Brands that build consumer trust will win big as online shopping explodes this year. As the COVID-19 pandemic propels more shoppers online, an astounding $5 trillion (30%) of annual global retail sales is up for grabs as the market shifts to e-commerce, according to Boston Consulting Group.[1]

Notably, e-commerce has changed brands’ retail processes. Unlike brick-and-mortar stores, the digital shelf is where brands manage their company and products among online shoppers, influencing what they browse and buy.

Rather than stocking merchandise through retailers’ physical stores, brands can now manage their online products by working with logistics experts like Fulfillment by Amazon. Instead of merchandising in stores with planograms and endcap displays, brands promote their digital assortment with targeted product content that resonates and keeps them coming back.[2] The evolution of retail can help brands save time and effort, and increase their agility and effectiveness.

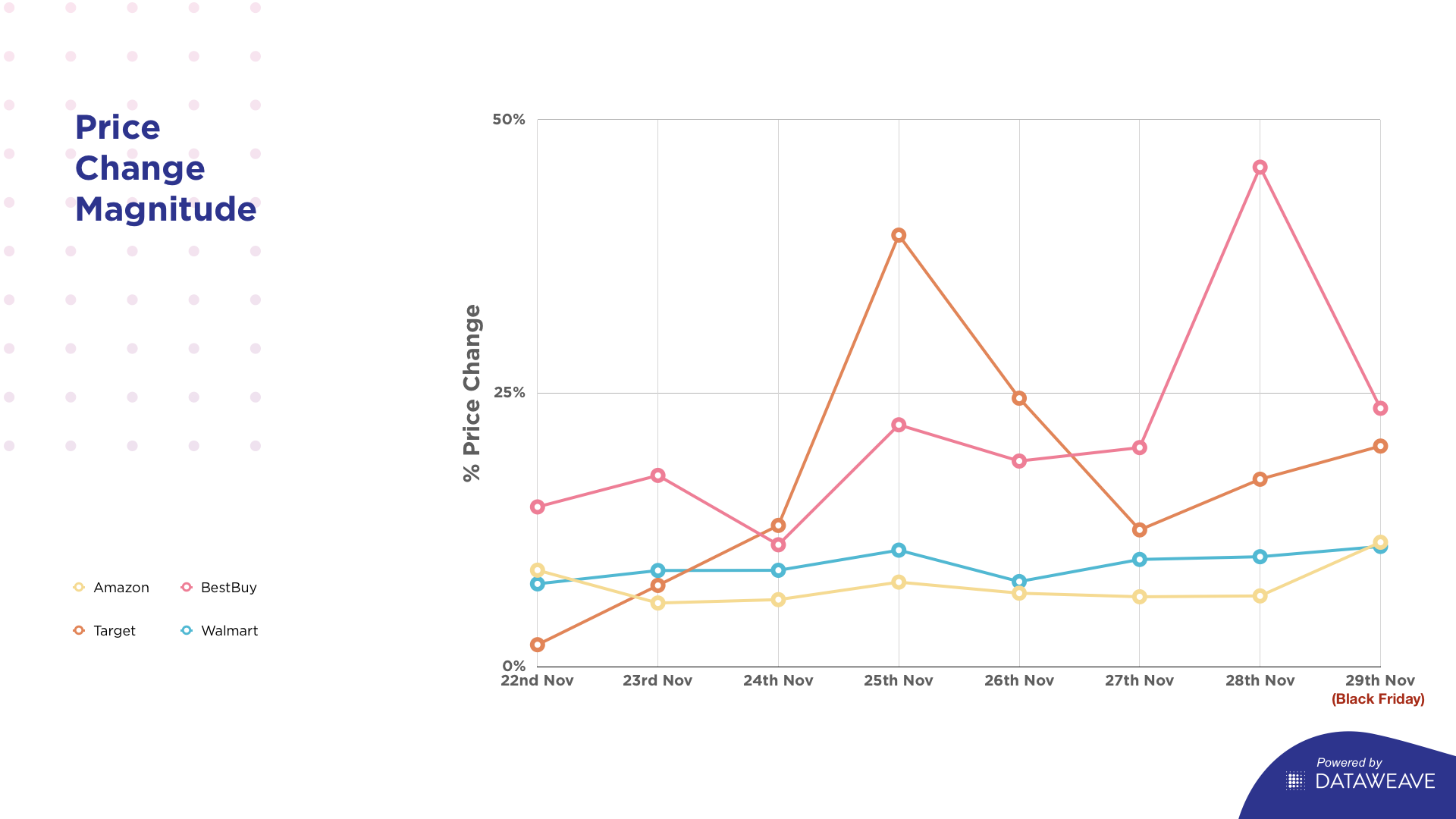

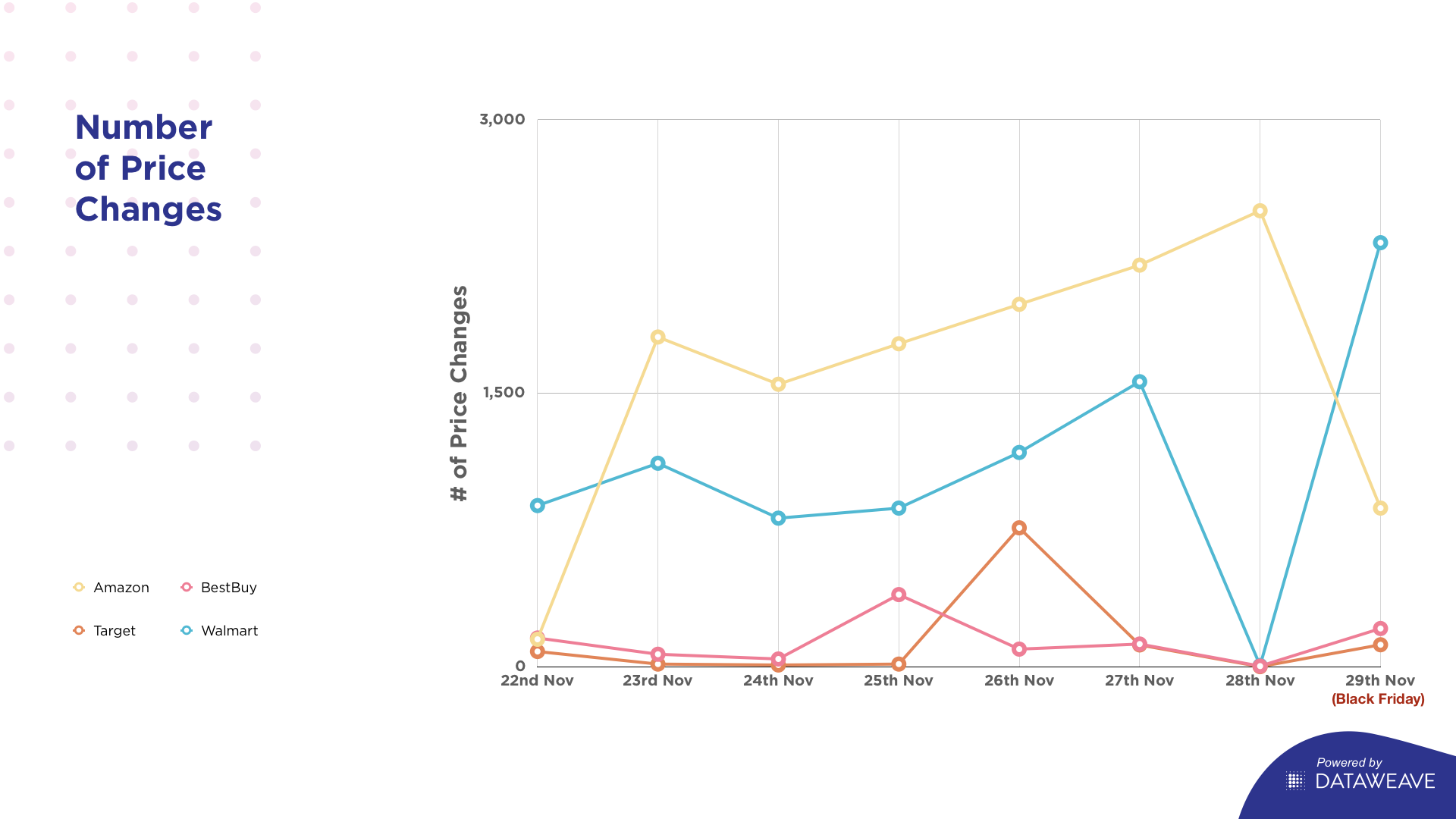

Gaining high visibility on the digital shelf can help brands boost their reach, brand awareness and sales. That’s why more brands are now investing in proven e-commerce best practices to increase consumer confidence by offering reliable products, relevant marketing and a smooth online experience. Now that the 2020 holiday sales season is underway, it’s the perfect time to see how leading brands compete in the increasingly crowded online market by demonstrating credibility and consistency.

Market fragmentation increases brand complexity

Selling across multiple online touchpoints means brands have more e-commerce websites and digital shelves to monitor to ensure compliance with brand guidelines to ensuring a consistent customer experience. To engage online shoppers, brands’ marketing strategies must now diligently manage their digital shelf across diverse online shopping arenas, including:

- Direct-to-consumer (DTC) sites: More brand manufacturers are shortening the supply chain by bypassing retailers and selling directly to consumers, including sales through their own e-commerce websites.eMarketer predicts that U.S. DTC e-commerce sales will grow by 24% to reach nearly $18 billion in 2020.[3]

- Retailers’ e-commerce sites: Brands are also migrating online because the retailers who sell their merchandise moved online this yearto adapt to the pandemic and survive shuttered storefronts. As of April 21, e-commerce grew 129% year-over-yearin U.S. and Canadian orders and U.S. e-commerce sales are on track to hit nearly $710 billion this year.[4] More than ever, sharing timely, accurate product information with retail partners is essential for success.

- Online marketplaces: A growing number of brands are investing in digital advertising and content to stand out on popular, high-traffic online marketplaces. Global e-commerce leaders Amazon, eBay and China’s Alibaba and JD, are mostly search-based sites, as users know what they want and search for it, which makes product description pages and ads important marketing tools. Conversely, China’s Pinduoduo platform involves group-buying and interactive games to boost brand awareness and sales by entertaining online consumers and inspiring flattering word-of-mouth.[5] Among online marketplaces, digital content fuels brand discovery and sales.

- Last-mile delivery channels: Brands can also sell in collaboration with their last-mile partners. Last-mile experts like Peapod, Instacart, Uber and Shipt offer online advertising opportunities for brands to reach new audiences. For instance, Instacart launched a self-serve advertising platform that lets brands promote their products in search results. Brands can choose the products to promote, set a budget and pay when users engage with those products.[6]

- Social media: To reach and influence consumers where they already spend their time, more brands are investing in social media promotions and even embracing social commerce innovation. Social media matters to brands’ marketing effectiveness, as 52% of online brand discovery happens on social feeds.[7] Also, 92% of Instagram users say they’ve followed a brand, visited their website or made a purchase after seeing a product on Instagram.[8]

Brand promotions have evolved beyond Google AdWords and Facebook campaigns. Now promotions include digital content and ads across all of these digital touchpoints, which increases the scope of brand marketing efforts to reach online consumers.

How brands transform digital shelf complexity into clarity

To earn online shoppers’ trust across e-commerce arenas, more leading companies are turning to a common solution: data.

Too often, online shoppers abandon their cart due to concerns that they will unwittingly buy inauthentic products from fraudulent sellers. To protect their brands, manufacturers use data insights to pinpoint and prevent unauthorized sellers, counterfeit products and minimum advertised price (MAP) violations to demonstrate authenticity, accountability and price parity.

“Digital is the new normal”

~ Nike CEO John Donahoe[9]

To invigorate underperforming online promotions, brands rely on analytics to connect the dots among their online promotions, marketing performance and share of voice. Insights on advertising, keywords and consumer reviews help brands make better marketing decisions faster. These insights help brands stand out from competitors and build relationships with shoppers by ensuring their promotions resonate and drive more sales online.

To overcome low online traffic and sales, more brands apply data insights to improve their digital presence, visibility and sell-through rates. Brand analytics measure their popularity on e-commerce websites and track their stock status to improve accessibility, optimize digital shelf velocity and deliver a reliable customer experience that builds trust.

Watch over your brand: To stay competitive and earn consumer trust, more brands now rely on data insights to make fast, effective decisions that enhance their reputation and boost online sales.

As e-commerce explodes, more leading brands are collaborating with DataWeave for actionable brand analytics to protect their digital shelves, decrease complexity and boost consumer trust. These accurate, trusted insights help brands gain clarity to make smarter e-commerce decisions faster. Making data-driven brand management, promotional and digital marketing decisions helps brands prove their authenticity, improve marketing effectiveness and boost online sales. To see how DataWeave helps brands stand out, sell more and stay competitive, visit www.dataweave.com.

[1] Taylor, Lauren, Chris Biggs, Ben Eppler, Henry Fovargue and Gaby Barrios. How Retailers Can Capture $5 Trillion of Shifting Demand. Boston Consulting Group. August 31, 2020.

[2] Gibbons, David. Ecommerce and content: How retailers have shifted strategies during the COVID-19 pandemic. Digital Commerce 360. August 18, 2020.

[3] US Direct-to-Consumer Ecommerce Sales Will Rise to Nearly $18 Billion in 2020. eMarketer. April 1, 2020.

[4] Wertz, Jia. 3 Emerging E-Commerce Growth Trends To Leverage In 2020. Forbes. August 1, 2020.

[5] Lee, Emma. The incredible rise of Pinduoduo, China’s newest force in e-commerce. TechCrunch. July 26, 2018.

[6] Goyal, Vivek. Browsing e-commerce: An untapped $250B+ opportunity. Medium. September 27, 2020.

[7] Cooper, Paige. 43 Social Media Advertising Statistics that Matter to Marketers in 2020. Hootsuite. April 23, 2020.

[8] Cooper, Paige. 43 Social Media Advertising Statistics that Matter to Marketers in 2020. Hootsuite. April 23, 2020.

[9] Grill-Goodman, Jamie. ‘Digital is the New Normal,’ Nike CEO Says. RIS News. September 23, 2020.

![[INFOGRAPHIC] 2019 at DataWeave: Blazing New Trails](https://stage-cdnblog.dataweave.com/wp-content/uploads/2020/01/2020-.jpg)