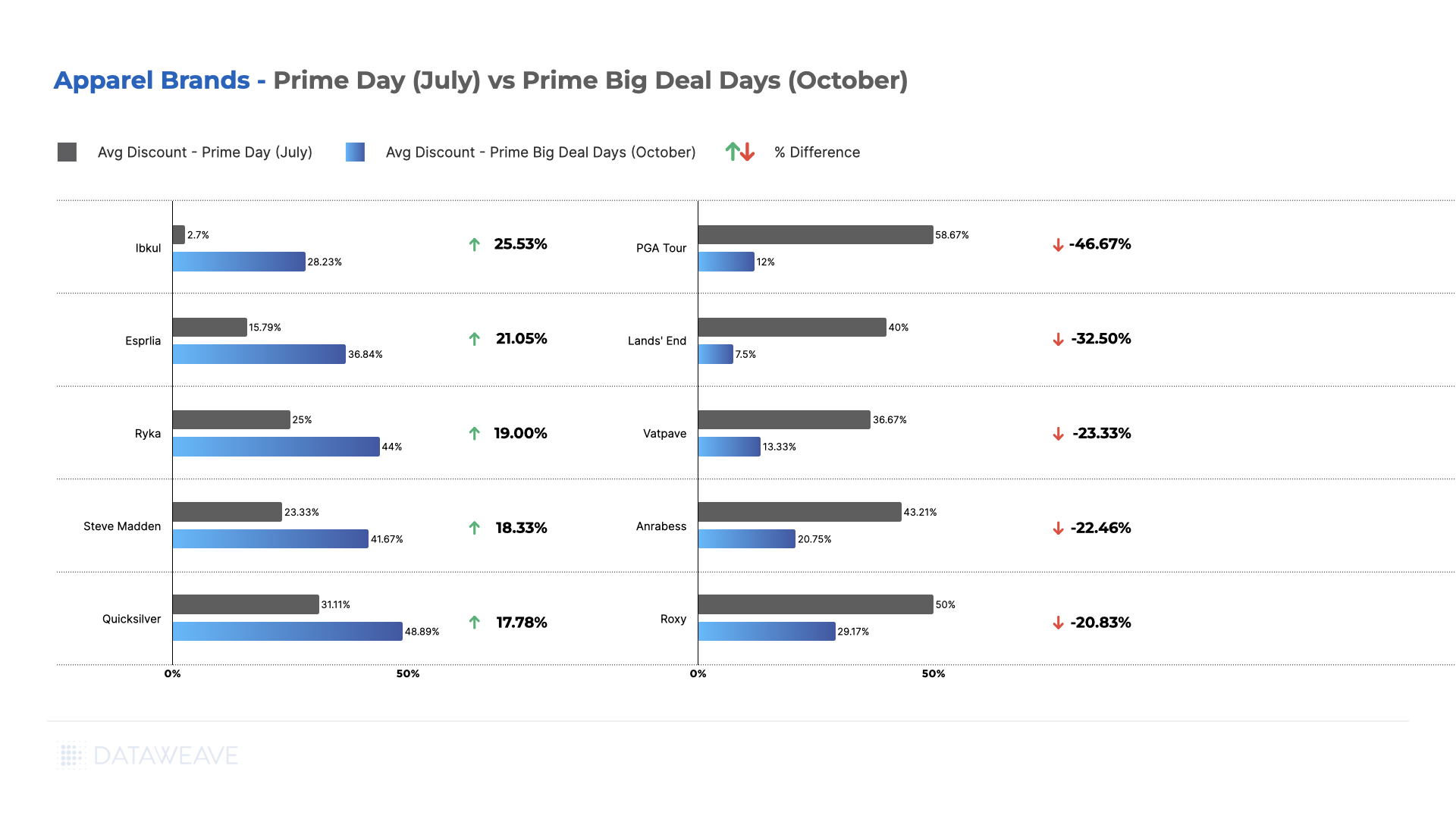

Apparel

In the Apparel category, Walmart’s Additional Discount was 3.1%, demonstrating its willingness to be priced competitively on a small portion of its assortment during the sale, without compromising much on margins.

Target, on the other hand, opted out of competing with Amazon on price during the sale, choosing instead to maintain its Absolute Discount level of around 11%.

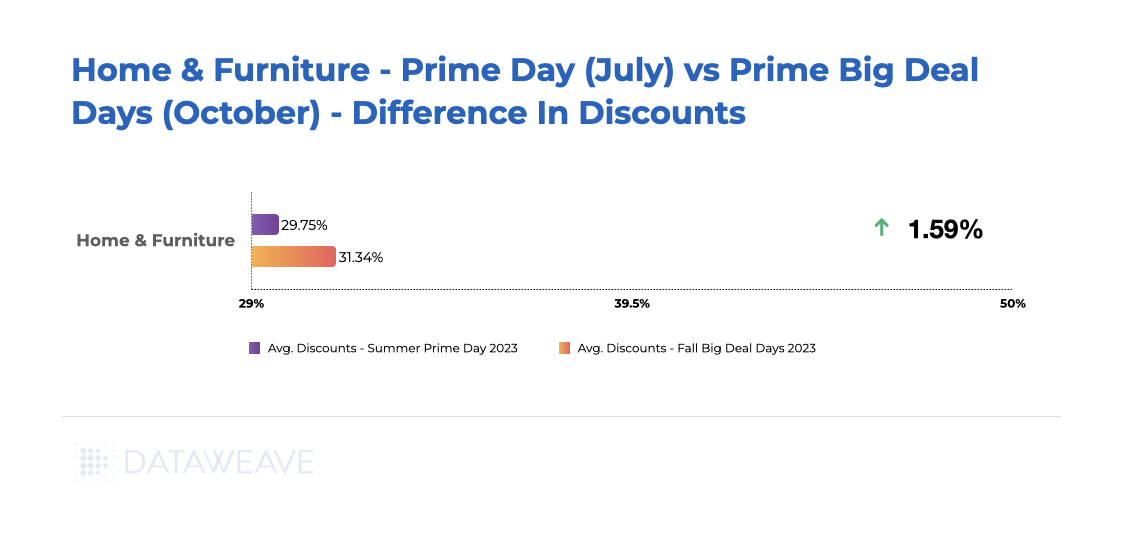

Home & Furniture

The Home & Furniture category showcased diverse strategies from retailers. Specialty furniture retailers such as Overstock and Home Depot provided Additional Discounts of 3.9% and 2.5%, respectively, compared to Amazon’s 6.9%. This indicates a clear intent to maintain market share and remain top-of-mind for consumers despite Amazon’s competitive pricing.

Although Target didn’t significantly lower its prices during the sale, its Absolute Discount remains substantial at 18.9%. This suggests that Target’s markdowns were already steep before the event, which could explain the lack of further reductions during the sale.

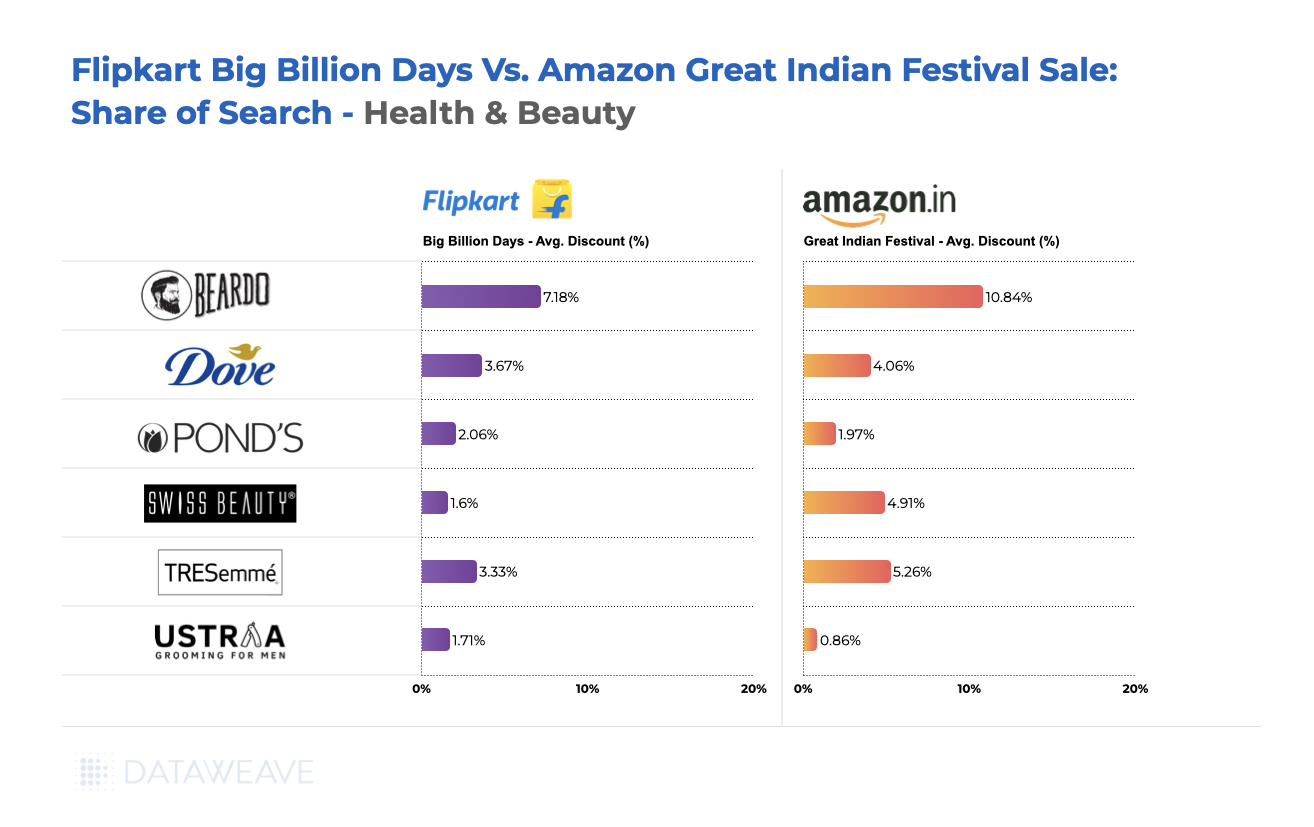

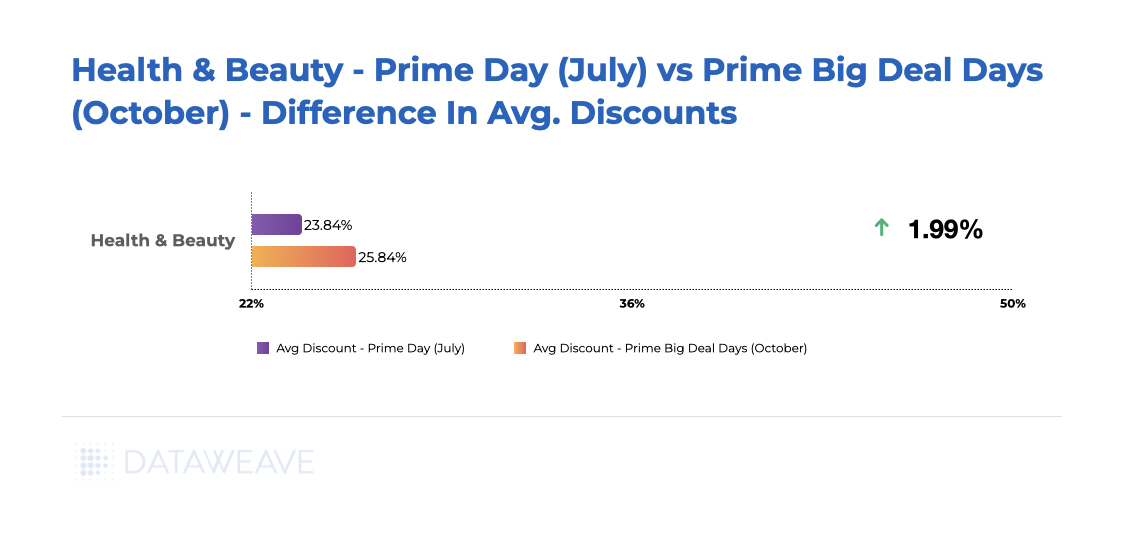

Health & Beauty

The Health & Beauty category saw minimal participation from Amazon’s competitors, with the exception of Sephora, which reduced prices by 3.7% during Prime Day.

Ulta Beauty chose not to adjust its prices, likely reflecting its strategy to uphold a premium brand image. Walmart, on the other hand, offered a modest Additional Discount of 2% on select items. Given Walmart’s generally affordable product range, its total discount remained relatively low, around 3.5%.

In Conclusion

During Prime Day, Walmart was the only major retailer that made an effort to compete, albeit modestly. Target, on the other hand, largely chose not to offer any additional markdowns. However, several category-specific retailers, such as Best Buy in Consumer Electronics, Overstock and Home Depot in Furniture, and Sephora in Health & Beauty, aimed to retain market share by providing notable discounts.

What this means for consumers is that even on Amazon’s Prime Day, it’s not a bad idea to compshop to identify the best deal.

For retailers, the key takeaway is the importance of quickly analyzing competitor pricing and making agile, data-driven decisions to improve both revenues and margins. By utilizing advanced pricing intelligence solutions like DataWeave, retailers can optimize their discount strategies, better navigate pricing complexities, and drive revenue growth — all while staying prepared for major shopping events and beyond.

As the dust settles on Amazon’s 8th Prime Day extravaganza in India, held on July 20-21, 2024, the eCommerce giant has once again shattered records. This year’s event saw unprecedented engagement, with 24% more Prime members participating compared to 2023, marking the highest-ever Prime member involvement in the sale’s history.

At DataWeave, we’ve conducted an extensive analysis of this landmark event, examining over 47,000 SKUs across major categories for Flipkart and Amazon to uncover compelling insights into pricing strategies, competitive positioning, and emerging trends in the Indian eCommerce space. This follows our comprehensive analysis of Prime Day in the USA across categories and brands, which readers can explore for a global perspective on Amazon’s strategies.

Key Highlights:

Tier-2 Cities Drive Growth: This year’s exponential growth was notably fueled by orders from tier-2 cities, highlighting the expanding reach of eCommerce in India.

Swift Deliveries: Most Prime members’ orders from metros were delivered the same day or the next, while tier-2 cities saw deliveries in less than 2 days, highlighting the importance of delivery time when it comes to purchase decisions.

Brand Participation: Over 450 top Indian and global brands participated, including Intel, Samsung, OnePlus, and Puma, alongside 3,200 new product launches from small and medium Indian businesses. This highlights Amazon’s policy to promote small, local businesses globally in 2024.

Premium Products in Demand: Despite modest discounts across electronics and similar offerings, consumers chose to purchase premium products during Prime Day. With financial flexibility and no-cost EMI options, Indian consumers, especially Gen Z and millennials, are now ready to invest in premium products and experiences.

Our analysis focused on both the Additional Discounts offered during Prime Day (calculated relative to prices the week prior to the event), highlighting the event’s genuine benefits, and the Absolute Discounts offered during Prime Day, representing the total markdown relative to the MRP.

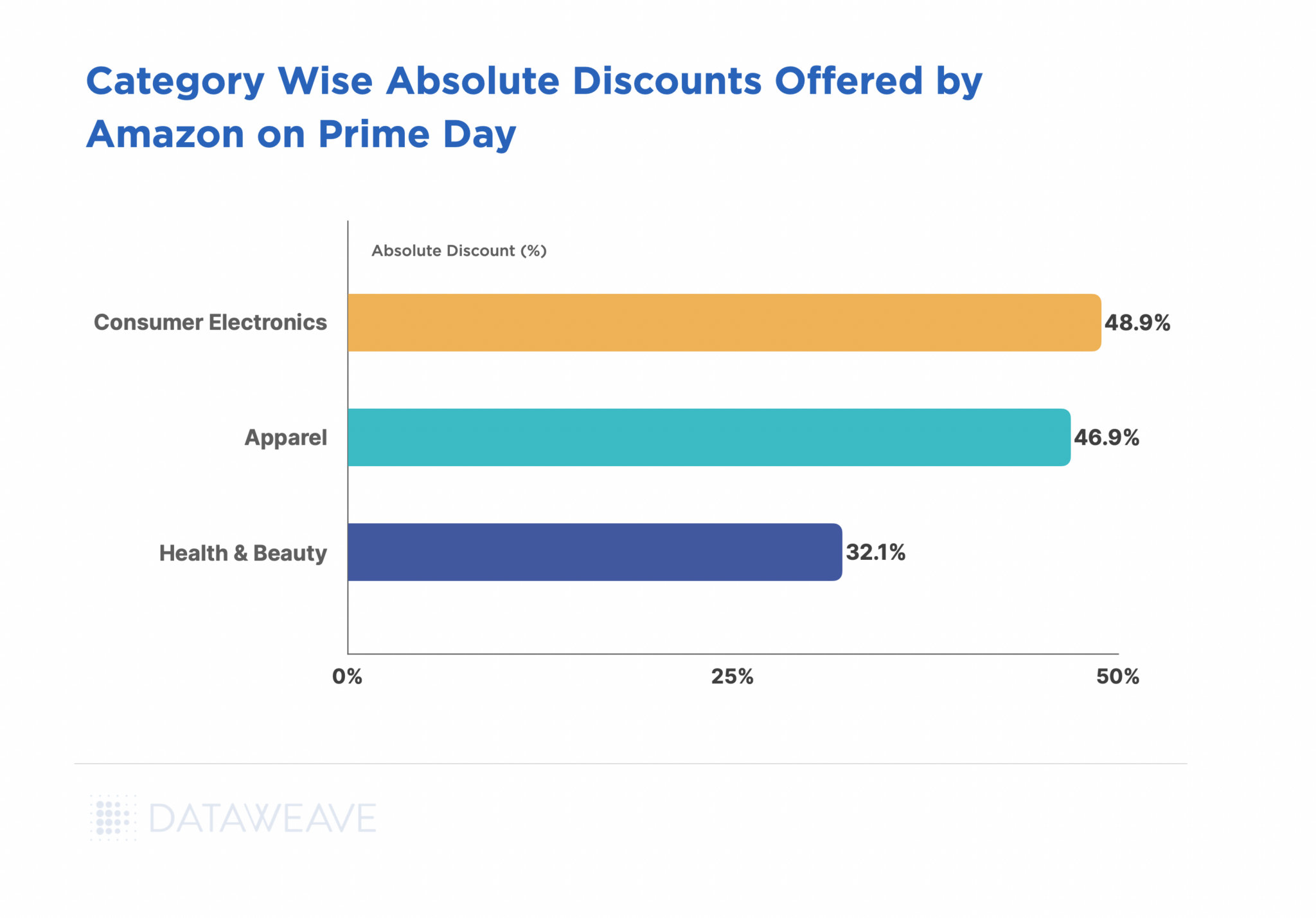

Cross-Category Discount Strategy

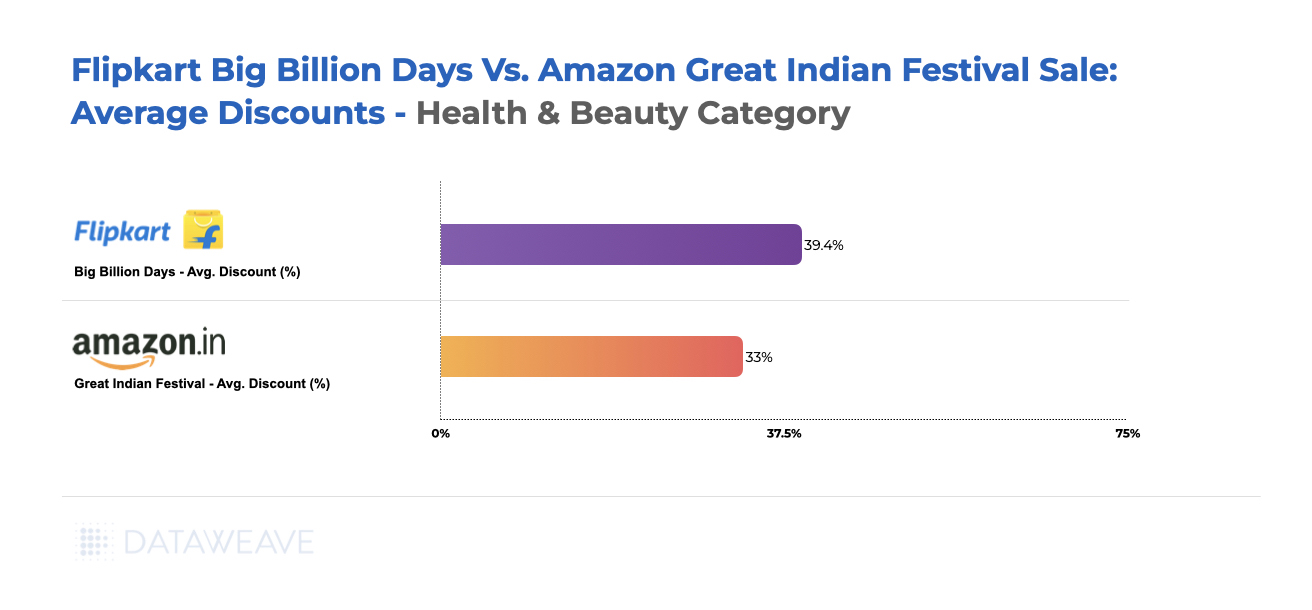

Our analysis this year reveals that the Consumer Electronics category saw the highest Absolute Discounts with an average of 48.9%, closely followed by Apparel at 46.9%. The Health & Beauty category had the lowest Absolute Discount at 32.1%.

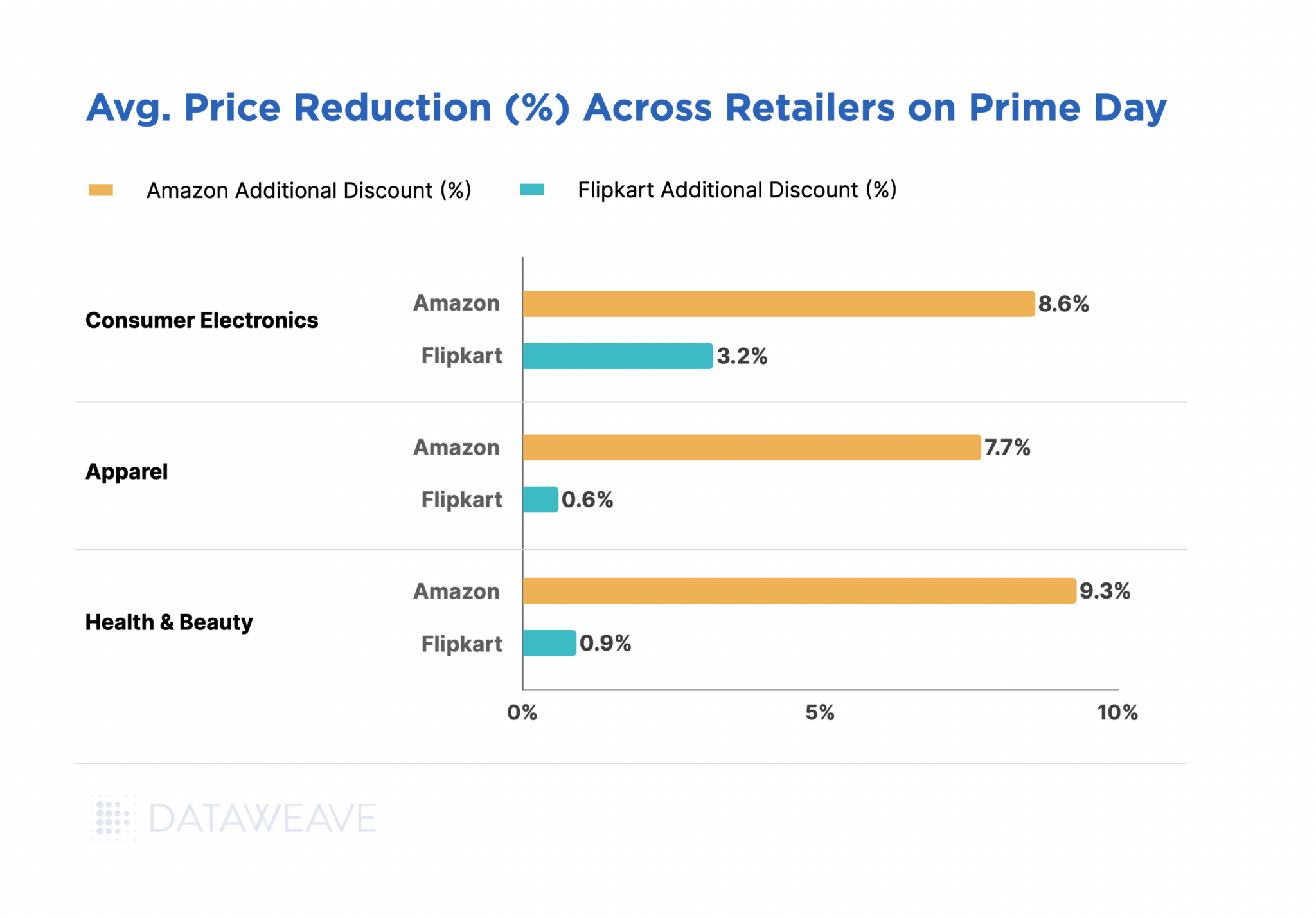

However, Amazon offered the highest Additional Discount in Health & Beauty at 9.3%. Electronics and Apparel had additional discounts of 8.6% and 7.7% respectively.

Overall, Flipkart chose to not compete aggressively with Amazon during Prime Day this year. Only in Electronics did Flipkart offer an additional discount of 3.2% during the sale. Price changes in Apparel and Health & Beauty were negligible.

Category Deep Dive

Consumer Electronics

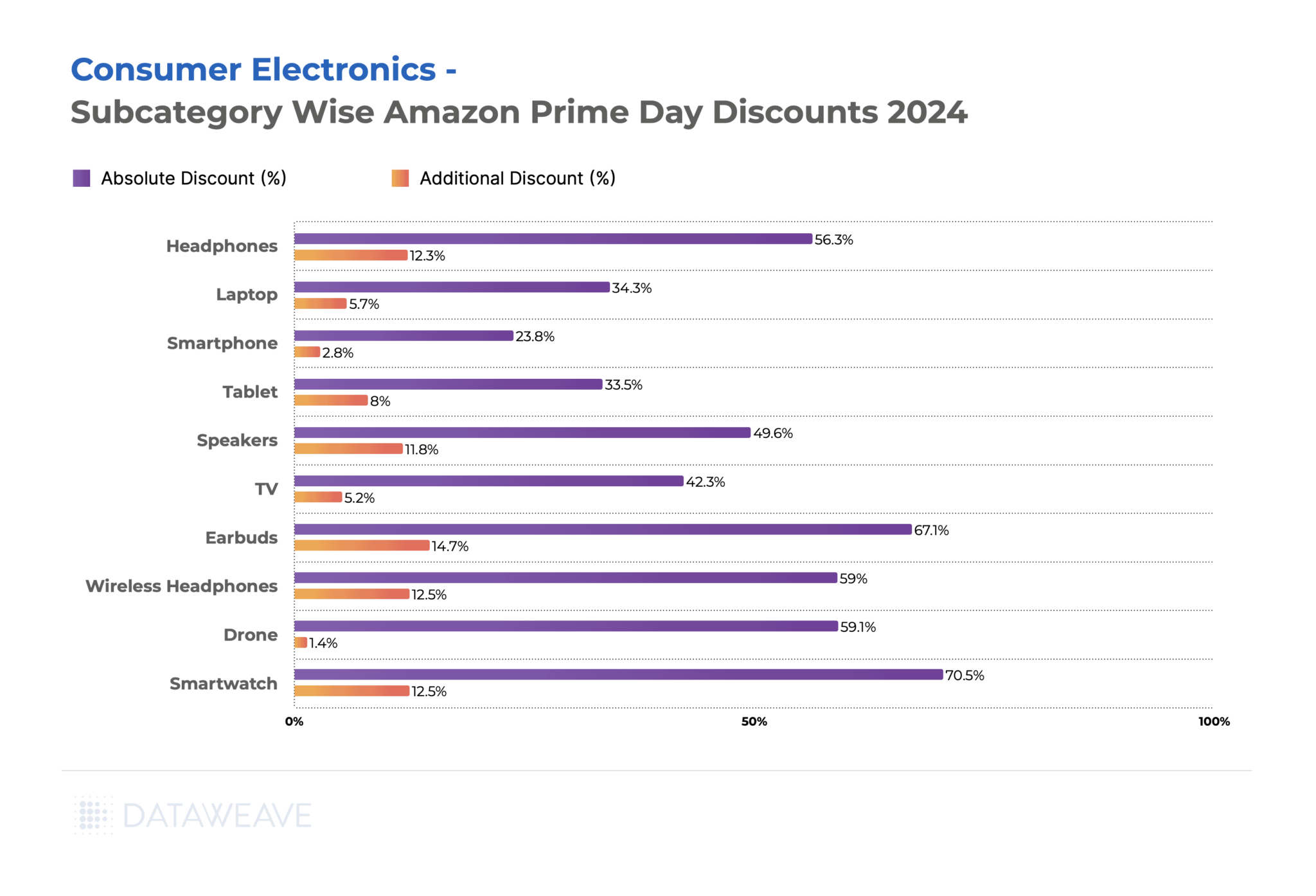

In Electronics, Earbuds (14.7%) and Wireless Headphones (12.5%) saw the highest Additional Discounts on Amazon, likely due to high demand for personal audio devices. Smartwatches followed closely at 12.5%, indicating a strong push in the wearable technology sector.

Larger electronic appliances like TVs saw more modest Additional Discounts (5.2%), despite a significant Absolute Discount (42.3%).

Smartphones, interestingly, had the lowest Additional Discount (2.8%) among the subcategories, potentially due to their already competitive pricing or brand-specific strategies.

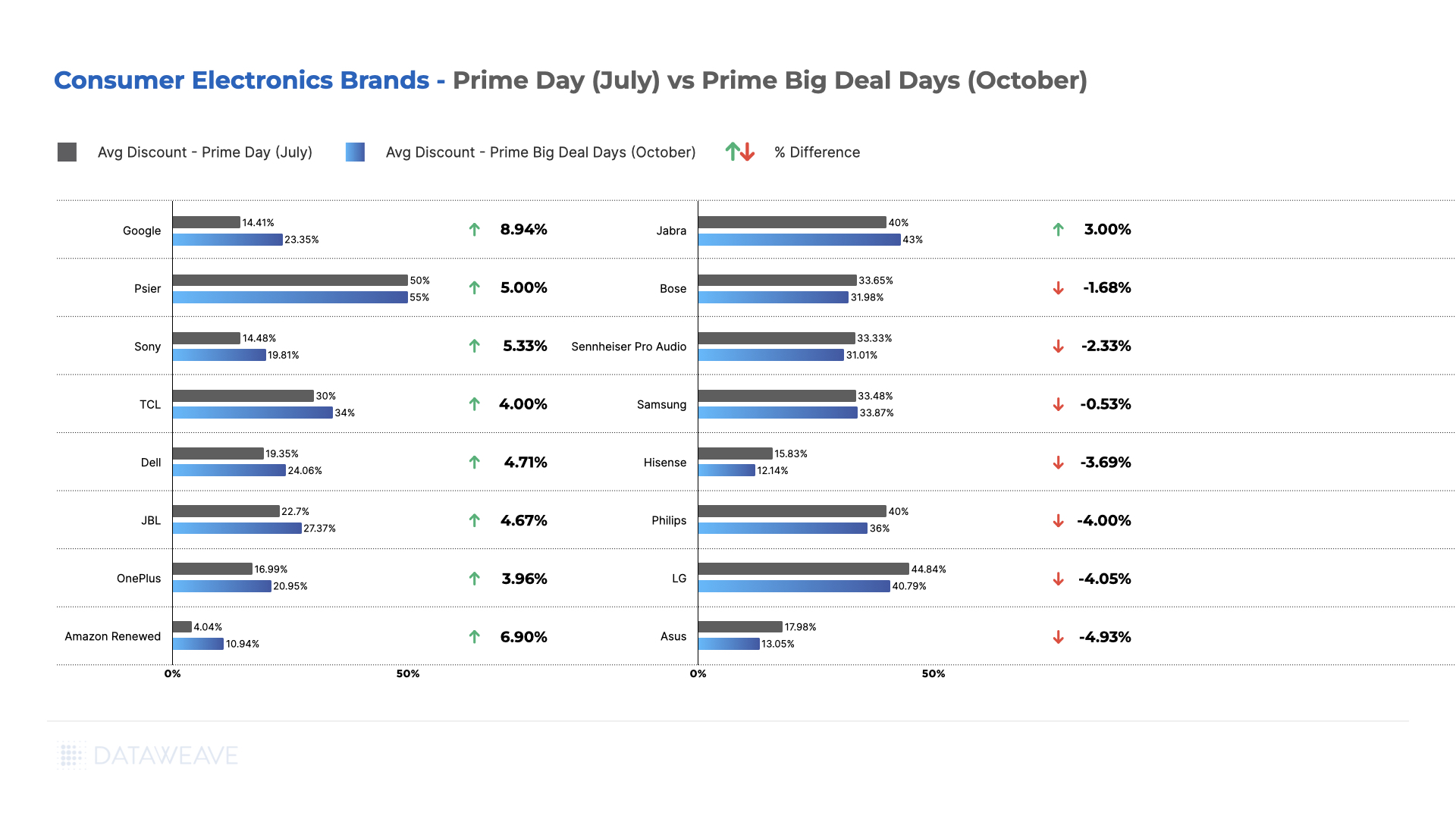

Brand-level Insights in Consumer Electronics

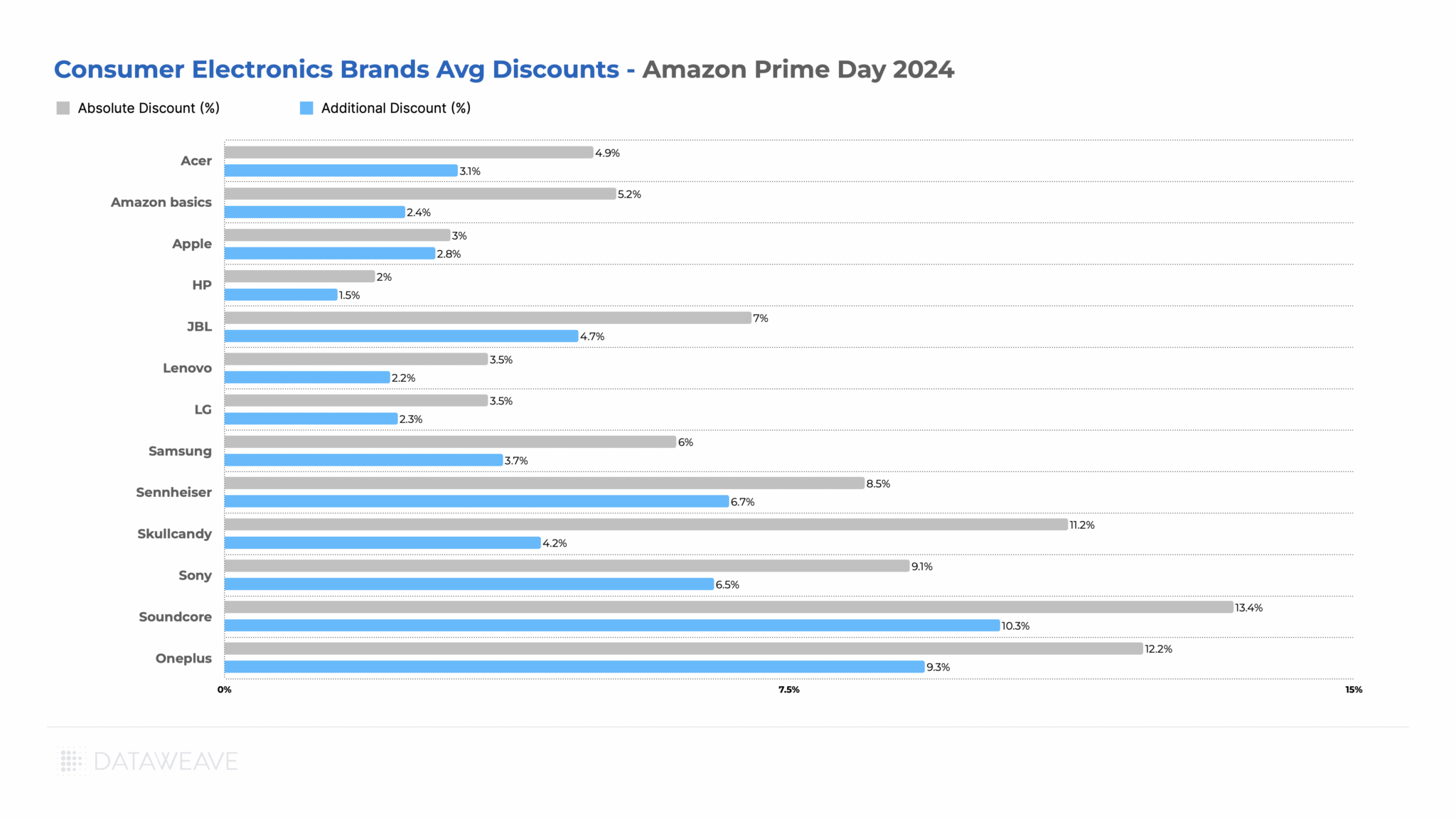

During the sale event, Soundcore (headphone and earphone brand from Anker) led with the highest Additional Discount of 10.3%, followed closely by OnePlus at 9.3%. These brands clearly leveraged Prime Day to drive sales and potentially gain market share.

Sennheiser and Sony also offered significant additional discounts, indicating aggressive promotional strategies during the event.

Notably, some well-known brands like Apple and HP offered more conservative discounts, possibly due to their established market positions or differing promotional strategies.

Despite modest discounts though, Amazon revealed that the iPhone 13 and OnePlus 12R were among the top premium smartphones customers bought this Prime Day. Prime members shopped from top brands such as LG, IFB, Bosch, and Haier and upgraded to premium appliances through affordability options of no cost EMI, Bank discounts and exchange offers, claims Amazon.

These learnings offer valuable insight into the mindset of the modern Indian consumer, who is ready to purchase premium products. Brands can leverage more detailed market intelligence to drive their positioning in India.

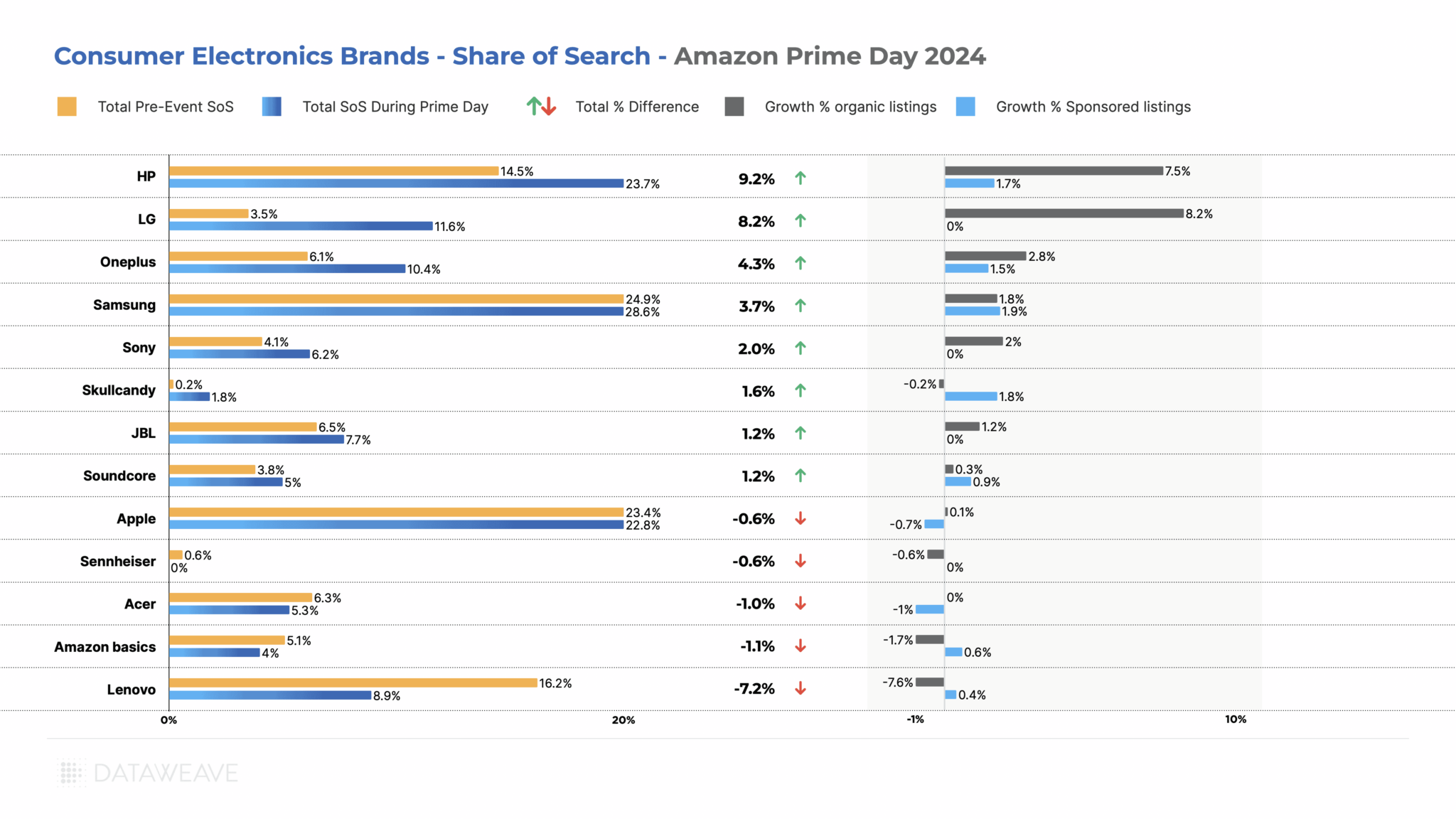

Share of Search Analysis

The Share of Search (SoS) for a brand represents the number of its products in the top 20 search results for relevant search keywords on Amazon, relative to that of its competitors. It provides insights into a brand’s visibility during the sale event.

HP saw the most significant improvement in its Share of Search during Prime Day, gaining 9.2%, with strong growth in both organic (7.5%) and sponsored (1.7%) listings. LG also made substantial gains of 8.2% and 5.3% respectively. Both brands offered significant markdowns on laptops and accessories.

Surprisingly, some popular brands like Apple (-0.6%) and Acer (-1.0%) experienced slight decreases in their SoS. Lenovo notably lost 7.2% of its visibility share, with a significant decline in organic listings (-7.6%). Samsung maintained its strong position with an increase in SoS (3.7%).

Key Takeaways:

While some brands like Soundcore and OnePlus used aggressive discounting to drive sales, others like HP and LG focused on improving their search visibility. The data suggests that a combination of attractive discounts and improved search visibility was key to success during the event. Brands that managed to balance these factors effectively, like HP and Samsung, seemed to perform particularly well. Interestingly, some brands with lower discounts (like HP) still managed to significantly increase their SoS, indicating that factors beyond pricing played a role in visibility during the event.

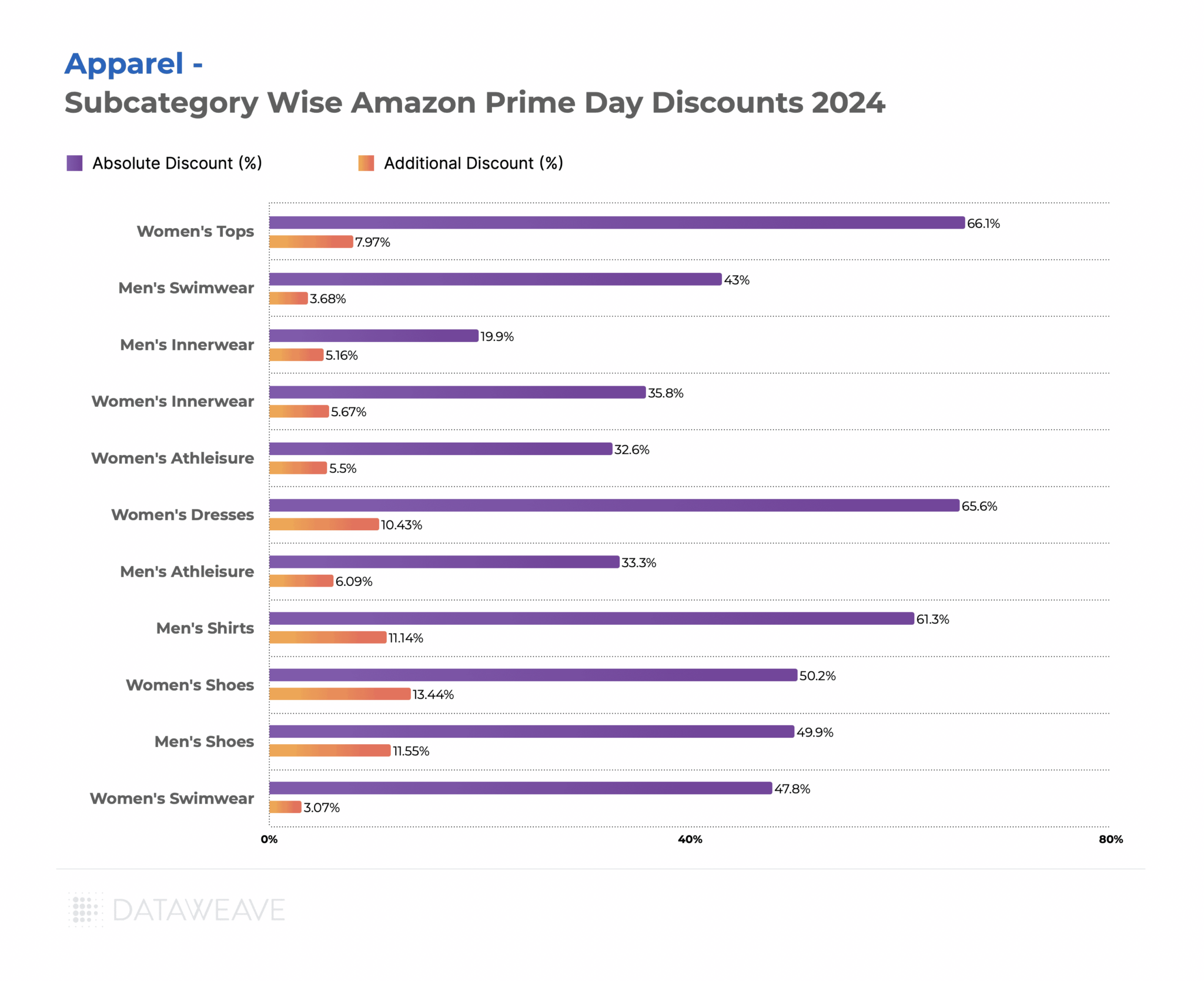

Apparel

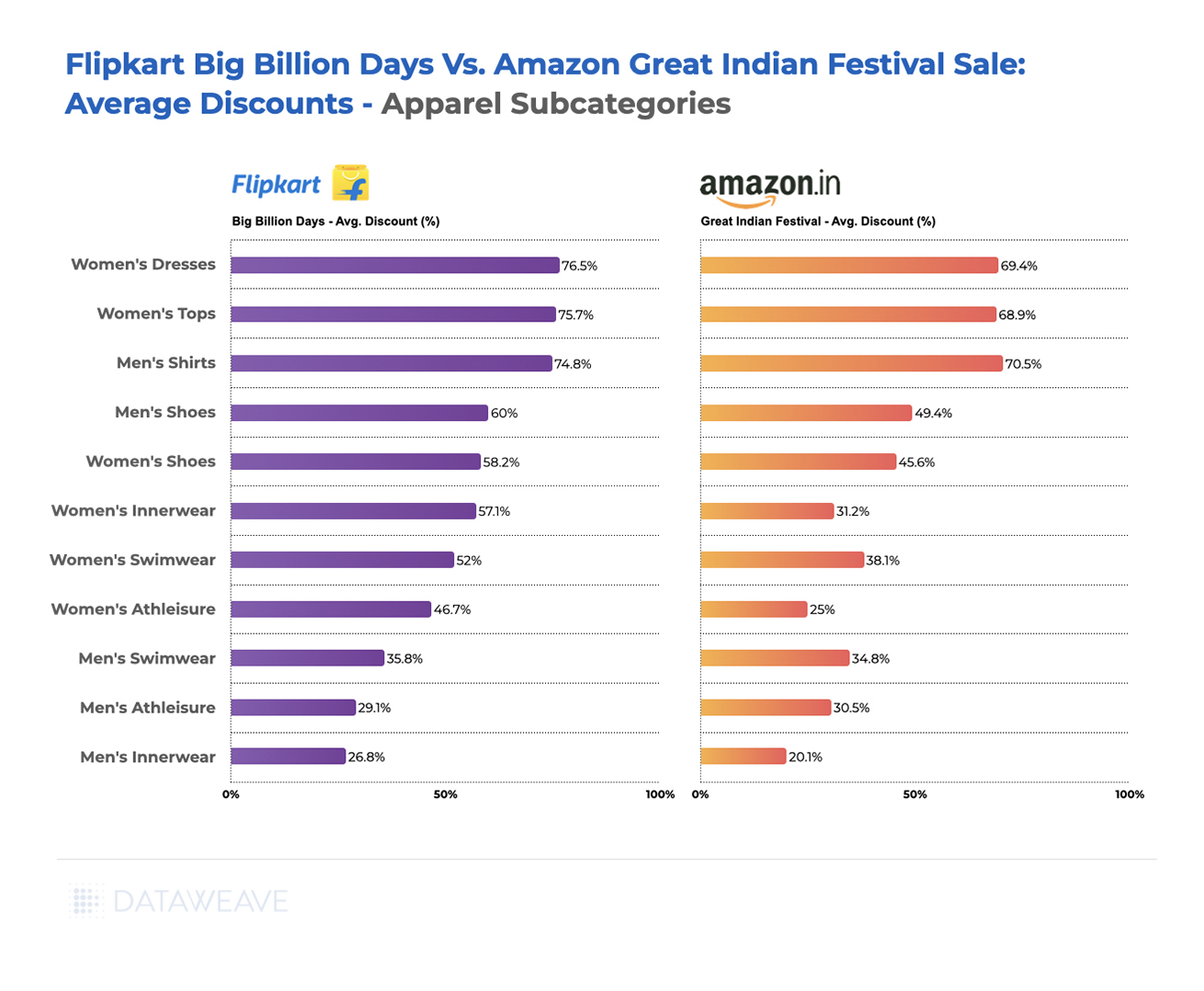

Within the subcategories analyzed, Women’s Shoes (13.4%) and Men’s Shoes (11.6%) saw the highest Additional Discounts on Amazon, indicating a strong focus on footwear during the event. Men’s Shirts followed closely at 11.1%

Women’s Tops had a more modest Additional Discount of 7.9% despite a high Absolute Discount before the event. Similarly, Women’s Dresses showed substantial Additional Discounts (10.4%).

Swimwear for both men and women saw low Additional Discounts (3.7% and 3.0% respectively). Innerwear categories for both men and women had more conservative discounts, with Men’s Innerwear showing the lowest Absolute Discount (19.9%) among all subcategories.

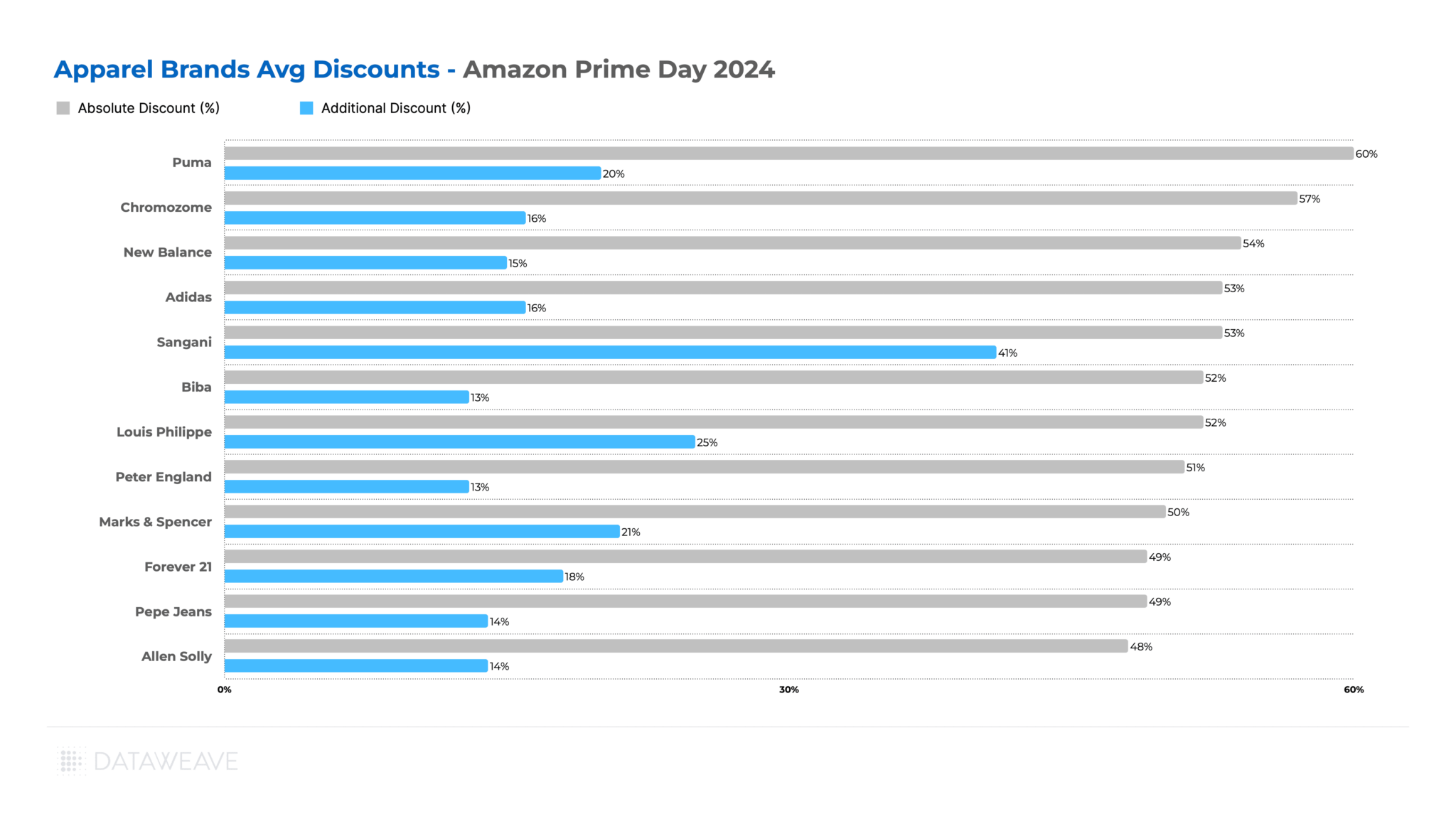

Brand-level Insights in Apparel

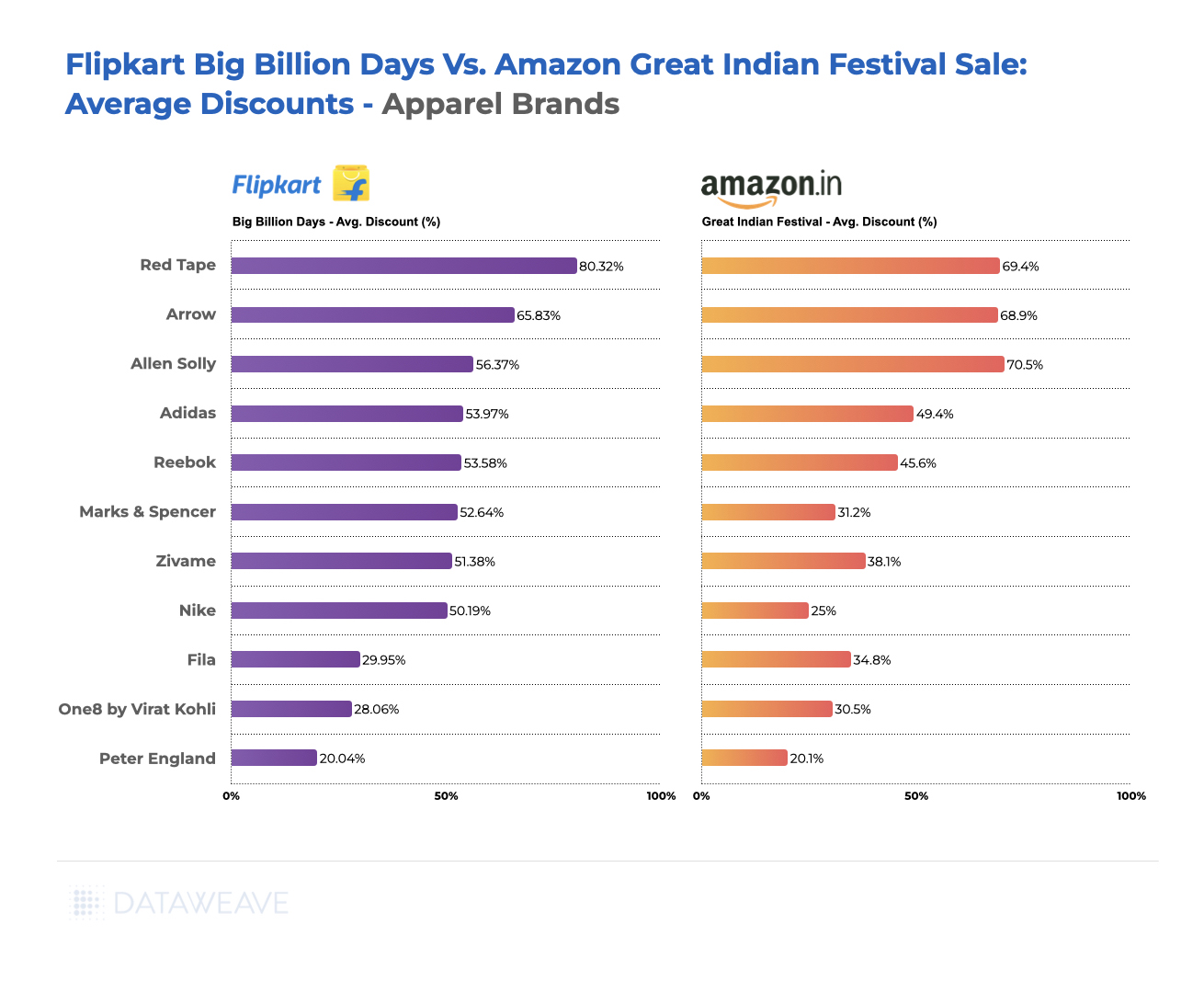

During the sale event, Sangani (innerwear brand) led with the highest Additional Discount of 41%, followed by Louis Philippe at 25%. These brands clearly leveraged Prime Day to drive sales and gain market share.

Puma offered the highest Absolute Discount at 60% with a significant Additional Discount of 20%, indicating a consistently aggressive promotional strategy. Chromozome (men’s innerwear brand) and Bacca Bucci (homegrown shoe brand of Shark Tank India fame) also offered substantial Absolute Discounts (57% and 56% respectively), but their Additional Discounts varied significantly (16% and 6% respectively).

Again, some well-known brands like Adidas, and Pepe Jeans offered more moderate Additional Discounts, possibly due to their established market positions.

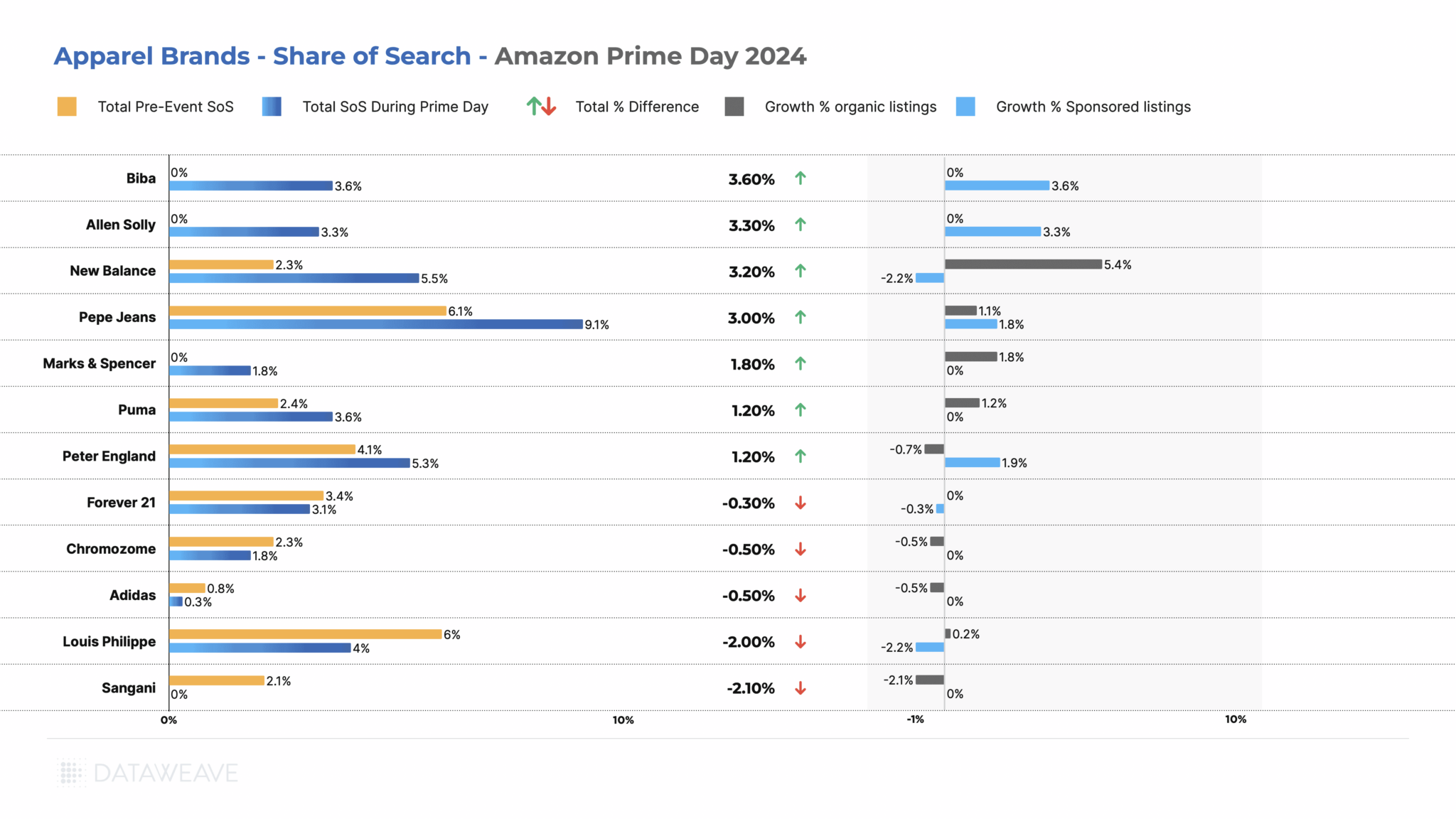

Share of Search Analysis

Biba (women’s ethnic wear brand) saw the most significant improvement in its SoS, gaining 3.60%, entirely through investments in sponsored listings. Allen Solly and New Balance (shoe brand) also made substantial gains of 3.3% and 3.2% respectively.

Surprisingly, some popular brands like Louis Philippe (-2.00%) and Sangani (-2.10%) experienced decreases in their SoS. Louis Philippe lost its share due to a roll back of its sponsored listings, while Sangini lost ground organically.

Key Takeaways:

While some brands like Sangani and Louis Philippe used aggressive discounting to drive sales, others like Biba and Allen Solly focused on improving their search visibility through sponsored listings.

Some brands with high discounts (like Sangani) saw a decrease in SoS, while others with more modest discounts (like Biba) significantly increased their visibility. This indicates that factors beyond pricing played a crucial role in brand performance during the event.

The significant use of sponsored listings by some brands highlights the importance of paid advertising in gaining visibility during competitive events like Prime Day.

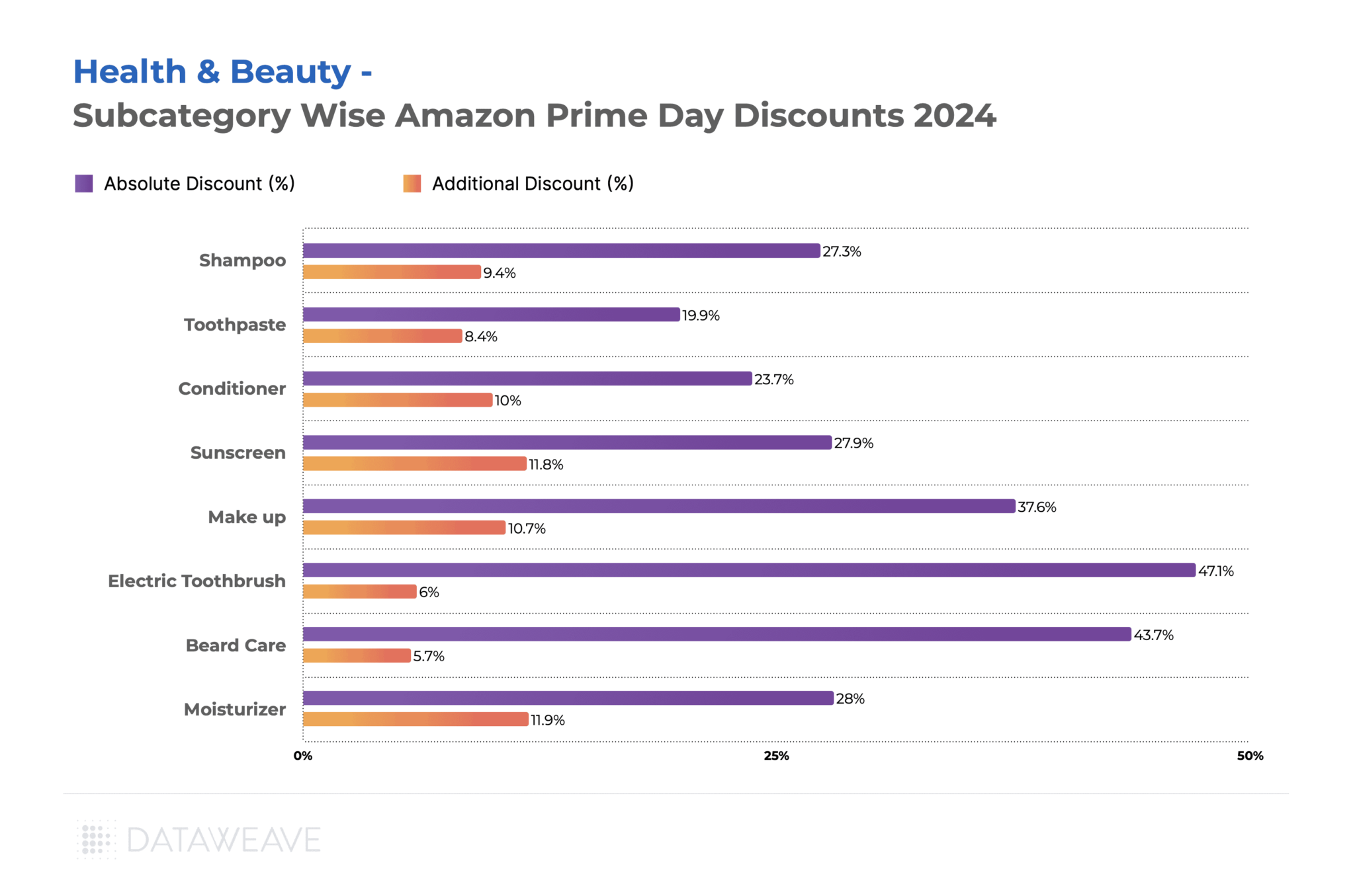

Health & Beauty

Health & Beauty emerged as a standout category during Amazon Prime Day India 2024, with significant discounts and competitive strategies at play.

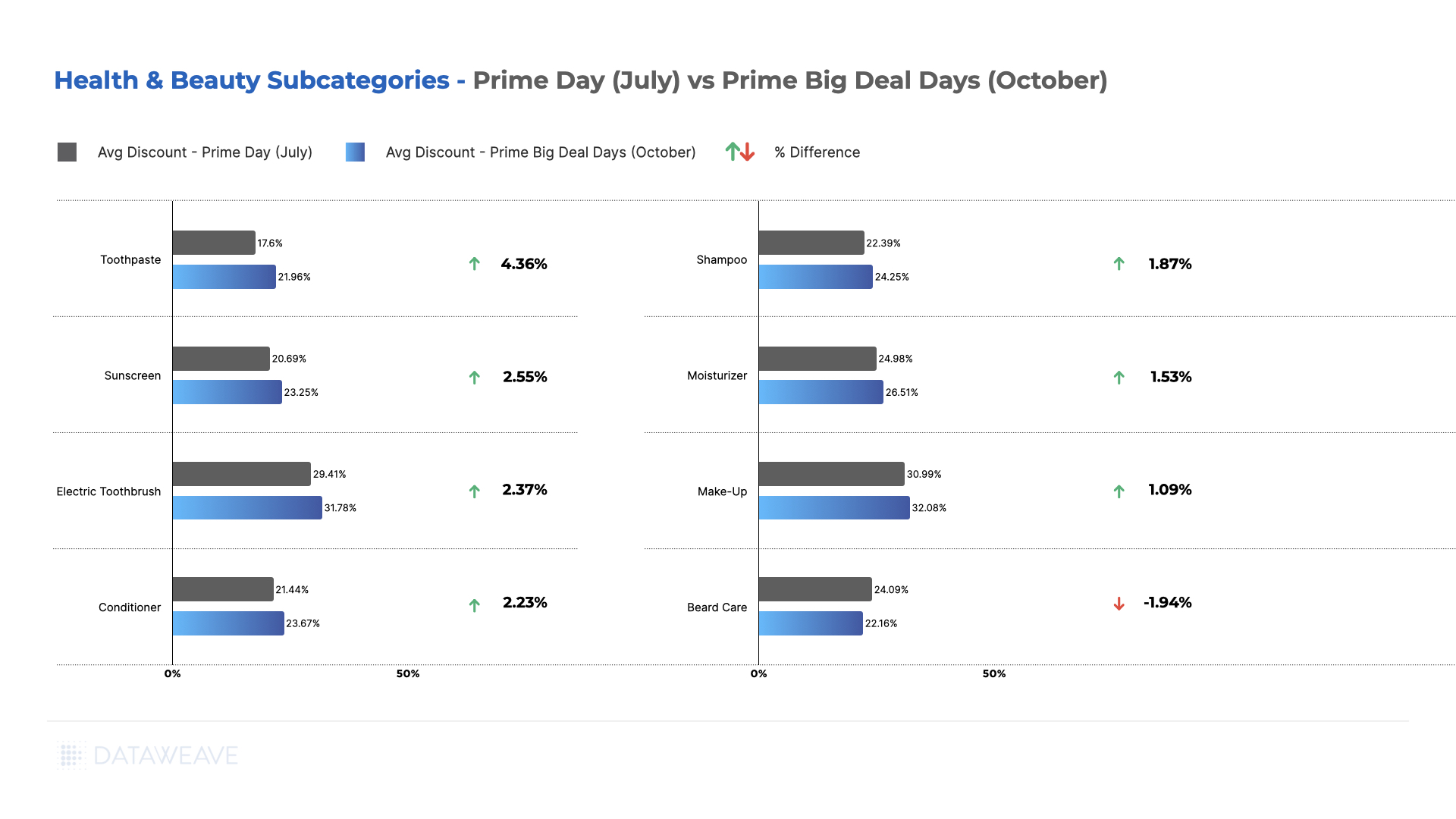

Within the subcategories we analyzed, Moisturizer (11.9%) and Sunscreen (11.8%) saw the highest additional price reductions on Amazon, likely due to seasonal demand during Prime Days. Make-up followed closely at 10.6%.

Electric Toothbrushes had the highest Absolute Discount at 47.1%, but a lower Additional Discount of 6.0%, highlighting that these products were already significantly discounted before the event. Similarly, Beard Care products showed high Absolute Discounts (43.7%) but lower Additional Discounts (5.7%) during Prime Day.

Everyday essentials like Toothpaste saw more modest discounts (19.9% Absolute, 8.4% Additional), reflecting steady demand for these products.

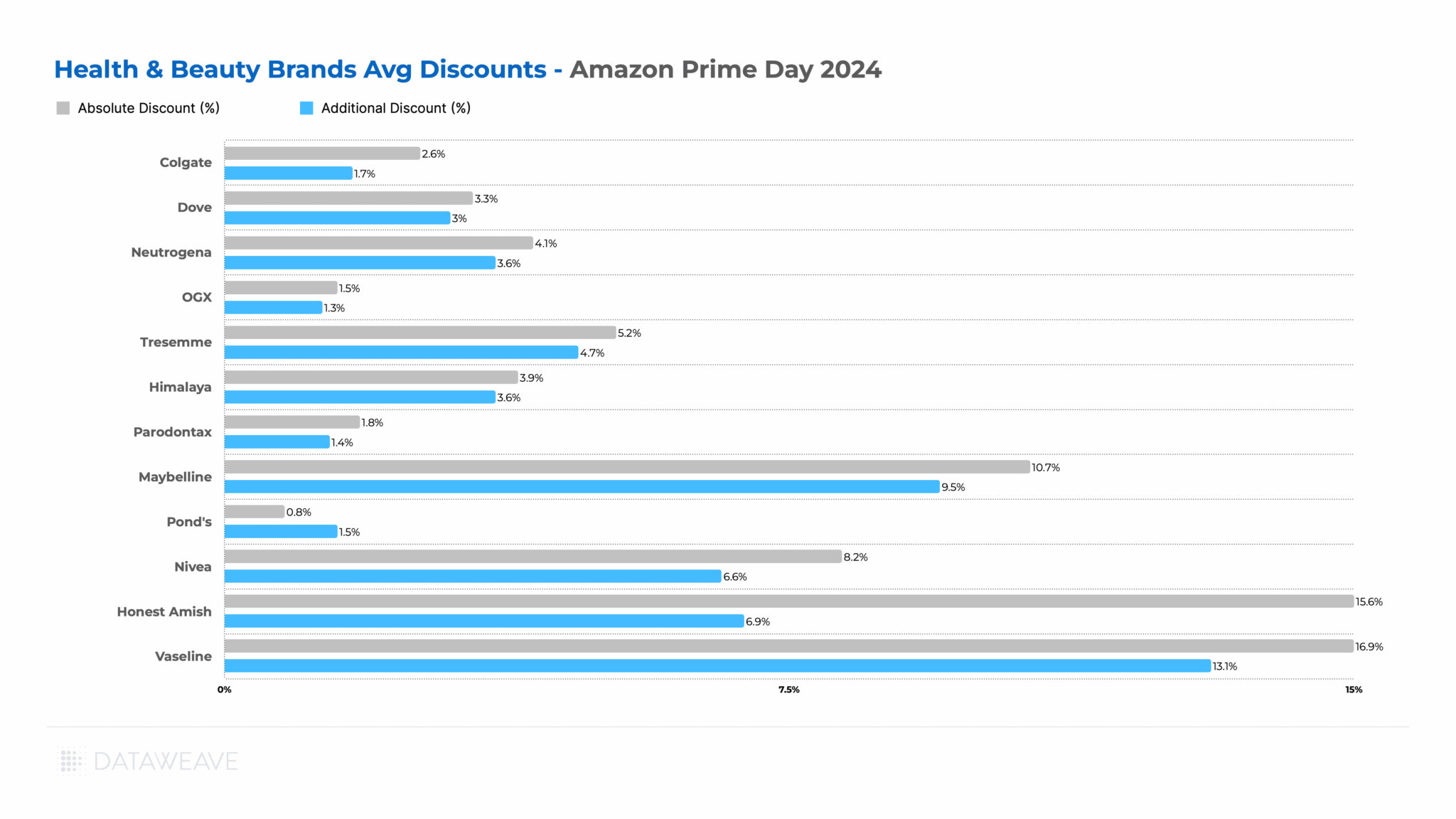

Brand-level Insights in Health & Beauty

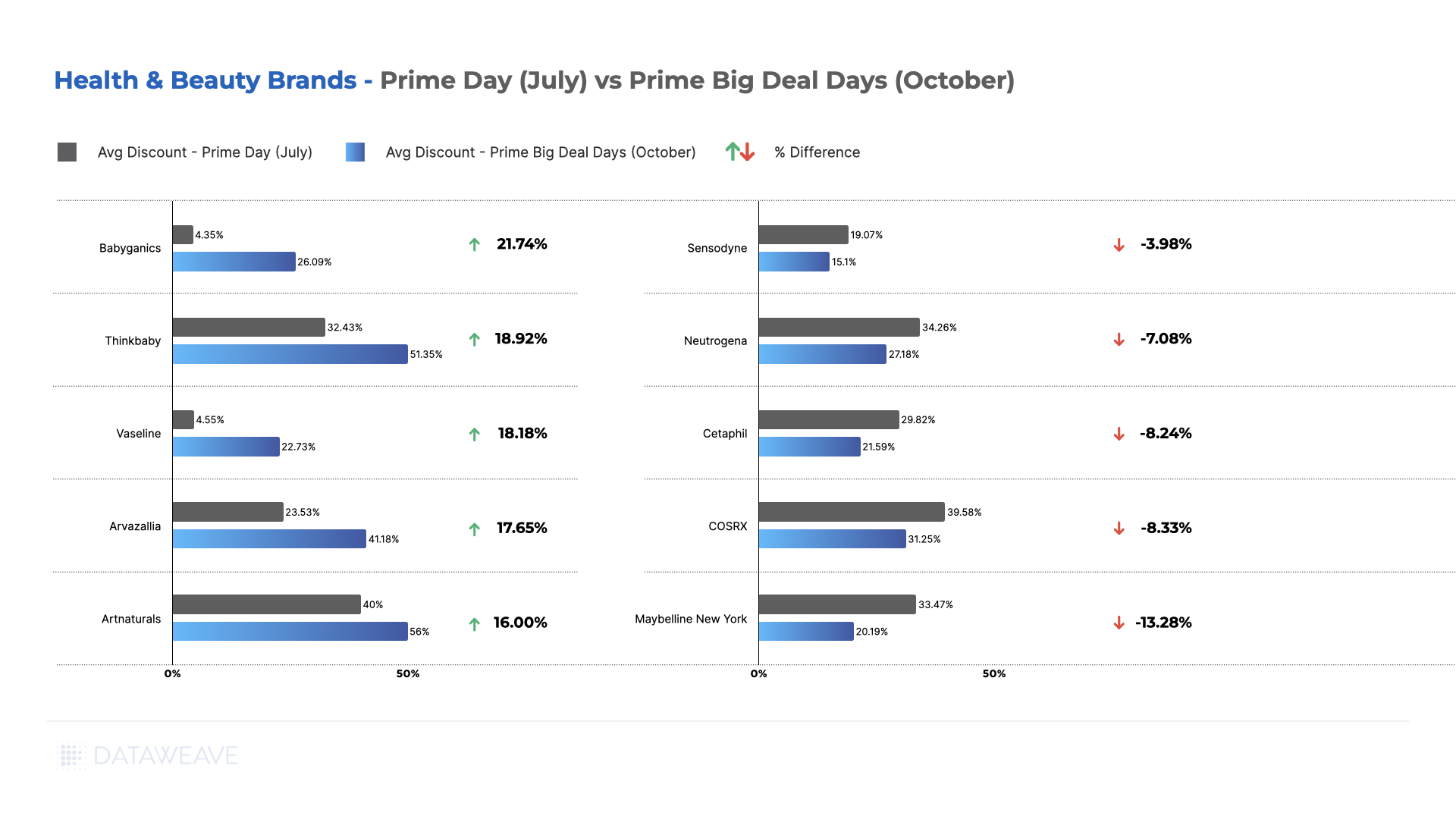

Vaseline led with the highest Additional Discount of 13.1%, followed by Maybelline at 9.5%. These brands clearly leveraged Prime Day to drive sales and potentially gain market share.

Honest Amish (beard care brand) and Nivea also offered substantial Absolute Discounts (15.6% and 8.2% respectively), but their Additional Discounts were lower, indicating pre-existing promotional strategies.

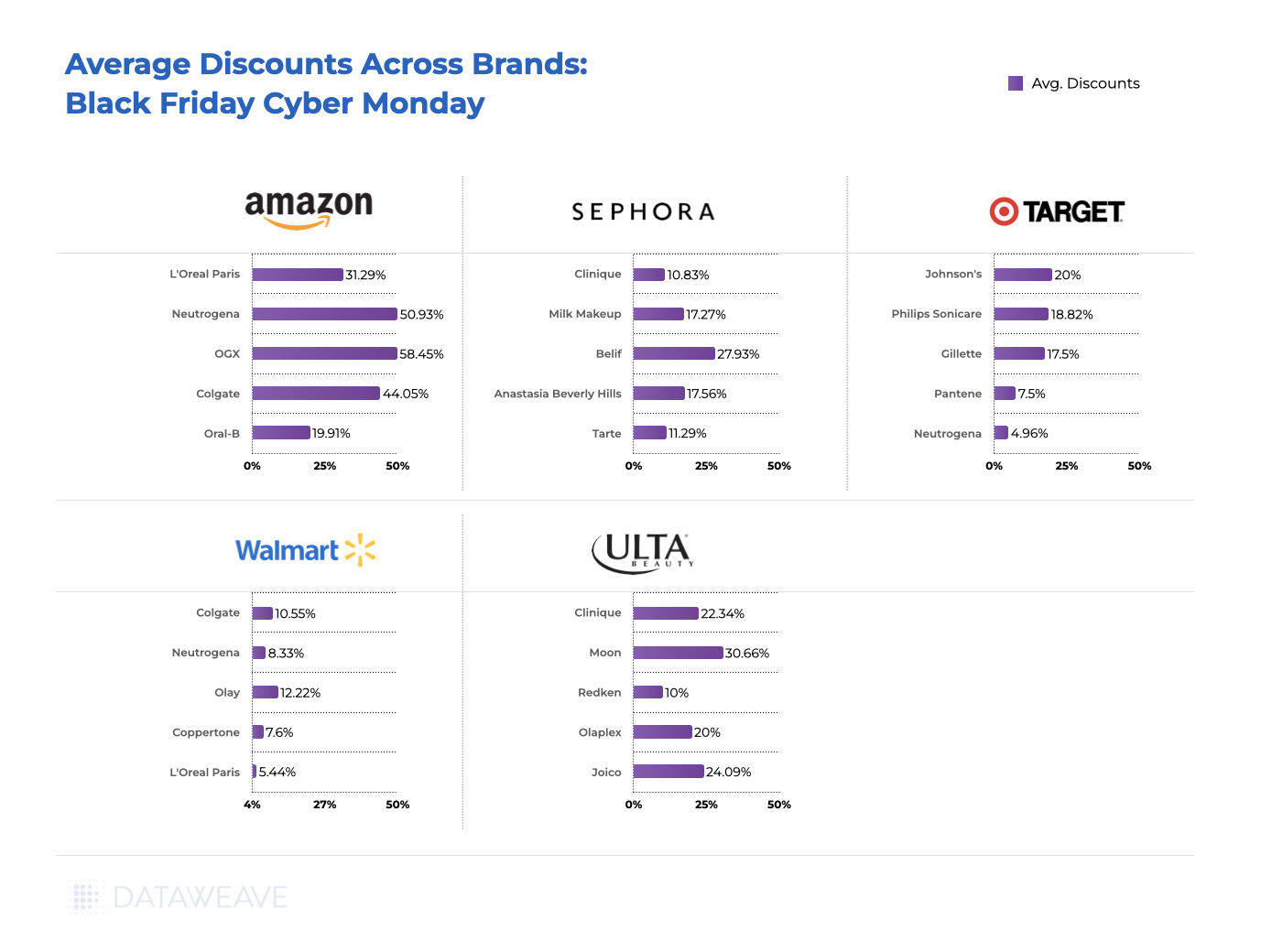

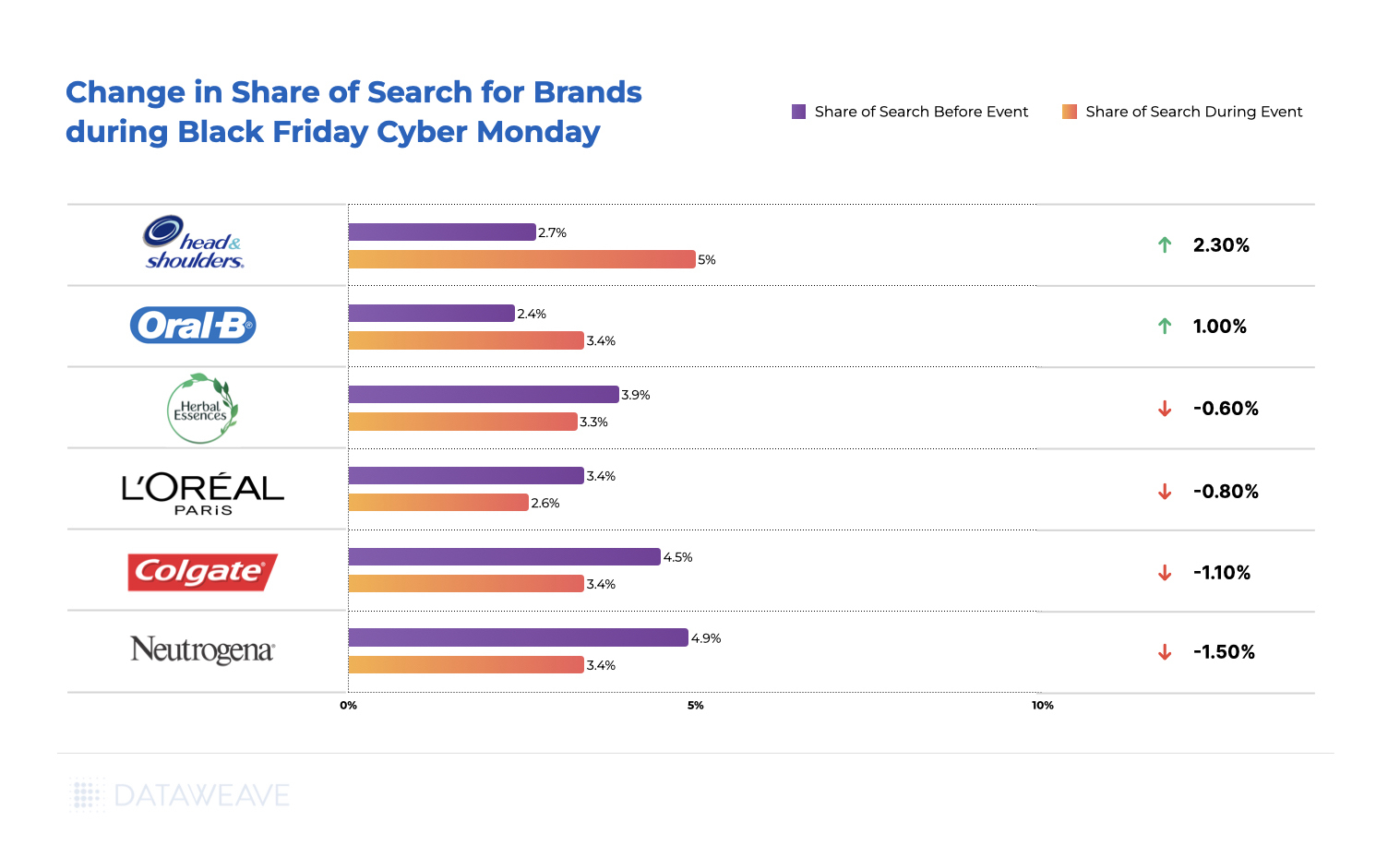

Once again, some well-known brands like Colgate, Dove, and Neutrogena offered more conservative discounts, possibly due to their established market positions or differing promotional strategies.

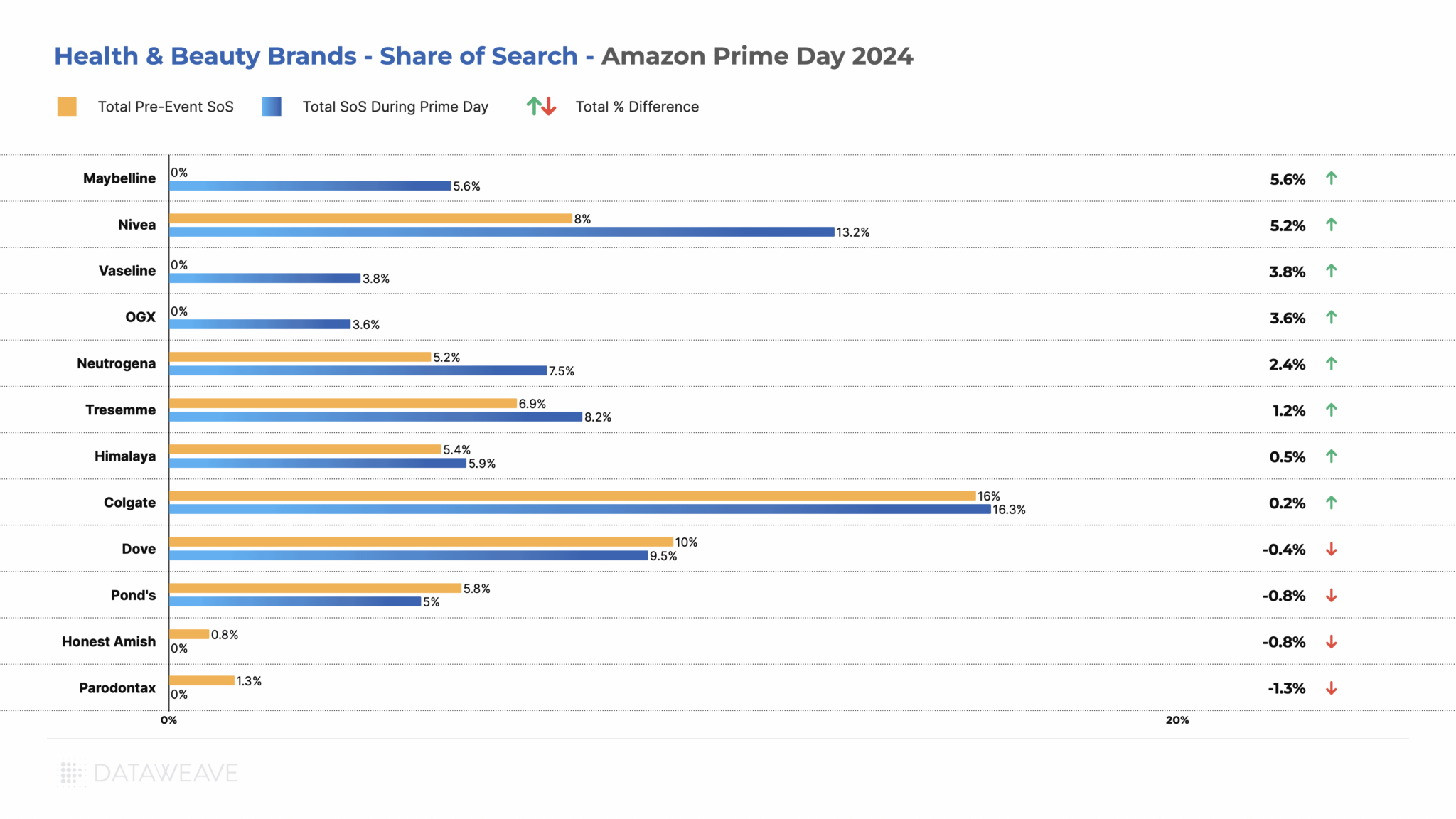

Share of Search Analysis

Maybelline saw the most significant improvement, gaining 5.6% in SoS, all through organic listings. The brand has been aggressively increasing market share with several new product launches and influencer campaigns. Nivea and Vaseline also made substantial gains of 5.2% and 3.8% respectively.

In this category as well, some popular brands like Dove (-0.4%), Pond’s (-0.8%), and Honest Amish (-0.8%) experienced slight decreases in their SoS. Parodontax (toothpaste brand) notably lost 1.3% SoS, with most of the decline in sponsored listings. Colgate maintained its strong position with a slight increase in SoS (0.2%), reflecting its dominant market presence.

Key Takeaways:

While some brands like Vaseline and Maybelline used aggressive discounting and improved visibility to drive sales, others like Colgate and Dove relied more on their established market positions.

None of the brands made any significant strides in sponsored listings, revealing that brands in this category are not yet fully leveraging retail media to help manage and boost their visibility on online marketplaces.

Final Thoughts

Amazon Prime Day 2024 has redefined the eCommerce landscape in India, yet again, showcasing diverse strategies employed by brands to maximize their impact. By understanding and leveraging these insights, brands and retailers can better navigate future sales events, optimizing their eCommerce strategies to achieve sustained growth and success.

Stay tuned to our blog for more in-depth analyses of brand and retailer performance across various retail events.

Reach out to us today to learn how you can leverage data-driven insights to optimize your eCommerce strategy.

Amazon Prime Day 2024 saw U.S. shoppers spending a staggering $14.2 billion online during the two-day event—an 11% increase from last year. This surge in spending reflects a significant shift in consumer behavior and presents a wealth of insights for brands and retailers alike.

Unlike last year’s focus on essentials, Prime Day 2024 saw Americans enthusiastically embracing both necessities and discretionary purchases. The Consumer Electronics and Health & Beauty categories, for example, experienced a notable uptick in interest, driven by major retailers slashing prices across CPG and Grocery segments, amid other reasons. Check out our first article in the Prime Day series 2024, analyzing retail insights across categories during the event.

This year, small businesses gained unprecedented visibility on Amazon, pushing relatively new brands into visibility.

At DataWeave, we recognize the critical importance of understanding these market dynamics for brands navigating the competitive eCommerce landscape. To provide actionable insights, we conducted an extensive analysis of over 47,000 SKUs across key categories before and during Amazon during Prime Day 2024. Our study delves into:

Pricing strategies: How did brands adjust their discounts to capitalize on the Prime Day frenzy?

Share of Search: Which brands achieved the highest visibility for major search keywords?

Dive into these insights below to uncover how brands performed during Amazon Prime Day 2024, and learn how you can leverage these findings to enhance your brand’s digital shelf performance.

Our Findings

Most brands offered substantial discounts before Prime Day, then added smaller discounts during the event. This strategy creates a perception of value while still allowing room for Prime Day-specific deals. To understand the real value offered by brands, we conducted an extensive analysis of brand performance, examining both pricing strategies and visibility on the platform. Our approach focuses on two key metrics:

Discounts: We analyzed both the Absolute Discount (total markdown relative to MSRP a week before Prime Day) and the Additional Discount (the price reduction during Prime Day compared to the week before).

Share of Search (SoS): We examined the visibility of brands in the top 20 search results. We also separately tracked this metric for organic and sponsored search results.

Let’s dive into the category and brand specific insights:

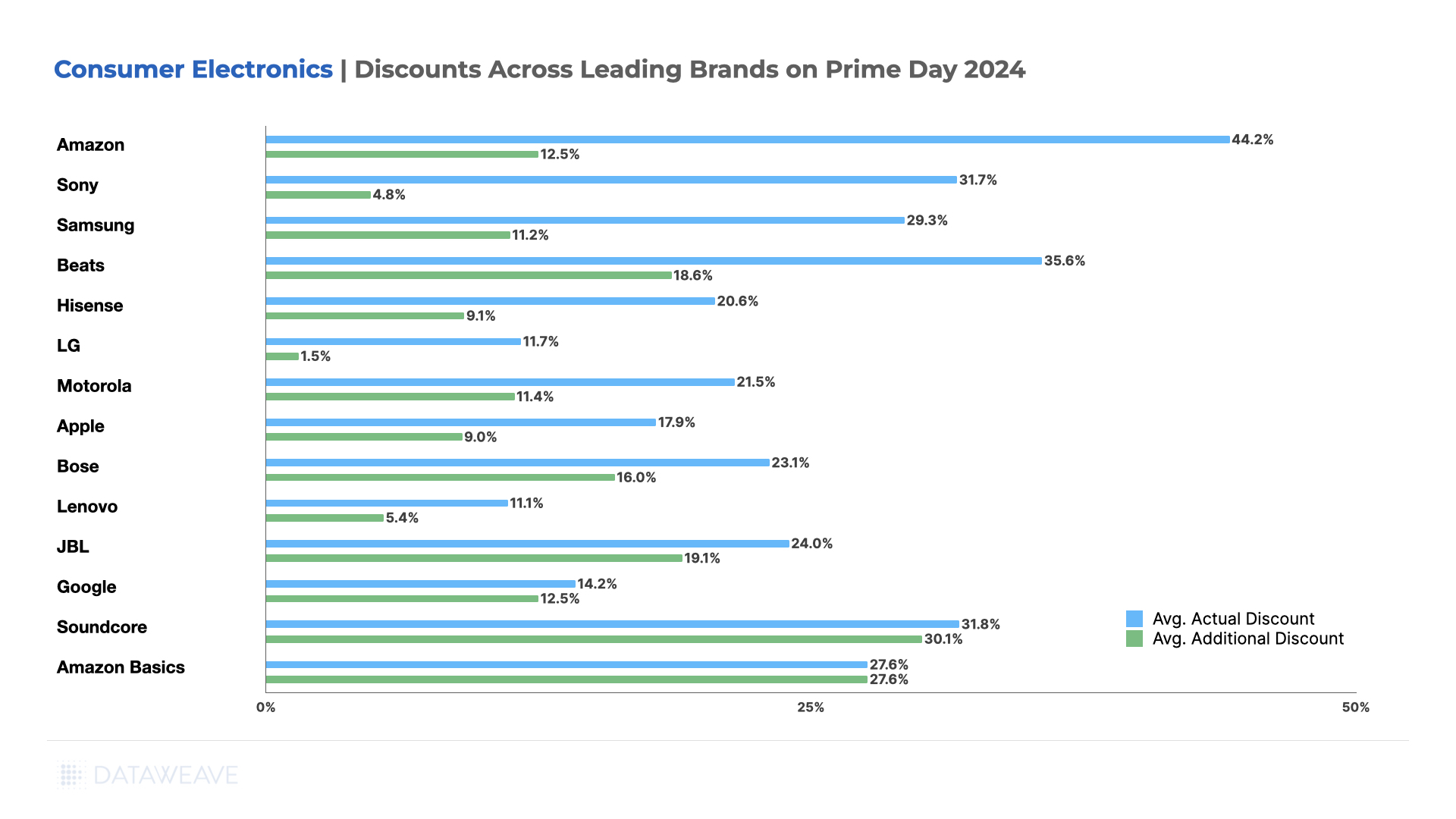

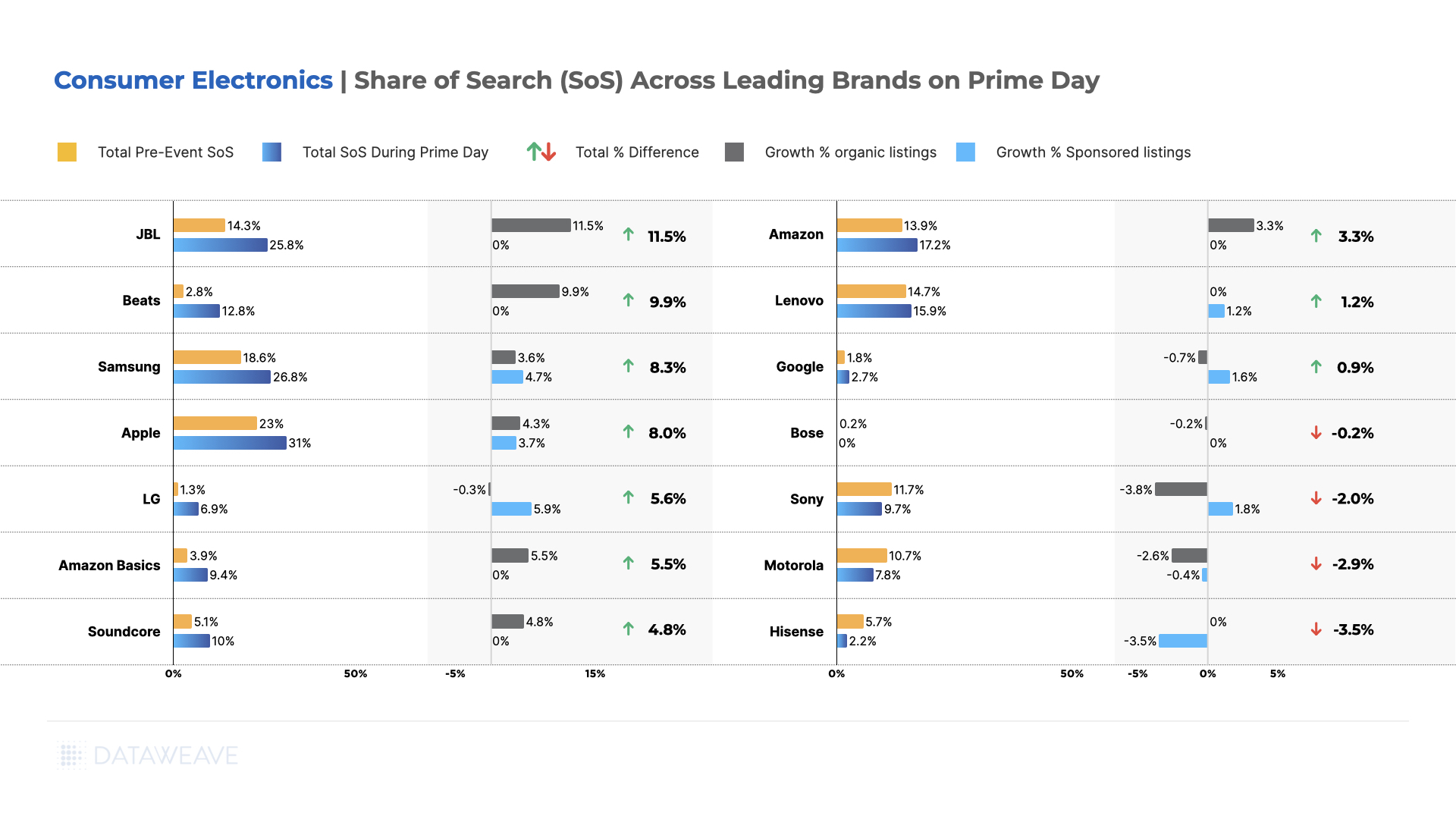

Consumer Electronics

Once again, in 2024, the Consumer Electronics category dominated discounts. Amazon’s own brands lead with the highest average Absolute Discount (44.2%) and a significant Additional Discount (12.5%), showcasing its aggressive push for Prime Day.

In a surprising twist, Amazon’s homepage wasn’t dominated by its own brands. Instead, tech giants like Apple and Samsung took centre stage. Despite this, Amazon’s own brands offered significant discounts across electronics products, including Amazon Kindle, Fire TVs, Fire TV Sticks, Echo Dot, and more, aiming to capture market share via markdowns.

Soundcore (earphone audio products brand) offered the highest discount during Prime Day, at 30.10%. Other headphone, earbuds, and wireless headphone brands including Sony, Beats, JBL, and more also offered significant discounts.

Premium brands like Apple (17.90% Absolute, 9.00% Additional) and Bose (23.10% Absolute, 16.00% Additional) offered relatively modest discounts, aligning with their brand positioning, but also taking advantage of the Prime Day frenzy.

Share of Search Insights in Consumer Electronics

JBL emerged as the standout performer, with the most significant increase in SoS, jumping from 14.3% pre-event to 25.8% during Prime Day, driven entirely by organic growth. Beats also saw a remarkable rise, increasing from 2.8% to 12.8%, again through organic listings only. Samsung maintained its strong presence, growing from 18.6% to 26.8%, with most of its growth influenced by increased ad spend.

Apple, despite already having a high pre-event SoS, managed to increase its share further from 23.0% to 31.0%, with some contribution via sponsored ads. LG saw a substantial increase from 1.3% to 6.9%, primarily through sponsored listings, opting for an inorganic approach to drive visibility during the sale.

Amazon and its AmazonBasics brand both saw notable increases in SoS, relying solely on organic growth. This is, of course, not surprising since Amazon controls its organic ranking algorithm.

Interestingly, some brands experienced decreases in SoS. Sony, Motorola, and Hisense all saw reductions in their share, with Hisense’s decline coming entirely from a reduction in sponsored listings.

Key Takeaway: Prime Day 2024 saw a significant reshuffling of brand visibility in the Consumer Electronics category. While some established brands like JBL, Beats, Samsung, and Apple strengthened their positions through a mix of organic and sponsored growth, others faced increased competition for consumer attention. The event highlighted the importance of a balanced approach to visibility, with successful brands leveraging both organic search optimization and strategic use of sponsored listings to maximize their presence during this high-traffic period.

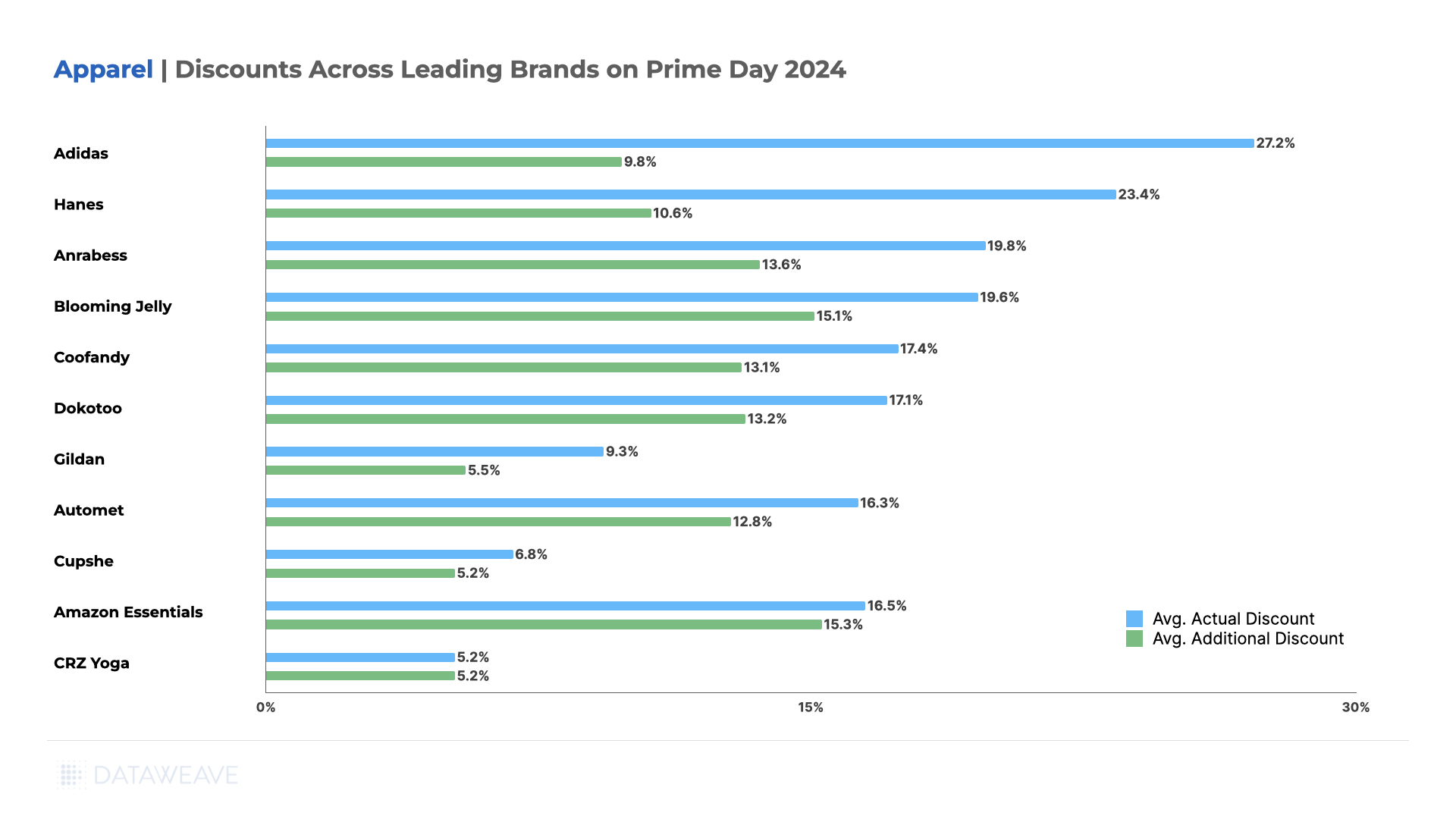

Apparel

In the Apparel category, Adidas led with the highest Absolute Discount (27.2%) and a significant Additional Discount (9.8%). Value brands like Hanes (innerwear brand) and Anrabess offered substantial discounts, while Amazon Essentials maintained high discounts across the board (16.5% Absolute, 15.3% Additional).

Some brands like Cupshe (swimwear and vacation apparel brand) offered relatively lower additional markdowns. Meanwhile CRZ Yoga (athleisure brand) did not offer additional markdowns on Prime Day.

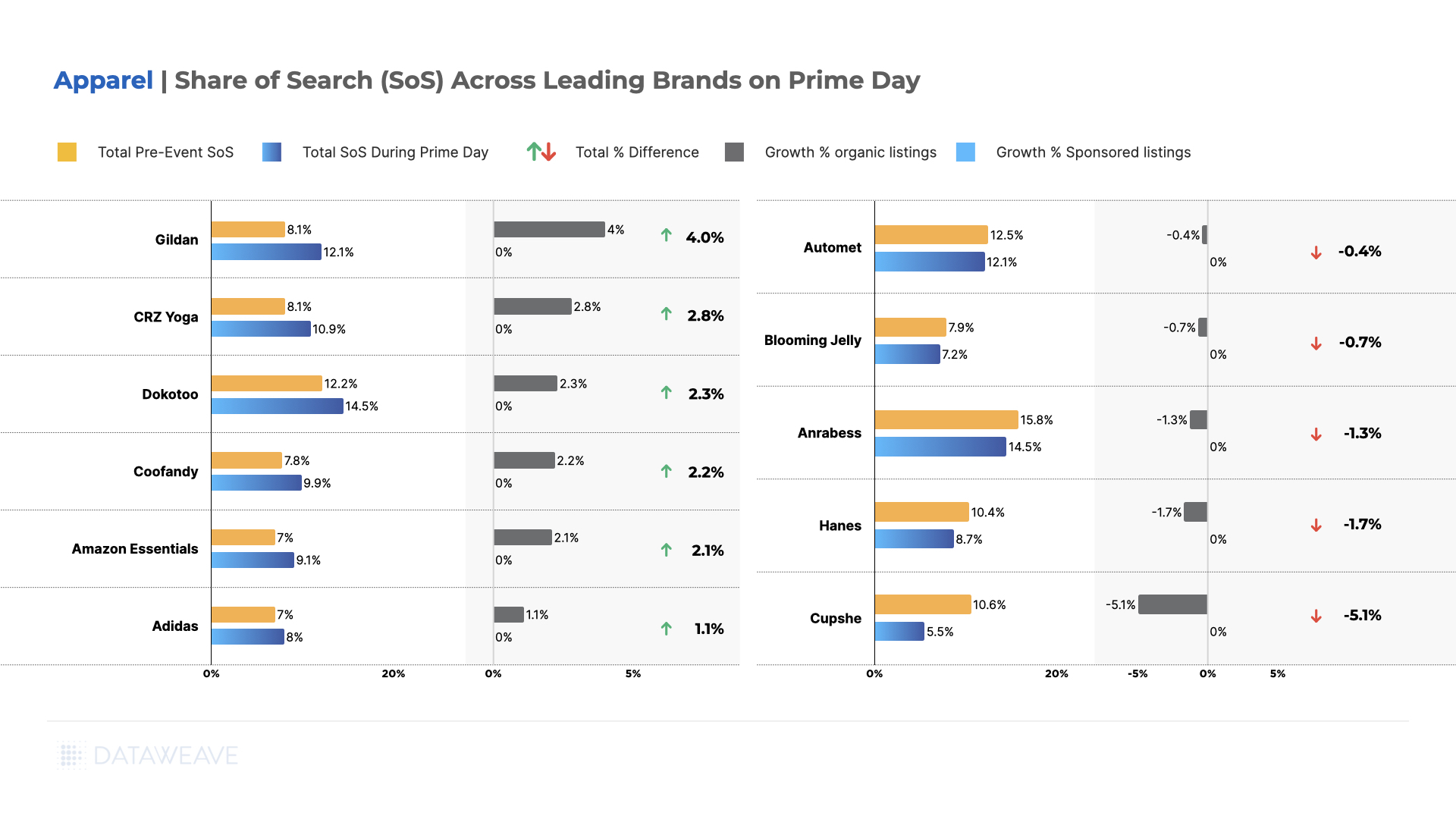

Share of Search Insights in Apparel

Gildan (activewear brand) emerged as the top performer in terms of SoS growth, increasing from 8.1% pre-event to 12.1% during Prime Day, driven entirely by organic growth. CRZ Yoga (an athleisure apparel brand) and Dokotoo (women’s casualwear brand) also saw significant increases in their SoS, rising by 2.8 and 2.3 percentage points respectively, again through organic listings only.

Amazon Essentials continued to perform well, increasing its visibility from 7.0% to 9.1%, aligning with its competitive pricing strategy. Coofandy also saw a notable increase, growing from 7.8% to 9.9%.

Interestingly, some brands that were previously highlighted for growth actually experienced decreases in SoS. Automet (clothing & accessories brand) saw a slight decline from 12.5% to 12.1%, while Anrabess (women’s fashion brand) dropped from 15.8% to 14.5%. Cupshe (swimwear brand) experienced the most significant decrease, falling from 10.6% to 5.5%.

Adidas, despite leading in discounts, saw only a modest increase in SoS from 7.0% to 8.0%. Notably, none of the brands visible in the top search results utilized sponsored listings, with all changes in SoS coming from organic growth or decline. This indicates a lack of maturity in this category in leveraging retail media.

Key Takeaway: Prime Day 2024 in the apparel category showcased the importance of organic search optimization. While some brands like Gildan and CRZ Yoga significantly improved their visibility, others faced challenges in maintaining their pre-event positions. The absence of sponsored listings across all brands highlights a unique dynamic in the apparel category, where organic search performance appears to be the primary driver of visibility during high-traffic events like Prime Day.

This suggests that Apparel brands may need to focus more on SEO strategies and organic content optimization to maximize their presence during major shopping events, rather than relying on paid promotions. On the other hand, smartly leveraging retail media to boost visibility can give apparel brands a competitive edge.

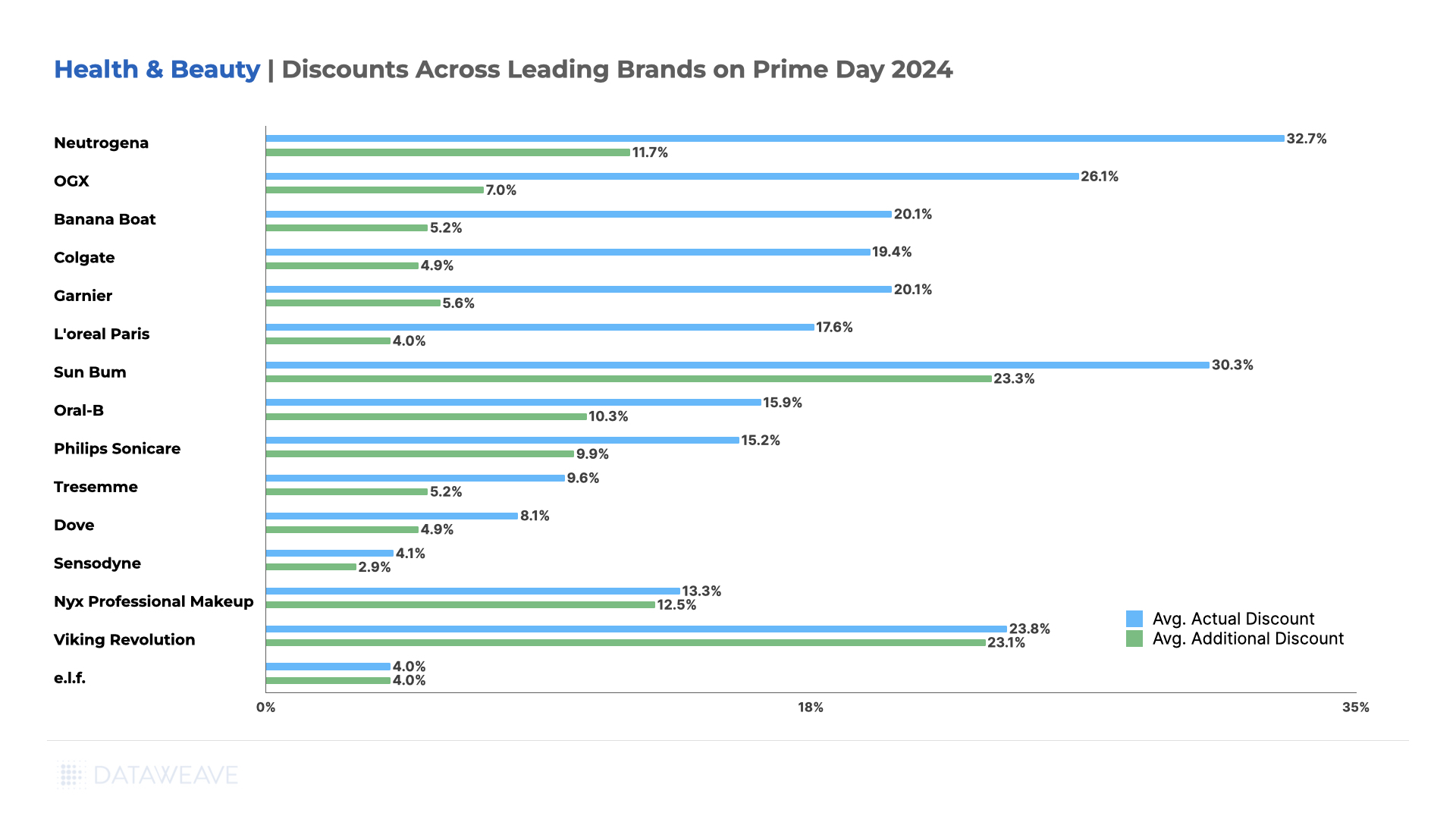

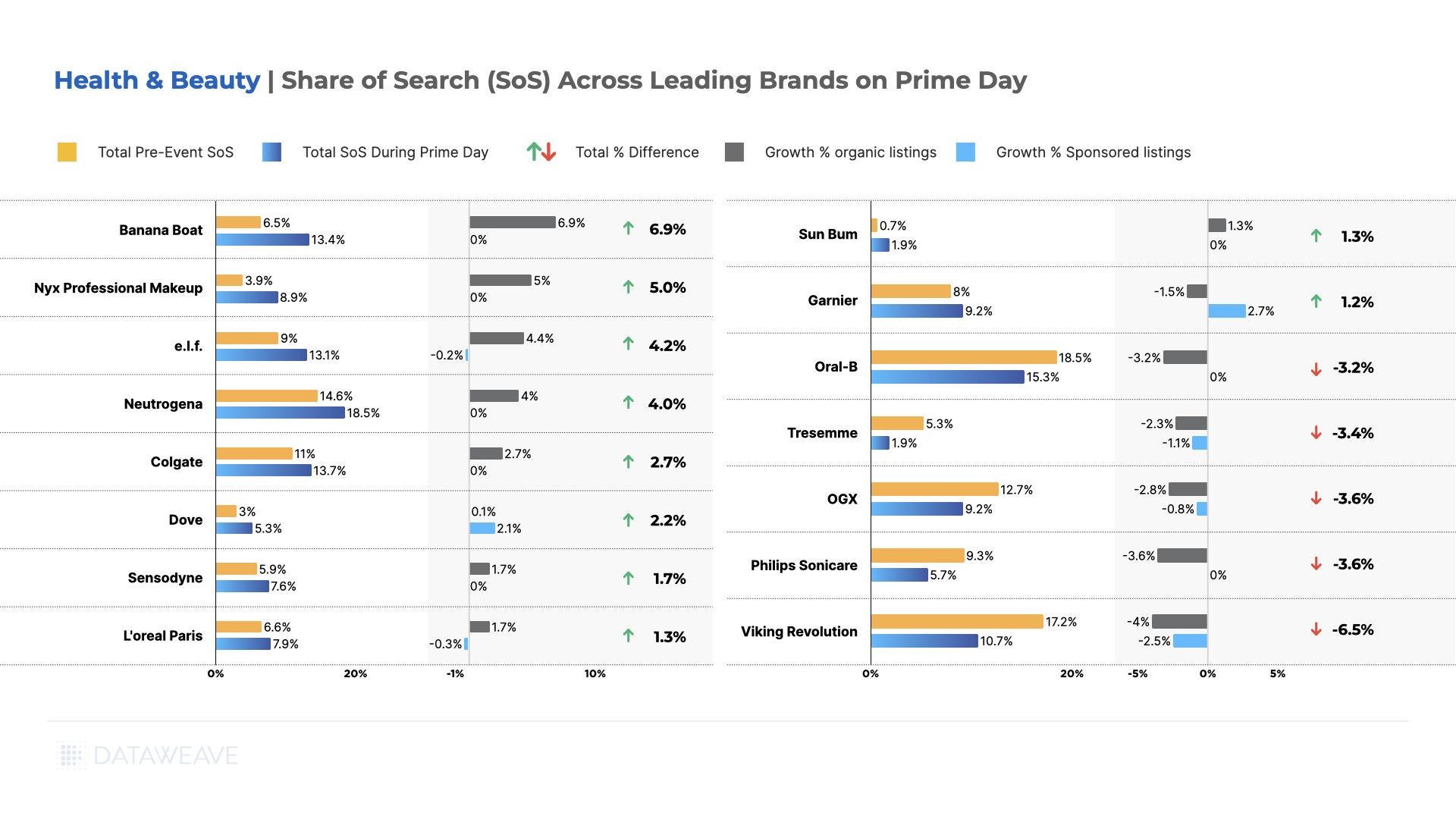

Health & Beauty

The Health & Beauty category this year got a push thanks to Amazon’s subscription offering. Prime members who subscribed for regular usage products like toothpaste and health aids or medicines availed higher discounts.

Amid Health & Beauty brands, Neutrogena led with the highest Absolute Discount (32.7%) and a significant Additional Discount (11.7%). Sun Bum moisturizers & sunscreen (23.3%) and Viking Revolution (23.1%) offered the highest Additional Discounts, indicating a strong Prime Day focus.

Premium brands like L’Oreal Paris and Philips Sonicare offered moderate discounts, balancing promotions with their intended brand image.

Share of Search Insights in Health & Beauty

Banana Boat (sunscreen brand) emerged as the standout performer, seeing the largest increase in SoS from 6.5% to 13.4%, achieved entirely through organic growth. Nyx Professional Makeup also saw a significant jump, rising from 3.9% to 8.9%, again solely through organic listings.

Contrary to previous analysis, e.l.f. actually experienced substantial growth, increasing from 9.0% to 13.1% SoS, with a strong focus on organic growth (4.4%) slightly offset by a minor decrease in sponsored listings (-0.2%).

Neutrogena maintained its strong performance, aligning with its aggressive discounting strategy, as its SoS increased from 14.6% to 18.5% through organic growth. Colgate also saw a notable increase from 11.0% to 13.7% SoS.

Interestingly, some brands employed a mixed strategy. Dove and Garnier saw overall increases in SoS, but achieved this through different means. Dove relied heavily on sponsored growth, while Garnier offset a decrease in organic listings with strong sponsored content growth.

Contrary to previous observations, Oral-B experienced a decrease in SoS from 18.5% to 15.3%, entirely in organic listings. Without any additional spend on sponsored listings to compensate, it lost significant ground in its visibility. Other brands facing significant declines include Tresemme, OGX, Philips Sonicare, and most notably, Viking Revolution, which dropped from 17.2% to 10.7% in its SoS.

Key Takeaway: The Health & Beauty category during Prime Day 2024 showcased a diverse range of strategies and outcomes. While some brands like Banana Boat and Nyx Professional Makeup achieved significant visibility gains through organic growth, others like Dove and Garnier relied more on sponsored content.

The success of e.l.f. and Neutrogena in aligning discounting strategies with increased visibility stands in contrast to the challenges faced by previously strong performers like Oral-B and Viking Revolution. This varied landscape shows the fierce competition in the category and the need for brands to employ multi-faceted strategies that balance organic optimization, sponsored content, and competitive pricing to succeed in high-stakes events like Prime Day.

Brand Strategies and Future Implications

Our analysis reveals several key trends:

Brand Positioning Matters: Premium brands like Apple and Bose maintained their positioning with modest discounts, while value-oriented brands like Soundcore and Hanes offered deeper cuts to attract price-sensitive shoppers.

Visibility vs. Discounting: Some brands, particularly in the Consumer Electronics category, prioritized increasing their visibility (Share of Search) over offering steep discounts. This strategy suggests a focus on long-term visibility and brand perception rather than short-term sales boosts.

Category-Specific Approaches: Apparel brands uniquely relied on organic search visibility, eschewing sponsored listings entirely. In contrast, several Health & Beauty brands leveraged sponsored content significantly to boost their presence.

Emerging Brand Opportunities: Lesser-known brands, especially in the Apparel and Health & Beauty categories, used Prime Day as a launchpad to increase their visibility, often outpacing established names in Share of Search growth.

Amazon’s Dual Strategy: As both a platform and a brand, Amazon showcased its ability to offer deep discounts on its own products while also providing a stage for other brands to shine.

Stay tuned to our blog for more in-depth analyses of brand and retailer performance and strategies across various retail events. Reach out to us today to learn how you can leverage data-driven insights to optimize your brand’s eCommerce strategy and performance.

Amazon Prime Day 2024 has once again shattered records, with more items sold during the two-day event than any previous Prime Day. Prime members worldwide saved billions across all categories, while independent sellers moved an impressive 200 million items.

At DataWeave, we conducted an extensive analysis of the discounts offered by Amazon across major categories. By examining over 47,000 SKUs, we’ve uncovered compelling insights into pricing strategies, competitive positioning, and emerging trends in the eCommerce space.

Since products on Amazon and other eCommerce websites are often sold at discounts even on normal days not linked to a sale event, we delved into the real value that Prime Day offers to shoppers by focusing on price reductions or the Additional Discount during the sale compared to the week before. As a result, our approach highlights the genuine benefits of the event for shoppers who count on lower prices during the sale. At the same time, our report also includes the Absolute Discounts offered during Prime Day, which represents the total markdown relative to the MSRP.

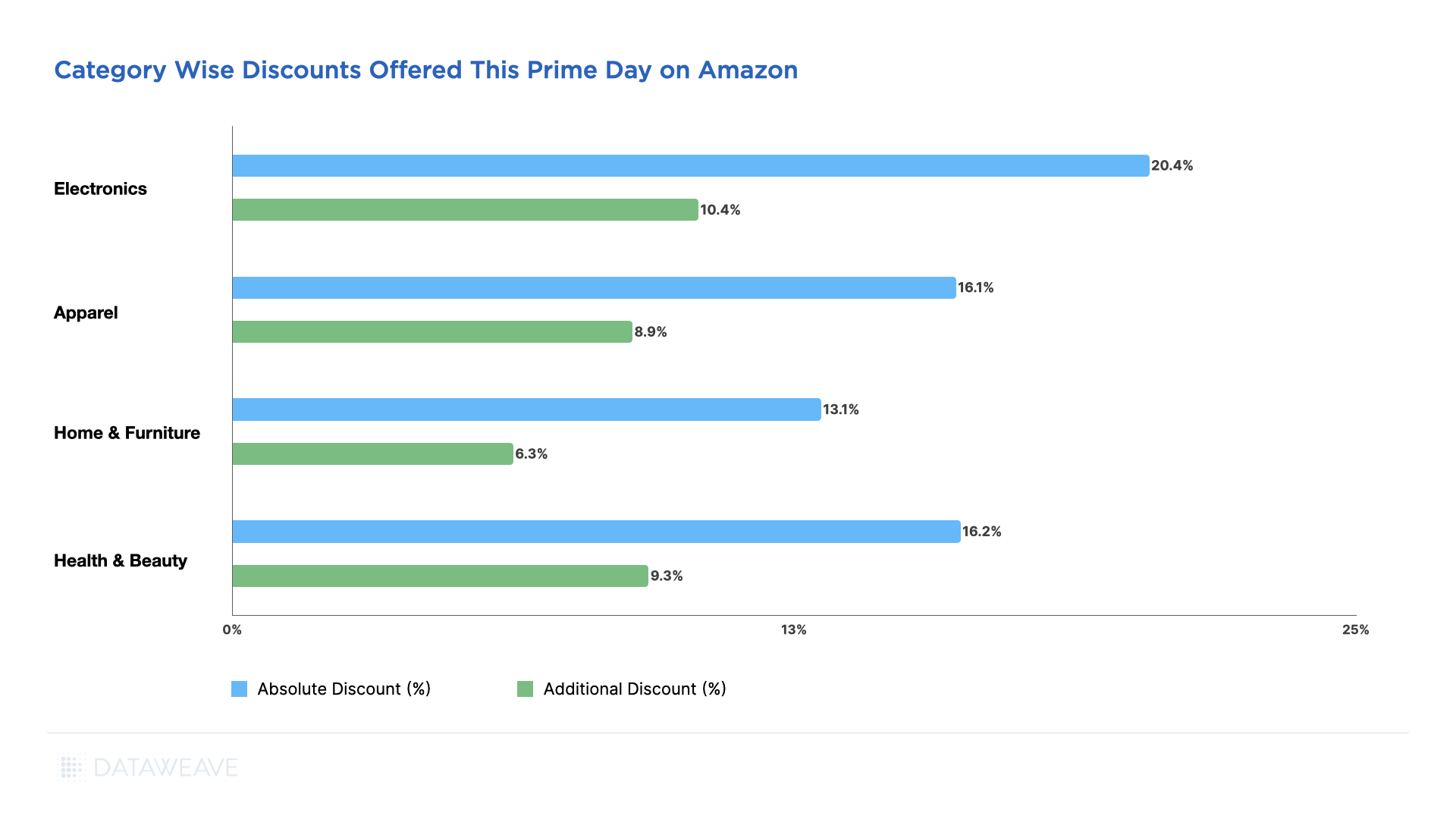

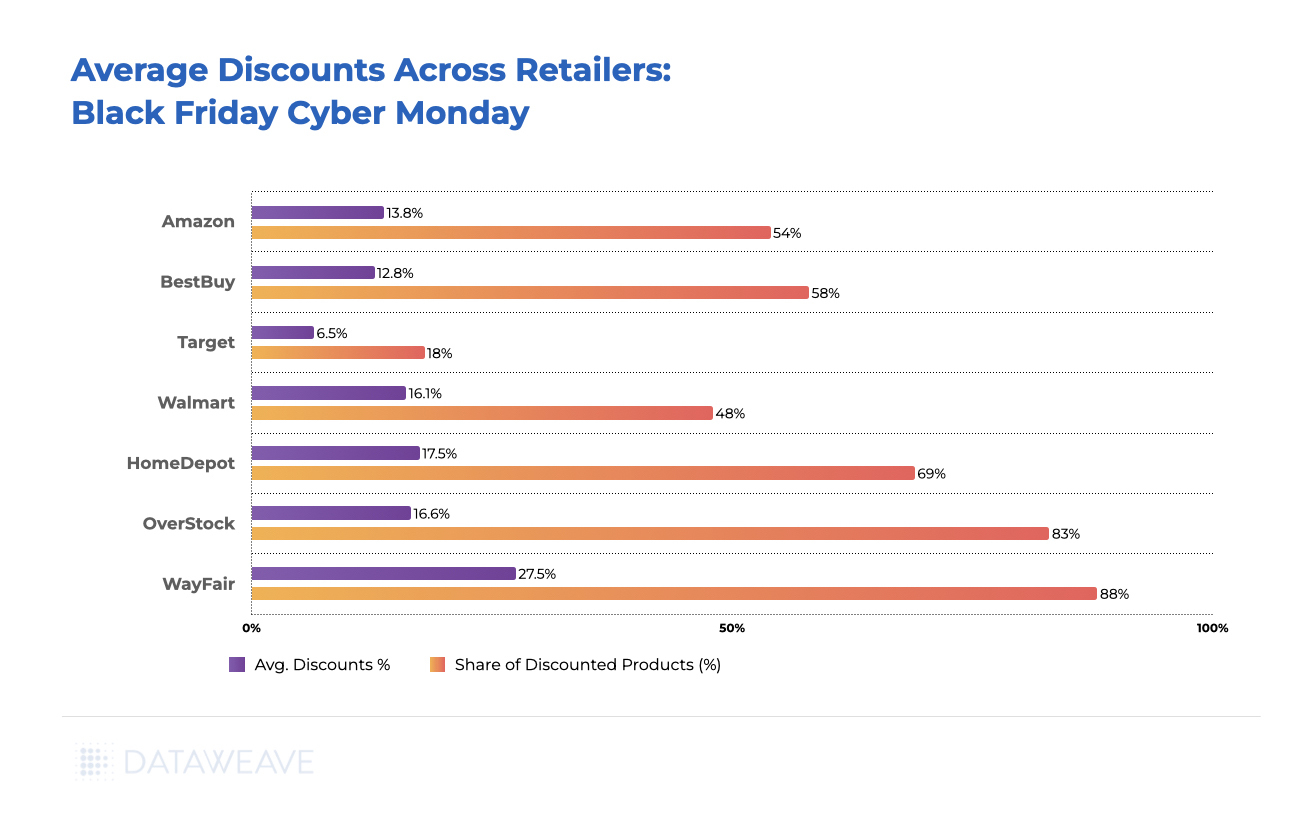

Amazon’s Cross-Category Discount Strategy

Our analysis reveals that the Electronics category saw the highest discounts with an average absolute discount of 20.4% and additional discounts on Prime Day amounting to 10.4%. Meanwhile the Home & Furniture had the lowest discount at 13.1%.

The Health & Beauty category saw significant additional discounts during Prime Day, at 9.26%. The Apparel category offered attractive absolute (16.10%) and additional (8.90%) discounts.

Category Deep Dive

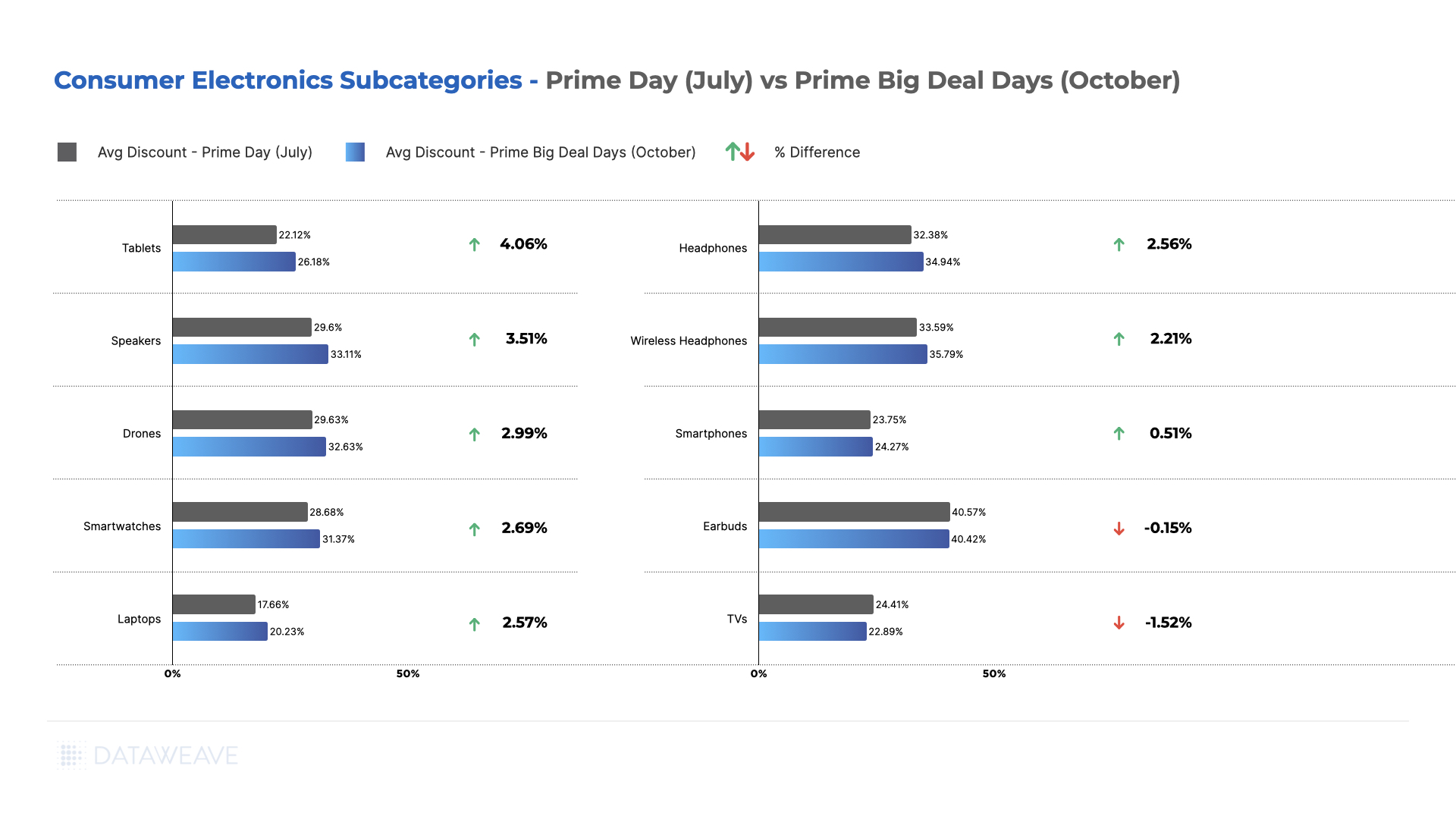

Consumer Electronics

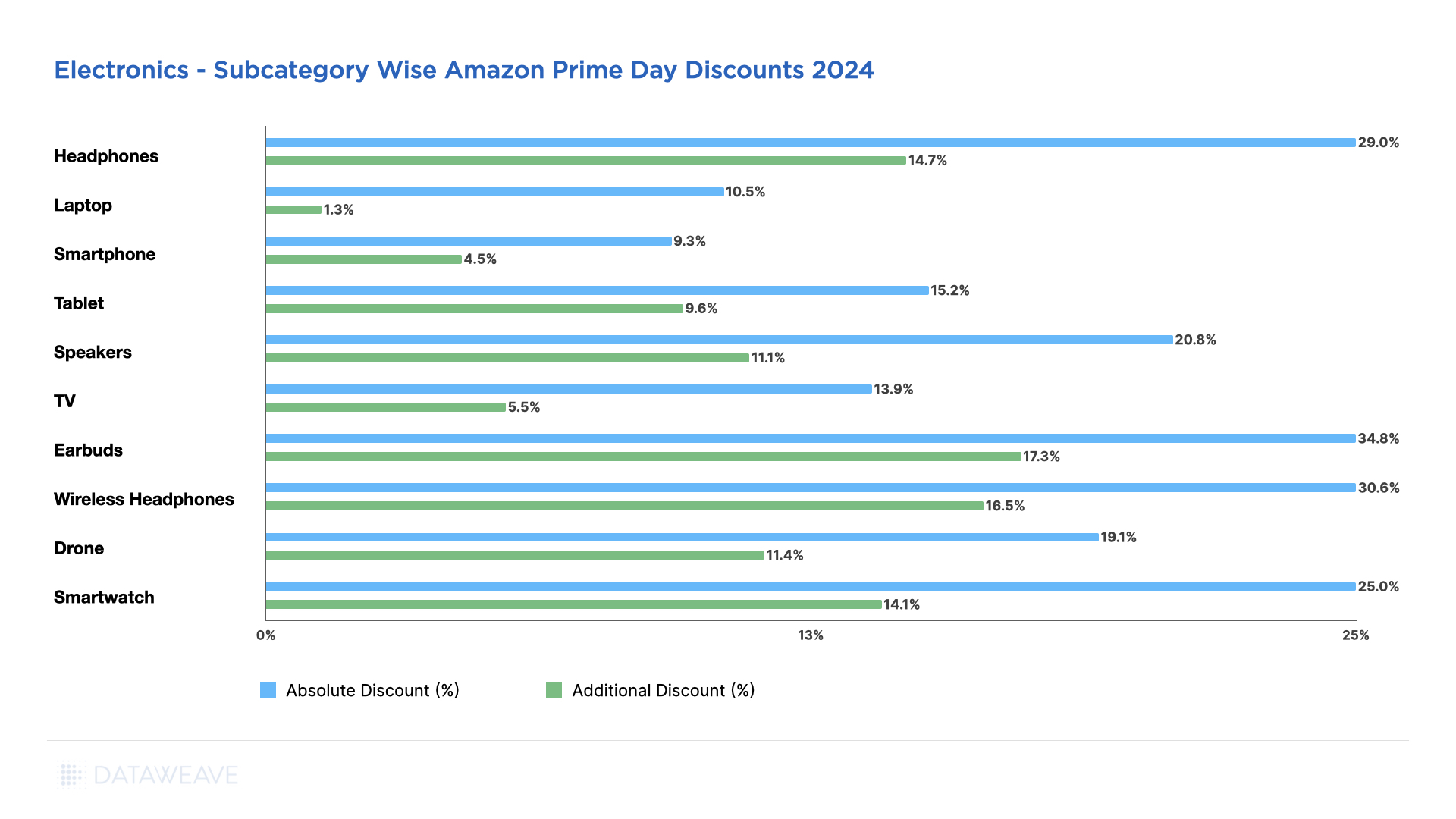

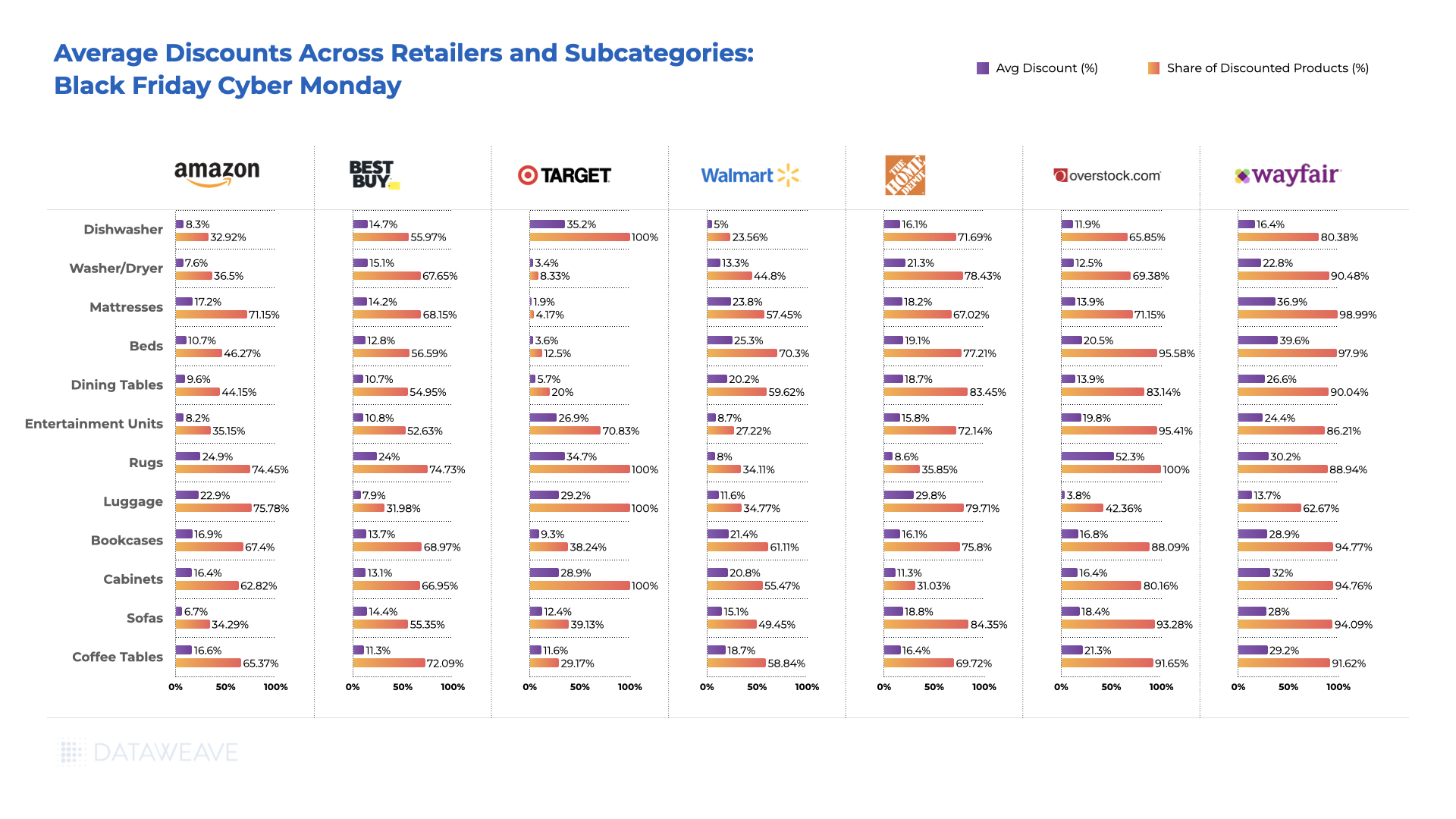

Still the star of the show, the electronics category saw the highest markdowns this Prime Day with absolute discounts at 20.40% and across 14.61% of their inventory.

Across Electronics subcategories, Earbuds had the highest markdowns at 34.80%, followed closely by Wireless Headphones at 30.60% and Headphones at 29.00%, with steep additional discounts during Prime Day as well. Apple AirPods Pro, for example, retailed at $168 (down from $249) at a 32% discount.

Meanwhile, smartphones had the lowest markdowns at 9.30%, followed by Laptops at 10.50%. Laptops also had the lowest additional discount during Prime Day at just 1.28%, significantly lower than other subcategories. Speakers (20.80%), Drones (19.10%), and Smartwatches (25.00%) offered moderate to high markdowns.

Notably, all Amazon products including Kindle, Echo, Echo Earbuds, Alexa, Fire TV, Fire TV Stick, and Fire Tablets, were aggressively discounted upwards of 30% this Prime Day. These products also came with the label “Climate Pledge Friendly.”

These aspects indicate Amazon’s push to promote its own ecosystem of products to the top, as well as cater to changing consumer preferences.

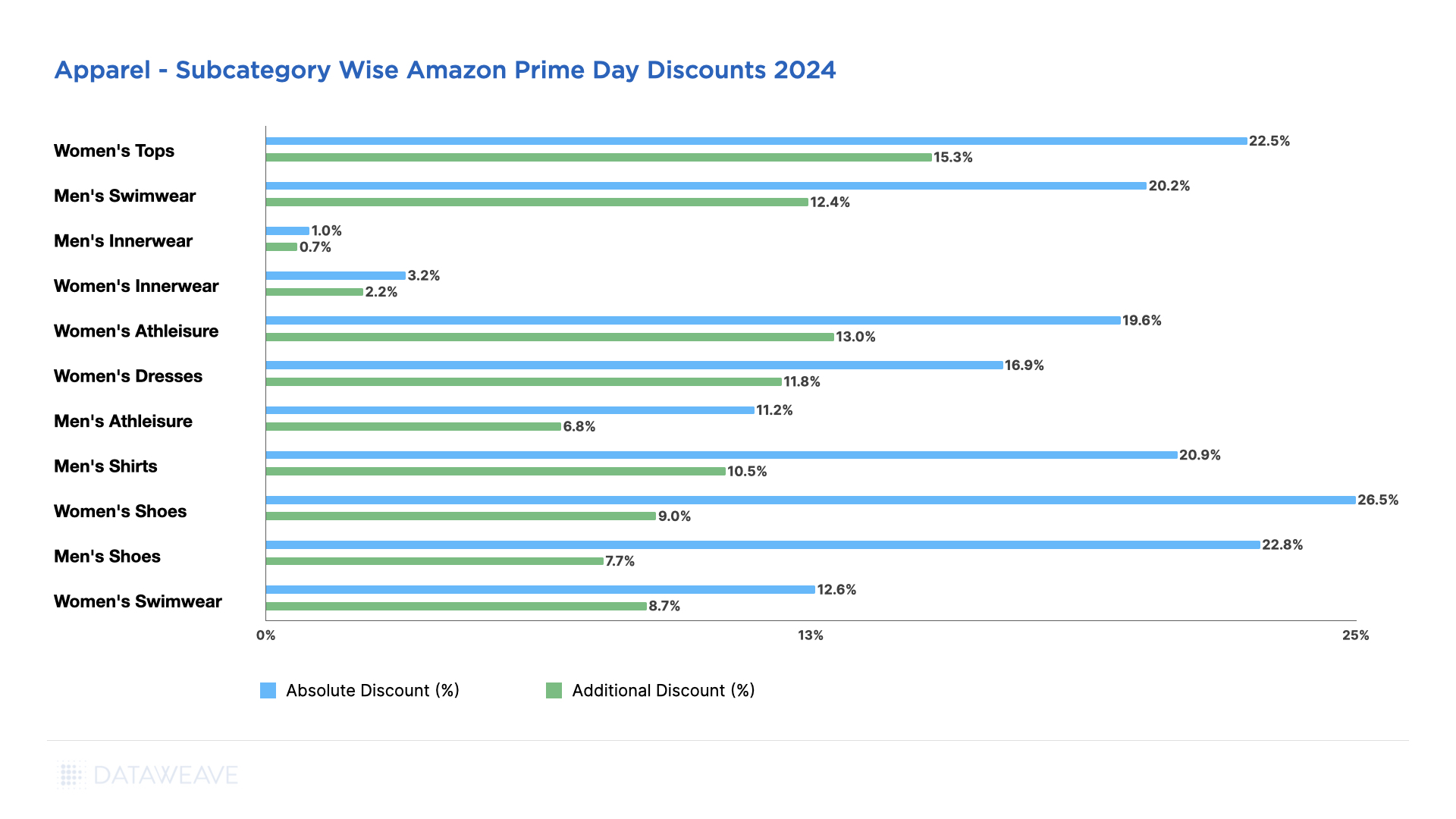

Apparel

Discounts offered this Prime Day increased from 13.2% in 2023 to 16.1% in 2024.

Amid apparel subcategories, Amazon appears to be pushing Women’s apparel categories more aggressively, particularly in Tops, Shoes, and Athleisure.

Women’s Shoes lead with the highest discounts at 26.50%, followed by Women’s Tops at 22.50% and Men’s Shoes at 22.80%. Women’s Tops also maintained the highest additional discount at 15.27%, followed by Women’s Athleisure at 13.03% and Men’s Swimwear at 12.44%.

Similar to 2023, Men’s Innerwear offered significantly lower discounts, with only 1% absolute discount and 0.72% additional discount. Women’s Innerwear also shows low discounts at 3.20% absolute and 2.23% additional.

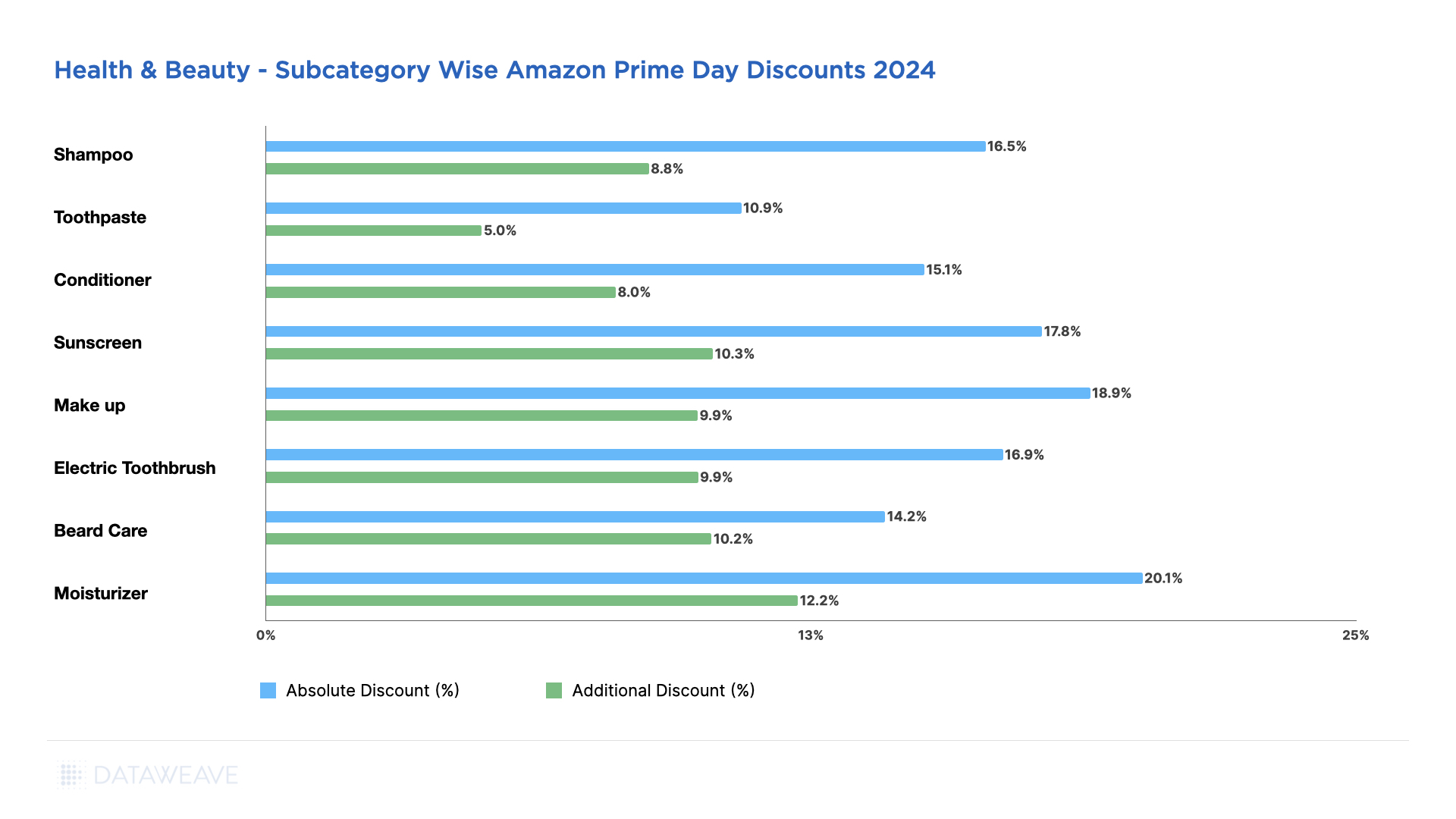

Health & Beauty

Amid health & beauty subcategories, Moisturizes witnessed the highest markdowns at 20.10%, followed by Make Up at 18.90%. The Moisturizer subcategory also offers highest additional discounts at 12.20%, followed closely by Sunscreen at 10.25% and Beard Care at 10.22%.

The Toothpaste subcategory has the lowest discounts, at 10.90%. The lower discounts on everyday essentials like this might indicate a steady demand or an attempt to maintain margins on frequently purchased items.

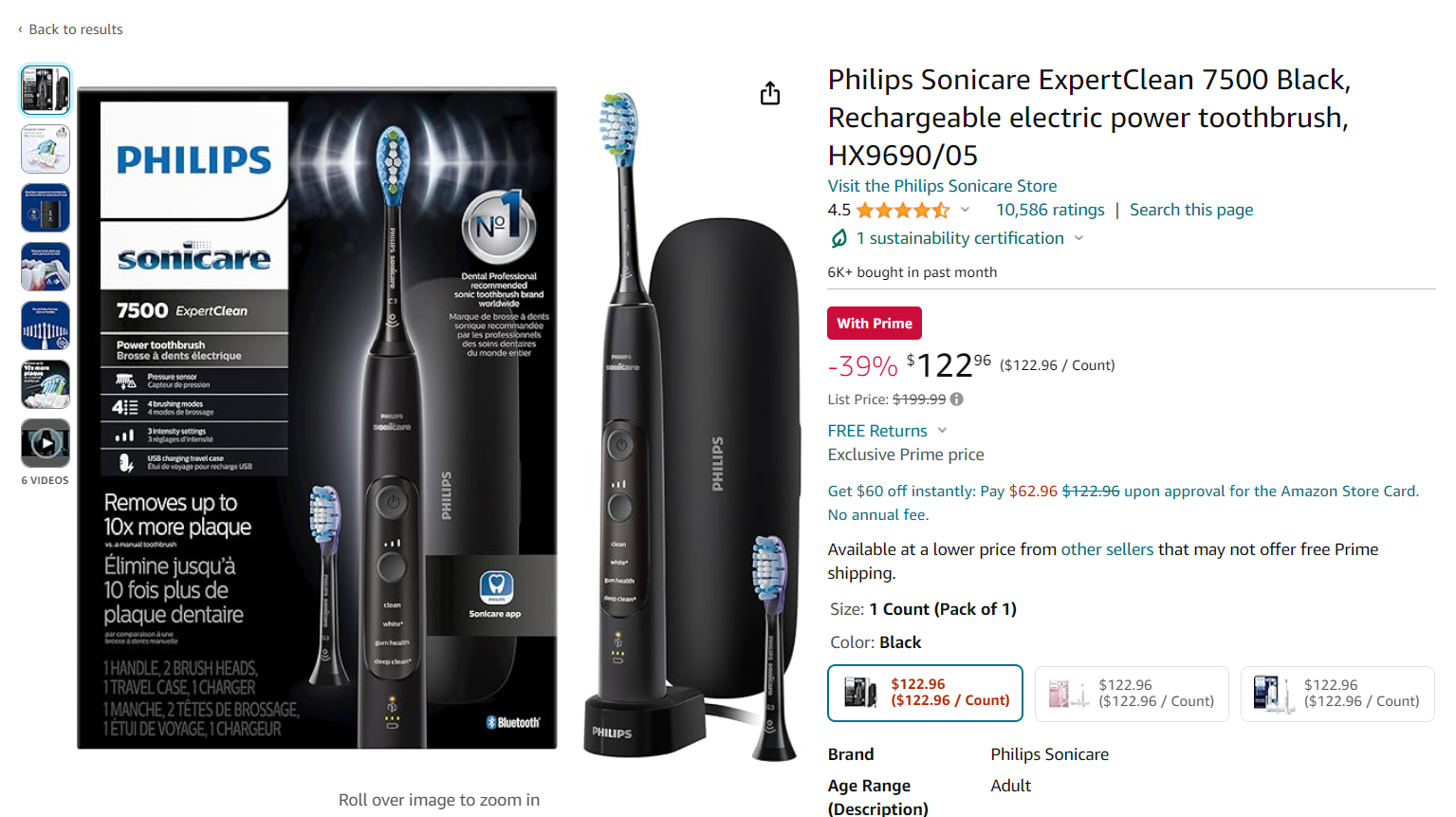

Most Health & Beauty subcategories fall in the 15-18% range for actual discounts and 8-10% range for additional discounts. Electric Toothbrush (16.90% actual, 9.91% additional) and Shampoo (16.50% actual, 8.78% additional) represent the middle of the pack. There were a few highly attractive deals though, such as the Philips Sonicare toothbrush retailing at $122.96 (down from $199.99), with a 39% discount.

Amazon also offered significant discounts on Open Box products (products that are returned, but unused, out of mint condition boxes) to Prime members.

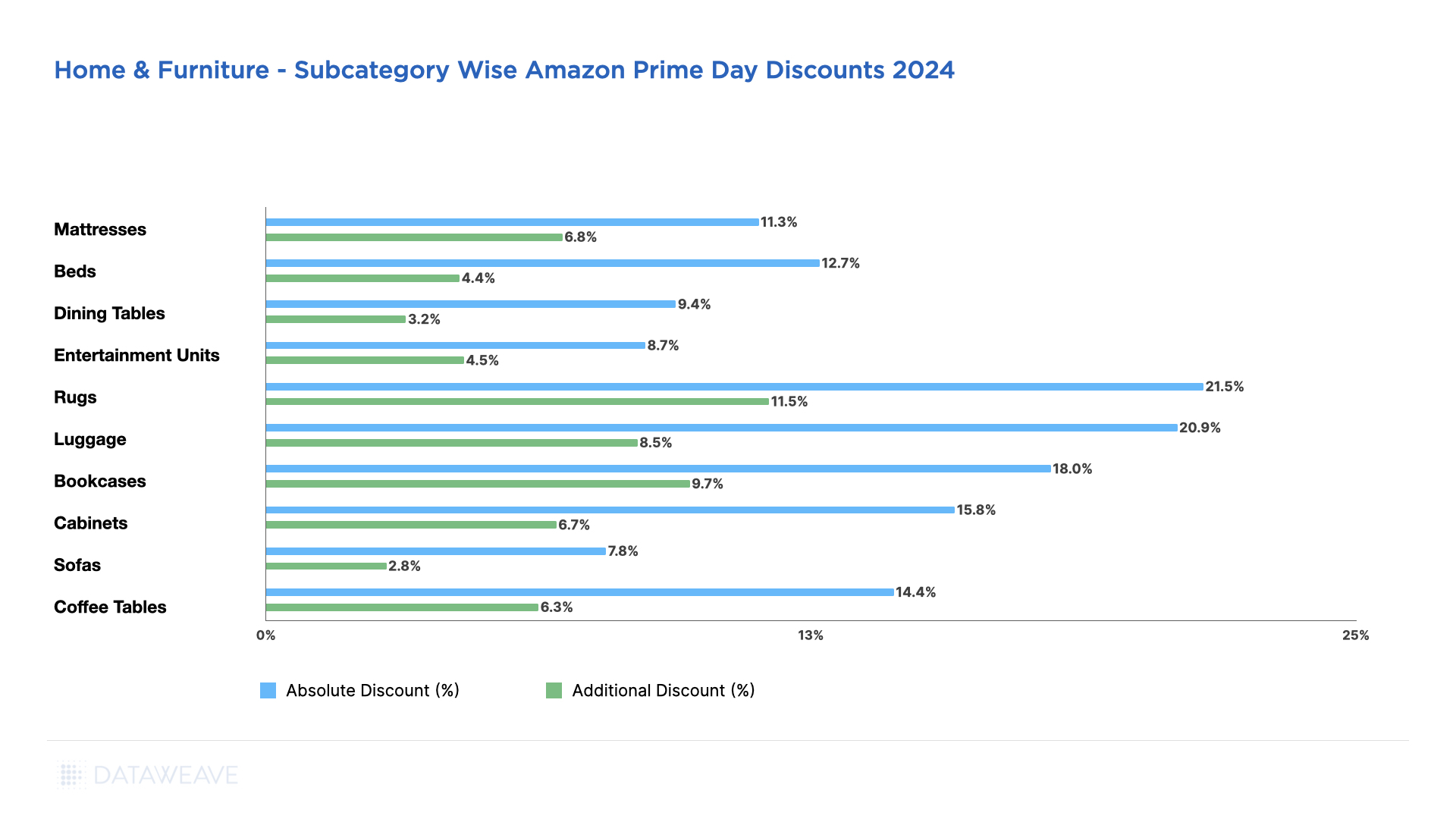

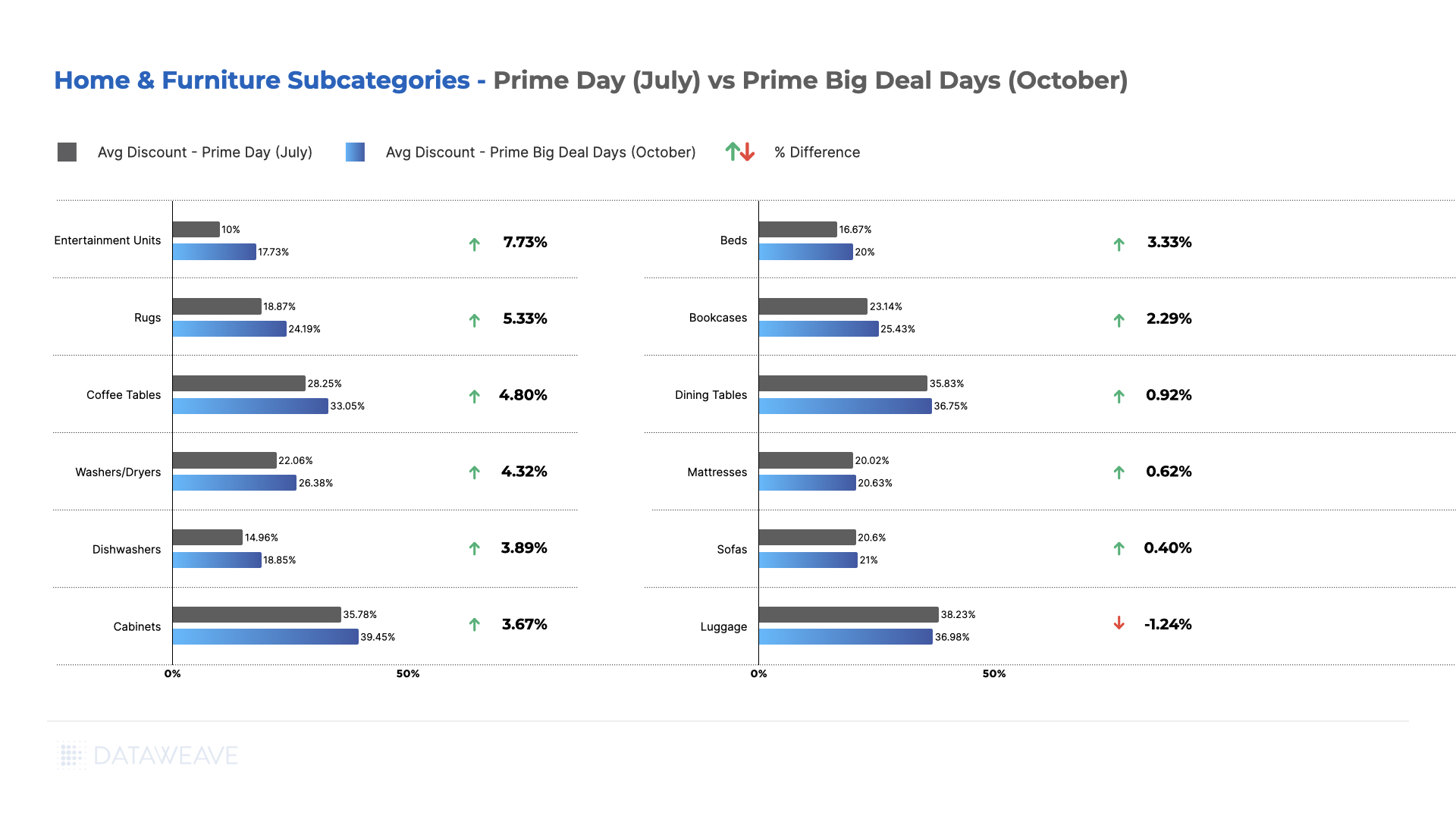

Home & Furniture

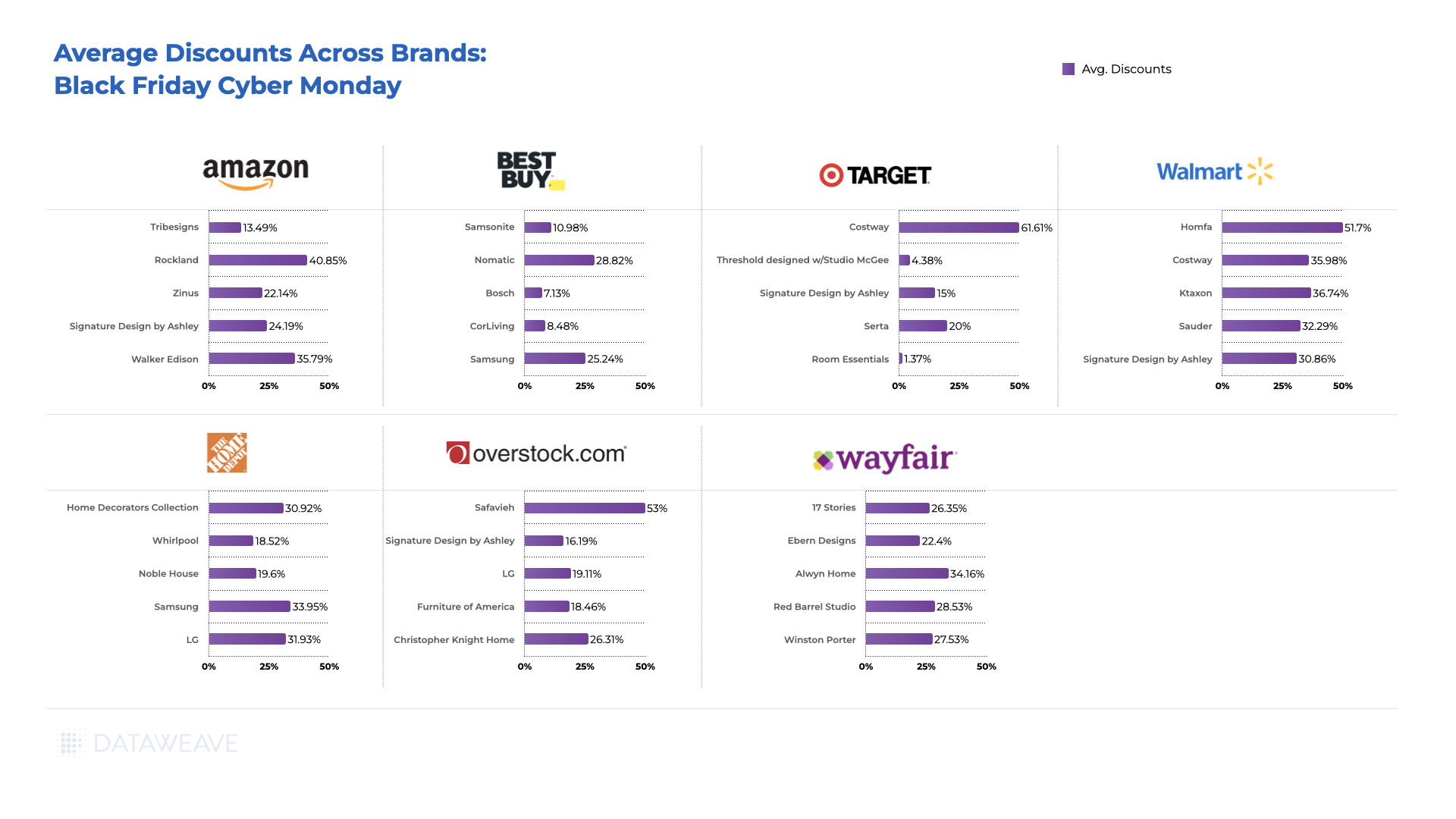

This category saw the lowest discounts for this Prime Day event at 13.1%. Across subcategories, Rugs lead with the highest average discount at 21.50%, closely followed by Luggage at 20.90%. Amazon seems to be pushing decorative and organizational items (Rugs, Bookcases) more aggressively, possibly due to higher margins. Rugs also stood out as the subcategory with the highest additional discount of 11.54%.

Sofas have the lowest additional discount at 2.76%, followed by Dining Tables at 3.21%. Items like Cabinets (15.80% absolute, 6.66% additional) and Coffee Tables (14.40% absolute, 6.25% additional) represent the middle range of discounts.

Watch Out For More

As the holiday season approaches, it’s clear that the retail landscape continues to evolve. While Amazon remains a formidable force, there are opportunities for savvy competitors to carve out their niches and attract deal-hungry shoppers. By analyzing these trends and adjusting strategies accordingly, retailers can position themselves for success in the high-stakes world of summer sales events.

Stay tuned to our blog for more insights on how Amazon’s competitors reacted to Prime Day, and how leading brands across categories fared in terms of their pricing and their visibility during the sale event. Reach out to us today to learn more.

Virtually every cuisine in the world uses eggs. They’re in your breakfast, lunch, dinner, and dessert — which is perhaps why the global egg market is expected to generate $130.70 billion in revenue in 2024 and is projected to grow to approximately $193.56 billion by 2029.

More specifically, the United States is the fourth-largest egg producer worldwide. The country’s egg market is projected to generate $15.75 billion in 2024 and increase to $22.51 billion by 2029.

Health-consciousness among consumers: Consumers value eggs for their essential nutrients and rich protein content.

Demand for convenience foods: Consumers’ preferences are shifting toward quick and easy foods, which drives demand for shell eggs and pre-packaged boiled or scrambled eggs.

Population Growth: A growing worldwide population increases the demand for eggs.

Affordability and accessibility: Eggs are an affordable and accessible nutrient-dense food source for many.

Despite these factors contributing to the U.S. egg market’s growth, recent times have seen egg prices fall dramatically.

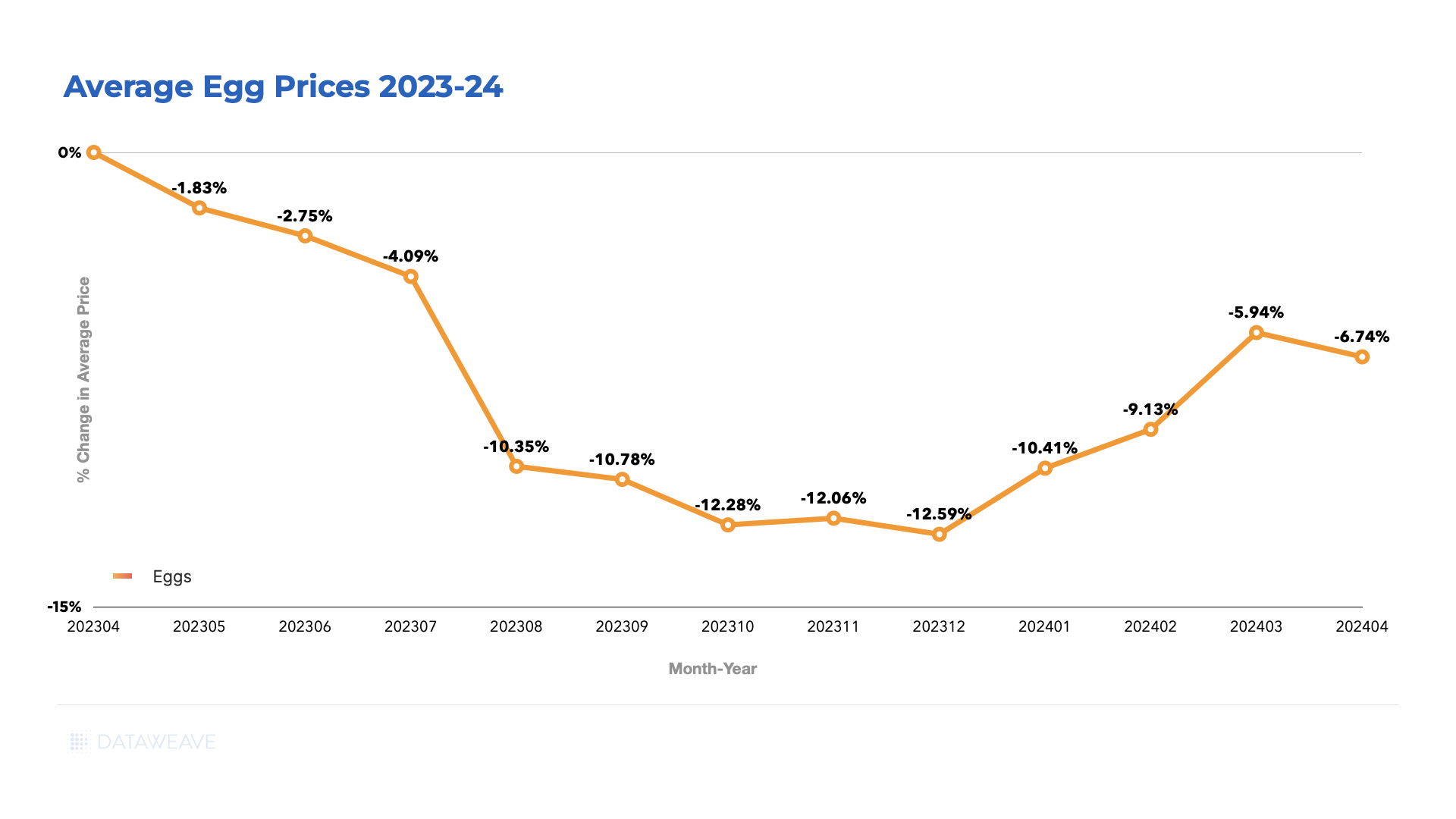

Based on a sample of 450 SKUs, DataWeave discovered that egg prices in the U.S. fell by 6.7% between April 2023 and April 2024, dipping to its lowest (-12.6%) in December 2023.

So, what’s causing the decrease in egg prices?

The Rise and Fall of Egg Prices: A Recent History

In 2022, avian influenza severely impacted the United States. The disease affected wild birds in nearly every state and devastated commercial flocks in approximately half of the country.

The 2022 incident was the first major outbreak since 2015 and led to the culling of more than 52.6 million birds, mainly poultry, to prevent the disease from spreading uncontrollably.

With almost 12 million fewer egg-laying hens, the United States produced around 109.5 billion eggs in 2022 — a drop of nearly two billion from the previous year.

Consequently, the cost of eggs soared, peaking at $4.82 a dozen — more than double the price of eggs in the previous year.

The avian flu continues to affect egg-laying hens and other poultry birds across the United States. As of April 2024, farms have killed a total of 85 million poultry birds in an attempt to contain the disease.

Despite the disease’s effects, production facilities have made significant efforts to repopulate flocks, leading to a steady increase in supply – and a much anticipated decrease in egg prices.

According to the U.S. Bureau of Labor Statistics, there was an increase in producer egg prices in 2022, reaching a peak in November 2022, at which point they began to fall.

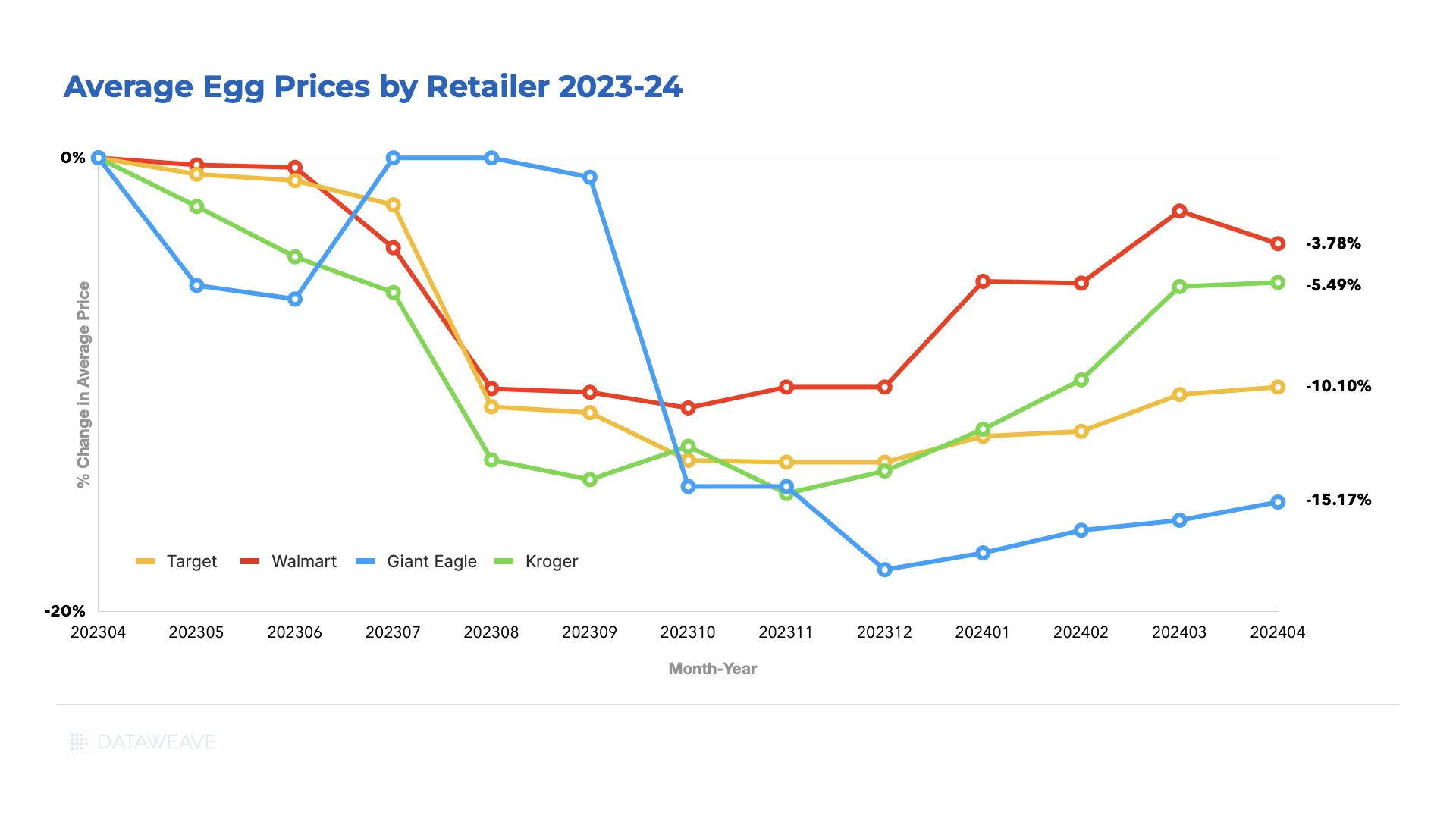

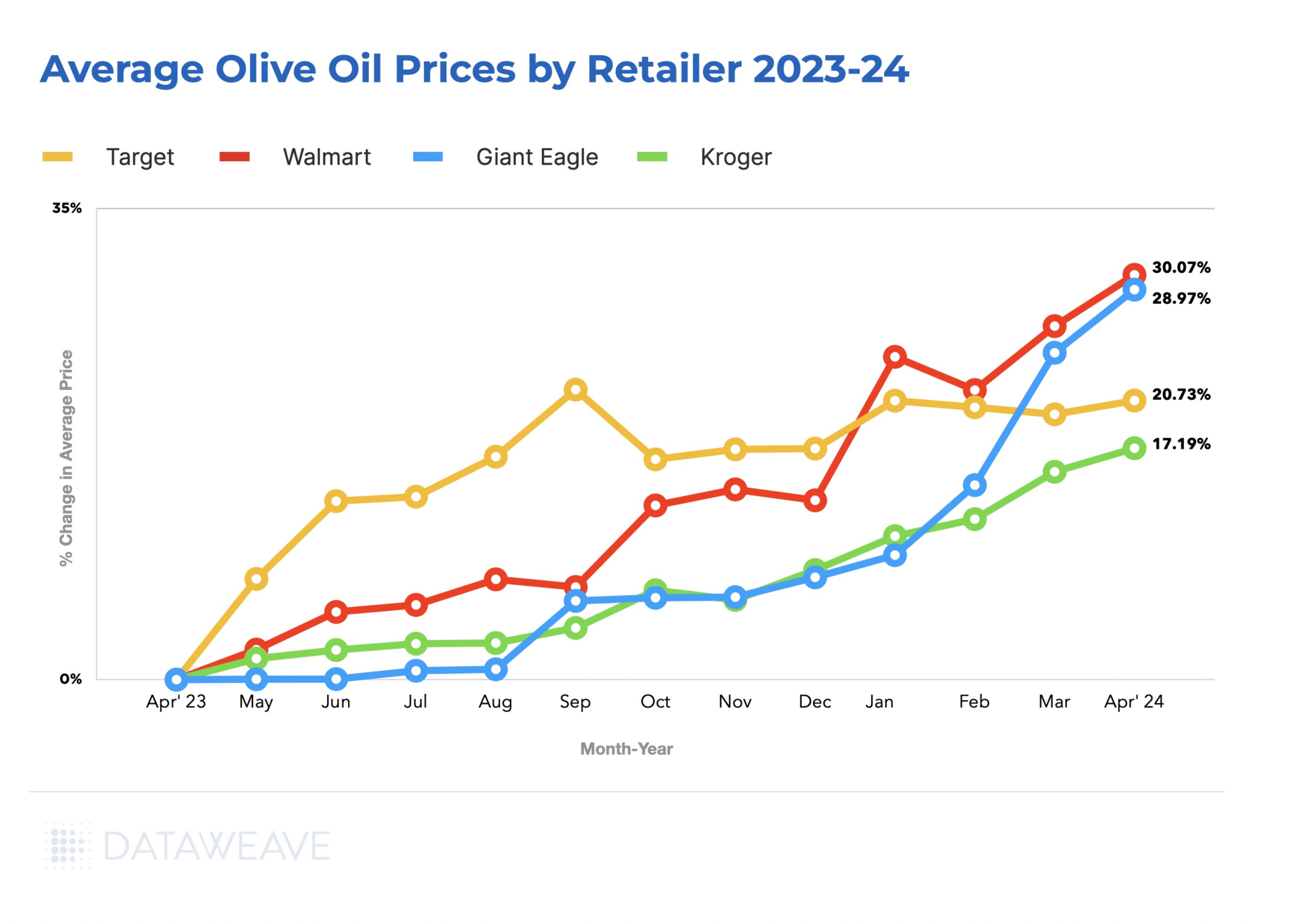

Retailer’s egg prices followed suit. The egg price chart below depicts retailers’ declining egg prices over one year, from April 2023 to April 2024, with Giant Eagle showing the most significant price reductions and Walmart the least.

What Does the Future Hold for Egg Prices?

The USDA reported recent severe avian flu outbreaks in June 2024. These outbreaks are estimated to have affected 6.23 million birds.

With a reduction in egg-laying hens, egg prices are likely to increase — time will tell.

Nonetheless, the annual per capita consumption of eggs in the U.S. is projected to reach 284.4 per person in 2024 from 281.3 per person in 2023. So for now, producers and retailers can rest assured of the growing demand for eggs.

How Can Retailers Adapt to the Unpredictability of Egg Prices?

Egg prices were down to $2.69 for a dozen in May 2024. However, they are still significantly higher than consumers were used to just a few years ago—eggs were, on average, $1.46 a dozen in early 2020.

Additionally, while the avian flu puts pressure on producers, inflation and supply chain disruptions exert pressure on retailers.

With such challenging egg market conditions, what can retailers do to maintain customer loyalty amid reduced consumer spending while maintaining profitability?

1. Give the Customer What They Want: Increase Offerings of Organic, Cage-Free, and Free-Range Eggs

As mentioned, Data Bridge Market Research’s trends and forecast report highlighted a significant increase in consumer health consciousness. Additionally, animal welfare increasingly influences consumers’ purchasing decisions when buying meat and dairy products.

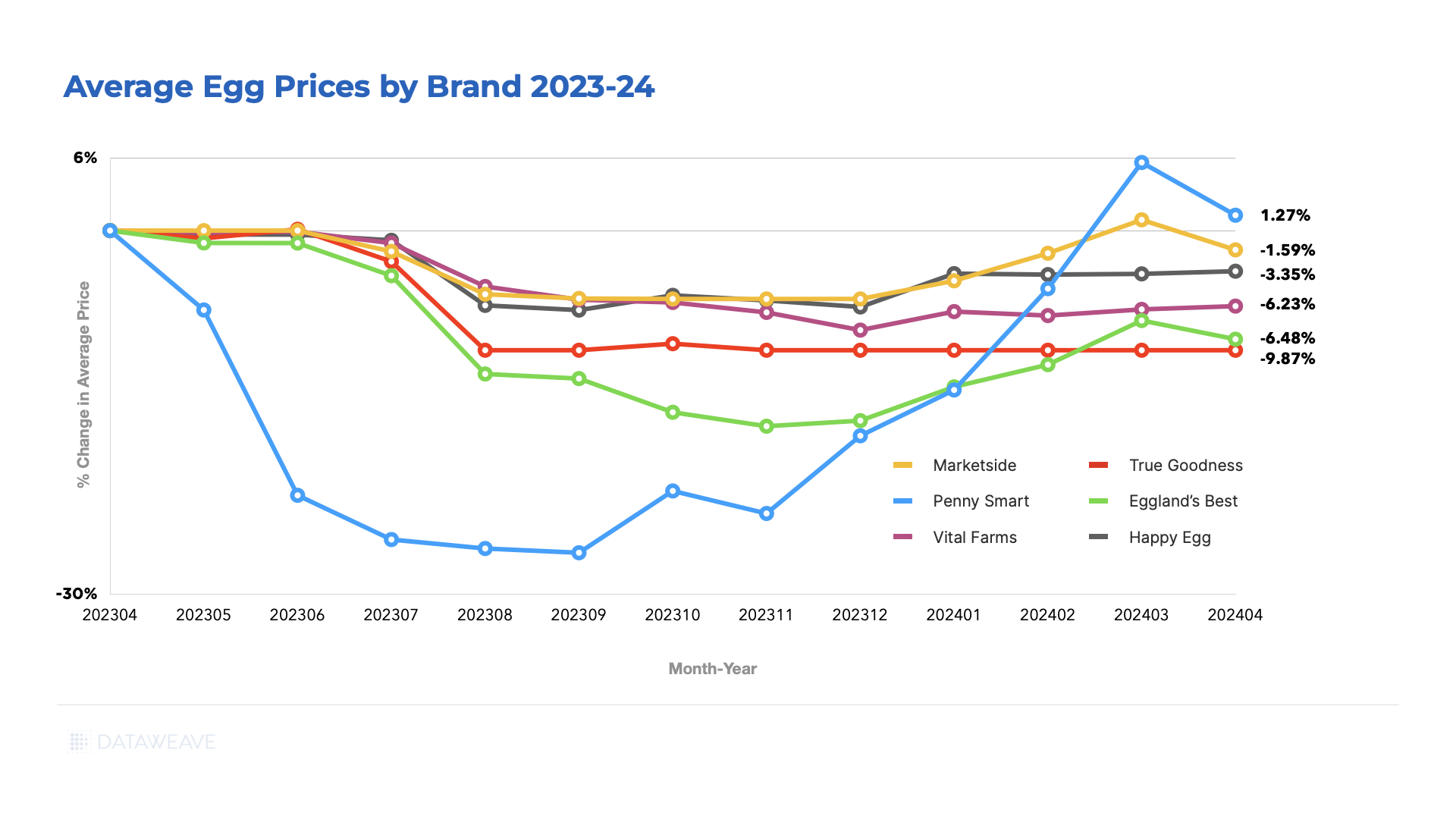

DataWeave data shows that the prices of organic, cage-free, and free-range eggs—such as those by brands like Happy Eggs and Marketside—have fallen less than those of non-organic, caged egg brands.

2. Increase Private-Label Offerings

Private labels typically offer retailers higher margins than national brands. These margins can shield consumers from sudden wholesale egg price swings, helping to preserve brand trust and consumer loyalty without sacrificing profitability.

Moreover, eggs are particularly suited to private labeling, given their uniform appearance and taste and the lack of product innovation opportunities.

Undoubtedly, this is why sales of private-label eggs dwarf sales of national egg brands in the United States. Statista reports that across three months in 2024, private label egg sales amounted to $1.55 billion U.S. dollars, while the combined sales of the top nine national egg brands totaled just $617.88 million U.S. dollars.

3. Price Intelligently

With the current and predicted fluctuations in egg prices over the foreseeable future, price competitiveness is paramount to margin management and customer loyalty.

This is especially true when lower prices are the primary factor influencing the average consumer’s choice of supermarket for daily essentials purchases.

AI-driven pricing intelligence tools like DataWeave give retailers valuable highly granular and reliable insights on competitor pricing and market dynamics. In today’s data-motivated environment, these insights are necessary for competitiveness and profitability.

Final Thoughts

Egg prices have fluctuated significantly due to the impact of avian flu. Despite recent price drops, future egg price increases are possible due to ongoing outbreaks. Retailers should adapt to unstable egg prices by increasing organic, free-range, cage-free, and private-label egg offerings while leveraging AI-driven pricing tools to maintain margins and customer loyalty.

Olive oil, renowned for its complex flavor and myriad health benefits, holds a significant place in the global market, valued at $14.64 billion in 2023. It is anticipated to reach $19.77 billion by 2032, with a steady compound annual growth rate (CAGR) of 3.42%.

This growth is fueled by:

Increased consumer demand for healthier oils.

Olive oil’s rising popularity in skincare products.

Greater retail availability.

Interestingly, this market expansion occurs alongside rising olive oil prices, mainly due to a notable decrease in production. Eight European Union countries, which are the main producers, saw a dramatic drop in output from an average of 2.17 million tons to just 1.50 million tons in 2022—a 30.88% decline. Unfortunately, this drop in production comes as no surprise.

Erratic weather patterns, rising temperatures, and exacerbating drought conditions in the Mediterranean basin have taken their toll. These climate changes disrupt the growing cycles of olive trees, leading to poorer crop yields and lower-quality olives.

In the US, where olive oil constitutes 19% of all cooking oils sold and 40% of sales value due to its premium pricing, the market is expected to grow at an impressive CAGR of 11.31% between 2024 and 2032. This forecast is significant despite a recent dip in domestic consumption, which may further decline due to economic pressures. As a result, consumers must make difficult choices as they battle inflation, shrinkflation, and thin budgets.

DataWeave’s Analysis of Rising Olive Oil Prices

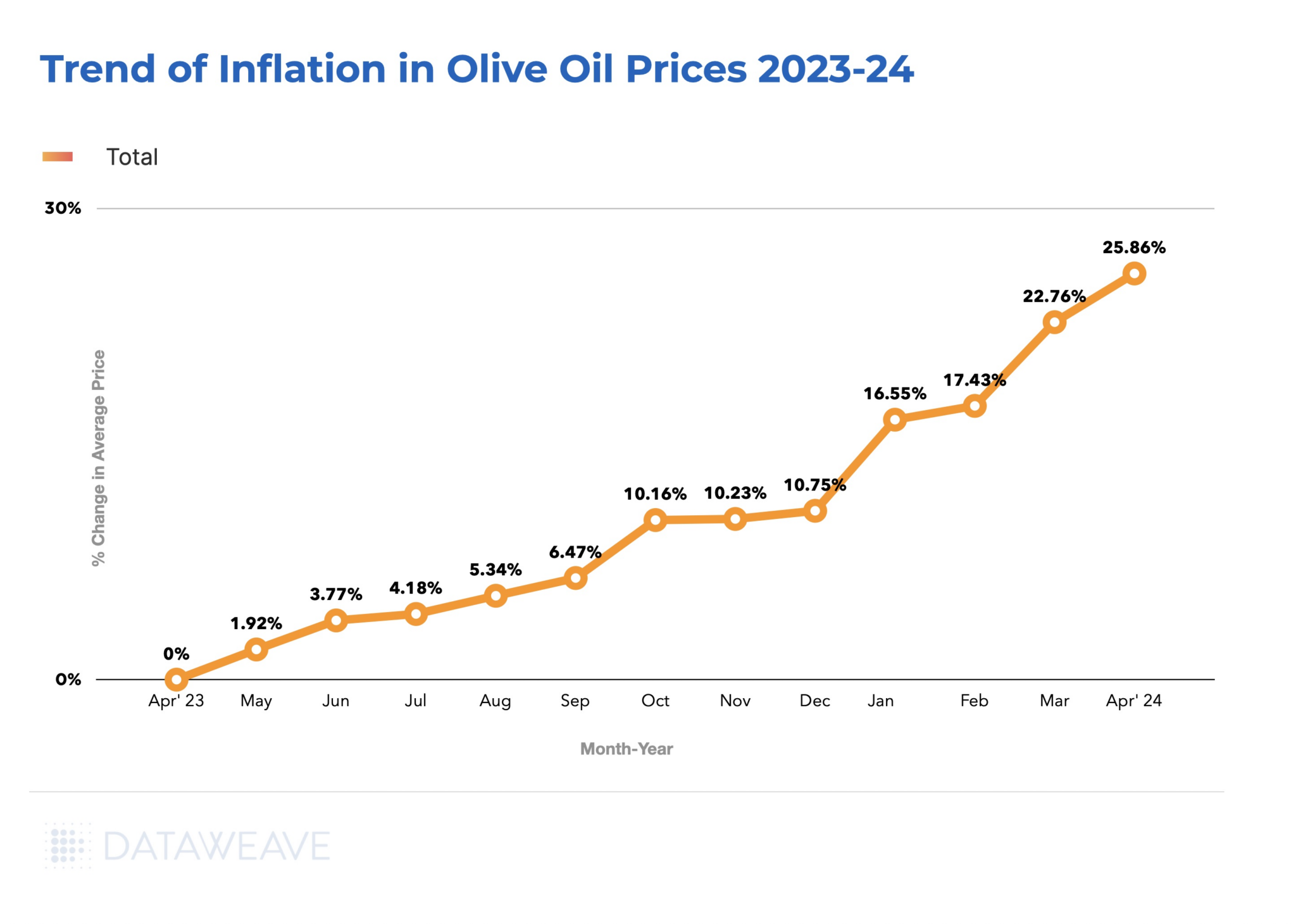

At DataWeave, we utilized our advanced AI-powered data aggregation and analysis platform to scrutinize the pricing trends of olive oils across key US retailers over the past year. Our analysis covered 130+ SKUs from major chains including Walmart, Kroger, Giant Eagle, and Target.

The data revealed a notable escalation in olive oil prices, with consumers facing a sharp 25.8% increase from April 2023 to April 2024.

This trend of rising costs was consistent across all analyzed retailers. Specifically, Walmart and Giant Eagle each reported a substantial 30% increase in their olive oil prices over the past year. In contrast, Target and Kroger experienced somewhat more modest hikes, at 20% and 15% respectively.

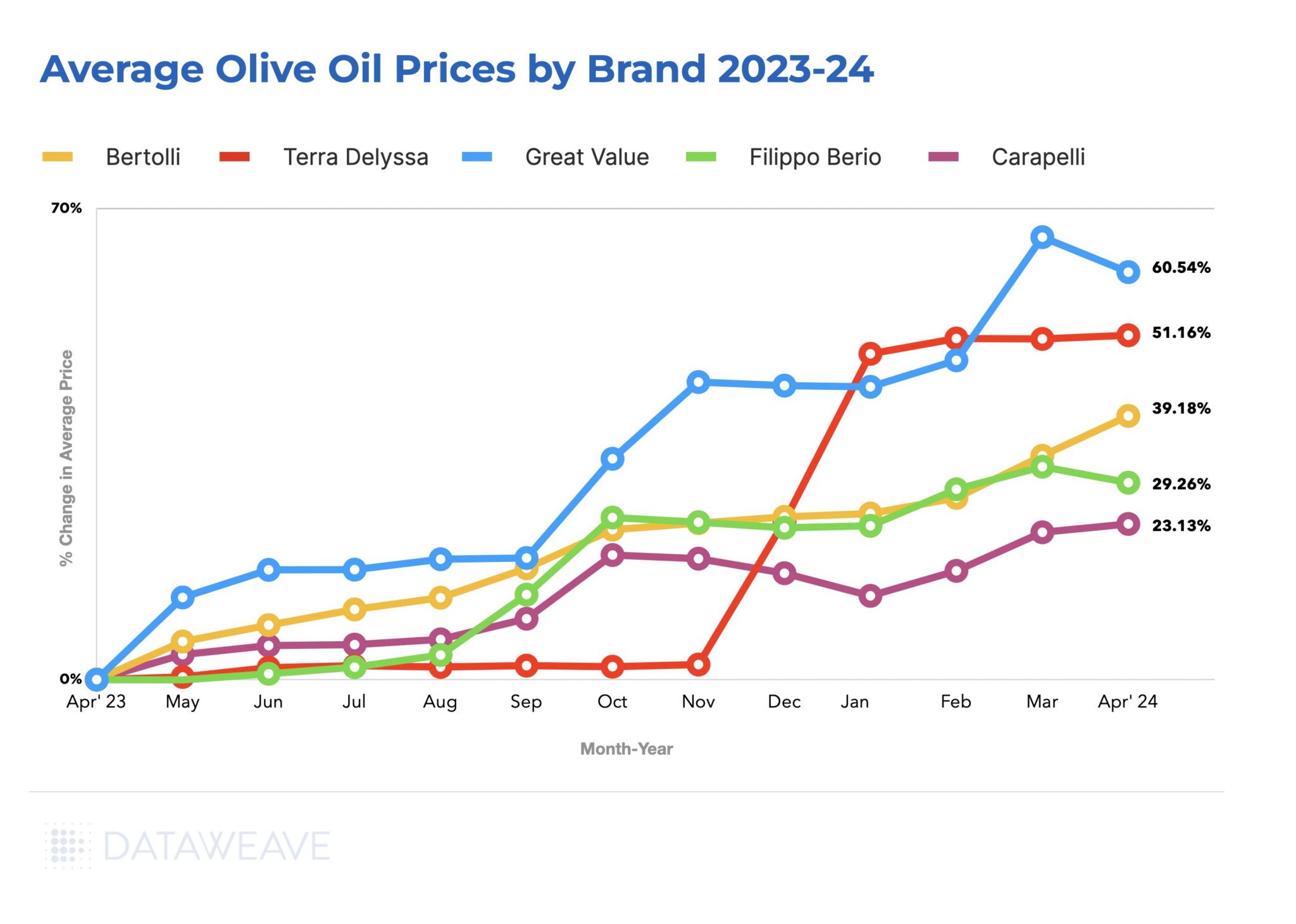

Further investigation into individual brands within our sample highlighted that no brand is immune to the impacts of the ongoing supply shortages. Walmart’s own Great Value brand saw an exceptional 60% surge in prices. Other prominent olive oil brands such as Carapelli, Terra Delysia, and Bertolli also faced significant price increases, ranging from 20% to 50%.

This across-the-board rise in prices underscores the widespread effect of supply constraints on the olive oil market, affecting both premium and private label brands alike.

What Strategies Can Retailers and Brands Employ?

In a market where consumer preferences and price sensitivities are rapidly evolving, retailers and brands must adopt versatile strategies without compromising on profit margins.

Diversifying Brand Selection

Retailers can enhance their appeal by offering a diverse range of olive oil brands, thereby stimulating competition among brands based on price, quality, innovation, and customer satisfaction. A well-curated selection that includes well-known brands like Filippo Berio and Bertolli, alongside emerging labels such as Terra Delyss, and premium options like Carapelli, allows retailers to meet a wide array of consumer preferences and budgets.

For premium outlets, it might be beneficial to introduce more economical options than typically offered to attract budget-conscious consumers. Employing advanced assortment intelligence tools can provide retailers with crucial data, helping them make informed decisions about which brands to stock and promote, ensuring they meet consumer demand effectively while managing inventory costs.

Data-driven Pricing

With rising olive oil prices, competitive pricing is more crucial than ever. Retailers must strive to balance competitiveness with margin preservation. It’s essential for retailers to not just passively respond to market price increases but to actively ensure that their offerings are competitively priced relative to the market.

This involves using sophisticated pricing intelligence tools, such as those provided by DataWeave, which track market trends and competitor pricing actions. These tools enable retailers to implement dynamic pricing strategies that respond promptly to market conditions and consumer demand shifts, helping to optimize sales and profitability.

Diversifying Sourcing

The traditional powerhouses of olive oil production, Spain and Italy, are now facing stiff competition from countries like Turkey and Tunisia. This shift is influenced by various factors, including currency fluctuations and changing trade policies, such as the imposition of tariffs on European olive oils by significant importers like the US. Retailers can take advantage of these changes by diversifying their sourcing strategies to include olive oil from non-traditional regions.

The 2022/2023 season saw remarkable production levels from countries outside the Mediterranean basin, with Iran and China setting new production records. By broadening their supply chains to incorporate these emerging markets, retailers can benefit from lower production costs and introduce unique products to their consumers, enhancing both competitiveness and profit margins.

Double Down on Private Labels

Large retailers have successfully used their scale to develop strong private-label brands that can buffer consumers from price hikes in the olive oil market. By focusing on expanding and promoting their private-label offerings, retailers can provide cost-effective alternatives to national brands.

Private labels generally have lower price points, making them particularly attractive during times of economic pressure and market volatility. Additionally, the development of private labels allows retailers to control more of their supply chain, from pricing to packaging, enabling them to offer high-quality products at competitive prices, thereby retaining customer loyalty and enhancing market share.

Navigating Market Pressures

High olive oil prices impact the entire supply chain, presenting varied challenges and opportunities:

Producers benefit from higher revenues but face increased pressure to maintain quality and yields in challenging climates. Adapting to these conditions with sustainable practices is crucial.

Exporters and Importers navigate tighter margins and greater risks due to tariffs and volume restrictions, requiring agility and strategic planning to adapt to market changes.

Retailers must carefully balance competitive pricing with rising procurement costs, affecting consumer affordability and potentially leading to shifts in buying patterns.

Consumers may seek cheaper alternatives or reduce their olive oil consumption, which influences overall market demand and pricing stability.

These dynamics underscore the necessity for retailers and brands to adopt innovative and proactive strategies to navigate the volatile olive oil market effectively. By focusing on adaptive pricing, diversified sourcing, and customer engagement, businesses can enhance their resilience and secure long-term success in this competitive landscape.

In the cutthroat world of retail, where razor-thin margins and fierce competition reign supreme, pricing becomes your secret weapon to driving sales. The magic bullet unlocks sales, attracts customers, and ultimately fuels your bottom line. But with ever-changing market trends and competitor tactics shifting constantly, effective pricing strategies become even more crucial.

A recent Bain & Company study highlights this very point. 78% of respondents acknowledged that their pricing decisions could be improved, leaving significant revenue untapped. John Furner, President and CEO of Kroger, echoes this sentiment. In a press release announcing a new pricing strategy, he emphasized their commitment to “providing our customers with predictable, affordable prices on the products they need most.” This focus on transparent and consistent pricing reflects the growing importance of building trust with customers, where value goes beyond just the lowest price tag.

The right pricing strategy can unlock a treasure trove of benefits for retailers, including attracting new customers, boosting sales, and ultimately increasing their bottom line.

But here’s the challenge: keeping pace with market trends and competitor strategies requires constant vigilance. This is where an advanced, user-centric pricing intelligence tool comes into play. Retailers need a platform specifically designed to address their unique challenges. It should empower them to protect margins, create a seamless pricing process, and attract and retain price-sensitive customers. To help you navigate this landscape, we’ve identified the must-have capabilities of a pricing intelligence solution that will transform your pricing strategy and propel your business toward long-term success.

1. Reliable and Accurate Data Collection

Retailers need a competitive intelligence solution that goes beyond merely capturing information en masse from competitor sites. An ideal solution ensures that data is consistent, extensive, and highly accurate, with an added level of granularity. This is achieved through statistical process control methods for data quality assurance, enabling highly accurate data capture and processing.

Such a platform should be capable of scraping data from various sources, including desktop sites, mobile sites, and mobile applications, as well as a variety of online platforms: aggregators, omnichannel retailers, delivery intermediaries, quick commerce platforms, D2C sites, and more. This versatility ensures that data is captured across any global region and in dozens of languages, making the system geography and language agnostic.

DataWeave’s solution includes a fast and automated data source configuration system, enabling a swift setup of new web sources for data capture. This capability ensures that retailers can stay ahead of the curve as the market landscape and competitor strategies evolve.

An effective competitive pricing intelligence solution allows retailers to move away from working with incomplete or inaccurate data and instead leverage a comprehensive information stream to create strategic pricing decisions and optimize their overall business strategy. At the end of the day, the insights you base your decisions on are only as good as the data you aggregate. Even with the world’s best analytics engine, it’s always a case of “garbage in, garbage out.”

2. Hyperlocal Insights From Store-Level Data

Monitoring pricing and availability across specific stores is crucial for retailers to gain critical insights into a vast network of locations, enabling them to make strategic decisions that enhance pricing strategies and supply chain effectiveness, thereby minimizing stockouts or pricing inefficiencies in key markets. A platform like DataWeave provides retailers with a comprehensive view of store-level data across ZIP codes, maintaining a hyperlocal competitive strategy. It offers detailed visibility into product availability, highlighting out-of-stock scenarios across different competitors. This capability is invaluable, allowing quick identification of price improvement opportunities and providing retailers with a bird’s eye view of where products can be priced higher than usual to gain margins.

The system operates at configurable intervals—daily, weekly, or monthly—enabling retailers to keep a vigilant eye on pricing, product availability, and delivery timelines based on the selected fulfillment option. Unlike many other providers who offer limited insights from a sample of stores, this solution delivers exhaustive analytics from every storefront. This comprehensive approach grants retailers (and brands) a strategic edge, facilitating efficient inventory tracking, precise pricing adjustments, and rapid responses to fluctuating market dynamics.

3. Sophisticated, AI-Powered Product Matching

A solution that matches products accurately at scale is essential for a robust and reliable competitive pricing strategy. Advanced platforms use unified systems for both text and image recognition to accurately match similar SKUs across thousands of eCommerce stores and millions of products. Deep learning architecture is employed to develop unique AI that matches text and images, grouping similar products based on their features, ensuring accurate matches even for private label products.

This AI identifies critical elements of products in images, such as focusing on the top half of a model wearing a shirt, the sleeve length, the color of the product, etc.. Deep learning models, trained on extensive datasets of images, enhance these images by removing irrelevant background details and improving the quality of the core product image. Innovative AI then extracts unique signatures from the photos, allowing for quick and efficient identification and grouping of products across billions of indexed items.

No matter how powerful the AI, combining it with human expertise is key to achieving true data veracity—ensuring accuracy, freshness, and comprehensive coverage required for reliable product matching. A human-in-the-loop approach elevates the AI-powered product matching process by addressing key challenges. AI algorithms may initially identify product matches with 80-90% accuracy, but human validation corrects errors, pushing accuracy closer to 100%. Humans apply contextual judgment for subjective criteria like aesthetics and design, making nuanced decisions that quantitative rules might miss. Continuous learning through an iterative feedback loop allows AI models to quickly adapt to changing trends and preferences as human experts provide context and re-label incorrect predictions. By integrating AI’s automation and scale with human validation, judgment, and knowledge curation, pricing intelligence solutions can achieve the accuracy and coverage necessary for actionable competitive pricing insights.

This approach results in retailers being able to match products and compare prices between identical products, similar products, and private label brands.

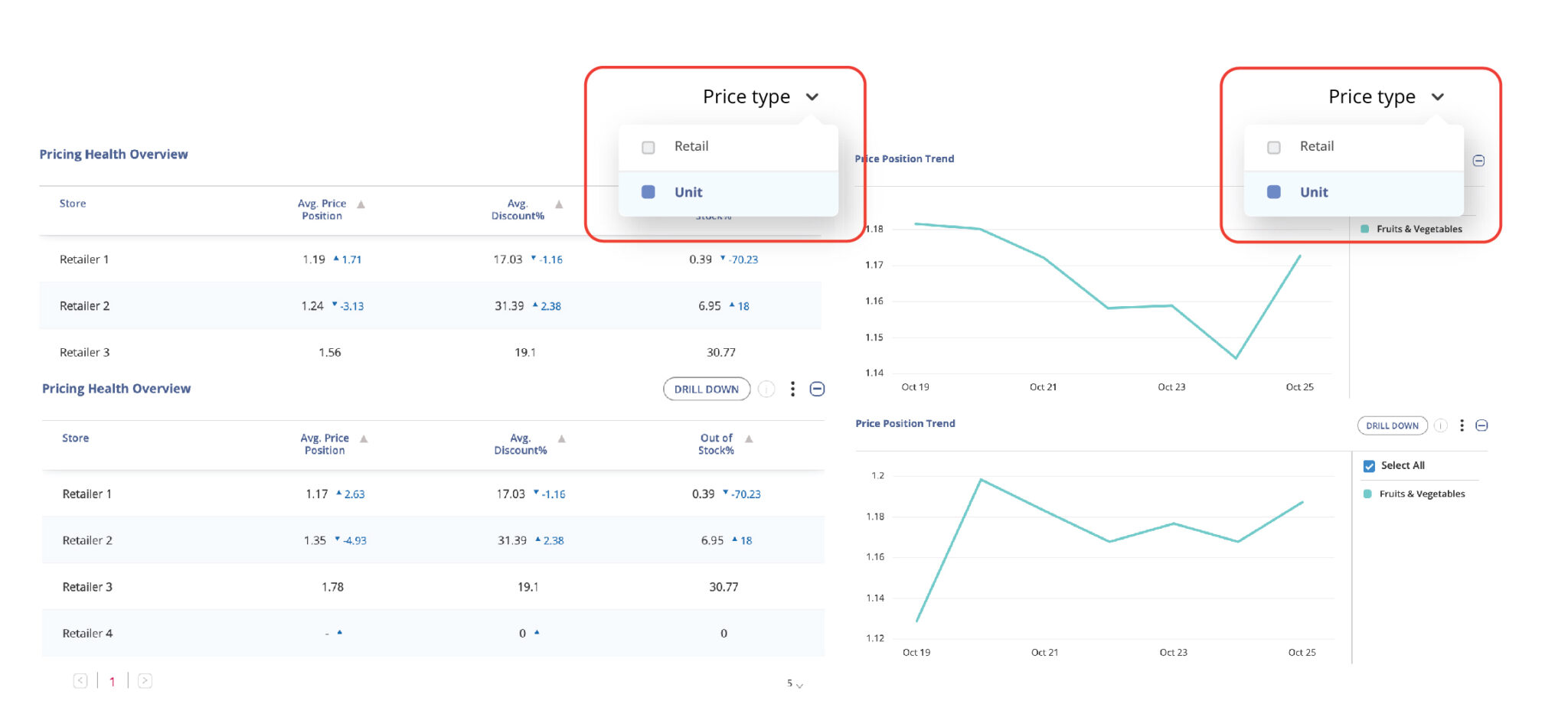

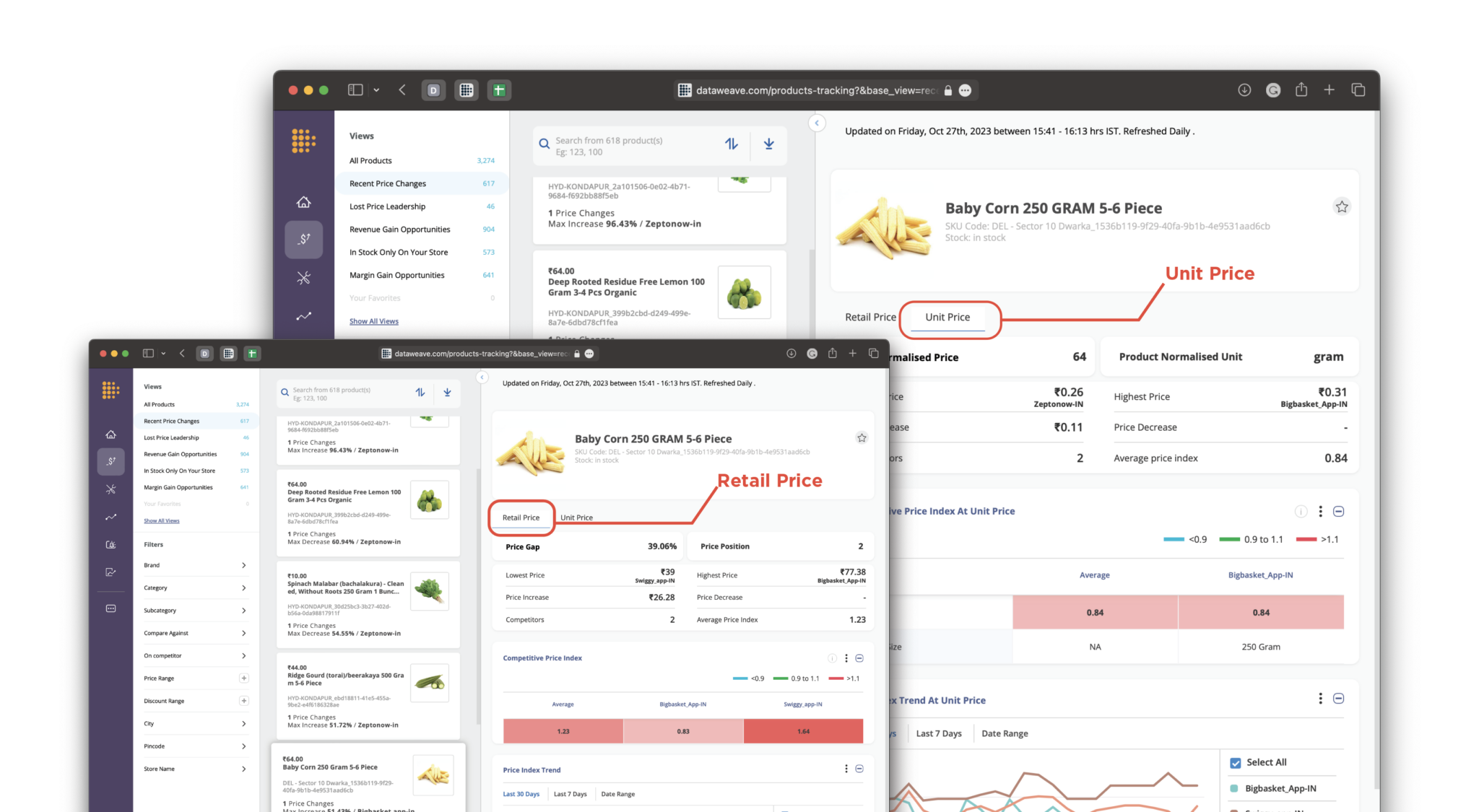

4. Unit of Measure Normalization

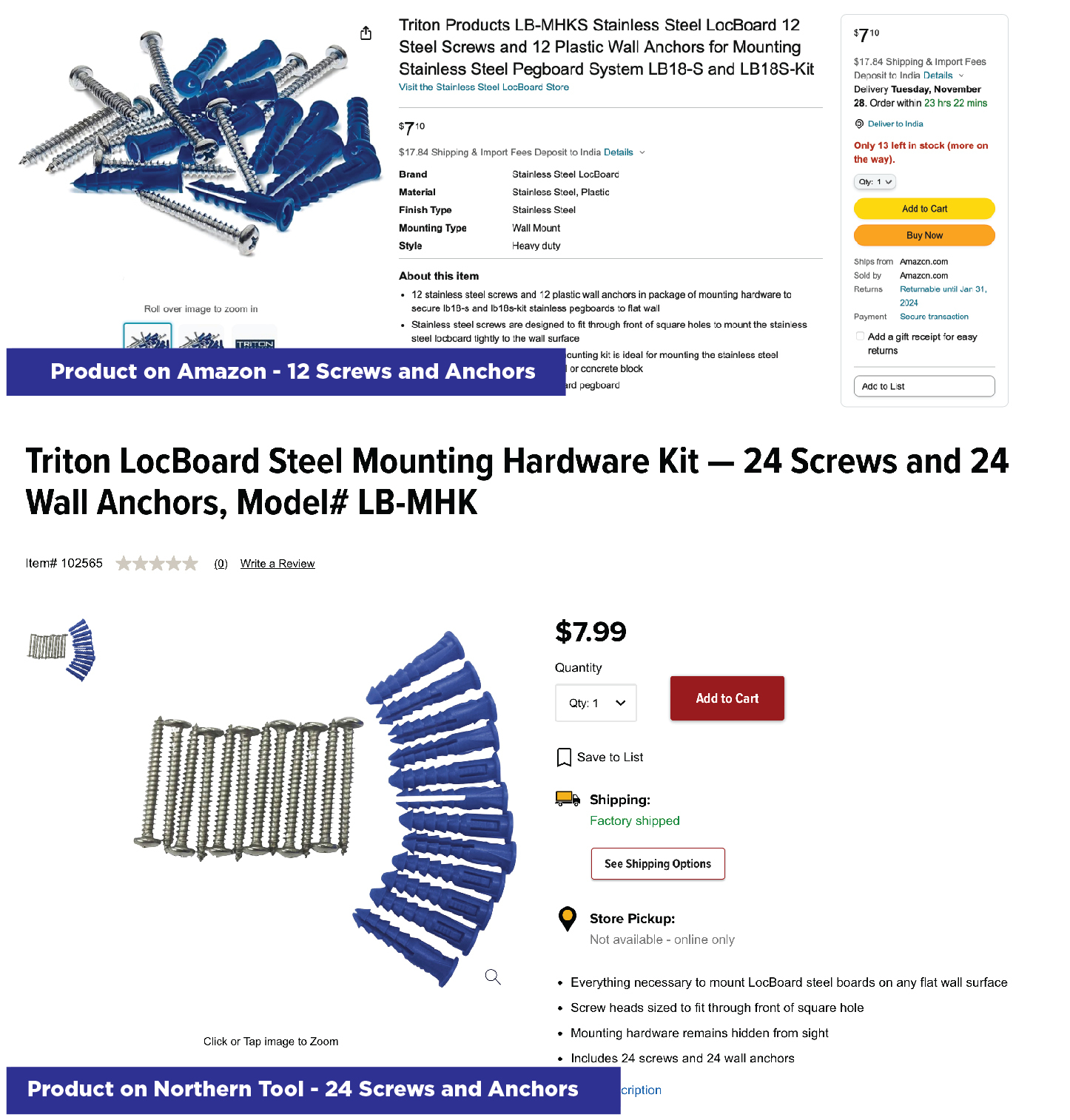

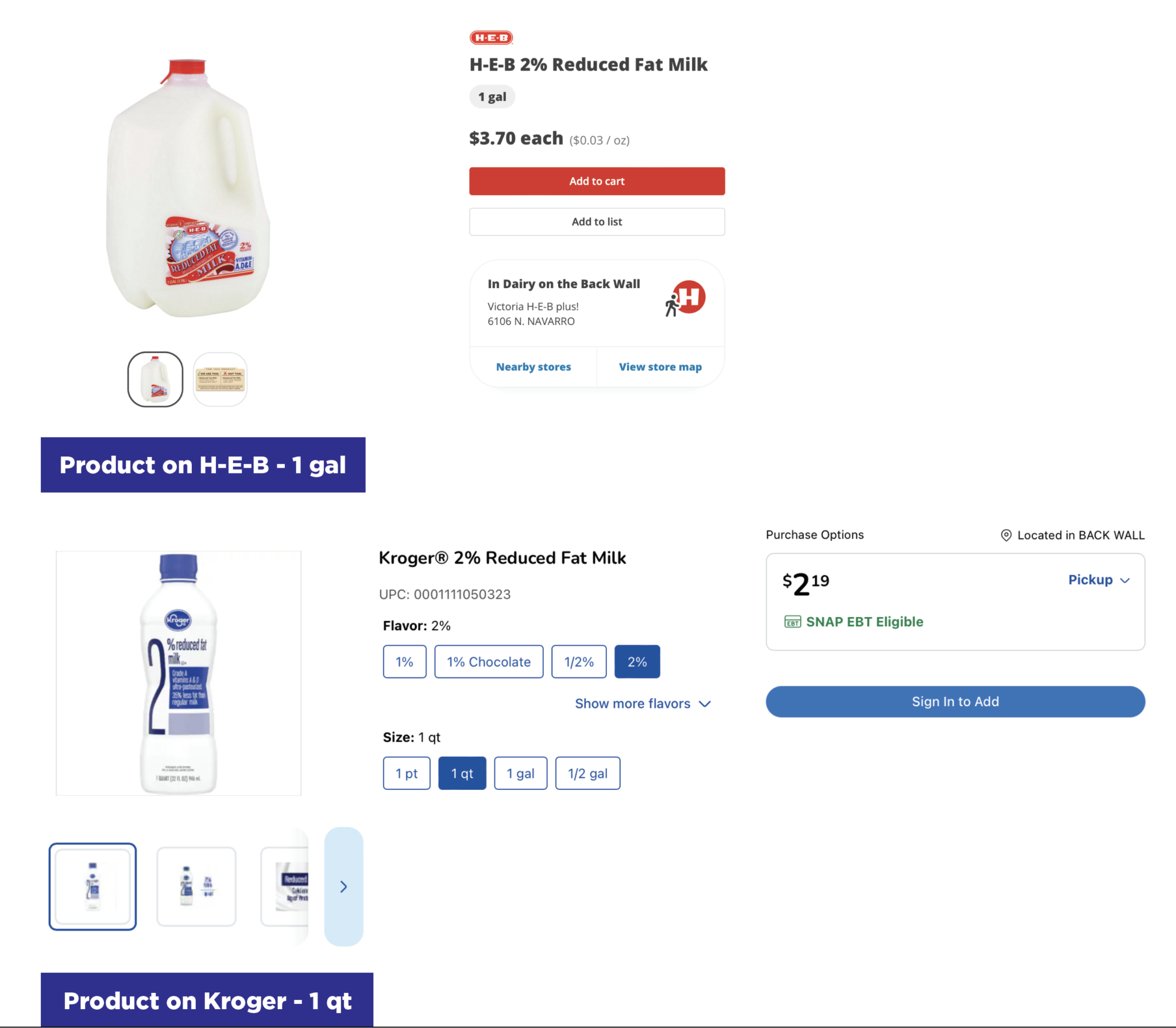

Effective product matching and grouping are crucial for maintaining competitive pricing, but this requires a tech stack that can normalize units of measure across various sites. For example, a 10.75oz can of chicken noodle soup priced at $3 may seem cheaper than a 12.90oz can priced at $3.20, but this isn’t always the case. Initially, the larger package might appear more expensive, but when prices are compared based on the same unit amount, it often offers better value. Therefore, it is essential for retailers to standardize units to accurately compare prices. Advanced technology goes beyond simply matching products; it ensures accurate comparisons by normalizing unit measurements, including weight, quantity, and volume—crucial factors for establishing a clear pricing picture across competitors.

Imagine comparing soup prices regardless of whether they are advertised in ounces, milliliters, or liters. By normalizing unit measurements, retailers can develop tailored pricing strategies on a level playing field, eliminating the risk of being misled by seemingly lower prices that conceal smaller quantities. Unit normalization allows retailers to uncover hidden value propositions by accurately determining the cost per unit, enabling them to set competitive prices, highlight the true value of their products, and make data-driven decisions.

5. Ease of Actionability

The most valuable insights are ineffective if they cannot be easily accessed and acted upon. Imagine a solution that not only provides industry insights but also customizes alerts and dashboards to show exactly how your prices compare to competitors in your specific categories and product groupings. An ideal solution would offer all this in one centralized platform, giving retailers easy access to data through intuitive dashboards, seamless data export options, and flexible API integrations. This enables a smooth, effortless process for adopting and utilizing the platform.

Ease of use and actionable insights should be at the core of such a solution. A SaaS-based web portal can provide businesses with access to insights through user-friendly dashboards, detailed reports, and impactful visualizations. Customized insights tailored for each persona within the organization facilitate swift actions on relevant competitive intelligence. Whether it’s day-to-day tactical recommendations or inputs for long-term strategies, the platform should ensure that all insights are easily consumable and actionable.

Moreover, the data should be accessible using plug-and-play APIs, enabling businesses to integrate external data with their internal pricing or ERP systems and BI tools. This integration generates predictive intelligence, enhances decision-making, and drives more robust business outcomes.

Choosing the Right Pricing Intelligence Solution Will Determine Your Success

Retailers need to leave behind generic pricing intelligence tools. For true success, retailers need a solution built to tackle their specific challenges. With capabilities like comprehensive data collection capturing granular details across regions and languages, local insights into store-level data for informed decision-making, accurate price comparisons with unit normalization, and access to actionable insights, retailers gain a complete and holistic picture of the pricing landscape, setting them up for success. Additionally, AI-powered and human-aided product matching ensures accurate competitor analysis

These are just some of the essential capabilities DataWeave offers to retailers. By prioritizing these, retailers can transform their pricing strategy into a profit-generating machine, keeping them ahead of the curve and exceeding customer expectations in a competitive market to help them stay at the forefront of their categories.

Cinco de Mayo is a vibrant celebration of Mexican-American and Hispanic heritage, marked by lively parades, festive tacos, and refreshing tequila across North America. For the service industry, brands, and retailers, this day offers a golden opportunity to roll out enticing promotions on beloved Mexican foods and beverages, drawing in large crowds and boosting sales.

Americans love to indulge in Mexican cuisine during Cinco de Mayo. Take avocados, for example: despite inflation, avocado sales soared to 52.3 million units this year, marking a 25% increase from last year, according to the Hass Avocado Board’s 2023 Holiday Report. Such festive events see a significant sales spike, largely driven by appealing discounts and special offers.

So, what discounts did retailers roll out this Cinco de Mayo?

At DataWeave, our cutting-edge data aggregation and analysis platform tracked and analyzed the prices and deals on Mexican food and alcohol products offered by leading retailers. Our in-depth analysis sheds light on their pricing competitiveness during Cinco de Mayo, revealing how pricing strategies differed across various subcategories and brands.

We conducted a similar analysis in 2022, allowing us to compare the prices of identical products this year versus last year. This comparison helps us understand the impact of inflation over the past two years on the prices offered today.

Our Methodology

For our analysis, we monitored the average discounts offered by major US retailers on over 2,000 food and beverage products during Cinco de Mayo, as well as in the days leading up to the event. Many retailers kick off their Cinco de Mayo promotions a week before, so we included the entire week leading up to May 5th in our analysis.

To truly demonstrate the value of Cinco de Mayo for shoppers, we concentrated on price reductions and additional discounts during the event. By comparing these with regular day discounts, we were able to highlight the genuine savings and benefits that Cinco de Mayo promotions offer to budget-conscious consumers.

Our Findings

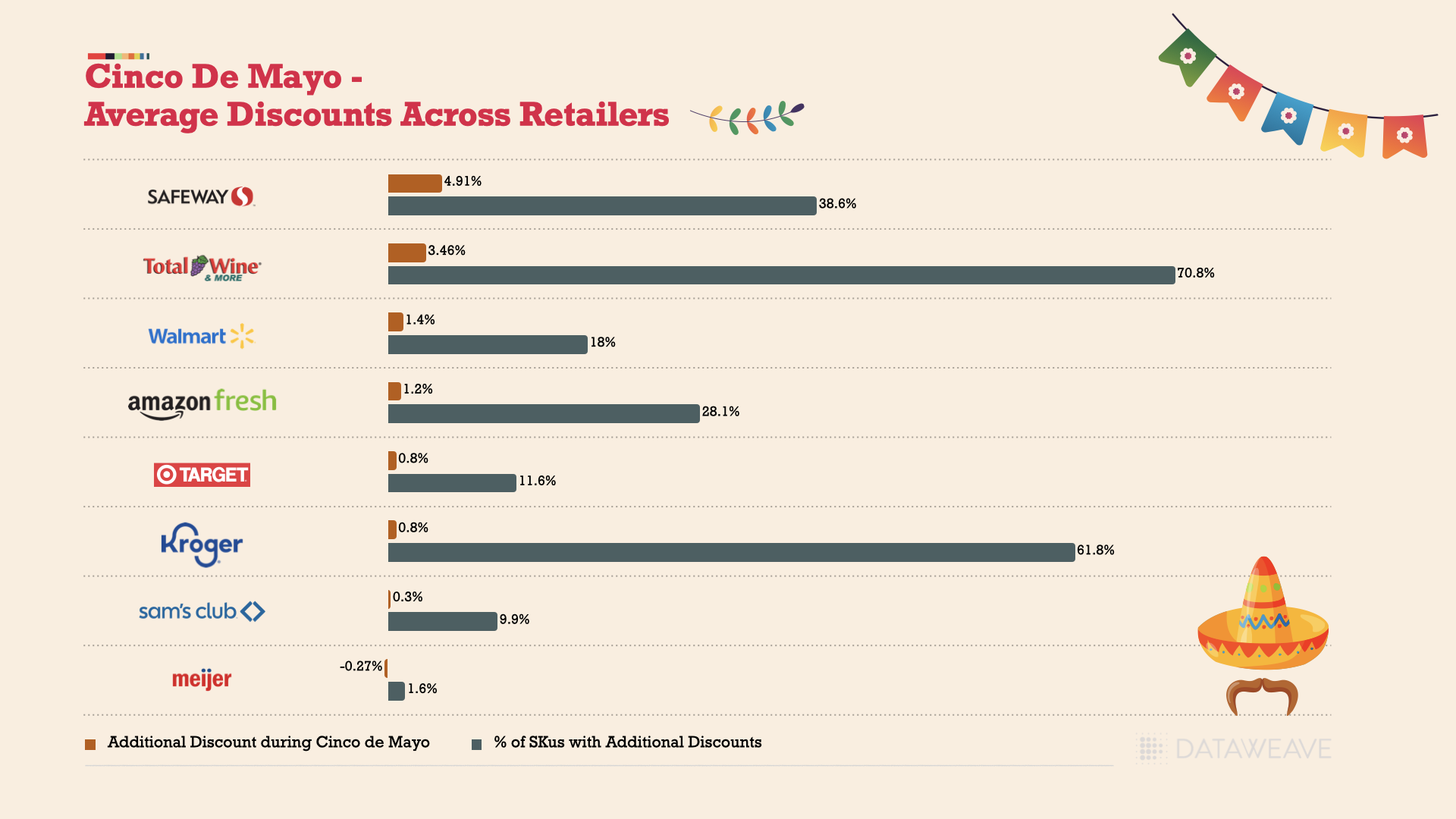

Safeway led the pack with the highest average additional discount of 4.91%, covering 38.6% of their food inventory for Cinco de Mayo. Total Wine & More followed closely, offering an average discount of 3.46% across 70.8% of its tequila, whiskey, mezcal, and other spirit products during the Cinco de Mayo week.

In contrast, Target provided minimal additional discounts, averaging just 0.8% over a small fraction (11.6%) of its SKUs. Similarly, Kroger’s additional discounts were also 0.8%, but they were spread across over 60% of its tracked products. Walmart (1.4%) and Amazon Fresh (1.2%) offered relatively conservative discounts during the sale period.

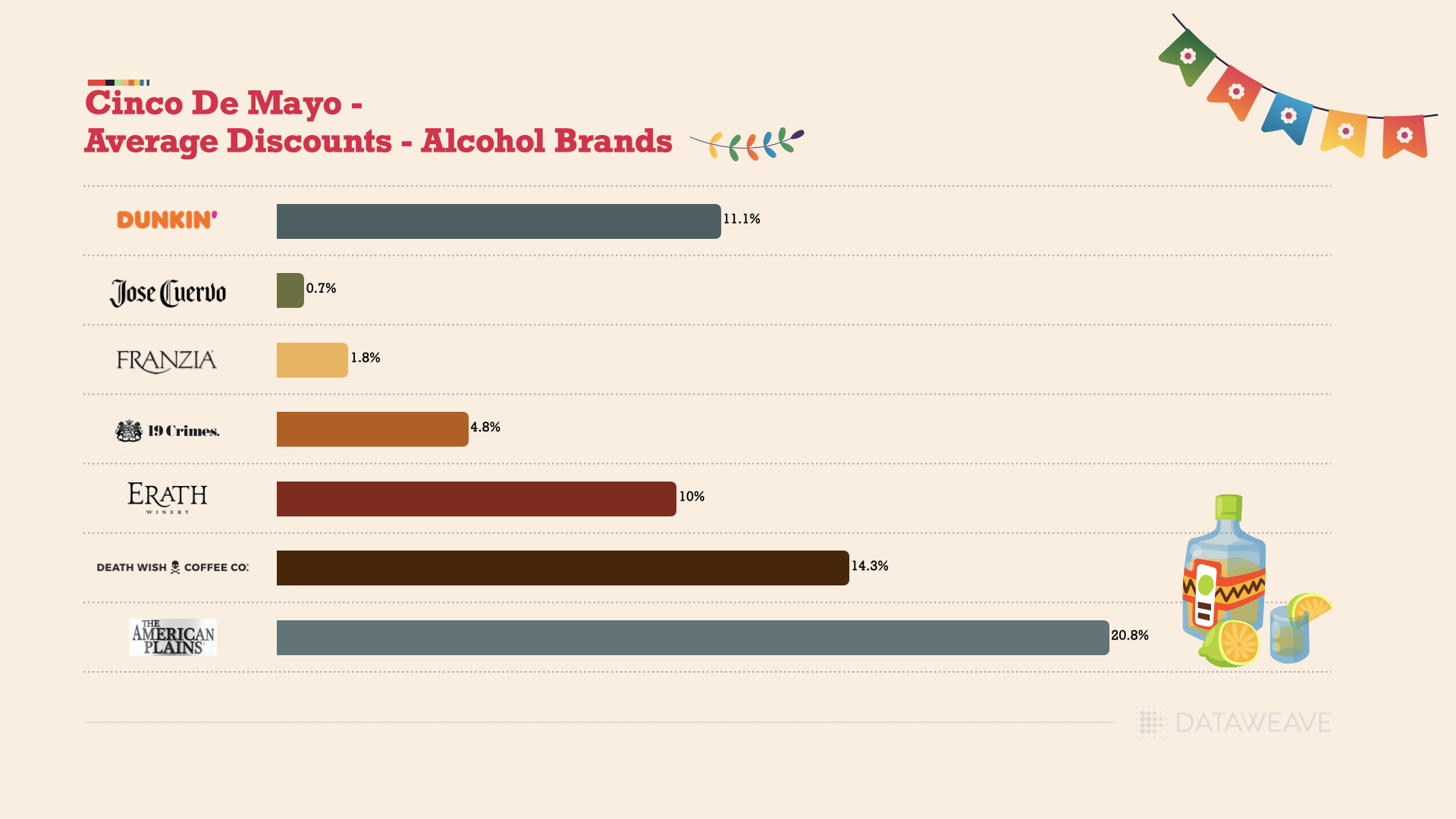

During Cinco de Mayo, various brands rolled out attractive discounts to entice shoppers. Among beverage brands, The American Plains vodka led the way with the highest average discount of 20.80%. Coffee brands also joined the festivities with significant discounts: Death Wish Coffee at 14.30%, Dunkin’ at 11.10%, and Starbucks at 5.70%. Notably, Dunkin’ and Death Wish Coffee introduced complimentary beverages such as whiskey barrel-aged coffee and spiked coffee products to celebrate the event.

In the wine category, Erath stood out with a 10% additional discount. However, brands like Jose Cuervo and Franzia offered more modest discounts of 0.70% and 1.80%, respectively.

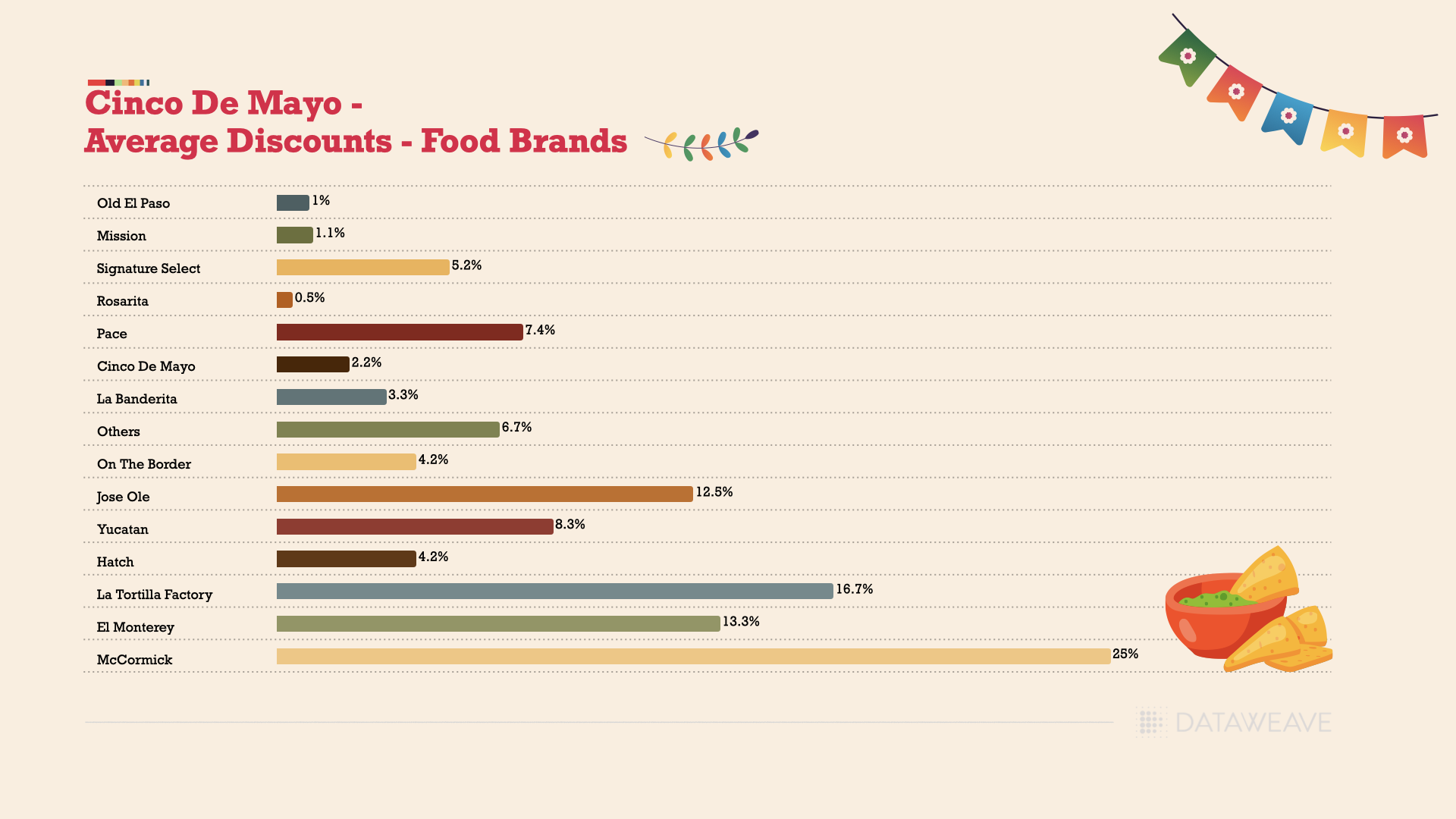

Food brands associated with traditional Mexican ingredients or products, such as tortillas, salsas, and spices, provided higher discounts compared to mainstream snack brands. For instance, McCormick (25%), El Monterey (13.3%), and La Tortilla Factory (16.7%)—known for ready-to-eat frozen foods, seasonings, and condiments—delivered the highest discounts. Other notable discounts included Jose Ole (12.5%), a frozen food brand, and Yucatan (8.3%), known for its guacamole.

Safeway’s private label brand, Signature Select, offered a 5.20% discount. Additionally, Safeway provided deep discounts on brands like Pace, Herdez, and Taco Bell, indicating an aggressive discounting strategy. In contrast, brands closely associated with Mexican or Tex-Mex cuisine, such as Old El Paso, Mission, Rosarita, and La Banderita, offered relatively modest discounts ranging from 0.5% to 3.3%.

The discount patterns varied between alcohol and food categories, with food brands generally offering higher discounts. This trend may be attributed to pricing being regulated in the alcohol industry. These differing discount levels highlight how brands navigated the balance between driving sales and maintaining profit margins during Cinco de Mayo, particularly in the context of inflation affecting costs.

Impact of Inflation on Cinco de Mayo Prices (2024 vs 2022)

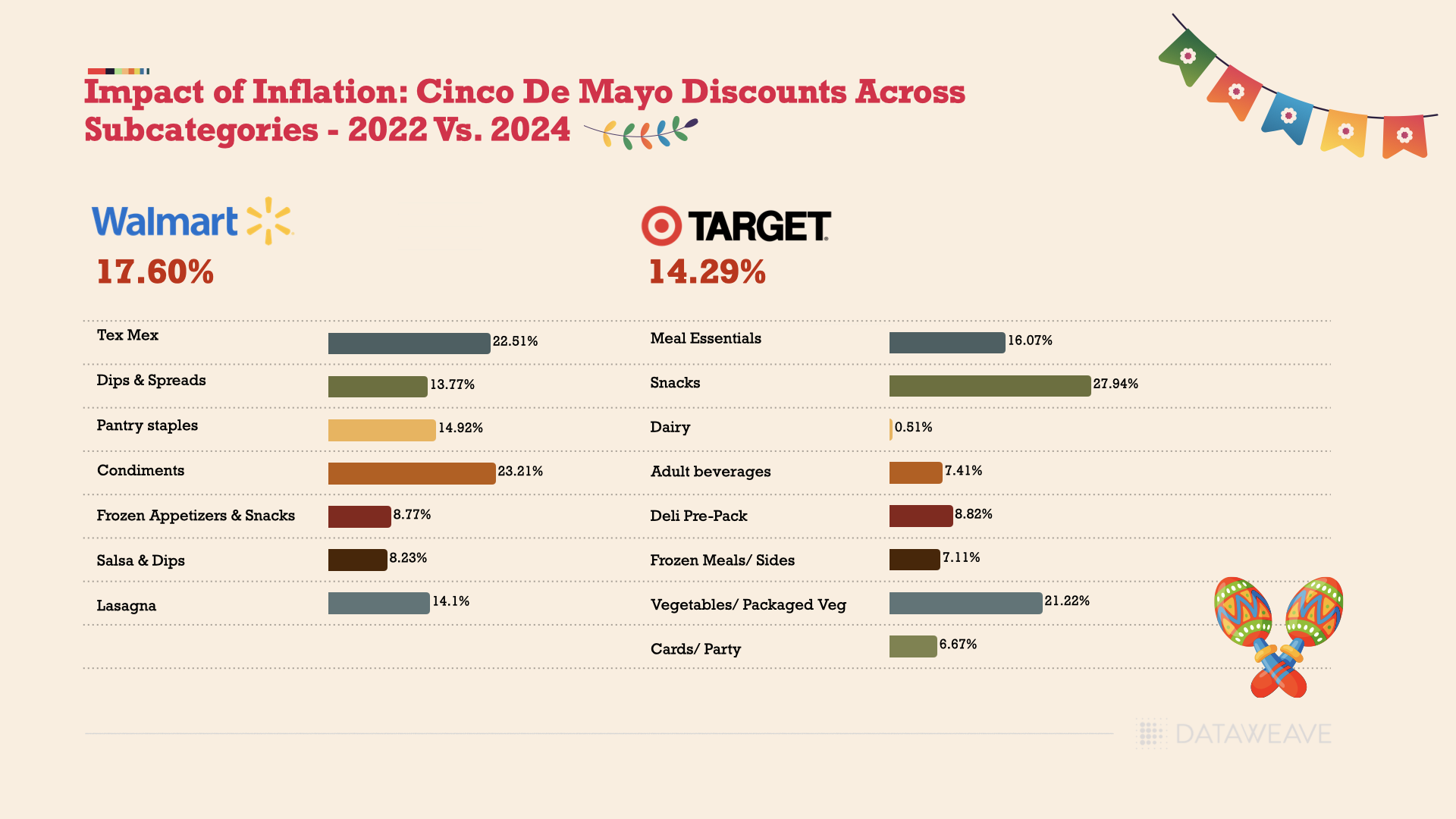

To gauge the impact of inflation on popular Cinco de Mayo products, we analyzed the average prices at Walmart and Target between 2022 and 2024. These two retailers were chosen due to their prominence in the retail sector and the robustness of our sample data.

At Walmart, the Tex Mex category saw the highest average price increase, rising by 22.51%. Other notable subcategories with significant price hikes include Condiments (23.21%), Vegetables/Packaged Vegetables (21.22%), and Lasagne (14.10%). Categories like Dips & Spreads (13.77%), Pantry Staples (14.92%), and Salsa & Dips (8.23%) experienced relatively lower increases.

At Target, the Snacks subcategory had the steepest average price rise at 27.94%, followed by Meal Essentials (16.07%) and Deli Pre-Pack (8.82%). Categories such as Dairy (0.51%), Frozen Meals/Sides (7.11%), and Adult Beverages (7.41%) saw smaller price increases.

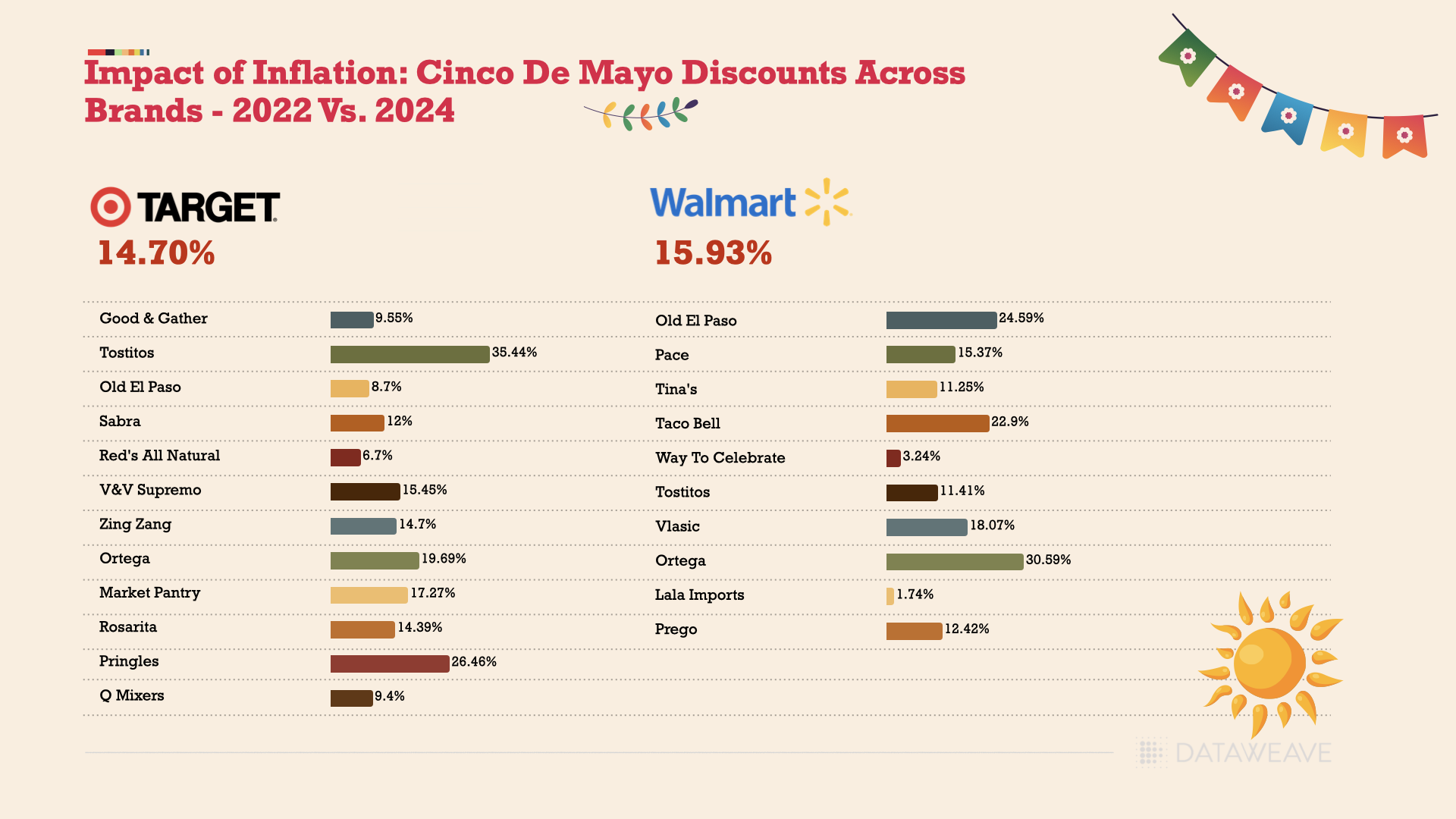

Brands associated with traditional Mexican or Tex-Mex cuisine faced higher price hikes. Examples include Old El Paso (24.59% at Walmart, 8.70% at Target), Tostitos (35.44% at Walmart, 11.41% at Target), Ortega (30.59% at Walmart, 19.69% at Target), and Rosarita (14.39% at Walmart).

In contrast, private label or store brands generally experienced lower price increases compared to national brands. For instance, Good & Gather (Target’s private label) saw a 9.55% increase, while Market Pantry (Walmart’s private label) had a 17.27% rise. This trend is understandable as retailers have more control over their costs with private label brands.

The data clearly indicates that both Walmart and Target have significantly raised prices across various categories and brands, reflecting the broader inflationary environment where the cost of goods and services has been steadily climbing.

Interestingly, we observed higher price increases at Walmart compared to Target. Although Walmart is renowned for its consumer-friendly pricing strategies, it too had to elevate grocery prices post-2022 to combat inflationary pressures. As consumers become more cost-conscious and reduce spending on discretionary items, Walmart and other retailers are now cutting prices across categories to align with shifting consumer behaviors.

Mastering Pricing Strategies During Sale Events

Our pricing analysis for Cinco de Mayo reveals compelling insights into the dynamics of retailer landscapes in the US. It highlights the enduring relevance of private label brands, even amidst fluctuating demand, showing the emergence of local, national, and small players vying for market share.

As retailers navigate inflationary pressures and evolving consumer behaviors, understanding these pricing dynamics becomes crucial for optimizing strategies and bolstering market competitiveness. This analysis offers actionable intelligence for retailers seeking to navigate the intricate terrain of sale event promotions while addressing shifting consumer preferences and economic challenges.

Access to reliable and timely pricing data equips retailers and brands with the tools needed to make informed decisions and drive profitable growth in an increasingly competitive environment. To learn more and gain guidance, reach out to us to speak to a DataWeave expert today!

Easter egg hunts just got more challenging for families this year as the price of chocolate and other candies has soared. The root of this price surge lies in a cocoa deficit, attributed to diseases affecting crops and the adverse effects of climate change on West African farms, which supplies over 70% of the world’s cocoa. This has resulted in a tripling of cocoa prices over the last year, causing a “cocoa crunch,” and severely impacted confectioners and chocolate makers.

Reuters recently reported that Iconic brands such as Hershey’s and Cadbury find themselves grappling with the need to adjust to escalating costs for raw materials. Given that Easter is one of the top three candy-purchasing occasions, these manufacturers are contemplating raising their prices to sustain their profit margins.

Despite the challenges posed by the cocoa shortfall and persistent inflation, the National Confectioners Association anticipates that Easter candy sales in the U.S. will match or even exceed last year’s figures, which amounted to approximately $5.4 billion. This expectation is predicated more on price increases than on a rise in sales volume.

At DataWeave, our ongoing analysis of pricing trends across various consumer categories among retailers has provided insight into the evolving landscape of chocolate and candy prices in 2023 and 2024.

Our Analysis of Inflation in Candy and Chocolate Prices

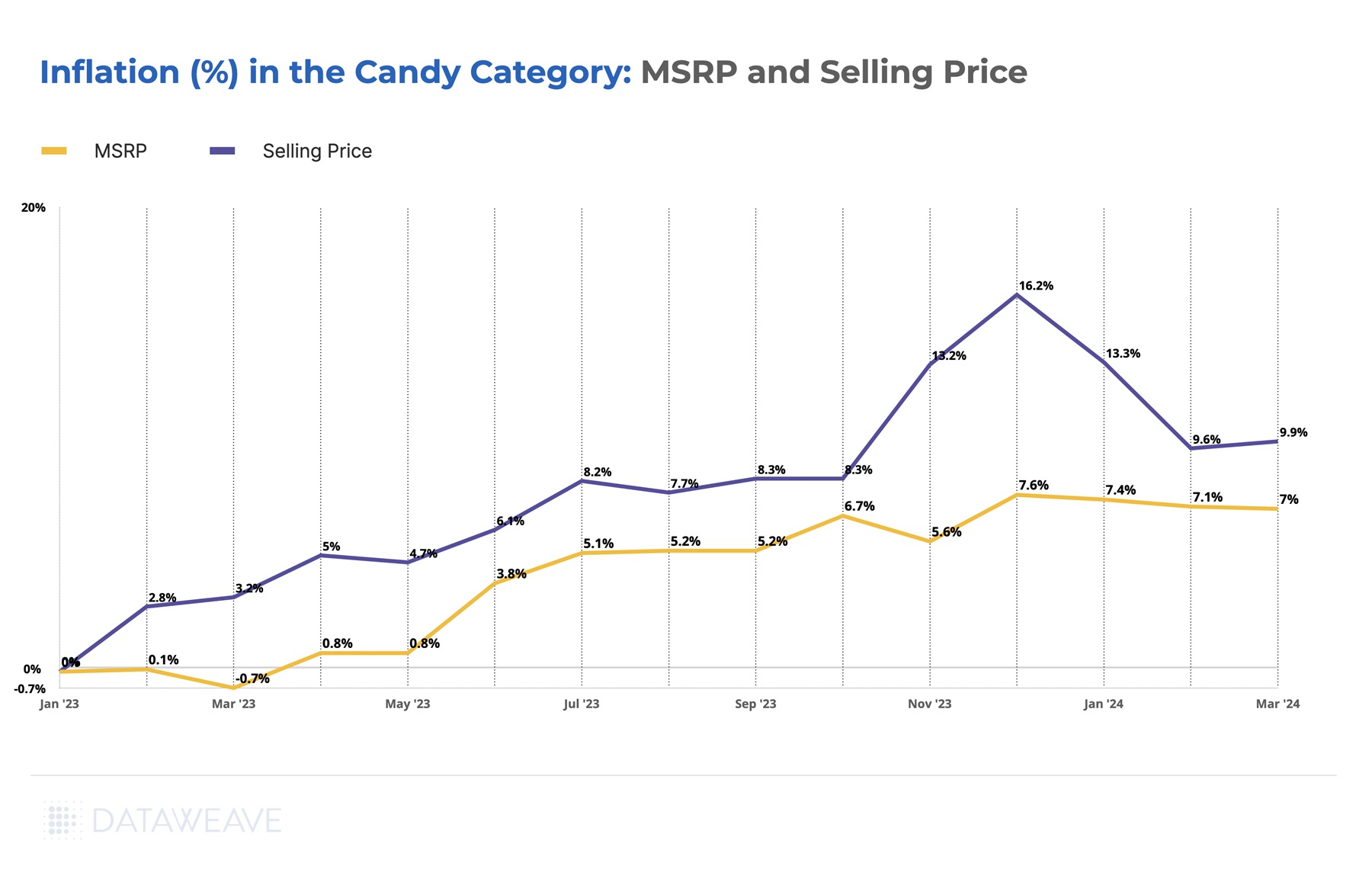

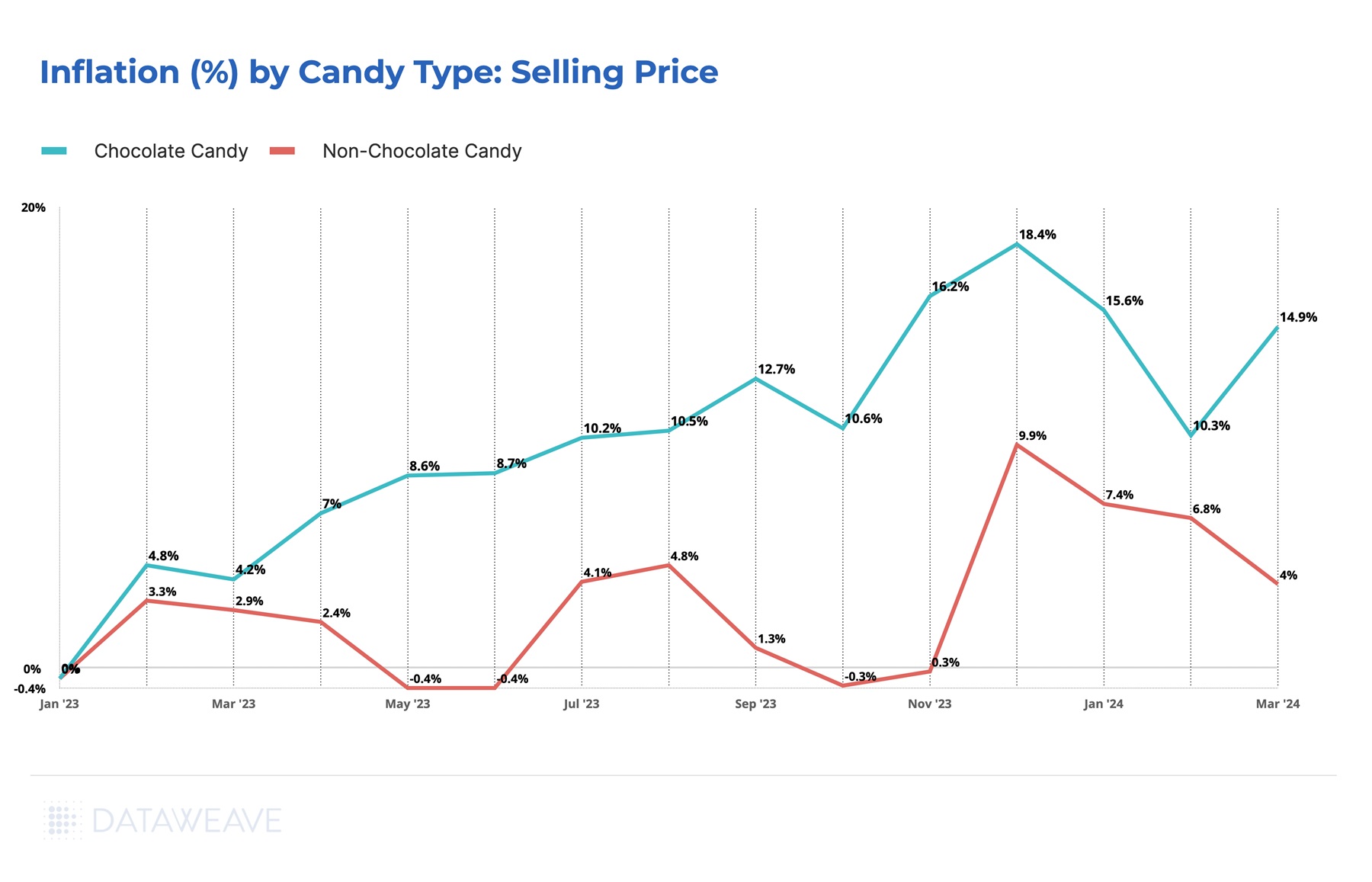

Our study encompassed a broad array of 3,300 products from leading U.S. retailers, Amazon, Target, Kroger, and Giant Eagle. As illustrated in the following chart, the trajectory of prices over the past 15 months was compared against the average prices in January 2023. Our tracking focused on two key price points: the selling price, which represents the final cost to consumers after applying any discounts or promotions, and the Manufacturer’s Suggested Retail Price (MSRP), as determined by the brands themselves.

The findings from our analysis indicate that the average selling price, primarily influenced by retailer decisions, has experienced a steady increase throughout 2023, reaching a peak at 16.2% above January 2023’s figures by December. As of March 2024, coinciding with the Easter season, the selling prices are approximately 10% higher than they were at the beginning of the previous year.

Simultaneously, the MSRP has seen a consistent uptick, driven by the climbing costs of cocoa. Brands have adjusted their suggested prices accordingly, with the current MSRP standing about 7% above its January 2023 level, after having peaked at a 7.6% increase by December 2023. This reflects the direct impact of rising cocoa costs on product pricing strategies.

Chocolate Candies Are Hit The Hardest

Across all candies, chocolate-based products have witnessed significantly sharper price increases than their non-chocolate counterparts. In the past 14 months, the selling prices of chocolate items have surged by 14.9%, a stark contrast to the modest 4% rise observed in non-chocolate candies.

This price escalation was particularly pronounced during the Christmas shopping period, a response to heightened demand, before experiencing a temporary decline in February.

The diminishing availability of cocoa, coupled with rising costs for packaging and transportation, has compelled brands and retailers alike to transfer these added expenses onto the consumer. This dynamic underpins the distinct pricing trends observed across the candy spectrum, with chocolate items bearing the brunt of these cost pressures.

Discounts Offered By Retailers and Brands to Entice Easter Shoppers

In our analysis, we delved deeper to identify the retailers and brands offering the most compelling prices for Easter-centric confections, including Chocolate Eggs, Chocolate Bunnies, and Easter-themed gift packs.

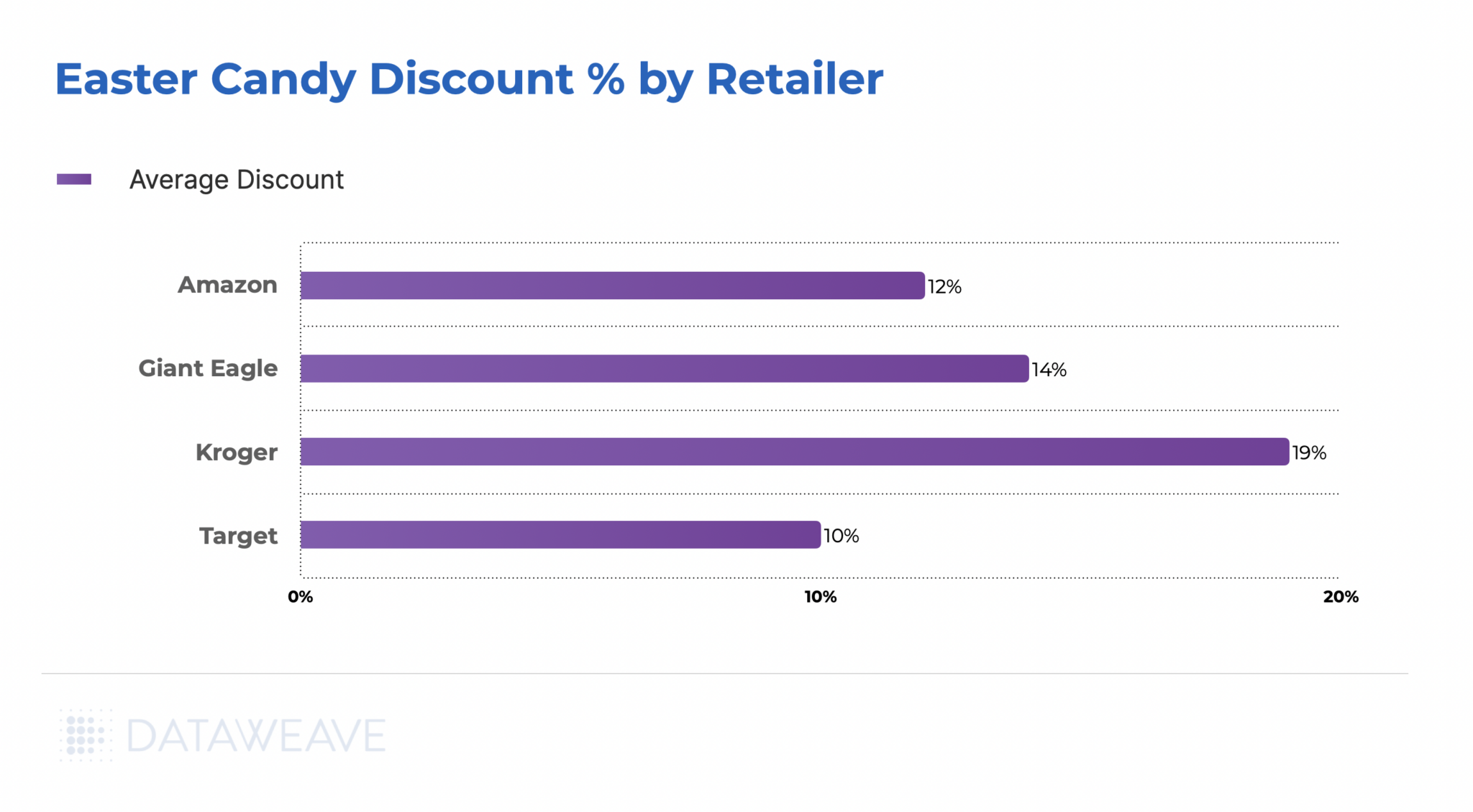

Kroger emerged as the frontrunner among the retailers we monitored, offering an impressive 19% discount on Easter candies. Giant Eagle followed with a solid 14% average markdown. Meanwhile, Amazon and Target provided more modest promotional discounts at 12% and 10%, respectively.

Kroger is making significant efforts to ensure consumers have access to attractively priced Easter treats. The retailer planned to keep its doors open throughout the Easter weekend, featuring baskets brimming with discounted items such as Russell Stover chocolate bunnies, Brach’s jelly beans, Reese’s eggs, and assorted bags of popular candies from Snickers, Twix, and Starburst, among others. Additionally, Kroger is enhancing its value proposition through gift card offers and exclusive Easter deals for its loyalty program members.

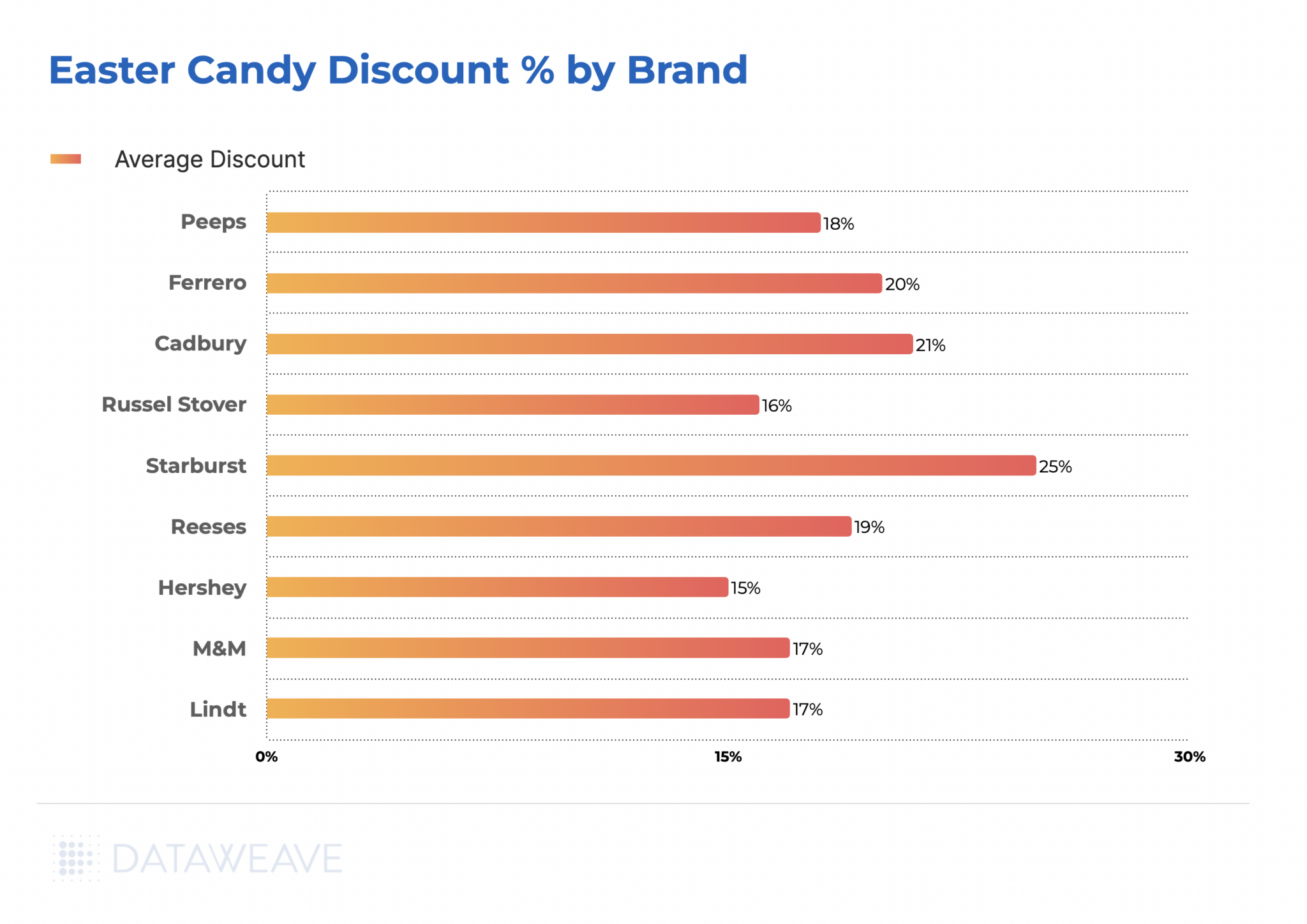

On the brand front, Starburst by Mars Wrigley leads with the steepest discount of 25%. Cadbury, under Mondelez, is not far behind, offering 21% off its mini eggs and other Easter treats, marking an increase from last year’s 17% discount. Ferrero Rocher is making a strong pricing move with an average 20% markdown on its Easter selections, including the chocolate bunny and squirrel figures.

The beloved Peeps marshmallow candies by Just Born are being offered at an 18% discount this year, slightly less than the 23% discount seen in 2023, likely reflecting the impact of rising sugar costs, given their sugar and corn composition.

Other notable brands, including M&M’s and the premium Swiss chocolatier Lindt, have elevated their average Easter discounts to 17% this year, up from the previous year’s discounts of 12%, and 10% respectively, showcasing a competitive pricing strategy to delight consumers this Easter season.