As consumer goods brands increasingly turn to eCommerce marketplaces as a source of profitable growth, it becomes harder for teams to grapple with the complexity of revenue growth management.

This complexity emerges from multiple fonts: there are hundreds, and even thousands, of competitors to consider when formulating strategies for managing pricing, promotion, and assortment changes. The world is currently experiencing a period of unprecedented supply chain instability, shifting more consumers away from traditional retail and into eCommerce shopping. And finally, consumer buying patterns, preferences, and trends are constantly shifting.

Revenue growth management (RGM) and net revenue management (NRM) were once less complex processes; but that is no longer the case. Now, some 80% of consumer brand CEOs report that they “aren’t satisfied with their RGM results.”

Gathering data, analyzing it, and acting on it quickly stand out as major challenges that businesses must overcome to grow their market share, earn more profits, and capitalize on market shifts in real time. In this article, we’ll dive into RGM and NRM, the obstacles business teams face, and explore how using technology for digital shelf analytics can help bridge the gap.

What is Net Revenue Management (NRM) or Revenue Growth Management (RGM)?

Every consumer goods company aims to increase profits and grow market share. This requires a concerted effort in RGM and net revenue management (NRM) strategy. Whether a company has a specific team dedicated to this task or relies on the abilities of business analysts or merchandisers, this function is crucial.

It’s worth mentioning that though the terms NRM and RGM are often used interchangeably, there are subtle differences. While both net revenue management and revenue growth management focus on maximizing overall revenue for the brand, NRM typically has a narrower focus and is specific to optimizing profitability through product pricing, promotion, product mix, and cost management. RGM strategies are a bit broader and tend to look at the top line to grow market share and expand the customer base.

The Challenges Revenue Teams Face

Differentiating between ‘good growth’ and ‘bad growth’ is central to NRM and RGM. Net revenue management and revenue growth management teams need the data and tools in place to determine if growth in one area is coming at the expense of another so as not to cannibalize business. Tracking and analyzing extensive data to successfully take action on opportunities and determine whether strategies are working as intended consumes a tremendous amount of mental bandwidth. The fact that these decisions are incredibly time-sensitive only compounds the issue.

To cope, many teams in charge of NRM or RGM employ digital shelf analytics strategies to help speed up data aggregation and analysis to make sure they’re capitalizing on potential opportunities.

eCommerce has added a whole new layer of complexity to consumer goods sales. Instead of a few relatively stable prices at big-box stores, a single item for sale may experience high price volatility, with dozens of minute pricing changes occurring online each day. In some cases, consumers become blind to price volatility, letting brands increase prices, but consumer sentiment, the overall price elasticity of the product, and dozens of other factors go into determining the final price of an online product. Net revenue teams need to modernize and adapt to changing eCommerce environments to competitively price, promote, and grow their revenue.

Here are the top three challenges standing in the way of net revenue management and revenue growth management teams and solutions to address these issues.

Challenge 1: Incomplete or Inaccurate Data

Incomplete and inaccurate data are critical for Net Revenue Management and Revenue Growth Management teams to get under control when attempting to modernize in a digital-centric selling environment. As more competitors enter the market, many brands find it hard to make strategic decisions without the complete picture.

Data may be incomplete or inaccurate because a brand is analyzing only part of the market, such as Amazon or another enterprise-scale eCommerce marketplace. Additionally, they might not be analyzing all types of online media, such as branded ads, sponsored search listings, or sponsored category listings.

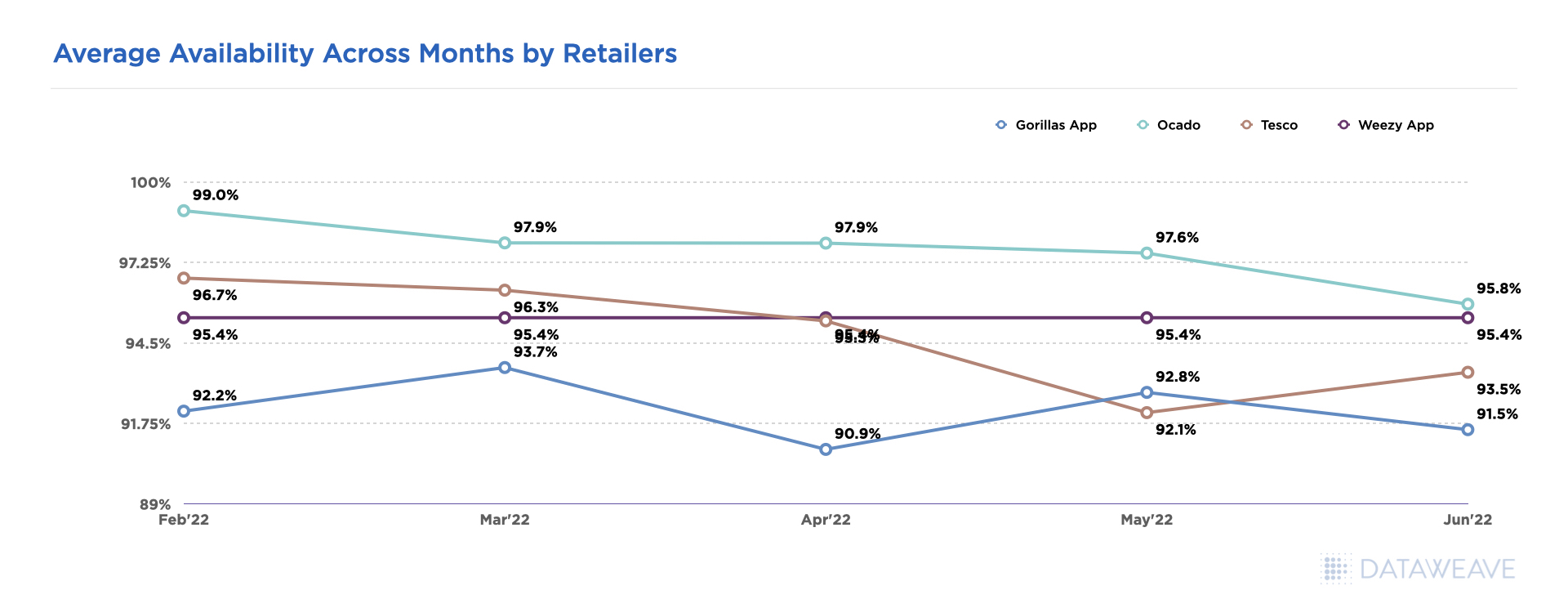

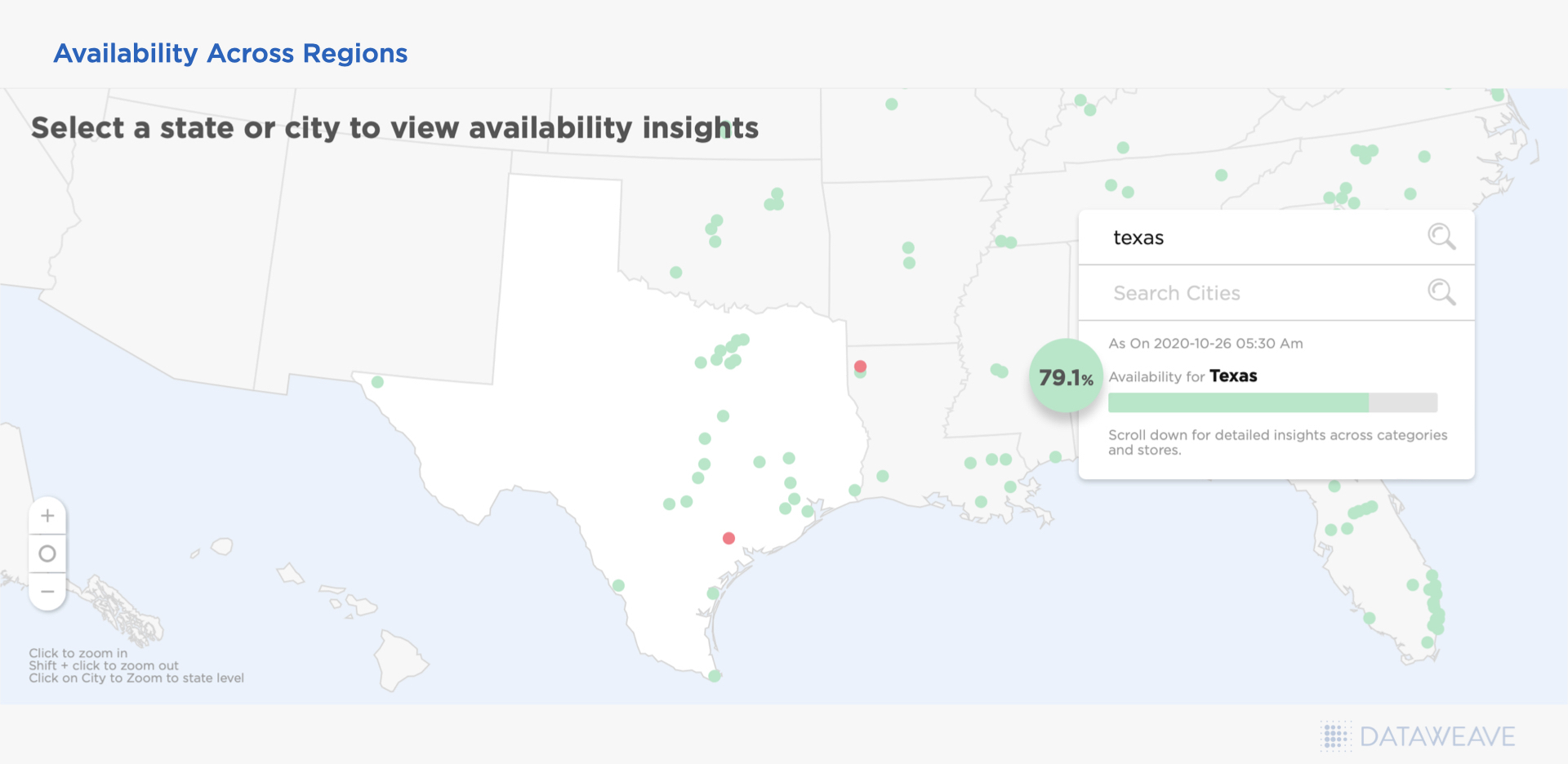

Most importantly, another pitfall is the lack of hyperlocal data. Generalized data across regions, states, ZIPs, and stores can skew the decision-making process and result in poor outcomes.

Overcoming Incomplete or Inaccurate Data

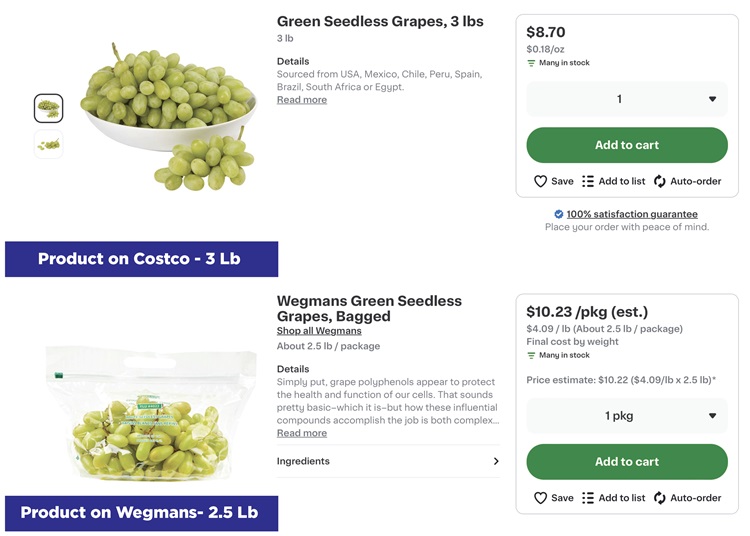

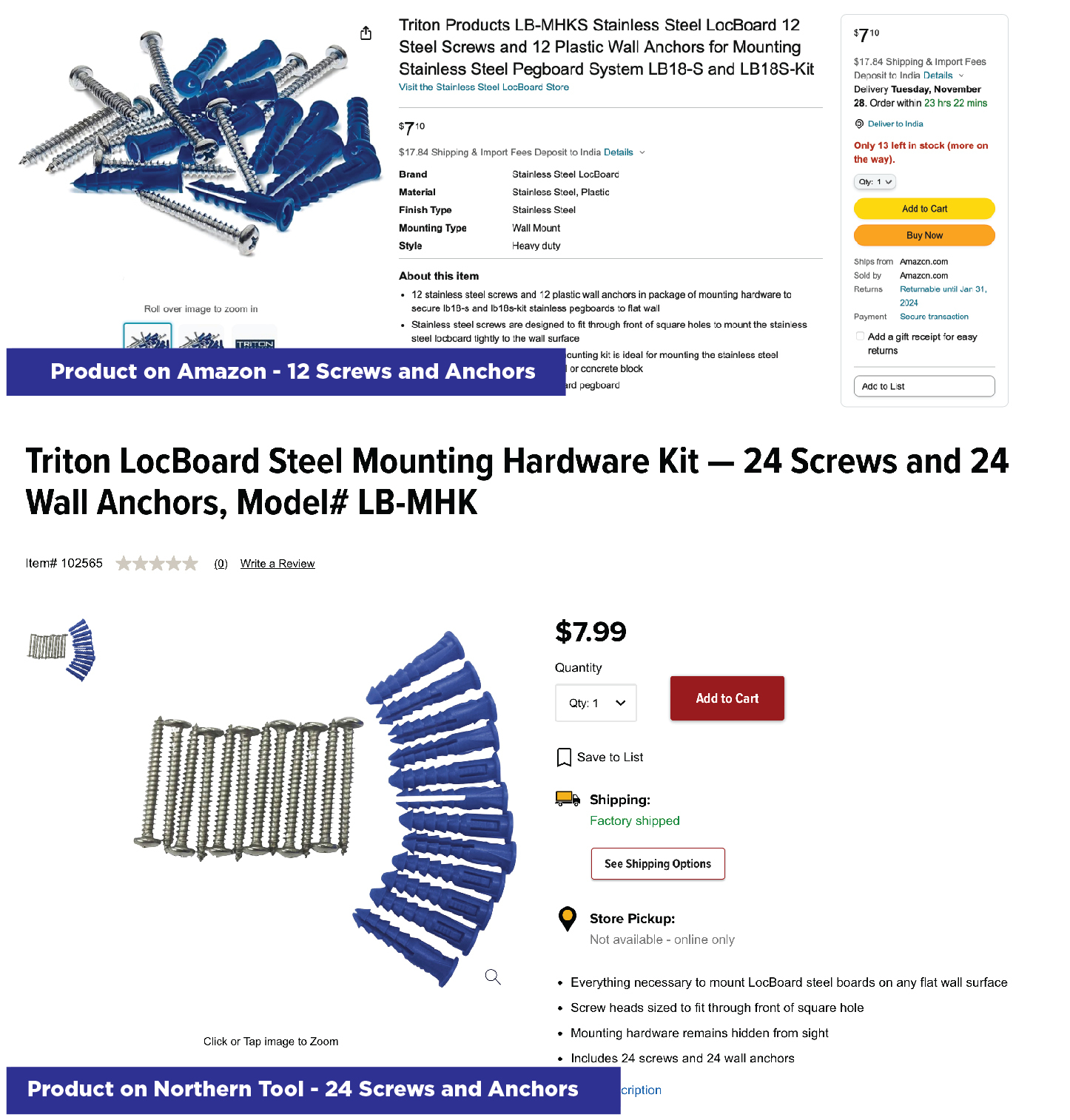

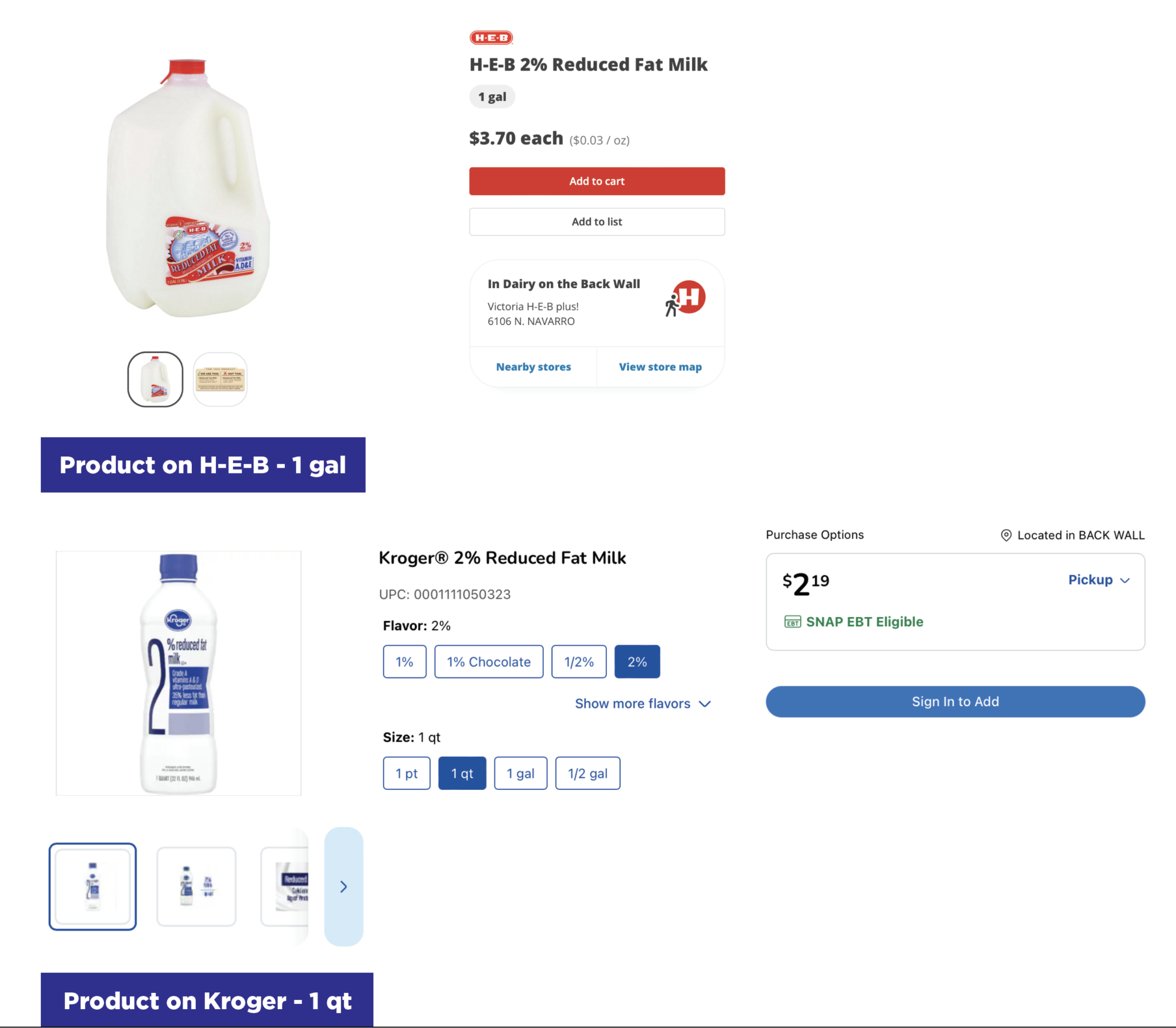

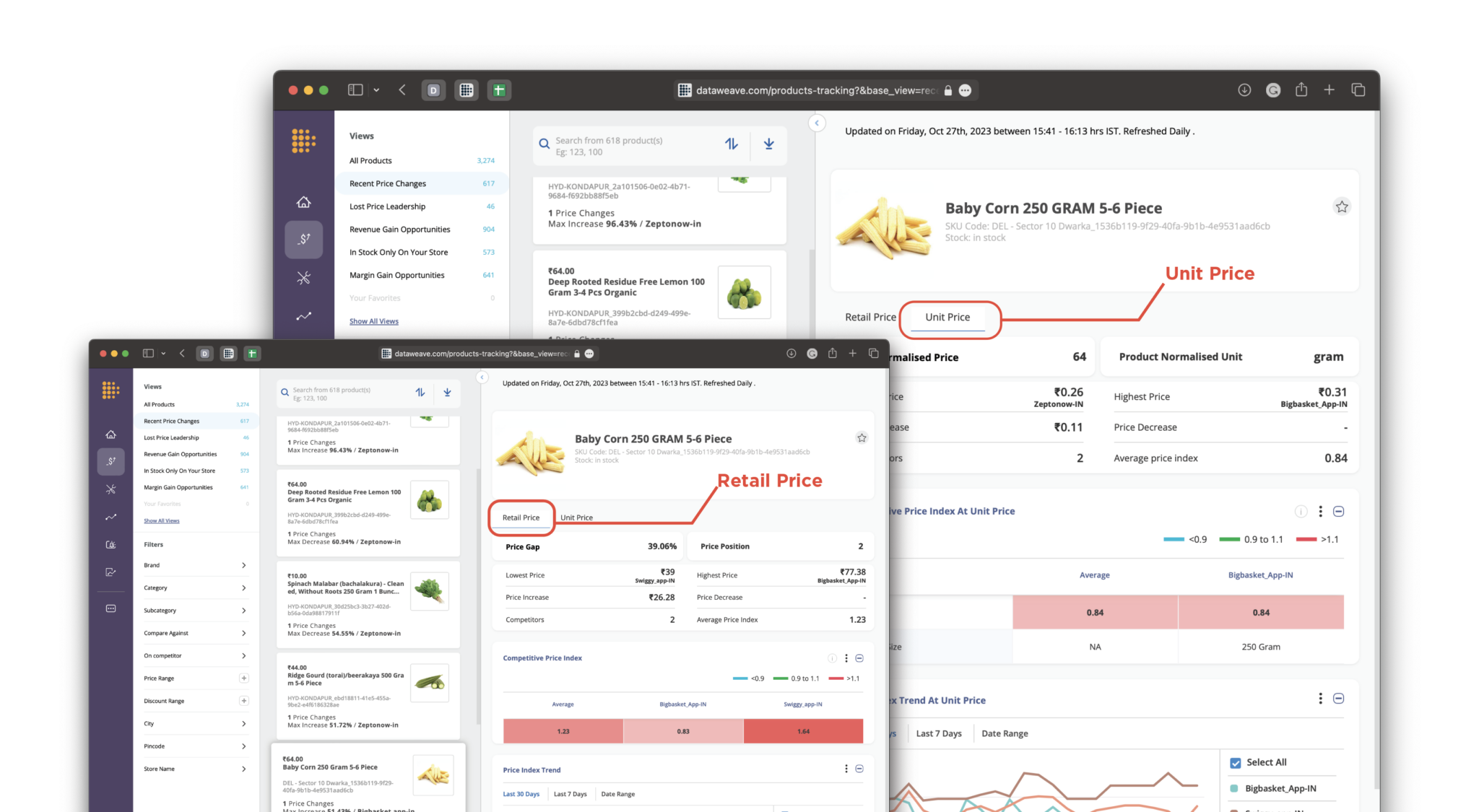

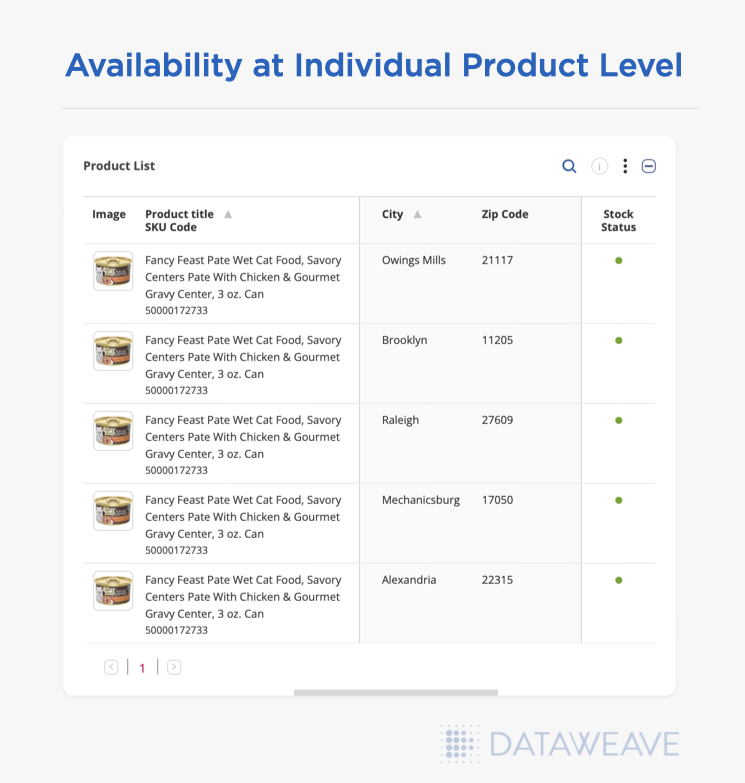

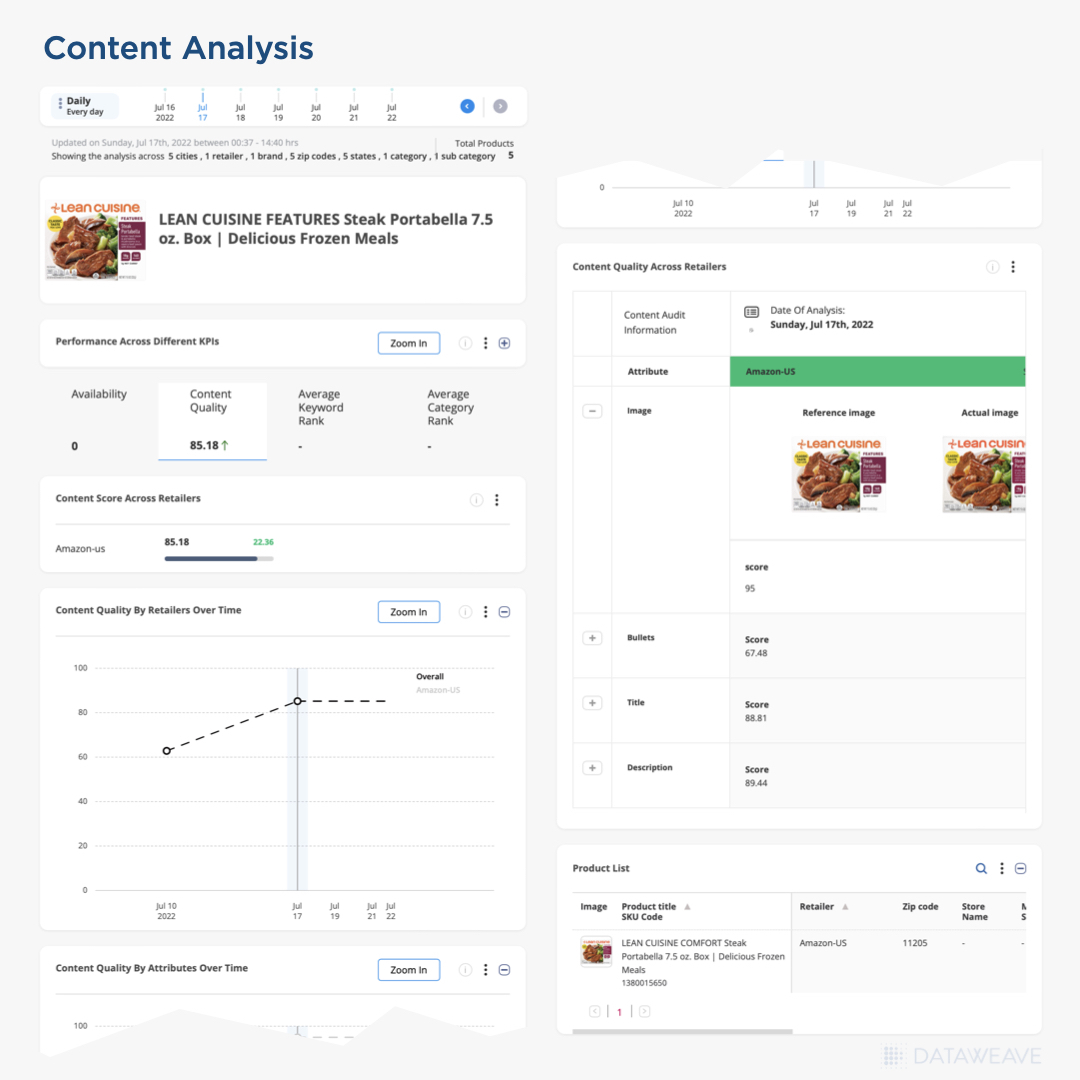

In order to get the full picture, consumer brands need to ensure they have a view of the entire competitive landscape across their channels. This includes gathering data down to the case pack, the unique product identifier, and the geography, including ZIP and store. They also need the respective MSRP by SKU, the unit normalized price, and the selling price at a specific moment in time. This is done by aggregating brick-and-mortar store information available online, such as when stores list curbside pickup SKUs and pricing online.

Individual teams cannot manually gather all this detailed data. The growth in eCommerce means there is simply too much data to find and aggregate. Instead, they can employ digital shelf technology to get more data from more sites. Teams can leverage AI to better match product listings, ads, and even visuals to avoid missing data on listings that lack common attributes, such as UPCs for normalization.

To add to this, advanced pricing intelligence systems can cache URLs to help teams audit and verify their data, avoiding delays and confusion when ad hoc requests arise.

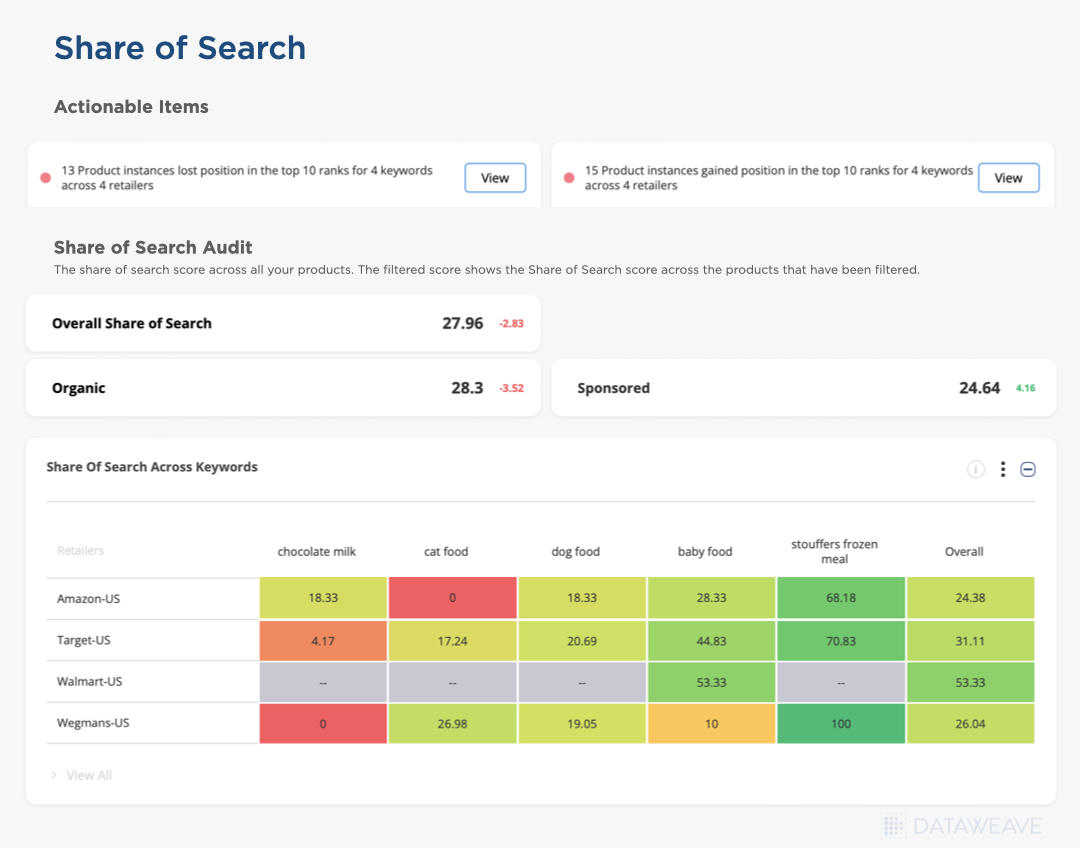

Challenge 2: Difficulty in Making Sense of the Competitive Landscape

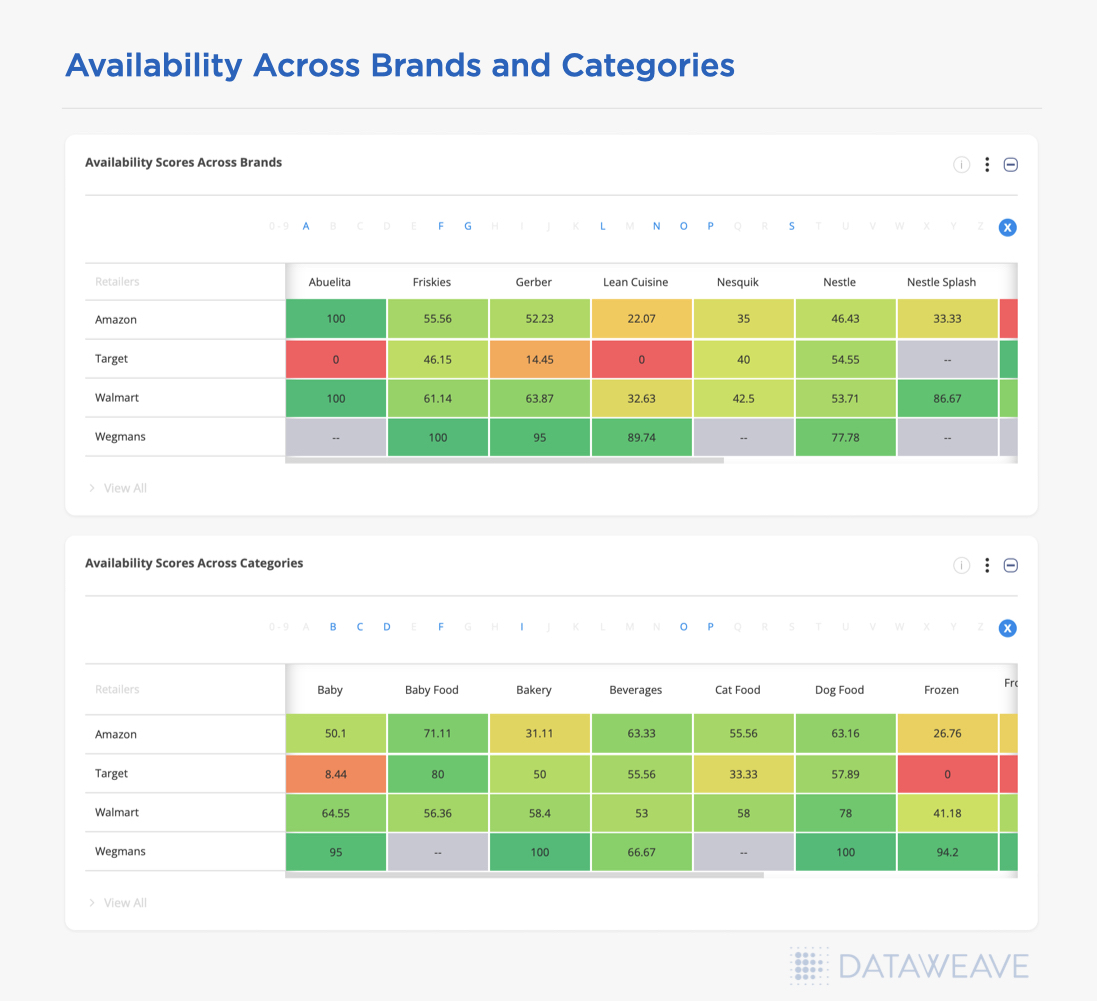

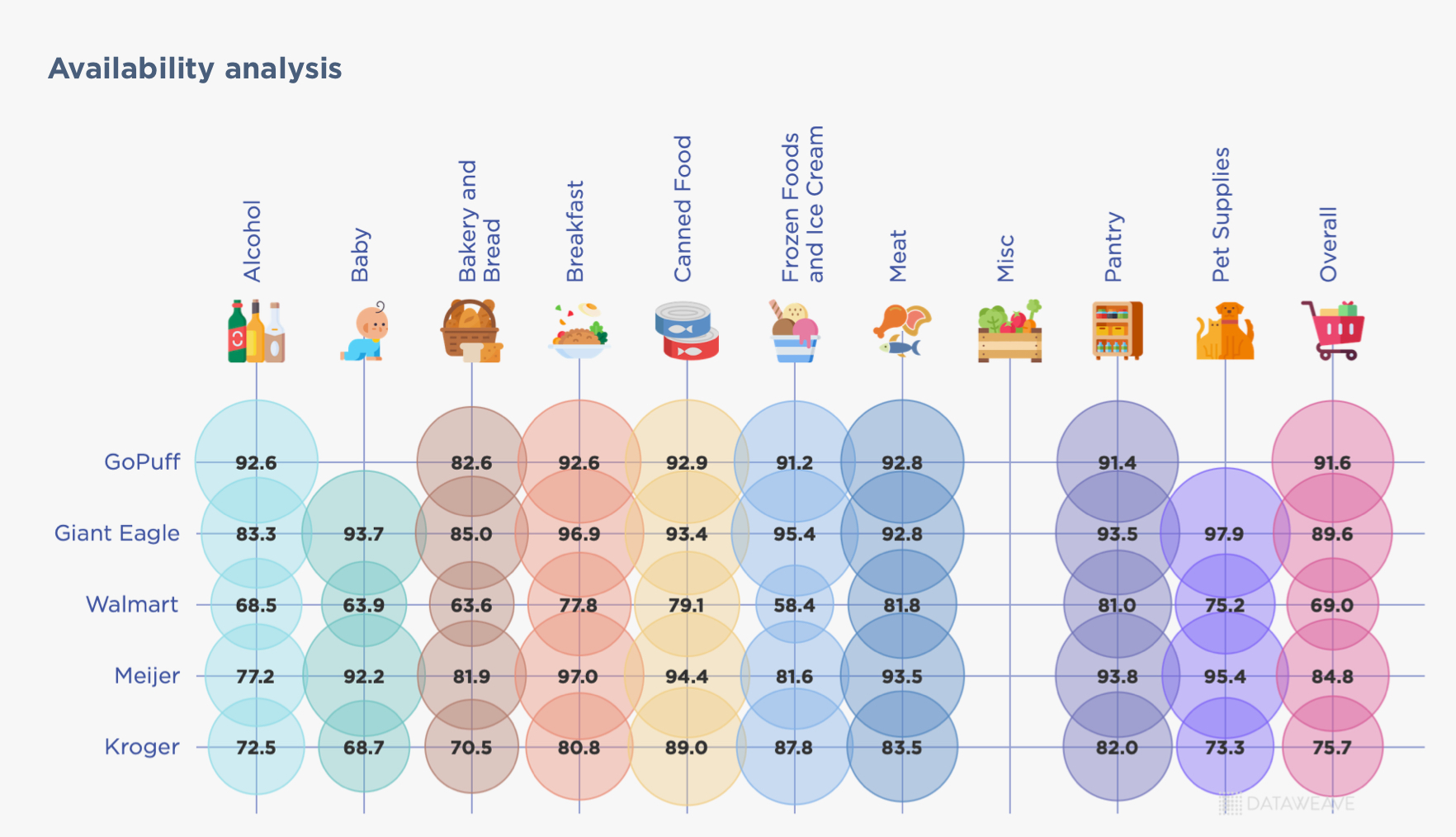

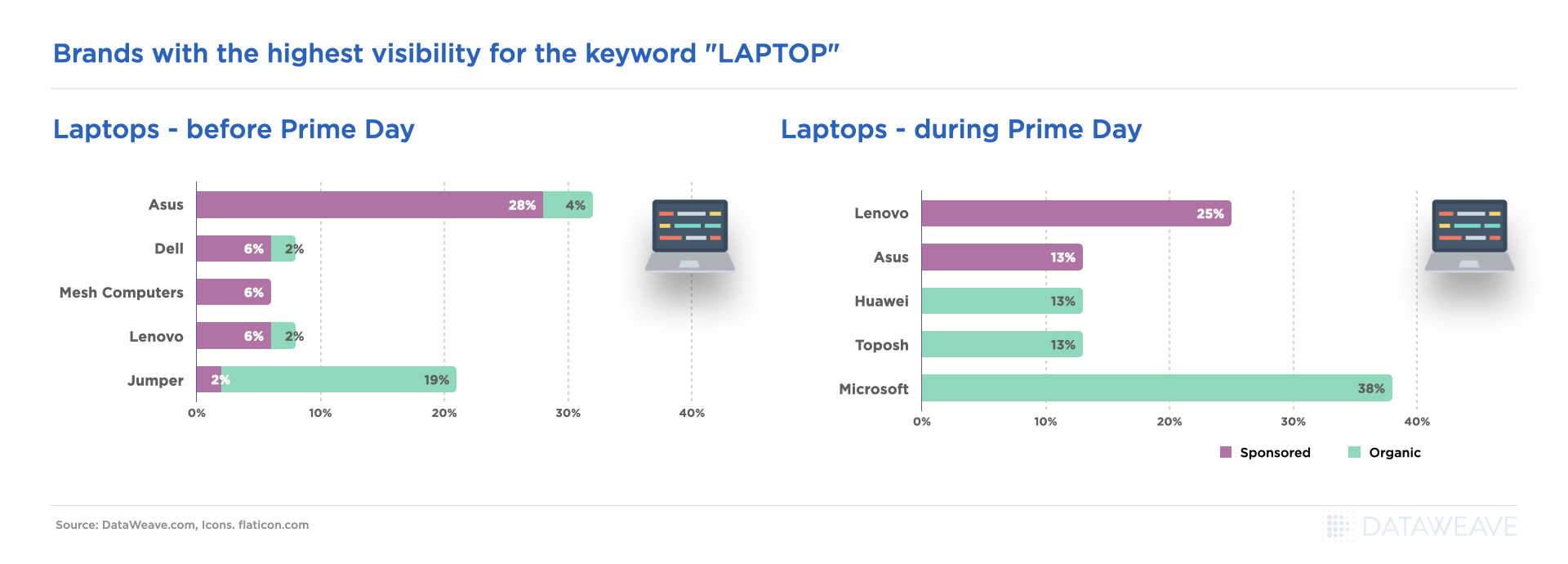

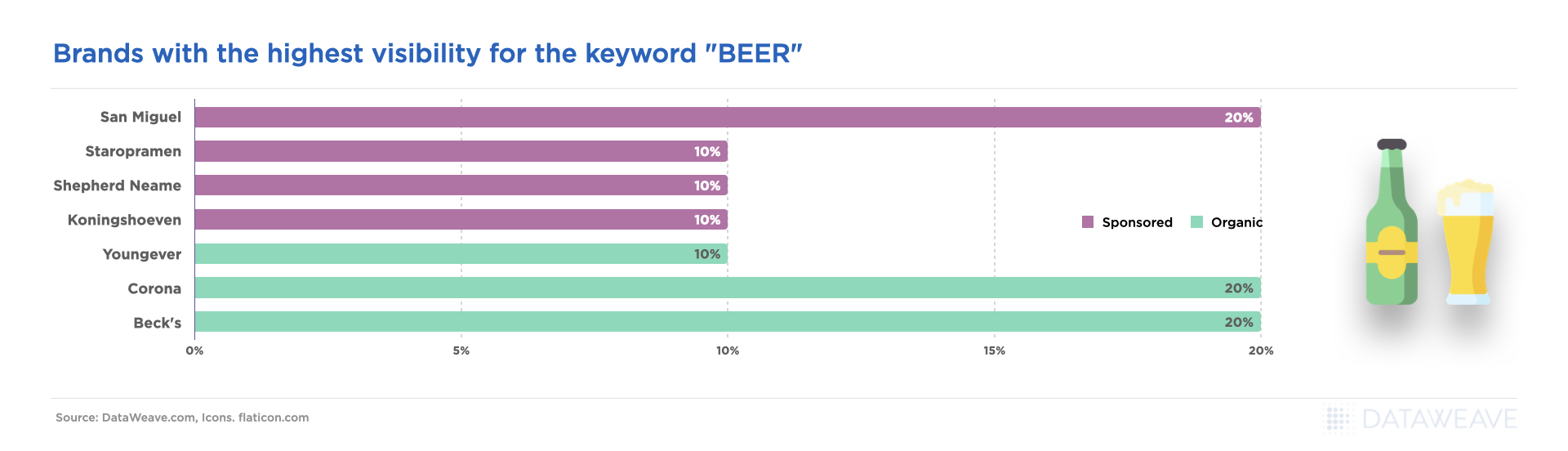

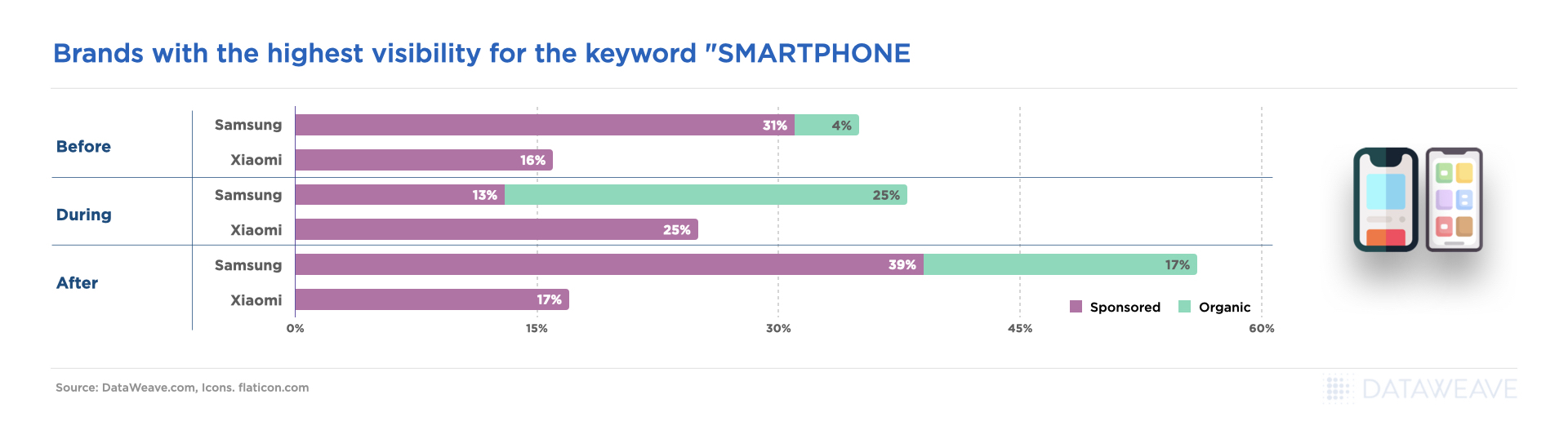

Once net revenue management and revenue growth management teams have gathered all of the available data, it’s time to make sense of it. This is a monumental challenge, and ends up being the stage where most NRM and RGM teams flounder. Disparate marketplaces include different product attributes and images. This makes it extremely complicated to sync competitors’ data to ready it for analysis, especially if this analysis is carried out manually in Excel. These are some of the attributes that teams need to harmonize in order to make sense of the competitive landscape:

- Product identifiers (UPC, SKU, Internal Code)

- Size, case, pack, volume, bundled offerings

- Language

- Currency

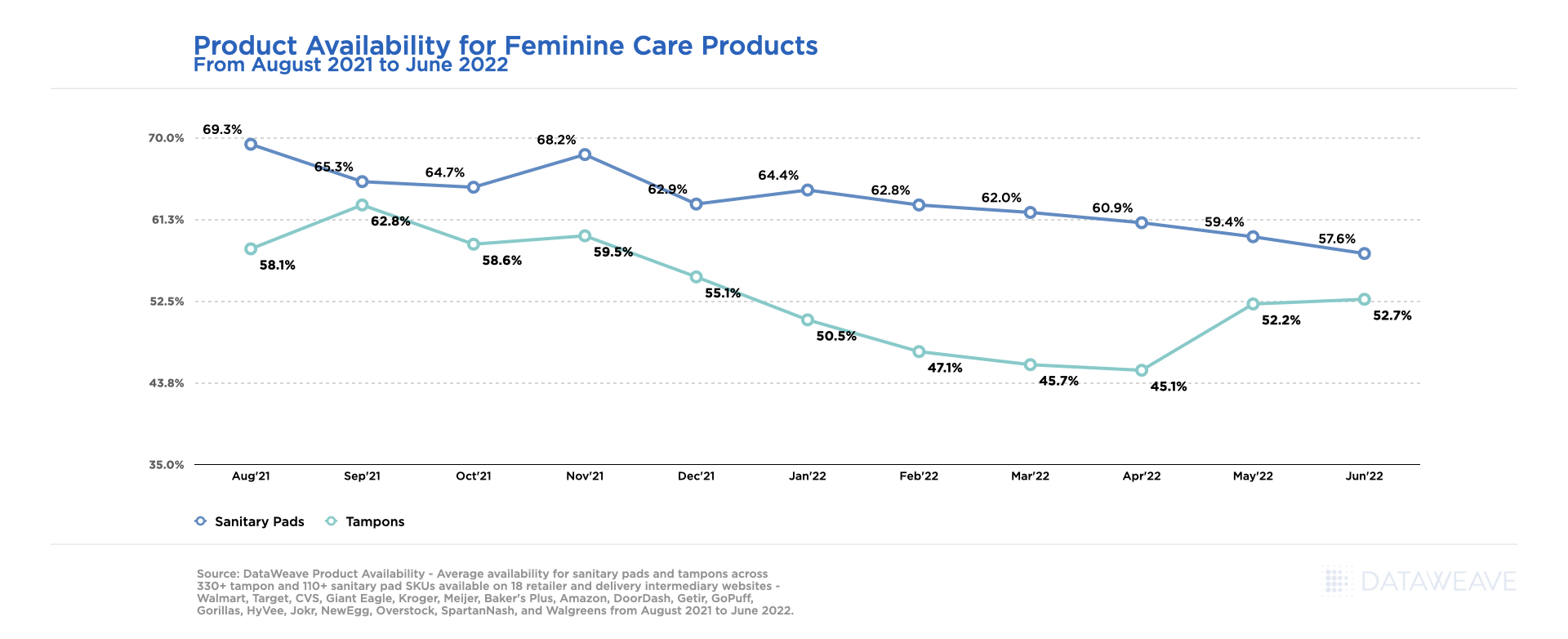

- Stock Status (Whether the product is available or not)

- Platform-specific attributes such as ‘Amazon’s Choice,’ ‘Best Seller,’ etc.

Teams also need to group and classify various categories of promotions. These can include sponsored listings, banner ads, coupons, bank offers, and others. Each of these categories needs to be tracked separately. This vast array of data points across hundreds of sites creates a big data problem for teams.

Making Sense of the Competitive Landscape

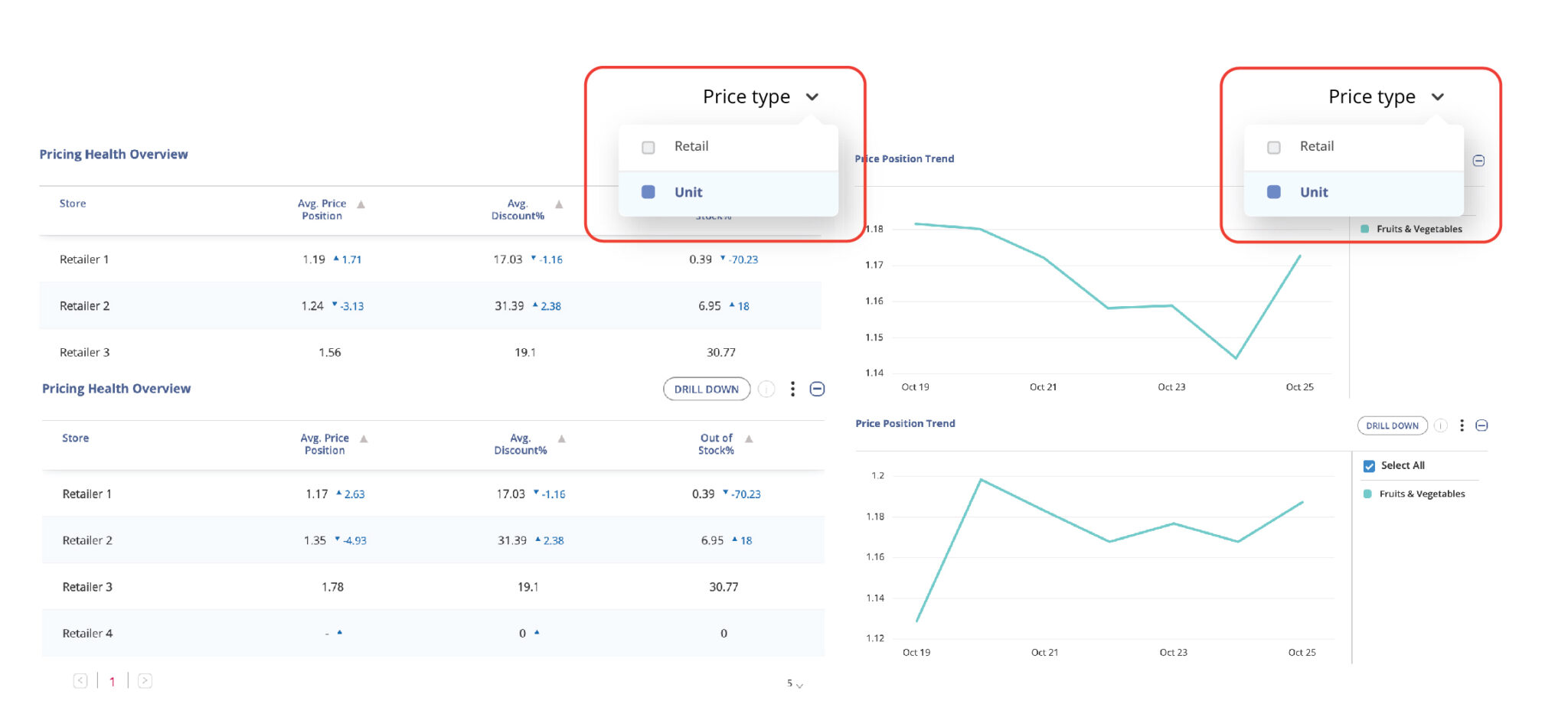

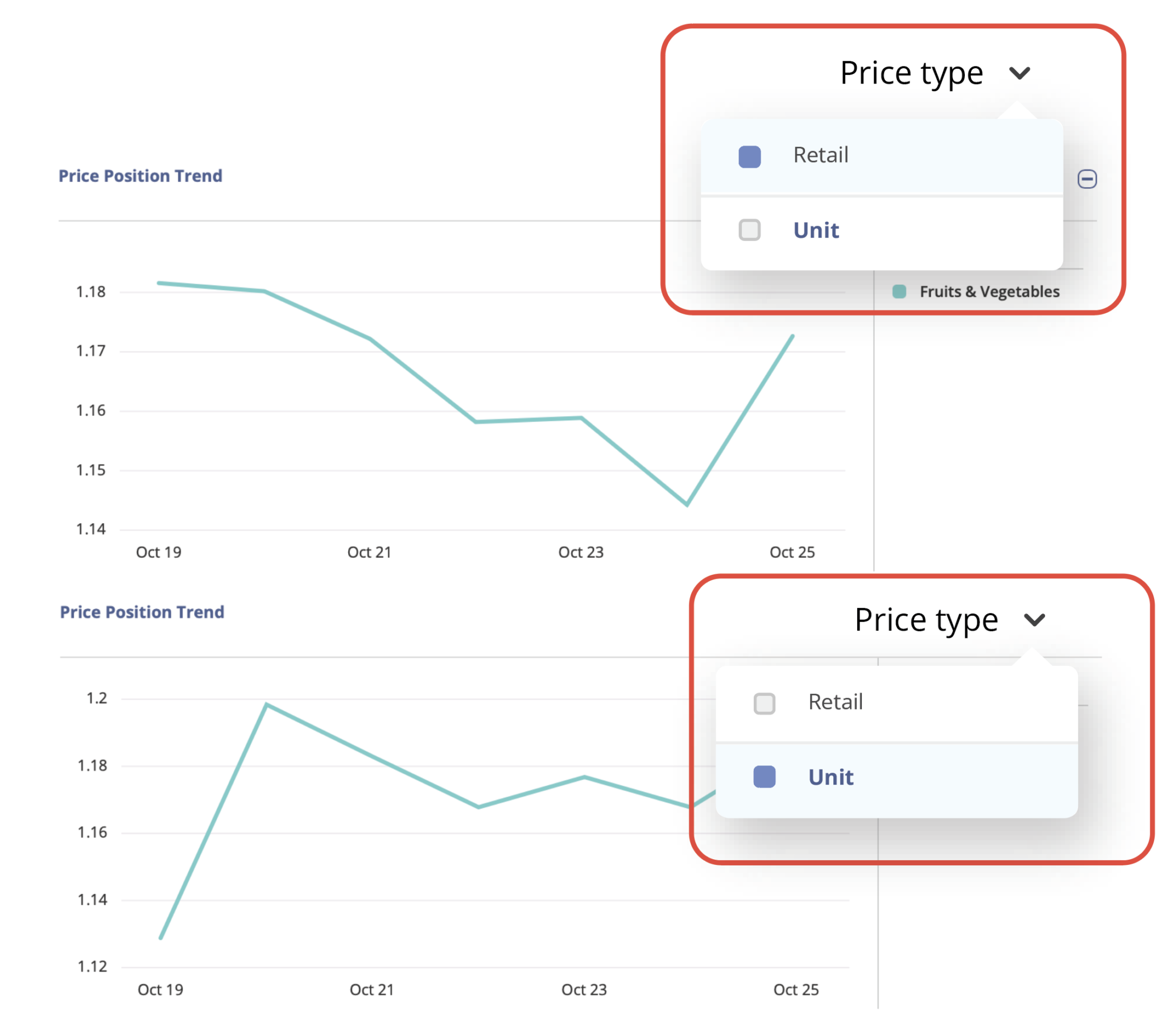

The best way to overcome this challenge is to task a digital shelf analytics system with gathering and harmonizing data automatically across the consumer goods competitive landscape. Competitive and market intelligence tools can help break down an overwhelming amount of data, matching similar products across competing brands and analyzing their various strengths and weaknesses. Once the technology matches complex product attributes and identifiers, it becomes easier for teams to gain insights and exploit findings. In a sense, the data needs to be cleaned before analysis can occur.

Technology can gather data in multiple ways, and the best systems employ several methods to get the best matches. Data consumption modes include API integrations, CSV and Excel file uploads, and proprietary scrapers that view websites independently of direct inputs. Having all the data in a single place helps net revenue management and revenue growth management teams gain indicative insights on product popularity, pricing, and sales, on their own and competitor products.

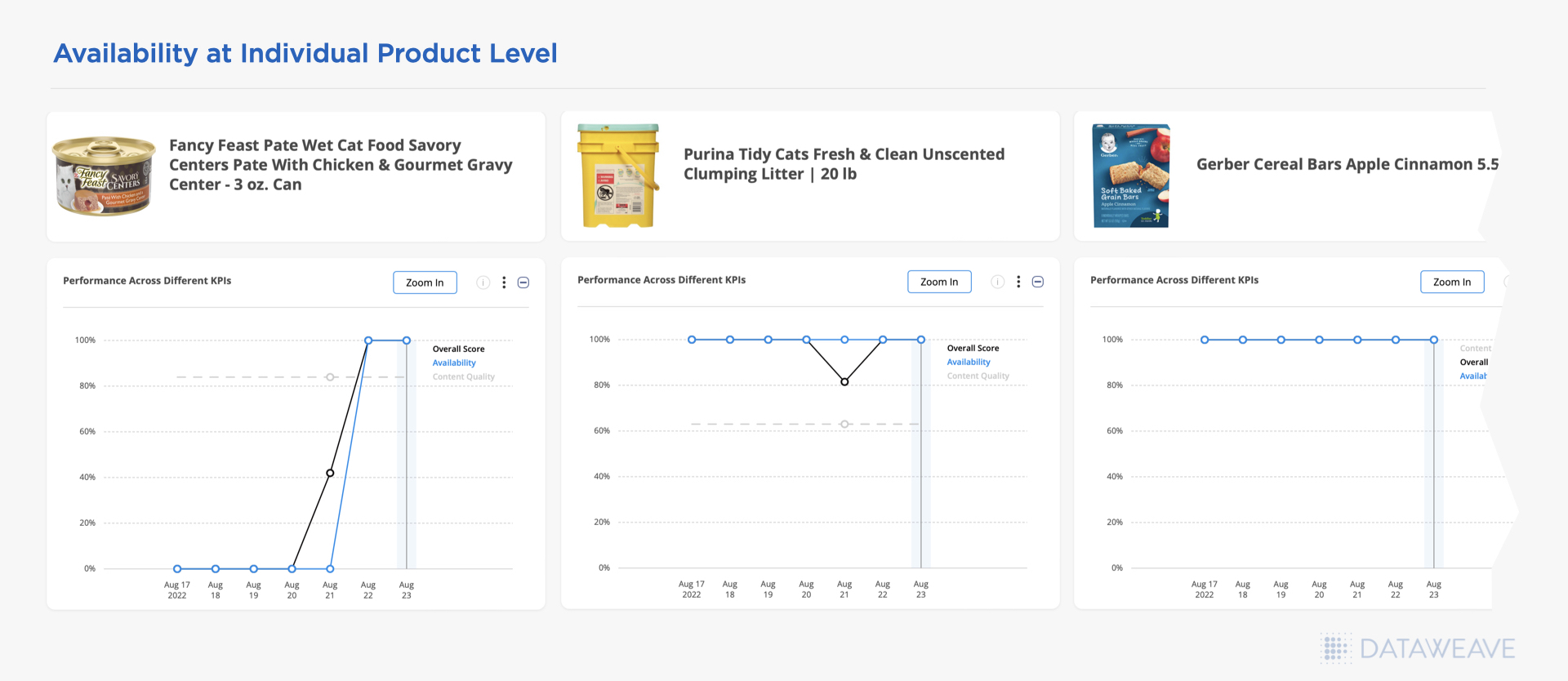

Challenge 3: Lack of Timely Visibility

The final challenge that many net revenue management and revenue growth management teams face is something of a ‘silent killer’ — timeliness. Even if they successfully gather data across the entire competitive landscape and harmonize that data into a format for easy analysis, a lack of timeliness can render even the best actions irrelevant.

Speed is of the utmost importance when there are market changes. If a product goes viral and competitors raise prices in response to increased demand, without timely visibility, the trend may be over before a consumer goods brand can successfully increase its prices for the duration of the trend. This can mean lost margins.

Another example is analyzing data and incorporating lagging promotional and sales data into analyses. This can skew pricing strategies because timely data is not accessible to inform decision-making. Many teams waste time firefighting due to a lack of timely pricing and promotional intelligence data.

Get Near Real-Time Insights for Faster Decision Making

Using technology that allows for net revenue management and revenue growth management teams at consumer goods brands to establish update frequencies can be a game changer. Teams can set update frequencies based on their need. They can set up the system to check a fast-moving product daily, while a slow-moving item might only need to be checked weekly, monthly, or even quarterly. This allows teams to focus on the highest-impact products first and address the largest exceptions before they lose out on an opportunity. Managing exceptions with a digital shelf analytics platform saves teams significant time instead of poring over low-impact changes in the data.

Digital Shelf Analytics for Net Revenue Management

Modernizing a consumer goods brand’s net revenue management or revenue growth management processes requires advanced digital shelf analytics. DataWeave provides consumer goods companies with the technology they need for quick and accurate pricing, promotional, and assortment intelligence. By tracking over 200 million products each day, users can be sure they get the widest and most timely view of the competitive landscape. DataWeave’s deep industry knowledge is baked into every aspect of its platform.