After demonetization, Covid-19 has probably been one of the worst scenarios for the retail sector in India. The entire nation went into lockdown and the industry noticed some big changes around the entire globe. From remote working to shopping, everything turned to digital and Bharat witnessed new trends across payments, e-commerce, and more.

Not surprisingly, D2C has been a favorite amongst businesses thanks to its agility. More than 800 brands have joined the direct-to-consumer bandwagon in order to reach their audience quickly and in an efficient way. Where brands such as MamaEarth, Clovia, Bewakoof, Lenskart have been some of the popular brands in the sector, last year even traditional giants such as LG, Ajanta-Orpat, Piaggio, Havells also adopted the D2C model.

Brands are more focused on making the user experience better and it will be safe to say that this year, D2C will be the highlight of the e-tail ecosystem. Naturally, e-commerce giants such as Amazon, Flipkart have played an important role in this revolution. Amazon, which has over 100 Million registered users in India, announced that it will host its flagship event, Prime Day this year on 26-27 July.

Let’s look at some of the things brands can do to leave their mark this Prime Day in India.

Given that the pandemic has accelerated online shopping nationwide, Digital Shelf Optimisation (DSO) should be the key lever for any brand to accelerate its digital commerce growth. Events such as Prime day are significant for a brand’s reputation, customer experience, overall sales and can help you build a loyal customer base.

With that in mind, we have prepared a list of things to consider, in order to help brands stand out from the crowd.

Pricing and Discounting: Offer discounts and deals to attract customers.

It is obvious that Prime Day will see a tremendous influx of shoppers. Noticeably, impulsive shopping is a trend during these sales, as everybody loves a good product for a discounted price. Make sure to offer discounts and deals to attract customers.

Another suggestion is to keep a track of competition, their pricing and promotional strategies and keep an eye on price changes happening across relevant categories or SKU’s (Stock Keeping Unit). Competition analysis is a powerful tool and having accurate data on their sales, market share is a critical part of this.

Product Visibility: Lakhs of sellers & brands are vying for the same spot

Marketplaces are crowded, and getting discovered is already hard. Lakhs of sellers & brands are vying for the same spot. And with more people moving online, it’s going to get increasingly harder for brands to stand out. Optimize your search visibility using the right keywords relevant to your brand, strategically spend on Sponsored Ads to secure high visibility placements on Amazon and lastly make sure your online product packaging via product pages contain attractive images to position your product in the best light.

Product Availability: Have plenty of stock available

Make sure to have plenty of stock available as shoppers are likely to turn to other brands/products in case your product is unavailable. Also, keep in mind that people are generally more open to trying new products during a sale as it offers discounts. Track your products’ stock status to make sure they’re available 24 x 7.

As the foremost goal during sales is to move inventory as much as possible, offering a large assortment is a good idea. Create product bundles that complement each other.

A+ Content is King: The new age packaging for your product

Content is the new age packaging for your product. Content is crucial to change consumer shortlists & considerations into conversions.

Your content tells your product story & gives customers the information they need to make a purchase. Use high resolution and accurate images, add features, benefits, USPs of your products clearly. It is advisable to use more than one image to show your product more clearly. Make sure all your brand & product pages on Amazon are optimized.

Reviews and Ratings: Feedback is a very important e-commerce tool.

Why would shoppers rely on word-of-mouth when they can take help from millions of people from the community? Not said enough, feedback is a very important e-commerce tool. Amazon’s A9 algorithm presents the choices to the consumers but reviews and star ratings still play an influential role in the journey from consideration to conversion.

Brands could consider partnering with Dataweave, to keep track of reviews and manage negative ratings on Amazon.

Summary

According to a report by EY-IVCA Trend Book 2021, “ The e-commerce industry in India is expected to reach $99 Bn by 2024 and penetration of retail is expected to be 10.7% by 2024, compared to 4.7% in 2019.”

Source: Statista

The same report also revealed that India will have 220 Million online shoppers by 2025. With e-commerce growing at an exponential rate, brands are advised to be more statistical & data-driven to win a larger % of online sales. If you think this is the right time to optimize your digital shelf, take a look at our products and services.

We at DataWeave would be happy to be a part of your e-commerce and digitization journey. You can sign up for a demo with our team to know more

As consumers socialize more this year, retailers around the world are competing for sales in the torrid health & beauty category.

That’s why we at DataWeave wanted to know how Prime Day 2021 discounts played a role in the pricing strategies for health & beauty products. We focused our analysis on how global retailers adapted their Prime Day pricing strategies to distinguish their offerings across seven health & beauty subcategories, including makeup, health care and baby care.

Our Methodology We tracked the pricing of products among 16 leading retailers in nine countries across five regions, including:

● The US (Amazon US, Sephora, Target, Ulta and Walmart) ● The UK (Amazon UK, Ebay, Etsy and OnBuy) ● Europe (Amazon France, Amazon Germany and Amazon Italy) ● The Middle East (Amazon Saudi Arabia and Amazon UAE) ● Asia (Amazon Japan and Amazon Singapore)

The results showed some surprising differences among retailers and regions. See how retailers used pricing as a competitive strategy to win Prime Day sales in the health & beauty category, as well as international health & beauty brands that stood out for the discounts on their products.

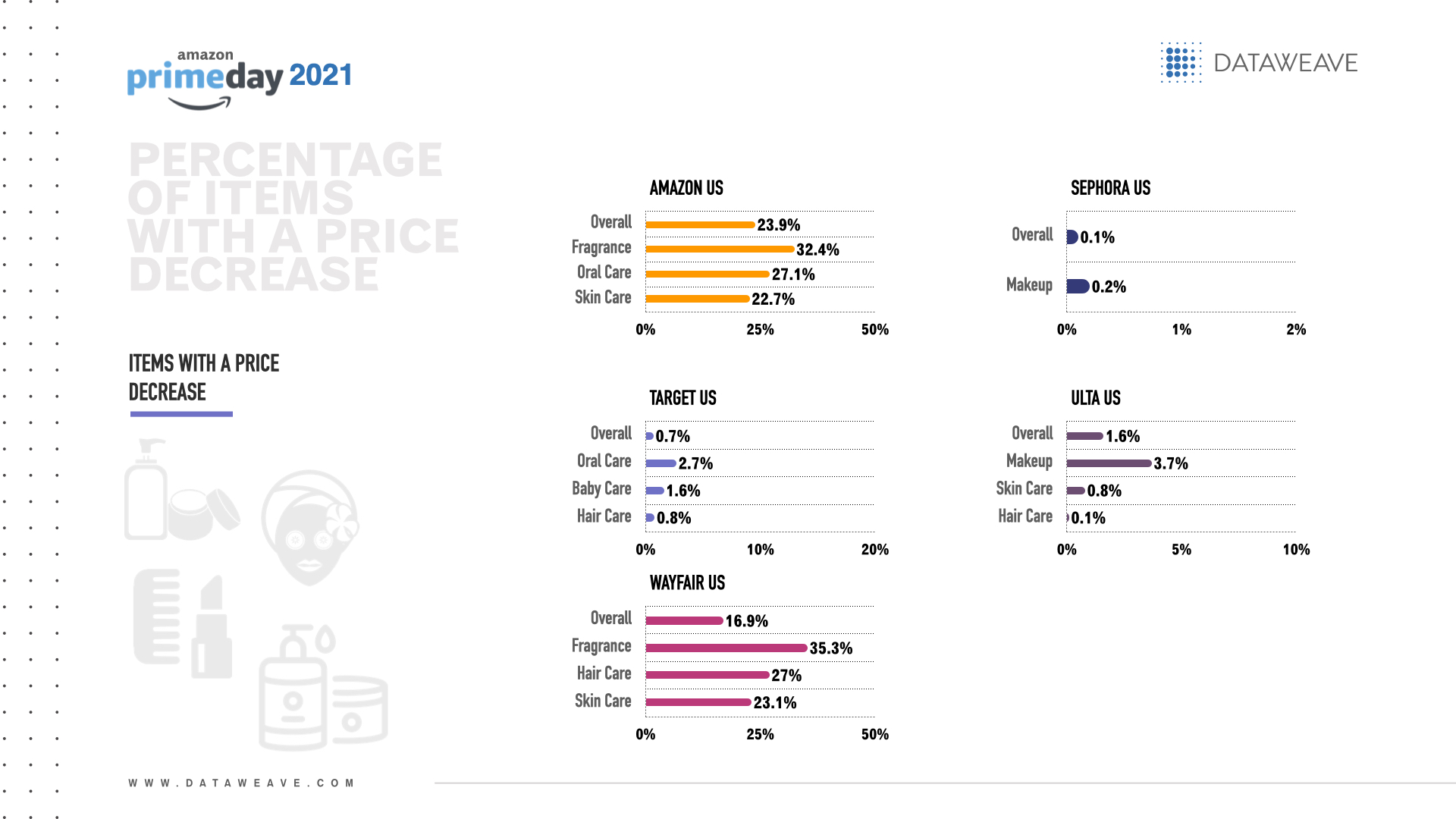

Percentage of items with a price decrease

The US retailer with the overall highest percentage of health & beauty products with a price decrease for Prime Day was Amazon US (23.9%).

Health & beauty subcategories with the highest percentage of items with a price decrease per US retailer were:

● Amazon US: Fragrance (32.4%), oral care (27.1%) and skin care (22.7%) ● Sephora: Makeup (0.2%) ● Target: Oral care (2.7%), baby care (1.6%) and hair care (0.8%) ● Ulta: Makeup (3.7%), skin care (0.8%) and hair care (0.1%) ● Walmart: Fragrance (35.3%), hair care (27.0%) and skin care (23.1%)

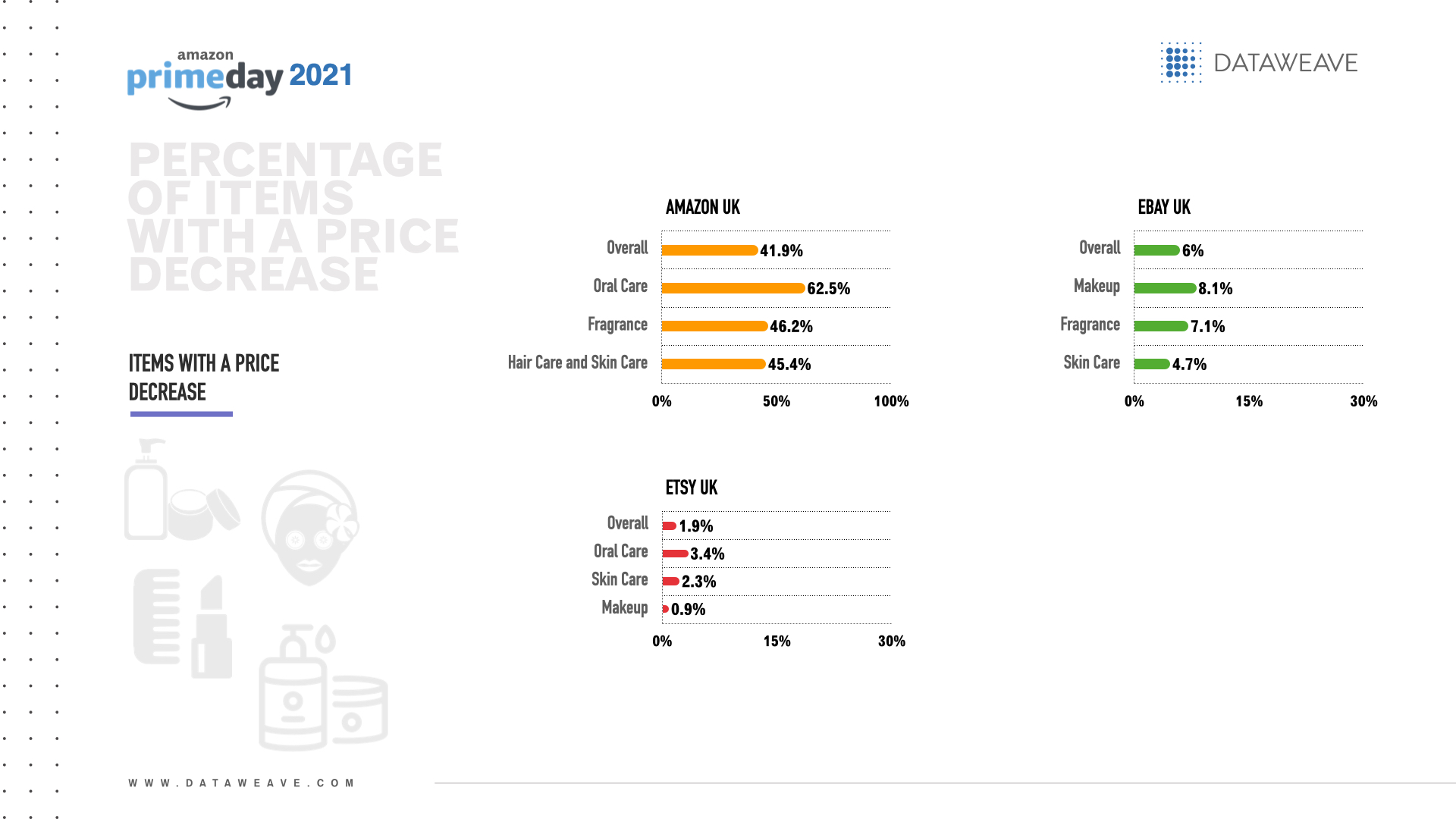

By far, the UK retailer with the overall highest percentage of items with a price decrease for Prime Day was Amazon UK (41.9%).

Health & beauty subcategories with the highest percentage of items with a price decrease per UK retailer were:

● Amazon UK: Oral care (62.5%), fragrance (46.2%) and hair care and skin care (both 45.4%) ● Ebay: Makeup (8.1%), fragrance (7.1%) and skin care (4.7%) ● Etsy: Oral care (3.4%), skin care (2.3%) and makeup (0.9%)

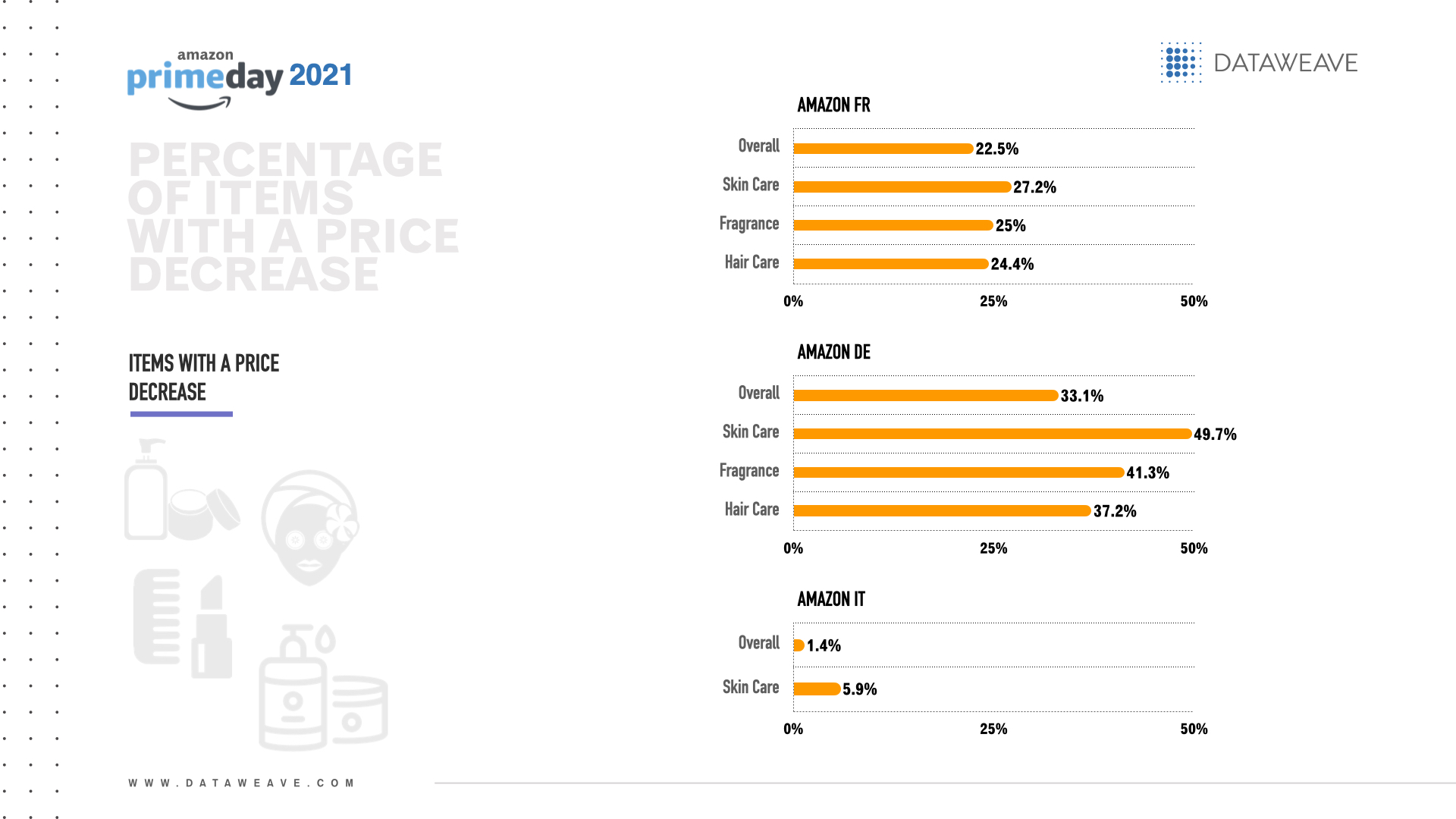

In Europe, Amazon Germany had the overall highest percentage of items with a price decrease for Prime Day (33.1%).

Health & beauty subcategories with the highest percentage of items with a price decrease per European retailer were:

● Amazon France: Skin care (27.2%), fragrance (25.0%) and hair care (24.4%) ● Amazon Germany: Skin care (49.7%), fragrance (41.3%) and hair care (37.2%) ● Amazon Italy: Skin care (5.9%)

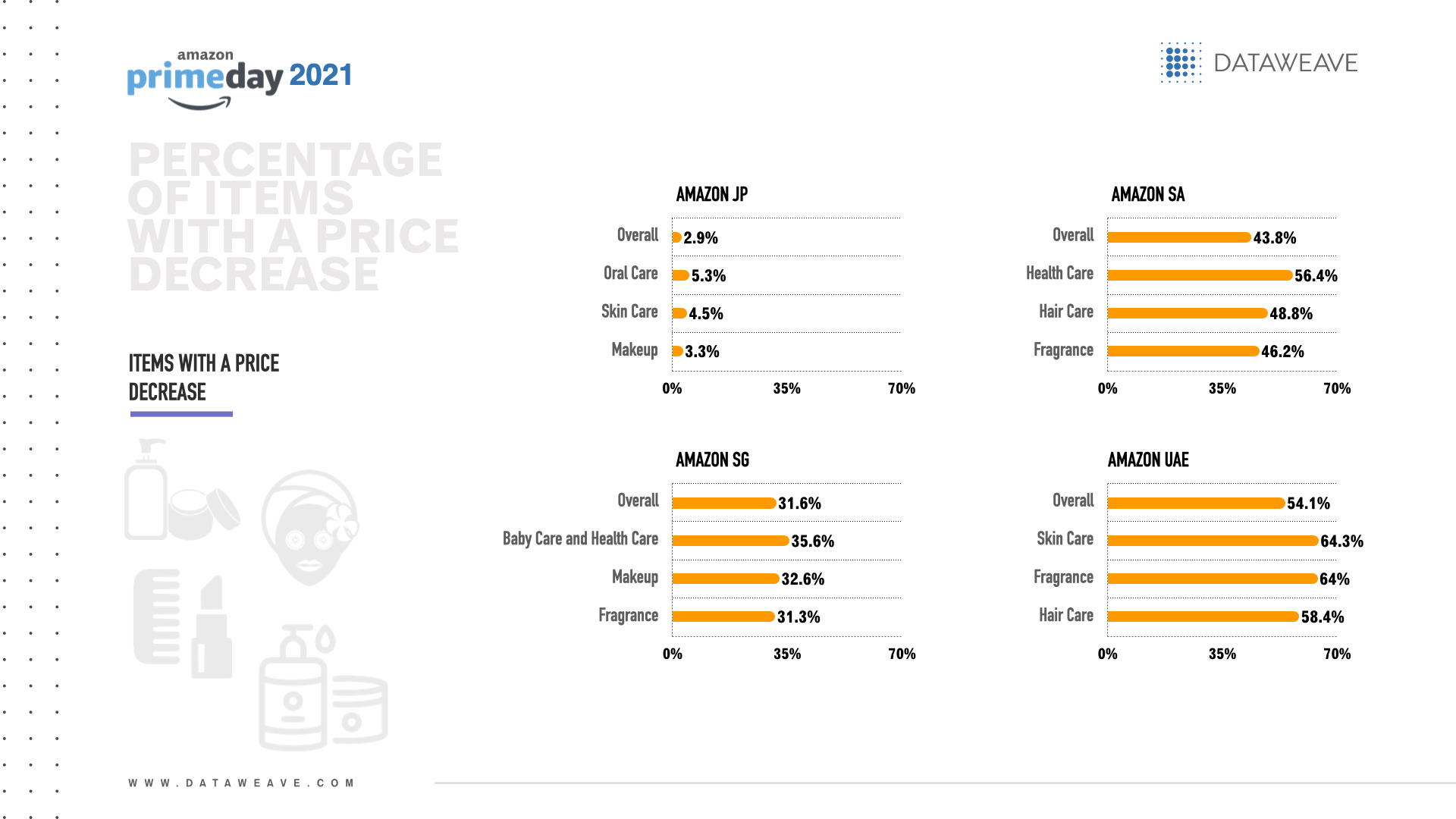

Across the Middle East & Asia, Amazon UAE had the overall highest percentage of health & beauty items with a price decrease for Prime Day (54.1%).

Health & beauty subcategories with the highest percentage of items with a price decrease per retailer were:

● Amazon Saudi Arabia: Health care (56.4%), hair care (48.8%) and fragrance (46.2%) ● Amazon UAE: Skin care (64.3%), fragrance (64.0%), and hair care (58.4%) ● Amazon Japan: Oral care (5.3%), skin care (4.5%) and makeup (3.3%) ● Amazon Singapore: Baby care and health care (both 35.6%), makeup (32.6%) and fragrance (31.3%)

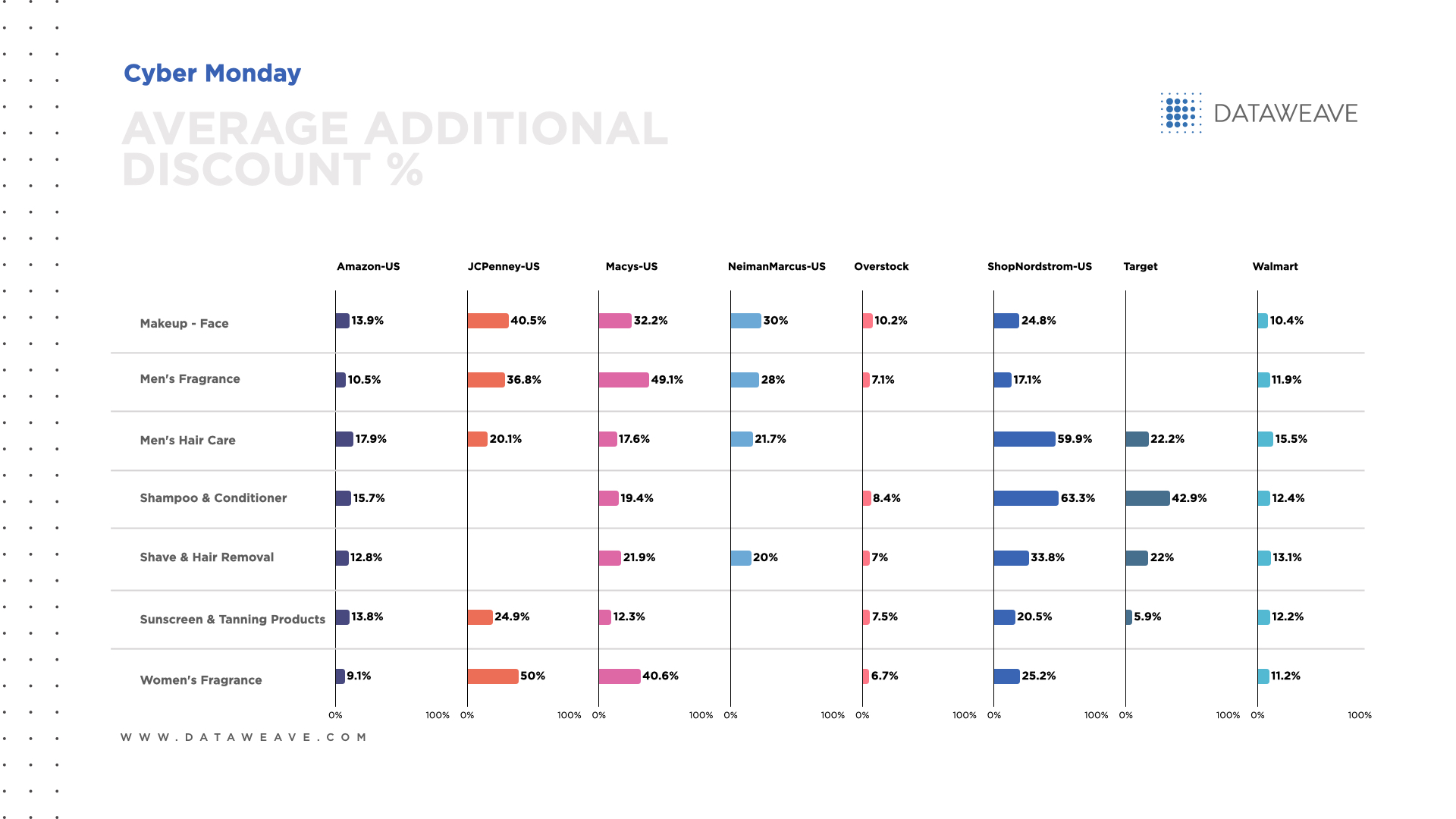

Magnitude of price decrease

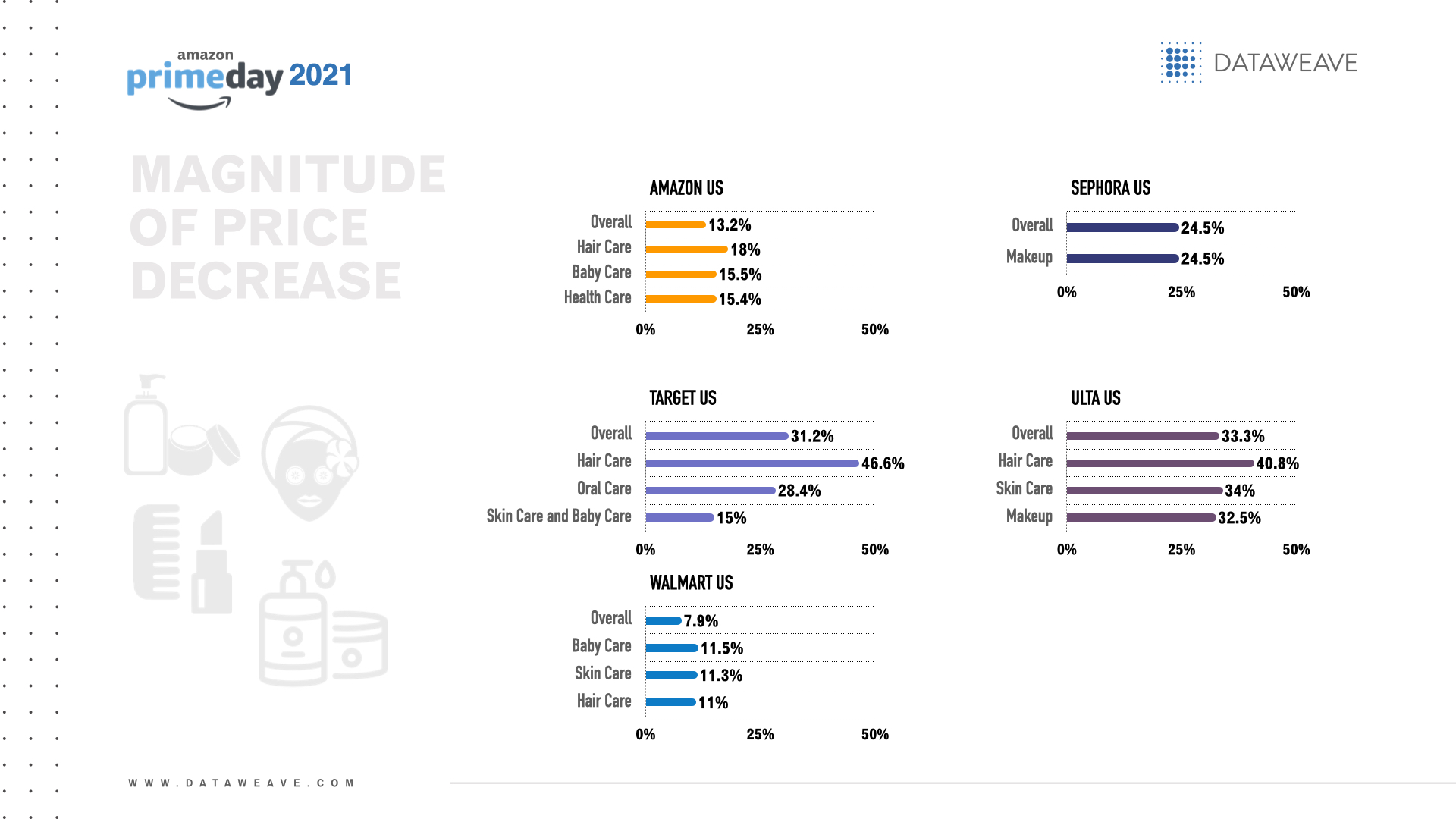

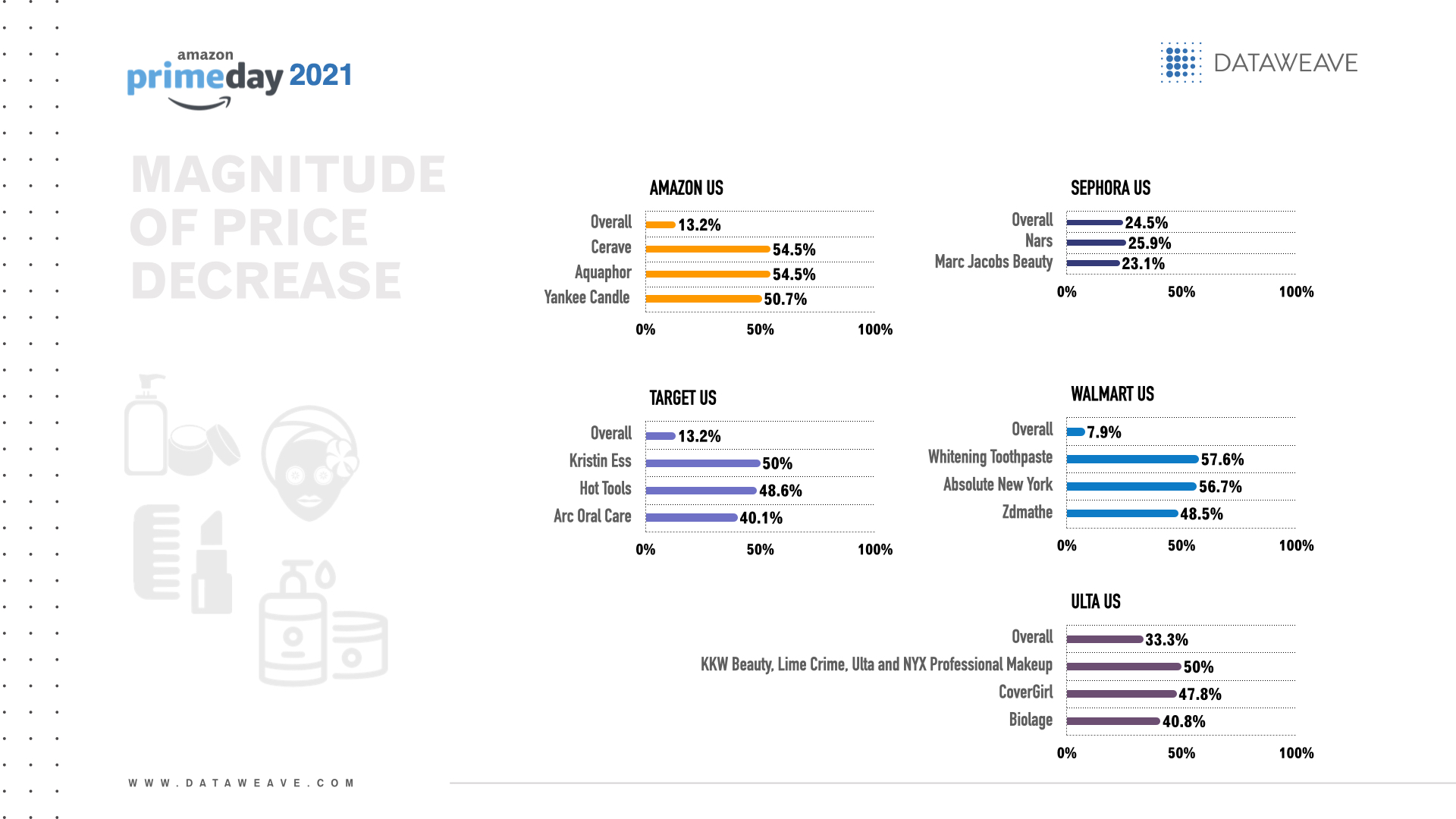

The US retailer with the greatest overall magnitude of price decrease for Prime Day was Ulta (33.3%).

The health & beauty subcategories with the greatest magnitude of price decrease per US retailer were:

● Amazon US: Hair care (18.0%), baby care (15.5%) and health care (15.4%) ● Sephora: Makeup (24.5%) ● Target: Hair care (46.6%), oral care (28.4%) and skin care and baby care (both 15.0%) ● Ulta: Hair care (40.8%), skin care (34.0%) and makeup (32.5%) ● Walmart: Baby care (11.5%), skin care (11.3%) and hair care (11.0%)

Brands with the greatest magnitude of price decreases per US retailer included:

● Amazon US: Cerave (54.5%), Aquaphor (54.4%) and Yankee Candle (50.7%) ● Sephora: Nars (25.9%) and Marc Jacobs Beauty (23.1%) ● Target: Kristin Ess (50.0%), Hot Tools (48.6%) and Arc Oral Care (both 40.1%) ● Ulta: KKW Beauty, Lime Crime, Ulta and NYX Professional Makeup (all 50.0%), CoverGirl (47.8%) and Biolage (40.8%) ● Walmart: Whitening Toothpaste (57.6%), Absolute New York (56.7%) and Zdmathe (48.5%)

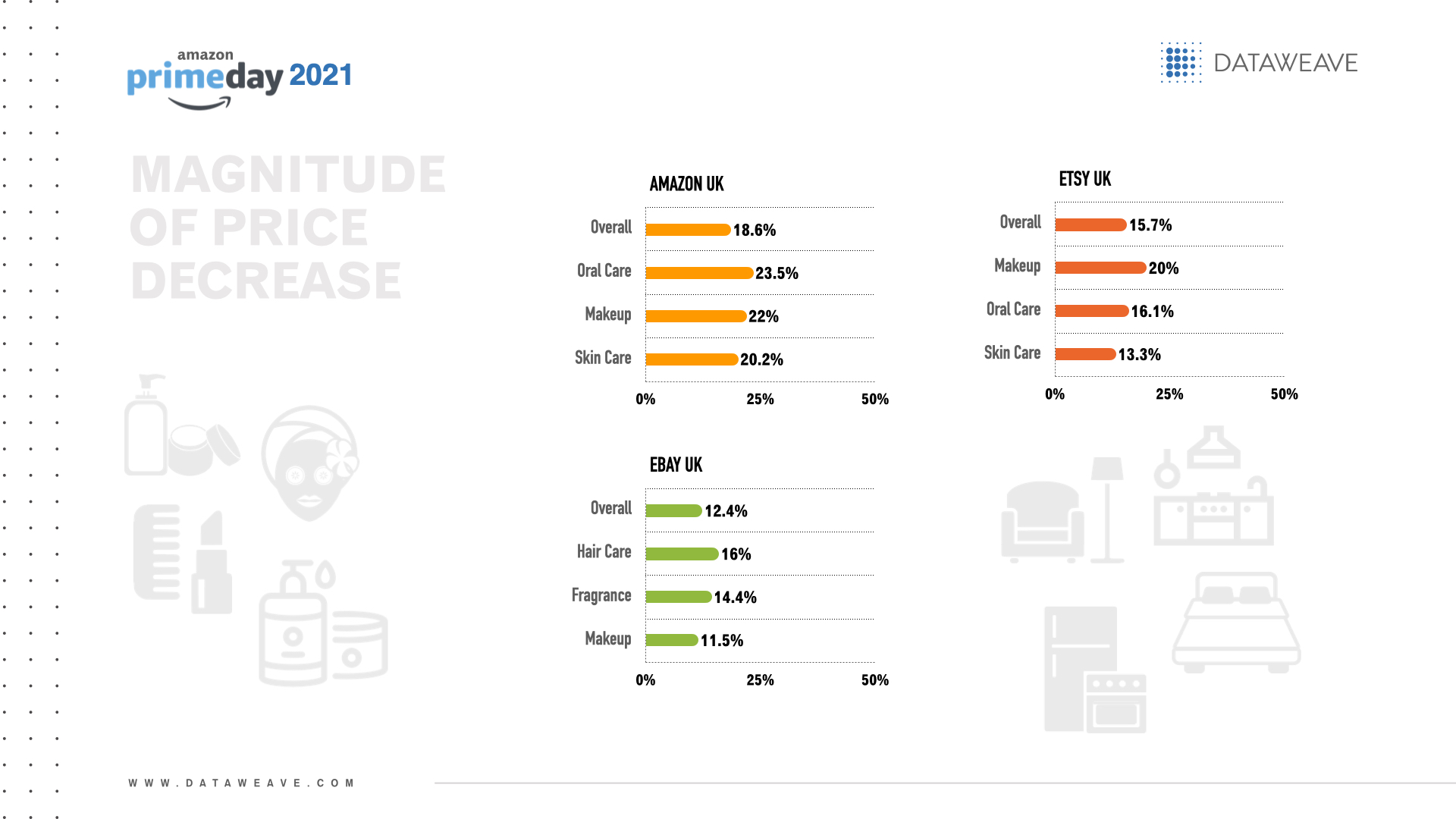

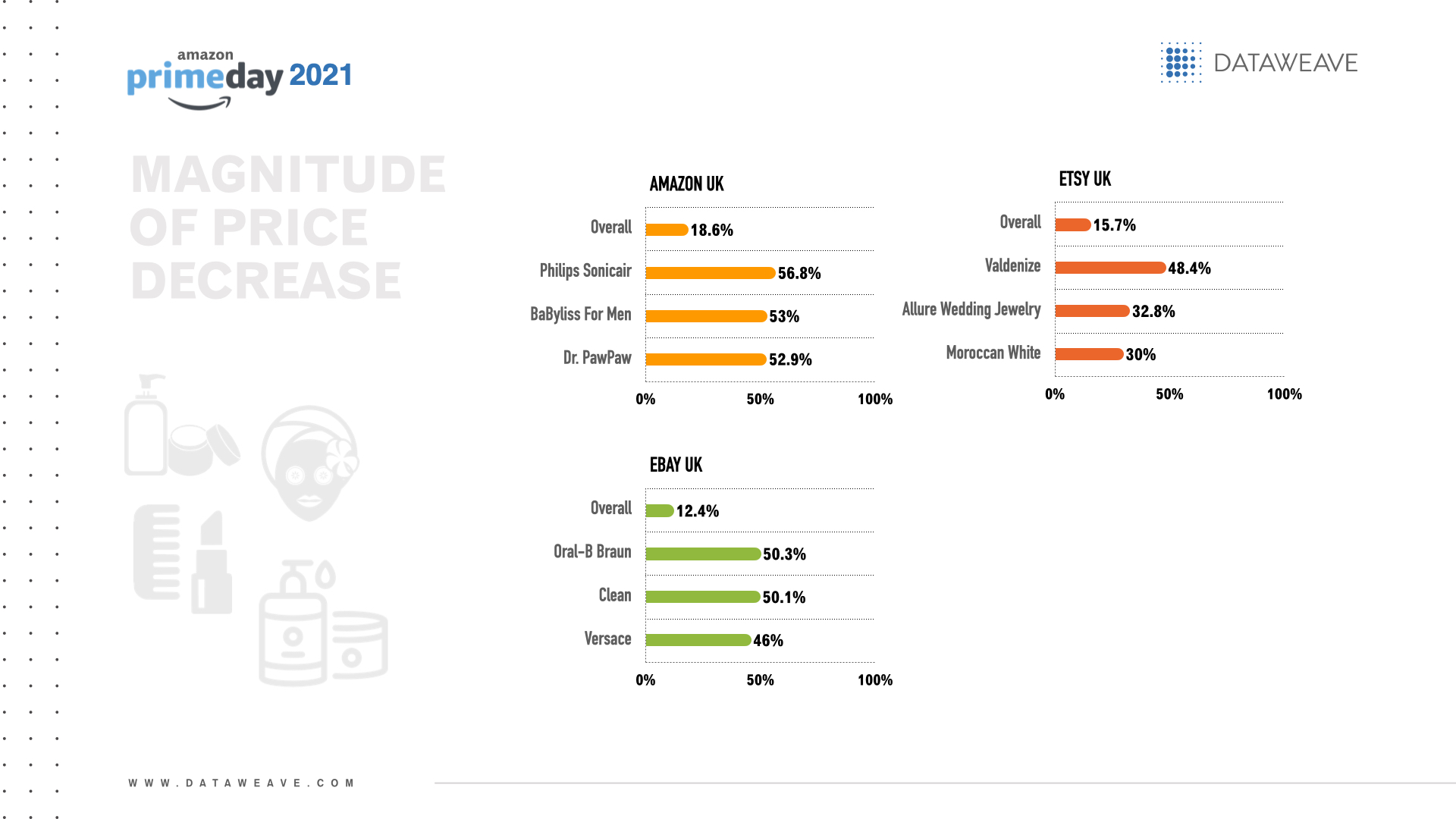

The UK retailer with the greatest overall magnitude of price decrease on health & beauty products for Prime Day was Amazon UK (18.6%).

The health & beauty subcategories with the greatest magnitude of price decrease per UK retailer were:

● Amazon UK: Oral care (23.5%), makeup (22.0%) and skin care (20.2%) ● Ebay: Hair care (16.0%), fragrance (14.4%) and makeup (11.5%) ● Etsy: Makeup (20.0%), oral care (16.1%) and skin care (13.3%)

Brands with the greatest magnitude of price decreases across health & beauty sub-categories per UK retailer included:

● Amazon UK: Philips Sonicair (56.8%), BaByliss For Men (53.0%) and Dr. PawPaw (52.9%) ● Ebay: Oral-B Braun (50.3%), Clean (50.1%) and Versace (46.0%) ● Etsy: Valdenize (both 48.4%), Allure Wedding Jewelry (32.8%) and Moroccan White (30.0%)

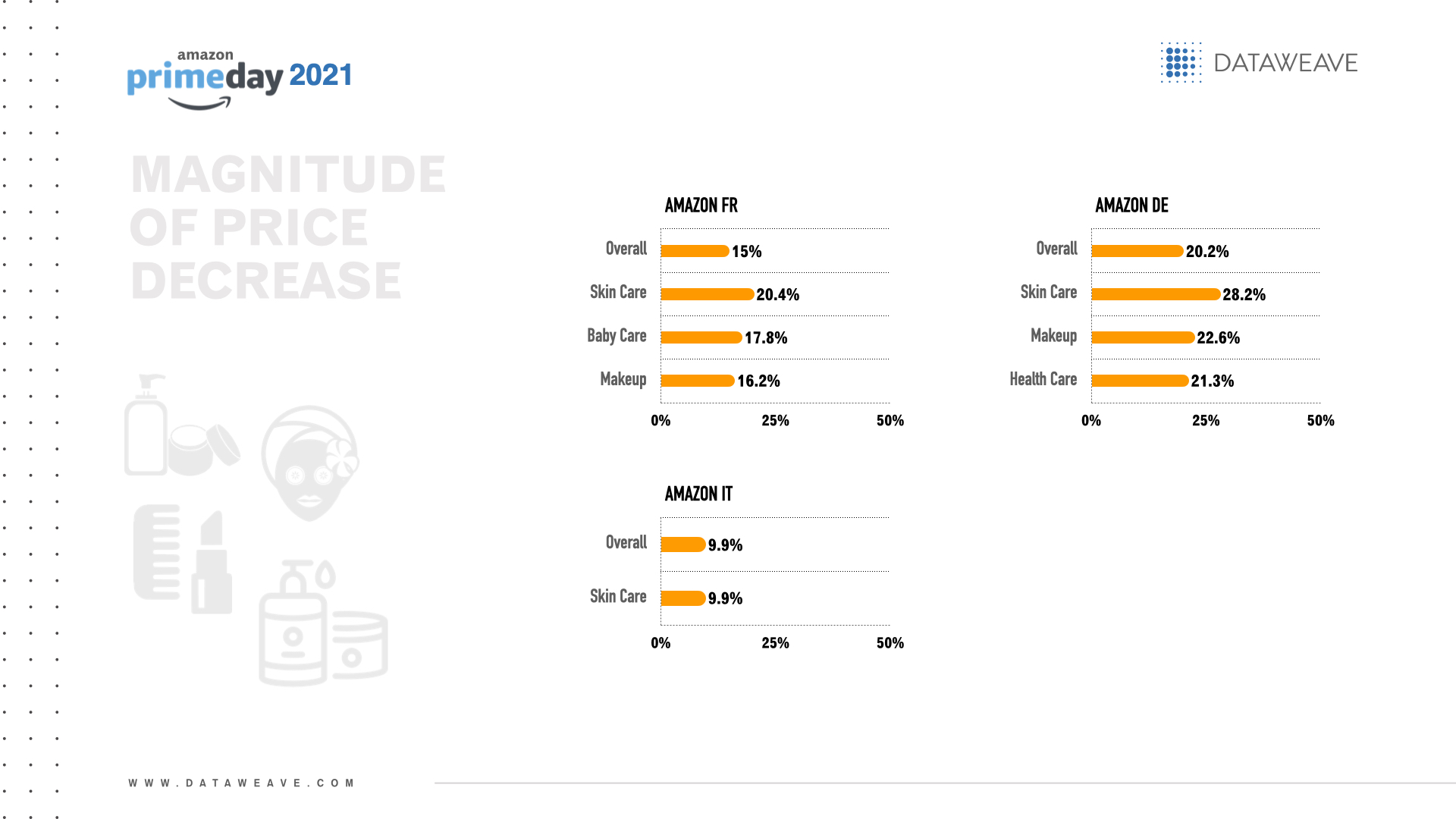

Among European retailers, Amazon Germany offered the greatest overall magnitude of price decrease on health & beauty products for Prime Day (20.2%).

The health & beauty subcategories with the greatest magnitude of price decrease per European retailer were:

● Amazon France: Skin care (20.4%), baby care (17.8%) and makeup (16.2%) ● Amazon Germany: Skin care (28.2%), makeup (22.6%) and health care (21.3%) ● Amazon Italy: Skin care (9.9%)

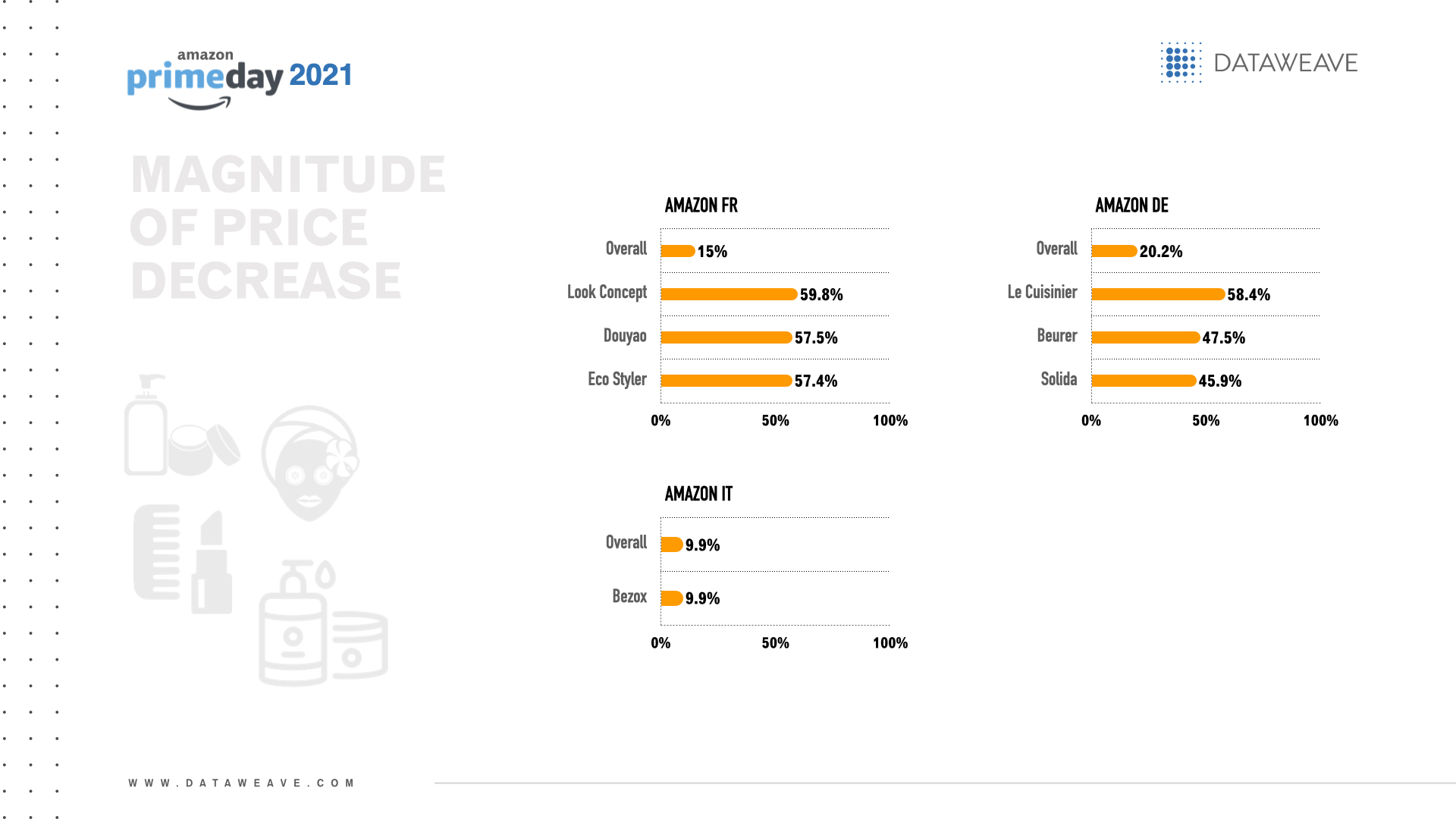

Brands with the greatest magnitude of price decreases per European retailer included:

● Amazon France: Look Concept (59.8%), Douyao (57.5%) and Eco Styler (57.4% for both hair care and health care) ● Amazon Germany: Le Cuisinier (58.4%), Beurer (47.5%) and Solida (45.9%) ● Amazon Italy: Bezox (9.9%)

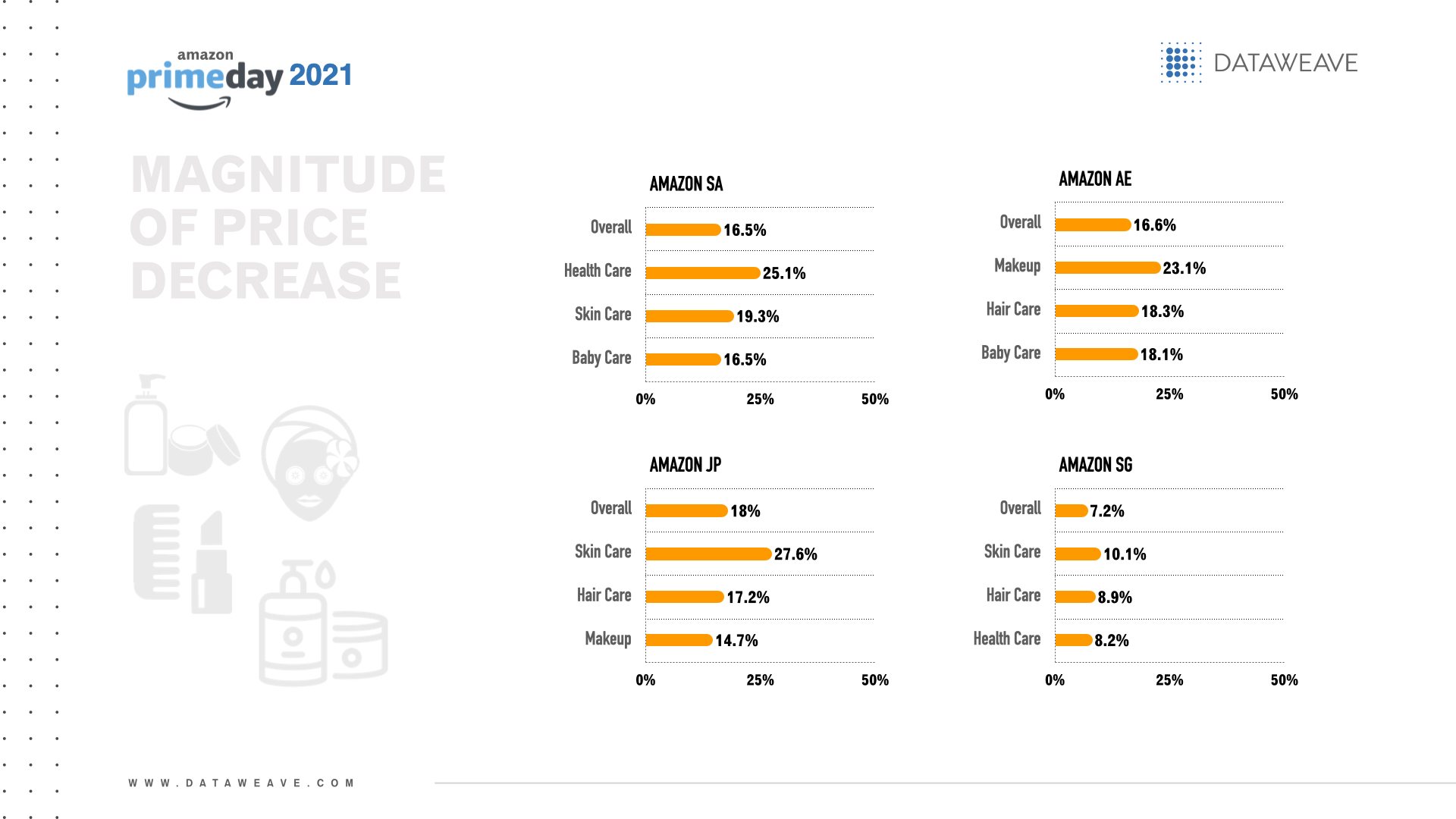

Across the Middle East and Asia, Amazon Japan offered the greatest overall magnitude of price decrease on health & beauty products for Prime Day (18.0%).

The health & beauty subcategories with the greatest magnitude of price decrease per retailer were:

● Amazon Saudi Arabia: Health care (25.1%), skin care (19.3%) and baby care (16.5%) ● Amazon UAE: Makeup (23.1%), hair care (18.3%) and baby care (18.1%) ● Amazon Japan: Skin care (27.6%), hair care (17.2%) and makeup (14.7%) ● Amazon Singapore: Skin care (10.1%), hair care (8.9%) and health care (8.2%)

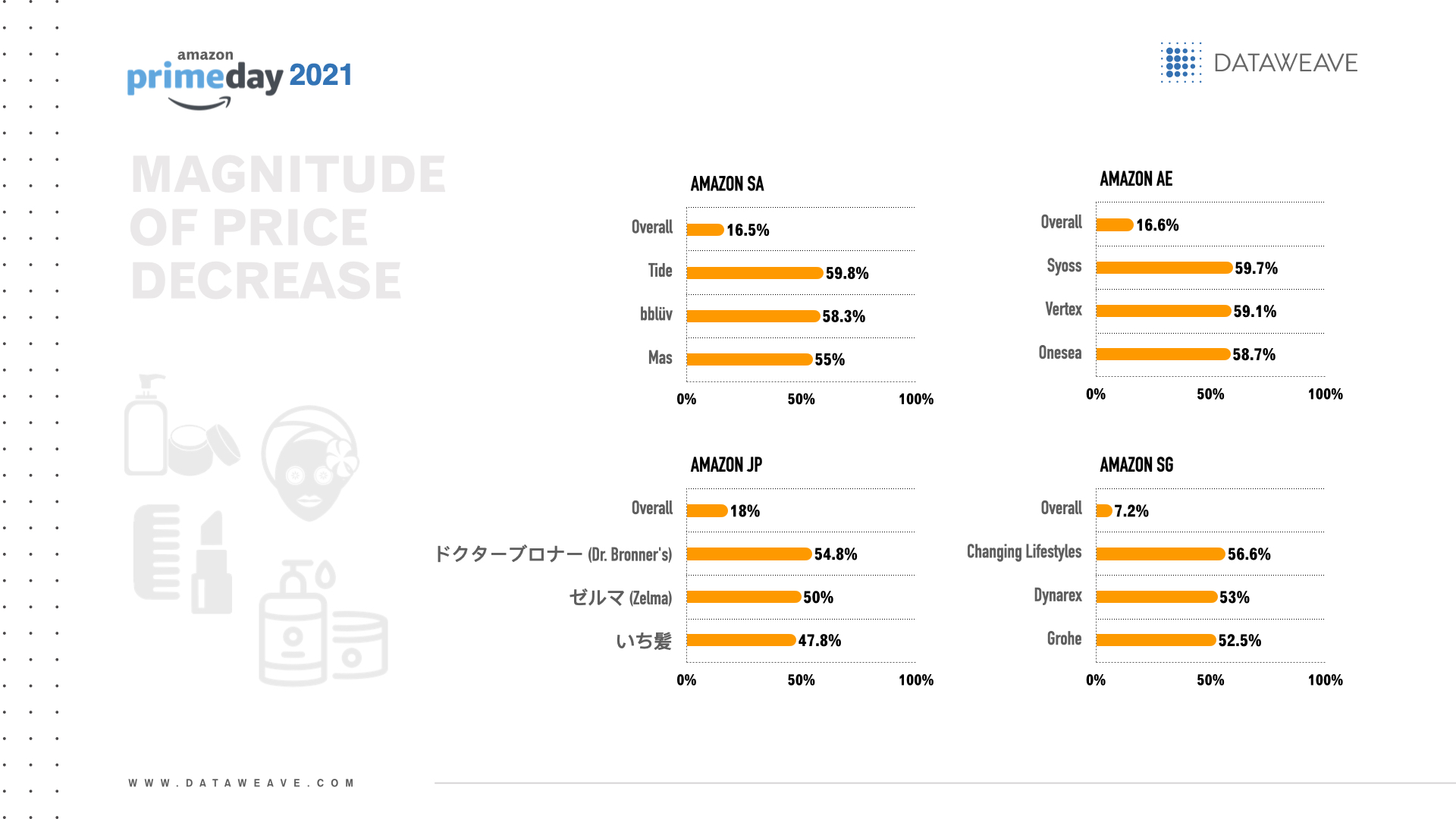

Brands with the greatest magnitude of price decreases per retailer in the Middle East and Asia included:

● Amazon Saudi Arabia: Tide (59.8%), bblüv (58.3%) and Mas (55.0%) ● Amazon UAE: Syoss (59.7%), Vertex (59.1%) and Onesea (58.7%) ● Amazon Japan: ドクターブロナー (Dr. Bronner’s) (54.8%), ゼルマ (Zelma) (50.0%) and いち髪 (47.8%) ● Amazon Singapore: Changing Lifestyles (56.6%), Dynarex (53.0%) and Grohe (52.5%)

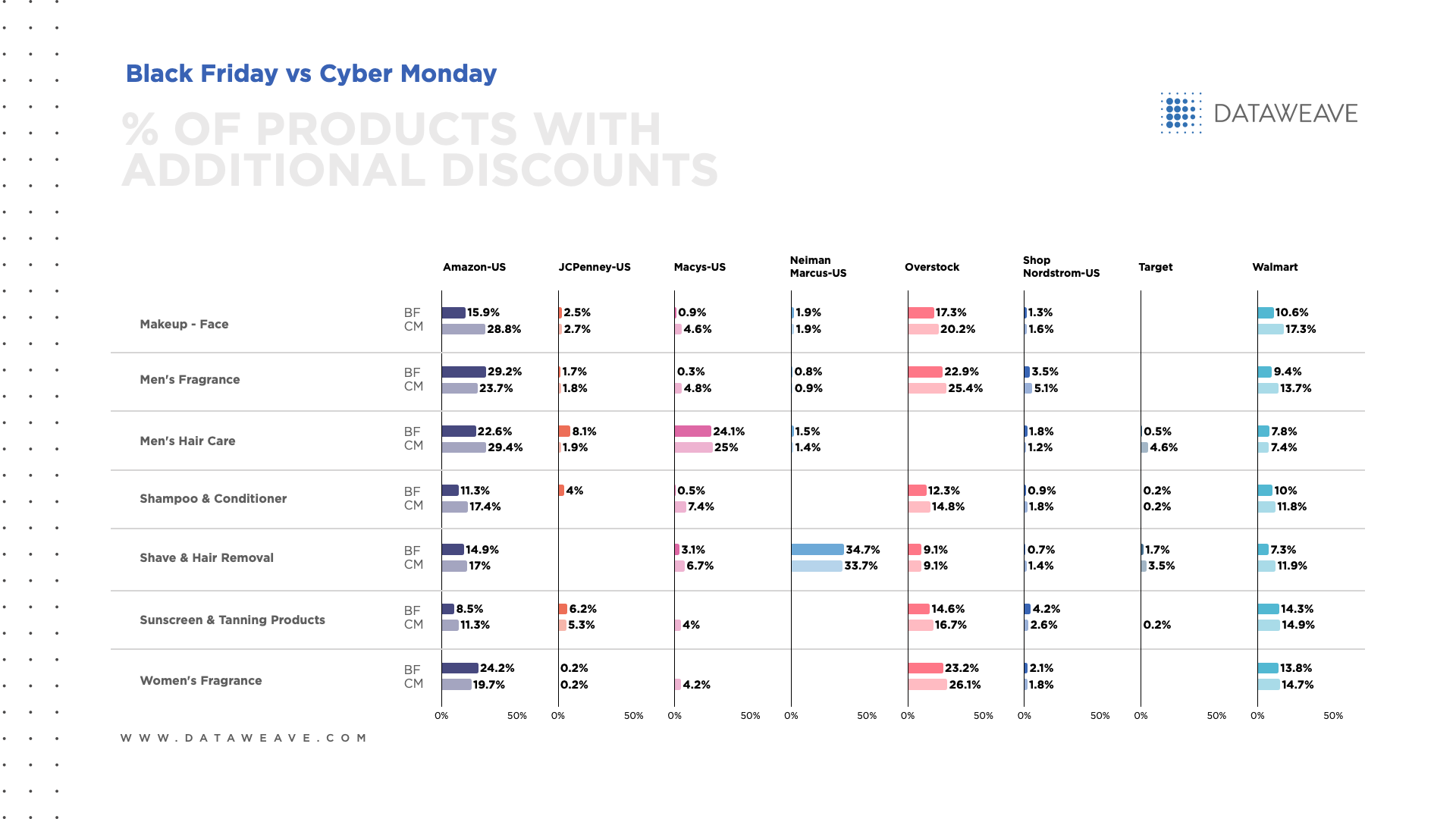

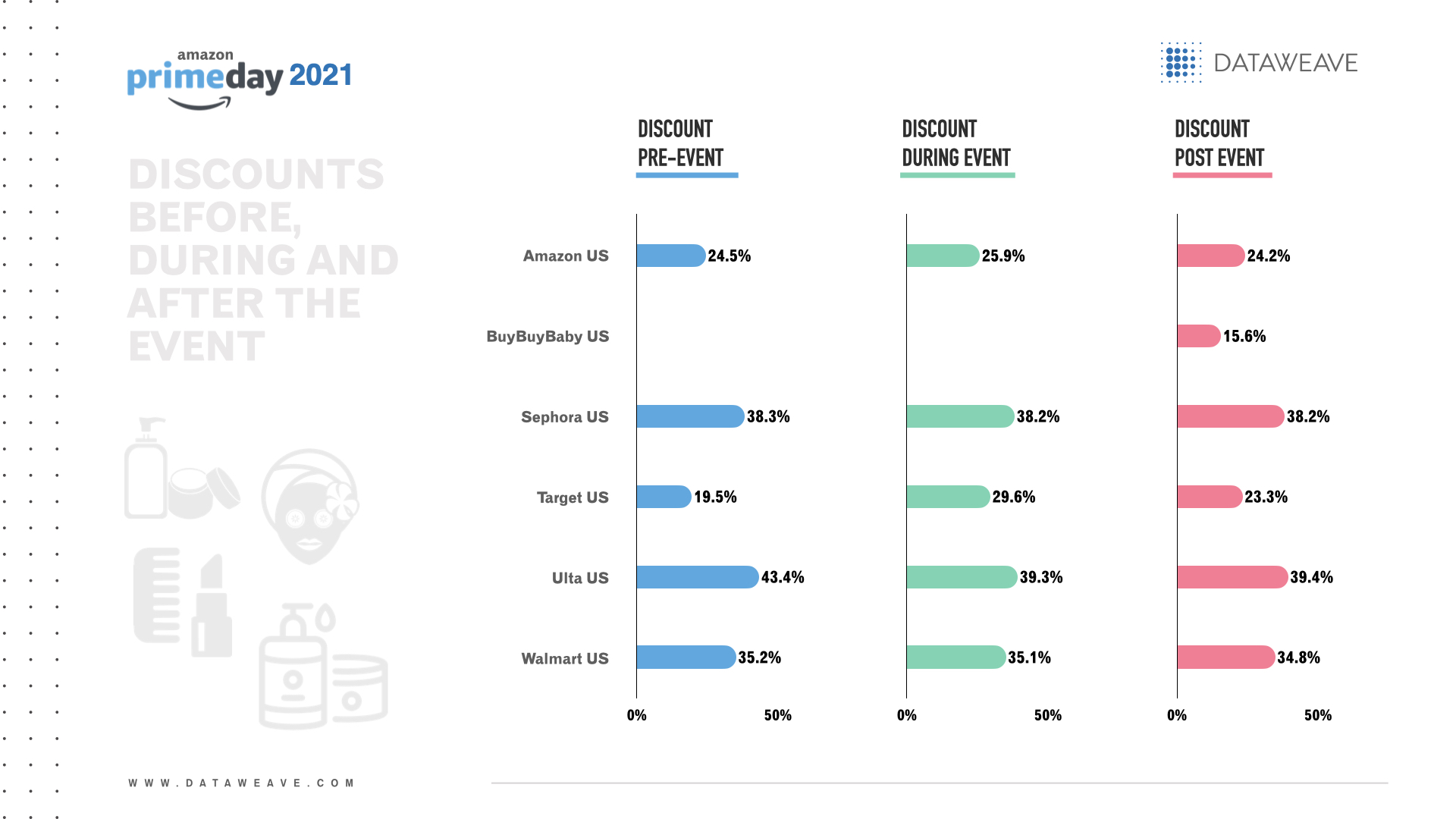

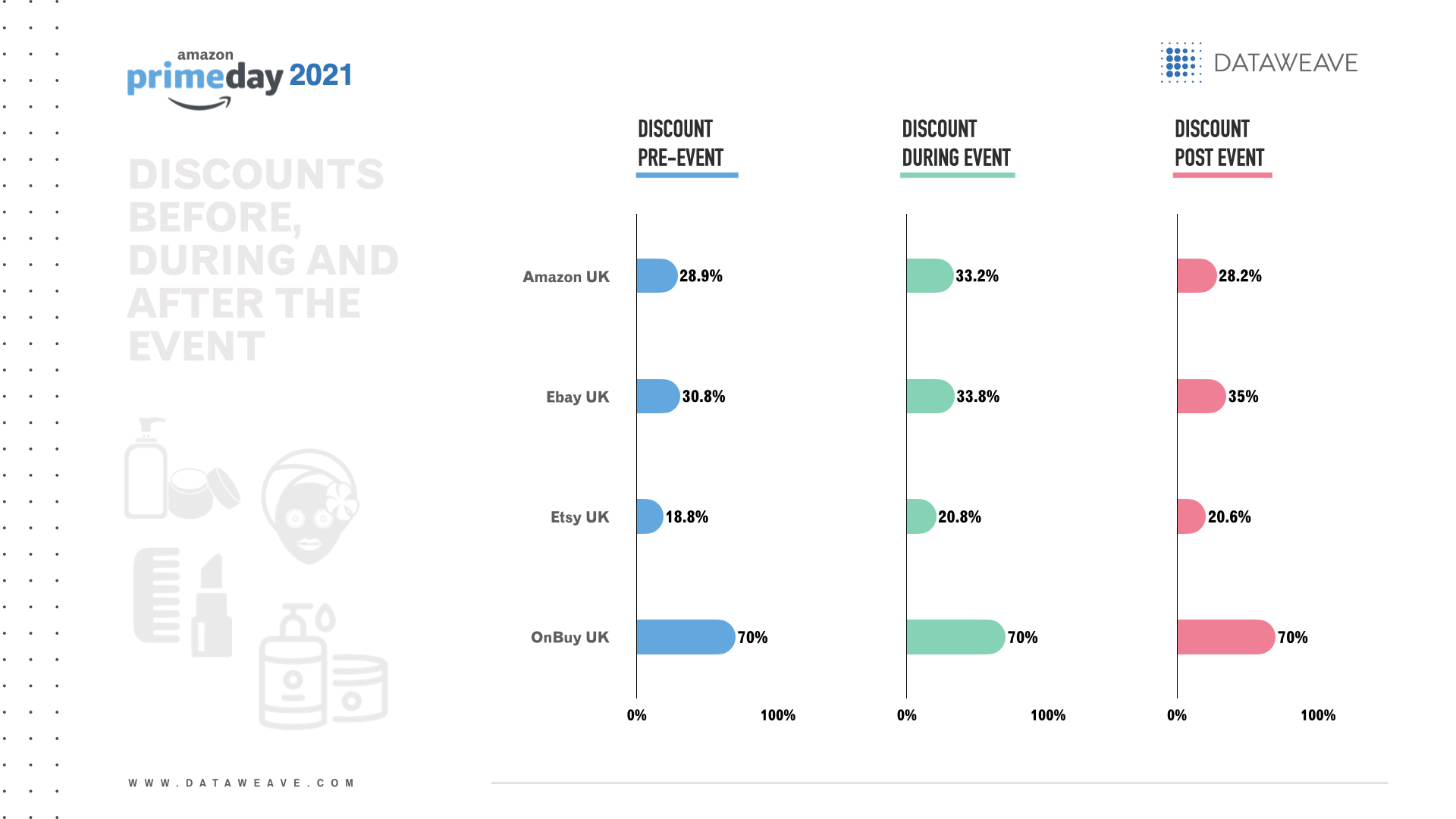

Discounts before, during and after the event

In the US, specialty beauty retailers’ discounts stood out during Prime Day sales. The US retailer with the biggest overall health & beauty discount before (43.4%), during (39.3%) and after (39.4%) Prime Day was Ulta. During and after Prime Day, Sephora was a close second at 38.2% for both periods.

Ulta’s biggest pre-event discounts were on makeup (44.2%) and skin care (33.0%). Hair care (40.8%). makeup (39.5%) and skin care (36.0%) were the leading subcategories for Ulta’s discounts during Prime Day. After the event, Ulta’s biggest discounts were for hair care (40.8%), makeup (39.6%) and skin care (37.3%)

In the UK, OnBuy offered the highest discounts before, during and after Prime Day at 70.0% off baby care products. Yet the total product count was only 2.

Among the remaining rivals, all of whom had a product count above 1000, Ebay had the highest discounts before (30.8%), during (33.8%) and after (35.0%) Prime Day.

Before Prime Day, Ebay biggest discounts were on hair care (48.9%), fragrance (23.9%) and makeup (23.4%). Ebay’s top discounts during Prime Day were on hair care (50.3%), makeup (24.9%) and fragrance (24.8%). Similarly, after the event, Ebay had the biggest discounts on hair care (49.9%), makeup (26.7%) and fragrance (26.2%).

Across retailers in the Middle East & Asia, Amazon UAE offered the biggest overall health & beauty discounts before (26.0%), during (30.7%) and after (26.0%) Prime Day.

In the pre-sales event, Amazon UAE offered the most generous discounts on makeup (30.7%), fragrance (29.9%) and health care (29.2%).

During Prime Day, Amazon UAE’s biggest discounts were on makeup (37.2%), fragrance (31.6%) and health care (31.3%).

During Prime Day, Amazon UAE offered the biggest discounts on fragrance (30.5%), makeup (30.0%) and health care and baby care (both 26.8%).

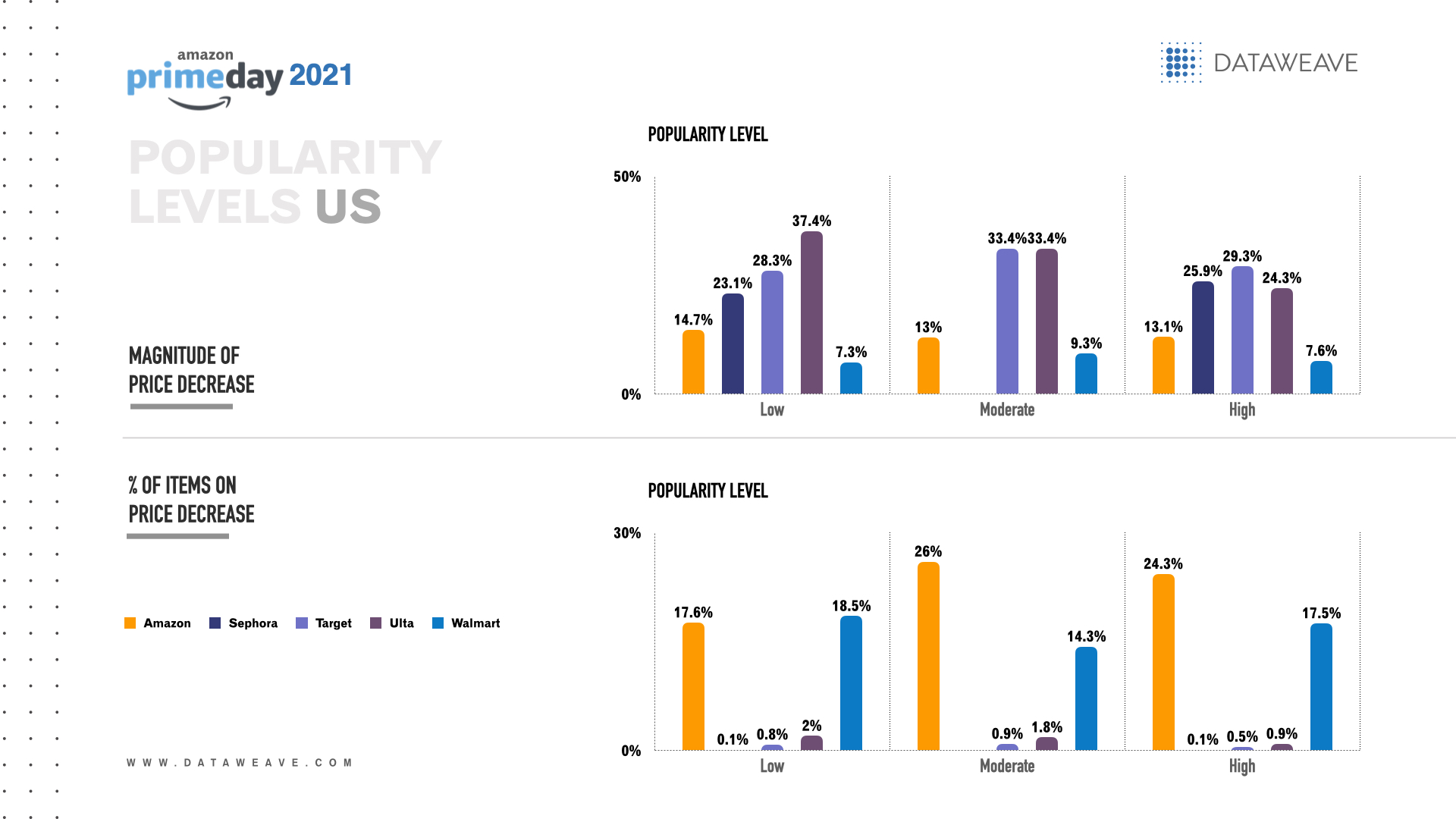

Popularity

In the US, among health & beauty products with high popularity, Amazon US offered the highest percentage of items with a price decrease (24.3%) and Target offered the greatest magnitude of price decrease (29.3%).

For health & beauty items with medium popularity, Amazon US offered the highest percentage of items with a price decrease (26.0%), and strategic partners Target and Ulta both offered the greatest magnitude of price decrease (33.4%).

Among health & beauty merchandise with low popularity, Walmart offered the highest percentage of items with a price decrease (18.5%) and Ulta offered the greatest magnitude of price decrease (37.4%).

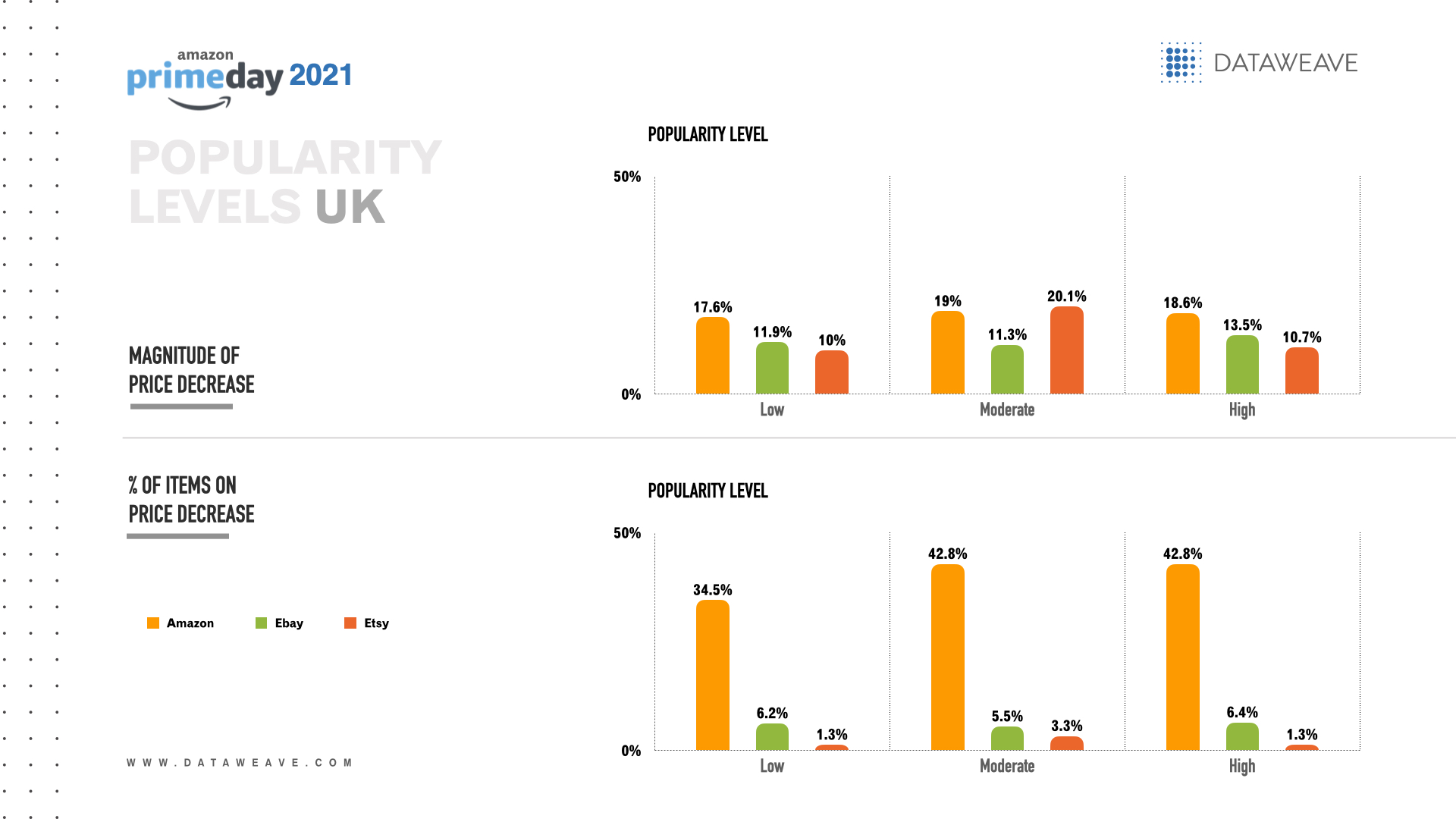

Amazon UK stood out among all levels of health & beauty product popularity.

In the UK, among health & beauty products with high popularity, Amazon UK offered both the highest percentage of items with a price decrease (42.8%) and the greatest magnitude of price decrease (18.6%).

For health & beauty items with medium popularity, Amazon UK offered the highest percentage of items with a price decrease (42.8%) and Etsy offered the greatest magnitude of price decrease (20.1%).

Among health & beauty merchandise with low popularity, Amazon UK offered both the highest percentage of items with a price decrease (35.4%) and the greatest magnitude of price decrease (17.6%).

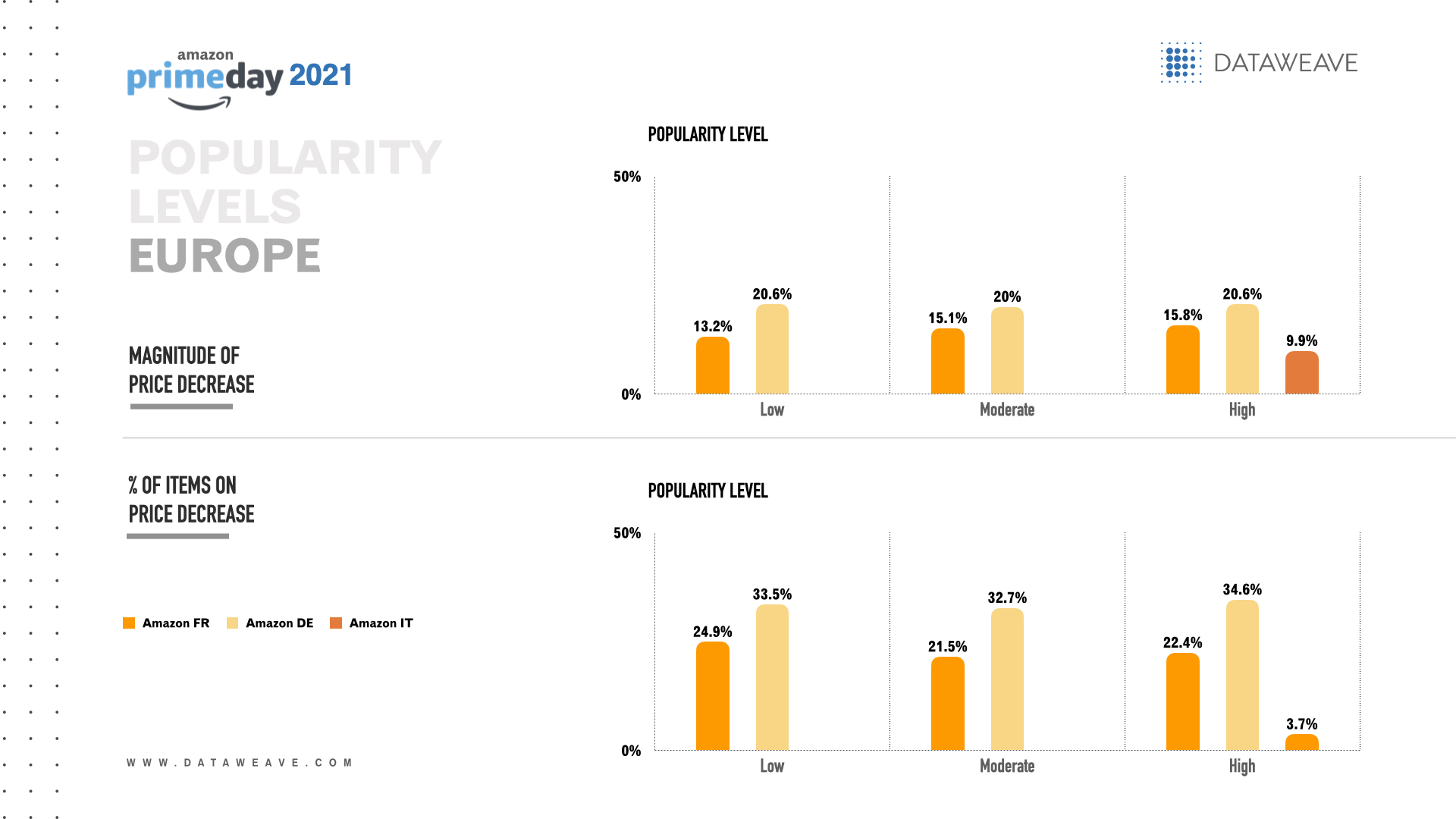

In Europe, Amazon Germany dominated discounts for health & beauty products across all levels of popularity.

Among health & beauty goods with high popularity, Amazon Germany offered both the highest overall percentage of items with a price decrease (34.6%) and the greatest overall magnitude of price decrease (20.6%).

For health & beauty items with medium popularity, Amazon Germany offered both the highest percentage of items with a price decrease (32.7%) and the greatest magnitude of price decrease (20.0%).

Among health & beauty merchandise with low popularity, Amazon Germany offered the highest percentage of items with a price decrease (33.5%) and the greatest magnitude of price decrease (20.6%).

In Middle East & Asia, among health & beauty items with high popularity, Amazon UAE offered the highest overall percentage of items with a price decrease (53.0%) and Amazon Saudi Arabia had the greatest overall magnitude of price decrease (18.7%).

For health & beauty products with medium popularity, Amazon UAE offered the highest overall percentage of items with a price decrease (55.3%) and Amazon Saudi Arabia had the greatest overall magnitude of price decrease (19.7%).

Among health & beauty goods with low popularity, Amazon UAE offered the highest percentage of items with a price decrease (54.5%) and Amazon Japan had the greatest magnitude of price decrease (18.7%).

Health & beauty’s stunning Prime Day deals

Overall, Prime Day 2021 gave shoppers around the world the opportunity to score generous discounts on health & beauty products.

According to our analysis, the retailers whose Prime Day pricing stood out the most were Amazon US and Ulta in the US, Amazon UK and Ebay in the UK, Amazon Germany in Europe, Amazon UAE in the Middle East and Amazon Japan in Asia.

Stay tuned for Prime Day 2021 international fashion and home goods pricing insights.

Amazon’s Prime Day 2021 global shopping event took place June 21 and 22, 2021 and smashed previous sales records. At DataWeave, we wanted to know how Prime Day 2021 deals and discounts on electronics compared across retailers and regions. We focused on how retailers adapted their Prime Day pricing strategies to stand out in the competitive consumer electronics category.

Our Methodology We tracked the pricing of several leading retailers in nine countries across five regions, including:

• The US (Amazon US, Best Buy, Target and Walmart) • The UK (Amazon UK, Ebay, Etsy and OnBuy) • Europe (Amazon France, Amazon Germany and Amazon Italy) • The Middle East (Amazon Saudi Arabia and Amazon UAE) • Asia (Amazon Japan and Amazon Singapore)

Let’s see how retailers used pricing tactics to gain a competitive advantage during Prime Day, as well as which electronics brands had the highest discounts around the world.

Percentage of items with a price decrease

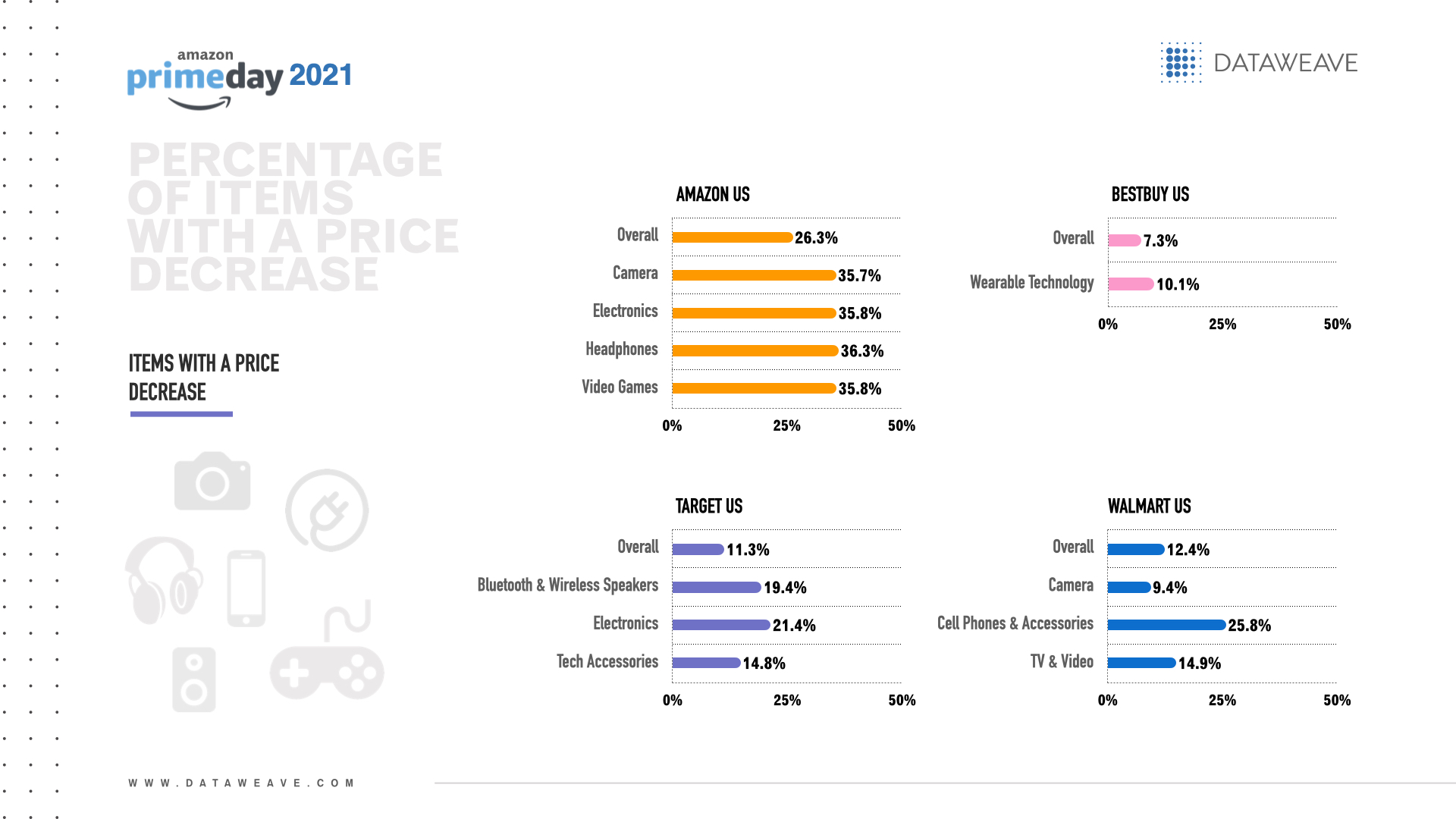

The US retailer with the overall highest percentage of items with a price decrease for Prime Day was Amazon US (26.3%).

Electronics subcategories with the highest percentage of items with a price decrease per US retailer were:

• Amazon US: Headphones (36.3%), video games and electronics (both 35.8%) and cameras (35.7%) • Best Buy: Wearables (10.1%) and electronics (6.8%) • Target: Electronics (21.4%), Bluetooth & wireless speakers (19.4%) and tech accessories (14.8%) • Walmart: Cell phones & accessories (25.8%), TV & video (14.9%) and cameras (9.4%)

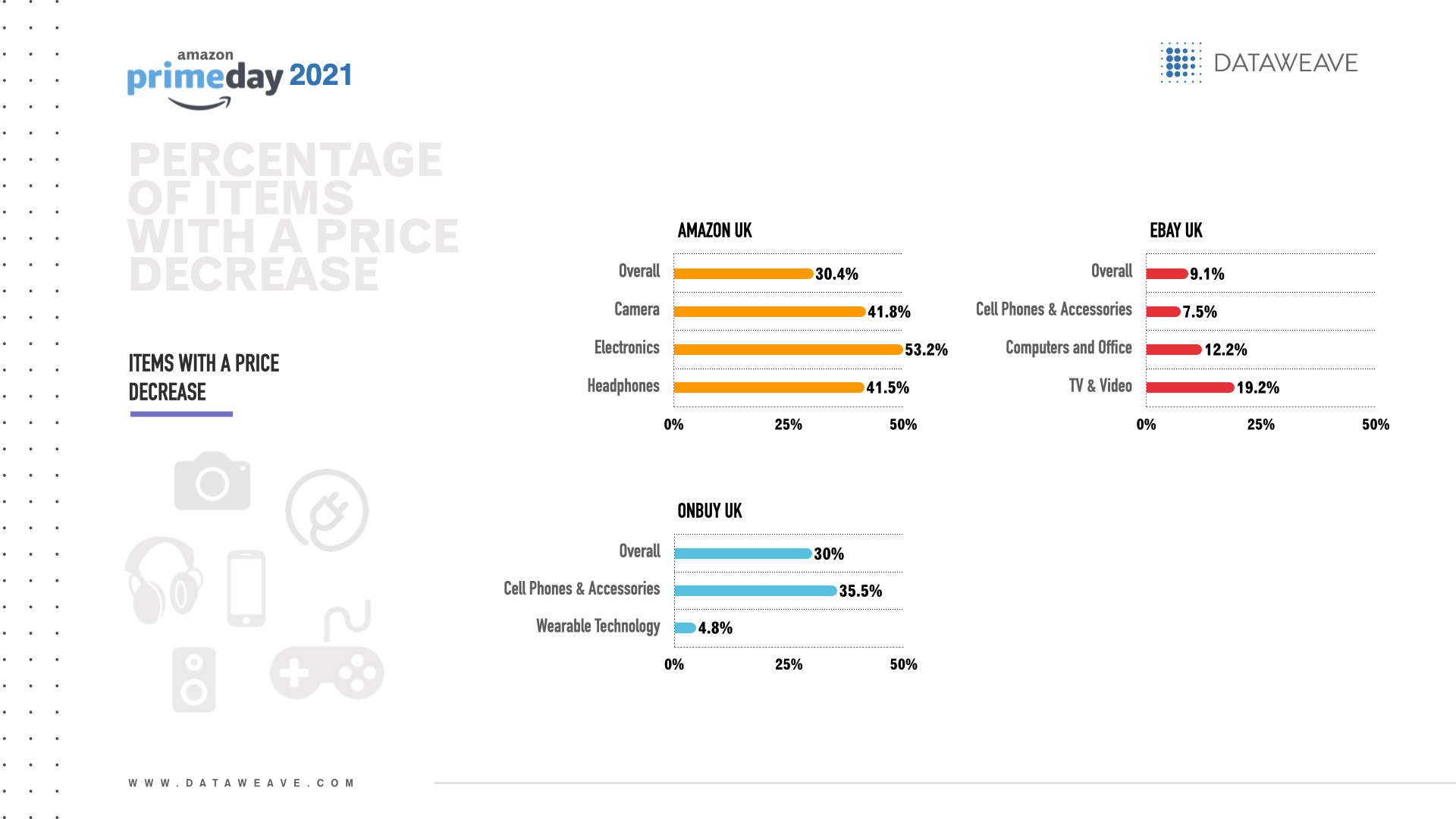

The UK retailer with the overall highest percentage of items with a price decrease for Prime Day was Amazon UK (30.4%), closely followed by OnBuy (30.0%). Of note, Amazon UK offered price increases on 10 times as many products as OnBuy (2379 vs. 237).

Electronics subcategories with the highest percentage of items with a price decrease per UK retailer were:

• Amazon UK: Electronics (53.2%), cameras (41.8%) and headphones (41.5%) • Ebay: TV & video (19.2%), computers & office (12.2%) and cell phones & accessories (7.5%) • Etsy: Electronics (1.4%) • OnBuy: Cell phones & accessories (35.5%) and wearables (4.8%)

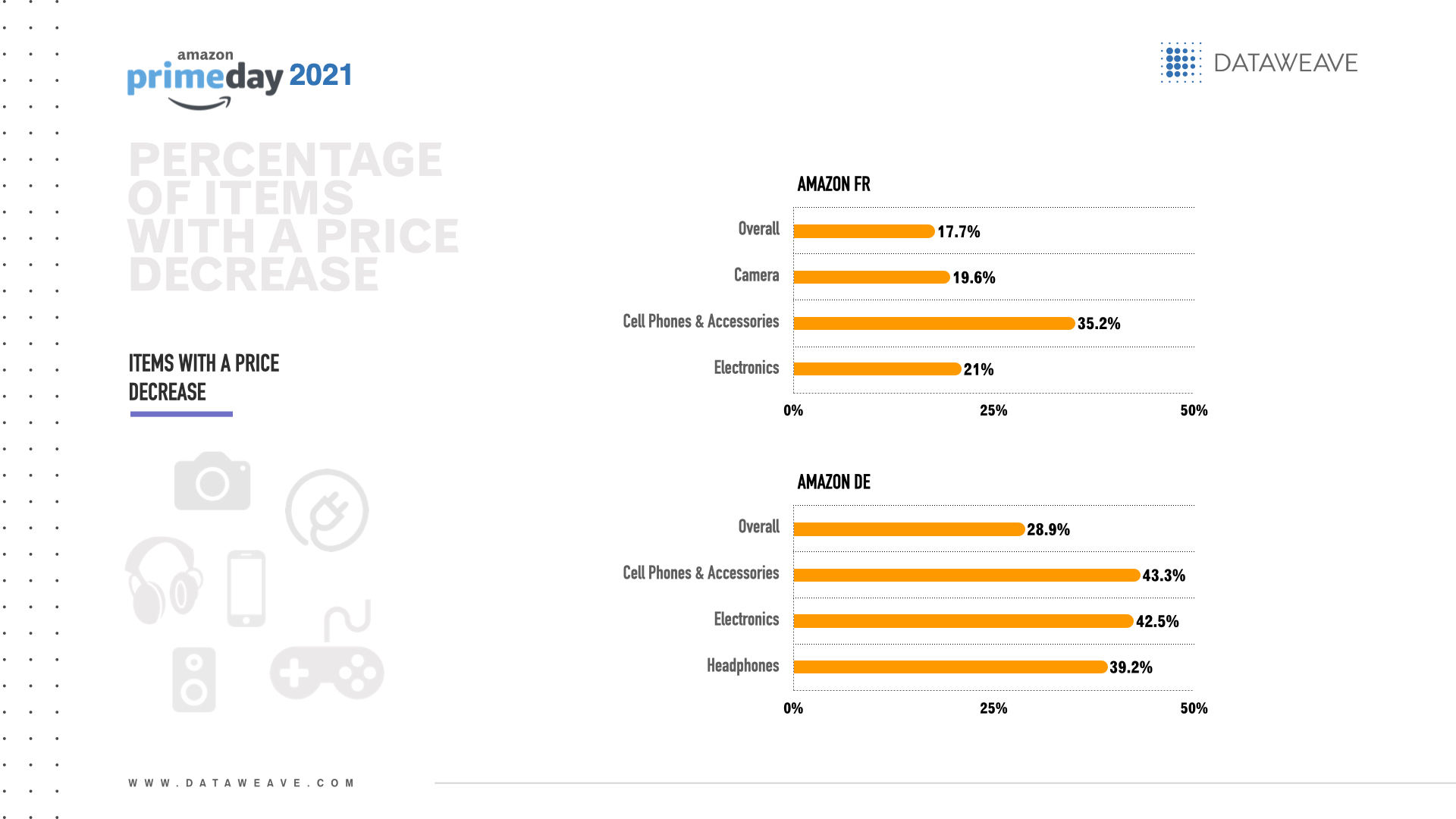

In Europe, Amazon Germany had the overall highest percentage of items with a price decrease for Prime Day (28.9%).

Electronics subcategories with the highest percentage of items with a price decrease per European retailer were:

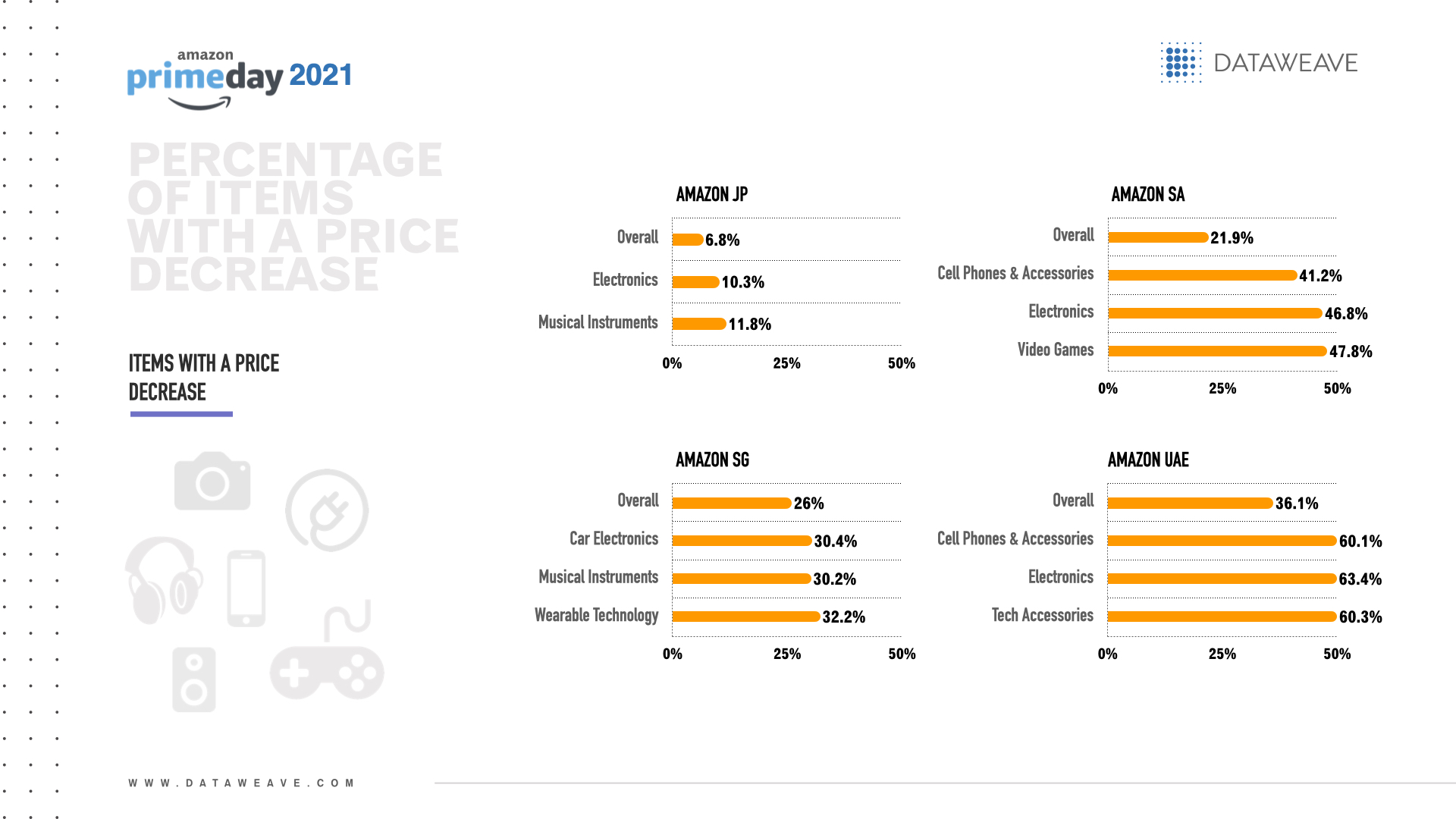

Across the Middle East & Asia, Amazon UAE had the overall highest percentage of items with a price decrease for Prime Day (36.1%).

Electronics subcategories with the highest percentage of items with a price decrease per retailer were:

• Amazon Saudi Arabia: Video games (47.8%), electronics (46.8%) and cell phones & accessories (41.2%) • Amazon UAE: Electronics (63.4%), tech accessories (60.3%) and cell phones & accessories (60.1%) • Amazon Japan: TV & video (14.9%), musical instruments (11.8%) and electronics (10.3%) • Amazon Singapore: Wearables (32.2%), car electronics (30.4%) and musical instruments (30.2%)

Magnitude of price decrease

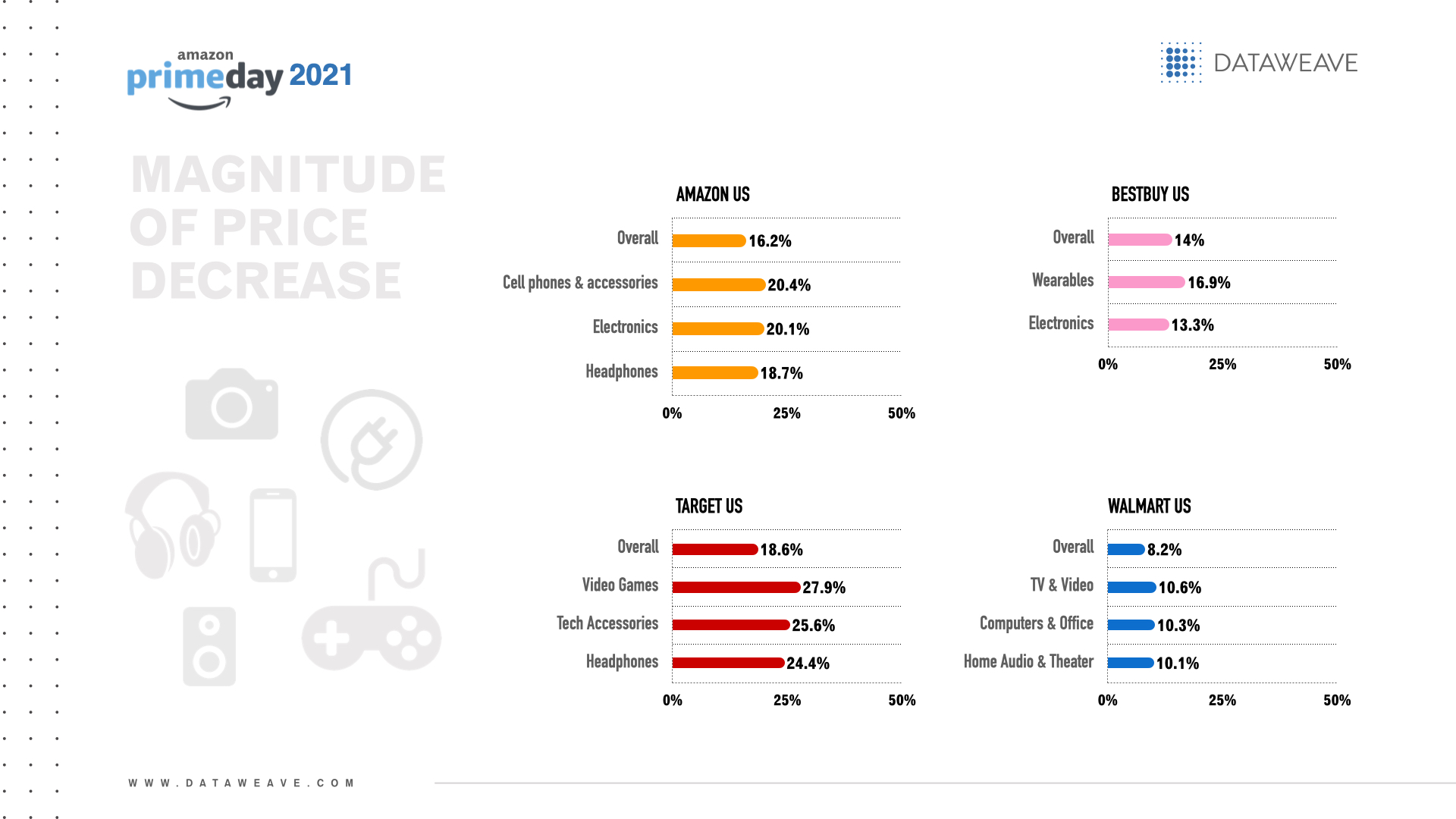

The US retailer with the greatest overall magnitude of price decrease for Prime Day was Target (18.6%).

The electronics subcategories with the greatest magnitude of price decrease per US retailer were:

• Amazon US: Cell phones & accessories (20.4%), electronics (20.1%) and headphones (18.7%) • Best Buy: Wearables (16.9%) and electronics (13.3%) • Target: Video games (27.9%), tech accessories (25.6%) and headphones (24.4%) • Walmart: TV & video (10.6%), computers & office (10.3%) and home audio & theater (10.1%)

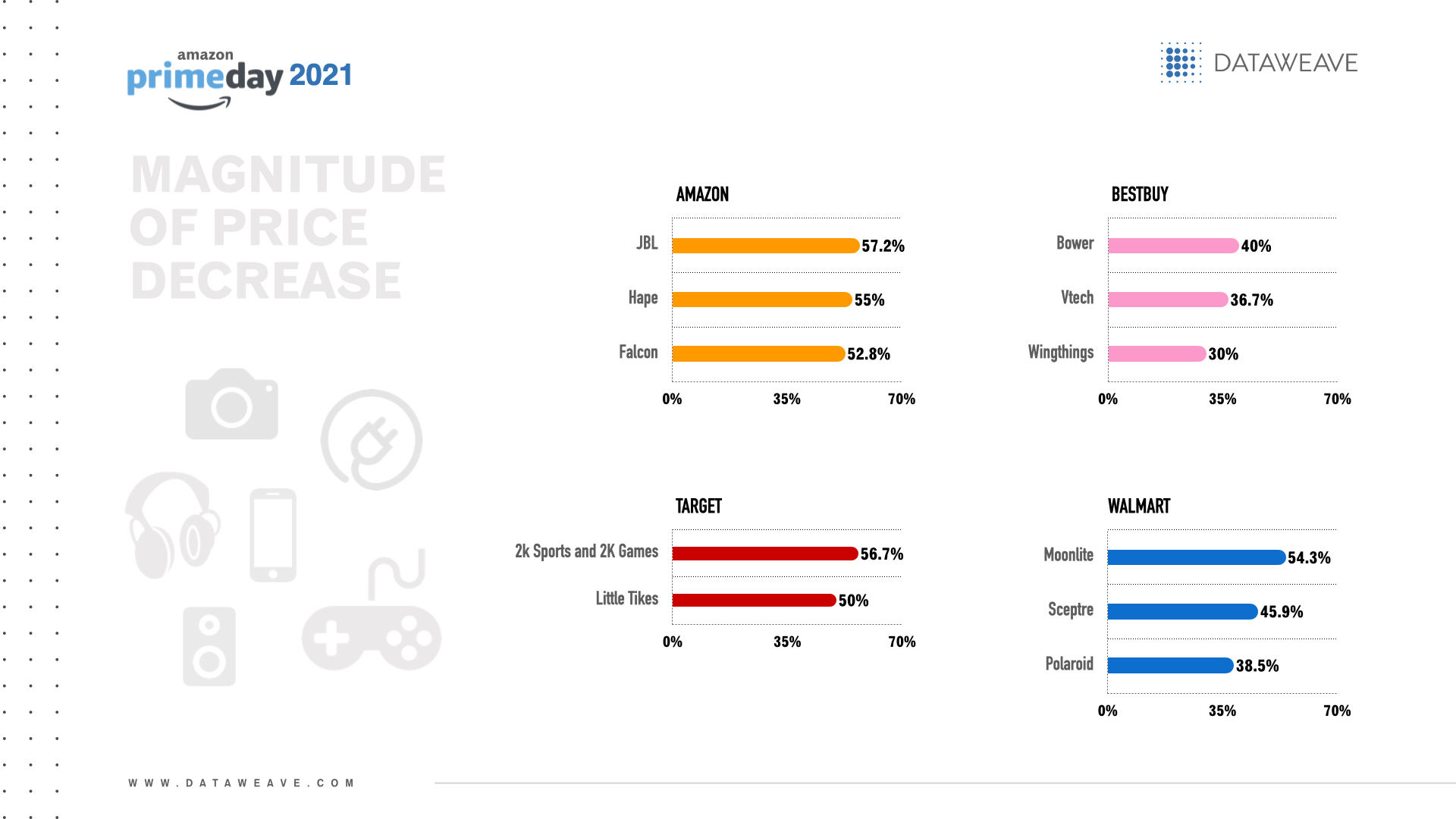

Brands with the greatest magnitude of price decreases per US retailer included:

• Amazon US: JBL (57.2%), Hape (55.0%) and Falcon (52.8%) • Best Buy: Bower (40.0%), Vtech (36.7%) and Wingthings (30.0%) • Target: 2k Sports and 2K Games (both 56.7%), Little Tikes (50.0%) • Walmart: Moonlite (54.3%), Sceptre (45.9%) and Polaroid (38.5%)

The UK retailer with the greatest overall magnitude of price decrease for Prime Day was OnBuy (22.1%).

The electronics subcategories with the greatest magnitude of price decrease per UK retailer were:

• Amazon UK: Home audio & theater (28.4%), electronics (21.7%) and cell phones & accessories (20.1%) • Ebay: TV & video (19.5%), wearables (18.7%) and computer & office (16.6%) • Etsy: Electronics (14.8%) • OnBuy: Cell phones & accessories (22.3%) and wearables (5.9%)

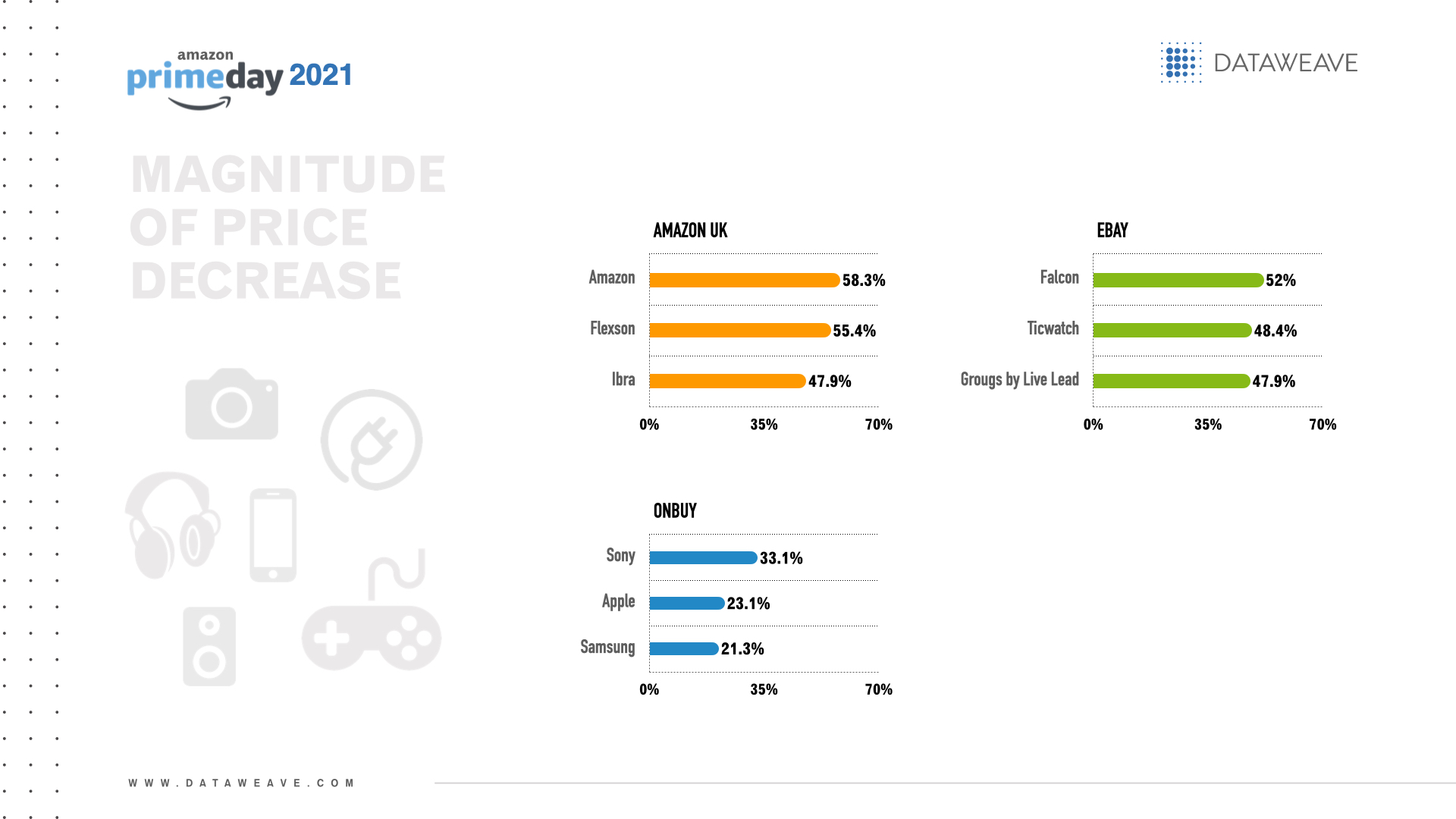

Brands with the greatest magnitude of price decreases across electronics categories per UK retailer included:

• Amazon UK: Amazon (58.3% for both cell phones & accessories and headphones), Flexson (55.4%) and Ibra (47.9% for both cameras and TV & video) • Ebay: Falcon (52.0%), Ticwatch (48.4%) and Grougs by Live Lead (47.9%) • OnBuy: Sony (33.1%), Apple (23.1%) and Samsung (21.3%)

Among European retailers, Amazon Italy offered the greatest overall magnitude of price decrease for Prime Day (18.9%) among a total of 66 products.

The electronics subcategories with the greatest magnitude of price decrease per European retailer were:

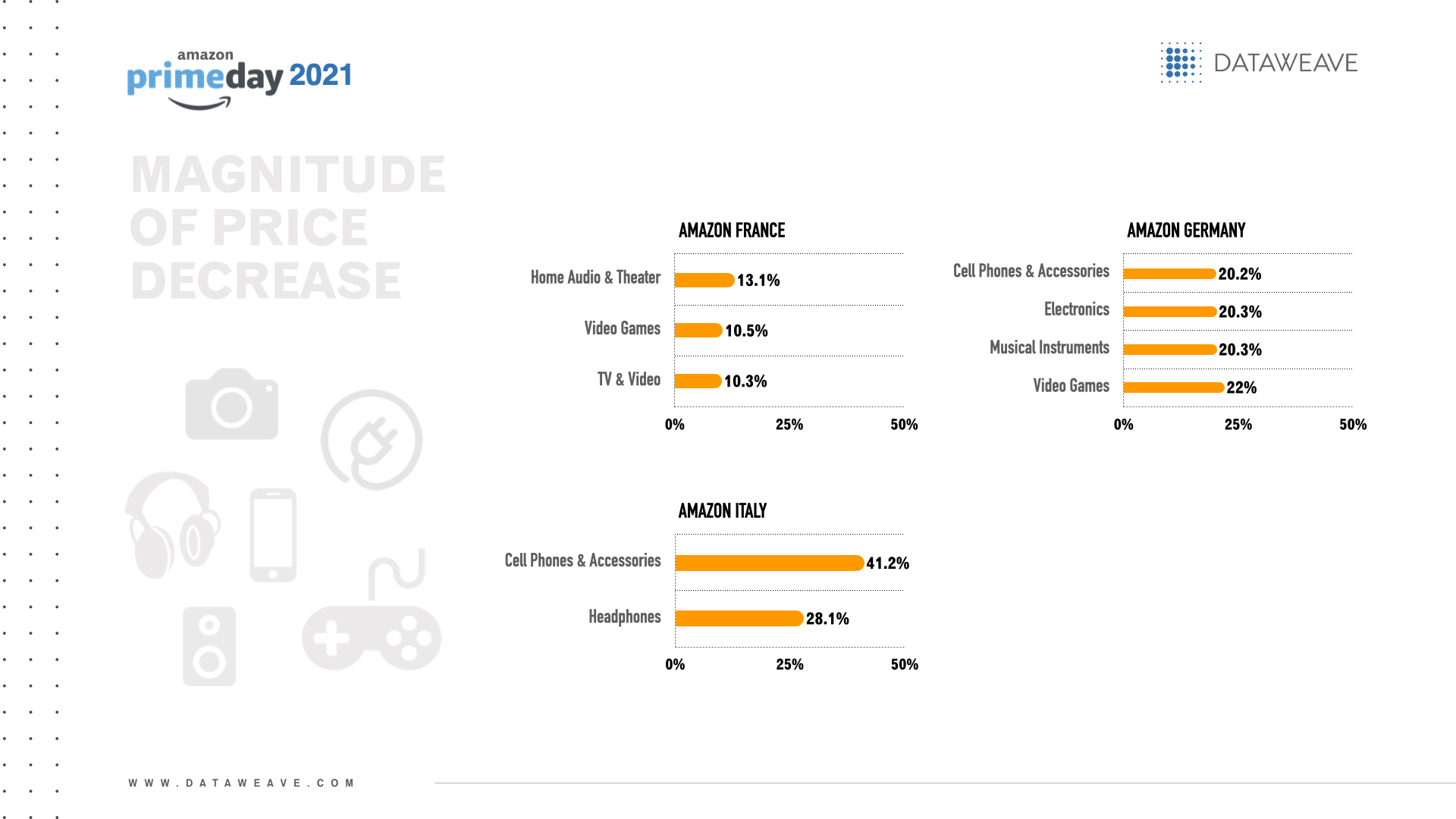

• Amazon France: Home audio & theater (13.1%), video games (10.5%) and TV & video (10.3%) • Amazon Germany: Video games (22.0%), electronics and musical instruments (both 20.3%) and cell phones & accessories (20.2%) • Amazon Italy: Cell phones & accessories (41.2%) and headphones (28.1%)

Brands with the greatest magnitude of price decreases per European retailer included:

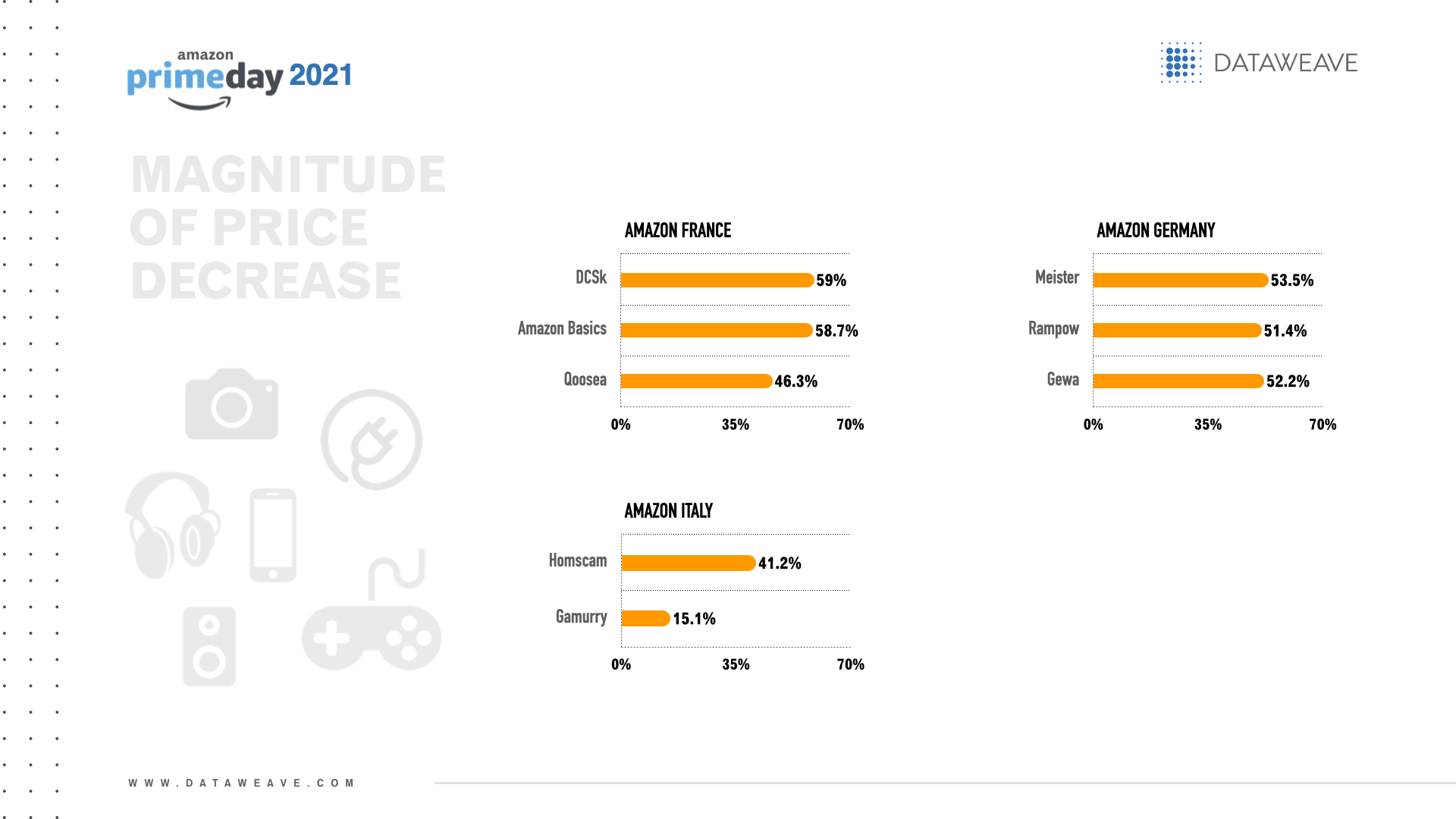

• Amazon France: DCSk (59.0%), Amazon Basics (58.7%) and Qoosea (46.3%) • Amazon Germany: Meister (53.5%), Rampow (51.4%) and Gewa (51.1%) • Amazon Italy: Homscam (41.2%) and Gamurry (15.1)

Across the Middle East and Asia, Amazon Japan offered the greatest overall magnitude of price decrease for Prime Day (11.9%) among a total of 66 products.

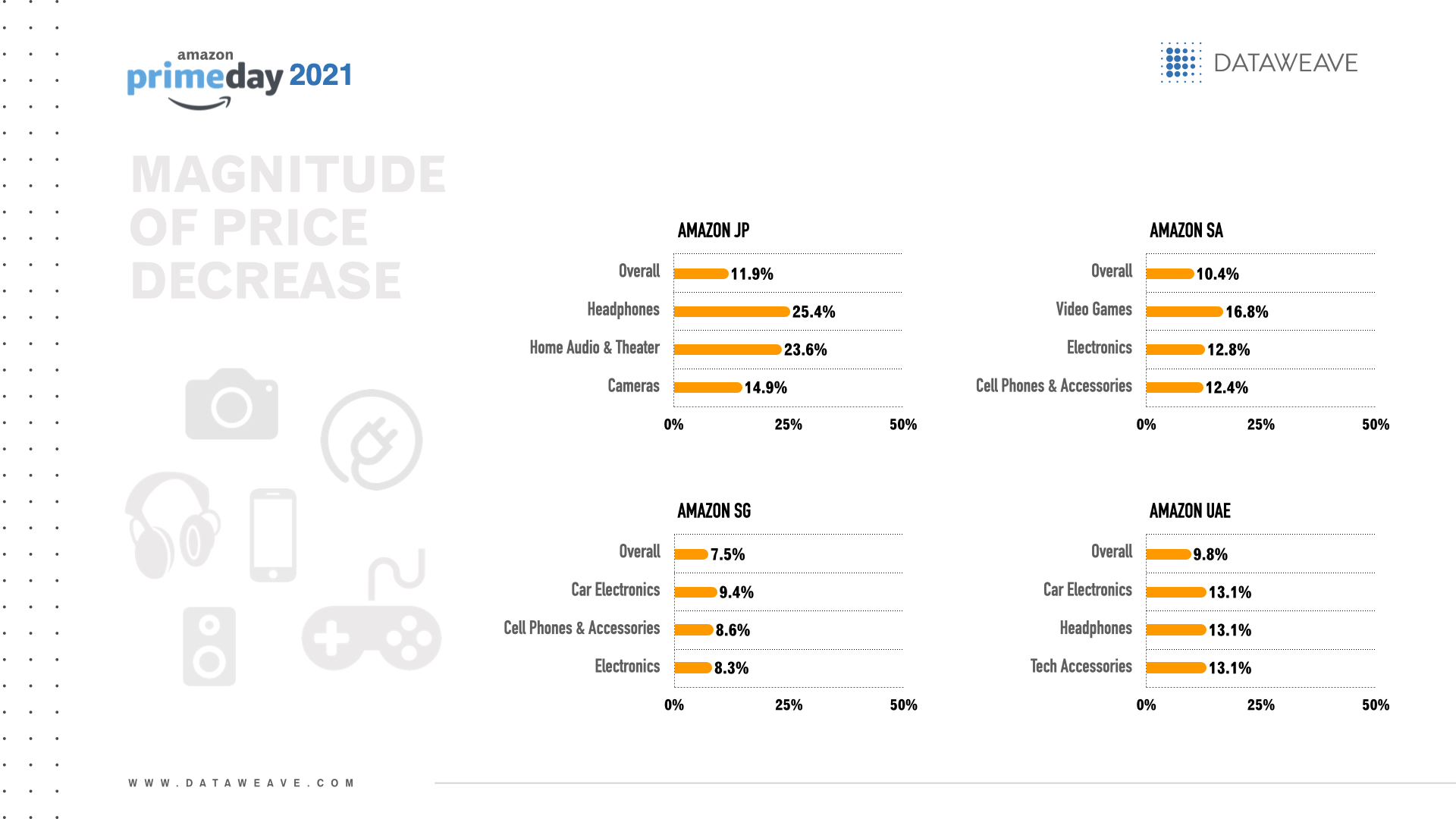

The electronics subcategories with the greatest magnitude of price decrease per retailer were:

• Amazon Saudi Arabia: Video games (16.8%), electronics (12.8%) and cell phones & accessories (12.4%) • Amazon UAE: Car electronics, headphones and tech accessories (all 13.1%) • Amazon Japan: Headphones (25.4%), home audio & theater (23.6%) and cameras (14.9%) • Amazon Singapore: Car electronics (9.4%), cell phones & accessories (8.6%) and electronics (8.3%)

Brands with the greatest magnitude of price decreases per retailer in the Middle East and Asia included:

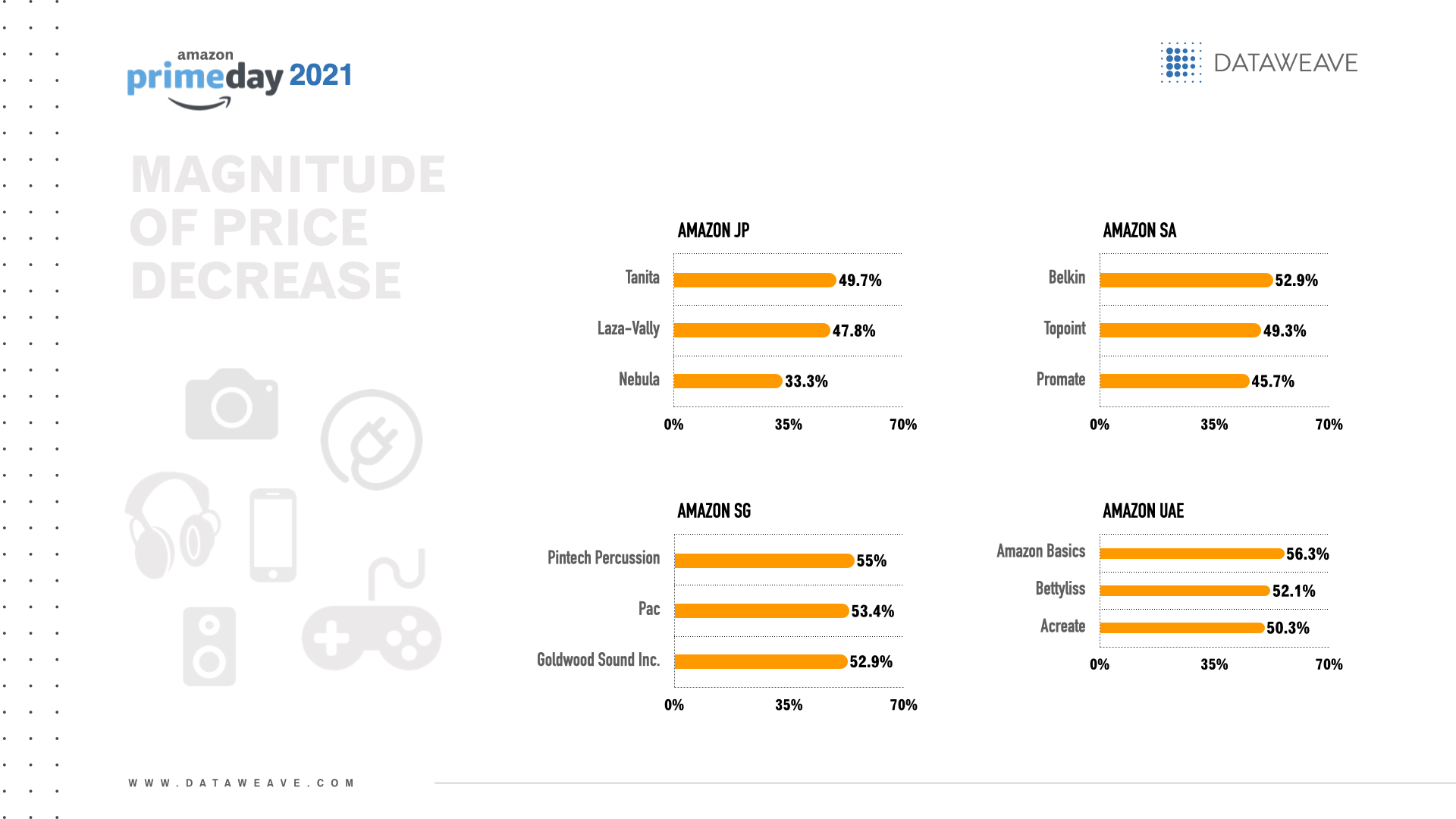

• Amazon Saudi Arabia: Belkin (52.9%), Topoint (49.3%) and Promate (45.7%) • Amazon UAE: Amazon Basics (56.3%), Bettyliss (52.1%) and Acreate (50.3%) • Amazon Japan: タニタ(Tanita) (49.7%), Laza-Vally (47.8%) and Nebula (33.3%) • Amazon Singapore: Pintech Percussion (55.0%), Pac (53.4%) and Goldwood Sound Inc. (52.9%)

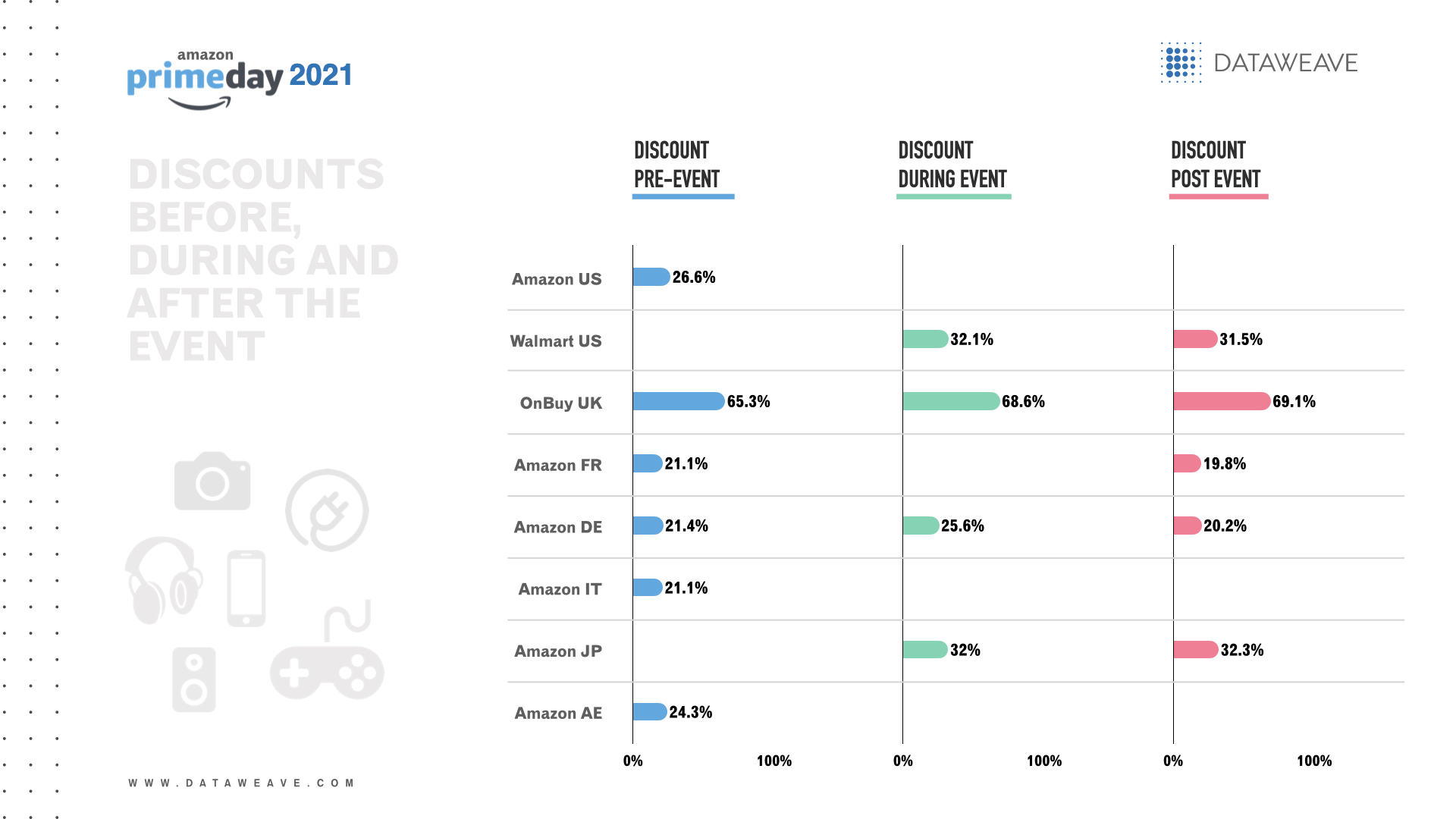

Discounts before, during and after the event

The US retailer with the biggest overall electronics discount before Prime Day was Amazon US (26.6%). Amazon’s biggest discounts were on home audio & theater (30.5%), TV & video (29.1%) and cell phones & accessories (28.6%).

Walmart offered the biggest discounts during (32.1%) and after (31.5%) the event. During the event, Walmart’s biggest discounts were on cell phones & accessories (46.3%), home audio & theater (35.5%) and computers & office (31.0%). Similarly, after the event, Walmart’s biggest discounts were on cell phones & accessories (45.8%), home audio & theater (35.3%) and computers & office (30.8%).

OnBuy was the UK retailer with the biggest overall electronics discount before (65.3%), during (68.6%) and after (69.1%) Prime Day with a product count of 237. OnBuy’s biggest discounts were on cameras (69.5% before, during and after the sales event), cell phones & accessories (rising from 67.6% before the sales event to 71.6% during and 71.8% after the event) and wearables (65.2% before and after the event yet 35.5% during Prime Day).

In Europe, Amazon Germany offered the biggest overall electronics discount before (21.4%), during (25.6%) and after (20.2%) Prime Day. Amazon France and Amazon Italy also offered comparable overall discounts (21.1%) before Prime Day.

In the pre-sales event, Amazon Germany gave the most generous discounts on cameras (34.1%), wearables (24.7%) and headphones (24.3%). During Prime Day, Amazon Germany offered the biggest discounts on video games (30.7%), headphones (30.1%) and electronics (28.3%). After Prime Day, Amazon Germany offered the biggest discounts on headphones (24.2%) electronics (22.6%) and cell phones & accessories (22.1%).

Across retailers in the Middle East & Asia, Amazon UAE offered the biggest overall electronics discount before Prime Day (24.3%), whereas Amazon Japan offered the biggest discount during (32.0%) and after (32.3%) Prime Day.

In the pre-sales event, Amazon UAE offered the most generous discounts on TV & video (31.3%), musical instruments (31.0%) and headphones (25.4%). During and after Prime Day, Amazon Japan offered the biggest discounts on Bluetooth & wireless speakers and electronics (both 99.0%).

Popularity

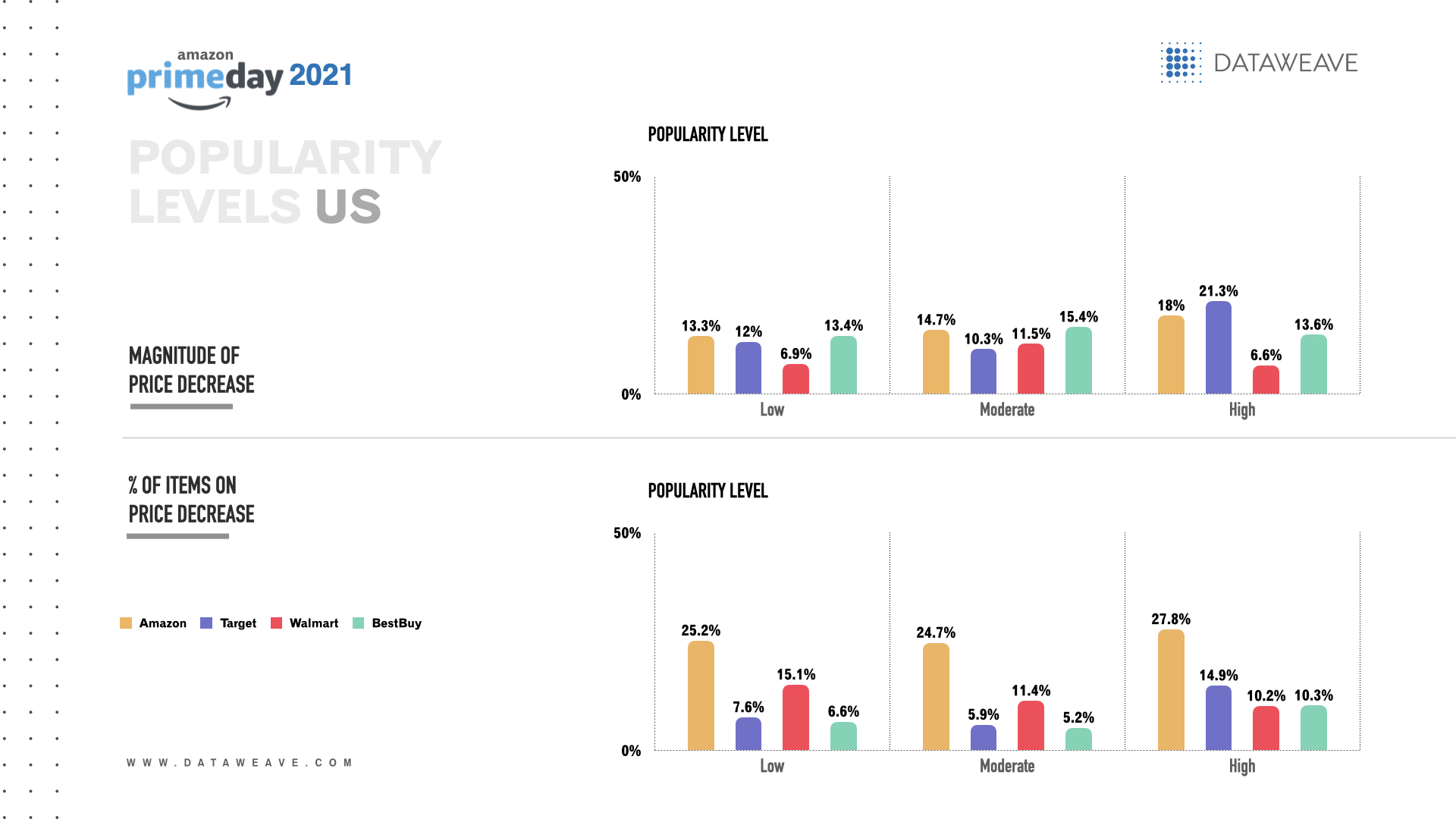

In the US, among electronics with high popularity, Amazon US offered the highest percentage of items with a price decrease (27.8%) and Target offered the greatest magnitude of price decrease (21.3%).

For electronics with moderate popularity, Amazon US offered the highest percentage of items with a price decrease (24.7%) and Best Buy offered the greatest magnitude of price decrease (15.4%).

Among electronics with low popularity, Amazon US offered the highest percentage of items with a price decrease (25.2%) and Best Buy offered the greatest magnitude of price decrease (13.4%), closely followed by Amazon US (13.3%).

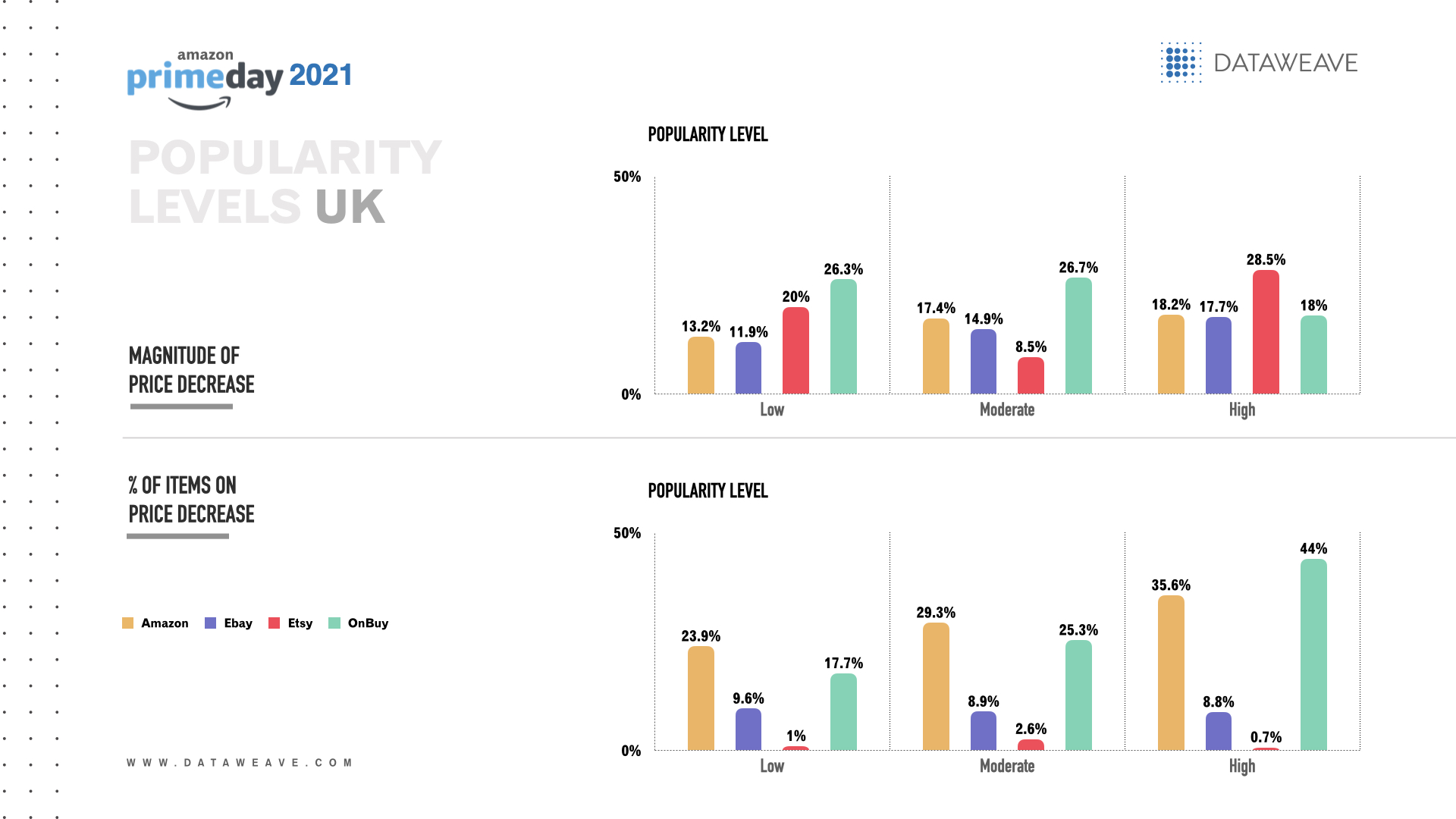

In the UK, among electronics with high popularity, OnBuy offered the highest percentage of items with a price decrease (44.0%) among 84 products and Etsy offered the greatest magnitude of price decrease (28.5%) among 150 products.

For electronics with moderate popularity, Amazon UK offered the highest percentage of items with a price decrease (29.3%) and OnBuy offered the greatest magnitude of price decrease (26.7%).

Electronics with low popularity, Amazon UK offered the highest percentage of items with a price decrease (23.9%) and OnBuy offered the greatest magnitude of price decrease (26.3%).

In Europe, among electronics with high popularity, Amazon Germany offered the highest overall percentage of items with a price decrease (30.1%) and the greatest overall magnitude of price decrease (20.2%).

For electronics with moderate popularity, Amazon Germany offered the highest percentage of items with a price decrease (29.7%) and Amazon Italy offered the greatest magnitude of price decrease (41.2%) among 12 products.

Among electronics with low popularity, Amazon Germany offered the highest percentage of items with a price decrease (26.7%) and the greatest magnitude of price decrease (17.2%).

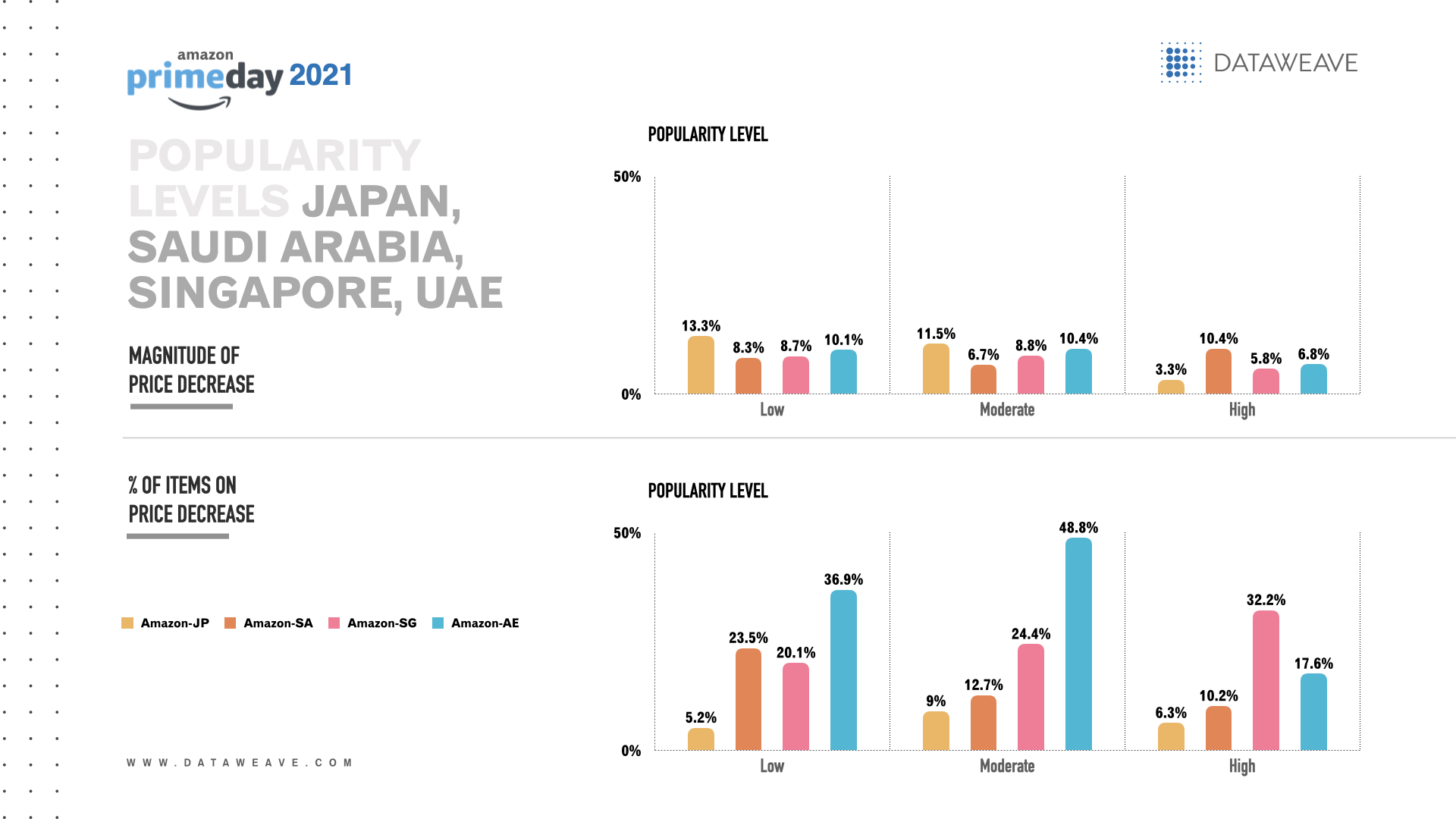

In Middle East & Asia, among electronics with high popularity, Amazon Singapore offered the highest overall percentage of items with a price decrease (32.2%) and Amazon Saudi Arabia had the greatest overall magnitude of price decrease (10.4%).

For electronics with moderate popularity, Amazon UAE offered the highest percentage of items with a price decrease (48.8%) and Amazon Japan offered the greatest magnitude of price decrease (11.5%).

Similarly, among electronics with low popularity, Amazon UAE offered the highest percentage of items with a price decrease (36.9%) and Amazon Japan the greatest magnitude of price decrease (13.3%).

Consumers won big on Prime Day 2021

Overall, Prime Day 2021 offered a wide range of deals across the competitive electronics category in each region. Almost all of the retailers we studied (except for Ebay) showed up in the analysis for offering notable discounts and pricing strategies this year. Amazon US, OnBuy, Amazon Germany, Amazon Japan and Amazon UAE appeared in the results most often among their respective regions. Stay tuned for Prime Day 2021 pricing insights across other categories, including home, health & beauty and fashion.

This year, shoppers will skip neckties and celebrate Dad with gifts for his home office or man cave. As our personal and professional lives grow increasingly digital and tied to our homes, retailers face new seasonal sales opportunities.Retailers whose assortments contain in-demand electronics and home products can drive more e-commerce sales revenue and gain a competitive edge in time for Father’s Day 2021.

According to the NRF, Father’s Day spending is expected to hit $20.1 billion, up 18% from 2020’s total of $17 billion. The vast majority (75%) of Americans plan to celebrate the fathers, husbands and other paternal figures in their life this Father’s Day. Popular products dads will love

Retailers can inspire Father’s Day shoppers by filling their assortments with in-demand electronics and home products, as these two categories continue to boom.

Consider these recent results related to electronics and home goods:

Online sales of consumer electronics grew 18% year-over-year in 2020 as more consumers work, shop and enjoy entertainment in the comfort of their homes.

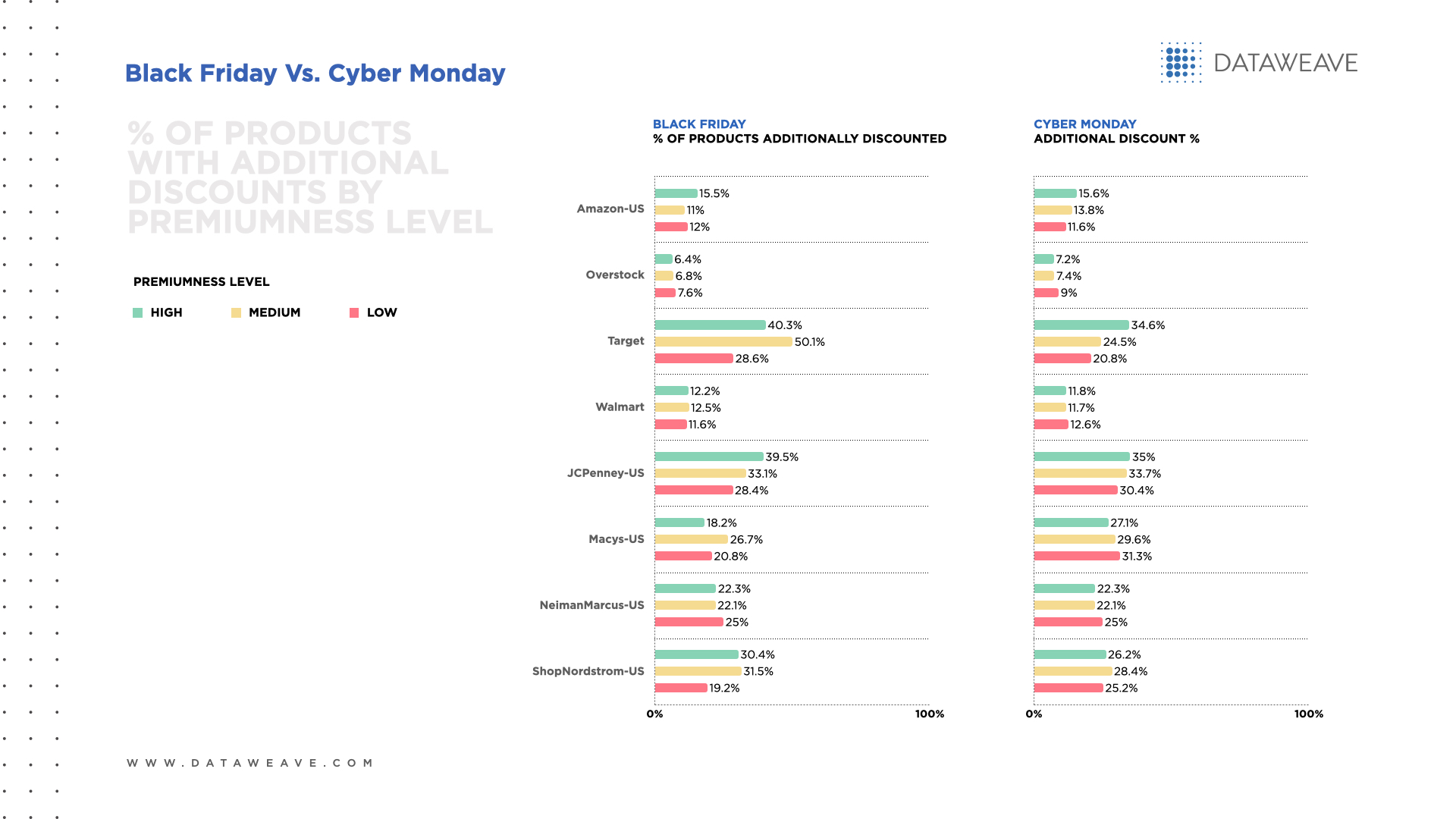

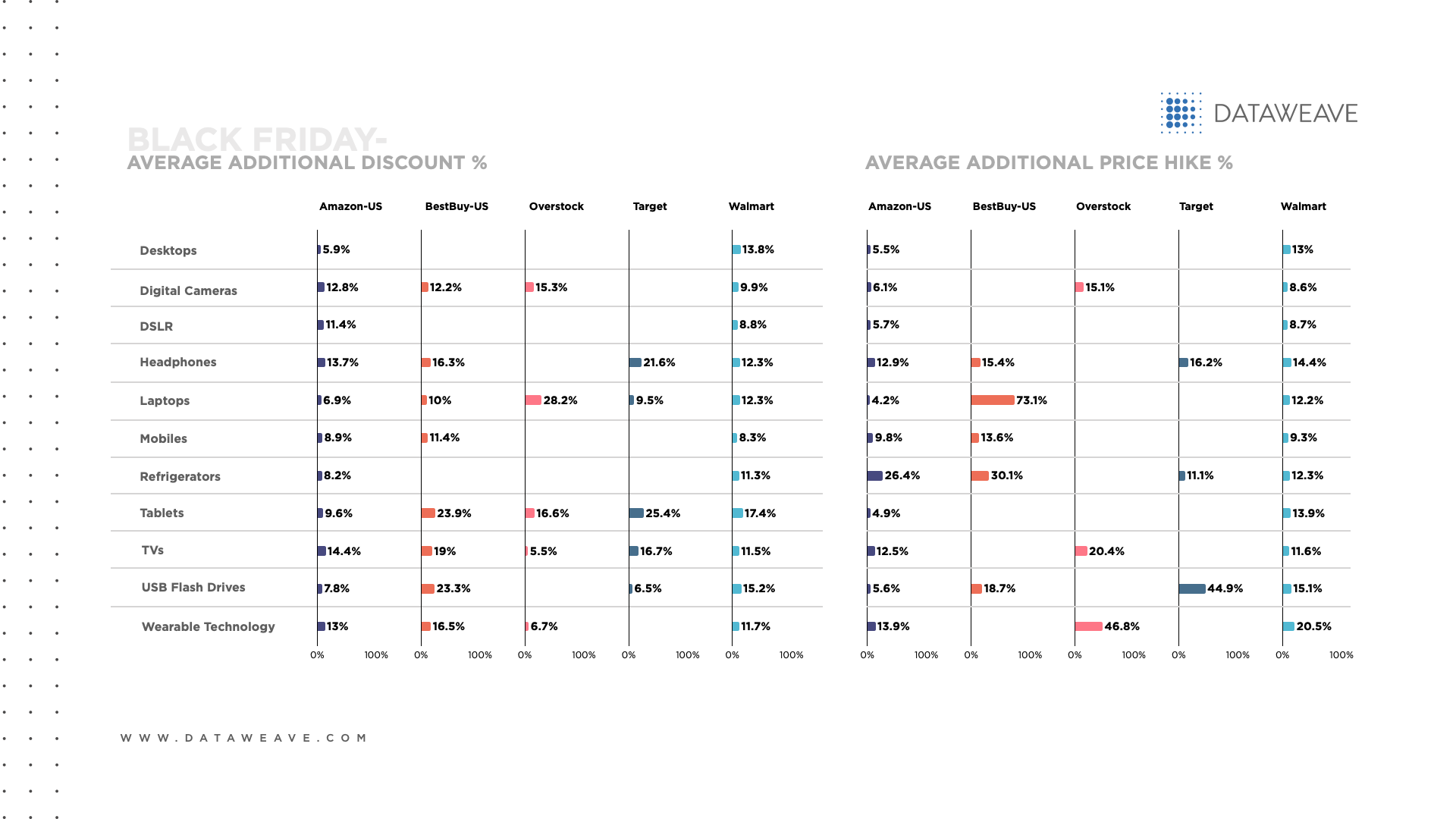

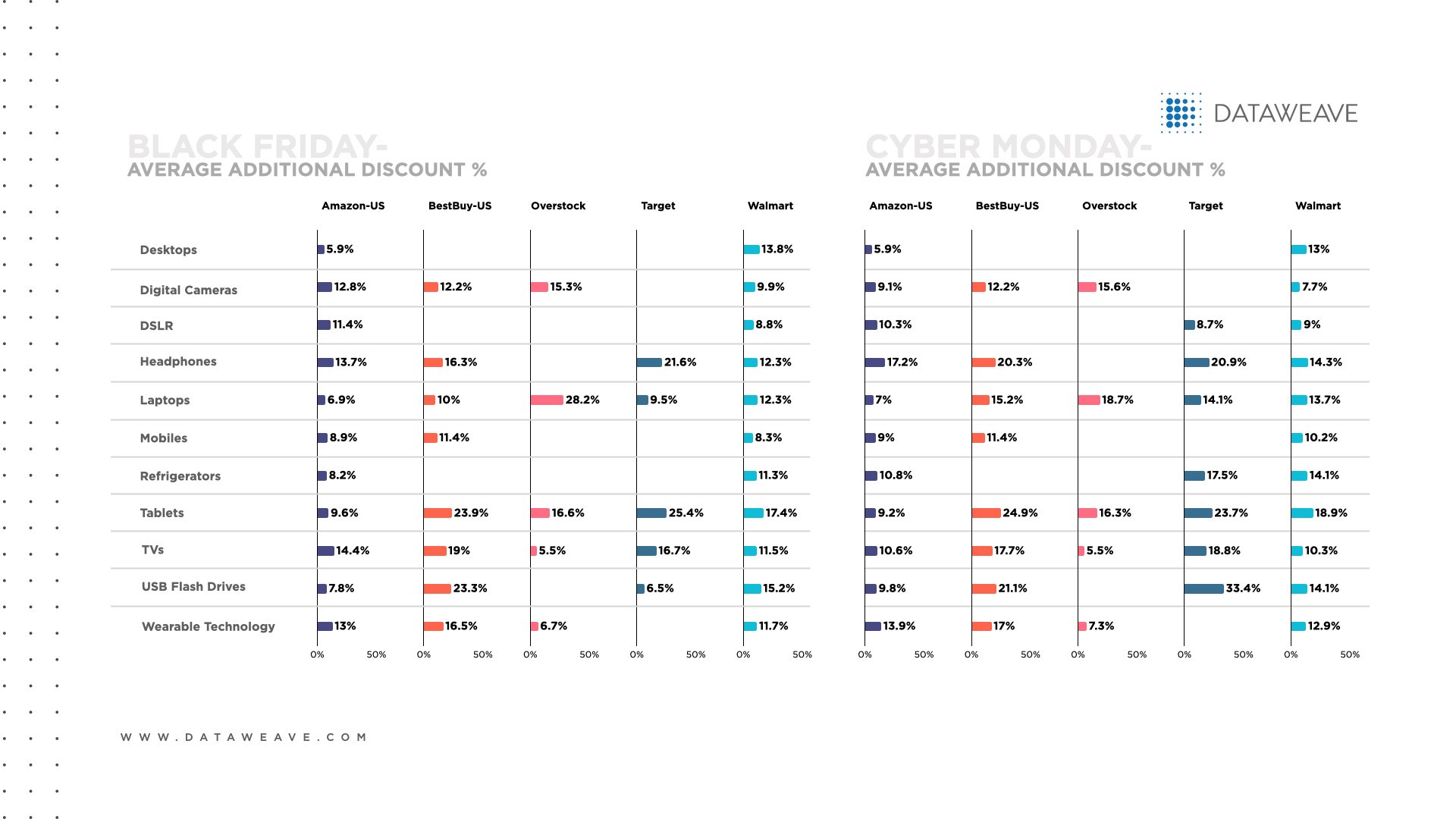

To win more sales on Black Friday 2020, certain retailers offered attractive deals and deep discounts on electronics like laptops, mobiles, wearables, USB flash drives, tablets and headphones.

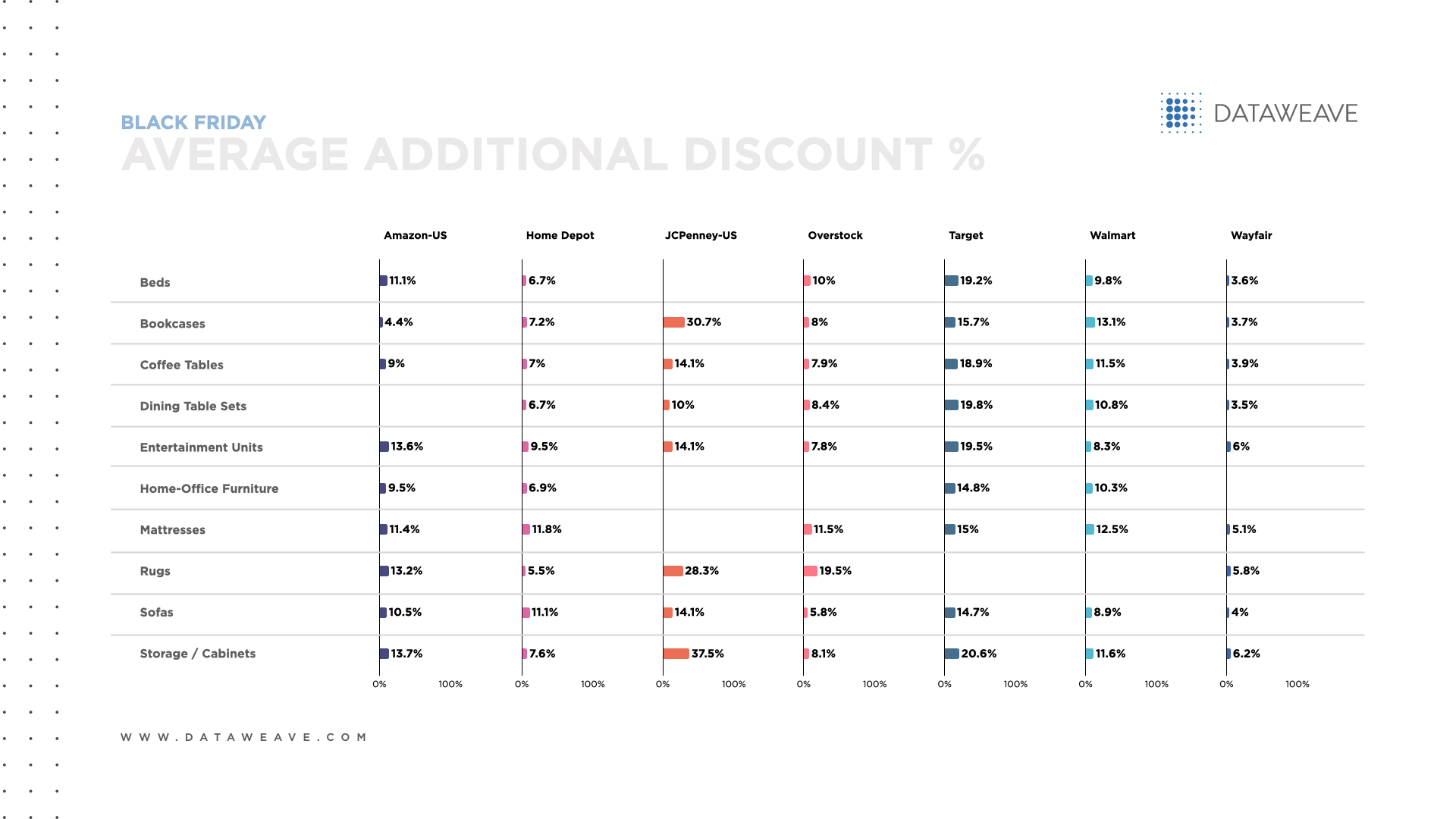

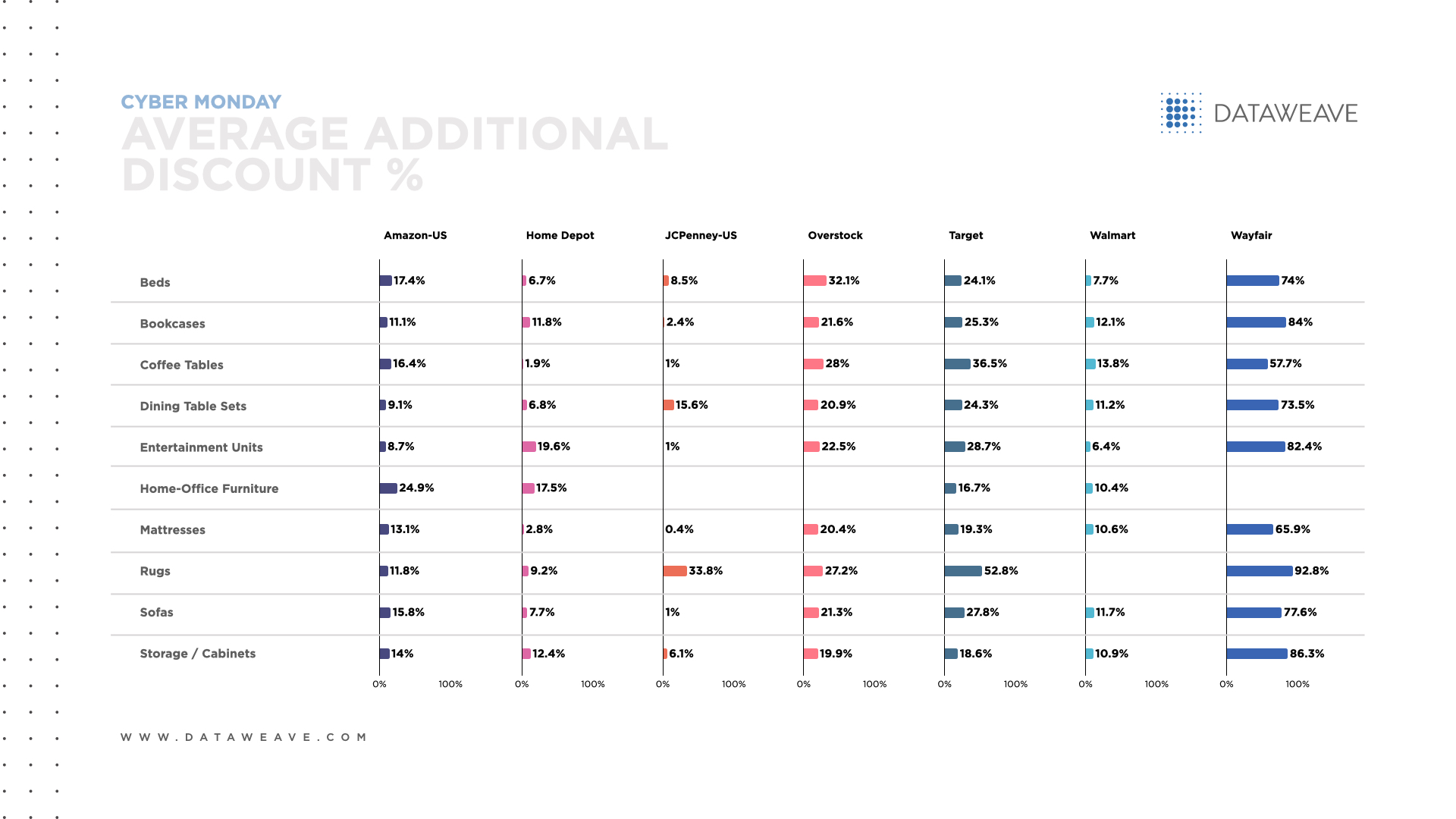

Home furnishings sales rose 12% year-over-year in 2020 as homebound consumers invested in products for domestic comfort, organization and functional purposes.

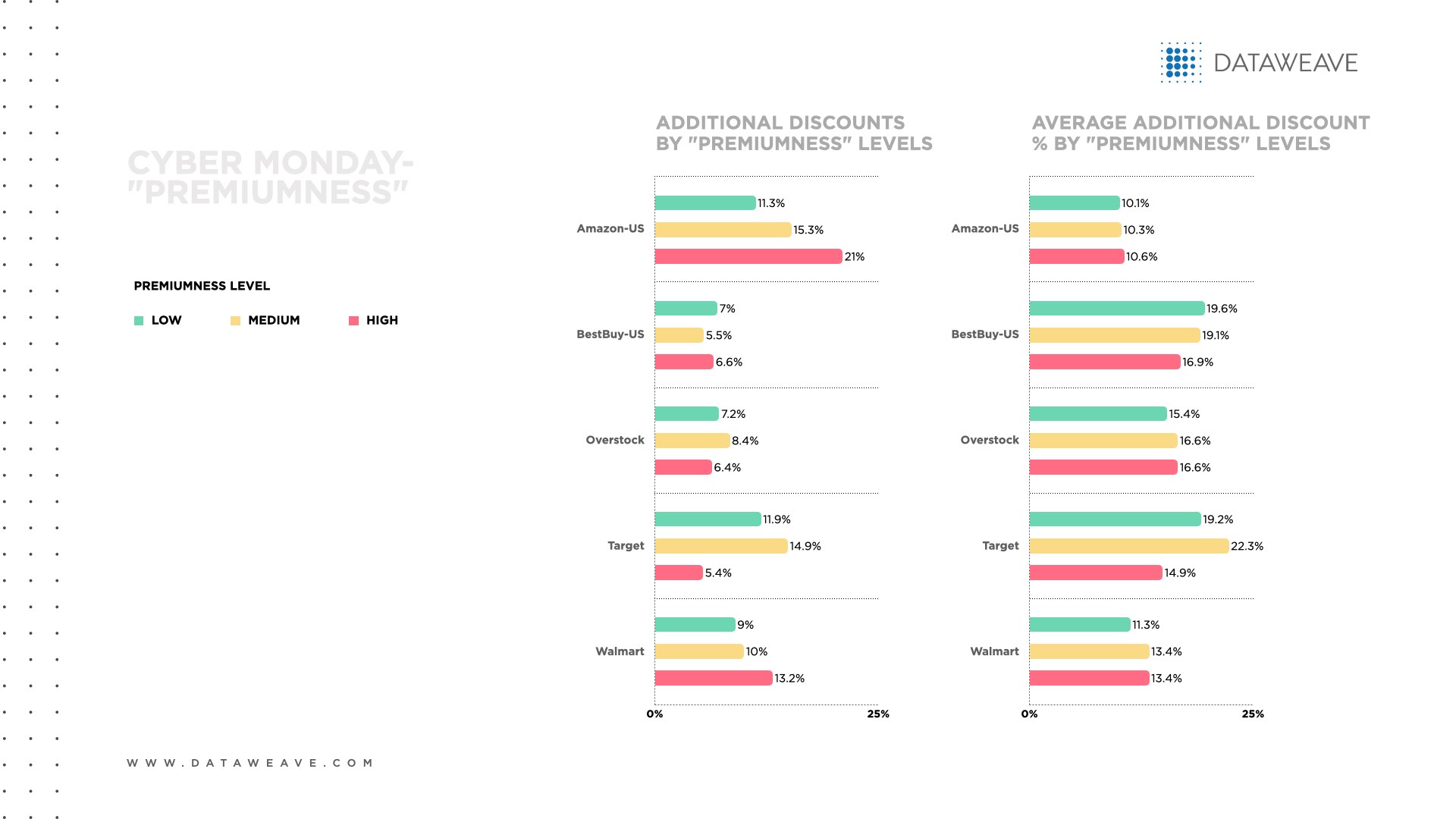

On Cyber Monday 2020, home merchandise saw bustling sales, as storage items, cabinets and bookcases were among the most competitively priced products in the category.

Since home is the new hub, retailers can plan their assortments to align with this enduring consumer trend to outplay rivals. Optimizing their product mix involves making decisions on the right balance among bestsellers, hot trends, unique products and essential items to gain a competitive advantage.

Grab shoppers’ attention with desirable promotions

Although shoppers appreciate variety, the abundance of product choices available online can overwhelm consumers. In response, retailers can craft persuasive and timely digital campaigns to help simplify the customer experience.

Digital promotions, including banner ads and search campaigns, can help retailers spark a sense of urgency that motivates shoppers to buy. The key is for retailers to connect to consumers with the right messaging, timing and targeting to earn their attention, trust and sales. Retailers need effective promotions to optimize their ad spend. Pricing secures the sale

To maximize top line performance, retailers also need to nail their Father’s Day pricing strategies.

Notably, consumption habits and loyalty have dramatically shifted during the pandemic, which has affected retailers’ pricing strategies. Value pricing continues to soar due to economic uncertainty, job losses and a growing desire for value for money. Last year, 30% of consumers switched to a new brand due to better prices, while 25% cited better value as the reason they switched, according to McKinsey & Company.

On the other side of the socioeconomic spectrum, premium pricing is also on the rise. Upscale shoppers are now more willing to splurge on high quality goods, including home furnishings and electronics. These consumers will pay more for merchandise that adds value or purpose to their lives. In addition, digitally-savvy Gen Z and Millennial consumers are spending 125% as much as they did in 2019. As a result, retailers that capitalize on consumers’ enthusiasm and price elasticity will drive incremental e-commerce revenue gains.

As e-commerce competition intensifies and informed, empowered shoppers know where to find the best prices, more retailers now seek a new pricing approach to stand out, drive sales growth and protect against price wars. Drive revenue with the right products, promotions and prices

To win the attention and sales of Father’s Day shoppers, more leading retailers now use data insights to make faster, more effective assortment and pricing decisions that maximize their e-commerce sales.

Data analytics help retailers know which products consumers will actually buy. Leading global retailers rely on Assortment Analytics from DataWeave to ensure their online assortments keep up with evolving consumer needs. Building acompetitive product mix can set retailers apart and boost e-commerce sales by offering in-demand merchandise. Assortment analytics give retailers insights on the most popular brands and products on any e-commerce website, and help them spot and fill any assortment gaps to capture more sales.

To captivate online shoppers’ attention, retailers use DataWeave’s Promotional Insights to lower acquisition costs with marketing promotions that resonate. As online shoppers increasingly seek timely offers, these insights help retailers quickly evaluate the effectiveness of their promotions and optimize their digital ad spend. Retailers gain near-real-time insights on the brands, categories and products their rivals promote, including campaign frequency, duration and messaging for promotions that convert.

Major retailers also turn to Pricing Intelligence from DataWeave to promptly adapt to rivals’ online price changes and shifts in consumer demand. Retailers drive more revenue and margin by easily identifying fluctuations in consumer demand and rivals’ pricing, as well as any gaps. Retailers gain an edge by seeing pricing patterns that their rivals miss. They gain accurate exact and similar product matching, and near real-time pricing updates to stay competitive and fuel e-commerce conversions. Data insights help retailers delight dads

This Father’s Day, retailers can apply data insights to offer consumers eye-catching promotions of in-demand electronics and home products at the right price to wow dads. Insights from DataWeave can help retailers make smart, competitive assortment, promotion and pricing decisions that boost agility, improve the customer experience and drive e-commerce sales for this special occasion – and all year long.

The pandemic’s profound economic impact sparked a surge in value shopping.

Between February and December 2020, 10 million Americans lost their jobs.1 Due to the pandemic, 36% of lower-income adults and 28% of middle-income adults lost a job or took a pay cut (vs. 22% of upper-income adults). In addition, less than a quarter of lower-income adults have three months’ worth of emergency funds (vs. 48% of middle-income adults and 75% of upper-income adults).2

These financial shifts matter to retailers, as lower- and middle-income households account for 81% (29% and 52%, respectively) of the total U.S. population.3 Reduced disposable income among households like these has led more consumers to embrace bargain-hunting as a shopping habit.

We’ll see why price sensitive consumers are influencing retailers to adjust their e-commerce pricing strategies to stay competitive and responsive.

Consumers seek value across retail categories

Recent research shows 50% of U.S. adults are more sensitive to product prices now than before the pandemic. Also, 80% of U.S. shoppers are taking at least one action to seek more value when they shop for groceries, prioritizing value for money over speed.4

According to McKinsey, 65% of consumers cited value as one of their top three reasons they switched brands during the pandemic. Also, 40% of shoppers cited a desire for better value and 38% cited better prices or promotions as reasons for choosing new products.5

Value-oriented pricing influences purchases, as 70% of consumers said product discounts are more important today compared to a year ago. In addition, 54% ofconsumers said better online deals and discounts are a leading factor that persuades them to choose a specific retailer.6

As e-commerce explodes, consumers have greater access to information. They can find the best price across online sites and receive notifications when a product’s price drops before they buy. Retailers face intense pricing pressure

Similar to the aftermath of the 2008 recession, discounters and dollar chain retailers are now thriving as consumers seek superior value for money. Consumers need new products yet they no longer want to spend as much as before.

That’s why bargain retail is poised to be among the biggest winners in 2021 as consumers get out and socialize more. 7

Dollar General continues to aggressively expand its omnichannel reach as value shopping soars.8 To stay competitive, Family Dollar has partnered with Instacart on same-day delivery.9 In the fierce grocery sector, hard discounter Aldi’s omnichannel expansion includes a focus on private labels and efficient operational processes that improve cost effectiveness and competitive pricing.10

Across retail categories,a remarkable 50 million price changes take place online every day.Given consumers’ shift to value shopping, more retailers are changing their pricing to offer discounts both online and in-store.11 However, to avoid costly price wars, more retailers are now taking a renewed approach to their pricing strategies to protect their margins as they compete.

Specifically, to optimize their e-commerce business for profitable growth, more retailers are modernizing their pricing strategies with data insights.

Pricing intelligence is retailers’ secret weapon

As e-commerce rivalry heats up, retailers must evaluate pricing across more online websites to keep their own prices competitive. This process is becoming increasingly complex and time consuming. Meanwhile, retailers may consider adopting aggressive pricing tactics to win online sales. Yet this pricing strategy is unsustainable over the longer term, as it erodes profit margins.

Today’s heated e-commerce rivalry means retailers can no longer afford to guess at price points or use the same pricing tactics that relied on before the pandemic.

That’s why leading retailers turn to data insights for their pricing strategies to stay agile and flexible while rapidly adapting to fluctuations in consumer demand and competitors’ pricing.

Now more retailers turn to DataWeave’s Pricing Intelligence to drive more revenue and margin.

To optimize profit margins, retailers use our actionable insights to make pricing decisions according to data-driven recommendations. They also make decisions to protect their desired price perception.

Monitoring competitors’ pricing moves helps retailers benchmark their own performance, identify gaps and respond to market trends faster. They can also refer to historic pricing data analytics to accurately anticipate and counter rivals’ next moves to gain an edge.

Retailers that apply data insights to optimize their pricing can drive more online revenue by finding the ideal price consumers are willing to pay while still maintaining profitability. Pricing intelligence can make customer acquisition more efficient, and help retailers grow online sales and market share.

Amid greater price sensitivity, retailers’ pricing strategies are evolving to use data to adapt to consumers’ needs and drive e-commerce sales and profitability. DataWeave’s Pricing Intelligence gives retailers an edge so they stay agile and competitive, and maximize e-commerce sales across consumers of all economic levels.

1. Howland, Daphne. The middle class is stressed and the pandemic isn’t helping. Retail Dive. January 20, 2021. 2. Howland, Daphne. The middle class is stressed and the pandemic isn’t helping. Retail Dive. January 20, 2021. 3. Bennett, Jesse, Richard Fry and Rakesh Kochhar. Are you in the American middle class? Find out with our income calculator. Pew Research Center. July 23, 2020. 4. Maake, Katishi. DoorDash, Instacart Eye Launching Credit Cards. The Harris Poll. April 9, 2021. 5. Charm, Tamara, Harrison Gillis, Anne Grimmelt, Grace Hua, Kelsey Robinson and Ramiro Sanchez Caballero.Survey: US consumer sentiment during the coronavirus crisis. McKinsey & Company. May 13, 2021. 6. Berthiaume, Dan. Survey: Deals drive purchases during pandemic. Chain Store Age. March 18, 2021. 7. Thomas, Lauren. Beauty and bargain retail could be the biggest winners in 2021, Wells Fargo predicts. CNBC. March 25, 2021. 8. Unglesbee, Ben. Dollar General ramps up expansion of Popshelf concept. Retail Dive. March 19, 2021. 9. Ryan, Tom. Will same-day delivery pay off for dollar stores? RetailWire. February 8, 2021. 10. Anderson, George. Should Aldi’s growing store count and digital progress keep rivals up at night? RetailWire. February 11, 2021. 11. Berthiaume, Dan. Survey: Deals drive purchases during pandemic. Chain Store Age. March 18, 2021

Moms deserve a scrumptious celebration. In time for Mother’s Day, restaurants and their food delivery partners can unburden mothers from the chore of cooking by delivering the gifts of ease, convenience and nourishment.

Over the past year, moms have been starved for time amid the disruption of working from home and supporting their children’s virtual schooling. Meanwhile, grandmothers have been starved for social connection, as many of them have only seen their loved ones on Zoom.

Restaurants can satisfy consumers’ unmet needs. Using timely, empathetic digital marketing can help restaurant operators stand out on food delivery apps (like DoorDash, Uber Eats, Grubhub and Postmates) and sell more online this Mother’s Day – and all year round.

Delight moms with what they really want

According to the NRF,83% of consumers plan to celebrate Mother’s Day in 2021. On average, shoppers plan to spend $220.48 (up $16 since last year), the highest amount in the history of NRF’s Mother’s Day surveys. 1

Most (62%) moms say they would love to eliminate the chore of cooking on Mother’s Day. Dinner is the most important meal on Mother’s Day, and most moms prefer restaurant meals (53%) to home cooked meals (39%). 2

Given consumers’ willingness to spend and Mom’s appetite for restaurants, Mother’s Day 2021 is poised to be a powerful sales event for restaurants.

Restaurants need new ways to navigate market trends

The restaurant industry faces consolidation, as 17% (110,000) of U.S. restaurants permanently closed in 2020, and 87% of full-service restaurants reported an average 36% drop in revenue. 3 These figures prove restaurant operators need help to boost their top line and cut costs as they adapt to intense rivalry and shifting market conditions.

During the pandemic, many consumers have embraced home for health or financial reasons or a creative outlet. Although 55% of consumers have been eating at home more often since the pandemic began, 65% say they are tired of cooking at home. 4

Fortunately, consumers are in a celebratory mood. Last year, Mother’s Day was a top sales day, as consumer spending at restaurants soared 103% on Mother’s Day Sunday and 63% on Saturday. 5 Restaurants can relieve consumers of the chore of cooking and add variety to dining occasions like Mother’s Day.

Successful restaurants gain a digital data advantage

To satisfy consumers’ needs and outplay rivals, restaurants now turn to data analytics from DataWeave to protect their profitability with effective pricing, menu and promotion decisions.

Pricing analytics

Restaurant operators can optimize their pricing to stay competitive. For instance, restaurants can compare their offerings and delivery fees with those of rivals to pinpoint and fill any gaps. Monitoring rivals’ pricing moves also helps restaurant operators stay flexible by keeping their prices affordable, so they can attract online sales growth.

Menu analytics

To minimize costs, more restaurants are streamlining their menus. Menu analytics can help operators spot the optimal mix of bestselling items and emerging food trends, like plant-based, vegan, gluten-free and local sourcing. To know which items to keep, operators can even use data insights on menu items down to the ZIP code level to localize their offerings and adapt to diverse tastes to drive online sales.

Promotion analytics

As consumers embrace home entertaining this Mother’s Day, restaurant operators can use data insights to boost sales.They can monitor rivals’ moves and compare their promotional strategies with those of competitors. Evaluating their digital marketing performance (like their brand’s discoverability and visibility ranking on food apps’ homepages) helps restaurants show up more prominently online and sell more.

Savvy restaurants welcome celebrations as lucrative sales occasions

Restaurants can spice up Mom’s life by letting her relax and receive the gifts of tasty meals, time savings and family festivities. Operators can simplify Mother’s Day celebrations by giving consumers a hassle-free dining experience so families can focus on connecting rather than cooking.

For a business advantage, restaurant operators can apply digital marketing insights to boost their agility in responding to consumers’ needs and rivals’ moves.

To stay agile and competitive as the food delivery market booms, leading restaurant chains and food delivery providers are collaborating with DataWeave to make data-driven pricing, menu and promotional decisions that fuel online sales.

1 Retail Holiday and Seasonal Trends: Mother’s Day. NRF. 2021 2 New Study Shows What Moms Really Want On Mother’s Day. US Foods. May 2020. 3 Valinsky, Jordan. 10,000 of America’s restaurants have closed in the past three months. CNN. December 9, 2020. 4 Contreras, Tricia. How the pandemic is shaping home cooking trends. SmartBrief. September 30, 2020. 5 Lalley, Heather. Despite pandemic, Mother’s Day was huge for restaurants. Restaurant Business. May 18, 2020.

Show moms extra love this year. With Mother’s Day coming up fast, savvy beauty and fashion brands will use this special occasion to inspire pampering and gift giving to fuel their e-commerce sales growth.

This year, beauty and fashion are poised to boom, as 40% of consumers plan to buy beauty products and 37% will buy new outfits for going out. 1 According to eMarketer,apparel and accessories e-commerce sales will grow nearly 19% this year due to pent-up demand for clothing, while health and beauty sales will rise 16%. 2

“People will be happy to go out again … there will be a fiesta in makeup and in fragrances.”

~L’Oréal CEO and Chairman Jean-Paul Agon

After beauty and apparel sales declined last year, brands now seize every opportunity to capitalize on the categories’ resurgence in 2021. To differentiate their goods, brands can use e-commerce marketing best practices to position their fashion and beauty items as spectacular gifts that moms will love.

Aligning with the latest trends can help brands boost online growth.

Hot trends dominating beauty and fashion

This Mother’s Day, shoppers can delight moms with beauty bestsellers like:

Mask-friendly makeup: As we continue to wear masks over the short-term, cosmetics like false lashes, smudge-proof mascara and ultra-hypoallergenic eyeshadow will remain popular. 3

Fragrances: Online fragrance sales rose 45% year-over-year in 2020. Clean and organic beauty categories grew 56% with fragrance brands growing the most. 4

Purpose-led brands: Consumers crave companies that care. More online searches contain keywords like “ethical beauty” and “sustainable makeup” for products that help consumers look good and feel good. 5

Online fashion is in vogue

Before the pandemic, consumers bought less than one-third of their apparel or footwear online; last year, the proportion surged to an astounding 51%. In 2021, consumers will invest even more in their wardrobes, including trends like:

Comfort: Athleisure will remain in demand as many consumers still prefer comfortable clothing when they work from home. 7

Beloved staples: Classic pieces like jeans, dresses and simple yet elegant tops are making a comeback as consumers start to go out more. 8

Retro ‘80s: Ladies are ready to party like it’s 1984. Bright and metallic colors and sequins for occasionwear (and even NFL linebacker-inspired shoulderpads) are recreating a fun, indulgent ’80s vibe. 9

Brands’ secret weapon for a competitive advantage

For successful Mother’s Day campaigns, more fashion and beauty brands will use digital shelf analytics for marketing decisions that maximize their ROI and e-commerce sales.

To ensure online shoppers discover Mother’s Day products with ease, brands are usingShare of Searchinsights to measure their share of digital shelf. These DataWeave analytics tell brands which keywords perform best. Brands can also benchmark their search and navigation visibility against rivals’ rankings across e-commerce categories, websites and geographic regions.

Using Content Auditinsights tells brands how their content is performing. They can discover and fill content gaps so their products show up more prominently. Optimizing content (like keywords, product page titles, descriptions, ads and sponsored space) and images to align with the retailers’ search algorithms ensures a consistent brand experience across all online channels. Improving content helps brands connect to consumers with marketing that resonates and inspires them to buy. Brands also use

Pricing and Promotionsinsights to measure the effectiveness of their online promotions and secure sales. Brands can stay competitive by ensuring their pricing and promotions are in line with rivals’ offers, such as identifying first movers and rivals with the deepest discounts across retailers and SKUs. Brands can even determine how imitating rivals’ pricing and promotional moves could impact revenue and sales volume.

Help shoppers make Mom’s day

Since Mother’s Day is almost here, beauty and fashion brands can apply these data insights to connect consumers with a variety of products moms will love. Digital shelf analytics from DataWeave can help brands deliver timely campaigns, improve their return on digital marketing spend and make effective marketing decisions to drive e-commerce sales.

1 Howland, Daphne. Wells Fargo sees permanent behavior shifts from the pandemic. Retail Dive. March 29, 2021. 2 Droesch, Blake. US Ecommerce by Category 2021. eMarketer. April 27, 2021. 3 Wood, Dana. Is Makeup Dead? The Robin Report. April 18, 2021. 4 Larson, Kristin. Fragrance Sales Pick Up As Consumers Reengage With The Outside World. Forbes. April 27, 2021. 5 What Can Brands Learn About Sustainability From Green Beauty Consumers? Beauty Business Journal. June 15, 2020. 6 Howland, Daphne. Wells Fargo sees permanent behavior shifts from the pandemic. Retail Dive. March 29, 2021. 7 Ibid. 8 Bhattarai, Abha. Americans are starting to buy real clothes again. The Washington Post. March 18, 2021. 9 Warren, Liz. Loose Denim and Bold Occasionwear on Full Display for Fall 2021. Sourcing Journal. April 2, 2021.

Soaring e-commerce growth has made retail more crowded, complex and competitive. Now retailers face an urgent need to keep an eye on more rivals with potential substitute products to maximize their own e-commerce growth.

Consider these recent figures, which illustrate online shoppers’ abundance of product choices:

24% year-over-year increase in direct-to-consumer (DTC) brands in the U.S. alone was estimated for 2020 as more brands bypass retailers1

55% of shoppers have purchased private label in the past year and many retailers are investing more in their own brands2

110% average increase in small retailers’ 2020 online holiday sales, as more players launched new e-commerce shops during the pandemic3

39% of U.S. consumers have changed brands, with the level of brand switching doubling in 2020 compared to 2019, especially among Gen Z and Millennial consumers, as loyalty declines4

These statistics prove that in 2021 retailers need to navigate more online players and products. Now retailers need a new approach to stay on top of market trends to keep their e-commerce strategies competitive, profitable and attractive to discerning online shoppers.

Retailers reduce the risk of substitutes with similarity matching

In response to online crowding, more leading retailers are turning to similarity matching. Similarity matching is a type of retail analytics that scour global e-commerce sites to find products that exactly match a specific item as well as products that closely match it. Similarity matching insights have grown in strategic significance because they increase retailers’ visibility into potential substitute products, so they can respond to all rivals’ moves with greater agility and efficiency to stay competitive.

In terms of e-commerce applications, similarity matching helps retailers gather insights on potential substitute products so they can adjust their pricing and assortment strategies accordingly. Retailers can align their pricing with rivals’ pricing moves for similar items to protect their margins and maximize profitability. They can also make informed assortment decisions, including which product mix of bestsellers, unique items and private labels could optimize their online sales performance.

Online shoppers search for productsdifferently across different categories

Consumer behavior plays a role, as online search habits differ across product categories, which influences the type of similarity matching retailers need. For example, categories like fashion, toys, home and kitchen work best with similarity matching based on text and images. In these highly-visual categories, consumers can quickly determine whether a product fits the design and aesthetic they are looking for. As a result, e-commerce product titles, descriptions and product images play a big role in consumers’ purchase decisions.

By contrast, consumer electronics and furniture are categories in which consumers tend to seek specific product attributes, such as a certain level of resolution for their high-definition TV or a couch with particular dimensions so it fits their living room. For these types of products, consumer purchases are driven by product specifications, so similarity matching takes into account their specific needs as well as a degree of tolerance for exact or near-similar attributes across online competitors.

Expect intense e-commerce rivalry in 2021

As more consumers shop online, they are increasingly informed by online product comparison information. A wide variety of product choices means consumers can substitute similar goods with ease, especially if a particular item is out-of-stock. Perceived product differentiation, price sensitivity and private labels can also influence consumers’ purchase decisions.

Across categories, e-commerce growth is outpacing total retail growth. When competition is this fierce, there is an increased risk that numerous and aggressive players will drive down profit margins. Leading retailers are now seizing opportunities to earn consumer loyalty. Using similarity matching helps retailers by offering in-demand products that consumers will actually buy and deliver exceptional online experiences to prevent shoppers from switching to rivals and their comparable products.

Similarity matching lets you stay competitive

As e-commerce traffic and rivalry increase, similarity matching helps retailers stand out and serve online shoppers more effectively.

Retailers gain visibility into their entire competitive landscape to keep their e-commerce strategy responsive to shifts among consumers and rivals. By knowing the full scope of potential substitute products available online, retailers can keep their pricing and assortment strategies in line with rivals’ to reduce their risk of losing sales to rivals, and boost their top line, profitability and cost savings.

The data insights give retailers the flexibility they need to align with online shoppers’ different needs across categories. As a result, retailers can use similarity matching to boost agility and gain a competitive advantage by adapting to online shoppers’ needs, winning their sales and fueling e-commerce growth.DataWeave’s similarity matching capability lets clients

1 US Direct-to-Consumer Ecommerce Sales Will Rise to Nearly $18 Billion in 2020. eMarketer. April 2, 2020.

2 Ochwat, Dan. Shopper study: Private brands purchased because they’re preferred. Store Brands. February 24, 2021 3 Miranda, Leticia. Small businesses who pivoted to e-commerce saw record sales during Black Friday weekend. December 1, 2020. 4 Charm, Tamara, Harrison Gillis, Anne Grimmelt, Grace Hua, Kelsey Robinson and Ramiro Sanchez Caballero. Survey: US consumer sentiment during the coronavirus crisis. McKinsey & Company. March 24, 2021.

The proliferation of informed shoppers, e-commerce sites, and competitors of all sizes has increased the complexity of – and lucrative opportunities in – brand management.

Now more brands rely on data insights to uncover specific ways to make their digital marketing more arresting, effective and profitable. Many brands struggle with e-commerce profitability due, in part, to advertising expenses that often yield lackluster results.1

Analytics are growing in retail significance, as 88% of retail and consumer goods marketers say data improves their marketing by allowing them to personalize touchpoints. Relevant marketing and great marketers helps brands connect with consumers. Let’s see why leading brands are adding data insights to their 2021 marketing strategies to fuel online sales growth.

Brands discover how to get discovered

Consumer goods brands no longer leave it up to chance that consumers will find them online. The digital migration of companies and consumers over the past year means more noise for brands to breakthrough.

Now search is growing in importance to improve brands’ online product discovery. Here’s why:

87% of shoppers begin their hunt in digital channels3

17% rise in paid search in late 20204

24% rise in paid social advertising during the same period5

To grab consumers’ attention by being easier to see, more brands are turning to data insights to track their online visibility.

Brands need to look for ways to mitigate the high costs of acquiring customers online6

Brands use marketing analytics related to keywords and navigation searches help brands know exactly how much space on the digital shelf they occupy across different online platforms.

These DataWeave’s Share of Search solutions help brands understand what percentage of the digital shelf they command through either keywords or navigation. These insights can help brands decide whether to boost their brand visibility using sponsored ads to ensure their products show up more prominently in online search results to boost brand reach and awareness on each channel. For instance, brands can tell whether consumers search for products using branded, generic or category-specific keywords to align their marketing accordingly.

In addition, brands can see how their organic and sponsored results rank compared to their competitors to spot ways to improve their visibility rank and decrease customer acquisition costs.

Content differentiates a brand’s digital shelf

For a striking digital presence and enhanced discoverability, leading brands measure how effectively their content inspires online shoppers to choose them.

Brands can improve their digital marketing results by using Content Audit insights to spot patterns among their top-performing campaigns. They can also benchmark their content with category bestsellers to discover how to optimize their online performance to grow sales volume and market share.

Strategic advertising requires high-quality photography and data-driven content7

Using these data insights from DataWeave helps brands determine how well their content (including product description pages and images) align with e-commerce algorithms and lead to online traffic, engagement and sales. Brands also adapt faster by adjusting underperforming campaigns to reduce costs and optimize their digital marketing spends.

Brands can fill content gaps across online channels with enhanced product information that aligns content and images with brands’ product information management (PIM). Using analytics to deliver a consistent brand experience across all online channels can help brands build relationships with consumers and earn their trust.

Alluring promotions help brands secure the sale

As e-commerce evolves, brands have matured beyond Google AdWords and Facebook campaigns to offer targeted promotions across digital touchpoints, which increases marketing reach and complexity.

To boost clarity, be in demand and drive sales across online platforms, more leading brands use data insights to measure the effectiveness of their digital Promotions. Promotional insights from DataWeave keep brands informed of trending categories and products to keep their online offerings relevant and timely. Brands can pinpoint exactly which products to promote and which e-commerce sites help them drive the most profitable results with compelling digital offers.

Brands that respond quickly to their customers’ needs have the upper hand8

Analytics also keep brands competitive and relevant by benchmarking their promotional strategies with their rivals’ and continuously monitoring rivals’ online moves. For instance, brands can track the promotions their competitors offer for similar products across different e-commerce sites. These competitive insights help brands quickly spot opportunities to optimize their online conversions with appealing promotions that reflect market trends.

Better marketing decisions can help brands grow sales and share

Data insights make brands more enticing by connecting the dots among their online visibility, content and promotions. Brands uncover ways to make smarter marketing decisions faster to improve their top line and decrease customer acquisition costs. DataWeave analytics also help brands stand out and improve product discovery, engagement and sales. As a result, brands save time and boost their agility with relevant marketing that resonates and inspires shoppers to keep coming back.

1 Jansen, Caroline, Cara Salpini and Maria Monteros. 8 DTC trends to watch in 2021. Retail Dive. February 3, 2021 2 Casna, Kathryn. Ecommerce Trends That Are Shaping the Way Businesses Sell Online. Salesforce. 2021. 3 Casna, Kathryn. Ecommerce Trends That Are Shaping the Way Businesses Sell Online. Salesforce. 2021. 4 The Future of eCommerce in 2021. Shopify Plus. 2021. 5 The Future of eCommerce in 2021. Shopify Plus. 2021. 6 Jansen, Caroline, Cara Salpini and Maria Monteros. 8 DTC trends to watch in 2021. Retail Dive. February 3, 2021. 7 Glasheen, Jasmine. 2021 Forecast: Next Gens in a Brand-New World. The Robin Report. January 3, 2021. 8 Monteros, Maria. Forrester: Few brands can anticipate and act on consumer needs. Retail Dive. February 10, 2021.

Brands that protect their bottom line will win online.

As global e-commerce smashes sales records, more brands are now taking control over their online presence (“digital shelf”) to enhance their performance and profit margins.

In the U.S., the increase in e-commerce penetration during the first half of 2020 was equivalent to that of the last decade.1 Last year also marked the first time in history that all retail sales gains came from e-commerce.2 E-commerce has lasting appeal, as two-thirds of consumers plan to continue to shop online after the pandemic.3

“Brands need to continue to look for ways to mitigate the high costs of acquiring customers online.” 4

To keep up as shopping migrates online, brands face bigger expenditures. In the second quarter of 2020, e-commerce costs grew much faster (up 60% year-over-year) than revenues (up 40%).5 Namely, brands face steep costs for customer acquisition and logistics, which erode their online profit margins.

The bottom line for brands is they must sell online – profitably – to stay competitive. They urgently need new ways to drive online sales and incur fewer costs. Let’s see why brand leaders are using data insights to optimize their e-commerce decisions and profitability.

Brands find new growth opportunities

Over the past year, e-commerce has gotten more crowded. Now brands seek proven ways to differentiate their offerings and consistently deliver an alluring online experience. That’s because a recent study found 42% of consumers cite less trust in online shopping due to poor experiences, such as inconsistent pricing and out-of-stock merchandise.6 In response, these e-commerce best practices can help brands improve the customer journey and top line sales.

To help consumers find their products online with ease, brands can use data insights for superior product discovery. Insights help brands know exactly which keywords shoppers search for to earn high visibility rankings among consumers’ online search results. Data analytics direct brands to the most relevant keywords, which they can use in marketing, including product descriptions, for effective online discovery.7

Brands also face increased pressure to keep up with rivals’ real-time pricing changes across retailers’ e-commerce sites, online marketplaces and social media. Insights help brands price competitively across channels by monitoring and promptly adapting to competitors’ online pricing moves. Brands can even use data to ensure merchants consistently respect pricing policies.

Data analytics also help brands measure their marketing effectiveness and popularity across e-commerce

websites, and how they compare to their rivals. Brands can improve how they promote their products by using targeted digital content that resonates. For instance, they can publish unique content on each channel tailored to the platform’s unique algorithm and use data to discover patterns among their top performing campaigns. Also, brands can determine when to use their own social media channels or pay for sponsored ads to drive more sales.

As we saw last March, in-stock merchandise is essential to maximize online sales. Data analytics help brands track their stock status to ensure products are available across all their digital channels for reliable service that sparks more sales.

Brands find new efficiencies

Cost effectiveness is also vital and these e-commerce best practices help brands boost their online efficiencies.

Brands use insights to pinpoint and keep sharing content that effectively resonates with and enages their target audience. They can use data insights to see where to allocate their marketing spend for online promotions and either revitalize or drop underperforming online promotions. Brands can also track whether their online promotions align with rivals’ promotions to stay competitive and agile.

Likewise, measuring a brand’s popularity through consumer reviews reveals which underperforming products to downplay to conserve marketing resources for the specific products and bundles that perform best in their categories. For instance, PepsiCo’s and Kraft Heinz’s new online shops offer only large items or bundles for basket sizes large enough to offset shipment costs.8

To reduce the high cost of product returns, brands can use data insights to prioritize bestselling products rather than items consumers are more likely to send back. Using clear, up-to-date content, including product descriptions with accurate dimensions, can also help online consumers know exactly what they’re buying to minimize returns.

How brands and consumers profit

When brands use insights to make better e-commerce decisions, they can compensate for ballooning expenses. Analytics help brands connect the dots among their online visibility, promotions, performance and reviews. These best practices can give brands an edge by uncovering how to be more aggressive with revenue-earning and cost-cutting opportunities. Brands find effective ways to acquire more online customers to improve their top line and offset e-commerce expenses with new efficiencies. Data-driven digital marketing decisions help brands improve their e-commerce effectiveness to stay profitable and competitive.

Meanwhile, consumers also win by having an inviting, smooth and reliable online shopping experience. They find the products they want with greater ease, and feel confident enough to buy based on information like a brand’s pricing, promotions and product availability.

1 Arora, Arun, Hamza Khan. Sajal Kohli and Caroline Tufft. DTC e-commerce: How consumer brands can get it right. McKinsey & Company. November 30, 2020. 2 Ali, Fareeha. US ecommerce grows 44.0% in 2020. Digital Commerce 360. January 29, 2021. 3 Arora, Arun, Hamza Khan. Sajal Kohli and Caroline Tufft. DTC e-commerce: How consumer brands can get it right. McKinsey & Company. November 30, 2020. 4 Jansen, Caroline, Cara Salpini and Maria Monteros. 8 DTC trends to watch in 2021. Retail Dive. February 3, 2021. 5 Haber, John. Logistics Costs Challenge E-Commerce Profit Margins. Parcel Industry. October 9, 2020. 6 O’Carroll, Derek. 5 Hidden Trends That Will Shape E-Commerce in 2021. Total Retail. February 4, 2020. 7 Leong, Brandon. COVID-19 strategy: Use the power of your digital sell sheet. Digital Commerce 360. August 23, 2020. 8 Arora, Arun, Hamza Khan. Sajal Kohli and Caroline Tufft. DTC e-commerce: How consumer brands can get it right. McKinsey & Company. November 30, 2020.

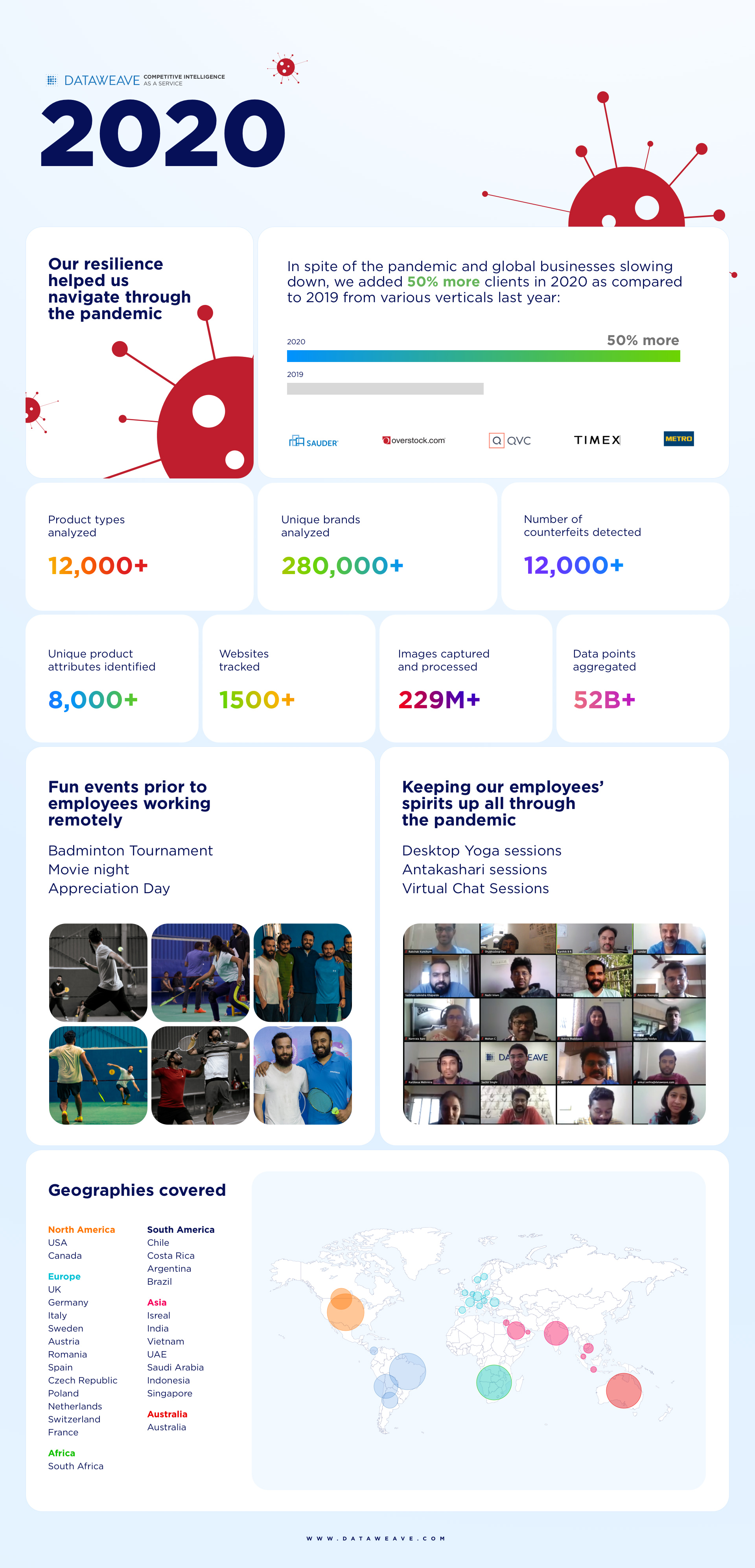

The start of 2020 brought with it the promise of global economic growth. Markets in the US were on a steady rise we also witnessed demand from brands and retailers in Europe and the Middle East. All seemed to be on track to make it a year of plenty.

Out of nowhere, the end of the first quarter saw the world coming to a grinding halt. The world was held hostage by a global pandemic and the force with which we were hit, was unprecedented.

From February to mid-May we saw things come to a sharp halt. We at DataWeave seized this intermittent downtime to bolster our product offerings.

On the flip side, when the world did start opening May onwards, we saw completely new categories take center stage digitally. With new habits and trends taking shape, the pandemic single-handedly caused exceptional growth in the Food and Grocery Delivery intermediaries. Predictably, the rest of the world followed. Our existing customers saw the competition rise steeply with everyone coming online. We invested substantially in our Digital Shelf Analytics solutions after noticing that e-commerce was seeing a boom. 2020 saw brands making their online presence the new norm. This meant that small, medium and large enterprises had to now divert their spending to analytics and e-commerce.

It is interesting to note that the rise in the food and grocery delivery segment gave brands another channel to focus on vis a vis their presence. Brands that were available on these sites focused on how they could optimize their sales on these channels, which proved to be the front runners during the height of the pandemic. While the challenges and opportunities for both these segments overlapped and seemed similar, our solutions helped measure and optimize brand performance across all online channels. Some of the in-demand solutions and analytics we saw our customers use were; share of search, content audit, assortment and availability, pricing and promotions, and ratings and reviews.

There were mixed emotions in the market, with regard to the best use of marketing spends. Human resource and client cutbacks happened across the board. At DataWeave however, we had the pleasure of onboarding 25 new clients including retailers and brands ranging from food and grocery delivery, home improvement from across multiple geographies.

Infographics

Throughout the year, the work never ceased at DataWeave. The team showed incredible resilience while working remotely, making sure our deliverables were being taken care of, at all times. Due to the e-commerce boom and immense pressure from existing and new entrants in the digital space, our clients saw a need to gather more insights. With the given uptick, we are happy to report that our stellar 95%+ accuracy record for in-depth insights at scale, was maintained through the course of all the work done.

Looking forward to the year 2021:

In the US, the adoption of e-commerce accelerated as traditional brick and mortar stores shut down and pivoted. To put things into perspective, e-commerce adoption grew only by 4.3% from 2014 to 2019. In just three months in 2020, e-commerce adoption grew at 4.3%! Add to that, with approved vaccines making their way slowly to the public, we do anticipate the travel sector to open up and we look forward to working with new clients.

Nike’s Chief Executive, John Donahoe recently said, ” We know that digital is the new normal. The consumer today is digitally grounded and simply will not revert back…the shift to online sales could be a permanent trend.” We could not agree more! With online sales here to stay, brand and retailers’ requirements to keep their competitive edge will only continue to grow. We at DataWeave, look forward to delivering the results they want in this new year, and for the years to come.

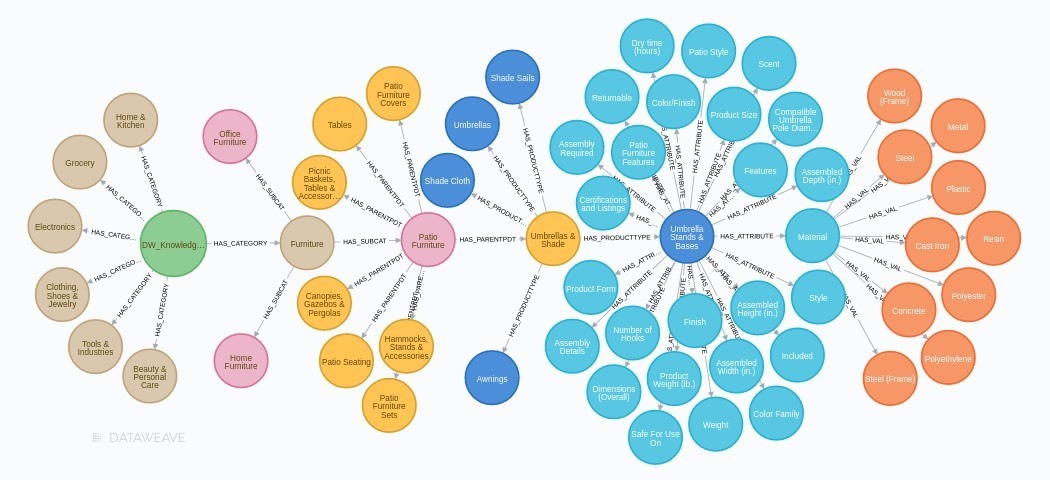

In Part 1 we discussed the importance of Retail taxonomy and the applications of mapping retail taxonomies in Assortment Analytics, building Knowledge Graph, etc. Here, we will discuss how we approached the problem of mapping retail taxonomies across sources.

We solved this problem by classifying every retail product to a standard DataWeave defined taxonomy so that products from different websites could be brought at the same level. Once these products are at the same level, mapping taxonomies becomes straightforward.

We’ve built an AI-based solution that uses state-of-the-art algorithms to predict the correct DataWeave Taxonomy for a product from its textual information like Title, Taxonomy and Description. Our model predicts a standard 4 level (L1-L2-L3-L4) taxonomy for any given product. These Levels denote Category, Sub Category, Parent Product Type and Product Type respectively.

Approach

Conventional methods for taxonomy prediction are typically based on machine learning classification algorithms. Here, we need to provide textual data and the classifier will predict the entire taxonomy as a class.

We used the classification approach as a baseline, but found a few inherent flaws in this:

A Classification model cannot understand the semantic relation between input text and output hierarchy. Which means, it cannot understand if there’s any relation between the textual input and the text present in the taxonomy. For a classifier, the output class is just a label encoded value

Since the taxonomy is a tree and each leaf node uniquely defines a path from the root to leaf, the classification algorithms effectively output an existing root-to-leaf path. However, it cannot predict new relationships in the tree structure

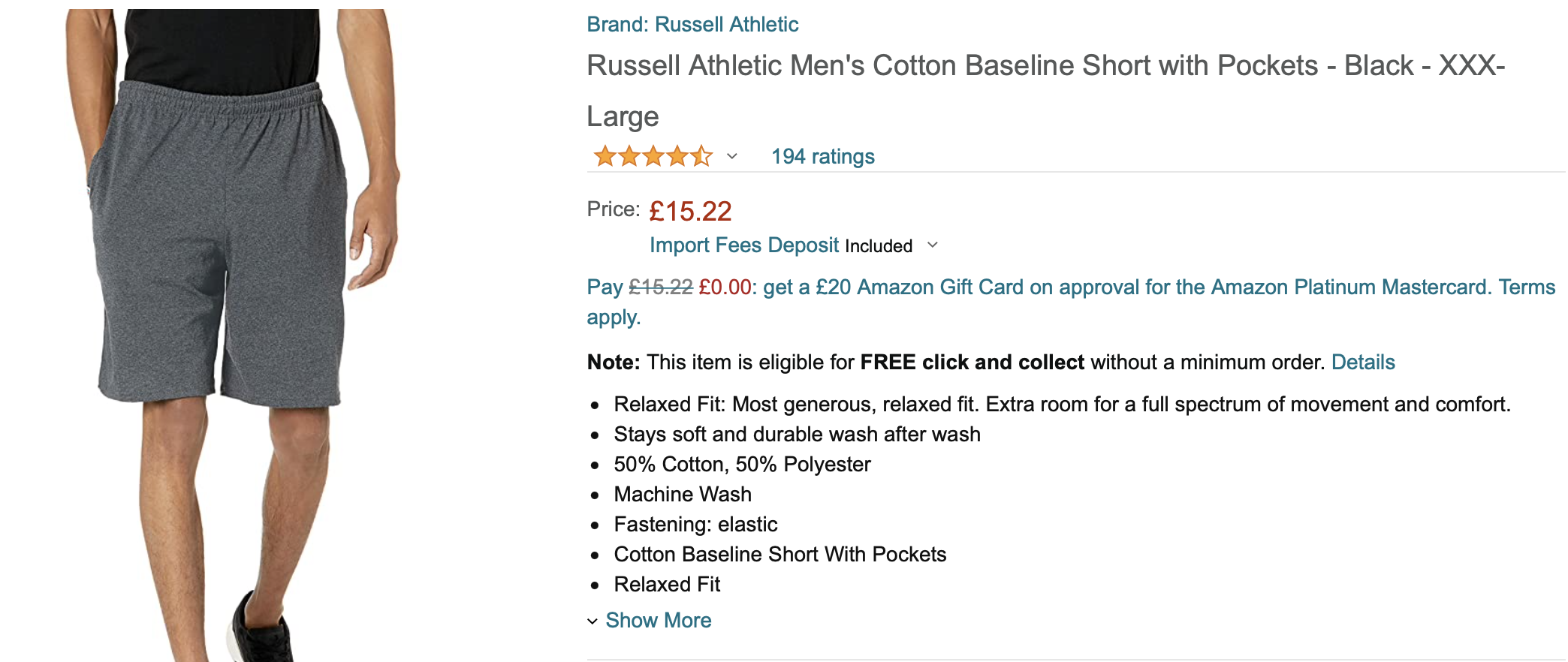

Let’s say, our training set has only the records for “Clothing, Shoes & Jewelry > Men > Clothing > Shorts” and “Clothing, Shoes & Jewelry > Baby > Shoes > Boots”, Example:

{‘title’: “Russell Athletic Men’s Cotton Baseline Short with Pockets – Black – XXX-Large”,

Now, if a product with Title “Burt’s Bees Baby Baby Boys’ Terry Short” comes for prediction, then the classifier will never be able to predict the correct taxonomy. Although, it would have seen the data points of Shorts and Baby.

E-commerce product taxonomy has a very long tail, i.e. there’s a huge imbalance in counts of data per taxonomy. Classification algorithms do not perform well for very long tail problems.

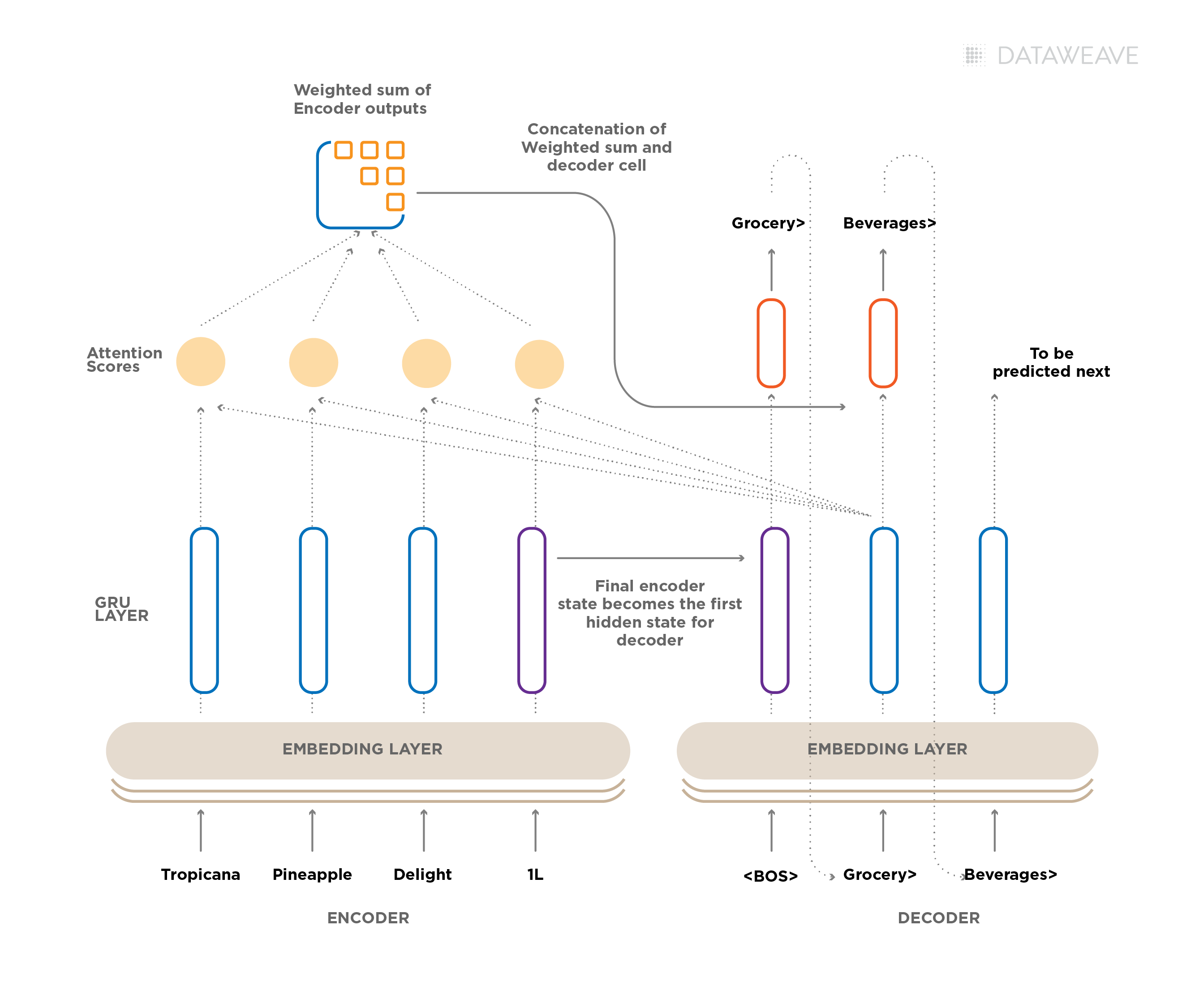

Encoder-Decoder with Attention for Taxonomy Classification

What is Encoder-Decoder?

Encoder-Decoder is a classical Deep Learning architecture where there are two Deep Neural Nets, an Encoder and a Decoder linked with each other to generate desired outputs.

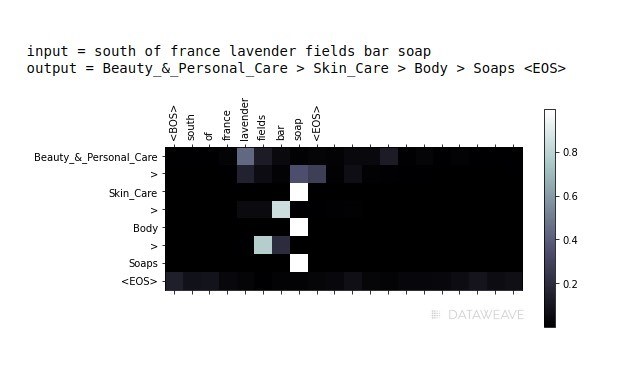

The objective of an Encoder is to encode the required information from the input data and store it in a feature vector. In case of text input, the encoder is mostly an RNN or Transformer based architecture and for image input, it is mostly a CNN-based architecture. Once the encoded feature vector is created, the Decoder uses it to produce the required output. The Encoder and Decoder can be interfaced by another layer which is called Attention. The Role of Attention mechanism is to train the model to selectively focus on useful parts of the input data and hence, learn the alignment between them. This helps the model to cope effectively with long input sentences (when dealing with text) or complex portions of images (when input is an image).

Instead of classification-based approaches, we use an Encoder-Decoder architecture and map the problem of taxonomy classification to the task of machine translation (MT) AKA, Seq2Seq. An MT system takes the text in one language as input and outputs its translation as a sequence of words in another language. In our case, the input maps to the textual description of a product, and the output maps to the sequence of categories and sub-categories in our taxonomy (e.g., Clothing, Shoes & Jewelry > Baby > Shoes > Boots). By framing taxonomy classification as an MT problem, we overcome a lot of limitations present in classical classification approaches.