Black Friday 2025 marked another significant shopping event for Canadian consumers, with retailers deploying sophisticated pricing strategies to capture holiday spending. Online and in-store spending on Black Friday reached an estimated $865 million in Canada, which marked a 6% increase compared to last year.

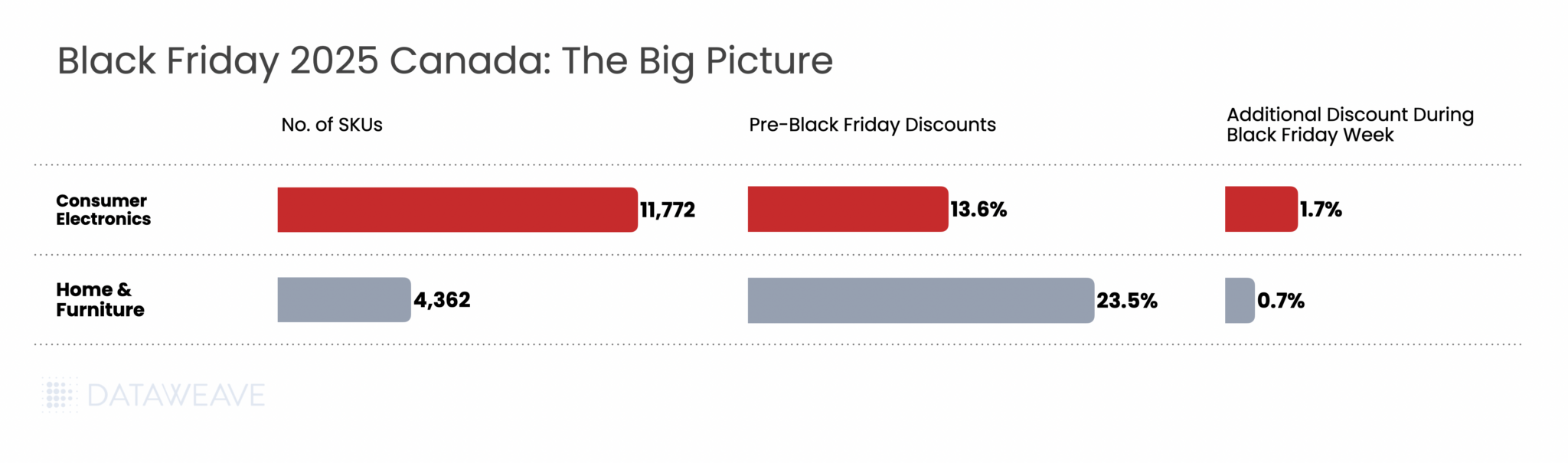

At DataWeave, we analyzed Black Friday 2025 pricing dynamics across two major categories in the Canadian market: Consumer Electronics and Home & Furniture. Our AI-powered pricing intelligence platform tracked approximately 16,000 SKUs across leading Canadian retailers like Target, Walmart, Wayfair, Home Depot, Amazon, Best Buy, Loblaws, Metro and more, uncovering distinct patterns in how brands and retailers structured their promotional calendars this year.

Our Methodology

DataWeave monitored pricing and discount trends across Canadian retailers during two key timeframes:

Pre-Black Friday Period: Up to November 23, 2025 – establishing baseline promotional activity and early holiday deals

Black Friday Week: November 24 – December 1, 2025 – spanning Thanksgiving through Black Friday (November 28) and Cyber Monday (December 1)

Our dataset included top-performing products across multiple subcategories on major Canadian retail platforms. We also tracked Share of Search metrics, measuring brand prominence by analyzing which brand names appeared in the top 20 search results for high-value keywords during each period.

Black Friday 2025 Canada: Overview

Here’s how average discounts compared between the Pre-Black Friday period and Black Friday Week:

Key Finding: Canadian retailers front-loaded their promotional strategy significantly, with Pre-Black Friday discounts averaging 16.3% across categories. The additional lift during Black Friday Week was modest at 1.4%.

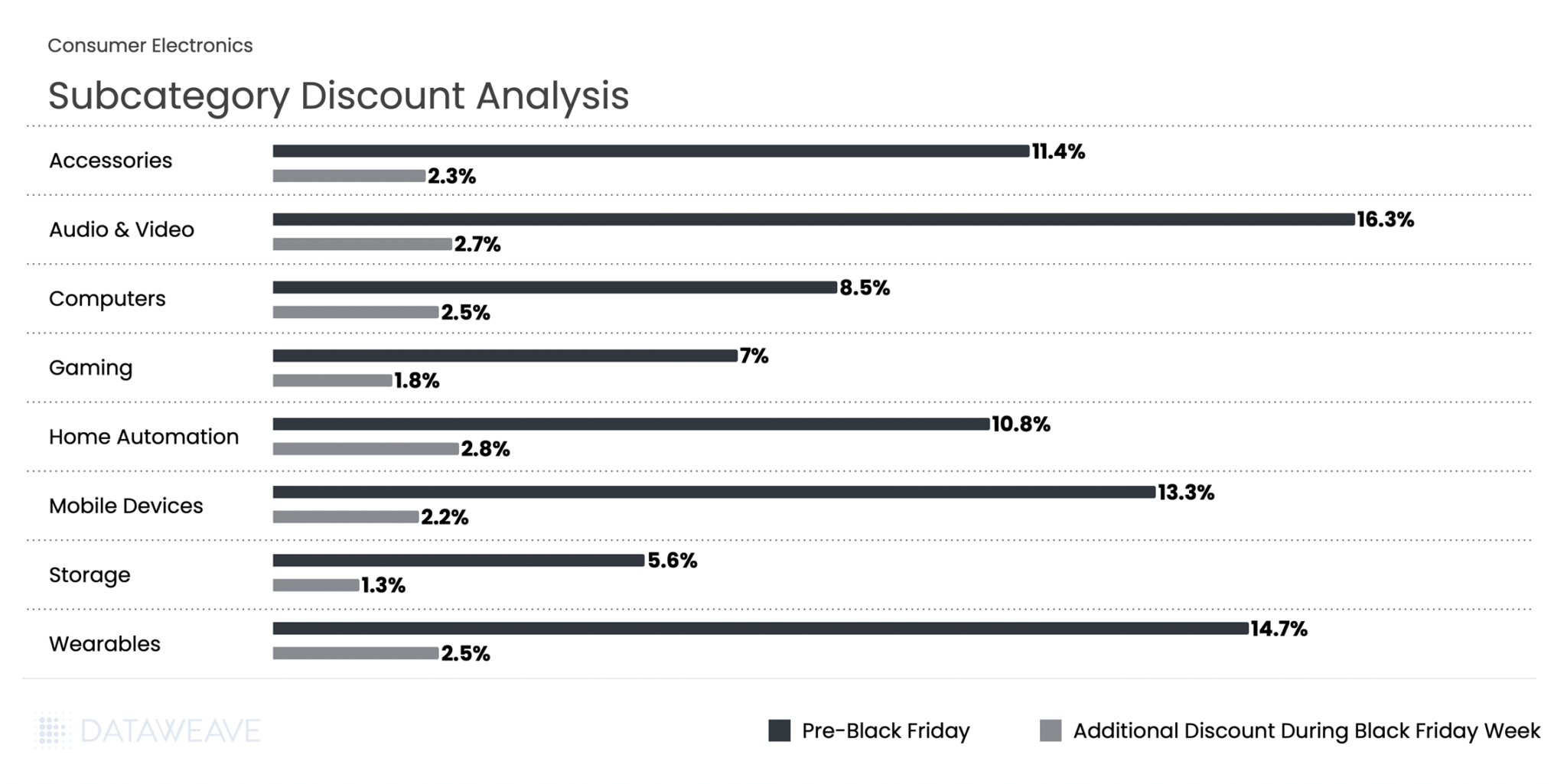

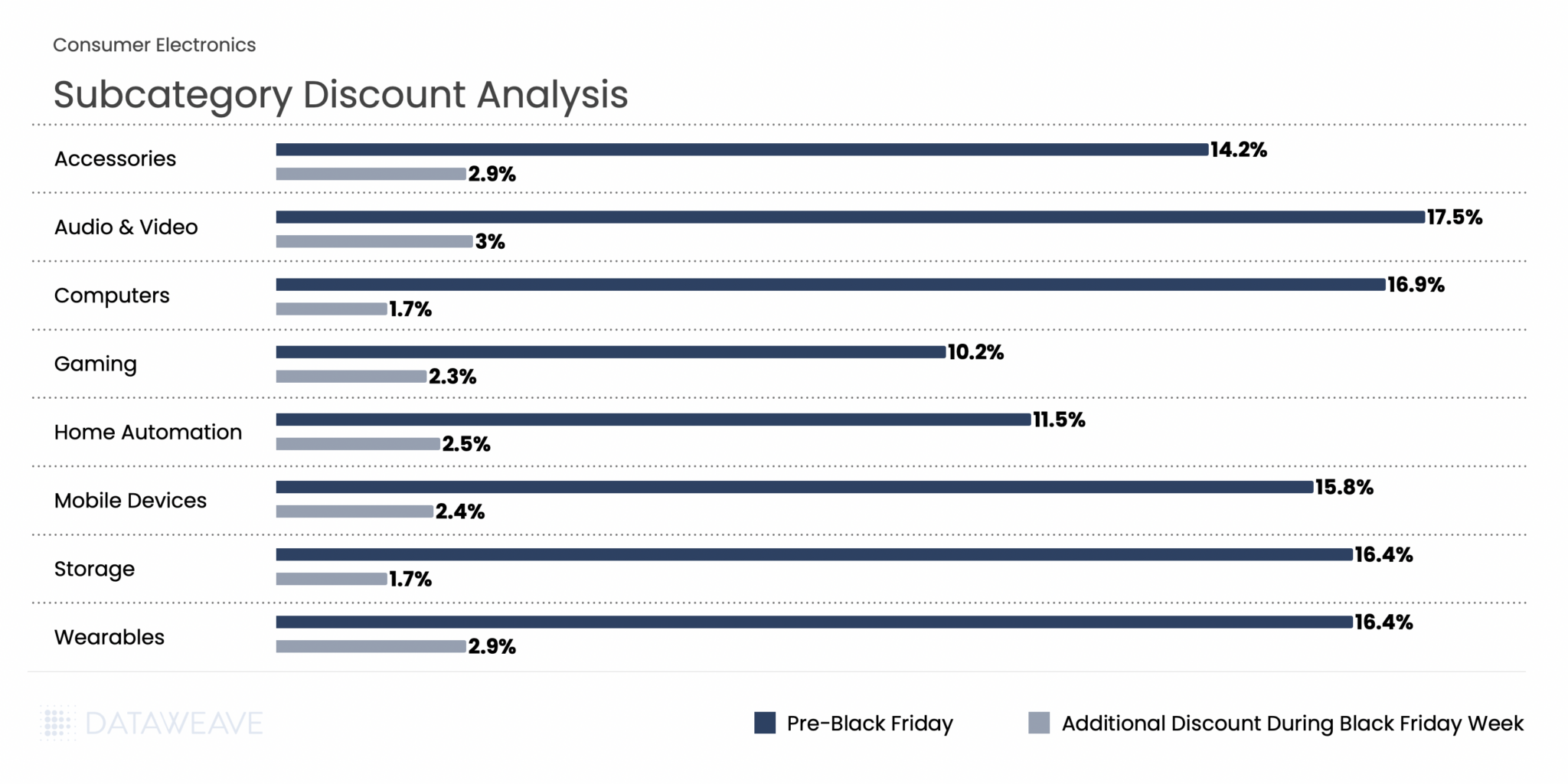

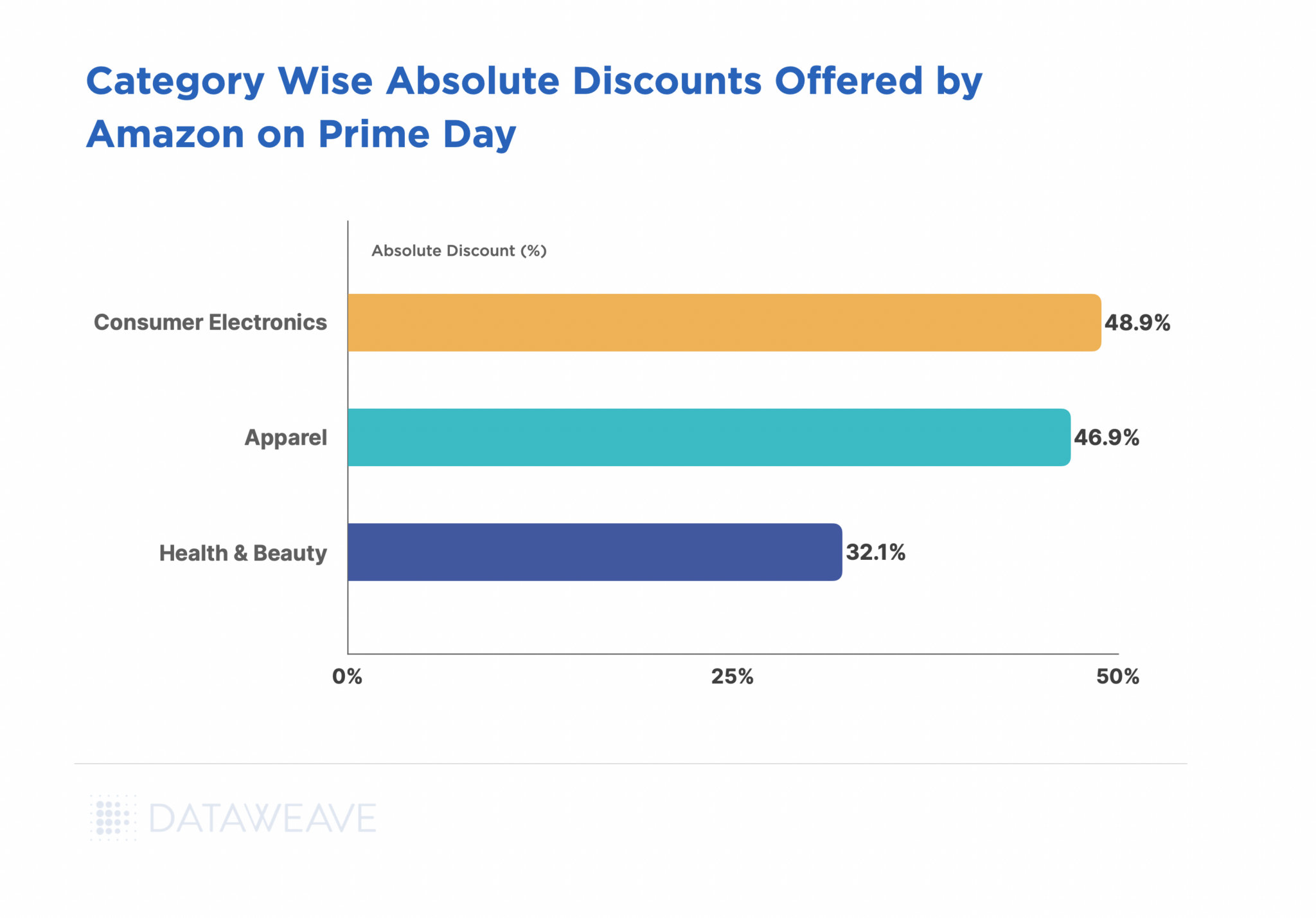

Consumer Electronics

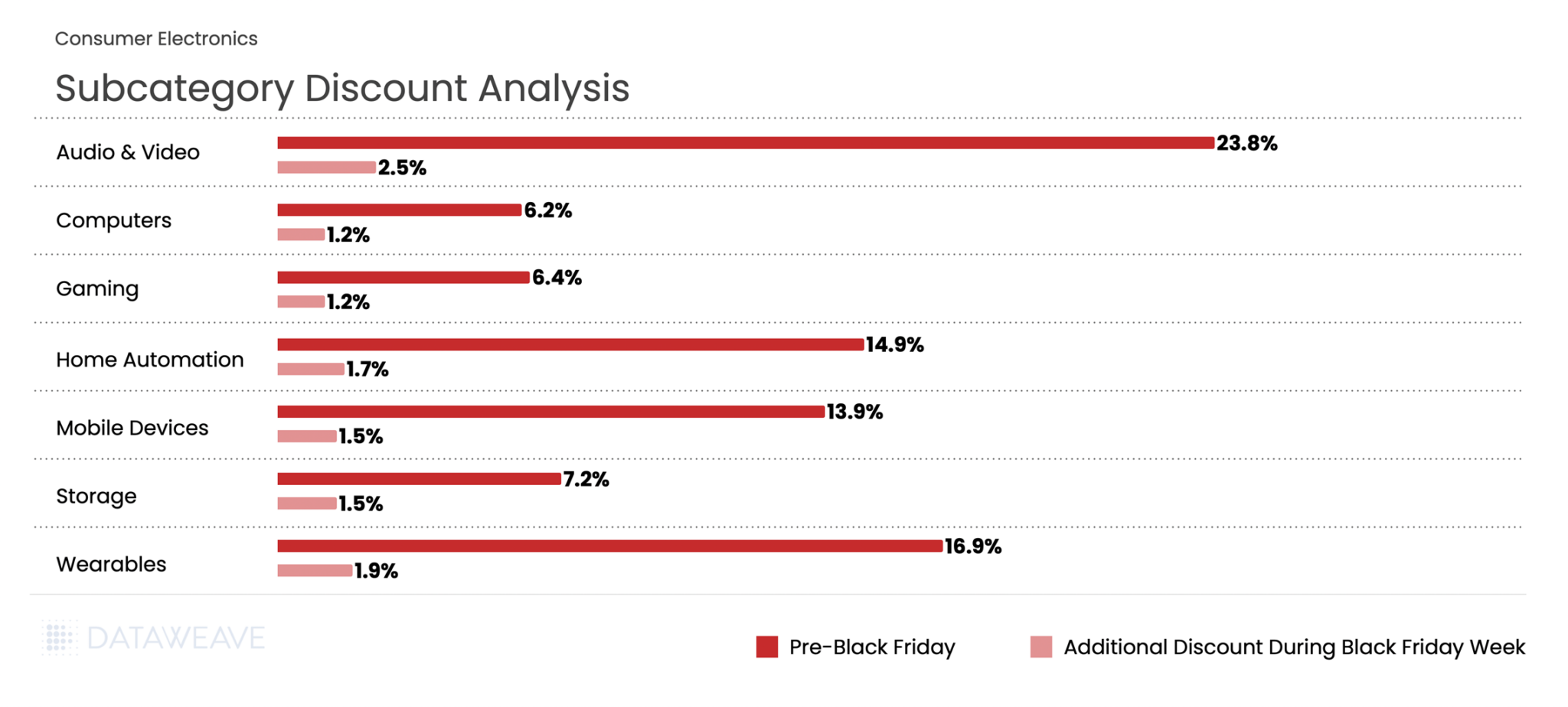

Consumer electronics consistently drives Black Friday traffic, and Canadian retailers delivered compelling early-season value. Our analysis of 11,772 SKUs reveals nuanced subcategory performance.

Subcategory Discount Breakdown

Consumer Electronics averaged 13.6% discounts in the Pre-Black Friday period, with Black Friday Week adding 1.7%. Audio & Video dominated early promotional activity at 23.8%, signalling retailers’ intent to clear inventory ahead of the main event. Wearables followed at 16.9%, likely timed to capture gift-buying momentum.

During Black Friday Week, Audio & Video maintained leadership with an additional 2.5% discount, the highest incremental lift in the category. Meanwhile, Computers and Gaming, already positioned at modest pre-sale discounts of 6.2% and 6.4%, saw minimal additional movement, suggesting constrained inventory or deliberate pricing discipline in these segments.

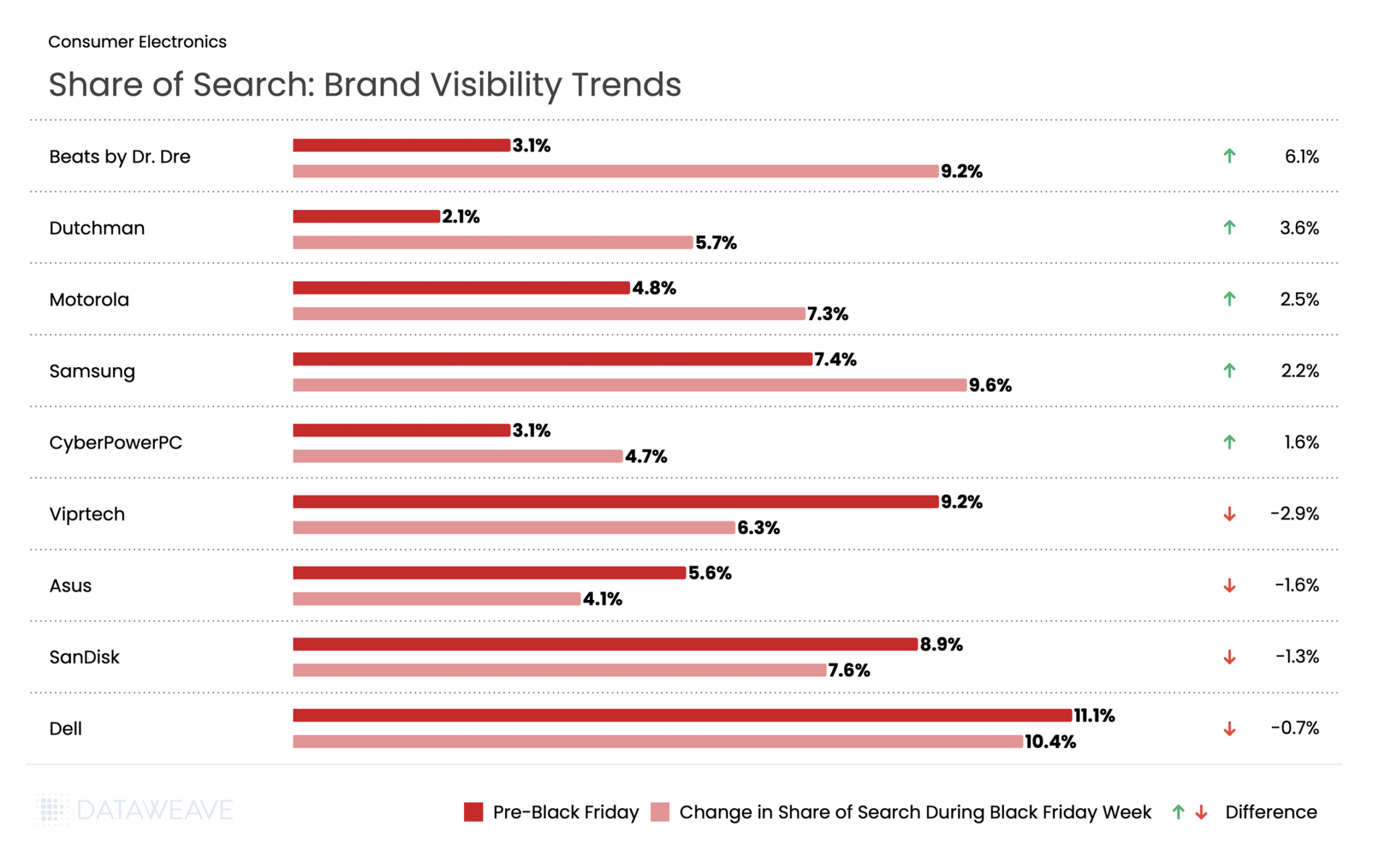

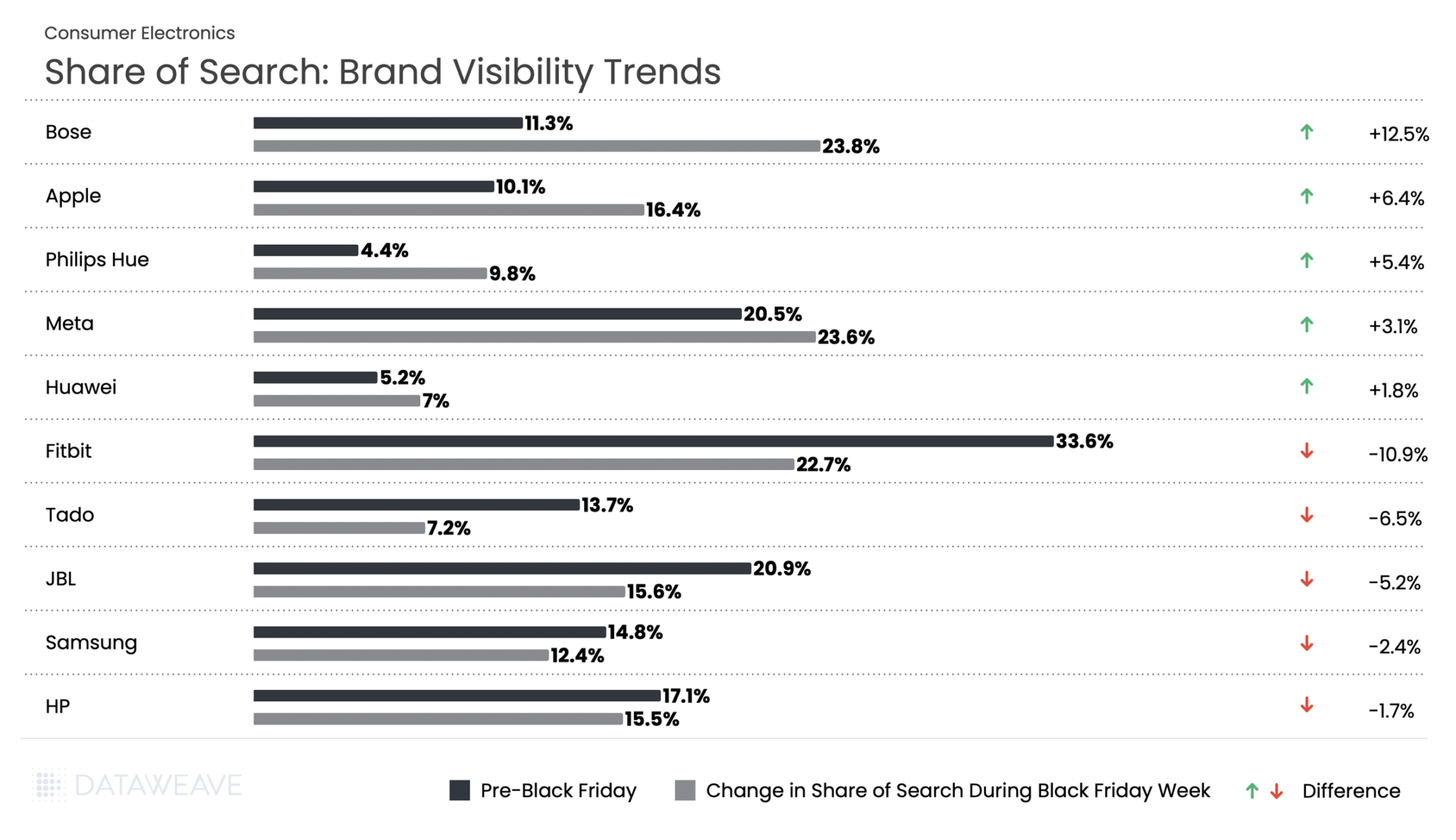

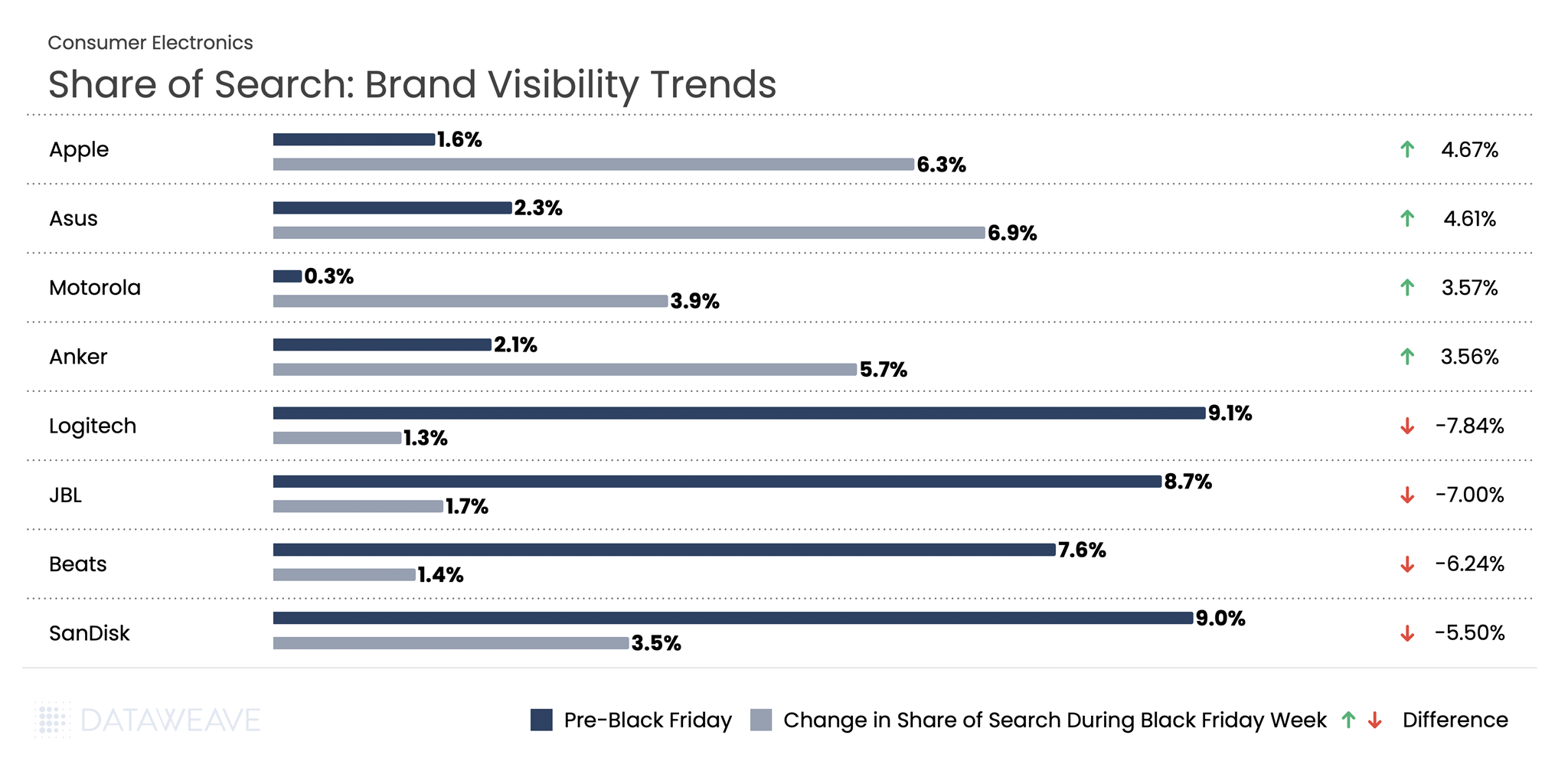

Share of Search: Brand Visibility Trends

Our Share of Search data reveals which brands gained or lost prominence during Black Friday Week:

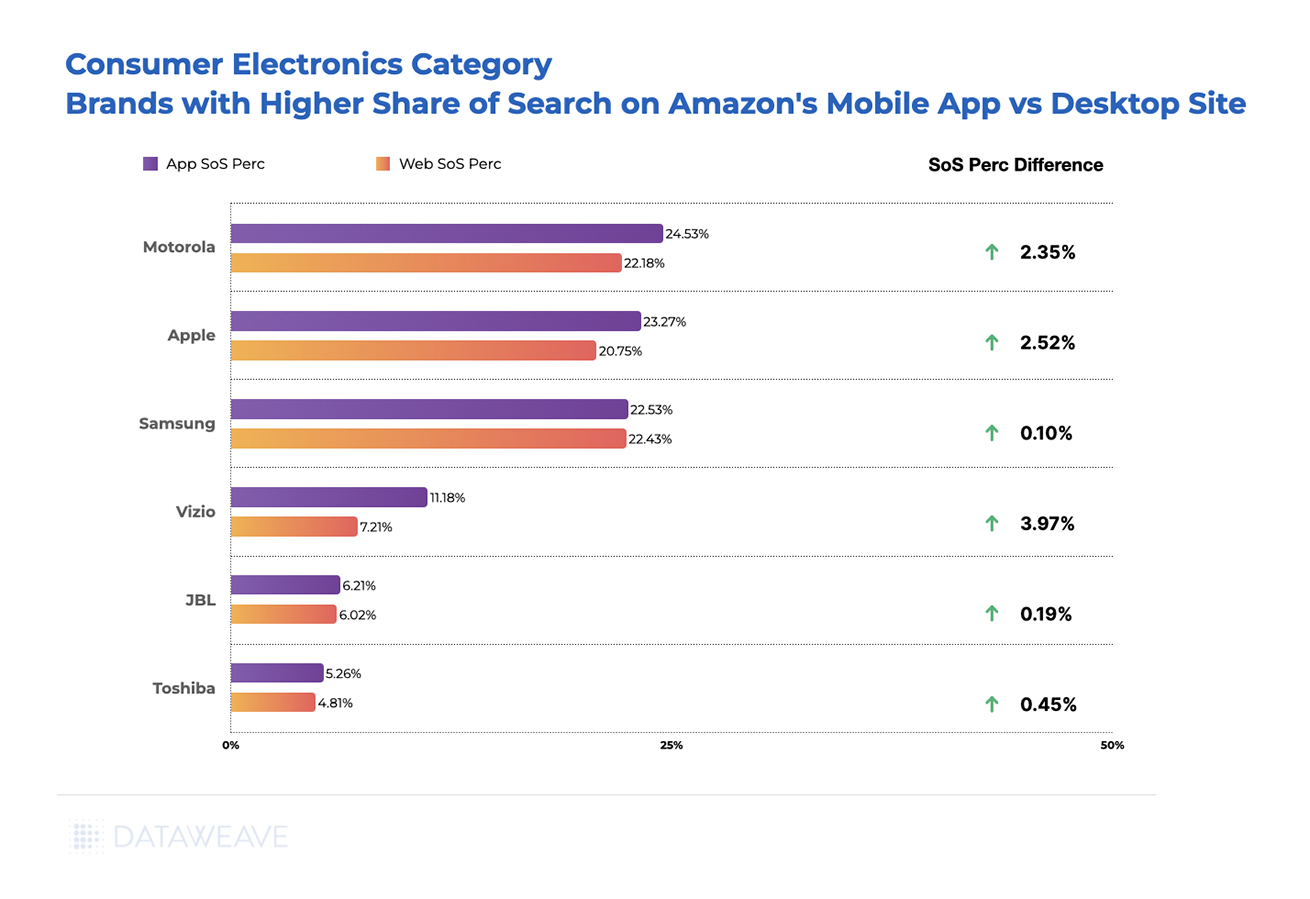

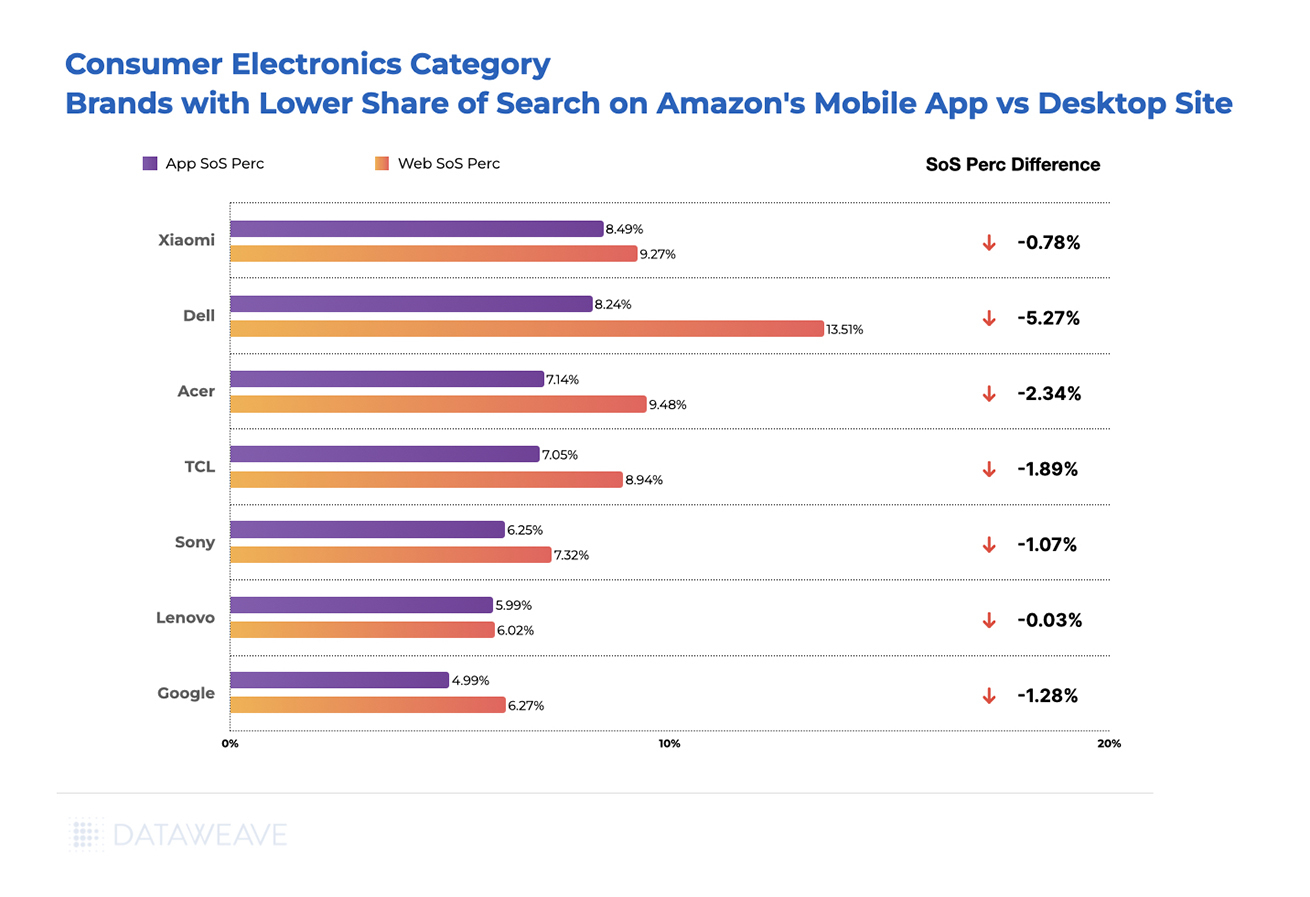

Audio brands dominated visibility gains during Black Friday Week. Beats by Dr. Dre nearly tripled its Share of Search from 3.1% to 9.2%, showing the strongest gains. Visibility for Dutchman climbed 3.6%. Motorola and Samsung also captured increased search prominence with gains of 2.5% and 2.2% respectively.

Conversely, some established tech brands experienced visibility declines. Gaming brand Viprtech by 2.9%. Asus declined by 1.6%, and SanDisk dropped by 1.3%.

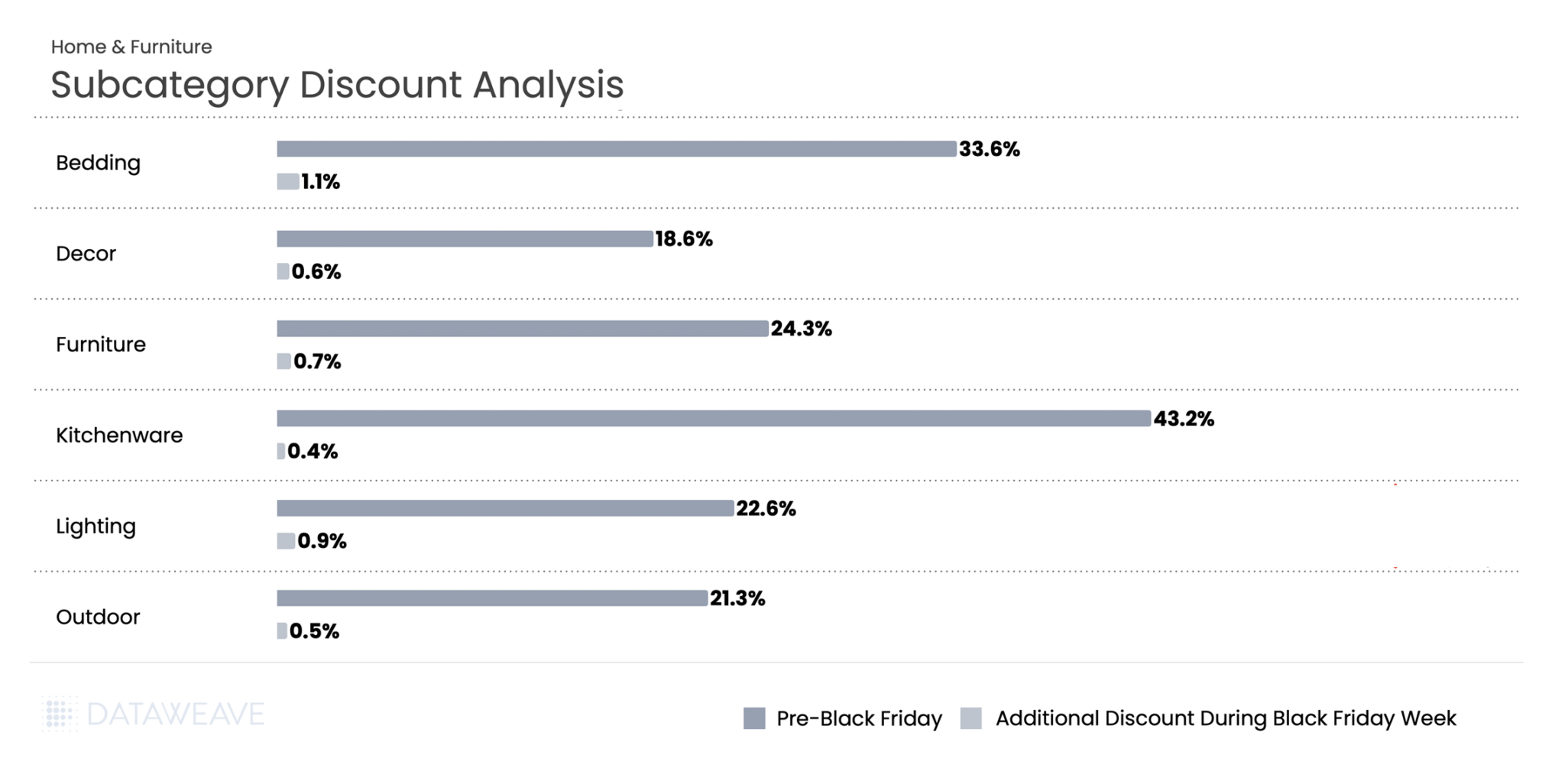

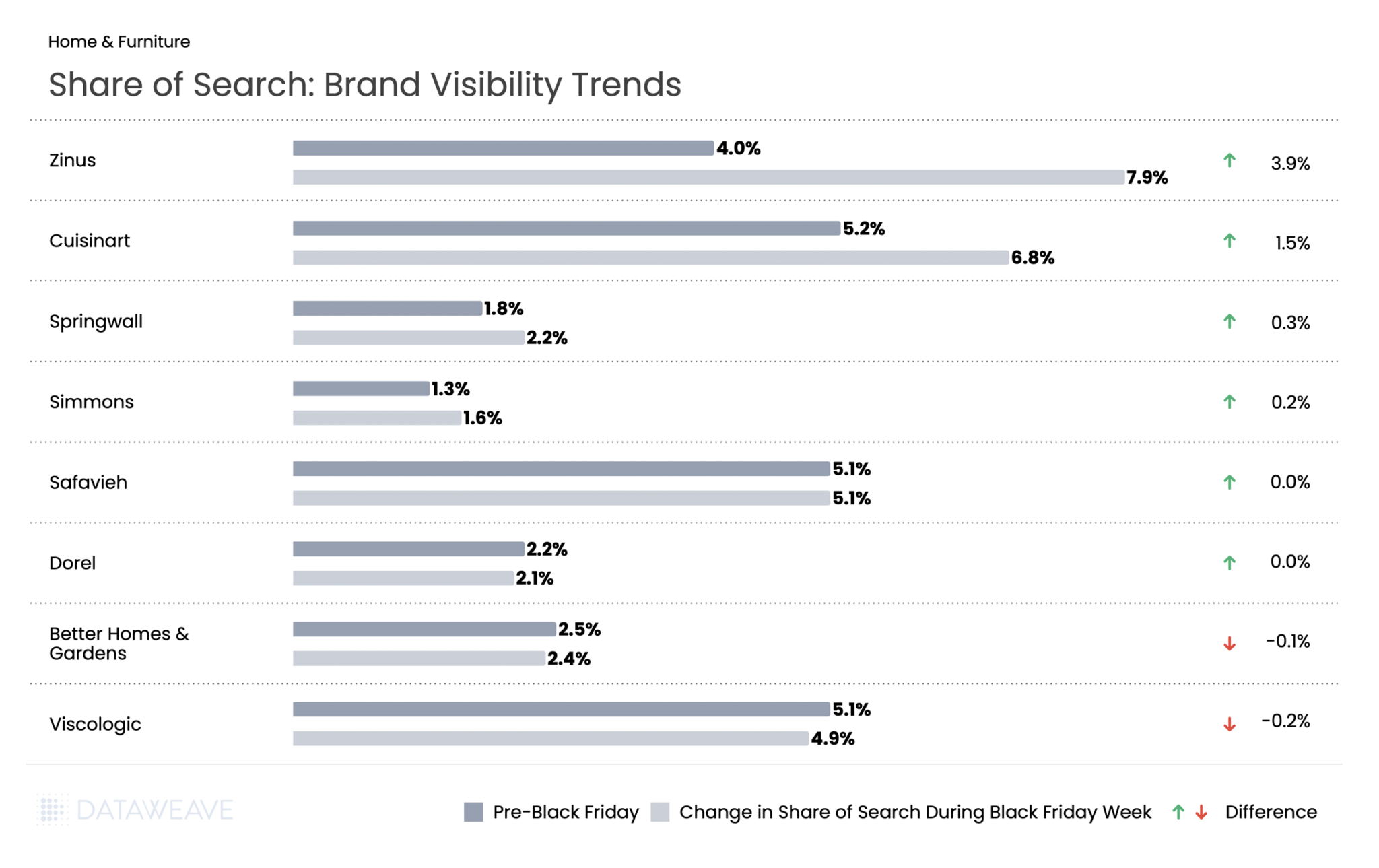

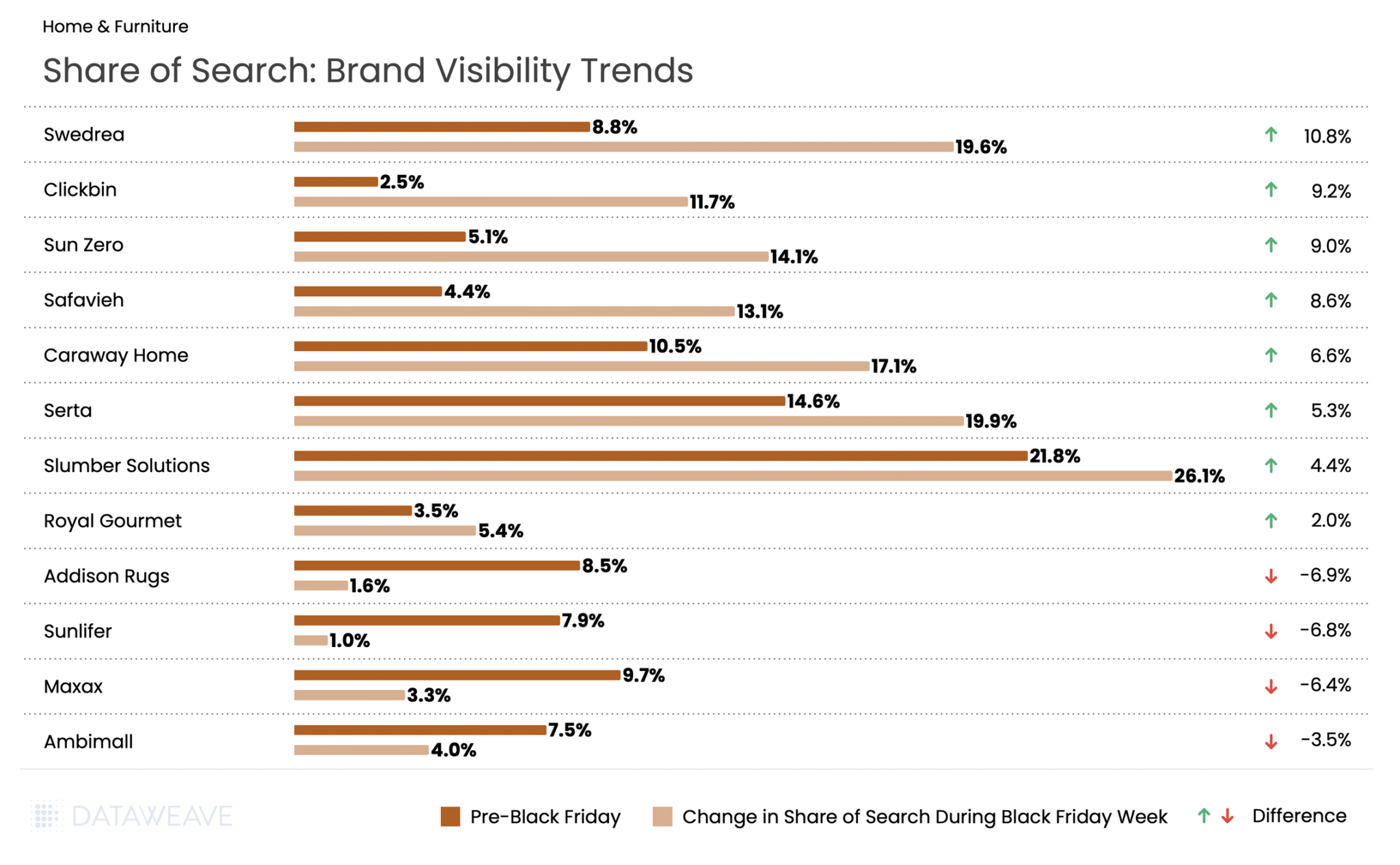

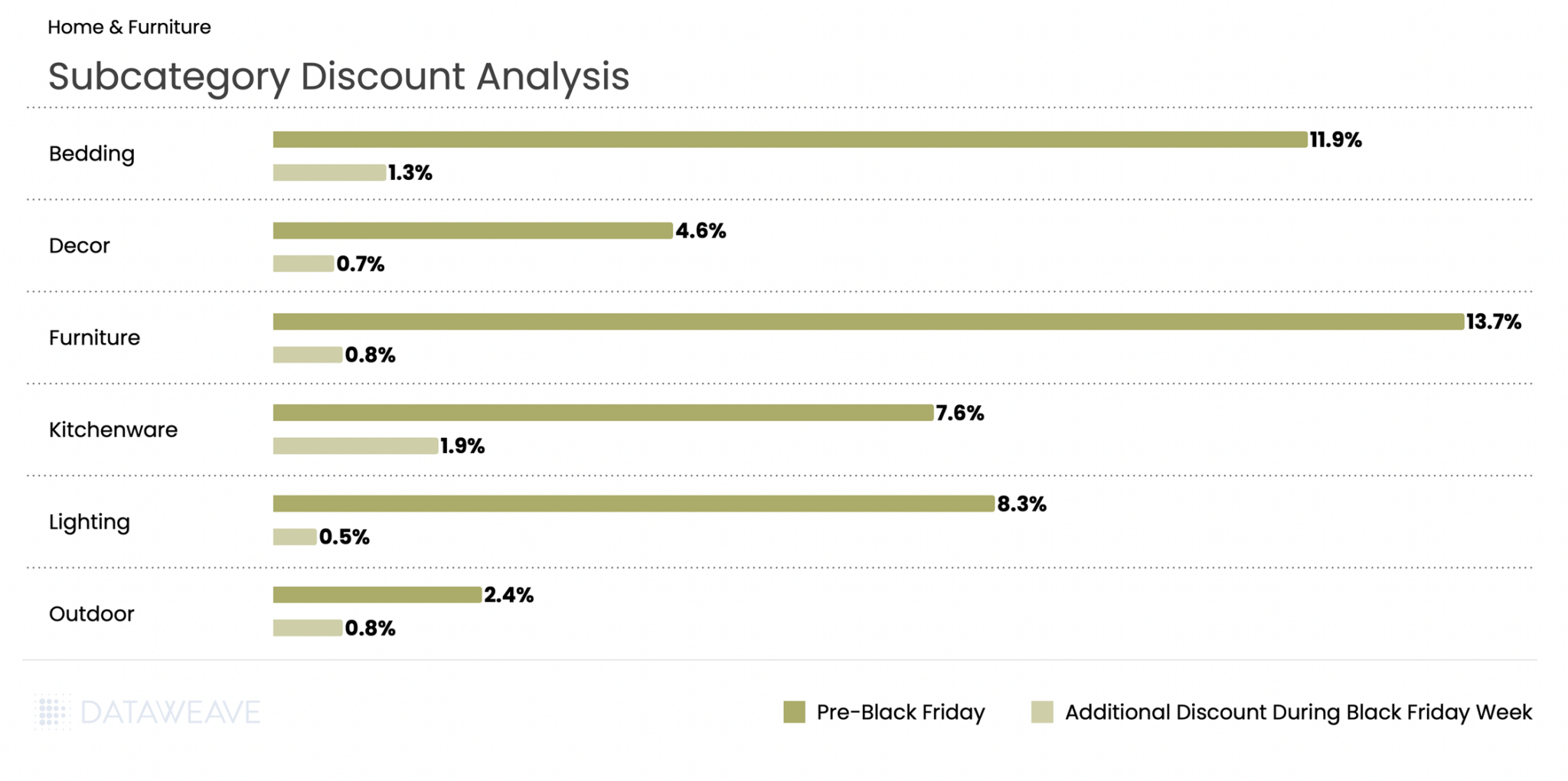

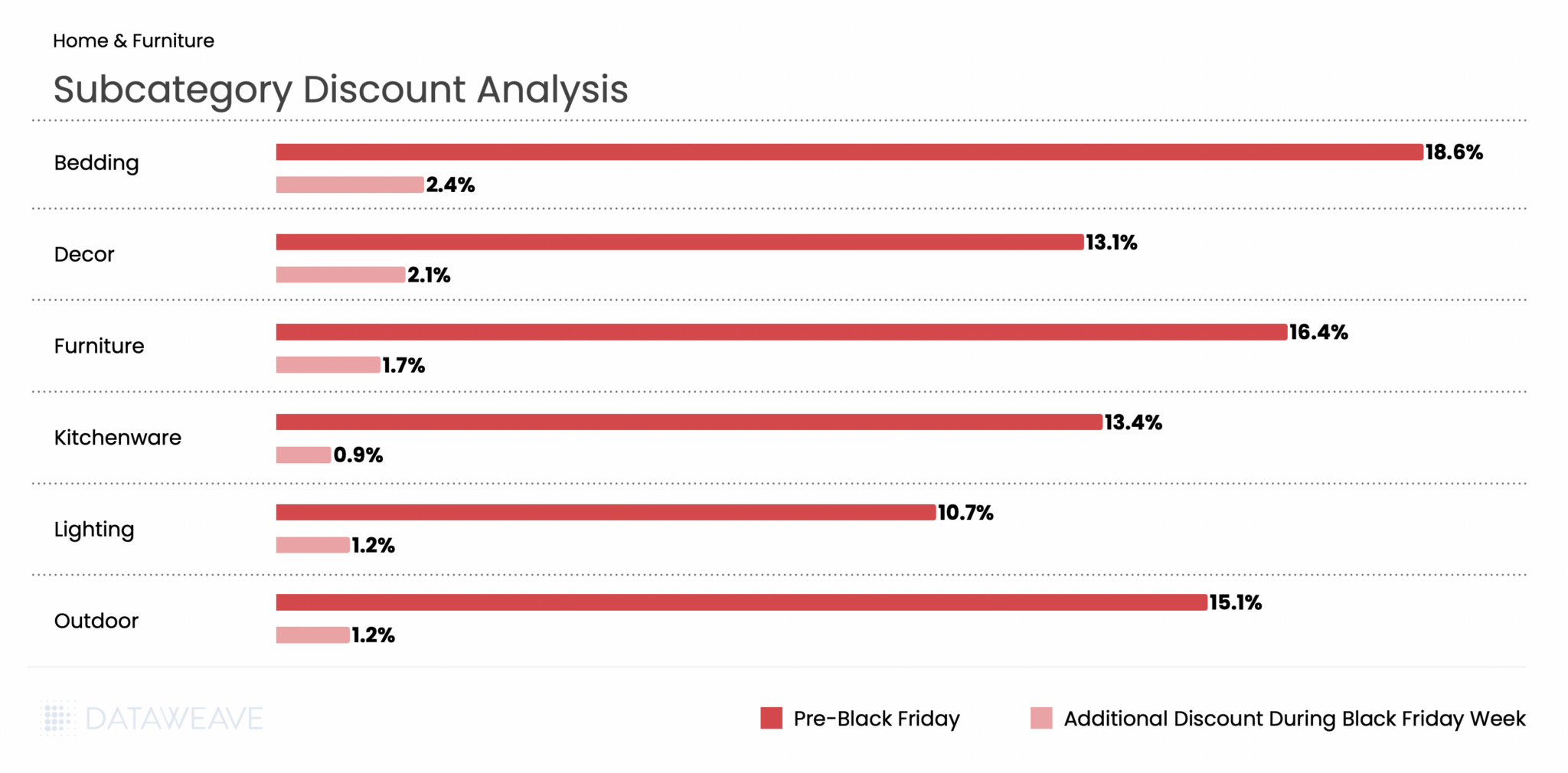

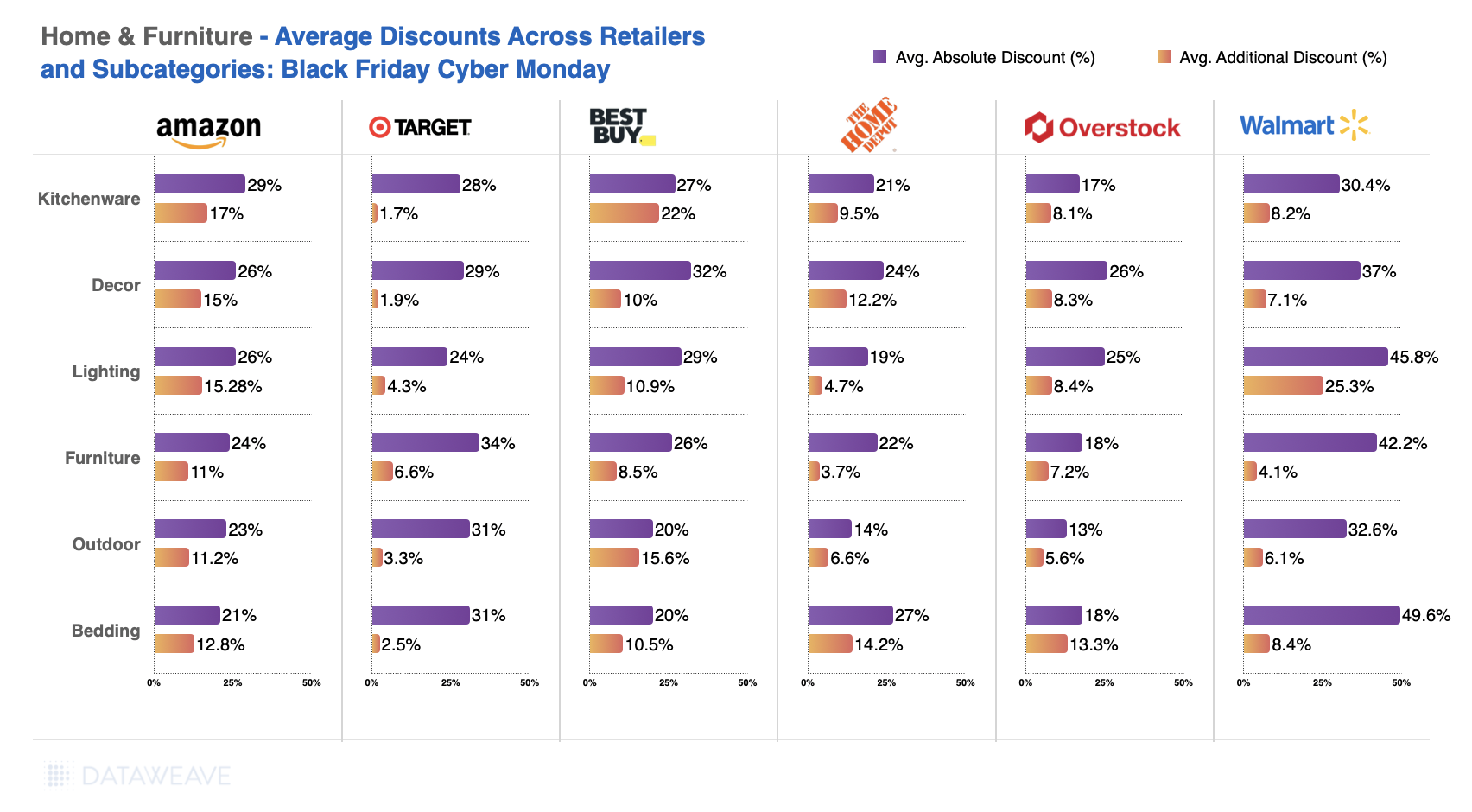

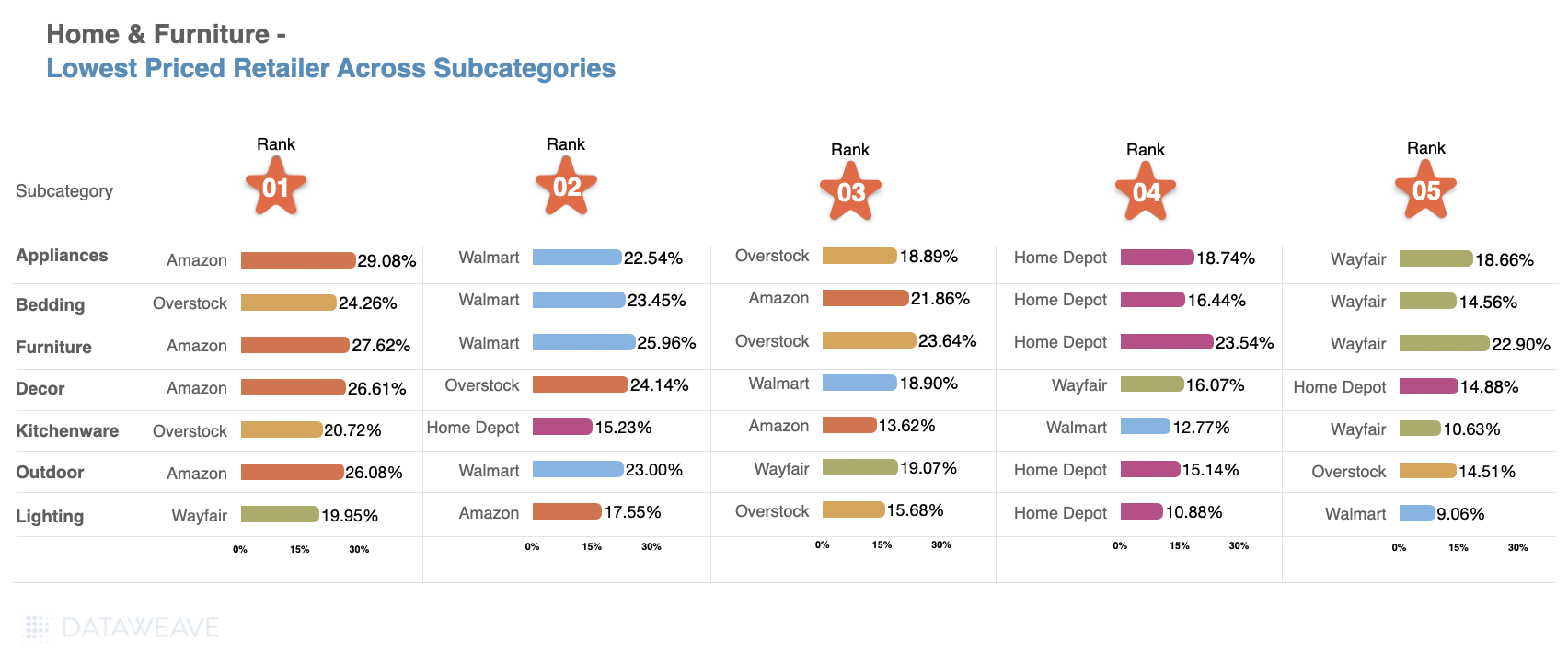

Home & Furniture

Home & Furniture showed the most aggressive early discounting of any category in our Canadian analysis. Tracking 4,362 SKUs, we found retailers heavily promoted home goods well before Black Friday weekend.

Subcategory Discount Breakdown

Home & Furniture led all categories with Pre-Black Friday discounts averaging 23.5%, but Black Friday Week added only 0.7%, the smallest incremental discount in our entire study. Kitchenware saw extraordinary pre-sale discounts of 43.2%, the highest in any subcategory we tracked. Bedding followed at 33.6%, while Furniture reached 24.3%. These deep early discounts likely aimed to drive early conversions and manage bulky inventory ahead of peak logistics constraints.

During Black Friday Week, additional discounting remained minimal across the board. Bedding posted the highest lift at 1.1%, while Kitchenware saw just 0.4%. The data suggests Canadian home goods retailers viewed the pre-sale period as their primary promotional window, with Black Friday serving more to sustain momentum than deliver new value.

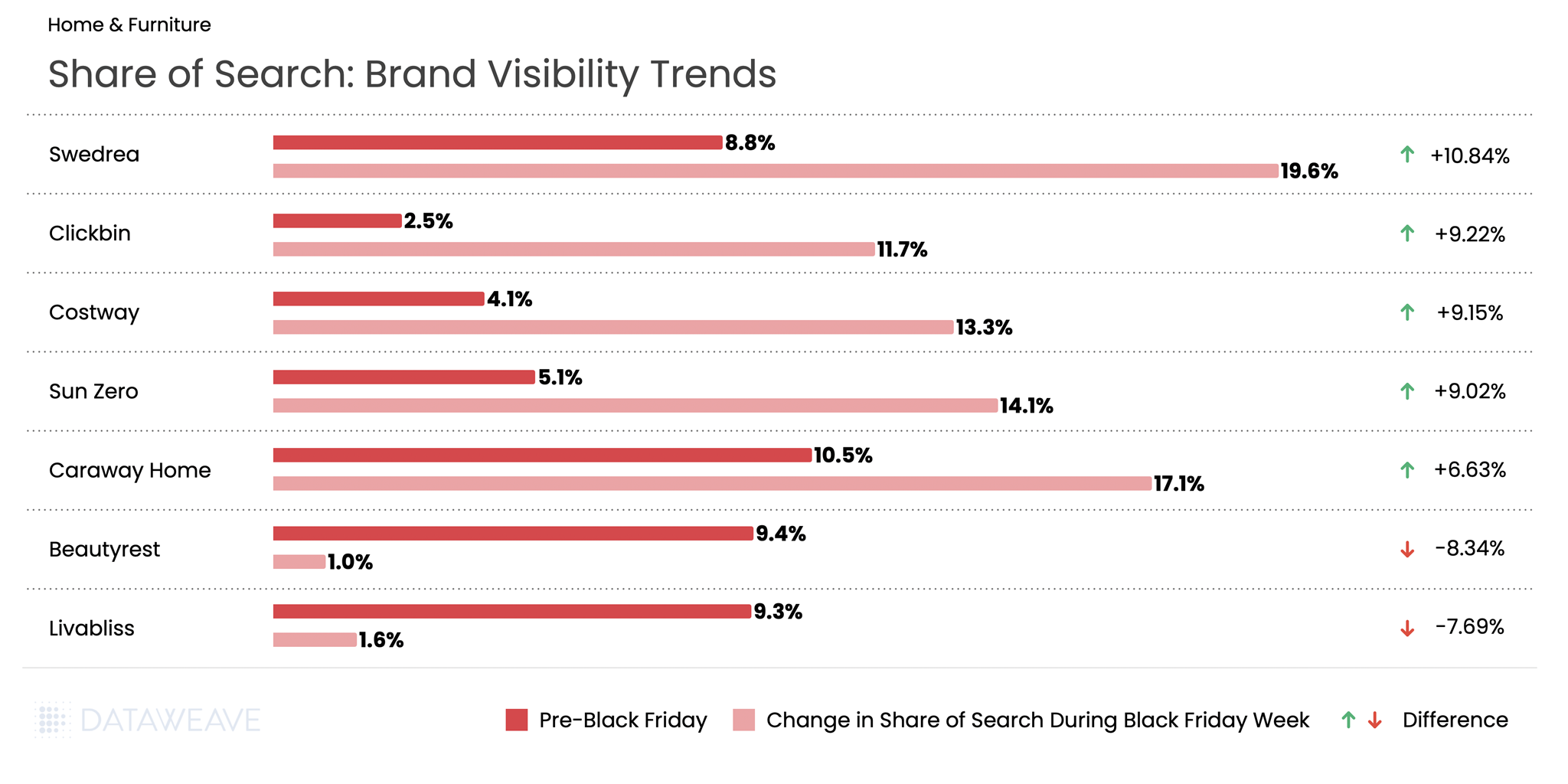

Share of Search: Brand Visibility Trends

Mattress brand Zinus led gains with a 3.9% increase, positioning itself as a value-focused furniture leader during the sale period. Cuisinart climbed by 1.5%, suggesting strategic amplification of this established kitchenware brand.

Most home brands maintained relatively stable visibility throughout the sale period. Safavieh and Dorel showed essentially no change, while Better Homes & Gardens and Viscologic experienced only minor declines of 0.1% and 0.2% respectively.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Check out our coverage on Black Friday 2025 across US, UK, and Germany. Follow our blog for more insights on retail pricing trends, brand visibility analysis, and data-driven commerce intelligence.

Black Friday 2025 solidified its position as a major retail event in the German market. German consumers demonstrated an average Black Friday budget of €317, the highest among select European countries.

The German market, however, exhibited unique consumer behavior patterns during Black Friday 2025. Rather than meticulous planning, 59% of German shoppers allowed deals to inspire their purchases, compared to just 32% who shopped with predetermined lists and budgets. This spontaneous yet budget-conscious approach distinguishes German consumers from other markets, where FOMO-driven purchasing tends to dominate.

Against this backdrop of rational deal-seeking and regional diversity, how did retailers and brands perform across key categories this Black Friday?

At DataWeave, we conducted a comprehensive analysis of Black Friday 2025 discounting trends across five major categories in the German market: Consumer Electronics, Home & Furniture, Health & Beauty, Grocery, and Apparel. Our AI-powered pricing intelligence platform monitored over 16,000+ SKUs across leading German retailers like Amazon, Aldi, Douglas, Nutritienda, Carethy, Bofrost, and more, revealing fascinating patterns in how retailers and brands approached this year’s sale season.

Our Methodology

For this analysis, DataWeave monitored average discounts across leading German retailers during two distinct periods:

Pre-Black Friday: November 6 – November 23, 2025 – capturing early holiday deals and baseline pricing

Additional Discounts During Black Friday Week: November 24 – December 1, 2025 – covering Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

Our sample encompassed the top-ranked products across subcategories on major retail sites. We also analyzed Share of Search data, which measures brand visibility by monitoring which brand names appear in the top 20 search results for critical keywords.

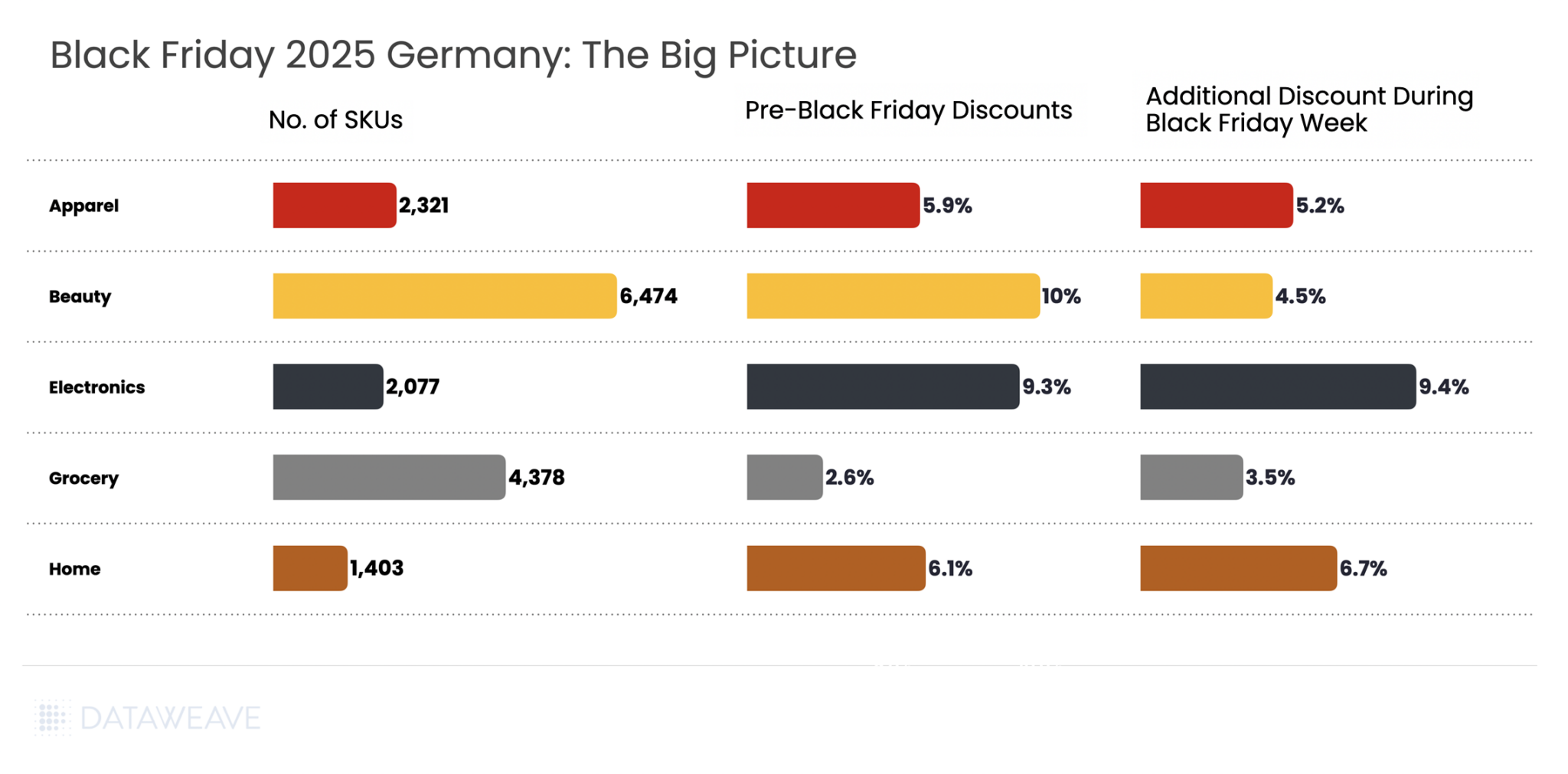

Black Friday 2025 Germany: The Big Picture

Our analysis covered 16,653 SKUs across five major categories. Here’s the snapshot of average discounts during the Pre-Black Friday period compared to Black Friday Week:

Key Insight: The German market presented a notably different discounting pattern compared to other markets. Pre-Black Friday discounts averaged 7% across all categories, with Black Friday Week adding 5.1% on average. Unlike the UK and US markets where retailers front-loaded promotions heavily, German retailers took a more balanced approach, with several categories actually seeing higher discounts during the main Black Friday Week.

Beauty led pre-sale discounts at 10%, followed by Electronics at 9.3%. Consumer electronics stood out with the highest Black Friday Week discounts at 9.4%, slightly exceeding even the pre-sale period at 9.3%.

Shopping Behavior Patterns: The relatively modest discount levels reflect the rational, value-oriented approach of German consumers. With the majority of shoppers setting budgets between €100-€299 and prioritizing wish fulfillment over impulse purchases, German retailers focused on strategic discounting rather than aggressive margin erosion.

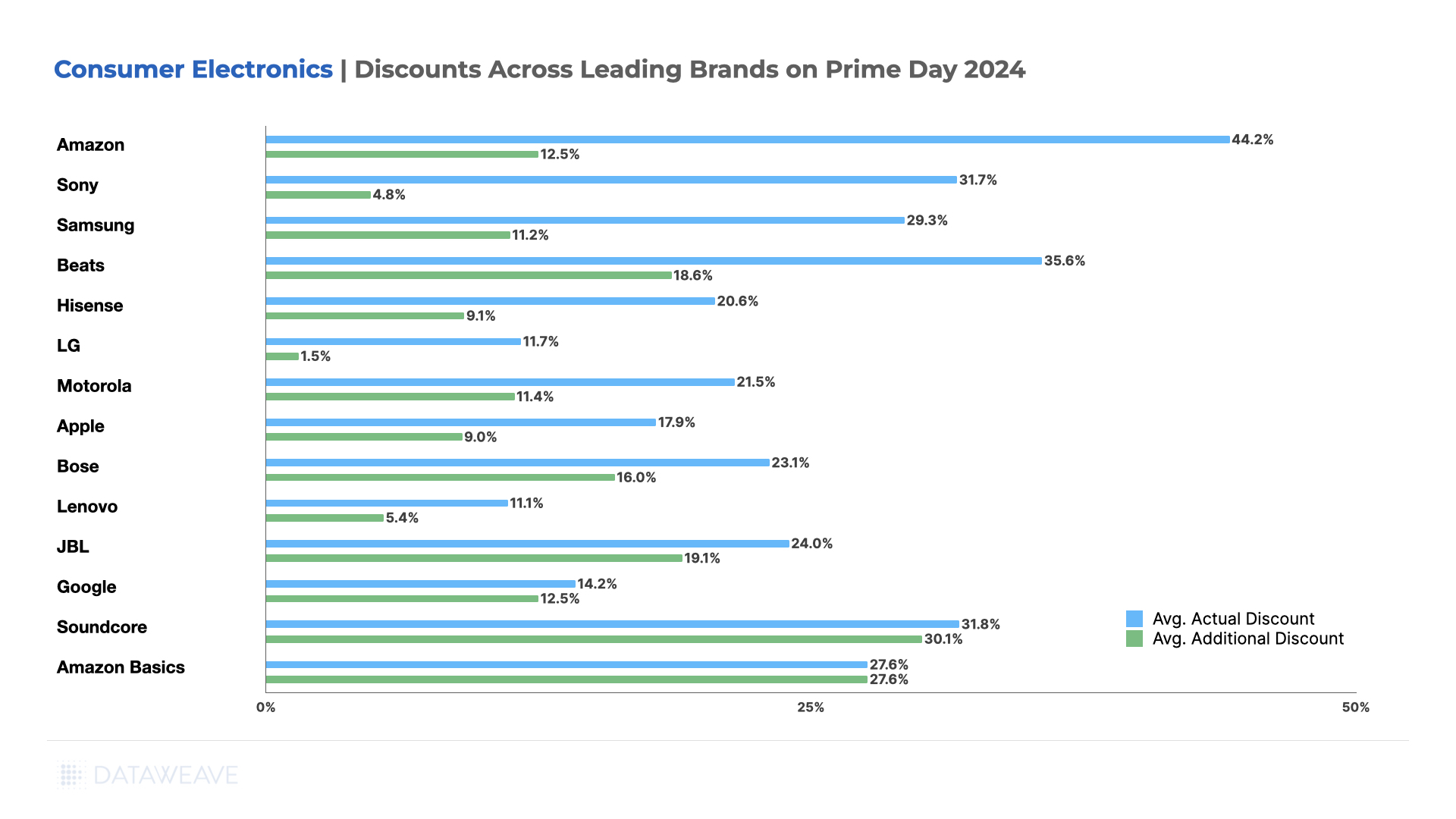

Consumer Electronics

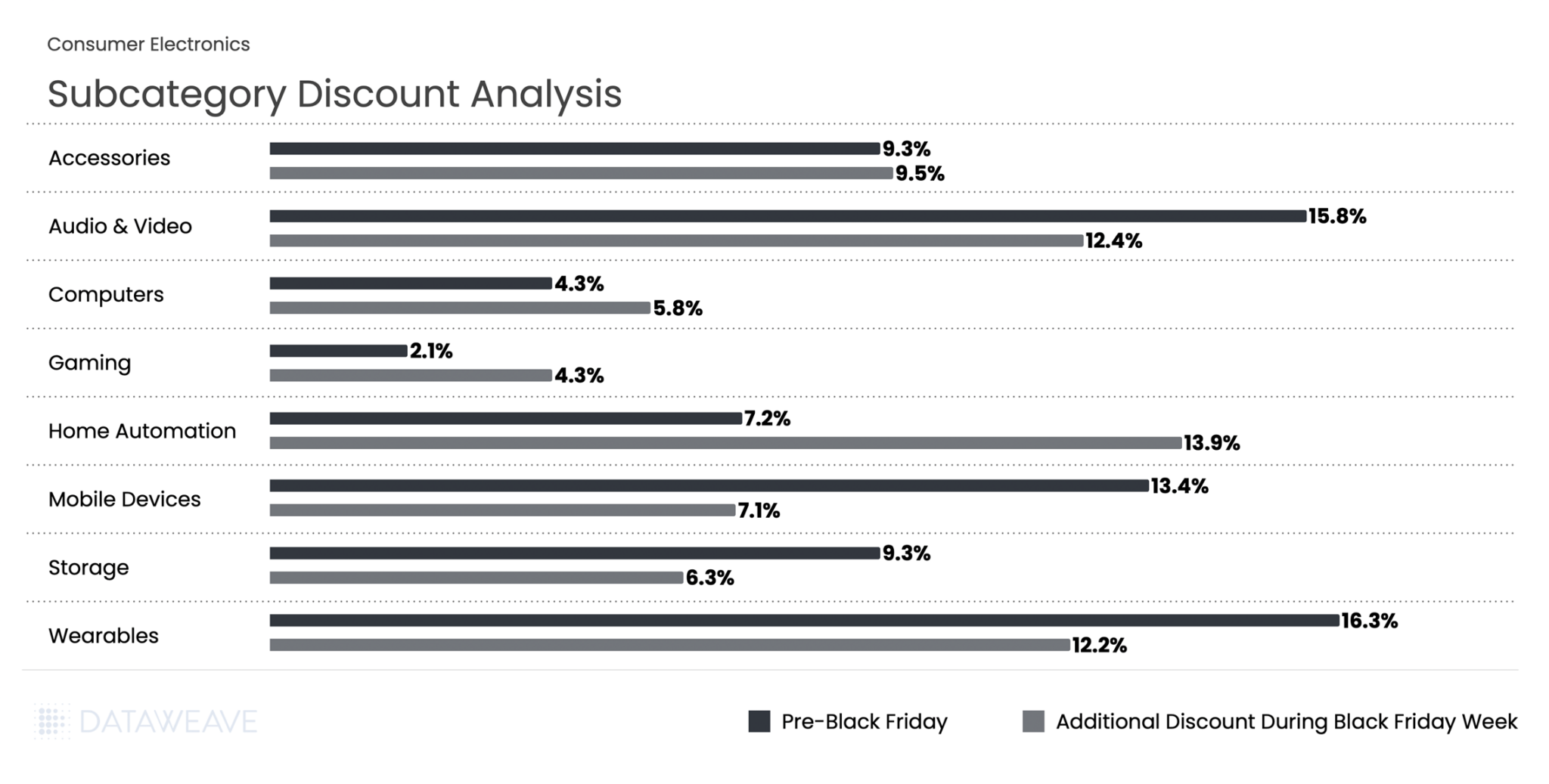

Consumer electronics dominated German Black Friday interest, with 77% of German shoppers most interested in electronics deals, making it the most anticipated category during the sales period. Our analysis of 2,077 SKUs reveals how discounts varied across subcategories and which brands dominated search visibility in this highly competitive category.

Subcategory Discount Analysis

This was one of the few categories where Black Friday Week discounts matched or exceeded pre-sale levels. Wearables led pre-sale discounting at 16.3%, followed closely by Audio & Video at 15.8%. During Black Friday Week, these categories saw additional discounts of 12.2% and 12.4% respectively.

The standout performer was Home Automation, which nearly doubled its additional discount from 7.2% to 13.9% during Black Friday Week. Mobile Devices saw additional discounts dropping from 13.4% pre-sale to 7.1% during Black Friday Week. Meanwhile Gaming doubled additional discounting from 2.1% to 4.3%.

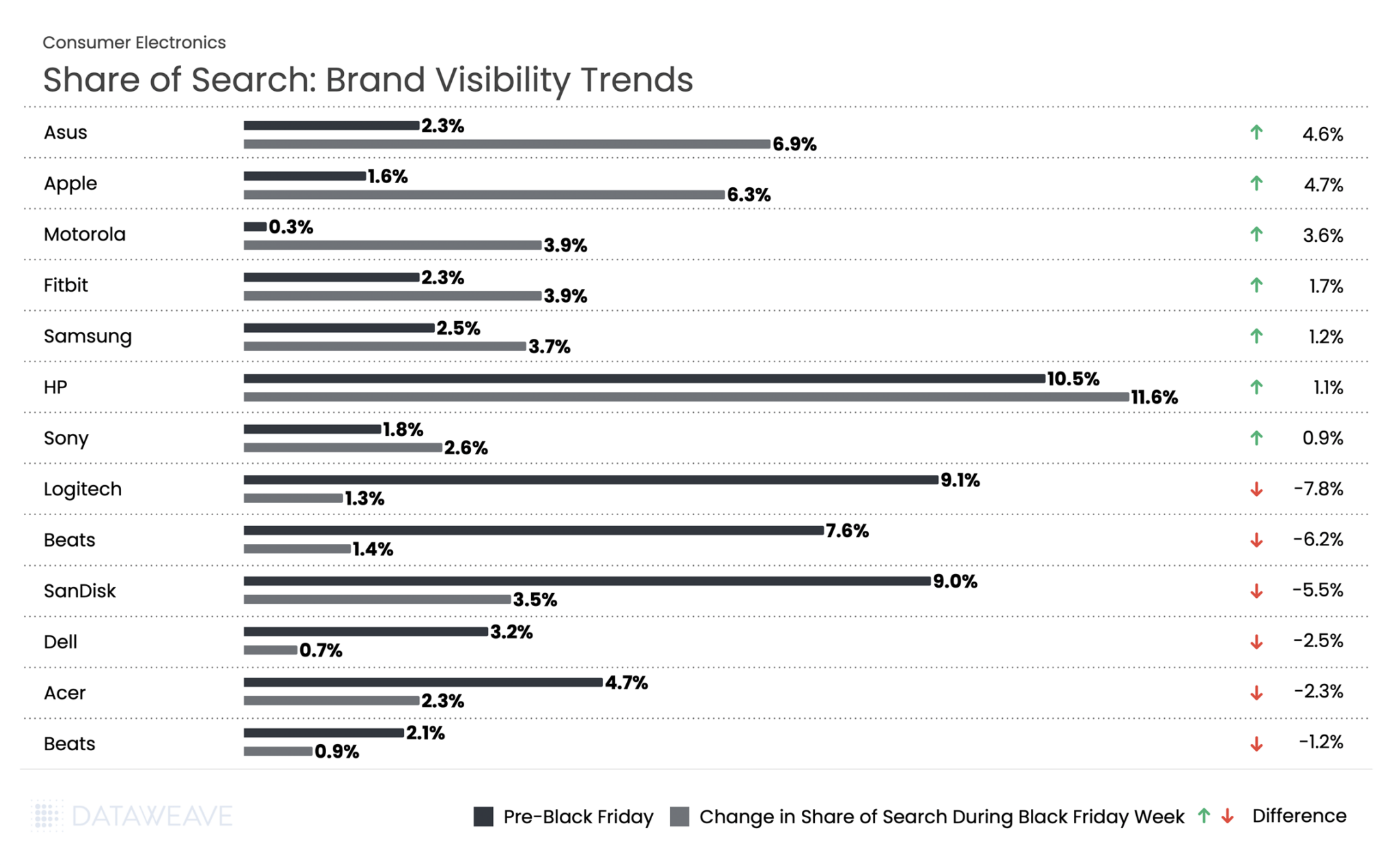

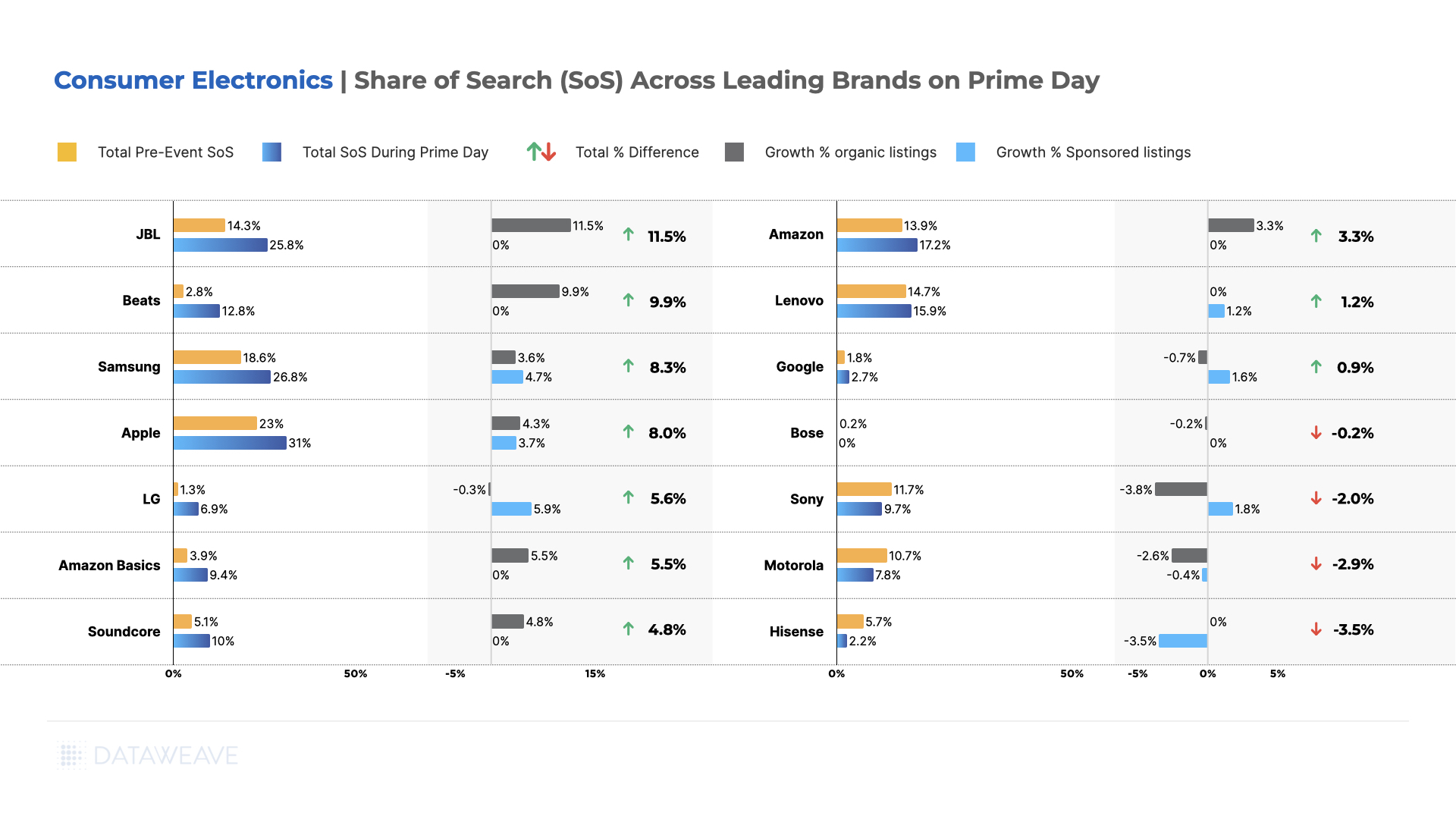

Share of Search: Brand Visibility Trends

Our Share of Search analysis reveals significant shifts in brand visibility during Black Friday Week:

HP saw the highest share of search across Black Friday at 10.5% pre event and 11.6% during the event. Apple led with a 4.7% increase in visibility, jumping from 1.6% to 6.3%. Asus followed at 4.6%. Motorola surged 3.6 %, while wearables brand Fitbit gained 1.7%.

In stark contrast, Logitech dropped by 7.8 %, Beats fell 6.2 %, and SanDisk declined 5.5 %. Computer manufacturers Dell and Acer also struggled, falling 2.5 and 2.3 % respectively.

Home & Furniture

The Home & Furniture category in Germany showed unique discounting behavior compared to other markets, with additional Black Friday Week discounts (6.7%) actually exceeding Pre-Black Friday levels (6.1%). Our analysis of 1,403 SKUs shows how discounts were distributed across subcategories.

Subcategory Discount Analysis

Kitchenware led pre-sale discounts at 8.7%. Decor surged from 5% to 7.5%, lighting jumped from 5% to 6.9%, and bedding more than doubled from 3.2% to 6.6%. These substantial increases suggest strategic timing to capture consumer attention during peak shopping days.

Share of Search: Brand Visibility Trends

Mattress brand Slumber Solutions saw the highest share of search at 21.8% pre event and 26.1% during Black Friday week. Meanwhile, another mattress brand Swedrea led all brands with a remarkable 10.8% surge in visibility, jumping from 8.8% to 19.6%. Budget-friendly furniture brand Clickbin gained 9.2%, while window treatment brand Sun Zero increased 9% and home textiles brand Safavieh surged 8.6%.

Premium and established brands also performed well: Caraway Home (cookware) rose 6.6%, mattress brand Serta gained 5.3%, and Slumber Solutions added 4.4%. Royal Gourmet, specializing in outdoor cooking equipment, gained 2.0%.

However, several mid-tier brands faced steep declines. Addison Rugs dropped 6.9% from 8.5% to just 1.6%, while Sunlifer fell 6.8 % and Maxax declined 6.4 %.

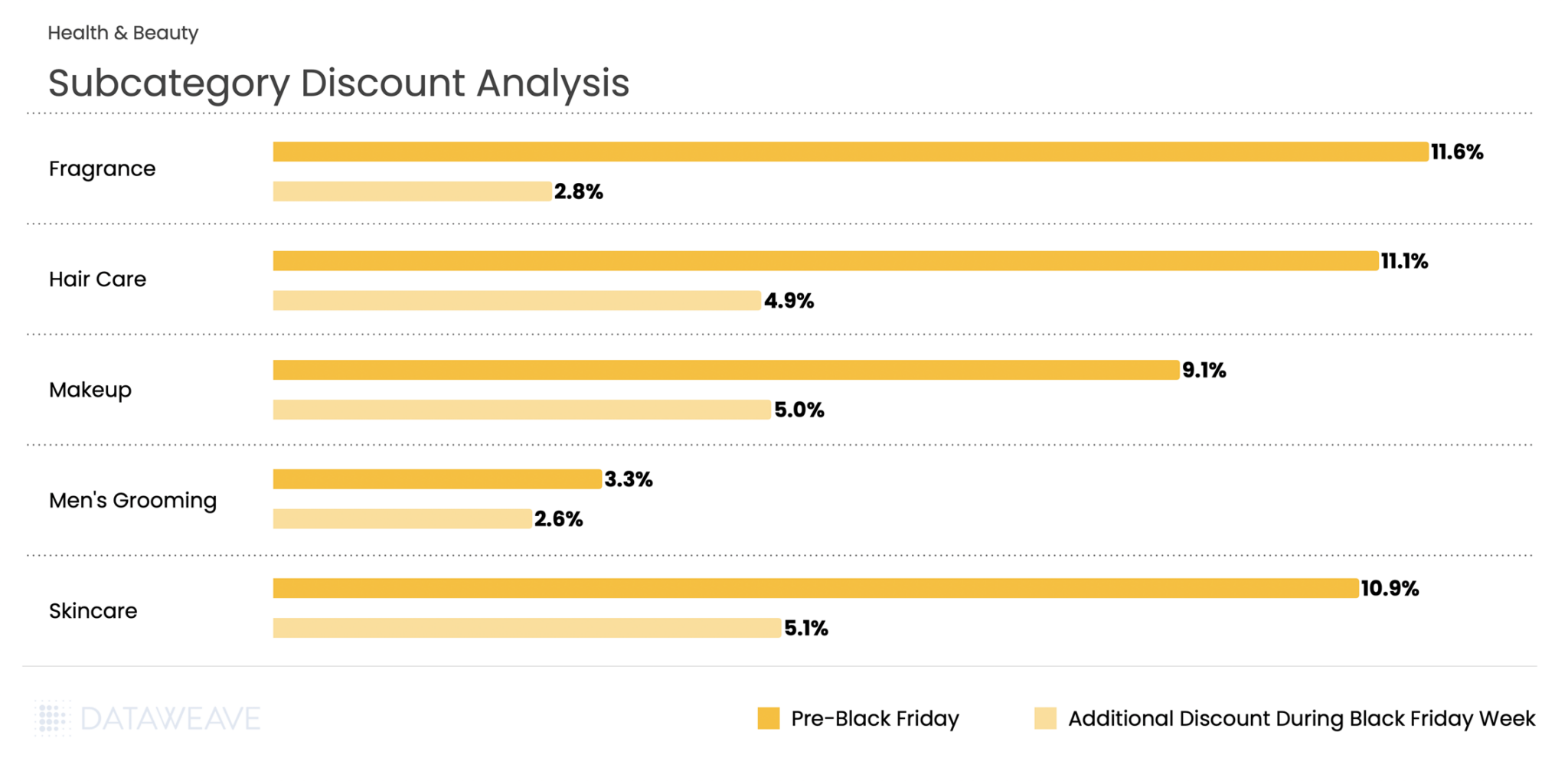

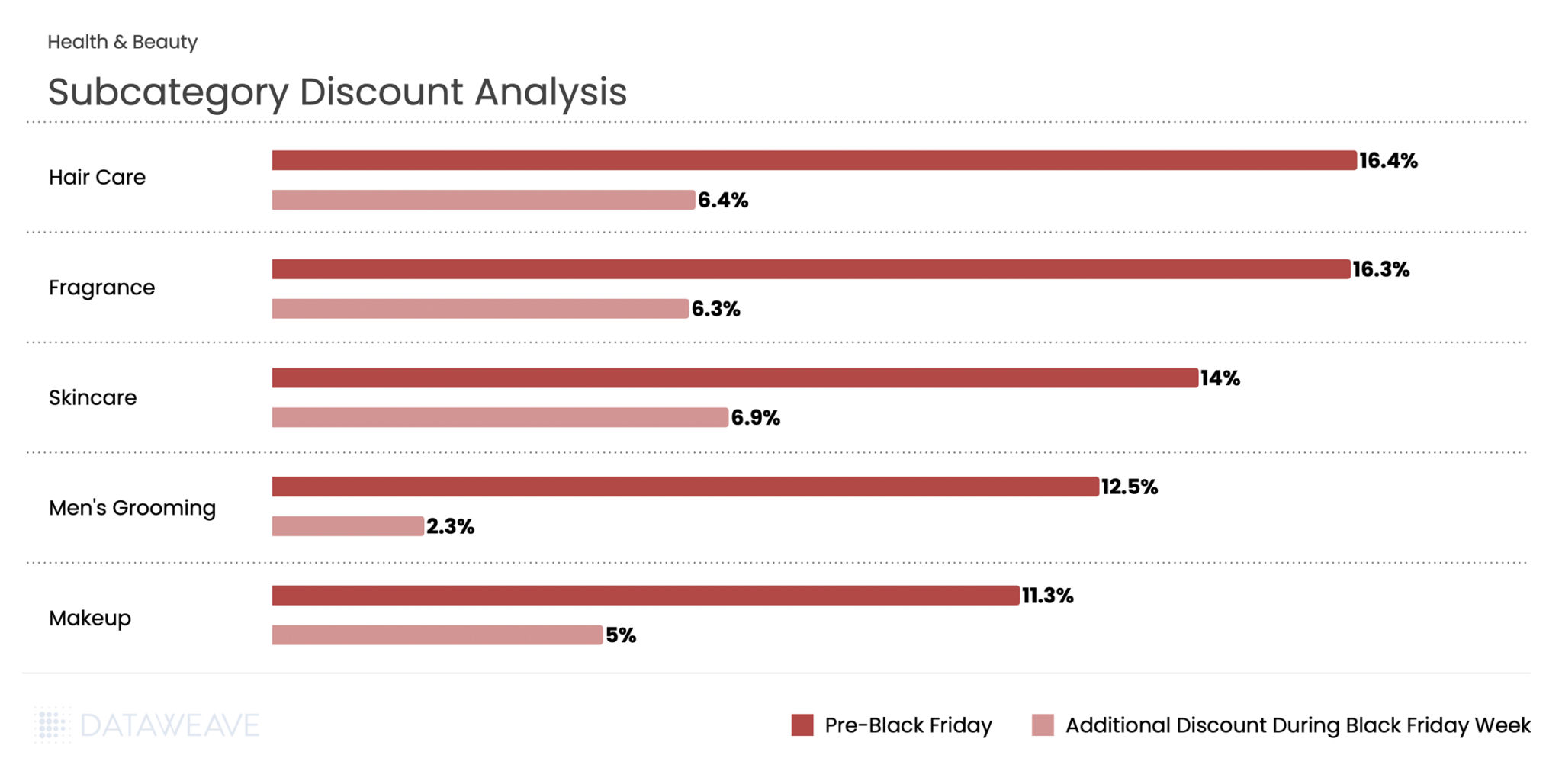

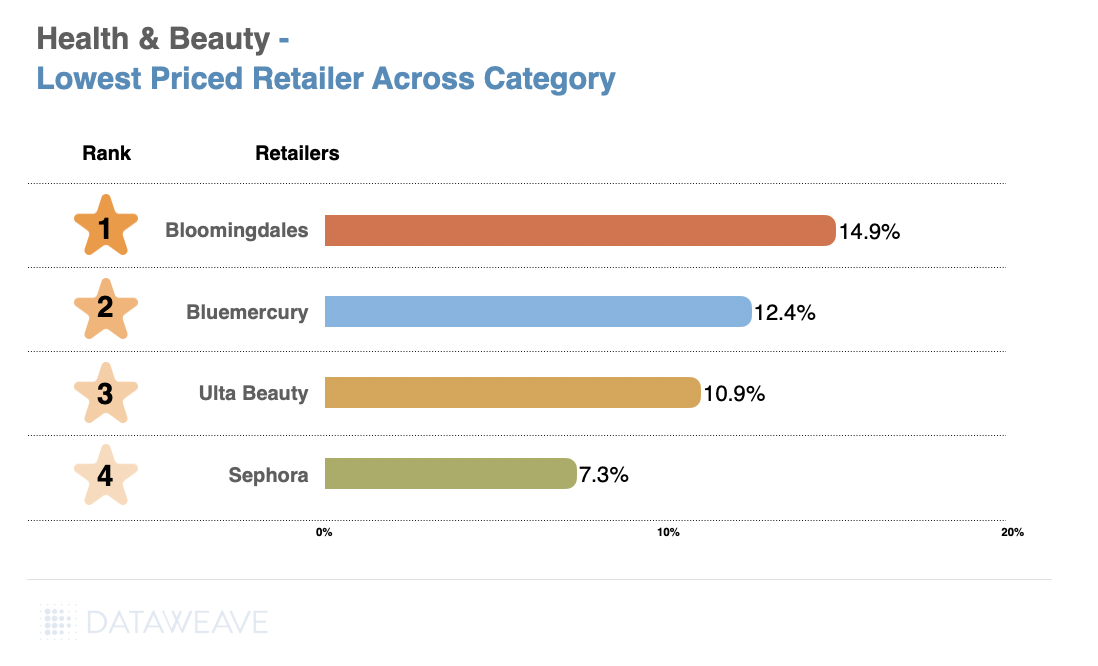

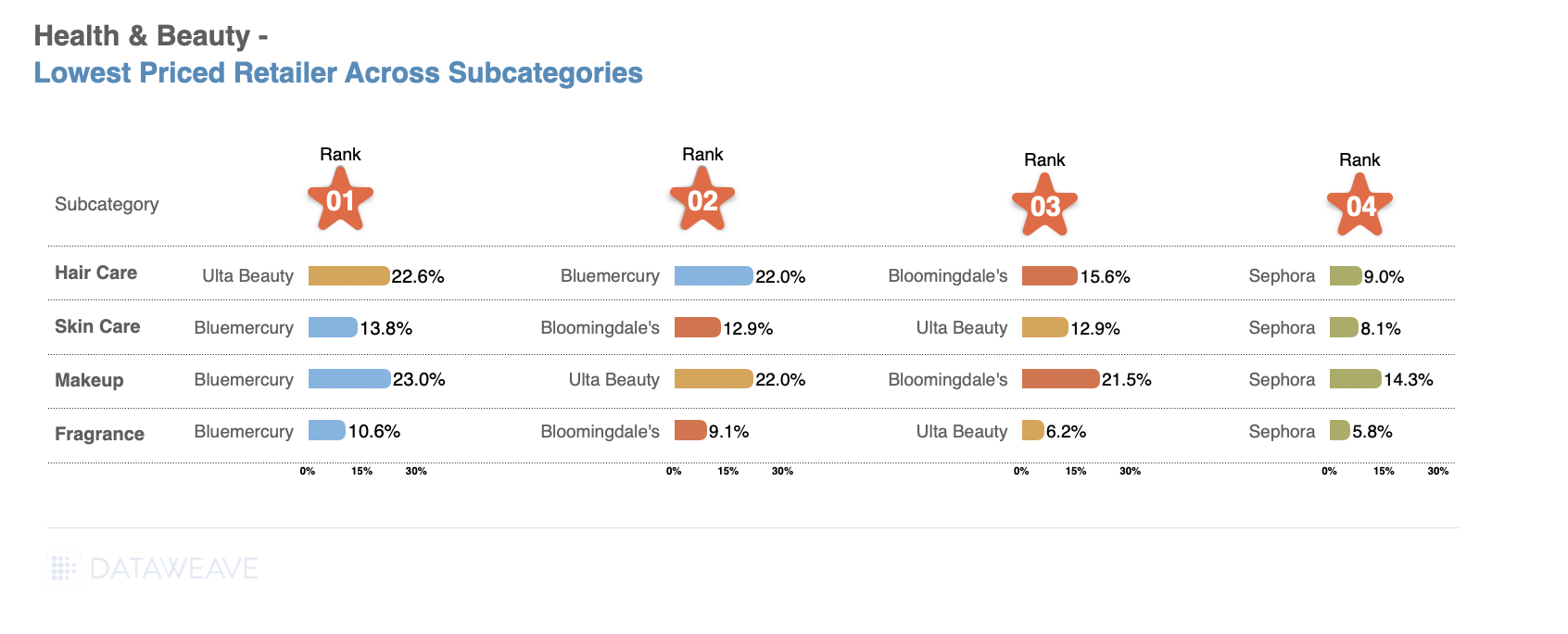

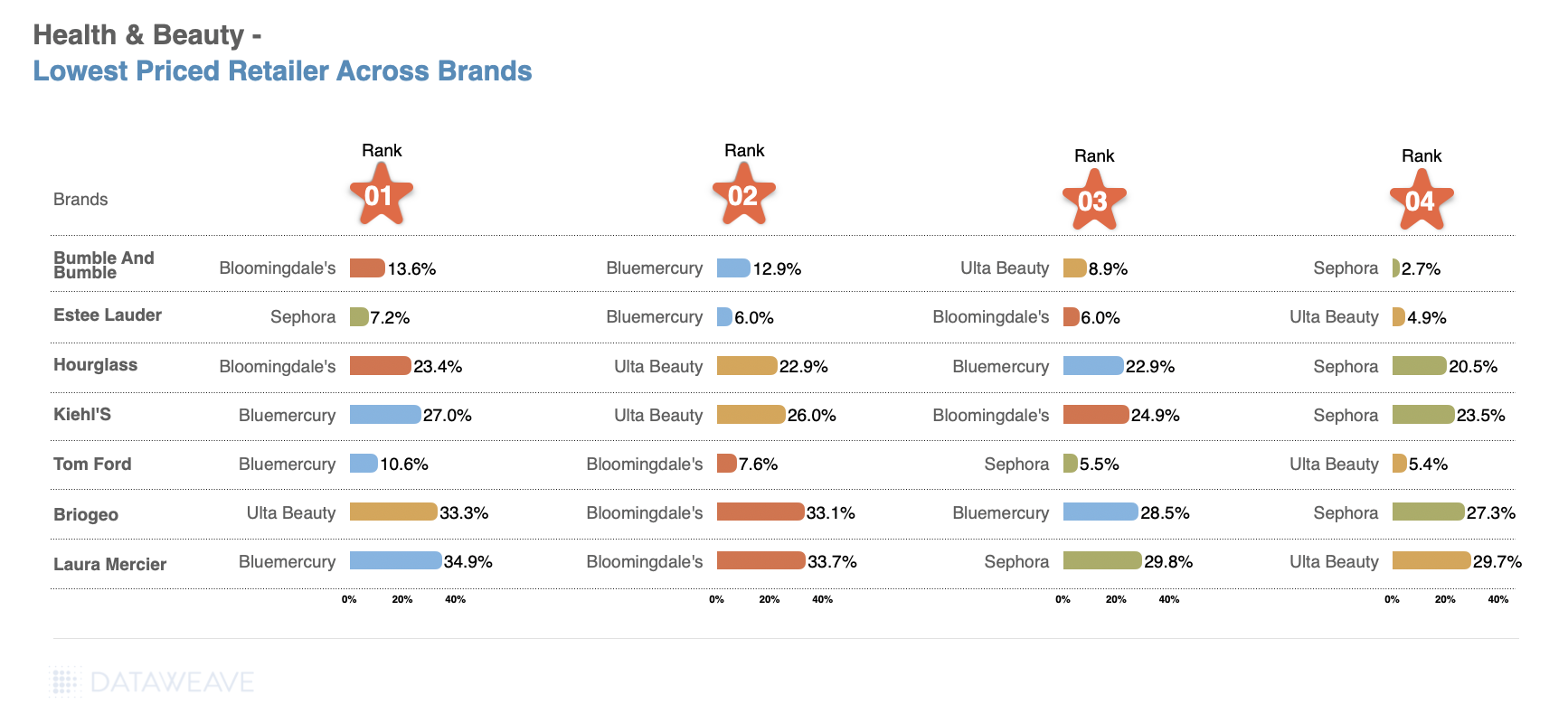

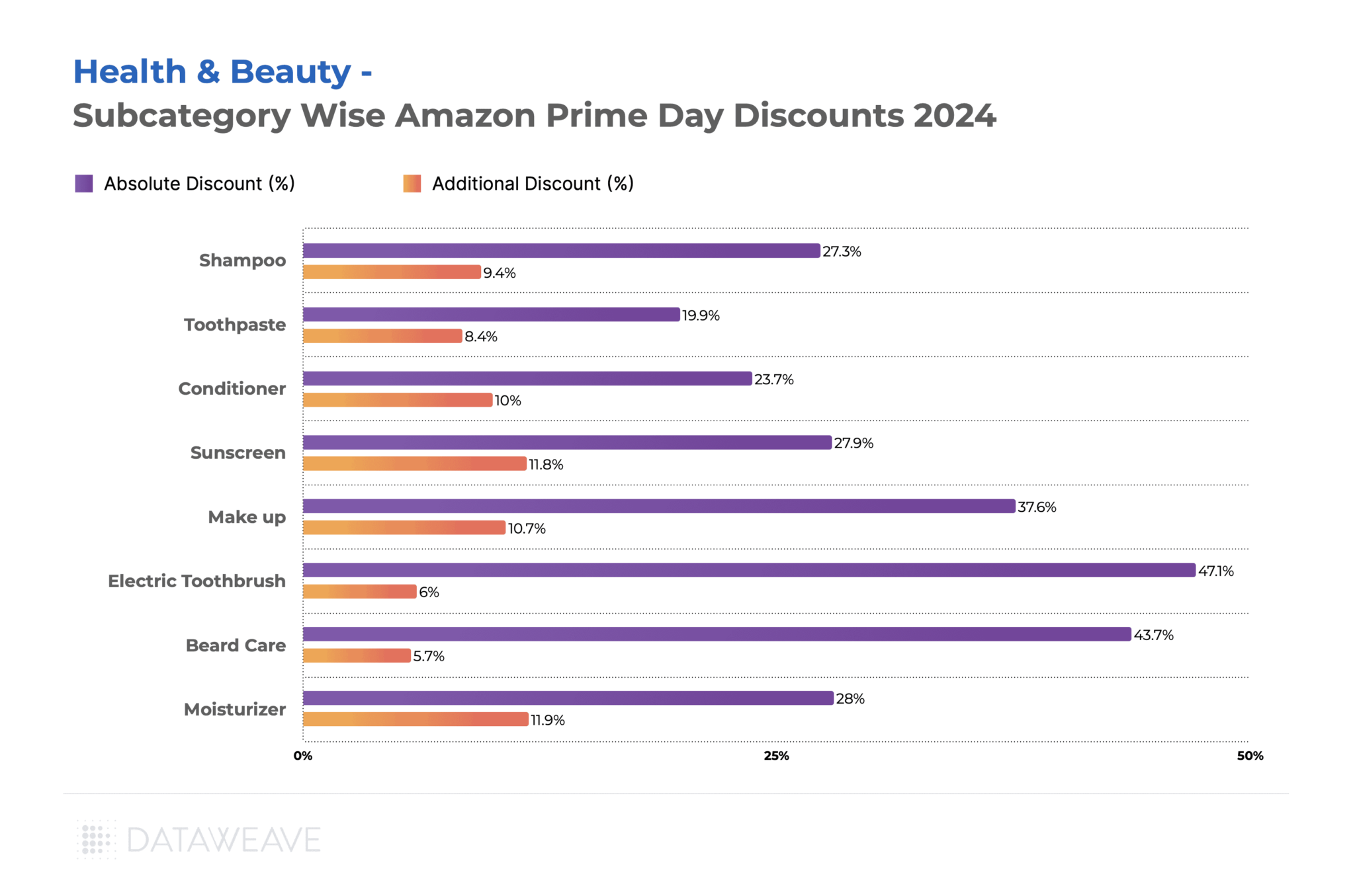

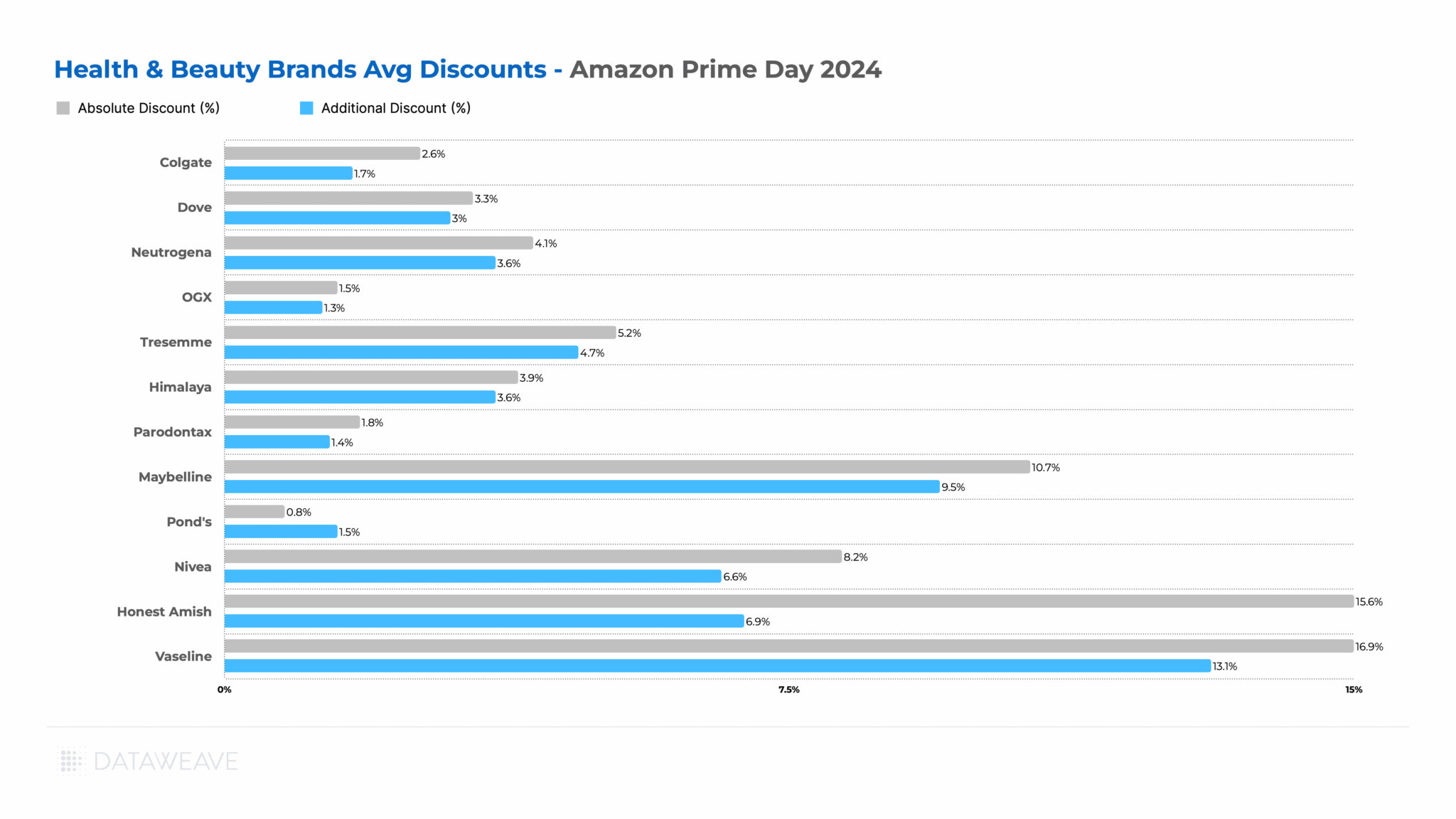

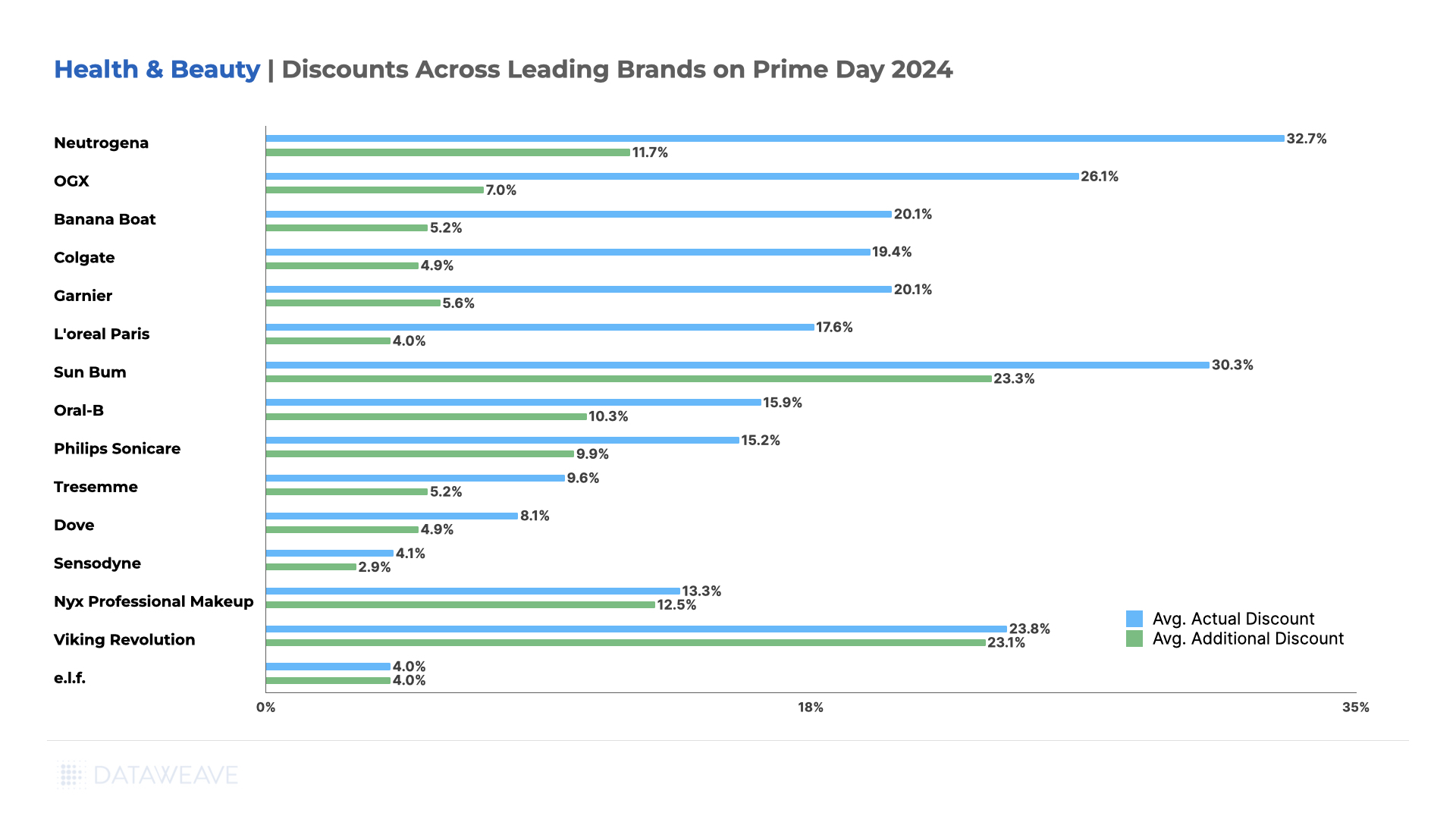

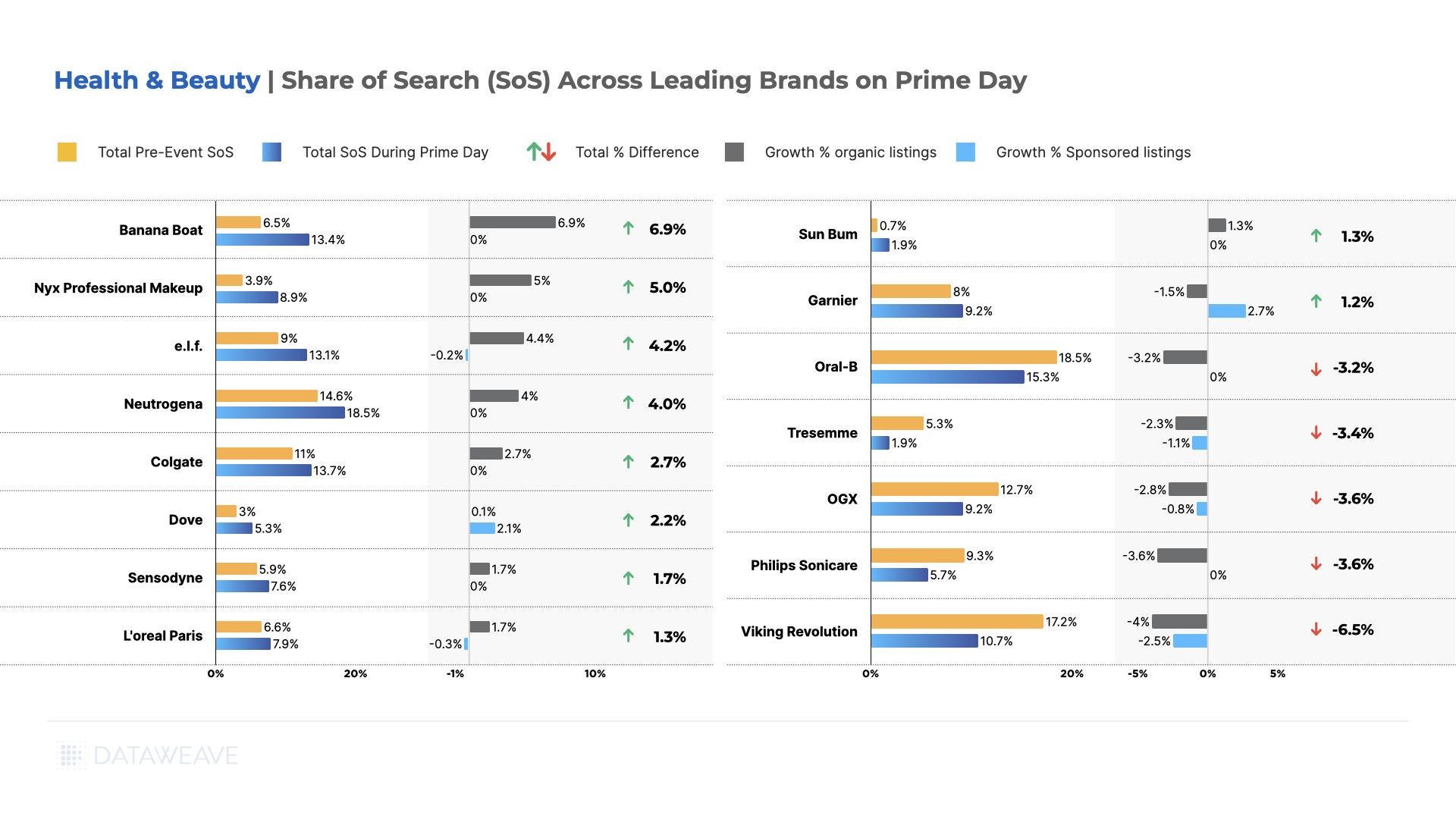

Health & Beauty

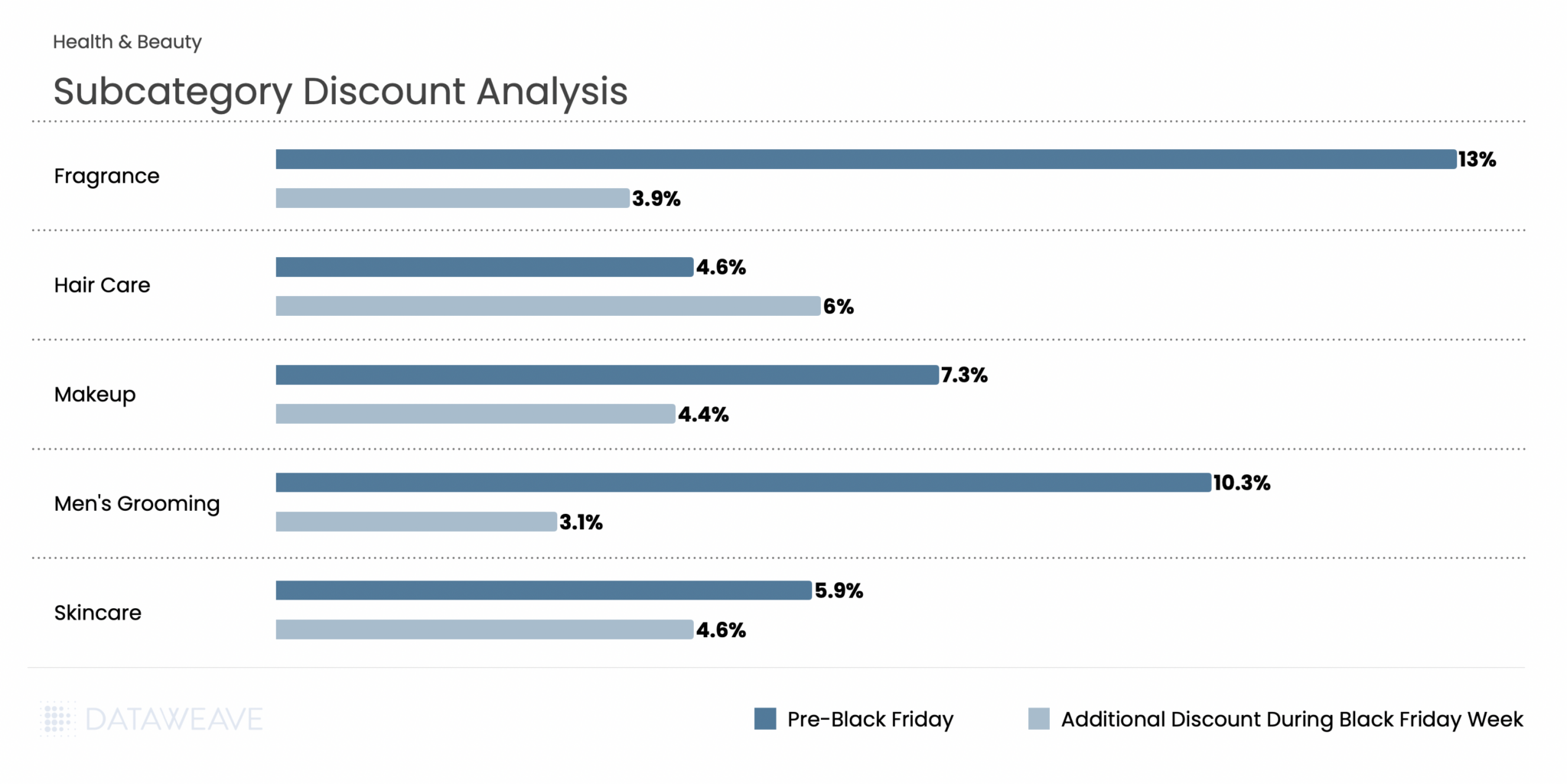

Our analysis of 6,474 SKUs reveals subcategory-level insights and dramatic brand visibility shifts that highlight the evolving German beauty landscape.

Subcategory Discount Analysis

Pre-Black Friday discounts averaged 10%, with Black Friday Week adding 4.5% on average. Fragrance led pre-sale discounting at 11.6%, positioning perfumes and colognes as attractive early holiday purchases. However, Fragrance saw the smallest Black Friday Week addition at just 2.8%.

Hair Care and Skincare both showed strong performance across both periods, with Hair Care at 11.1% pre-sale and 4.9% during Black Friday Week, while Skincare registered 10.9% and 5.1% respectively. Skincare’s 5.1% Black Friday Week discount was the highest in the category.

Men’s Grooming stood apart with notably lower discounts at 3.3% pre-sale and 2.6% during Black Friday Week, suggesting either tighter margins in this subcategory or strategic positioning at different price points.

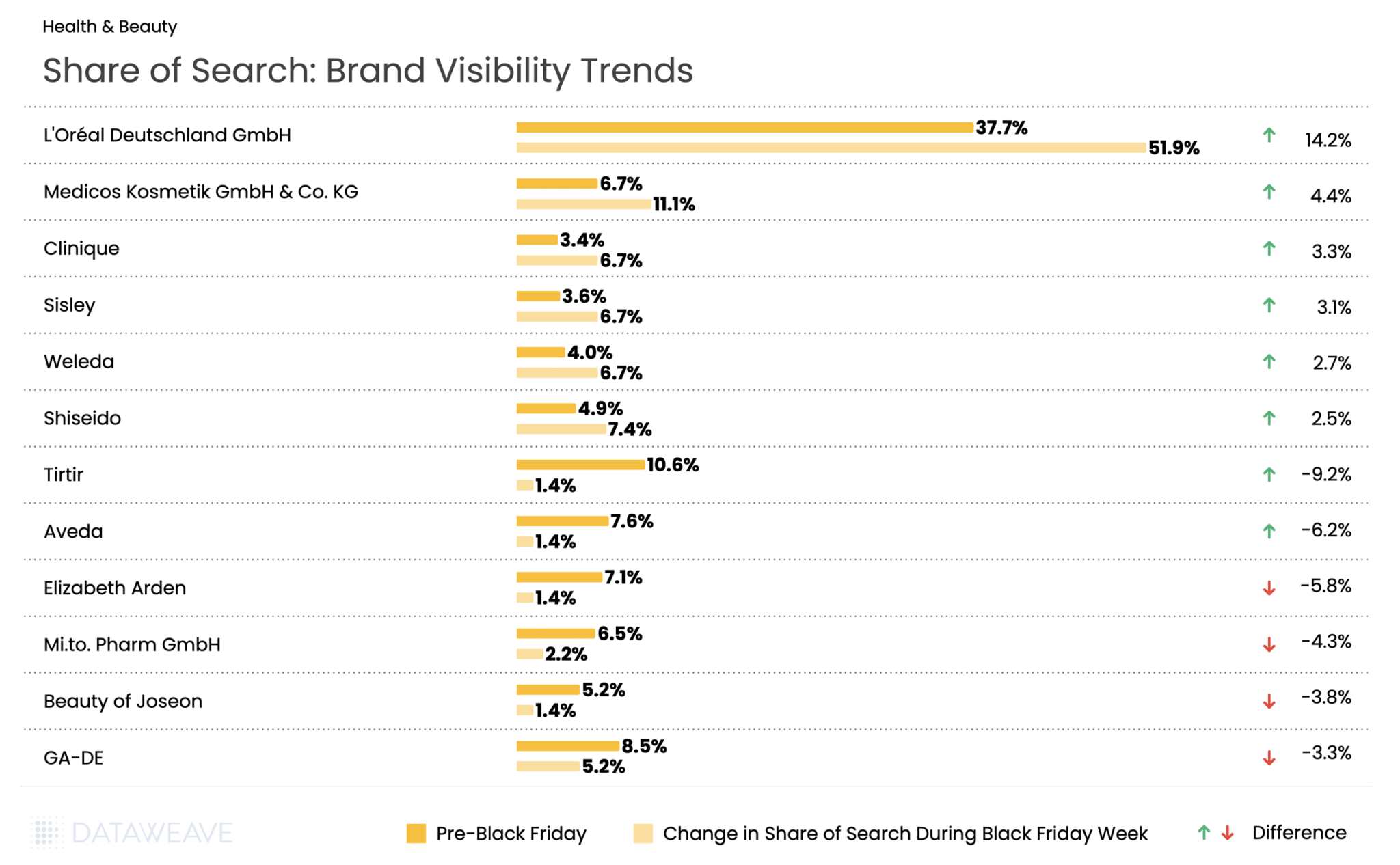

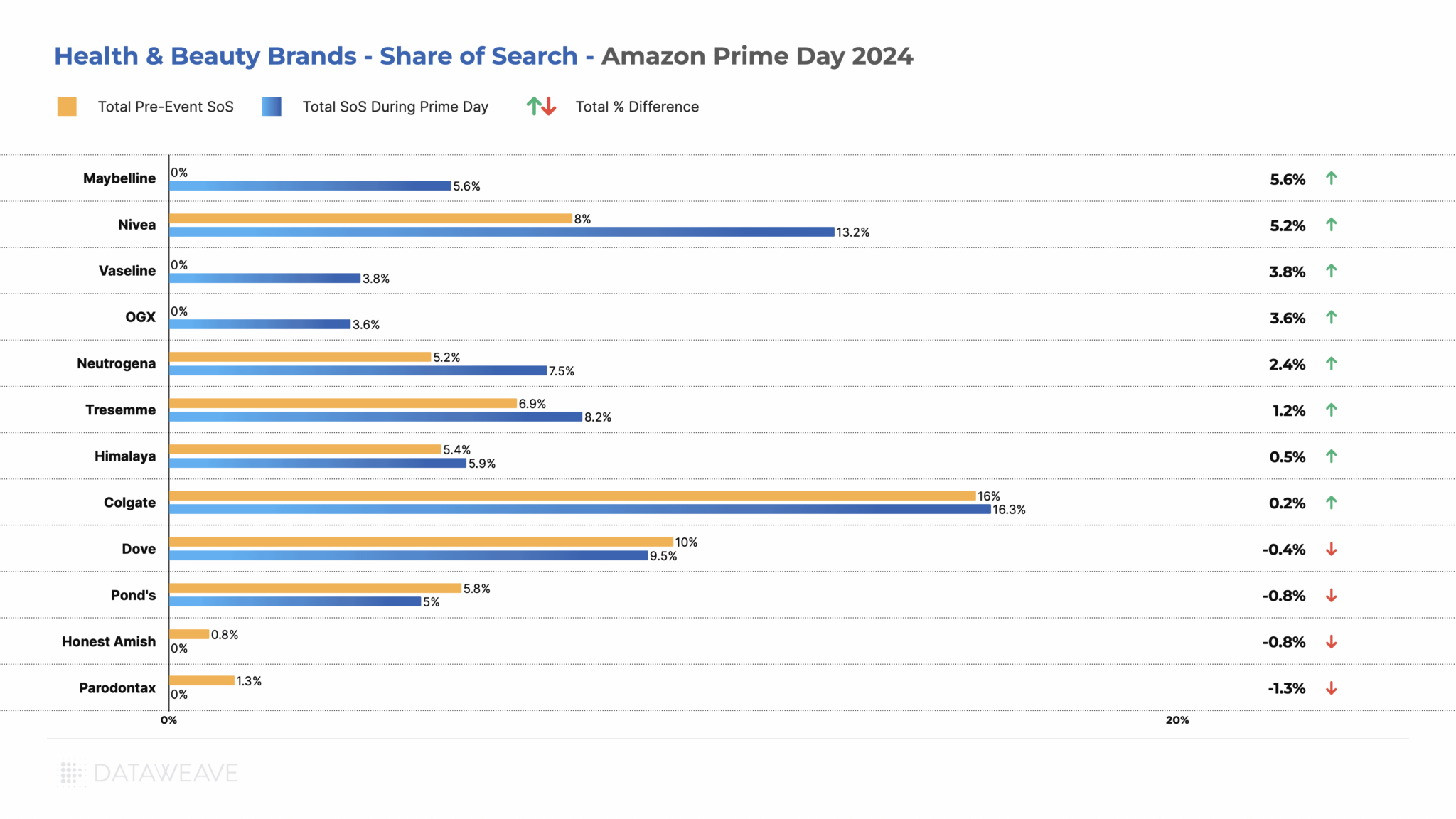

Share of Search: Brand Visibility Trends

L’Oréal Deutschland GmbH emerged as the most visible brand, surging from 37.7% to 51.9%, (+14.2). German pharmaceutical cosmetics company Medicos Kosmetik GmbH & Co. KG gained 4.4 %. Clinique gained 3.3 %, and French luxury brand Sisley added 3.1 %, German natural cosmetics brand Weleda rose 2.7 %, and Japanese prestige brand Shiseido gained 2.5 %.

The flip side? K-beauty brands and some international names faced significant challenges. Viral make-up brand Tirtir experienced the steepest decline visibility, dropping by 9.2 %. Aveda fell 6.2 %, Elizabeth Arden dropped 5.8 %, and Beauty of Joseon declined 3.8 %. German pharmacy brand Mi.to. Pharm GmbH lost 4.3 %, while Israeli makeup brand GA-DE fell 3.3 %.

The data reveals a clear German preference for European beauty heritage, pharmaceutical-grade cosmetics, and established prestige brands during Black Friday, rather than trendy K-beauty products or mid-tier international brands.

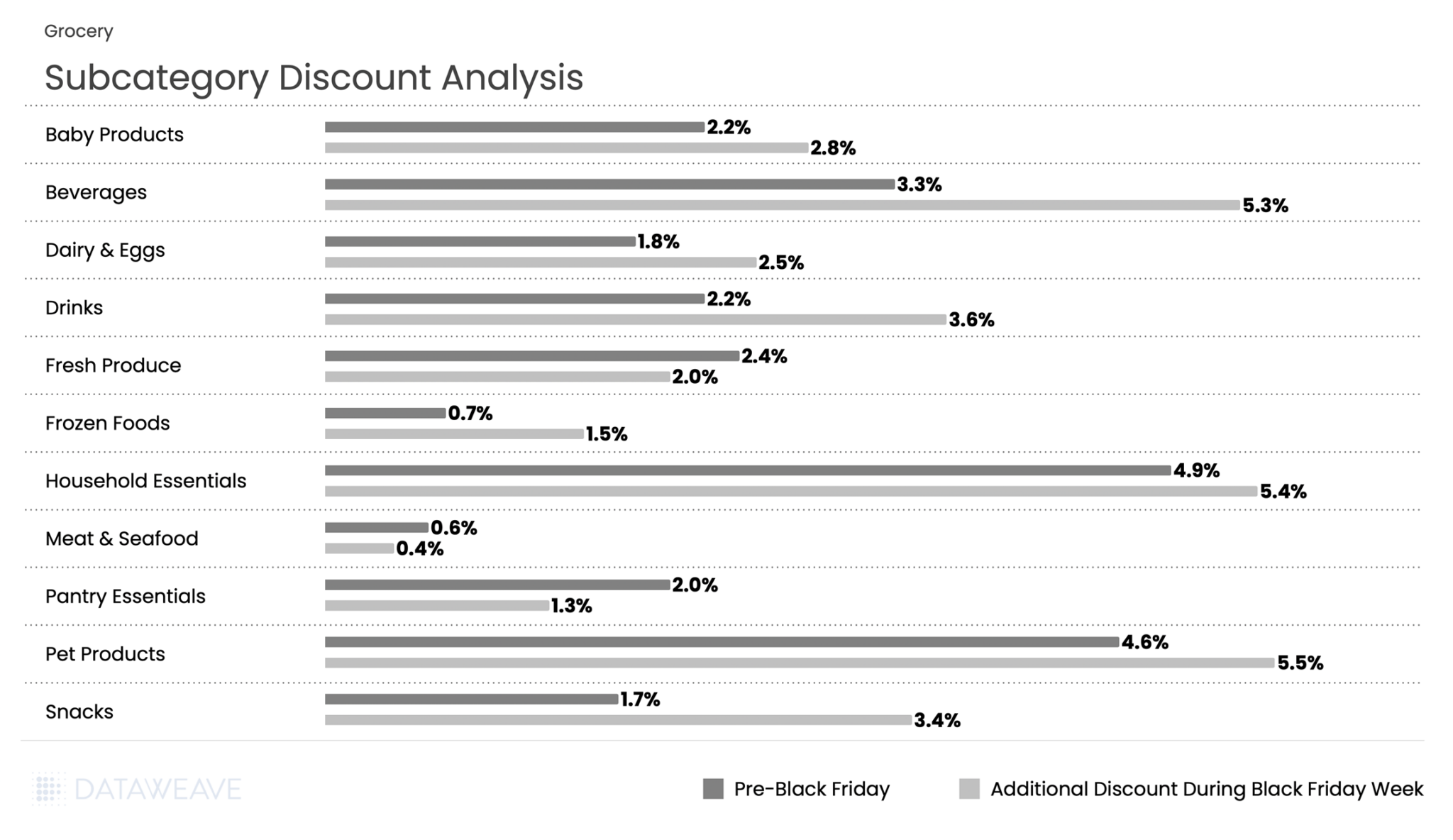

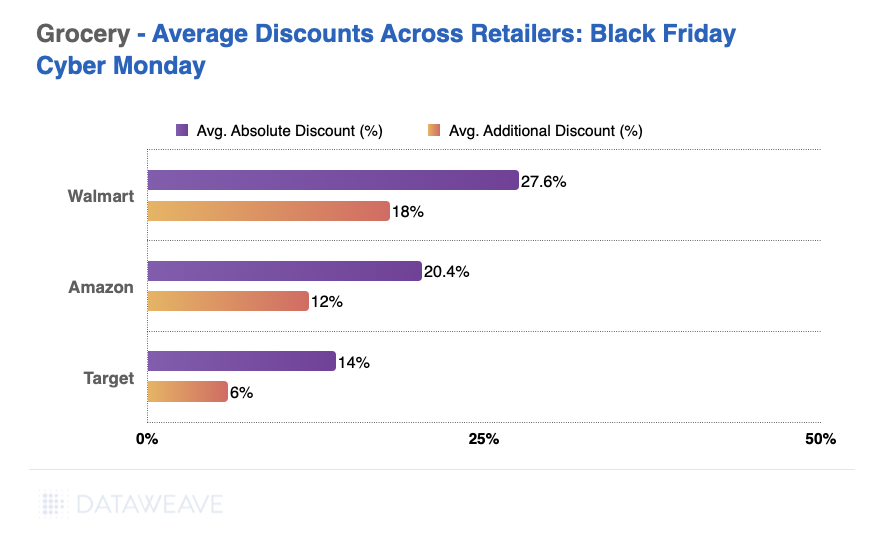

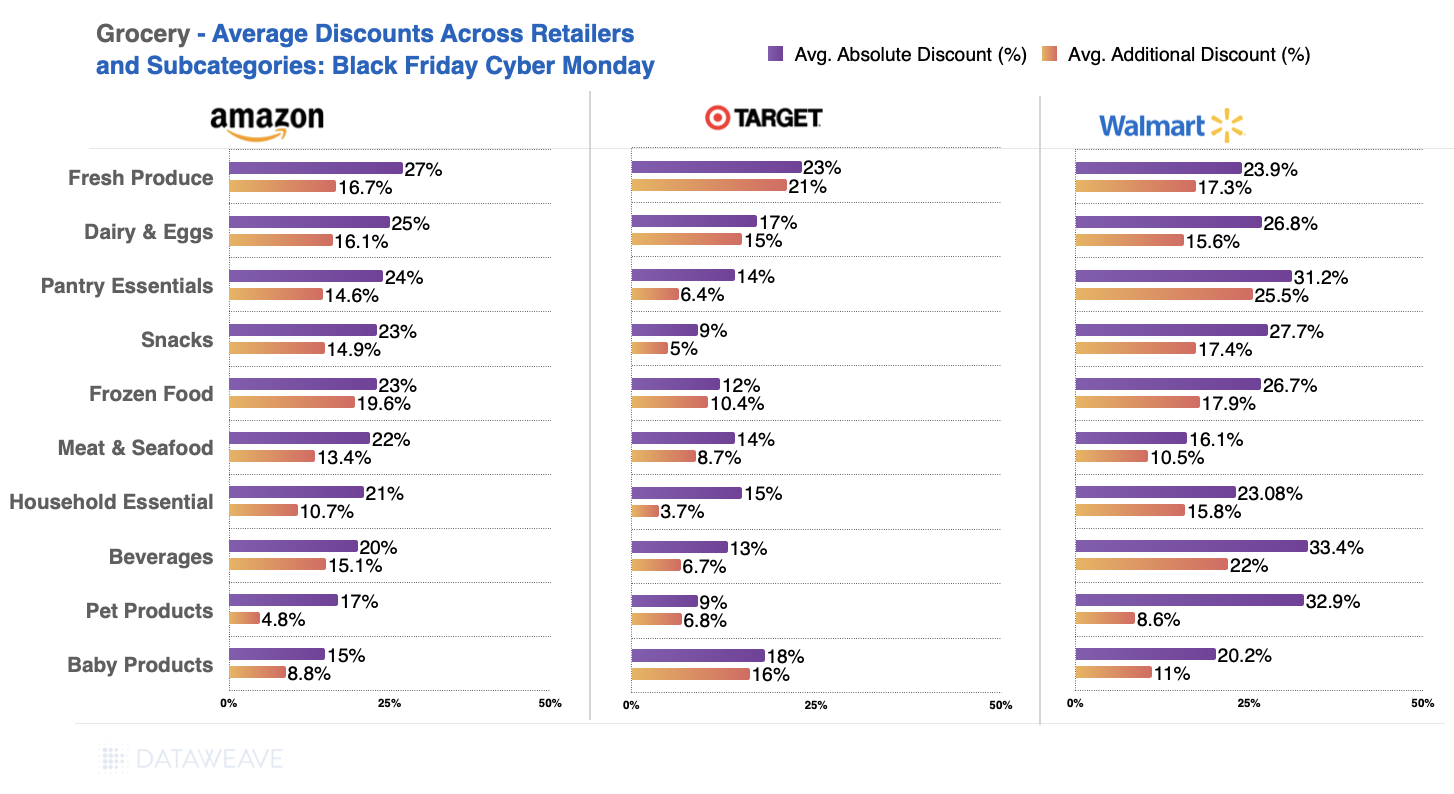

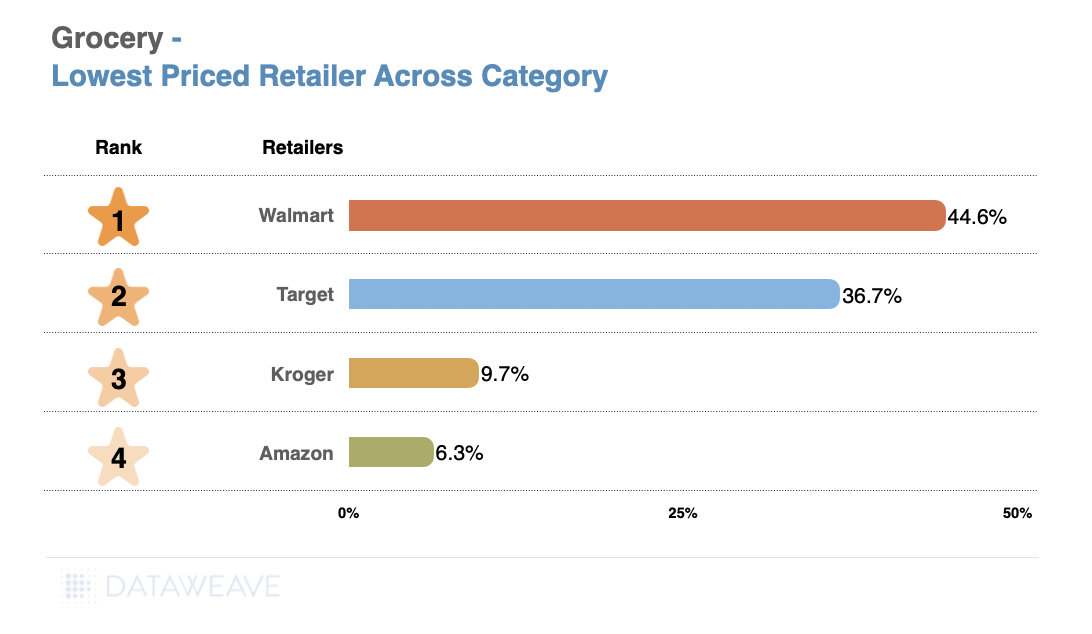

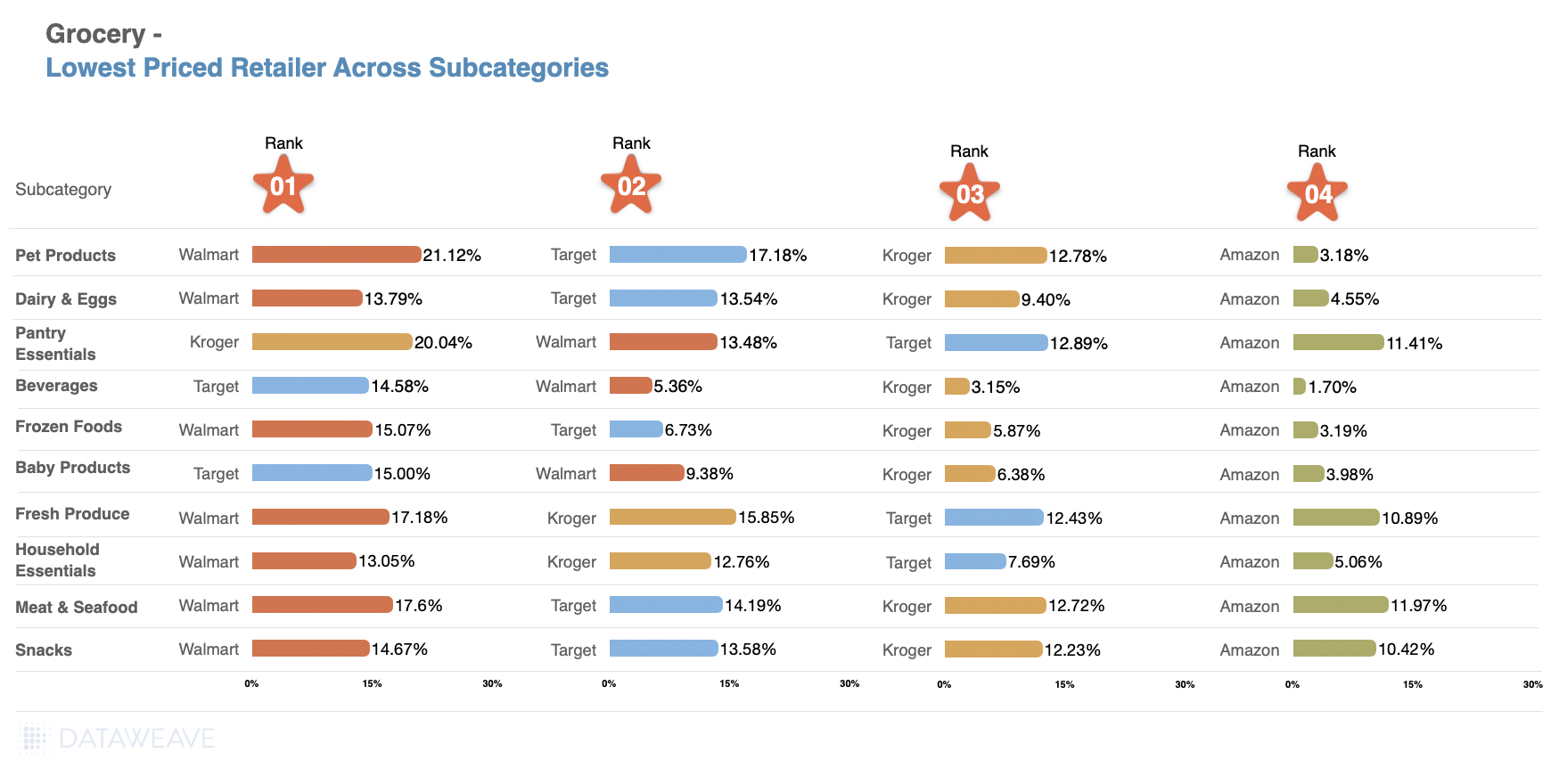

Grocery

While Grocery typically sees more modest discounts compared to discretionary categories, the German market showed interesting patterns with Black Friday Week discounts (3.5%) actually exceeding Pre-Black Friday levels (2.6%). Our analysis of 4,378 SKUs shows how German retailers approached promotions across essential and indulgent subcategories.

Subcategory Discount Analysis

Pre-Black Friday discounts averaged just 2.6% in grocery. But Black Friday Week saw this surging to 3.5%, an increase that represents the highest proportional jump among all categories.

Pet Products and Household Essentials led discounting, with Pet Products at 4.6% pre-sale and an additional 5.5% during Black Friday Week. Meanwhile Household Essentials registered 4.9% and 5.4% respectively.

Beverages showed particularly strong Black Friday Week performance, jumping from 3.3% to 5.3%, while snacks doubled from 1.7% to 3.4%. Fresh categories maintained minimal promotional activity consistent with perishable inventory constraints: Meat & Seafood saw negligible discounts (0.6% pre-sale, 0.4% Black Friday Week), while Fresh Produce actually decreased from 2.4% to 2% during the main event.

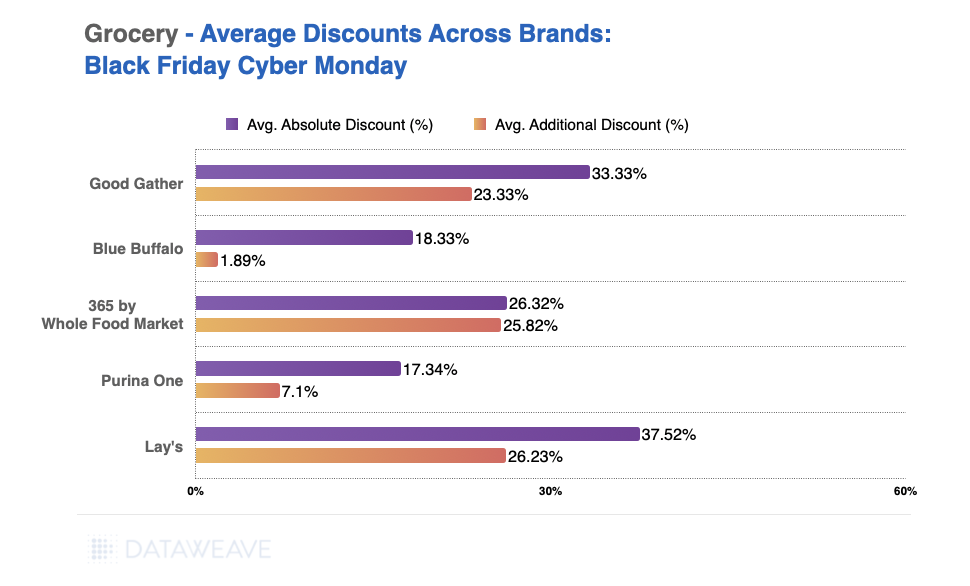

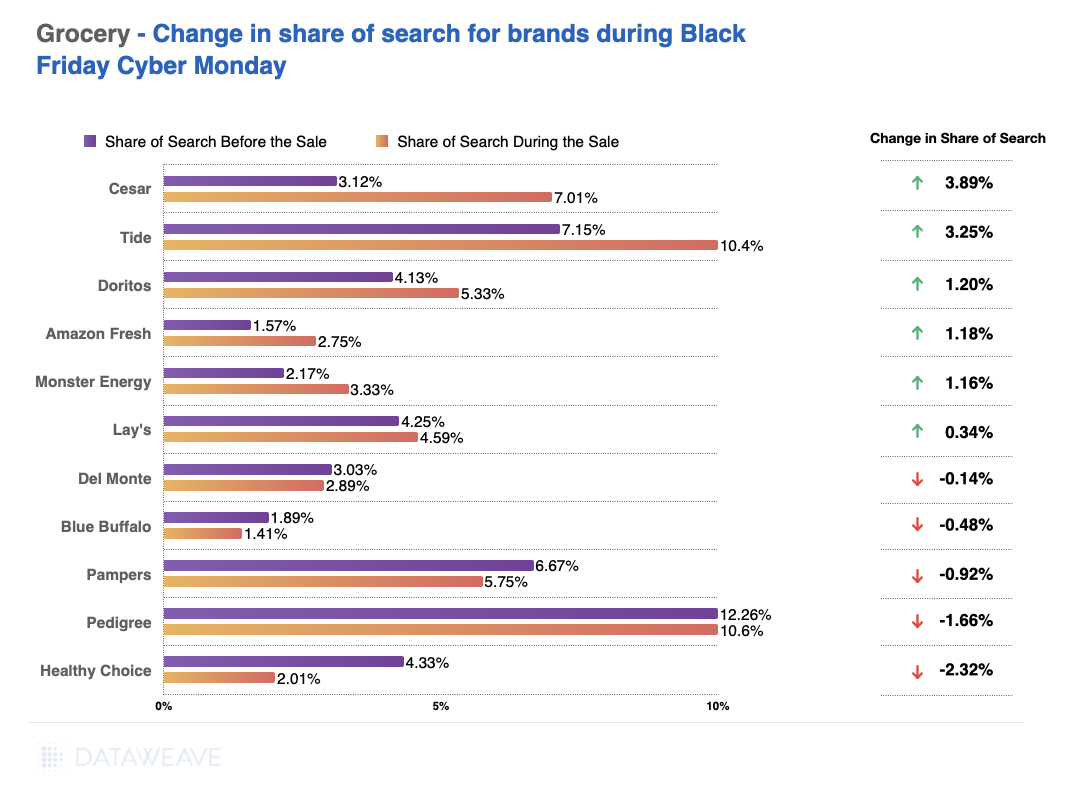

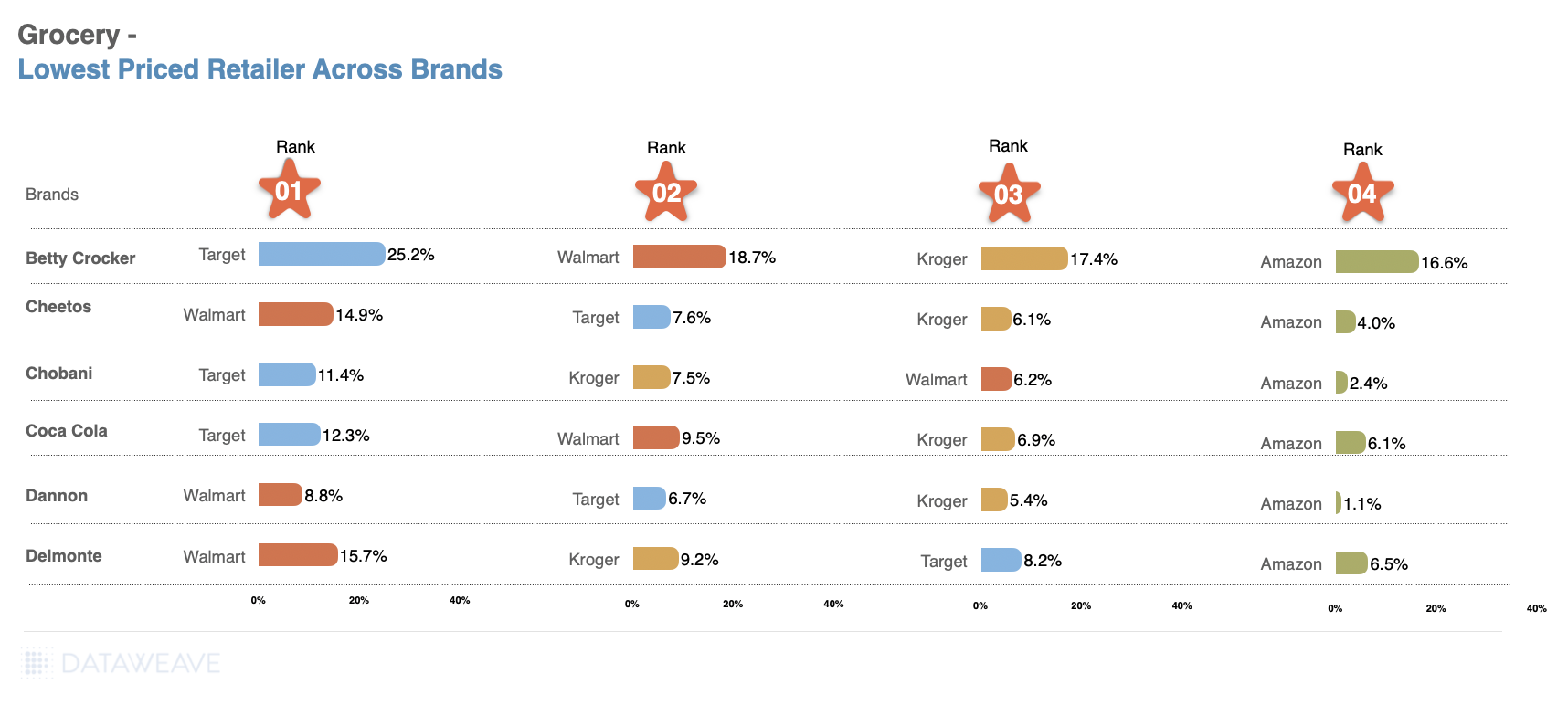

Share of Search: Brand Visibility Trends

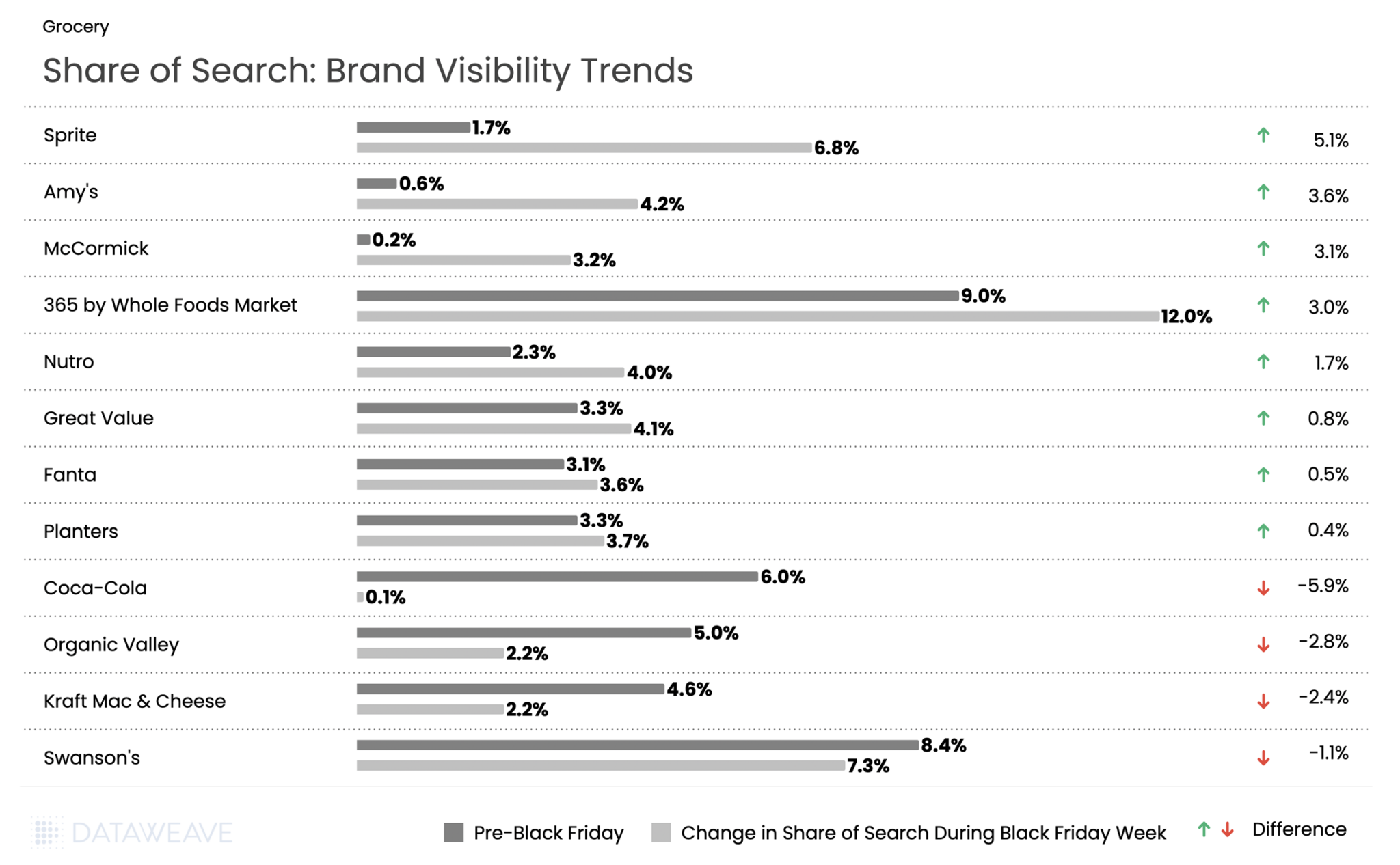

365 by Whole Foods saw the highest share of search at 9% pre event and 12% during Black Friday week. But Sprite led all brands with a 5.1% surge in share of search. Meanwhile, sister brand Coca-Cola experienced one of the steepest declines in our analysis, with visibility plummeting from 6.0% to just 0.1%. Fanta maintained modest search growth at 0.5 %. This stark divergence between two brands from the same parent company suggests vastly different promotional strategies during Black Friday Week.

Specialty and organic food brands performed well: Amy’s (organic/natural foods) gained 3.6 %, while spice brand McCormick surged 3.1 %. Pet food brand Nutro gained 1.7 %, while value-oriented Great Value added 0.8 %.

Snack brand Planters gained 0.4 %. On the decline side, Organic Valley dropped 2.8 %, Kraft Mac & Cheese fell 2.4 %, and Swanson’s declined 1.1 %.

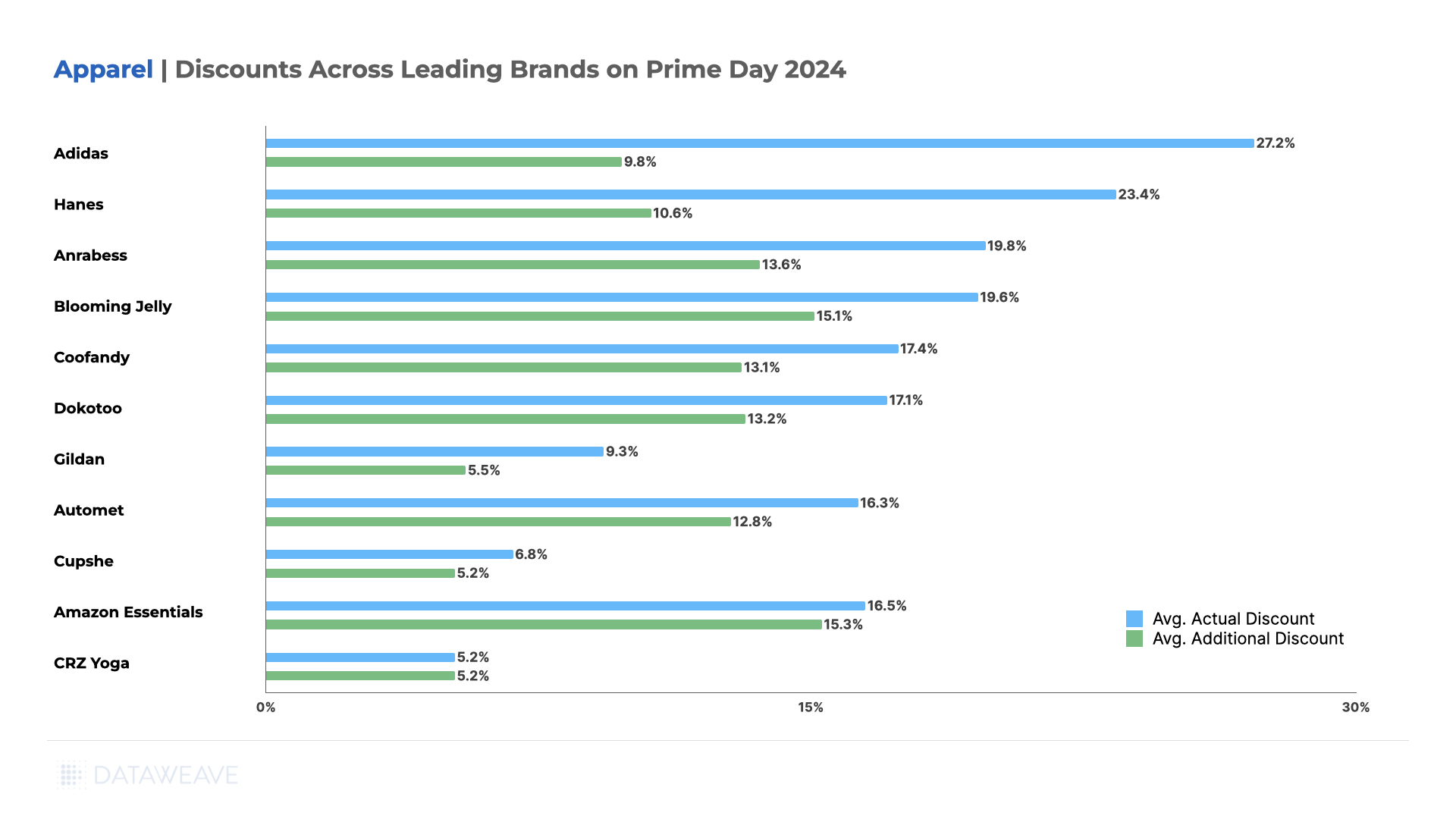

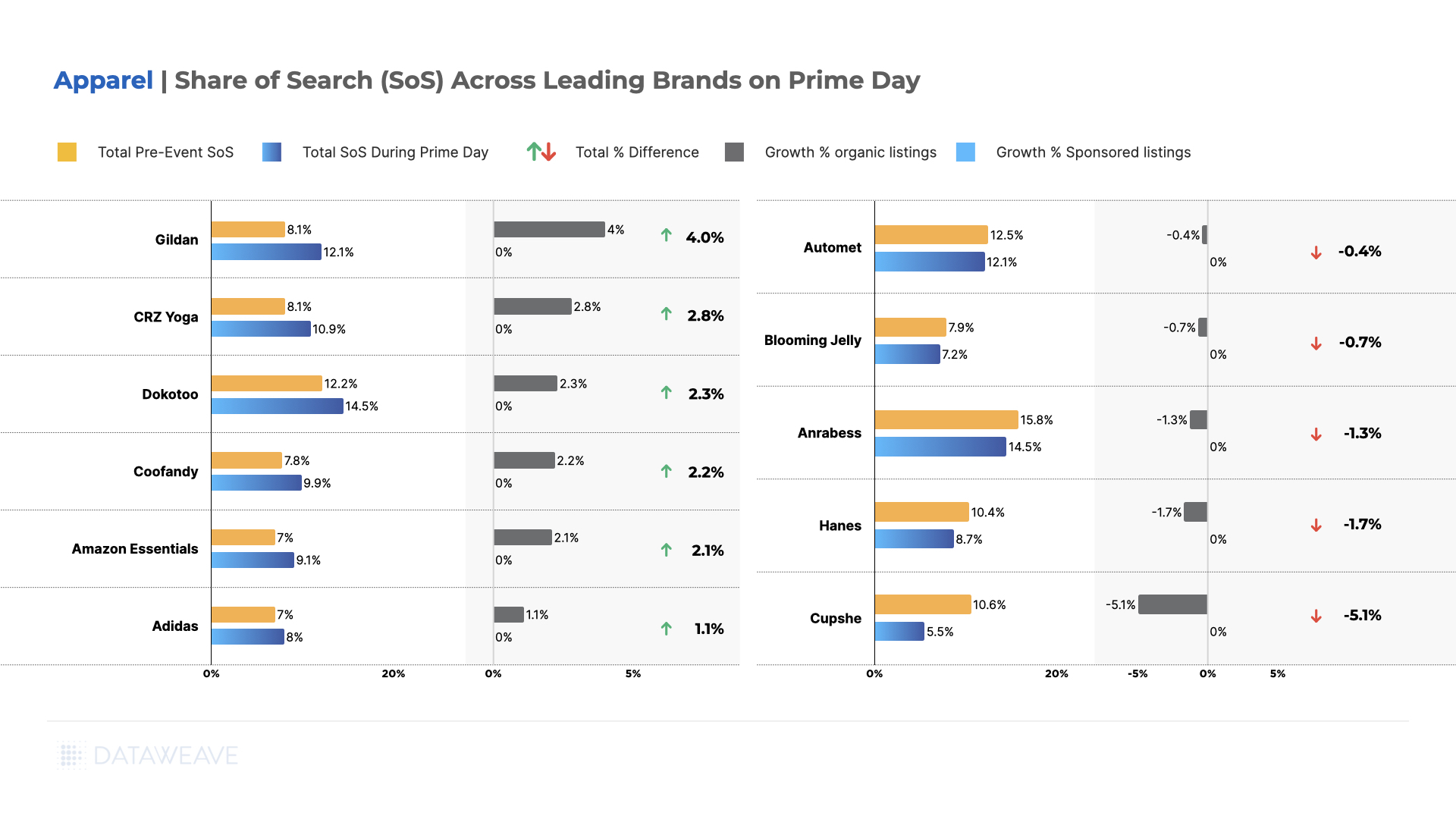

Apparel

Apparel in the German market showed modest promotional activity compared to other markets, with Pre-Black Friday discounts averaging 5.9% and Black Friday Week at 5.2%. Our analysis of 2,321 SKUs reveals interesting patterns across fashion segments in the German market.

Subcategory Discount Analysis

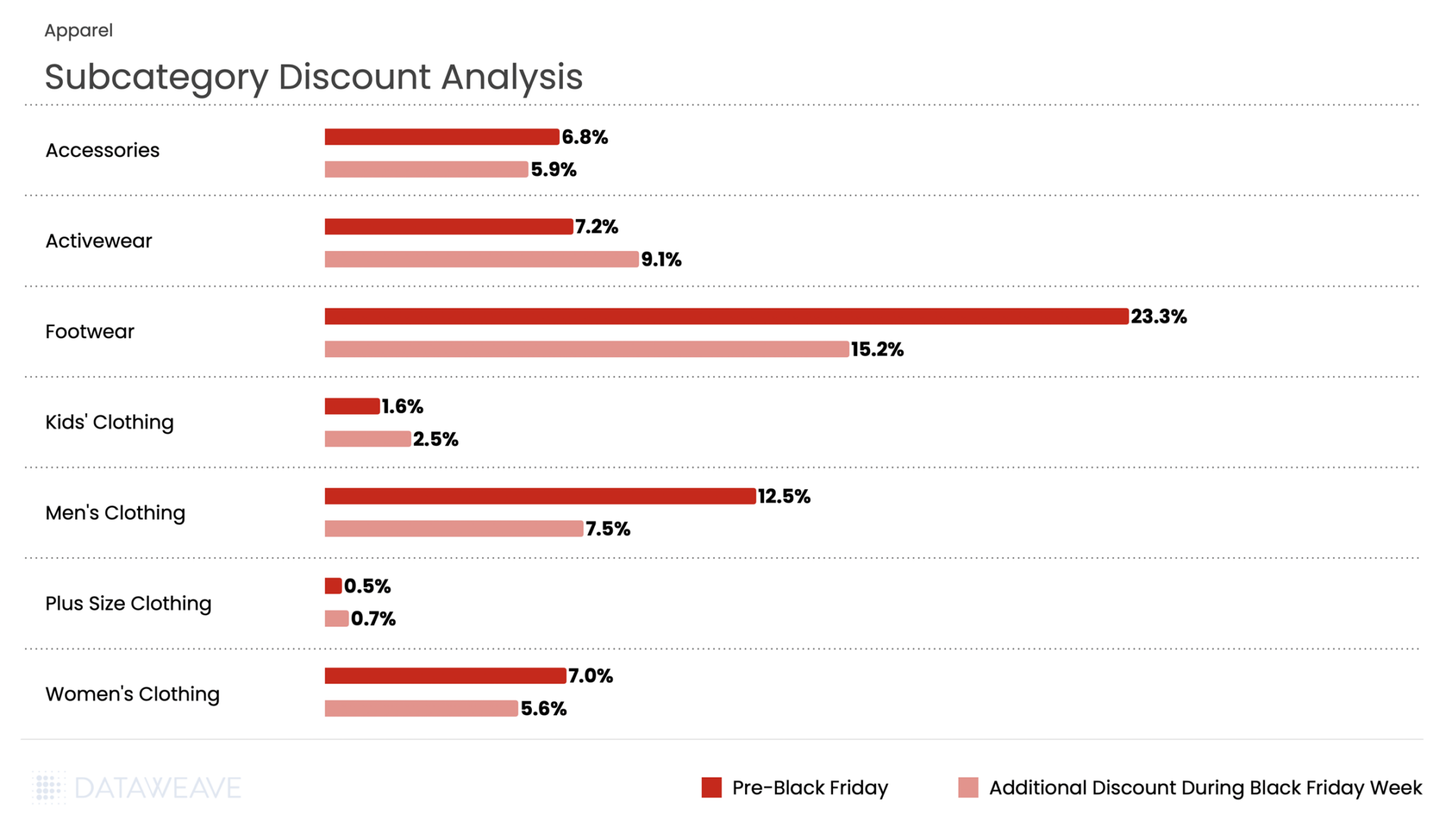

Footwear dominated discounting in both periods, with an impressive 23.3% pre-sale discount, and 15% additional discount during Black Friday Week. Men’s Clothing followed at 12.5% pre-sale, with additional 7.5% during Black Friday Week.

Activewear presented a unique pattern, with discounts increasing from 7.2% pre-event to additional 9.1% during Black Friday Week: one of the few subcategories to show higher discounts during the main event. Plus Size Clothing saw minimal promotional activity at 0.5% pre-sale and 0.7% during Black Friday Week, the lowest discounts in the entire category.

Share of Search: Brand Visibility Trends

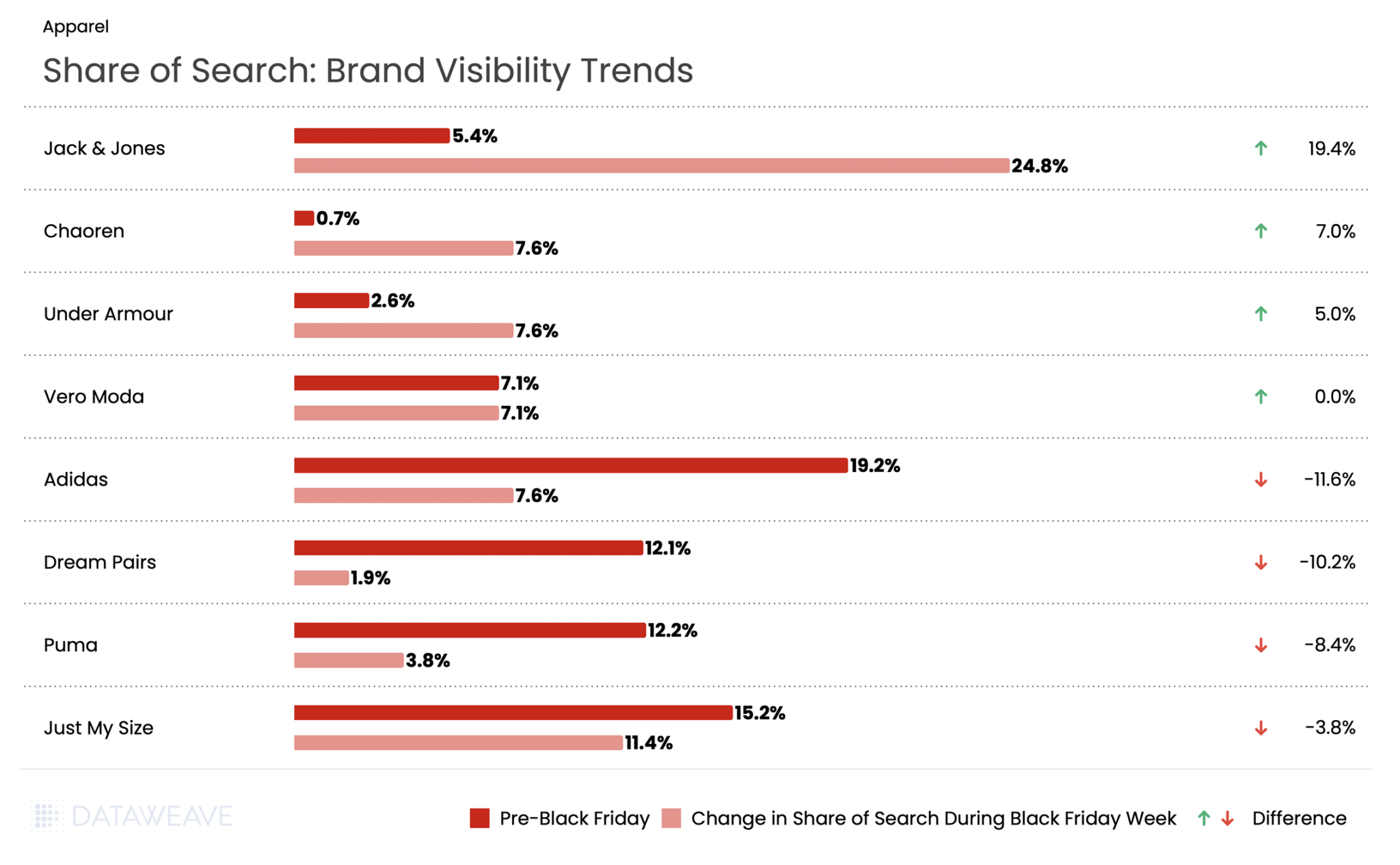

Danish fashion brand Jack & Jones experienced an unprecedented surge with a staggering 19.4% gain in visibility. Sister brand Vero Moda (also owned by Jack & Jones’ parent company Bestseller) maintained flat visibility at 7.1%. Footwear brand Chaoren gained 7%. Meanwhile activewear giant Under Armour rose by 5%.

However, established sportswear giants suffered dramatic visibility losses. Adidas experienced an 11.6% decline in share of search. Dream Pairs saw visibility drop by 10.2%, Puma fell 8.4%, and plus-size brand Just My Size declined by 3.8 %.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Check out our analysis on Black Friday Pricing and Discount trends in the USA and UK. Follow our blog for more insights on retail pricing trends, brand visibility analysis, and data-driven commerce intelligence.

Black Friday 2025 saw British shoppers spend an average of £430 each this year representing a £91 increase from last year and totaling over £10.2 billion across the sales period.

The 2025 sales event arrived at a pivotal moment for UK retail. Retail sales fell 1.1% in October 2025 as consumers held back spending in anticipation of Black Friday promotions, according to the Office for National Statistics. Over 2 in 5 UK adults participated in Black Friday shopping, with 45% planning to pick up Christmas gifts at a discount, according to a Barclays study.

Against this backdrop of cautious optimism and strategic consumer behavior, how did retailers and brands perform across key categories this Black Friday? At DataWeave, we conducted a comprehensive analysis of Black Friday 2025 discounting trends across five major categories in the UK market: Consumer Electronics, Home & Furniture, Health & Beauty, Grocery, and Apparel. Our AI-powered pricing intelligence platform monitored over 71K SKUs across leading UK retailers like Costco, Selfridges, Boots, Debenham’s, Carethy, Argos, John Lewis, Amazon, and more, revealing fascinating patterns in how retailers and brands approached this year’s sale season.

Our Methodology

For this analysis, DataWeave monitored average discounts across leading UK retailers during two distinct periods:

Pre-Black Friday: November 6 – November 23, 2025 – capturing early holiday deals and baseline pricing

Additional Discounts During Black Friday Week: November 24 – December 1, 2025 – covering Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

Our sample encompassed the top-ranked products across subcategories on major retail sites. We also analyzed Share of Search data, which measures brand visibility by monitoring which brand names appear in the top 20 search results for critical keywords.

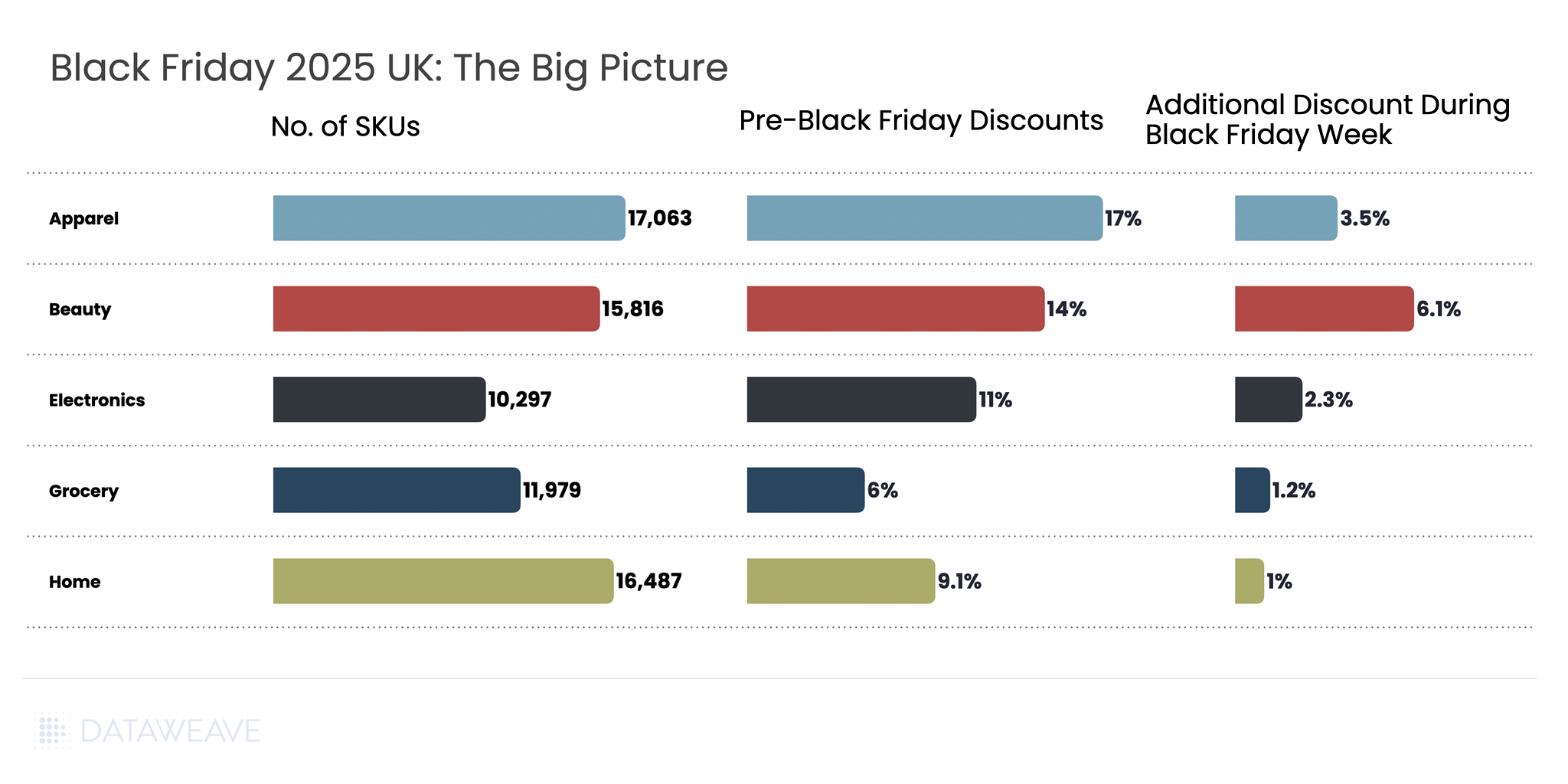

Black Friday 2025 UK: The Big Picture

Our analysis covered 71,642 SKUs across five major categories. Here’s the snapshot of average discounts during the Pre-Black Friday period compared to Black Friday Week:

Key Insight: Pre-Black Friday discounts were substantial across all categories. This suggests UK retailers front-loaded their promotions to capture early holiday shoppers, with additional discounts during Black Friday Week adding to the baseline discounts already in place. The extended promotional period transformed Black Friday from a single-day event into a month-long campaign, with 60% of UK shoppers beginning their deal searches as early as October.

Consumer Electronics

Consumer electronics remains a cornerstone of Black Friday shopping in the UK, with technology accounting for 48% of planned consumer spending during the sales period, according to PwC.

AI is transforming how consumers shop for electronics, with AI-driven traffic to retail sites expected to rise 410% year-on-year during the 2025 holiday season. Younger shoppers particularly embraced AI tools, with 17% of Gen Z consumers using AI platforms like Chat GPT and Gemini to source and compare deals. Our analysis of 10,297 SKUs reveals how discounts varied across subcategories and which brands dominated search visibility.

Subcategory Discount Analysis

Pre-Black Friday discounts averaged 11.1% across subcategories, while Black Friday Week saw an additional 2.3% discount on average. Audio & Video products led the pre-sale discounting at 16.3%, indicating retailers were eager to move inventory early in the season.

During Black Friday Week, Home Automation saw the highest additional discount at 2.8%. Wearables and Computers both saw solid 2.5% additional discounts, making them attractive categories during the peak shopping period.

Share of Search: Brand Visibility Trends

Our Share of Search analysis reveals significant shifts in brand visibility during Black Friday Week:

Bose dominated with its Share of Search more than doubling from 11.3% to 23.8%, a remarkable +12.5% gain. Lighting brand Philips Hue followed, gaining by +5.4% in share of search during Black Friday week. Notably, Meta, with it’s range of wearables, stands out for a +3.1% increase in visibility.

Apple’s Share of Search jumped from 10.1% to 16.4%, a gain of 6.4%. At the same time, Fitbit’s share dropped nearly 11%, the steepest decline in the entire electronics category. Meanwhile, Samsung and HP also lost on visibility this Black Friday in the UK.

Home & Furniture

The Home & Furniture category continues to attract UK consumers during Black Friday, though with a more measured discounting approach compared to other categories. Our analysis of 16,487 SKUs shows how discounts were distributed across subcategories.

Subcategory Discount Analysis

Home & Furniture saw Pre-Black Friday discounts averaging 9.1%, with Black Friday Week adding just 1% on average, the lowest additional discount among all categories. Furniture led pre-sale discounts at 13.7%, followed by Bedding at 11.9%. This suggests retailers aggressively promoted larger home goods early in the season to capture deal-seekers.

During Black Friday Week, Kitchenware saw the highest additional discount at 1.9%, making it attractive for holiday cooking and gifting needs. Conversely, Lighting saw minimal additional promotion at just 0.5%.

Share of Search: Brand Visibility Trends

Made.com, the contemporary furniture brand, saw visibility surge during Black Friday with an impressive 8.9% increase. Similarly, emerging mattress brand Vesgantti gained 5.4%. Rug specialist Gooch Oriental also made significant gains with a 4.9% increase.

On the flip side, British heritage brands faced challenges. Both Laura Ashley and Julian Bowen saw share of search drop 2.2%. Premium mattress maker Vispring also declined 2.1%, while French cookware brand Le Creuset fell 1.9%.

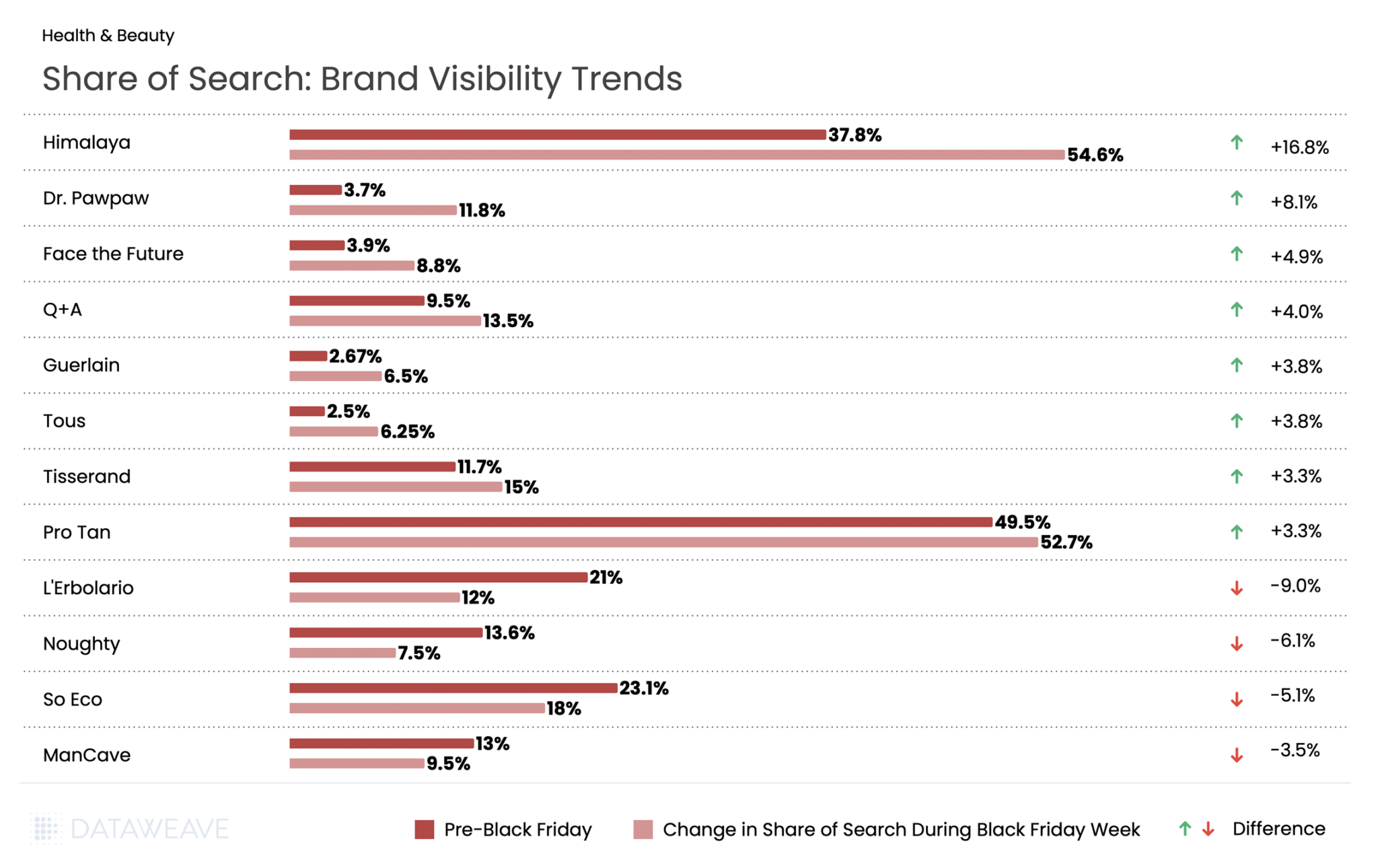

Health & Beauty

Health & Beauty has emerged as a growth engine during Black Friday in the UK. The beauty industry is projected to grow 5% annually through 2030 according to a McKinsey survey. The category continues to demonstrate resilience even as consumers show caution in other discretionary categories. Our analysis of 15,816 SKUs reveals fascinating subcategory-level insights and dramatic brand visibility shifts that highlight evolving consumer preferences in the beauty space.

Subcategory Discount Analysis

Health & Beauty presented a unique discounting pattern compared to other categories. Pre-Black Friday discounts averaged 14.4%, the second-highest among all categories. But Black Friday Week discounts were also robust at 6.1%, the highest additional discount increase.

Hair Care led both periods with 16.4% pre-sale discounts and an additional 6.4% during Black Friday Week. Skincare saw the highest Black Friday Week discount at 6.9%, suggesting retailers strategically saved their best skincare promotions for the main event when consumers are actively seeking holiday gift sets. Men’s Grooming stood apart with strong pre-sale discounts of 12.5% but more modest Black Friday Week additions of just 2.3%.

Share of Search: Brand Visibility Trends

The UK Beauty category saw some of the most dramatic Share of Search swings in our analysis.

Himalaya, the Ayurvedic skincare brand, dominated the category with a stunning 16.8% gain. British cult favorite Dr. Pawpaw exploded from 3.7% to 11.8%, a gain that reflects the brand’s growing mainstream appeal. Face the Future, the skincare specialist, also gained significant ground with a 4.9% increase.

Budget-friendly British brand Q+A continued its momentum, rising 4%, while prestige names like Guerlain and Tous each gained 3.8%.

Italian natural beauty brand L’Erbolario saw the steepest decline, with visibility dropping by 9%. Haircare brand Noughty fell 6.1%, and eco-beauty brand So Eco declined by 5.1%.

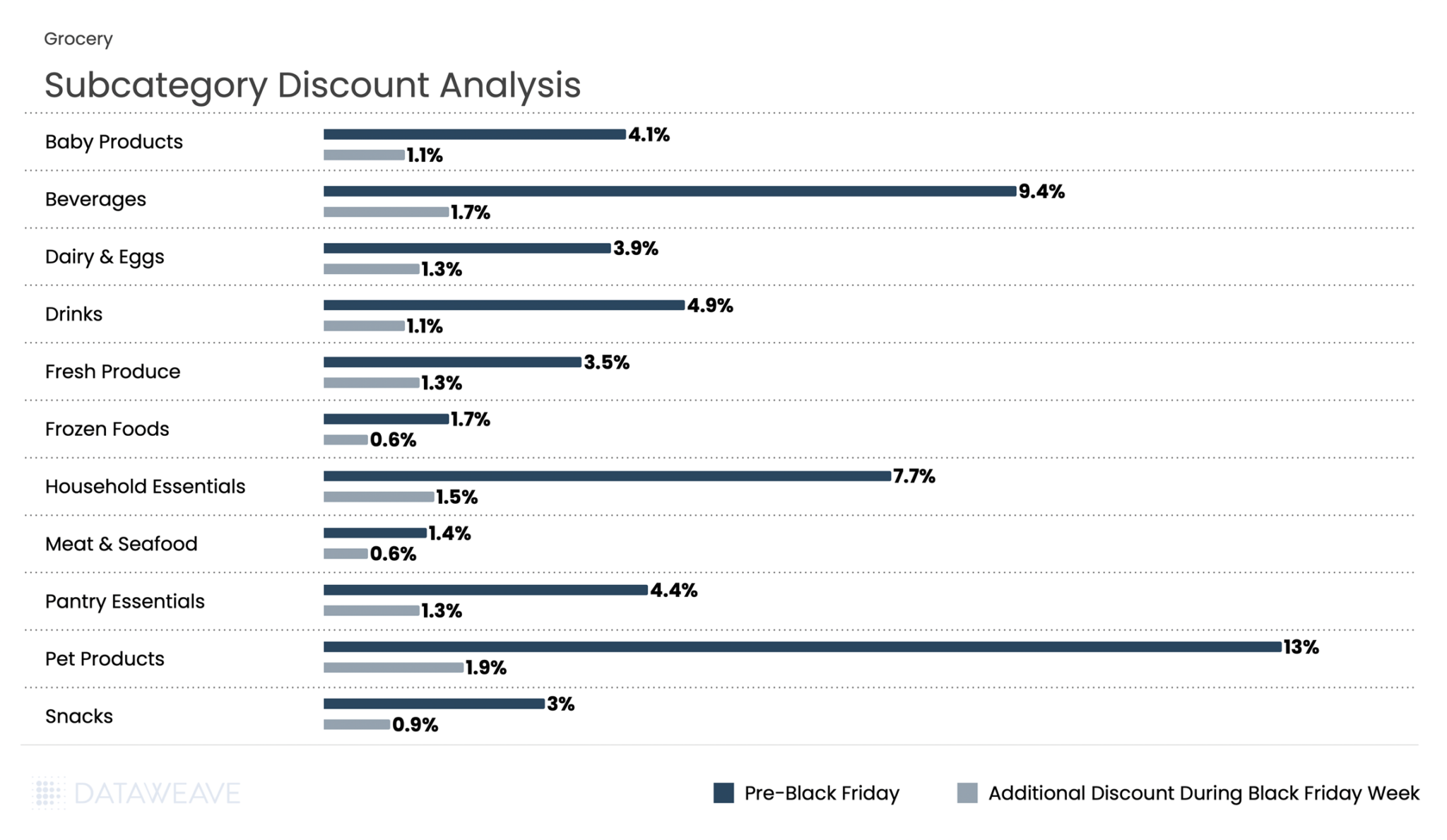

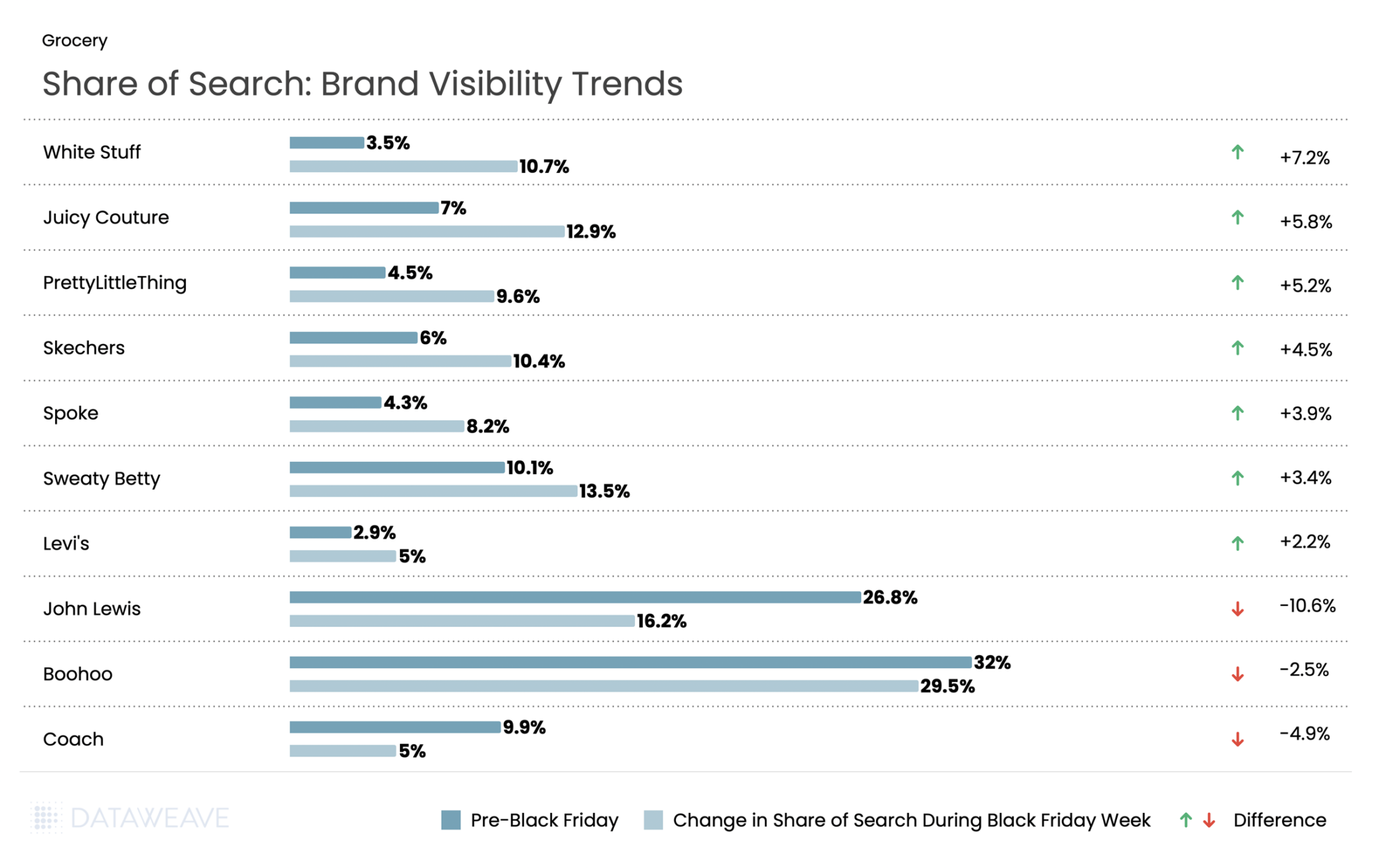

Grocery

While Grocery typically sees more modest discounts compared to discretionary categories, the sector remains a critical part of Black Friday shopping in the UK, particularly as consumers prepare for holiday entertaining and gifting. Our analysis of 11,979 SKUs shows how UK retailers approached promotions across essential and indulgent subcategories.

Subcategory Discount Analysis

Grocery had the lowest discounts across all categories, reflecting the already-thin margins in food retail. Pre-Black Friday discounts averaged just 5.7%, with Black Friday Week adding only 1.2%. Pet Products led pre-sale discounts at an impressive 13%, significantly outpacing other grocery subcategories.

Beverages and Household Essentials followed with 9.4% and 7.7% pre-sale discounts respectively, and maintained their lead during Black Friday Week with 1.7% and 1.5% additional discounts each. Fresh categories like Meat & Seafood (1.4% pre-sale, 0.6% Black Friday Week) and Frozen Foods (1.7% pre sale, 0.6% additional discounts during Black Friday week) saw minimal promotional activity, consistent with perishable inventory constraints and tight margins.

Share of Search: Brand Visibility Trends

Doritos led with a 7.3% surge in visibility. Pepsi delivered an equally impressive performance, rising from 3.6% pre Black Friday to 10.7% during Black Friday week. Fanta too saw 5.2% gain in share of search.

Conversely, Coca-Cola gained more modestly at 1.6%, while its Sprite brand actually declined 0.9%.

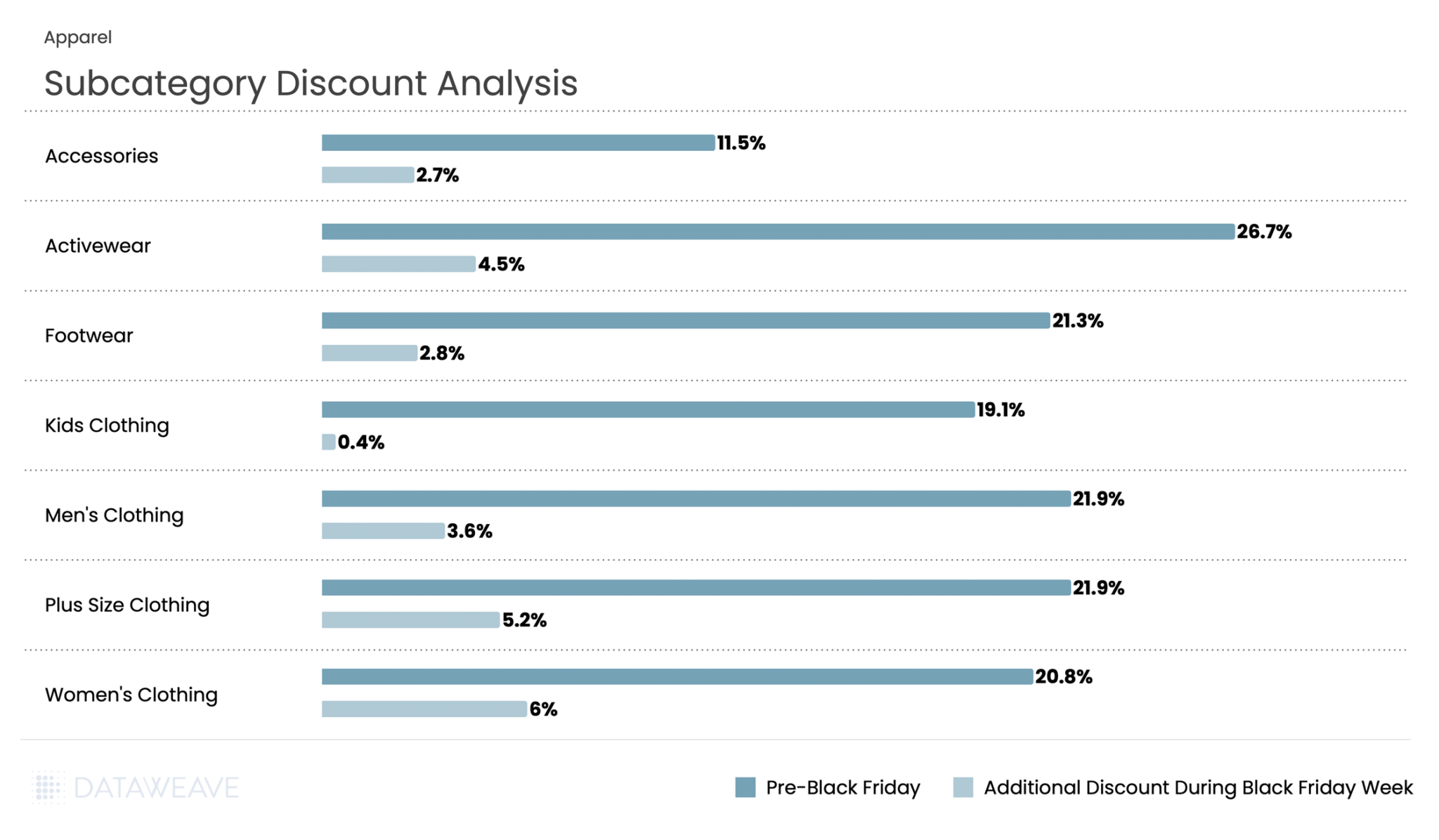

Apparel

Apparel remains a Black Friday staple in the UK and is projected to deliver the strongest year-on-year growth of any UK retail segment this festive season. With clothing accounting for 39% of planned Black Friday purchases, the category represents one of the most hotly contested battlegrounds during the sales period.

Our analysis of 17,063 SKUs, the largest category in our study, reveals interesting patterns across fashion segments that demonstrate both the opportunities and competitive intensity in UK apparel retail.

Subcategory Discount Analysis

Apparel showed the strongest discounting activity throughout the BFCM period among all categories. Pre-Black Friday discounts averaged 17.2%, with Black Friday Week adding 3.5%, making it one of the most heavily promoted categories.

Activewear led pre-sale discounts at an impressive 26.7%, with an additional 4.5% discount during Black Friday week. Plus Size Clothing and Men’s Clothing tied for second place in pre-sale discounts at 21.9% each. Notably, Plus Size Clothing saw the highest Black Friday Week discount at 5.4%.

Women’s Clothing saw robust discounts throughout, with 20.8% pre-sale and an additional 6% during Black Friday Week (the highest additional discount in the category).

Share of Search: Brand Visibility Trends

White Stuff, the British lifestyle brand, saw a 7.2% surge in visibility during Black Friday. Y2K fashion made a statement as Juicy Couture jumped 5.8 %. Fast fashion player Pretty Little Thing gained in visibility by 5.2%. Comfort brands performed strongly, with Skechers gaining 4.5% and activewear specialist Sweaty Betty rising 3.4%. Even premium denim brand Levi’s gained ground, increasing share of search by 2.2%.

However, retail giants faced significant visibility challenges. John Lewis saw the steepest decline in the Apparel category, with share of search dropping by 10.6% during Black Friday week. Fast fashion giant Boohoo declined 2.5%. Premium accessory brand Coach’s share fell 4.9%.

The data suggests UK consumers gravitated toward distinctive brands with clear identities during Black Friday, whether heritage British labels, Y2K nostalgia, or comfort-focused specialists, rather than generalist retailers or fast fashion platforms.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Black Friday 2025 shattered records once again. U.S. consumers spent a record $11.8 billion online on Black Friday, a 9.1% increase from 2024 and the first time online sales exceeded $11 billion. The National Retail Federation (NRF) projects holiday retail sales (November-December) to grow 3.7% to 4.2% over 2024, with total holiday spending expected to surpass $1 trillion for the first time ever. Against this backdrop of robust consumer spending, how did leading retailers and brands perform across key categories this Black Friday?

At DataWeave, we conducted a detailed analysis of Black Friday 2025 pricing trends across five major categories: Consumer Electronics, Home & Furniture, Health & Beauty, Grocery, and Apparel. Our AI-powered pricing intelligence platform monitored nearly 80,000 SKUs across leading U.S. retailers like Amazon, Walmart, Target, Macy’s, Home Depot, Sephora, and more, revealing interesting patterns in how retailers and brands approached this year’s sale season.

Our Methodology

For this analysis, DataWeave monitored average discounts across leading U.S. retailers during two distinct periods:

Pre-Black Friday: Up to November 23, 2025 – capturing early holiday deals and baseline pricing

Additional Discounts During Black Friday Week: November 24 – December 1, 2025 – covering Thanksgiving week through Black Friday (November 28) and Cyber Monday (December 1)

Our sample encompassed the top-ranked products across subcategories on major retail sites. We also analyzed Share of Search data, which measures brand visibility by monitoring which brand names appear in the top 20 search results for critical keywords.

Black Friday 2025: The Big Picture

Here’s the snapshot of average discounts during the Pre-Black Friday period compared to Black Friday Week:

Key Insight: Pre-Black Friday discounts were significant across all categories. This suggests retailers front-loaded their promotions to capture early holiday shoppers, with additional discounts during Black Friday Week adding to the baseline discounts already in place.

Consumer Electronics

Consumer electronics remain one of the most anticipated categories during Black Friday and Cyber Monday. Notably, AI traffic to retail websites grew 805% year-over-year, with consumers using AI tools most frequently for video games, appliances, and electronics categories. Our analysis of 10,356 SKUs reveals how discounts varied across subcategories.

Subcategory Discount Analysis

In Consumer Electronics, Pre-Black Friday discounts averaged 14.6% across subcategories, while Black Friday Week saw an additional 2.6% discount on average. Audio & Video products led the pre-sale discounting at 17.5%, indicating retailers were eager to move inventory early. During Black Friday Week, Audio & Video, Accessories, and Wearables saw the highest additional discounts (2.9-3 %), while Computers and Storage had already been heavily discounted pre-sale, leaving minimal room for further reductions during the main event.

Share of Search: Brand Visibility Trends

Our Share of Search analysis reveals significant shifts in brand visibility during Black Friday Week:

The Takeaway: Our analysis reveals significant shifts in brand visibility during Black Friday Week compared to the pre-sale period. Computing and mobile-focused brands like Apple and Asus gained substantial ground, while audio brands like Logitech, JBL, and Beats saw their visibility plummet. Apple’s Share of Search jumped from 1.58% to 6.2%, a gain of 4.6%, suggesting strong promotional activity or heightened consumer interest. Meanwhile, Logitech dropped nearly 8%, from 9.9% to just 1.2%.

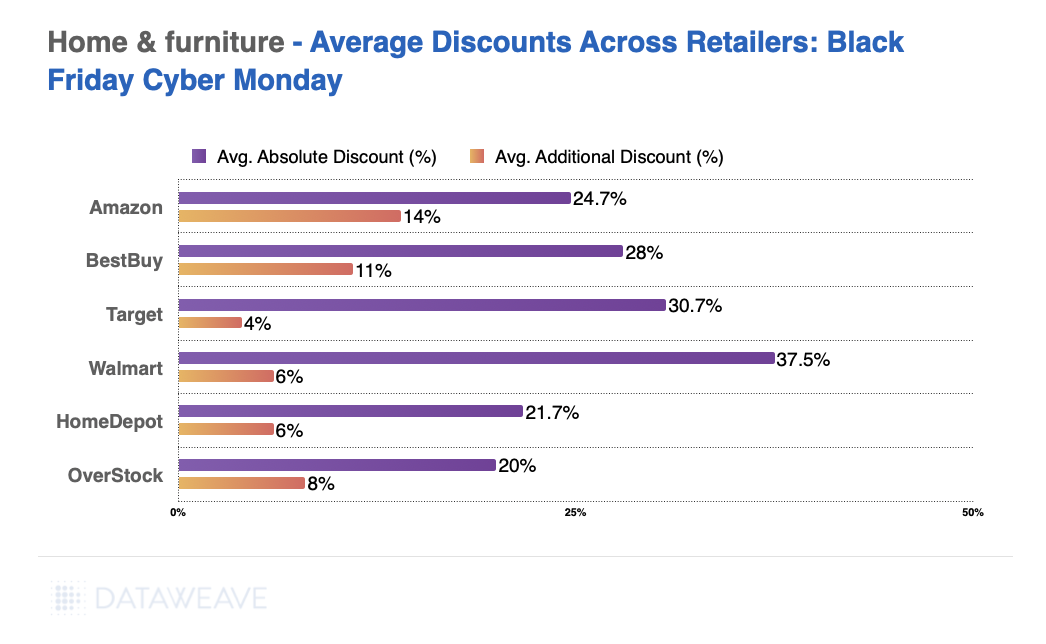

Home & Furniture

The Home & Furniture category continues to be a consumer favorite during Black Friday. Our analysis of 12,610 SKUs shows how discounts were distributed across subcategories.

Subcategory Discount Analysis

Home & Furniture saw Pre-Black Friday discounts averaging 13.9%, with Black Friday Week adding just 1.7% on average, the second-lowest additional discount among all categories. Bedding led pre-sale discounts at an impressive 18.6%, followed by Furniture at 16.4% and Outdoor at 15.1%. This suggests retailers aggressively promoted home goods early in the season to capture deal-seekers.

During Black Friday Week, Bedding maintained leadership with 2.4% additional discounts, while Kitchenware saw the smallest bump at just 0.9%, indicating early promotions had already captured most of the discount opportunity.

Share of Search: Brand Visibility Trends

The Takeaway: The Home & Furniture category saw some of the most dramatic Share of Search swings in our entire analysis. Emerging and value-oriented brands dominated the gains, with Swedrea surging from 8.7% to 19.6%, a remarkable 10.8% increase. Similarly, Clickbin and Costway each gained over 9%. On the flip side, established premium brands like Beautyrest and Livabliss saw sharp visibility declines, dropping over 7-8%.

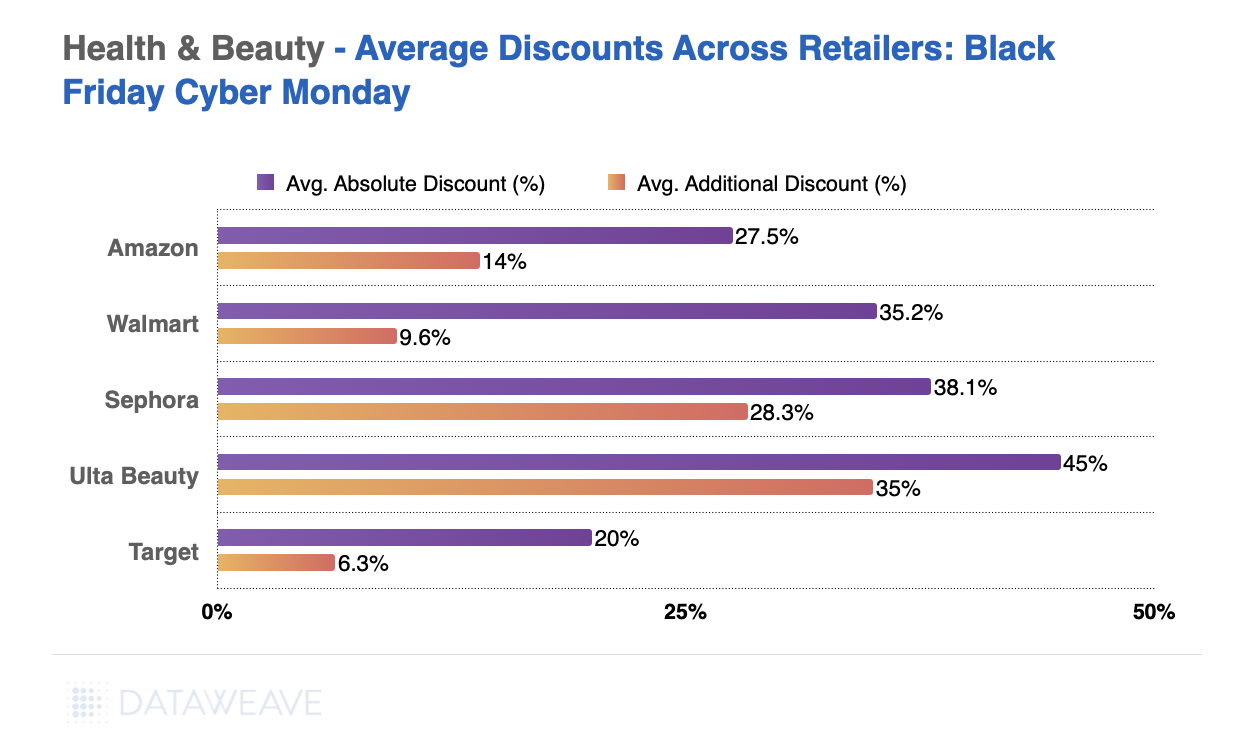

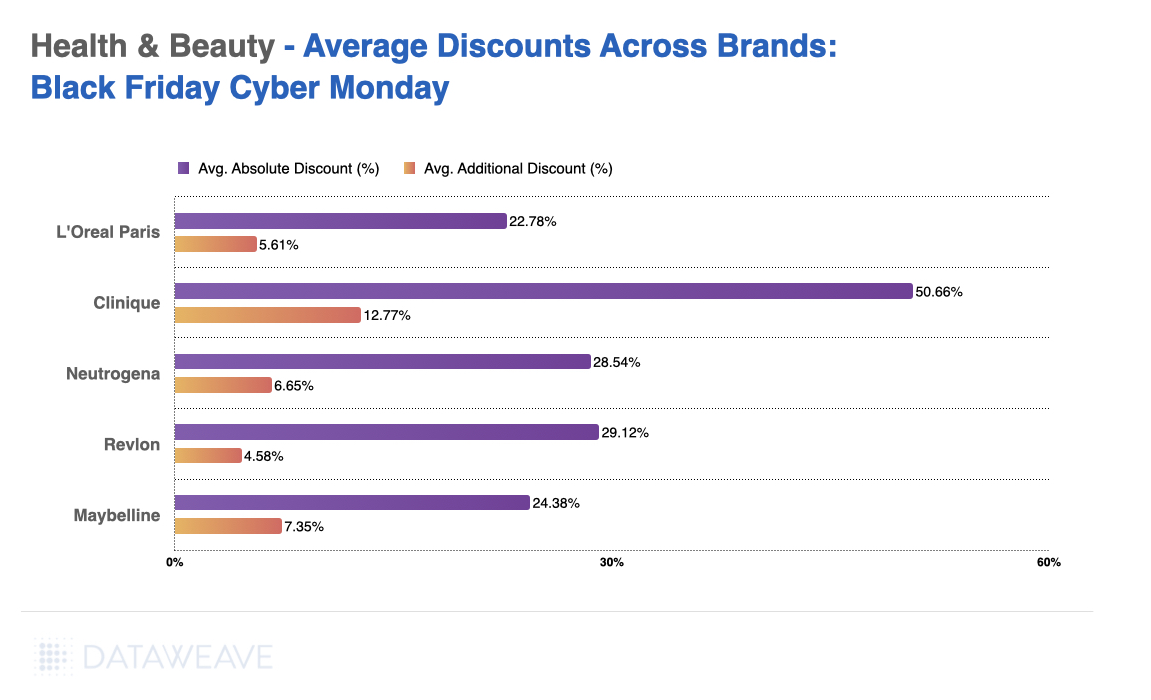

Health & Beauty

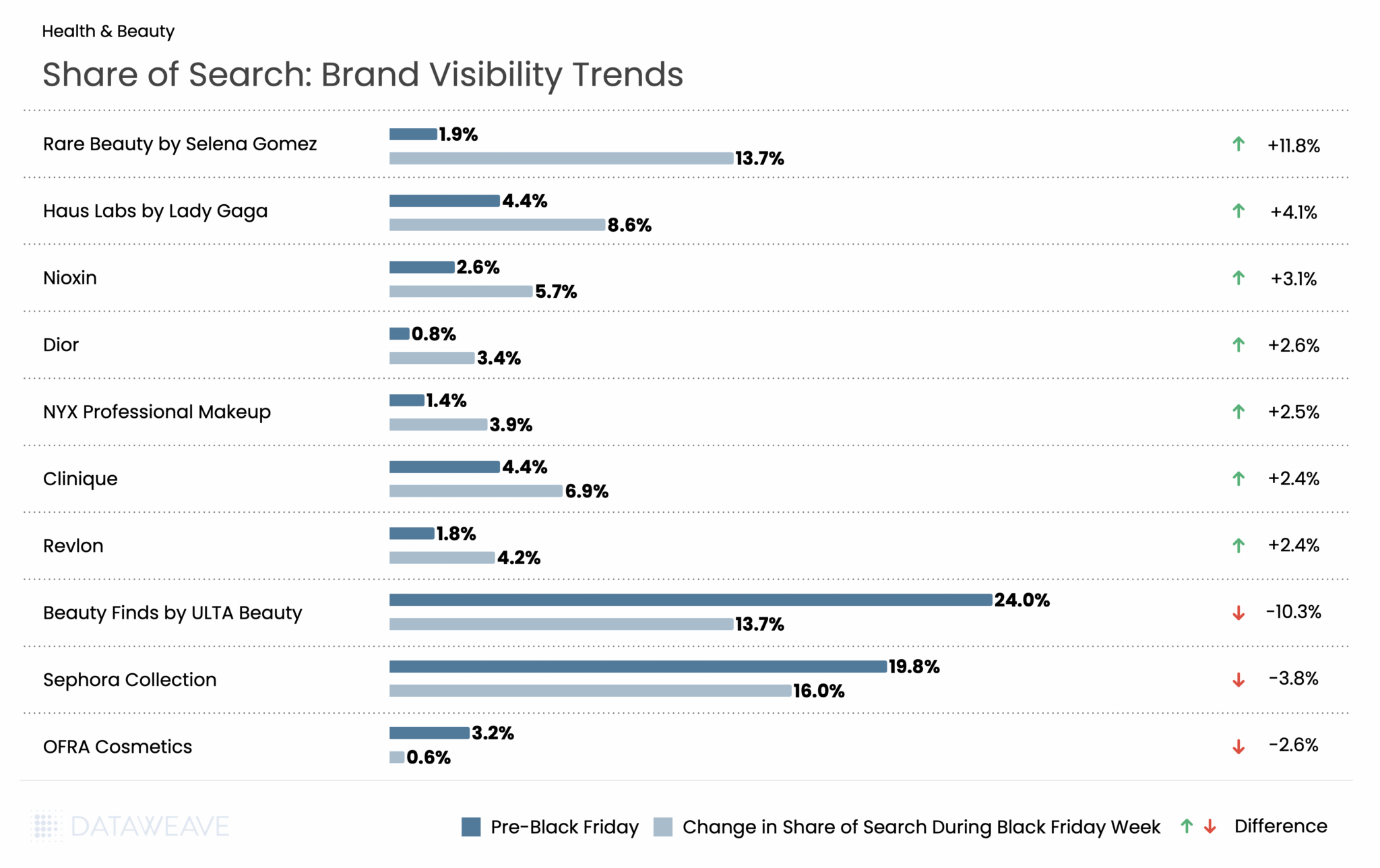

Health & Beauty has emerged as a growth engine during Black Friday. The beauty industry is projected to grow 5% annually through 2030 according to a McKinsey survey. Our analysis of 16,141 SKUs reveals subcategory-level insights.

Subcategory Discount Analysis

Notable finding: Health & Beauty presented a unique discounting pattern compared to other categories. Pre-Black Friday discounts averaged just 7.1%, the second-lowest among all categories. But Black Friday Week discounts were relatively strong at 4.8%. This indicates the Beauty category held back more discounts for the main event.

Notably, Hair Care was the only subcategory across our entire analysis where Black Friday Week discounts (6%) exceeded Pre-Black Friday discounts (4.6%), suggesting retailers strategically saved their best hair care promotions for the big weekend. Fragrance led pre-sale discounts at 13%, making it an attractive early shopping category.

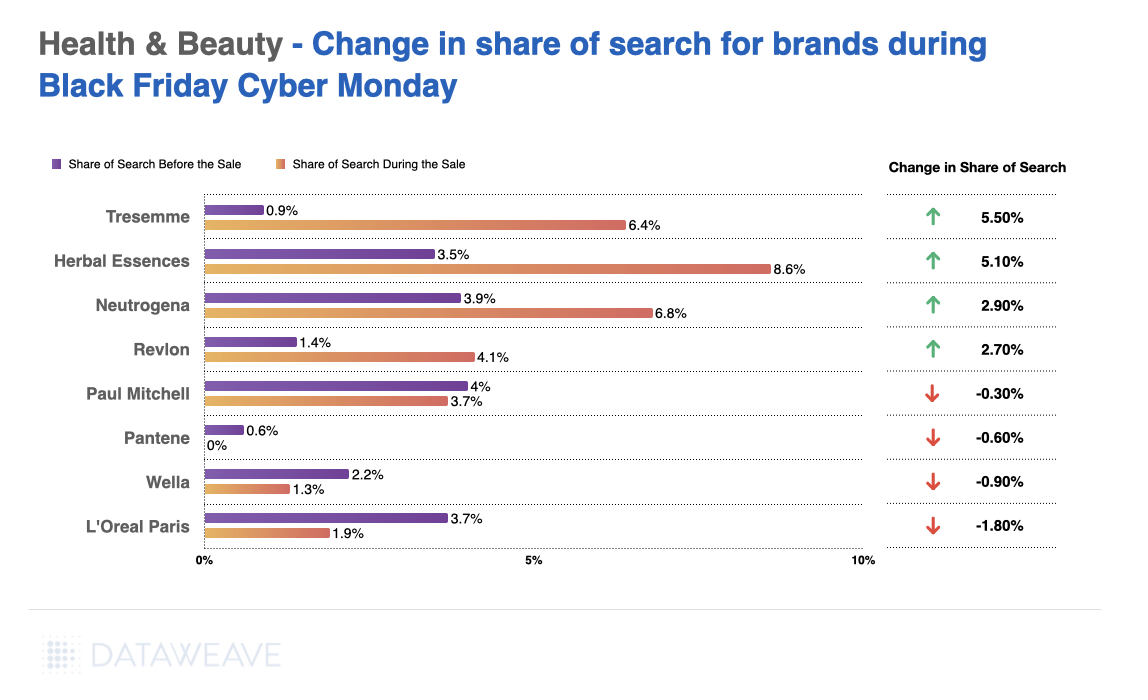

Share of Search: Brand Visibility Trends

Health & Beauty saw some of the most dramatic Share of Search swings in our analysis, driven largely by celebrity-backed brands. Rare Beauty by Selena Gomez exploded from just 1.9% to 13.7%, a whopping 11.8% gain that made it the biggest winner across all categories. Haus Labs by Lady Gaga also surged (+4.1%), while prestige brands like Dior (+2.6%) and Clinique (+2.4%) gained ground.

The flip side? Retailer private labels took a hit: Beauty Finds by ULTA Beauty collapsed from 24% to 13.7% (-10.3%), and Sephora Collection dropped from 19.8% to 16.0% (-3.8%).

Key Takeaway: The Beauty category tells a compelling story about the power of celebrity brands during Black Friday. The Share of Search shifts appear to reflect how retailers and brands recalibrated their promotional focus for Black Friday. Celebrity-driven lines rose sharply in visibility, suggesting stronger placement, promotion, or search prioritization during the sale period. At the same time, private-label ranges from ULTA and Sephora lost ground, indicating a pivot away from house-brand visibility in favor of more spotlighted national and prestige brands throughout the event.

Grocery

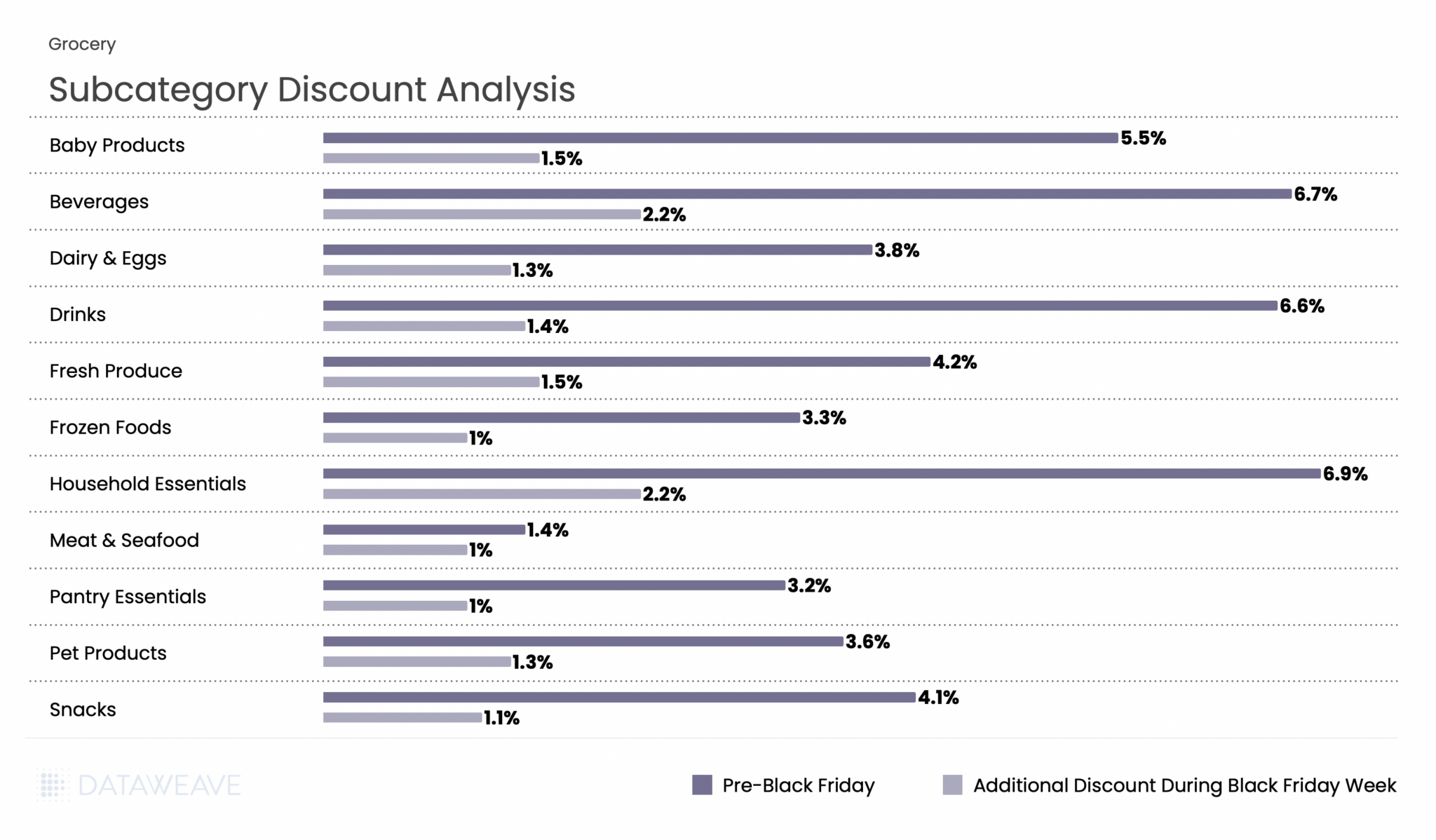

While Grocery typically sees more modest discounts compared to discretionary categories, the sector remains a critical part of Thanksgiving weekend shopping. According to the National Retail Federation, grocery stores and supermarkets ranked as the third most popular shopping destination during Thanksgiving weekend, with 40% of consumers making purchases there. Our analysis of 18,823 SKUs shows how retailers approached promotions across essential and indulgent subcategories.

Subcategory Discount Analysis

Grocery had the lowest discounts across all categories, reflecting the already-thin margins in food retail. Pre-Black Friday discounts averaged just 5.2%, with Black Friday Week adding only 1.5%. Household Essentials and Beverages led pre-sale discounts at 6.9% and 6.7% respectively, and maintained their lead during Black Friday Week with 2.2% additional discounts each. Fresh categories like Meat & Seafood (1.4% pre-sale, 1% Black Friday Week) and Frozen Foods (3.3%, 1%) saw minimal promotional activity, consistent with perishable inventory constraints and tight margins.

Key Takeaway: Grocery discounting remains conservative, with shelf-stable and household items seeing the most promotional activity. The Beverages and Household Essentials subcategories, which have longer shelf life and higher margins, were the primary battleground for grocery promotions during BFCM 2025.

Share of Search: Brand Visibility Trends

The Grocery category saw some surprising Share of Search swings during Black Friday Week. Most notably, there was a dramatic divergence between beverage giants: Sprite surged from 1.7% to 6.8% (+5.1%), while Coca-Cola collapsed from 6% to just 0.1% (-5.9%). This stark contrast suggests vastly different promotional strategies or algorithmic visibility changes between the two brands. Private label 365 by Whole Foods Market continued its steady rise, gaining 3%, reflecting ongoing consumer interest in store brands as shoppers seek value.

The Sprite vs. Coca-Cola divergence is one of the most striking findings in our analysis. Additionally, brands like Amy’s (organic/natural foods) and McCormick (spices/seasonings) gained significant visibility.

Apparel

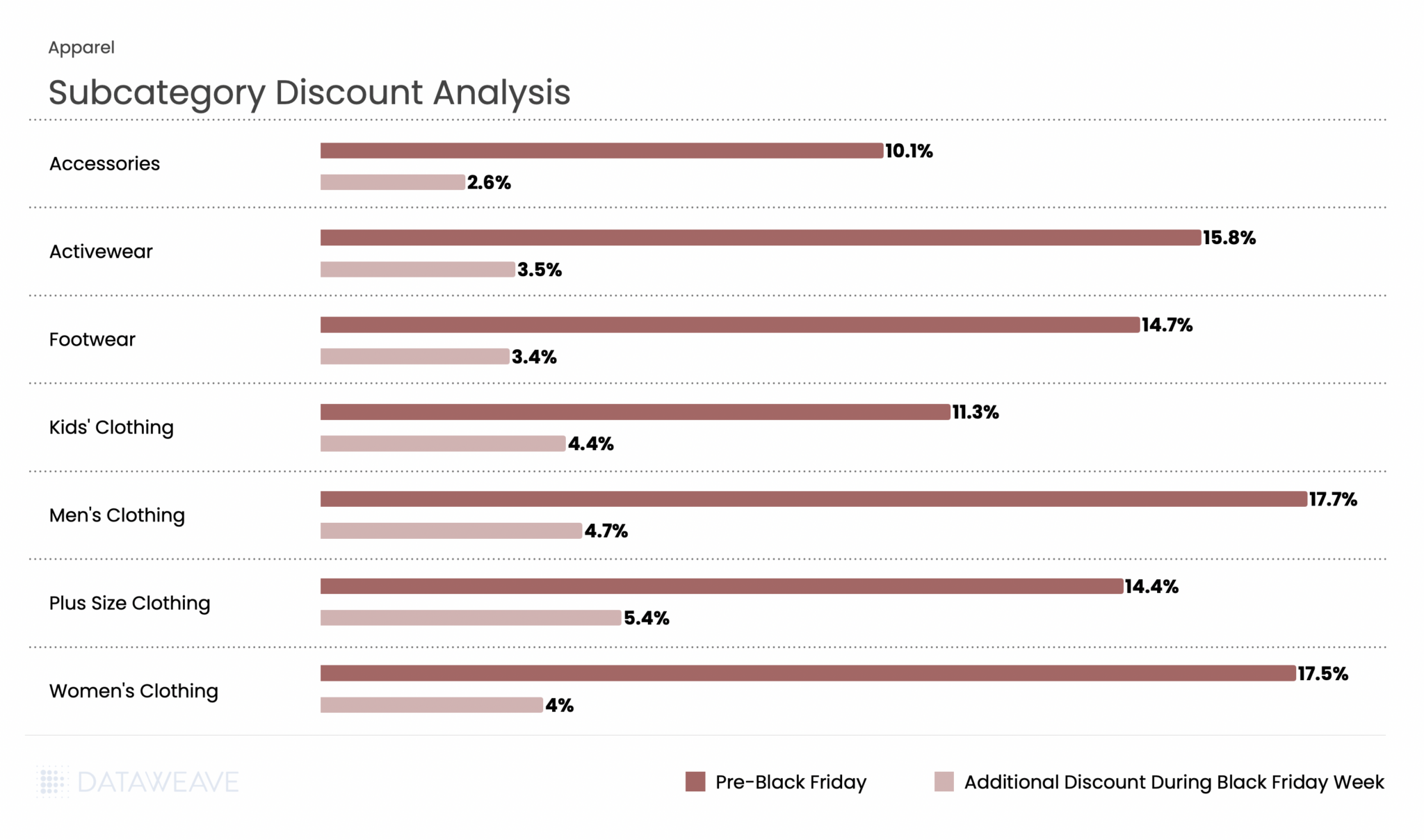

Apparel remains a Black Friday staple and performed strongly this year. Our analysis of 21,749 SKUs (the largest category in our study) reveals interesting patterns.

Subcategory Discount Analysis

Apparel showed strong discounting activity throughout the BFCM period. Pre-Black Friday discounts averaged 13.8%, with Black Friday Week adding 3.8%, the highest additional discount among all five categories. Men’s Clothing and Women’s Clothing led pre-sale discounts at 17.7% and 17.5% respectively, reflecting aggressive early promotions on core apparel. Interestingly, Plus Size Clothing saw the highest Black Friday Week discount at 5.4%, suggesting retailers pushed harder during the main event to drive conversions in this segment. Kids’ Clothing also saw strong Black Friday Week discounts at 4.4%.

Share of Search: Brand Visibility Trends

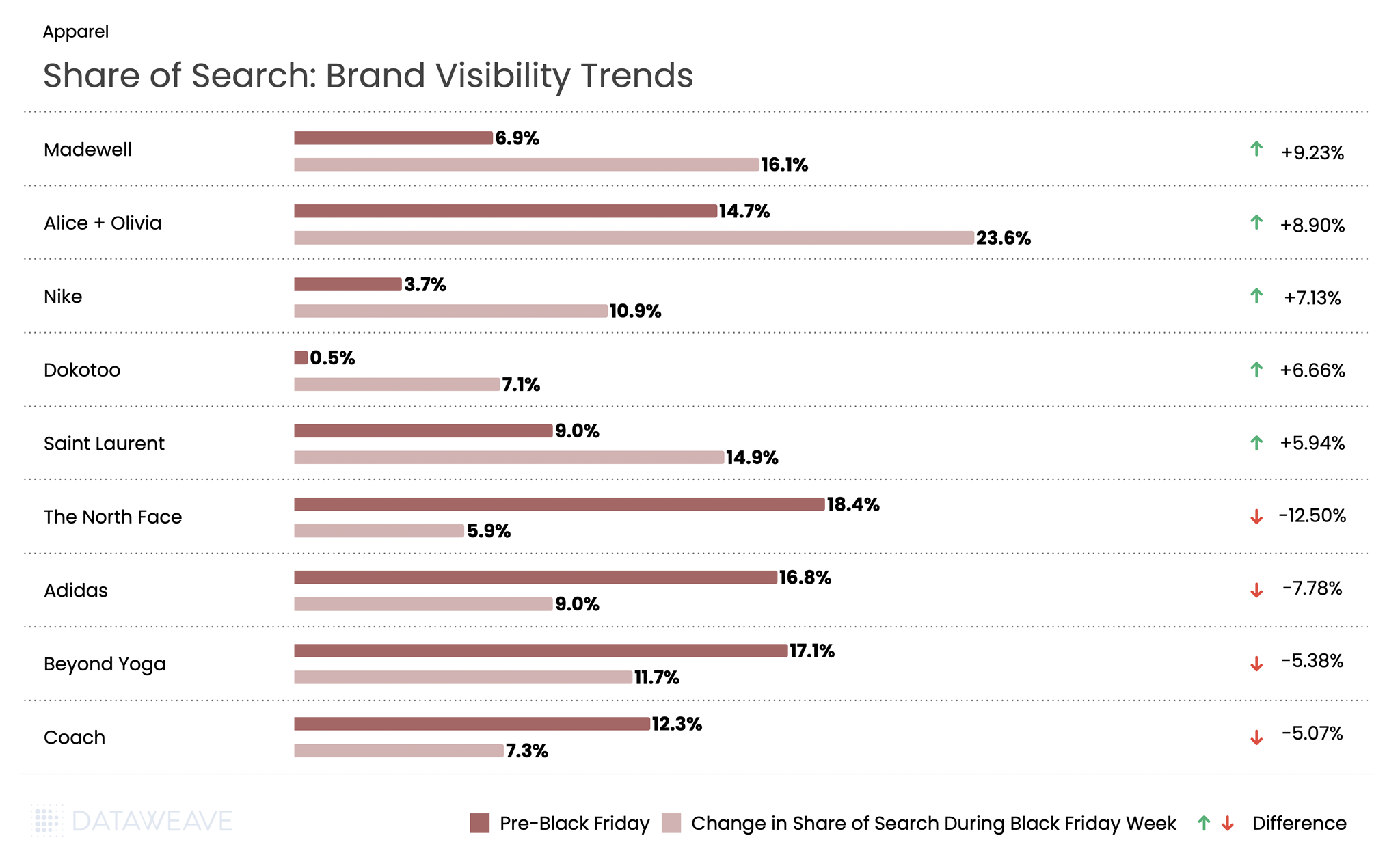

Apparel saw dramatic Share of Search movements during Black Friday Week. Fashion-forward brands dominated the gains: Madewell surged from 6.9% to 16.1% (+9.2%), while Alice + Olivia jumped from 14.7% to 23.6% (+8.9%). Nike also performed strongly with a 7.1% gain. Conversely, outdoor and athletic brands faced steep declines: The North Face dropped from 18.4% to 5.9%, a massive 12.5% decline, the largest in our entire analysis. Adidas fell 7.7%, Beyond Yoga declined 5.3%, and luxury brand Coach by 5%.

Key Takeaway: The data suggests fashion-forward and lifestyle brands (Madewell, Alice + Olivia, Saint Laurent) gained visibility at the expense of outdoor/athletic brands (The North Face, Adidas, Beyond Yoga). This could indicate that fashion brands invested more heavily in promotional visibility during the sale period.

Want to understand how DataWeave’s pricing intelligence platform can help your business make data-driven decisions during peak sales events? Contact us to learn more about competitive insights, price intelligence, assortment analytics, content analytics, and digital shelf analytics.

Follow our blog for more insights on retail pricing trends, brand visibility analysis, and data-driven commerce intelligence.

Tariffs can spike landed costs overnight, regulations rewrite labelling rules, and competitors slash prices before your team finishes its daily stand-up. And yet, some consumer brands thrive.

The winning brands see changes early, decide quickly, and execute flawlessly across the digital shelf. This post blends three decades of pricing and merchandising expertise with timely digital shelf insights from DataWeave, offering a clear path forward for brands navigating today’s volatile retail environment.

From Cost Shock to Chronic Uncertainty

Tariffs are no longer just one-off headlines; they’ve become an unpredictable, ongoing variable in the global marketplace. The true challenge isn’t always the duty rate itself, but the constant whiplash of not knowing if, when, or how much that duty will change. This pervasive uncertainty is having a tangible impact:

Unpredictable Competitive Response: Delaying price moves while watching competitors can erode margins as much as tariffs.

To stay ahead, pricing decisions must be stress-tested against multiple tariff scenarios and aligned with likely competitor reactions. Timing matters as much as accuracy, move too soon or too late, and margins suffer either way.

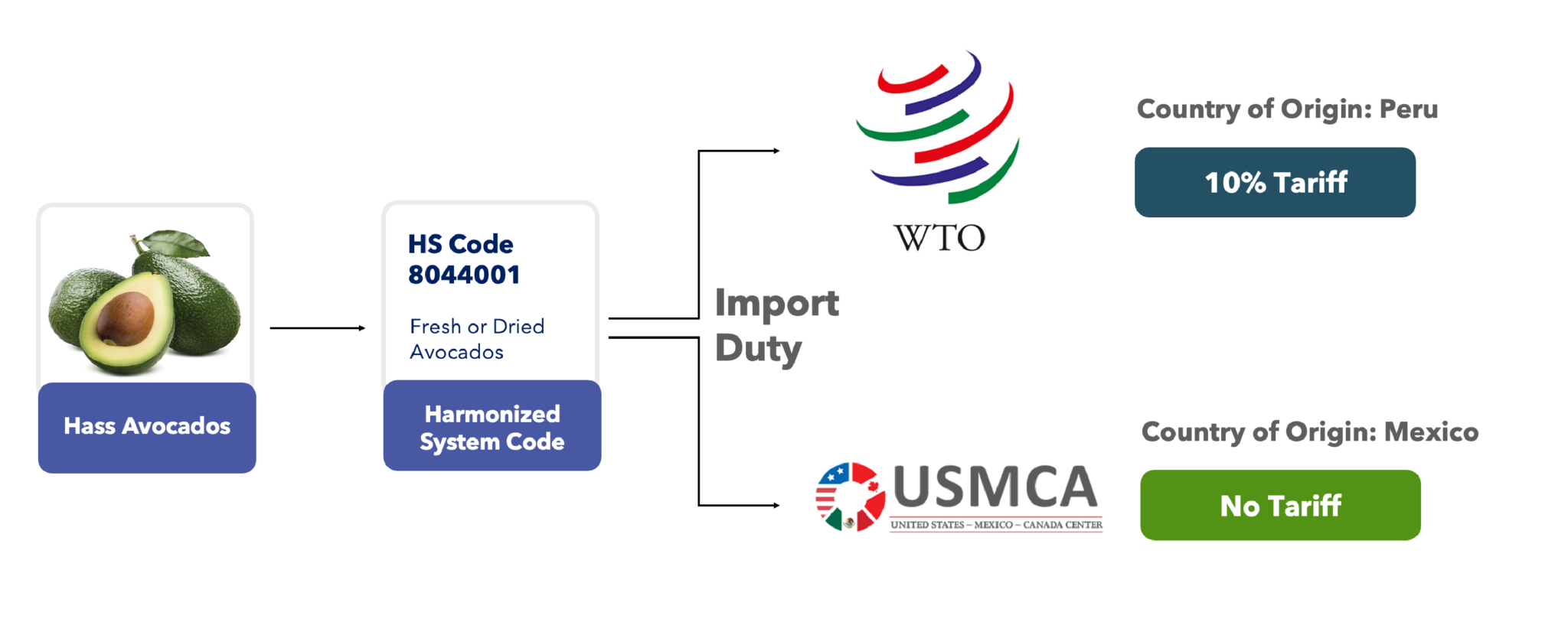

The Tariff Math No One Can Afford to Get Wrong

When it comes to tariff disruption, the difference between profit and loss often hinges on a precise understanding of a three-step process. Get any part of this chain wrong, and the financial ripple effect can undermine pricing and promotions. The duty you pay, therefore, is the direct result of the following three critical steps:

Step 1: Harmonized System (HS) Code

What it is: A six- to ten-digit classifier that drills down to product sub-types.

Why it matters: A single digit change can shift an item into a higher-tariff bracket.

Step 2: Country of Origin

What it is: The nation in which the imported item was made.

Why it matters: Mis-tagging the origin can lead to mis-pricing and inaccurate margin calculations.

Step 3: Trade-Agreement Overlay

What it is: Differentiation between the World Trade Organization (WTO) baseline tariffs and special trade agreements (e.g., USMCAUnited States-Mexico-Canada Agreement).

Why it matters: The same HS code can result in significantly different duties, up to a 10% swing, depending on the originating country (see the example below).

This isn’t just about paying the correct duty; it’s about safeguarding your bottom line in a global marketplace where every digit and every designation carries substantial weight.

The wrong origin, the wrong rule, the wrong margin.

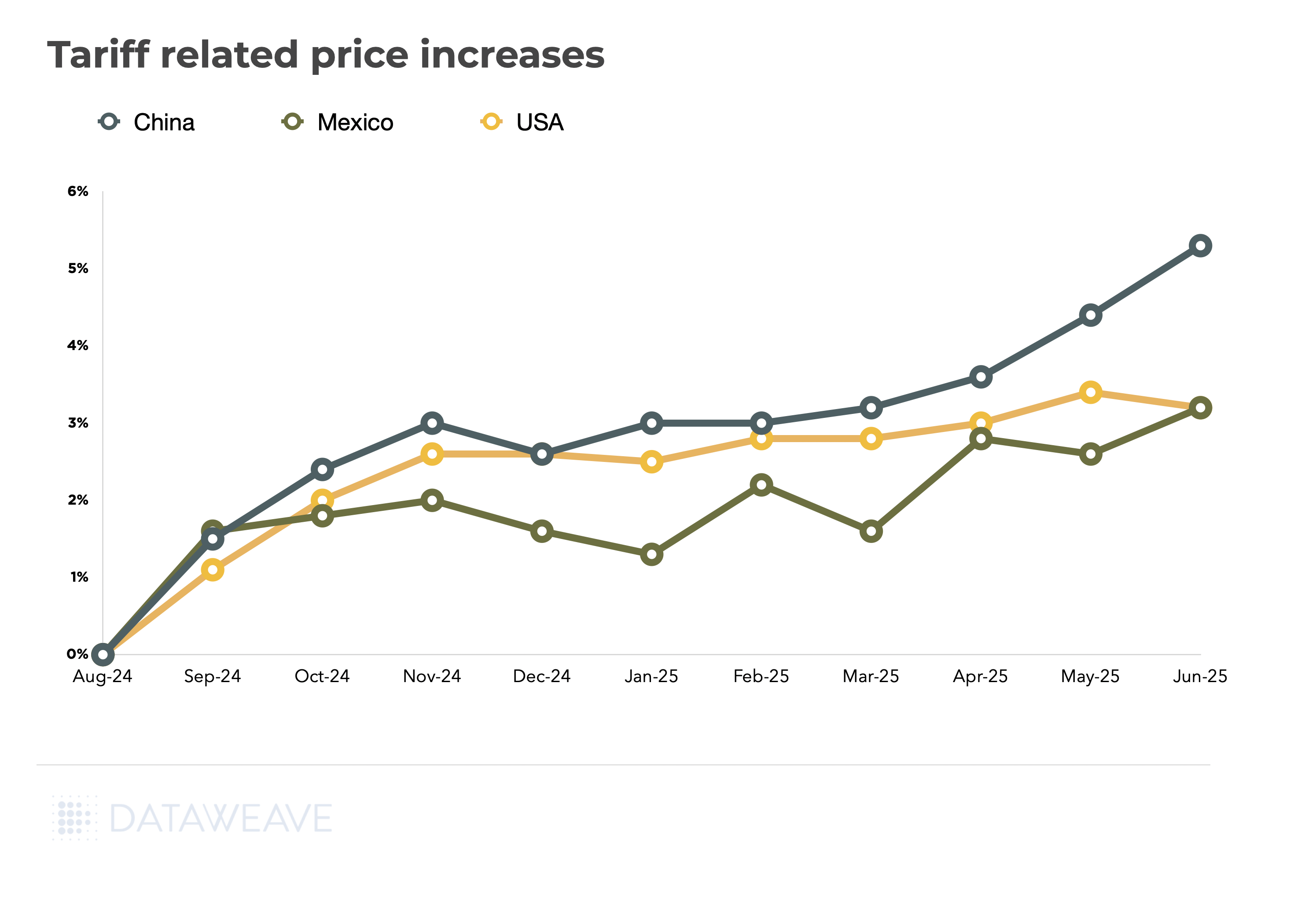

Hard Numbers: Where Prices Are Already Climbing

DataWeave’s latest digital shelf analysis shows import-driven price inflation diverging sharply by source country.

The intricate dance of HS codes, country of origin, and trade agreements directly translates into the prices consumers see. And the data doesn’t lie. Below, we delve into the hard numbers: where prices are already climbing, as illuminated by DataWeave’s latest digital shelf monitoring, showing significant import-driven price inflation by source country.

China: Products sourced from China are up 5%. This is largely attributable to the numerous tariffs currently imposed on Chinese goods.

Mexico: Prices for products from Mexico have risen by 3%.

United States: Interestingly, even U.S.-sourced products show a 3% increase.

This rise in U.S. product prices might seem counterintuitive if tariffs are solely focused on imports. However, the reality lies in the global supply chain for many products.

Consider guacamole as an example: While the final product might be “Made in the USA,” its components often come from various international sources. Avocados might be imported from Mexico, lime juice from Central America, and seasonings from India or China. Even packaging could originate in Asia. Each of these imported components can be subject to tariffs. Therefore, even if an item is assembled in the U.S., the tariffs on its constituent parts contribute to an overall price increase, explaining the rising rates for U.S.-sourced goods.

Action step: Map tariff exposure at both finished-goods and component-level to avoid “Made in USA” blind spots.

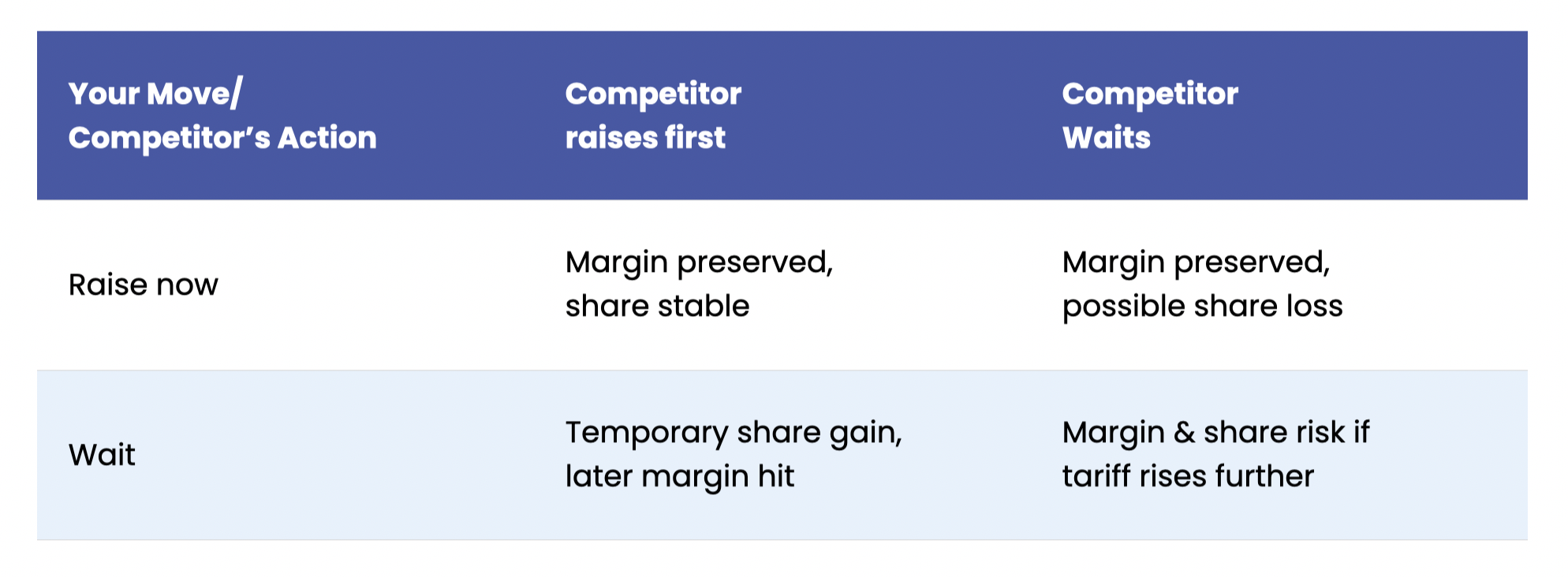

Timing Is a Competitive Weapon

With duty tables and competitor reactions changing fast, the question is: move first or follow? Early movers recoup cost fastest but risk overshooting if tariffs ease; laggards may enjoy a brief price advantage but suffer sudden margin compression.

The Strategic Dilemma

The table below illustrates this strategic choice and its potential outcomes:

Shrinkflation: Margin Patch or Trust Erosion?

Beyond direct price adjustments, many brands are turning to shrinkflation to manage tariff-driven cost pressure, shaving net weight instead of hiking prices. DataWeave’s analysis reveals an average package reduction of 5 – 6%, with extreme cases reaching 15 – 25%, sometimes even coupled with a shelf-price increase.

While this can cushion immediate margin, it comes at a significant cost: brand credibility. Savvy shoppers quickly spot these changes, sharing “before-and-after” photos online and fueling consumer frustration. What begins as a margin patch can rapidly erode trust and damage long-term loyalty.

Ultimately, navigating this volatile environment requires dynamic intelligence and a holistic pricing strategy that balances profitability with market share and, crucially, consumer trust.

Price Hikes May be Inevitable, But You Can Still Run Your Digital Shelf

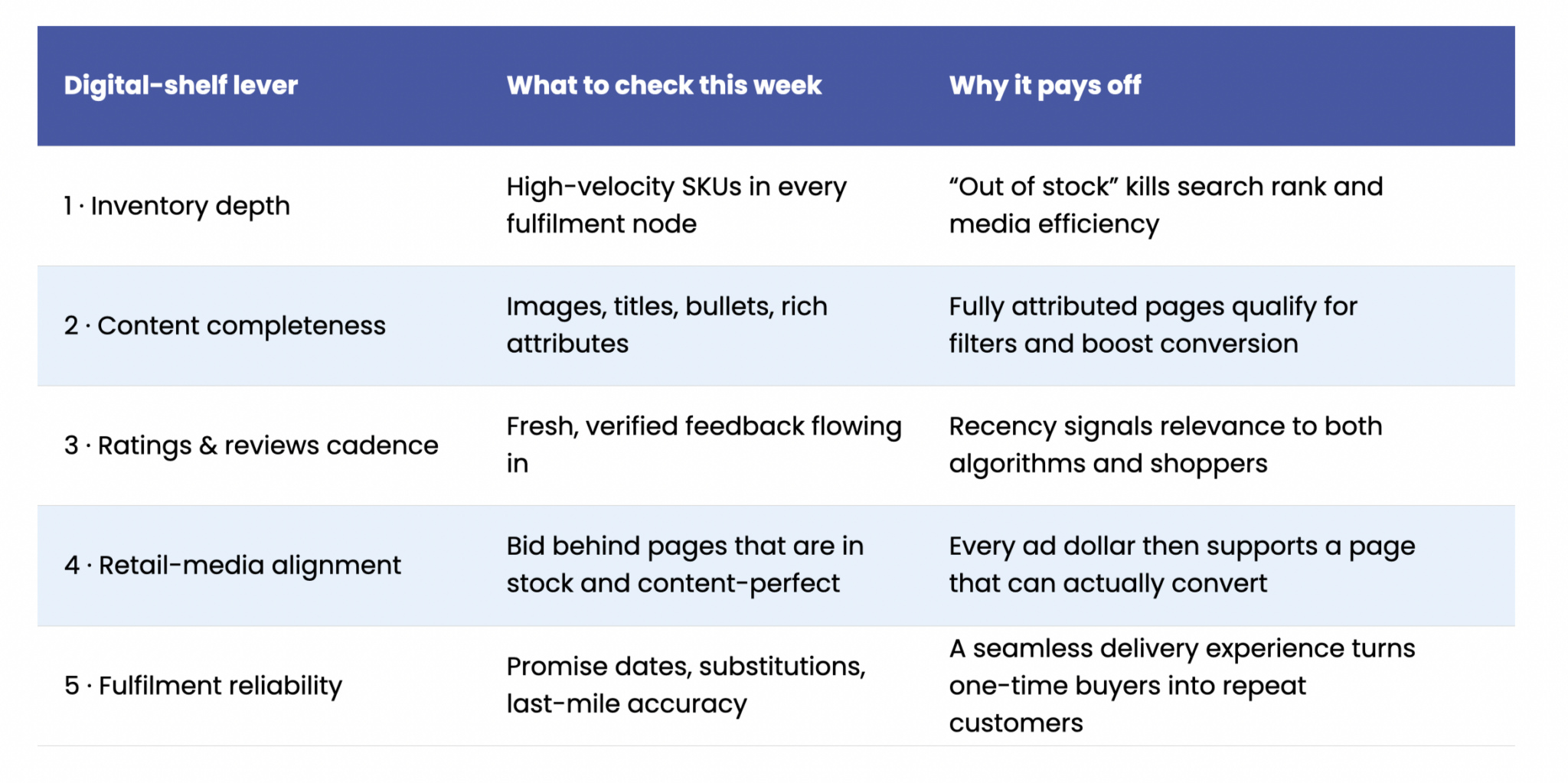

Tariff‑driven cost pressure can force list‑price increases, but it does not dictate how well your products show up, sell through, or satisfy shoppers online. Those outcomes still hinge on five levers that live entirely inside your control. Master them and you cushion margin hits while protecting (or even expanding) share.

The Five Levers of Digital‑Shelf Control

Inventory Depth – Maintain online in‑stock rates above 95 percent for high‑velocity SKUs and flag substitute logic when unavoidable out‑of‑stocks occur.

Content Quality & Accuracy – Keep titles keyword‑rich, imagery crisp, and attributes complete so search filters never bury you.

Ratings & Reviews Cadence – Proactively request fresh reviews to earn retailer search boosts and reassure value‑conscious shoppers.

Retail‑Media Precision – Bid where pages are healthy and in‑stock; pause spend on broken listings that leak conversion and ROAS.

Fulfillment Excellence – Monitor pick‑pack accuracy, on‑time delivery, and substitution rates; each one influences retailer algorithmic visibility.

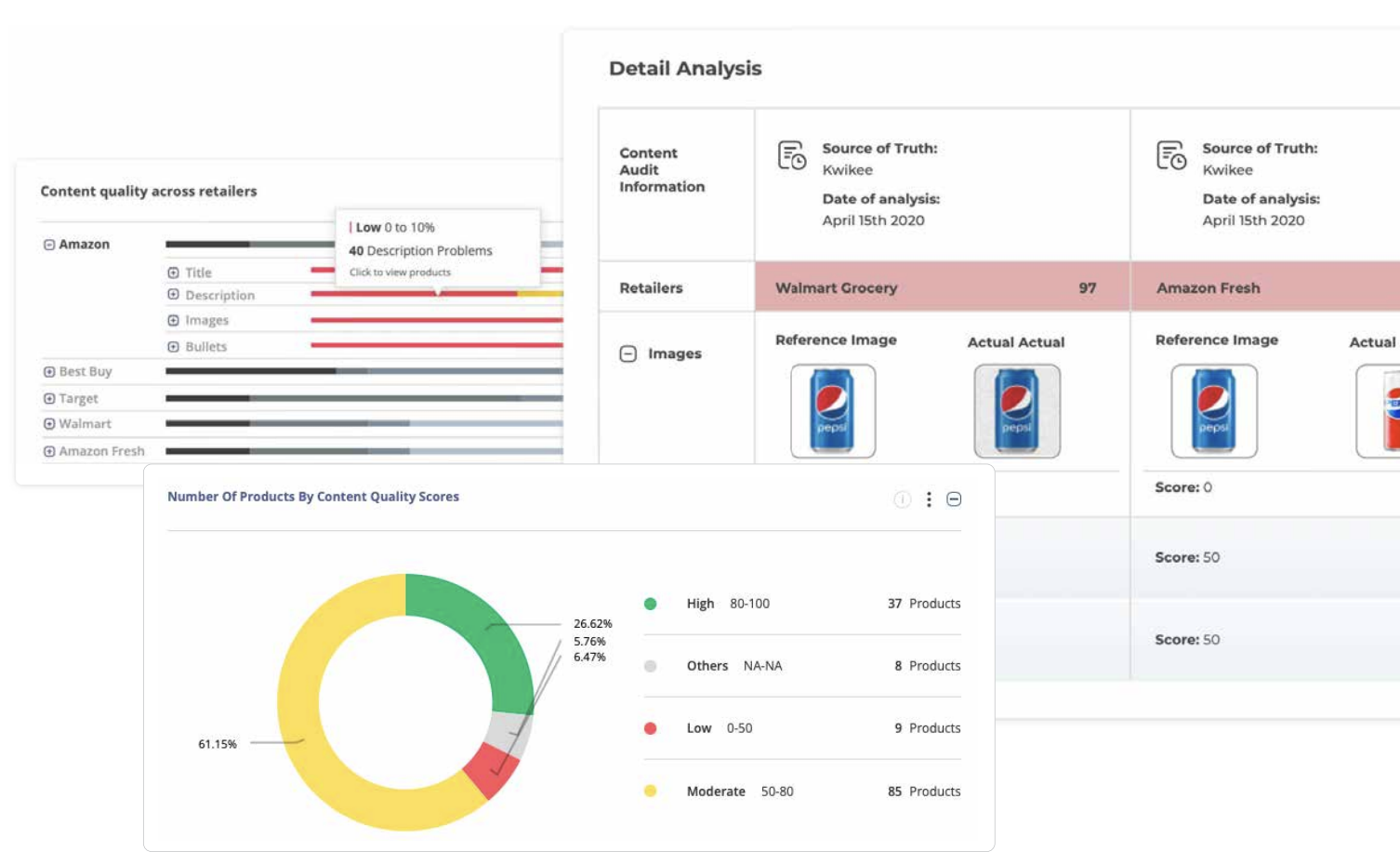

Content Hygiene Keeps You Visible, Compliant, and Conversion-Ready

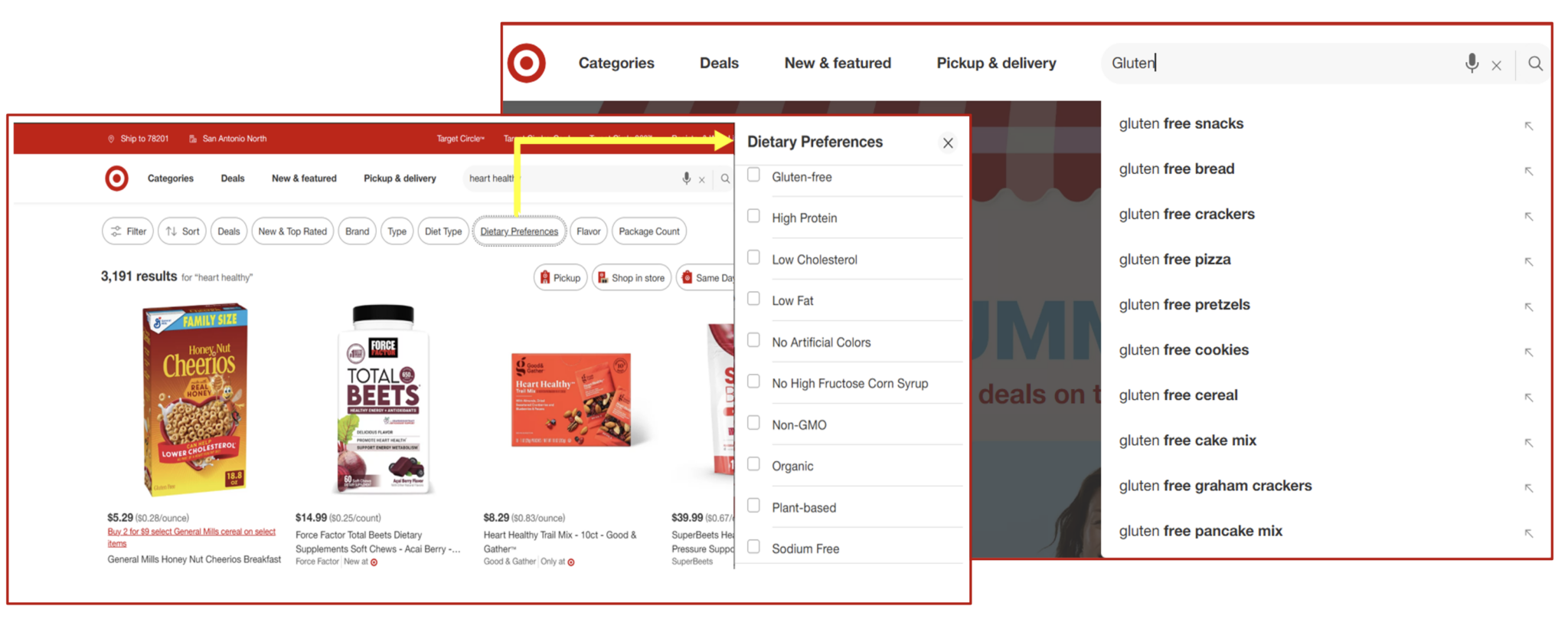

Missing or incorrect product attributes (e.g., “gluten-free,” “caffeine content”) can swiftly jeopardize both regulatory compliance and your product’s fundamental search visibility. Simply put, if it’s not labeled right, it won’t be found.

This impact plays out in two crucial areas:

Retailer Search Visibility: Filter logic on major e-commerce platforms like Target.com, Walmart.com, and Instacart is increasingly driven by precise attribute tags (e.g., “gluten-free,” “BPA-free,” “0g added sugar”). Fail to provide or correctly format these claims, and your product will simply never appear when shoppers apply these critical search filters. You become invisible to a motivated audience.

Regulatory Compliance: Global regulatory bodies, including the U.S. FDA and EU authorities, now treat online product detail pages as officially regulated labeling space. This means that a single missing allergen statement or an inaccurate nutritional claim can trigger severe consequences, from product takedowns and hefty fines to a devastating “straight-to-zero” share of search. Non-compliance isn’t just a legal risk; it’s a direct threat to your market presence (see example below).

The Hygiene Playbook: Audit → Score → Fix → Grow

Your Product Detail Pages (PDPs) are your digital storefronts, and they need to be impeccable. Modern content-intelligence tools are like vigilant auditors, constantly scanning, structuring, and scoring every PDP across your retail network.

Tools like DataWeave do the heavy lifting by:

Surfacing critical gaps: They’ll pinpoint issues like blurry images, inaccurate titles, or missing nutrition information.

Optimizing for search: They ensure your product attributes align with live search filters, turning claims into clicks.

Flagging compliance risks: You’ll know about potential issues before regulators or retail partners ever do.

Quantifying your impact: Get a clear Content Quality Score that your teams can own and improve, week after week.

When you execute this well, it’s not just about tidying up; it’s a powerful growth engine. This proactive approach fuels every step of the digital customer journey – from getting found, to winning the click, converting the cart, and ultimately, capturing reviews that boost your search rankings.

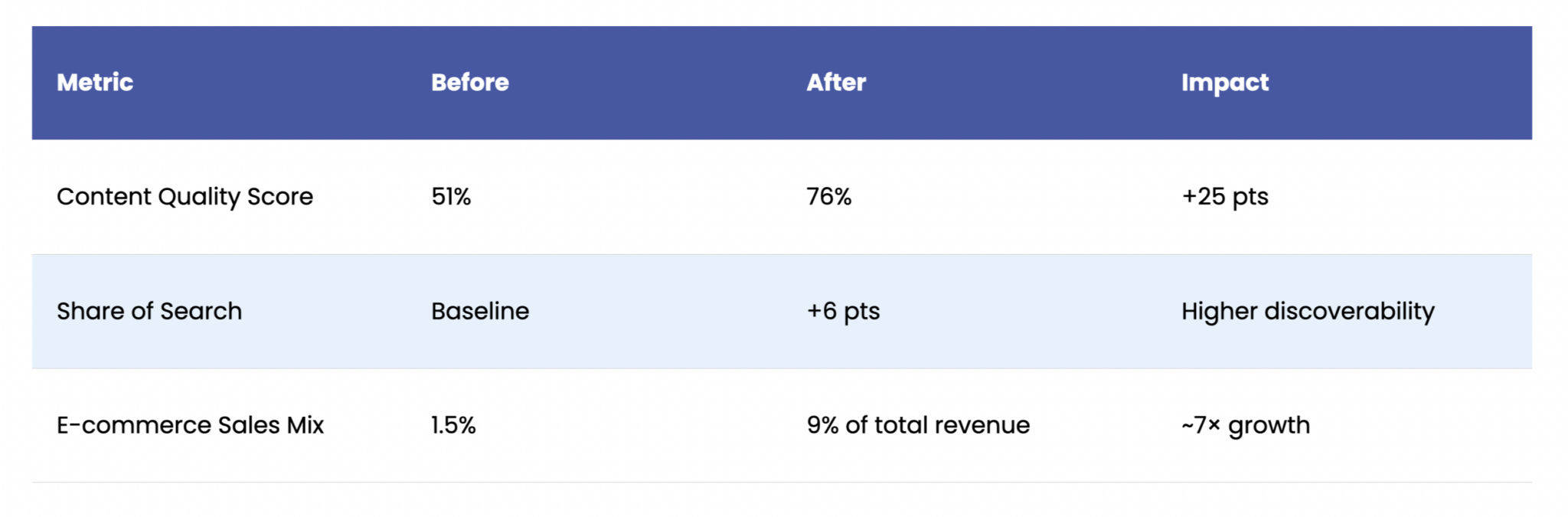

A Case Study: Bush’s Beans Converts Visibility into Revenue

Before Bush’s Beans achieved rapid success with their “audit → scorecard → rapid-fix” approach, they confronted a significant hurdle. Here’s how they overcame it to drive impressive revenue growth.

The Challenge

Bush’s Beans saw its e-commerce contribution stall at just 1.5 percent while competition in canned goods intensified. A quick audit revealed three root causes:

Dipping online sales that signalled slipping visibility and conversion.

Fragmented product content across major retailer sites as images, titles, and claims were inconsistent or missing altogether.

Heavier category competition making it harder to hold first-page search positions.

The Fix

The brand adopted DataWeave’s Digital Shelf Analytics to create a single source of truth for every PDP. A lean internal team then:

Ran content audits across priority retailers to surface incomplete or non-compliant attributes.

Prioritized quick wins focusing on high-velocity SKUs where simple edits (e.g., adding pack-size keywords or allergy statements) would unlock search filters.

Tracked progress weekly using an automated scorecard to keep everyone focused on the next set of fixes.

The Win

Twelve months later the numbers told the story:

Bush’s Beans transformed their product data into a strategic asset, significantly improving online visibility, safeguarding brand reputation, and driving sustained revenue growth. Accurate and complete product pages ensured compliance and boosted search rankings, directly increasing sales. While you can’t control external factors like tariffs, you can control the quality and compliance of your product pages and that control directly translates margin pressure into market share gains.

Unified Insight: Turning Signals into Sustained Advantage

Imagine one living dashboard where every digital shelf signal like timely price moves, share-of-search shifts, retail media spend, on-shelf availability gaps, compliance flags, MAP breaches, plus content and review health flows together. With that single lens, the “whose numbers are right?” debate disappears and cross-functional teams can act in minutes rather than days.

A consolidated feed lets you:

Build market awareness: Spot competitor price changes as they happen, understand who owns first-page search, and measure the true lift of retail media campaigns.

Mitigate emerging risks: Surface impending out-of-stocks before rank erodes, catch claim or label errors ahead of audits, and receive instant alerts when a seller breaks MAP.

Activate growth levers: Prioritize content edits that open search filters and use ratings and reviews trends to fine-tune messaging and assortment.

Brands that weave these signals into one workflow move faster than the disruption. That’s the connective tissue highlighted in our recent post on pairing Digital Shelf Analytics with Digital Shelf Impact Modelling: when granular shelf data sits beside strategic performance metrics, smarter decisions follow.

A platform like DataWeave brings the pieces together quietly ingesting millions of price checks, availability reads, and PDP audits each day, then presenting only the next best actions. The payoff is simple: sharper market awareness, lower operational risk, and growth that compounds with every iteration.

Keep Moving, Keep Winning

Tariffs, evolving regulations, and agile competitors are no longer storms; they are the climate. Brands that pair a clear, shared insight stream with rapid execution turn volatility into durable advantage. Keep your data united, keep iterating on the five digital-shelf levers, and every new headwind becomes another step ahead.

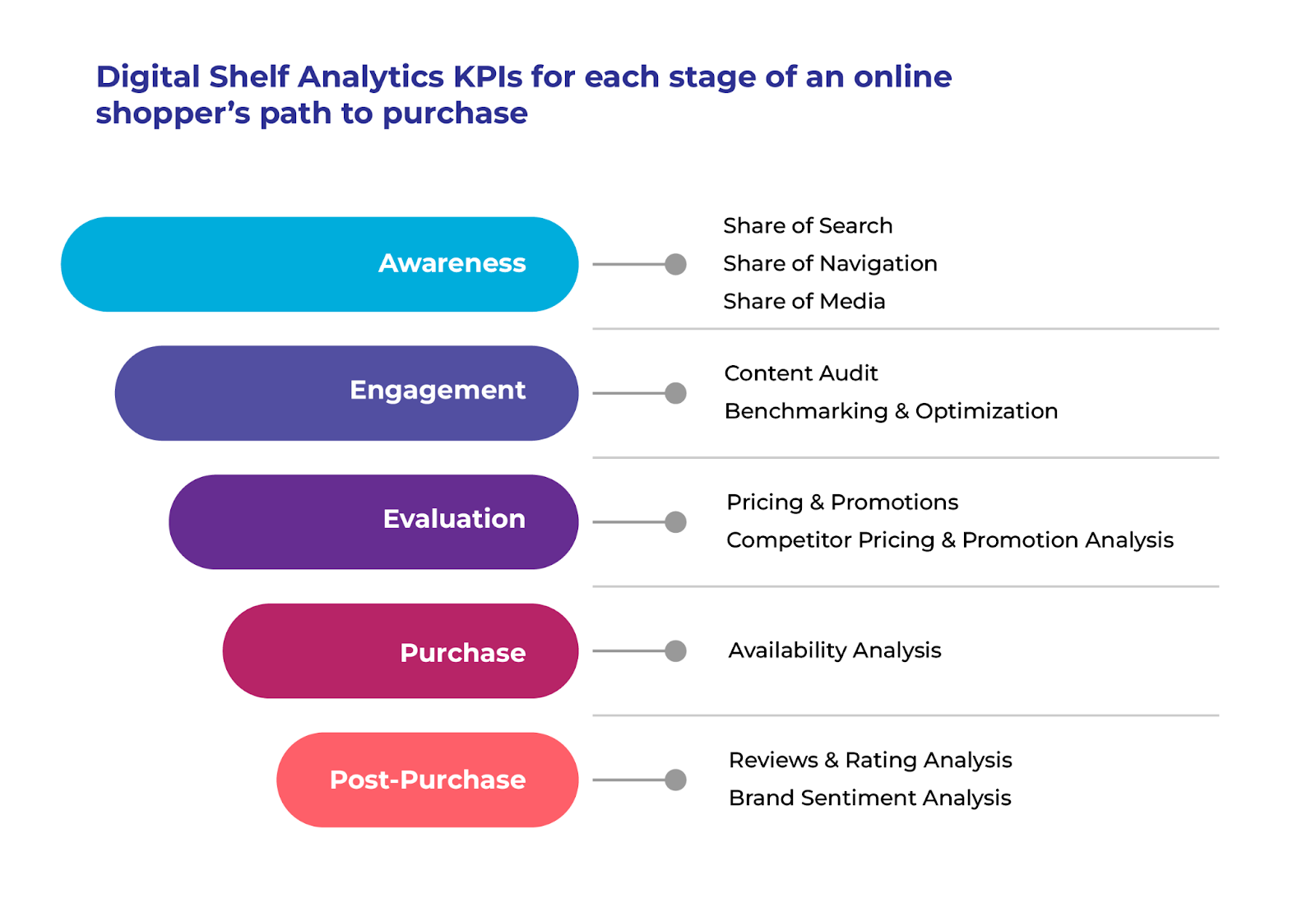

Marketing analytics has evolved dramatically over the past decade, yet many brands still struggle to connect their marketing investments to real business outcomes. While traditional analytics platforms provide valuable historical insights, they often miss the critical external factors that drive consumer behavior in today’s fast-moving digital marketplace.

The challenge isn’t just about measuring what happened. It’s about understanding why it happened and predicting what comes next. This is where Digital Shelf Impact Modeling becomes essential for smarter marketing investments.

The Critical Data Gap In Marketing Analytics

Traditional marketing analytics expose brands to considerable risk, especially in the CPG and retail space. The fundamental challenge lies in their reliance on lagging indicators for essential metrics like historical sales and ad spend. Data inputs may be months or quarters old before they’re used for strategic decision-making.

That’s like making million-dollar marketing decisions while only looking in the rearview mirror when you need to watch the road ahead simultaneously.

Most marketing analytics tools also typically overlook external market factors that can dramatically impact performance. In today’s retail landscape, where market conditions change rapidly, being blind to real-time competitive dynamics creates significant vulnerability. Key external factors that traditional analytics fail to capture include:

In fact, opaque data integration and siloed insights remain substantial barriers to actionable intelligence from marketing analytics tools. Most critically, old school approaches often miss vital such variables influencing consumer behavior.

These blind spots must be addressed to unlock the full value of marketing analytics investments and make truly informed marketing decisions.

How Digital Shelf Impact Modeling Completes The Picture

This is where Digital Shelf Impact Modeling plays a complementary role. Brands leveraging digital shelf analytics gain insights into actual market dynamics that traditional analytics alone cannot provide. However, brands using digital shelf insights in isolation often struggle to quantify how digital shelf improvements directly impact revenue. Answering questions like “Did better product content drive sales, or was it the influencer campaign?” remains challenging.

Bridging these disconnected platforms requires intentional integration and a solution that can feed intensively cleaned and organized data into existing analytics frameworks. With the right data inputs, companies establish a powerful feedback loop for agile, data-driven decisions.

A comprehensive DSA solution like DataWeave provides granular, actionable data on critical external variables such as:

Daily or weekly competitor pricing movements and promotional activity

Product content standardization and optimization across retailers

Review sentiment trends and potential reputation issues

Share of search/shelf performance relative to competitors

When merged with established analytics capabilities, digital shelf impact modeling creates a complete picture that fills the blind spots holding marketing teams back from maximizing ROI.

The Digital Shelf Advantage in Retail Media

The popularity of retail media networks has further amplified the need for integrated digital shelf analytics approaches. These advertising platforms, operated by retailers, allow brands to display targeted ads to shoppers across digital properties based on first-party customer data and purchase insights.

The retail media revolution has transformed e-commerce pages into sophisticated search engines for product discovery. This evolution has been so impactful that retail media ad revenue surged 16.3% in 2023, reaching $43.7B in the U.S., with continued growth projected.

Major platforms like Walmart have expanded their retail media networks to capitalize on closed-loop attribution. Since retailers own the entire customer journey, they can track everything from ad impression to purchase on their e-commerce sites. This creates a significant advantage through accurate ROI measurement, unlike traditional advertising where attribution remains challenging.

How Digital Shelf Impact Modeling Enhances Retail Media Optimization

With retail media emerging as a top-performing sales channel, brands need sophisticated optimization strategies. Every brand wants to maximize visibility and performance across individual eCommerce sites, just as they optimize for Google or emerging AI platforms.

Integrating digital shelf analytics into marketing mix models enables brands to:

Allocate ad spend more intelligently using real-time competitive insights

Identify timely campaign activation opportunities in response to market changes

Monitor organic ranking trends to strategically time paid promotional activities

Measure true campaign impact on digital shelf performance metrics

For example, when a competitor launches an aggressive price drop in your category, Digital Shelf Impact Modeling provides immediate visibility into this change. This intelligence can trigger recommended campaign adjustments, such as increased sponsored ad bidding in affected categories. Traditional analytics alone cannot deliver this level of responsive optimization.

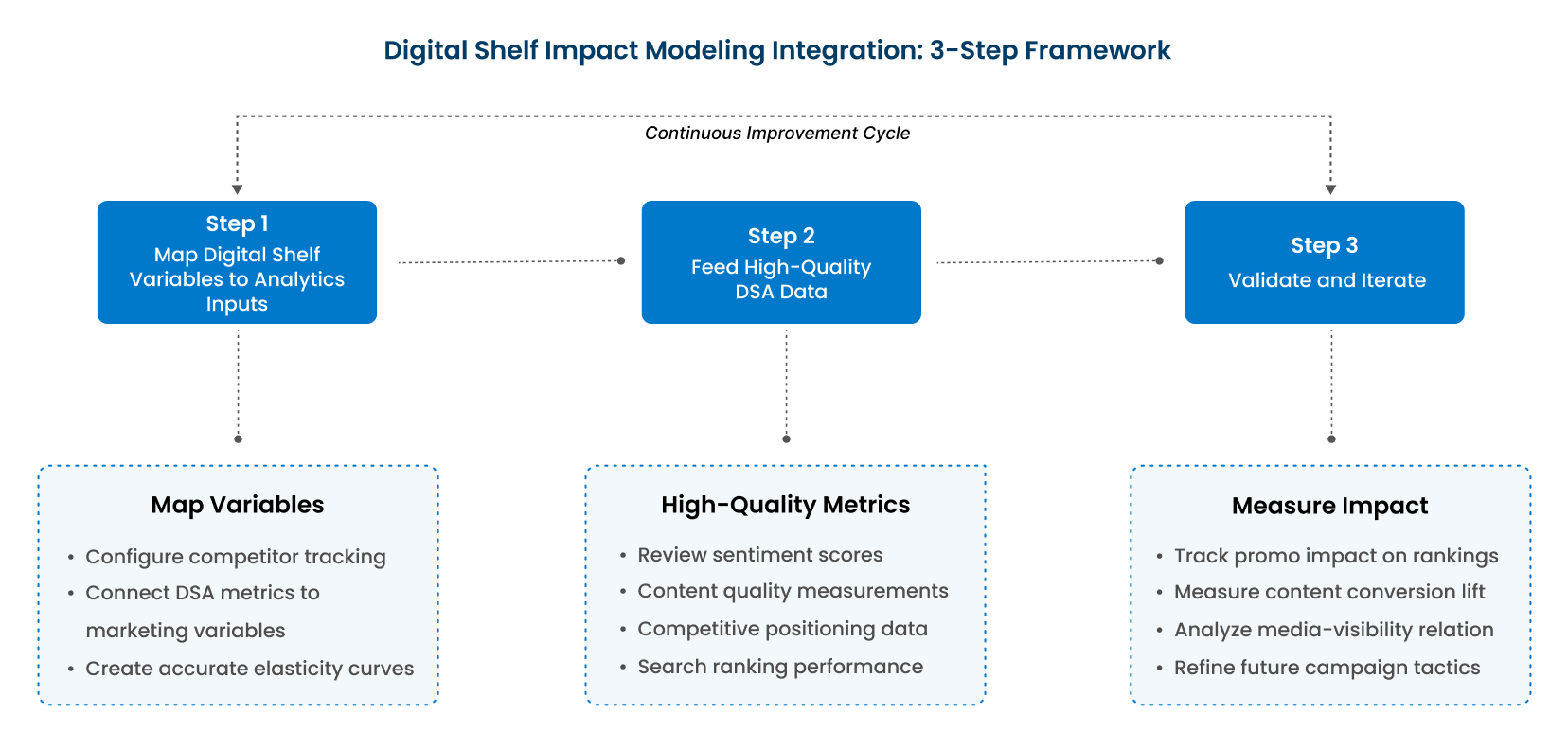

How to Integrate Digital Shelf Impact Modeling: A 3-Step Framework

Here’s how to integrate Digital Shelf Impact Modeling into your marketing strategy to start making better data-driven decisions for your brand.

Step 1: Map Digital Shelf Variables to Analytics Inputs

Begin by mapping specific digital shelf variables to your existing analytics inputs. Ensure that competitors are properly configured for monitoring in your digital shelf platform and that timely metrics like price changes and search ranking positions are linked with your marketing measurement systems.

This integration is crucial because traditional analytics rely exclusively on historical data for forecasting. Adding real-time inputs delivers several benefits:

More accurate elasticity curves reflecting current market conditions

Better understanding of root causes behind demand shifts

Prevention of misattributing sales changes to your marketing activities when external factors may be responsible

At DataWeave, our comprehensive coverage spans 500+ billion data points, 400,000 brands, and 1,500+ websites, ensuring brands never miss a competitor move and maintain complete visibility across the connected e-commerce landscape.

Step 2: Feed High-Quality Digital Shelf Data into Analytics Platforms

Next, integrate critical digital shelf metrics into your measurement framework:

Review and sentiment scores and trends

Content quality measurements

Competitive positioning data

Price gap analytics

Search ranking performance

DataWeave employs a rigorous data accuracy validation process to ensure teams work with the cleanest, most reliable data possible. Our sophisticated processing pipeline removes anomalies and standardizes information across retailers, providing the consistent, high-integrity data foundation that robust marketing mix modeling demands.

Step 3: Validate and Iterate

A powerful Digital Shelf Impact Modeling solution helps measure whether your marketing efforts achieved their intended impact on the digital shelf. Use your digital shelf platform to assess your campaigns’ actual effect on key performance indicators:

Do promo-driven sales lifts correlate with improved search rankings?

How do content improvements impact conversion rates?

What is the relationship between paid media and organic visibility?

It is no surprise to anyone that we are living through volatile times. Executives may be uncomfortable if they cannot provide their teams with strategic direction based on data or the tools they need to accelerate their workdays.

By integrating Digital Shelf Impact Modeling with existing analytics, companies gain early warning signals about market shifts, enabling smarter resource allocation during budget constraints. This integration helps organizations move from tactical execution to strategic direction by:

Providing cross-channel impact analysis to understand the full marketing ecosystem

Equipping category managers with tactical optimization tools that support broader strategic objectives

Identifying competitive threats before they impact sales

Forecasting potential ROI impacts across various spending scenarios

These capabilities help prevent wasted ad spend, missed opportunities, and lost sales.

Future-Proofing Your Marketing Strategy with Digital Shelf Impact Modeling

Several emerging trends highlight the growing importance of digital shelf-enhanced marketing analytics:

Trend 1: Navigating Economic Volatility – Brands can use Digital Shelf Impact Modeling to track how competitors adjust pricing in response to cost shocks like tariffs and inflation. This real-time intelligence directly improves demand forecasting accuracy.

Trend 2: AI-Powered Predictive Insights – Combining digital shelf trend detection (such as viral product reviews or sudden inventory fluctuations) with marketing performance metrics helps forecast demand spikes from otherwise unforeseen events.

Trend 3: Automated Optimization – Smart campaign activations and adjustments based on real-time digital shelf triggers drive efficiency. DataWeave’s vision includes an automated retail media intelligence layer that optimizes spend across channels based on integrated insights.

DataWeave’s Unique Advantage

At DataWeave, we’ve seen our digital shelf analytics customers significantly improve their organic search rankings because of better-sponsored ad campaigns. What makes DataWeave’s approach to Digital Shelf Impact Modeling uniquely powerful? Our platform is specifically designed to address the challenges of modern marketing measurement:

Superior data refresh rates ensure timely insights when they matter most

Unmatched marketplace coverage across more than 1,500 eCommerce sites globally

Advanced data normalization that standardizes metrics across disparate categories and retailers

API-first architecture enabling flexible data access and utilization

Conclusion – From Hindsight to Foresight

In the past, companies relied primarily on historical data for their marketing analytics. Today’s market leaders are incorporating Digital Shelf Impact Modeling to unlock superior insights, improve decision accuracy, and drive measurable ROI.

DataWeave serves as the essential bridge between traditional analytics systems and real-time, comprehensive market intelligence. When digital shelf analytics and marketing measurement work together, brands gain a complete picture: traditional analytics show precisely what happened, while Digital Shelf Impact Modeling explains why it happened. Together, they reveal what’s coming next.

Ready to transform your marketing analytics from hindsight to foresight? Contact us today to discover how our Digital Shelf Analytics can enhance your existing marketing investments and drive measurable business results.

Black Friday and Cyber Monday are major retail events in Canada, with 43% and 29% of the population making purchases during these sales respectively, according to a YouGov report. Consumer electronics continue to lead the Canadian retail market during these events, with 55% of surveyed shoppers choosing to buy tech products on Black Friday. Household appliances come in second, with 25% of shoppers opting for these items, while 18% prefer to shop for furniture deals.

These statistics highlight the importance of delivering value during the Thanksgiving sales week. Retailers must cater to shoppers’ expectations with competitive pricing, attractive deals, and a seamless shopping experience. So, what unique offerings did Canadian retailers present to shoppers this season?

To understand the pricing and discount dynamics during BFCM 2024 in Canada, DataWeave analyzed discounts across leading consumer electronics and home & furniture retailers. Using our AI-powered pricing intelligence platform, we analyzed 37,108 SKUs across these categories for major retailers including Amazon, Walmart, Best Buy, Home Depot, and Canadian Tire from the 10th to 29th November. We focused on the top 500 products ranked for each search keyword on each retail site, using targeted terms aligned with categories like “sofa” and “wearables”.

In the following insights, the Absolute Discount represents the reduction of the selling price compared to the Manufacturer’s Suggested Retail Price (MSRP). The Additional Discount reflects how much lower the selling price is during Black Friday compared to its price a week before the sale. This metric reveals the actual or effective value of the sale event, beyond the standard discounts typically offered.

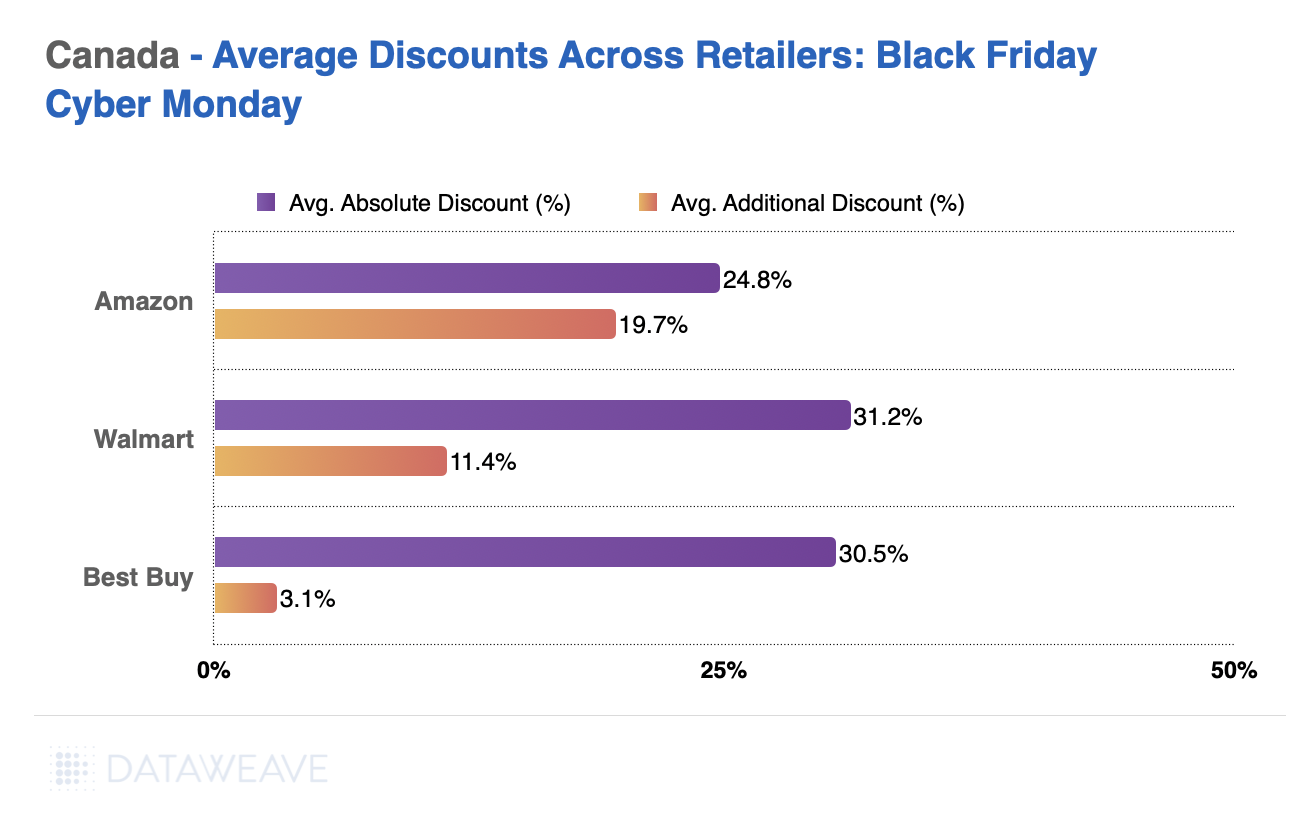

Consumer electronics saw robust participation from major retailers, with Amazon, Best Buy, and Walmart leading the charge. Here’s how they stacked up in terms of discounts:

Best Buy emerged as the frontrunner in absolute discounts at 31.2%, while Amazon impressed with a notable 19.7% additional discount, indicating a strong Black Friday-specific markdown strategy.

Walmart offered steady competition, particularly in audio and video products, which reached an average absolute discount of 37.2%. However, it’s average additional discount was only 3.1%, indicating muted BFCM-specific price reductions in this category.

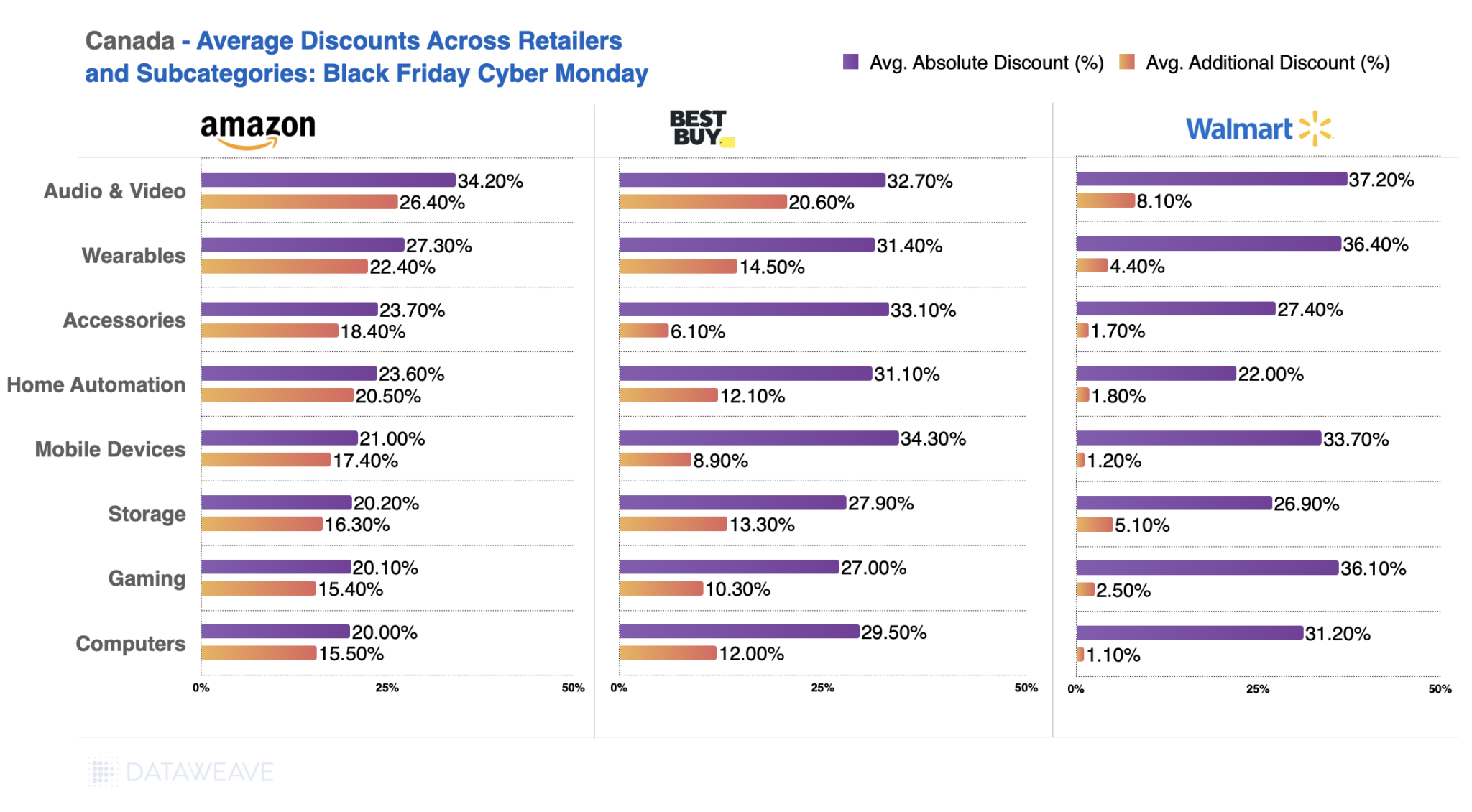

Subcategory Insights

Diving deeper into consumer electronics subcategories, we observed varied discounting strategies.

Audio & Video stood out as the most discounted subcategory, with Walmart leading at 37.2%.

In Wearables, Walmart again took the top spot with 36.4%, while Amazon offered higher additional discounts (22.4%).

Discounting for computers and gaming was less aggressive, highlighting strategic pricing to maintain profitability in these high-demand segments.

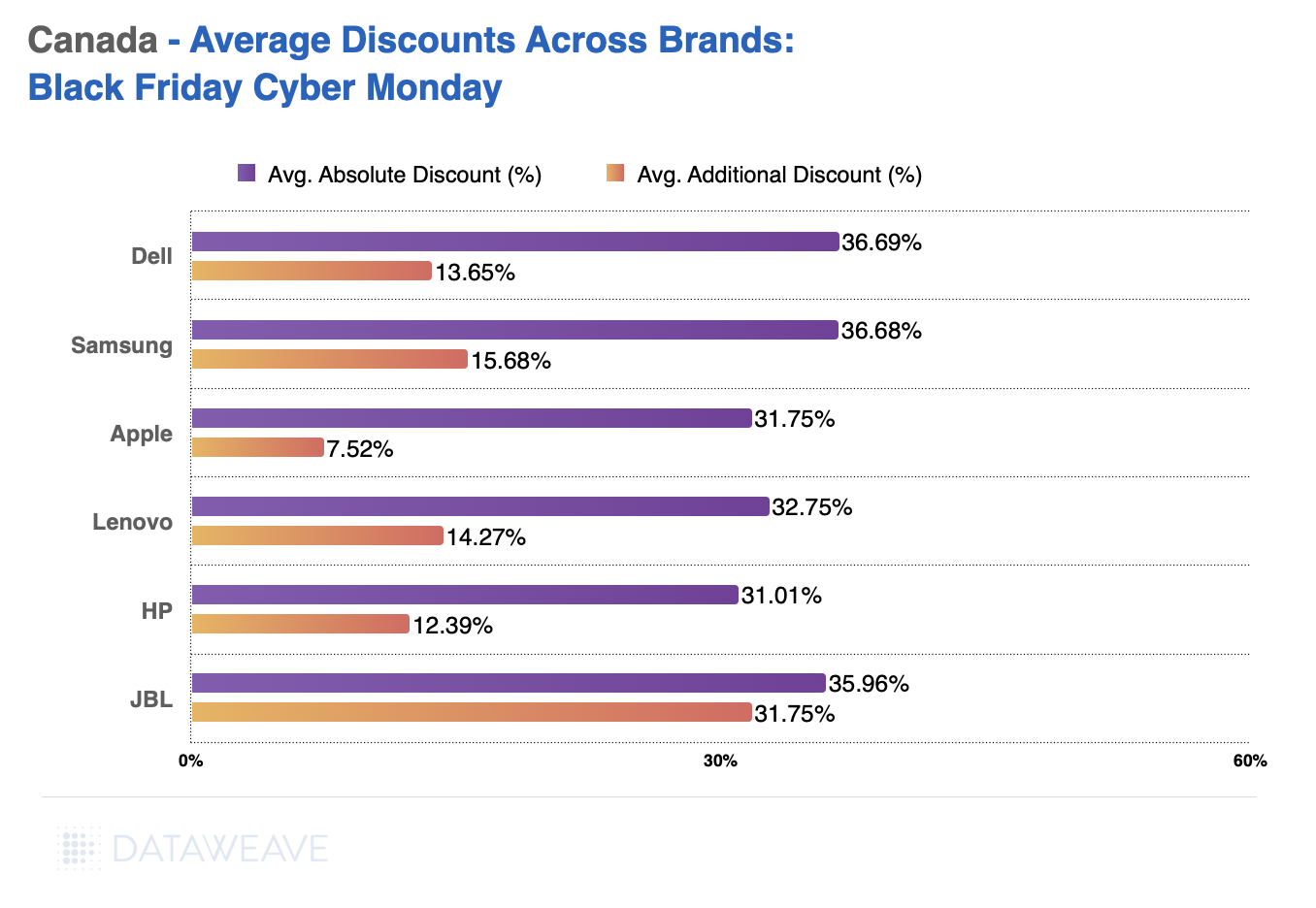

Brand Performance

Brand-level data highlighted how key players used Black Friday to drive visibility and sales.

Dell led in average absolute discounts (36.7%) followed by Samsung at 36.68%

Audio brand JBL offered significant absolute discounts at 35.9%.

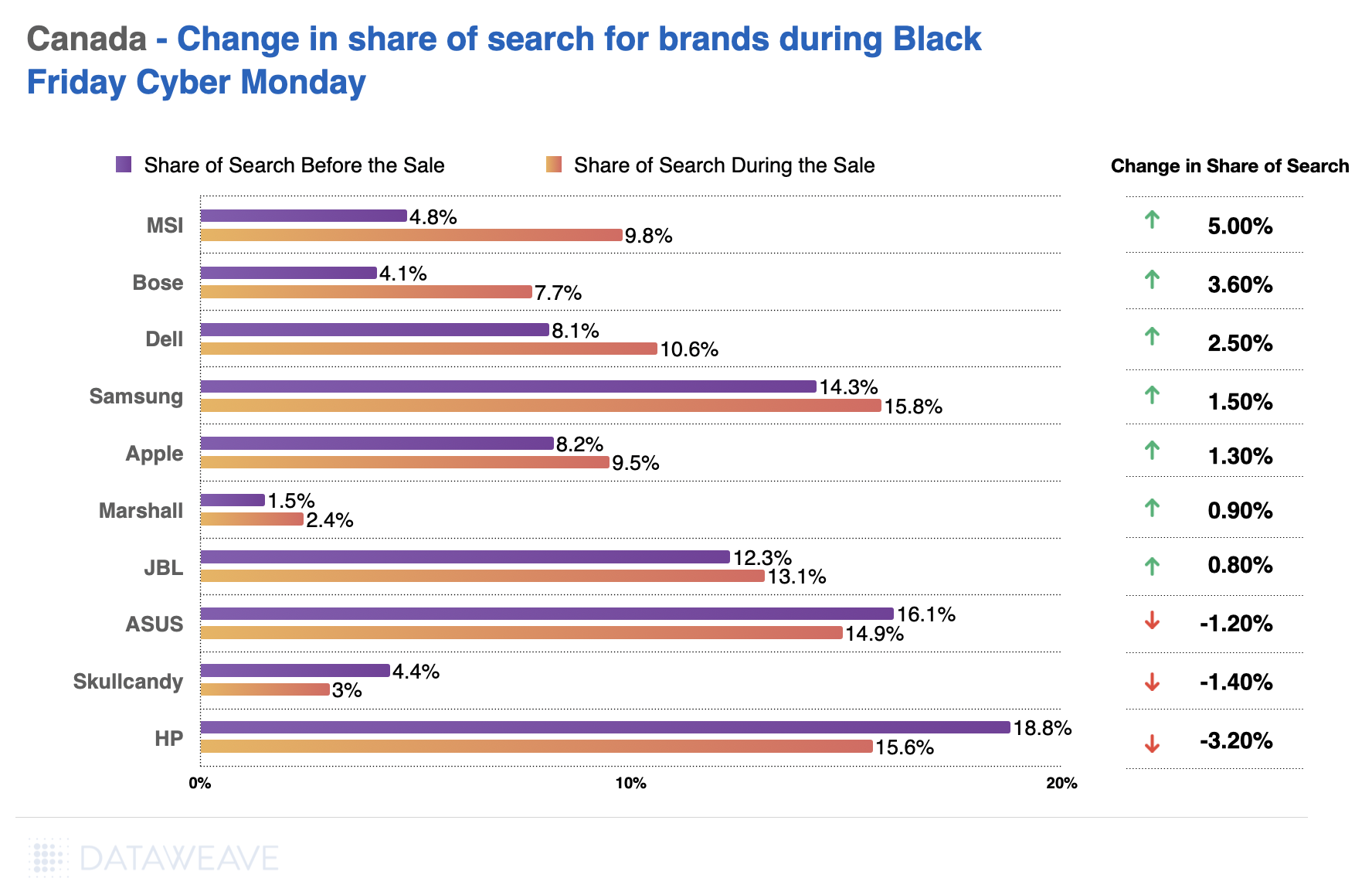

Apple and Lenovo offered comparatively fewer discounts but maintained strong visibility, as seen in their increase in the Share of Search during the sale period.

MSI (laptop brand) and Bose (audio and earphone brand) experienced significant increases in visibility, with Share of Search increases of 5% and 3.6%, respectively.

Notably, HP faced a decline (-3.2%) in the Share of Search, suggesting missed opportunities to align promotions with consumer interest.

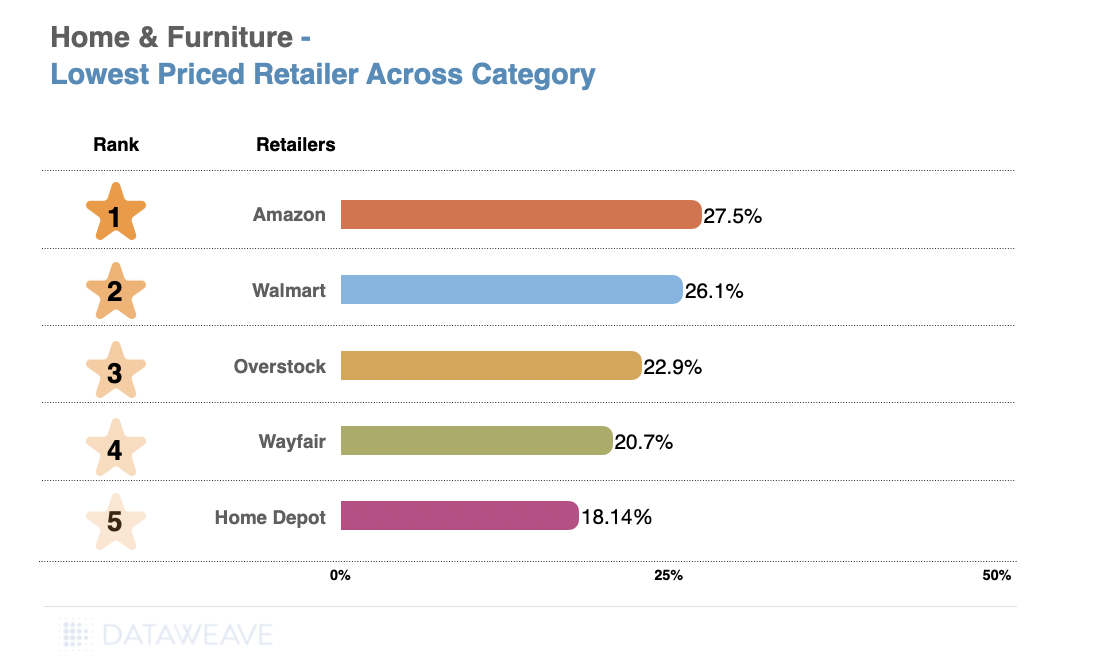

Home & Furniture

Retailers in Focus

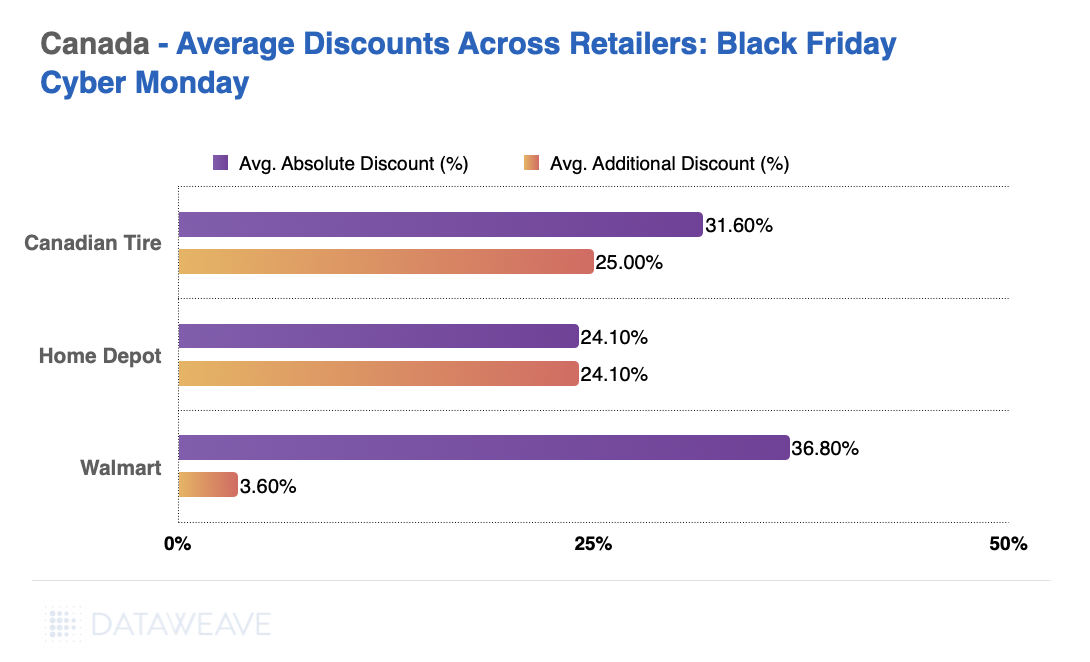

The home and furniture category saw competitive discounting, with Walmart, Canadian Tire, and Home Depot vying for consumer attention.

Walmart took the lead with the highest absolute discounts at 36.8%. The retailer’s additional discounts were more conservative at 3.6%. This is similar to their discount levels in Consumer Electronics.

Canadian Tire offered stiff competition, providing 31.6% absolute discounts and 25% additional discounts.

Home Depot matched its absolute and additional discounts, maintaining consistency at 24.1%.

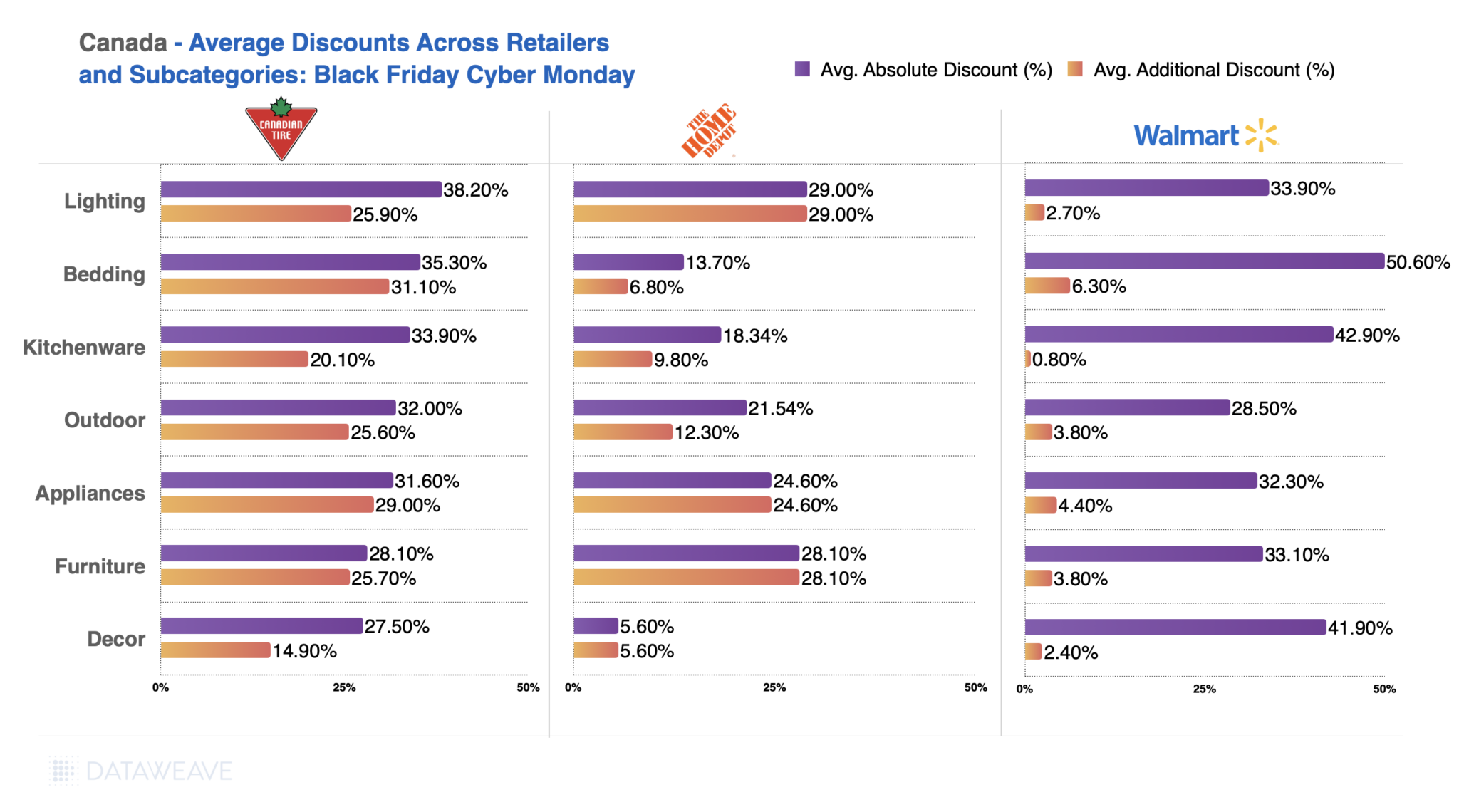

Subcategory Insights

Home and furniture subcategories revealed targeted discount strategies.

Bedding emerged as the most discounted subcategory at Walmart (50.6%) and Canadian Tire (35.3%).

Kitchenware saw competitive pricing, with Walmart leading at 42.9%, followed by Canadian Tire at 33.9%.

Canadian Tire focused on lighting, offering the highest absolute discounts in this subcategory (38.2%)

Brand Performance

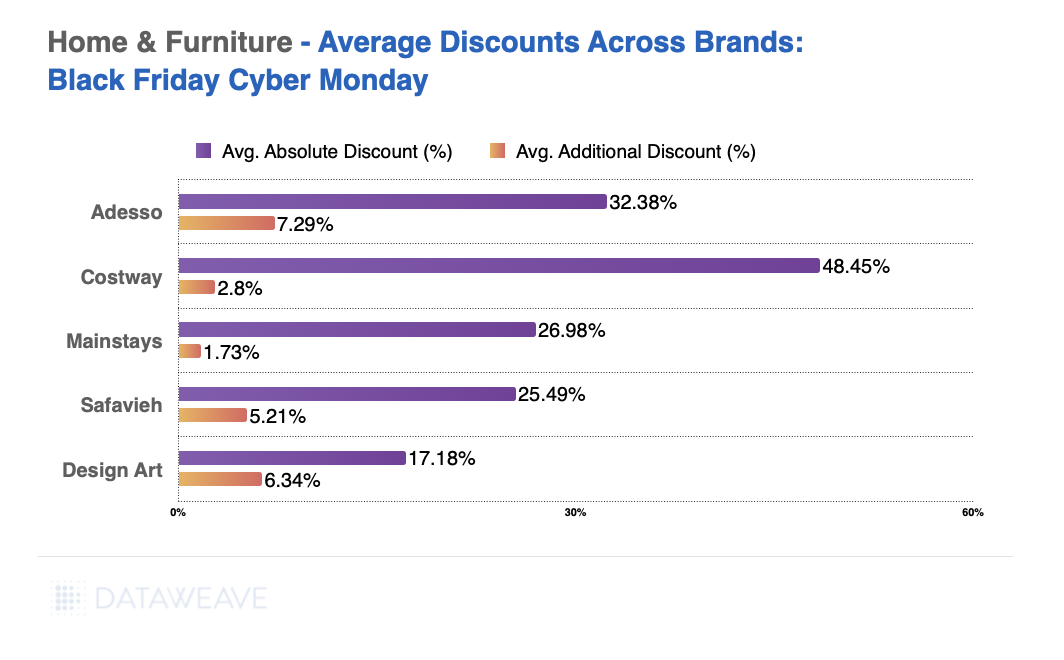

Brand-level analysis revealed stark contrasts in discounting approaches.

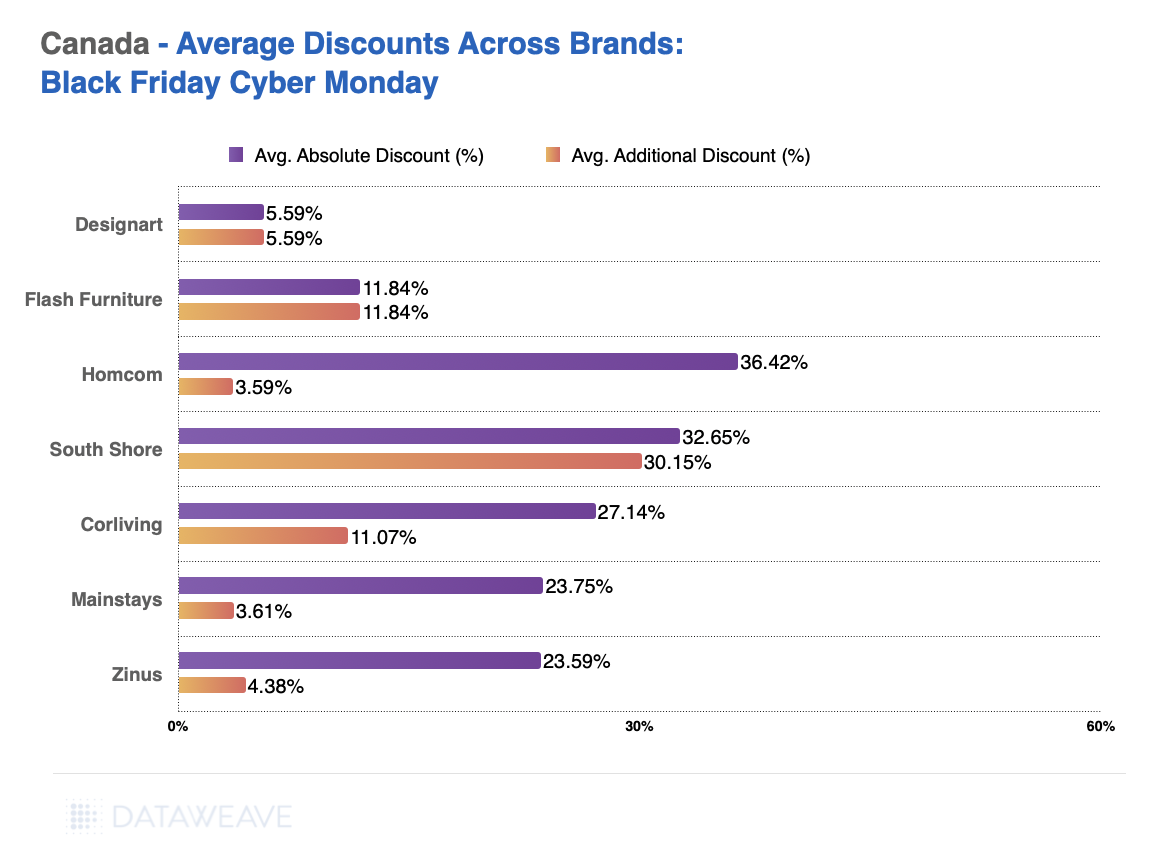

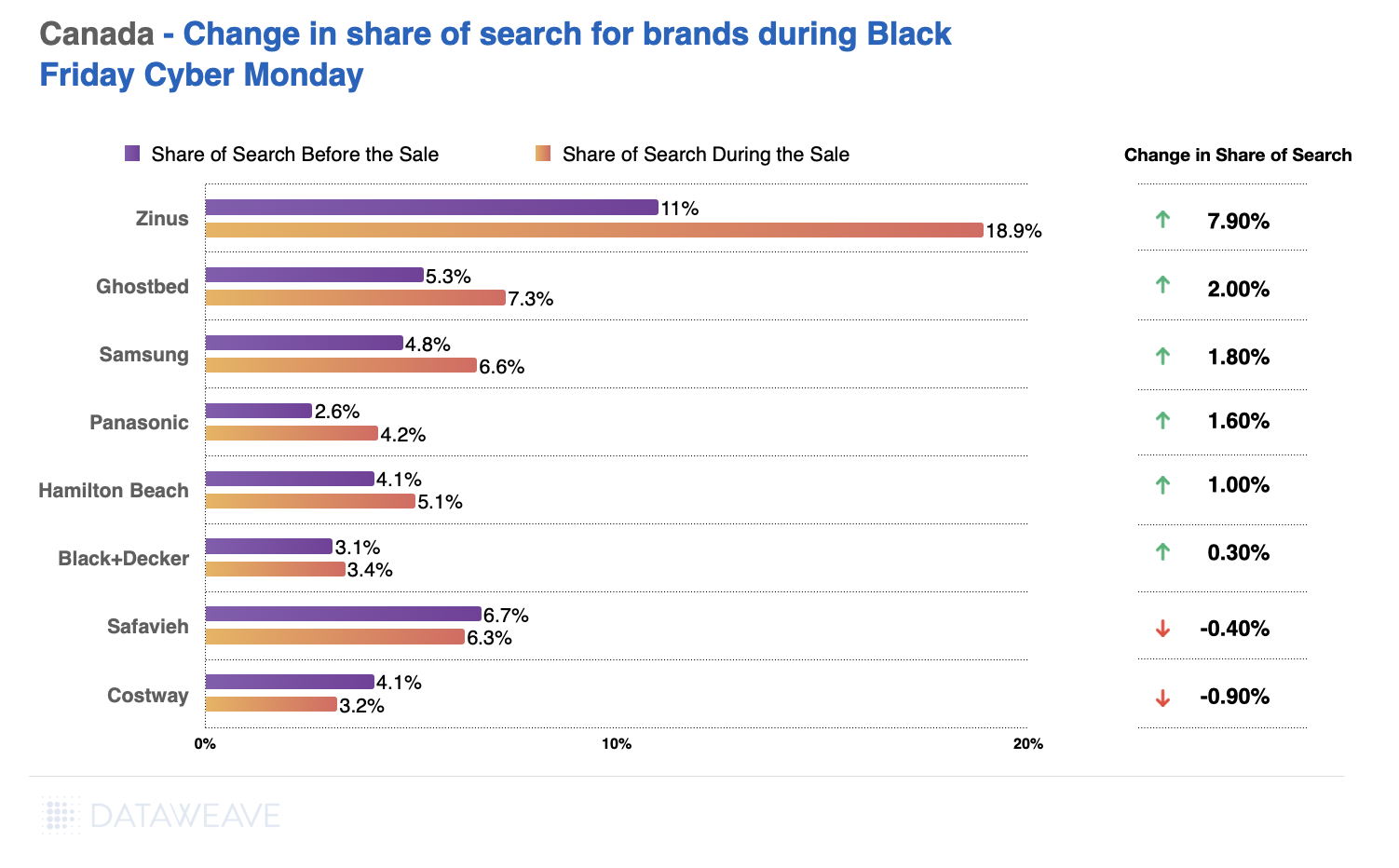

Furniture brands Homcom led in absolute discounts (36.4%), while South Shore stood out with the highest additional discounts (30.2%).

Value-oriented brands like furnishings brand Mainstays and mattress and bedding brand Zinus offered more modest discounts, focusing on consistent affordability.

Zinus (mattresses and sofa brand) experienced a significant 7.9% increase in the Share of Search, driven by aggressive promotions.

Home furnishings brands like Costway and Safavieh faced declines, reflecting the importance of aligning promotional strategies with consumer expectations.

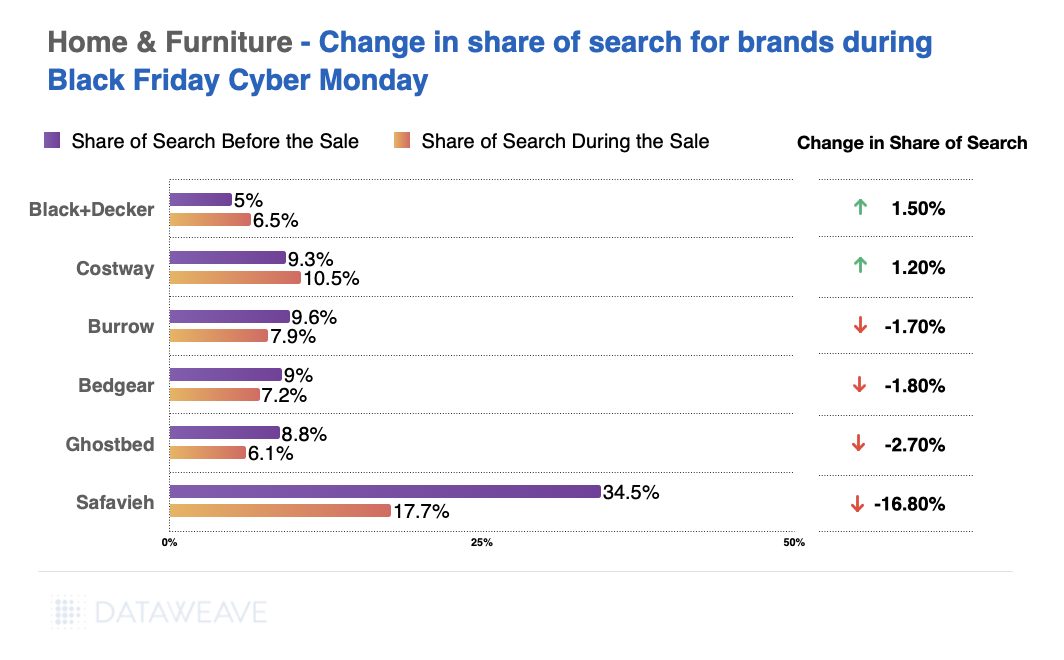

Insights for Retailers and Brands

This Black Friday, Canadian retailers effectively balanced deep discounts with category-specific strategies to maximize sales. However, the fluctuating Share of Search highlights the critical need for brands to align promotions with consumer interest.

For brands and retailers looking to stay ahead of the competition, DataWeave’s pricing intelligence platform offers unparalleled insights to refine discounting strategies and boost visibility. Contact us to learn how we can help you stay competitive in this dynamic retail landscape.

Americans spent a whopping total of $10.8 billion online this Black Friday. As Thanksgiving Week 2024 wraps up, one thing is clear: the consumer electronics category continues to dominate seasonal shopping trends. Fueled by a blend of enticing deals and high consumer demand, the sector delivered competitive discounts across subcategories like wearables, gaming, and mobile devices.

At DataWeave, we analyzed discounting trends in the U.S. consumer electronics market during this year’s sales events. Using our AI-powered pricing intelligence platform, we tracked pricing and promotions for 22383 SKUs across Amazon, Walmart, Target, and Best Buy from November 10 to 29. We focused on the top 500 products ranked for each search keyword on each retail site, using targeted terms aligned with categories like “gaming” and “apple.” Here’s what we uncovered.

Retailers Battle It Out with Competitive Discounts

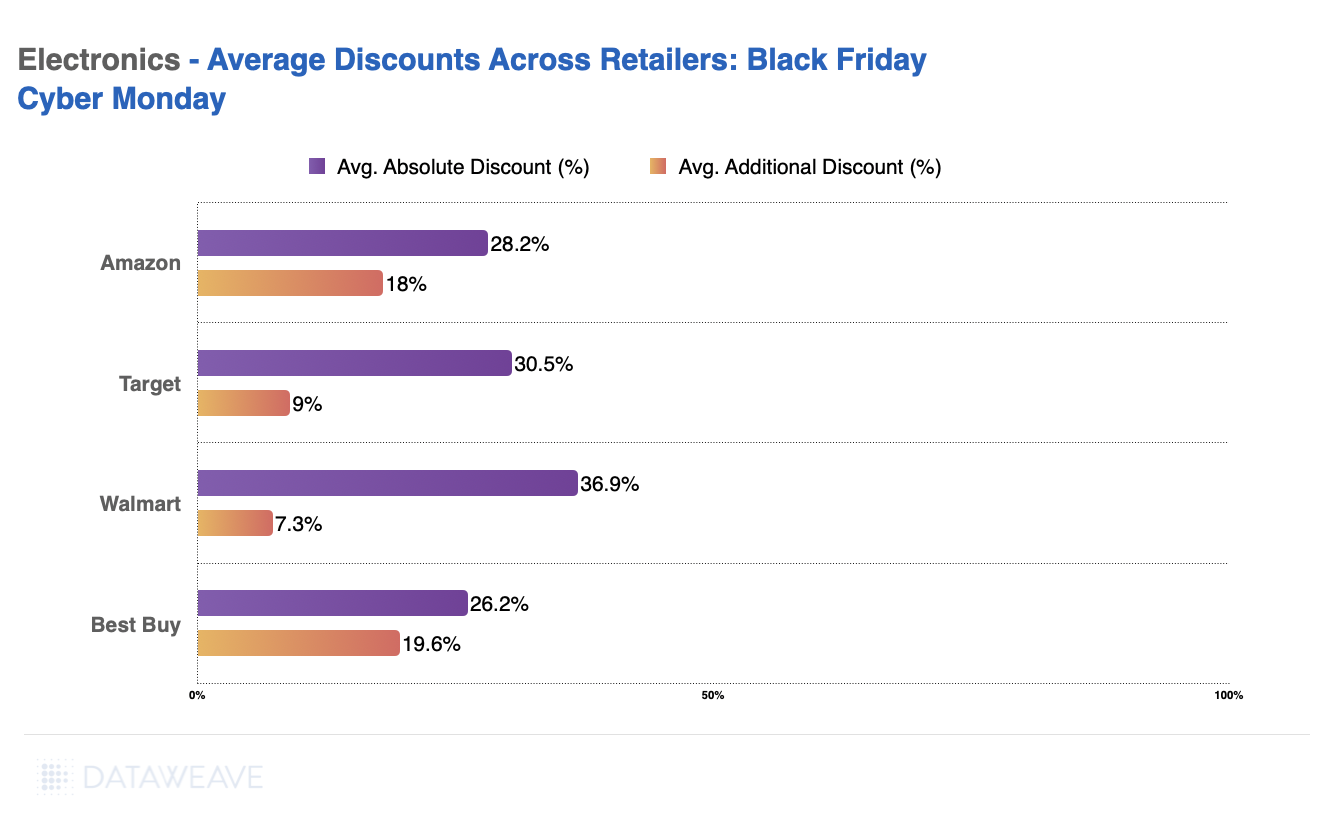

Discount trends reveal clear leaders in terms of markdowns:

Walmart offered the deepest average absolute discounts at 36.9%.

Amazon and Target followed closely, highlighting a diverse range of deals designed to appeal to budget-conscious shoppers

Best Buy, the specialist consumer electronics retailer, offers the lowest discounts this Black Friday at 26.2%.

Note: The Absolute Discount represents the reduction of the selling price compared to the Manufacturer’s Suggested Retail Price (MSRP). The Additional Discount reflects how much lower the selling price is during Black Friday compared to its price a week before the sale. This metric reveals the actual or effective value of the sale event, beyond the standard discounts typically offered.

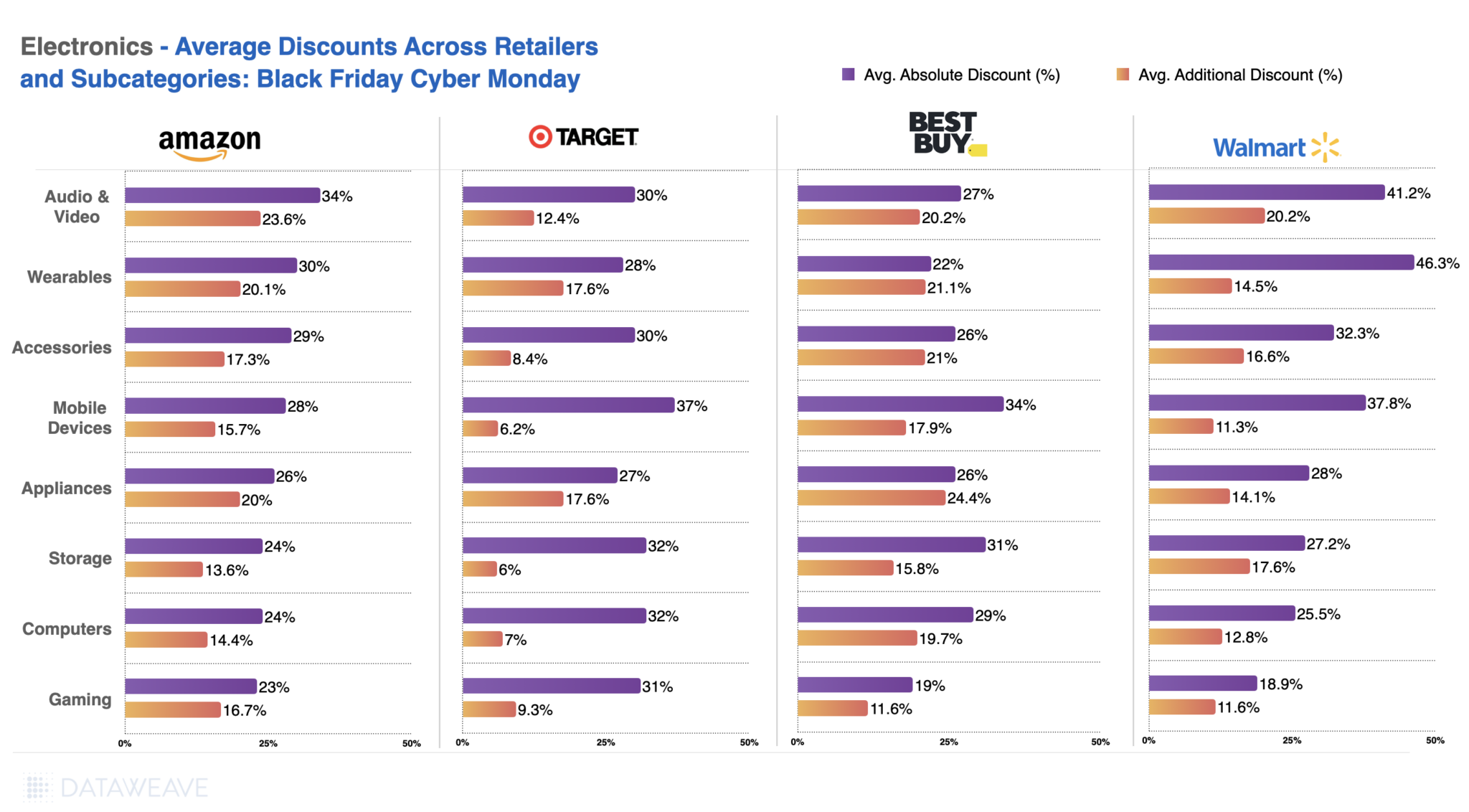

Subcategory Spotlight: Where the Best Deals Happened

From audio & video to wearables, each retailer carved out competitive advantages across subcategories.

Both Amazon and Walmart offered high discounts in audio & video and wearables, but Walmart led, with discounts up to 46.3%.

Best Buy, meanwhile, offered high absolute discounts on Mobile Devices(34%) and Storage (31%), followed by high discounts on wearables and Audio & Video.

Amazon maintained a balanced approach, excelling in audio & video and mobile devices.

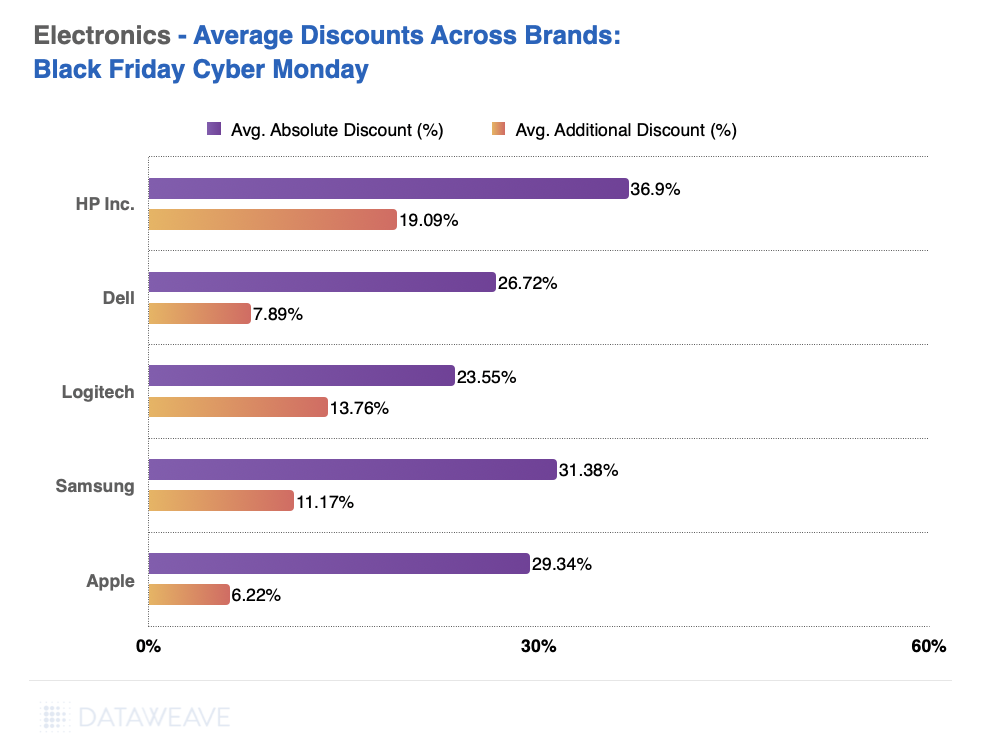

Brand-Level Insights: HP and Samsung Dominate

The biggest winners this year were brands that strategically leveraged Black Friday discounts to boost visibility and sales:

HP took the top spot with average discounts of 36.9%, followed by Samsung at 31.4%.

Despite its premium reputation, Apple offered an average discount of 29.3%, signaling a shift in strategy to attract deal hunters.

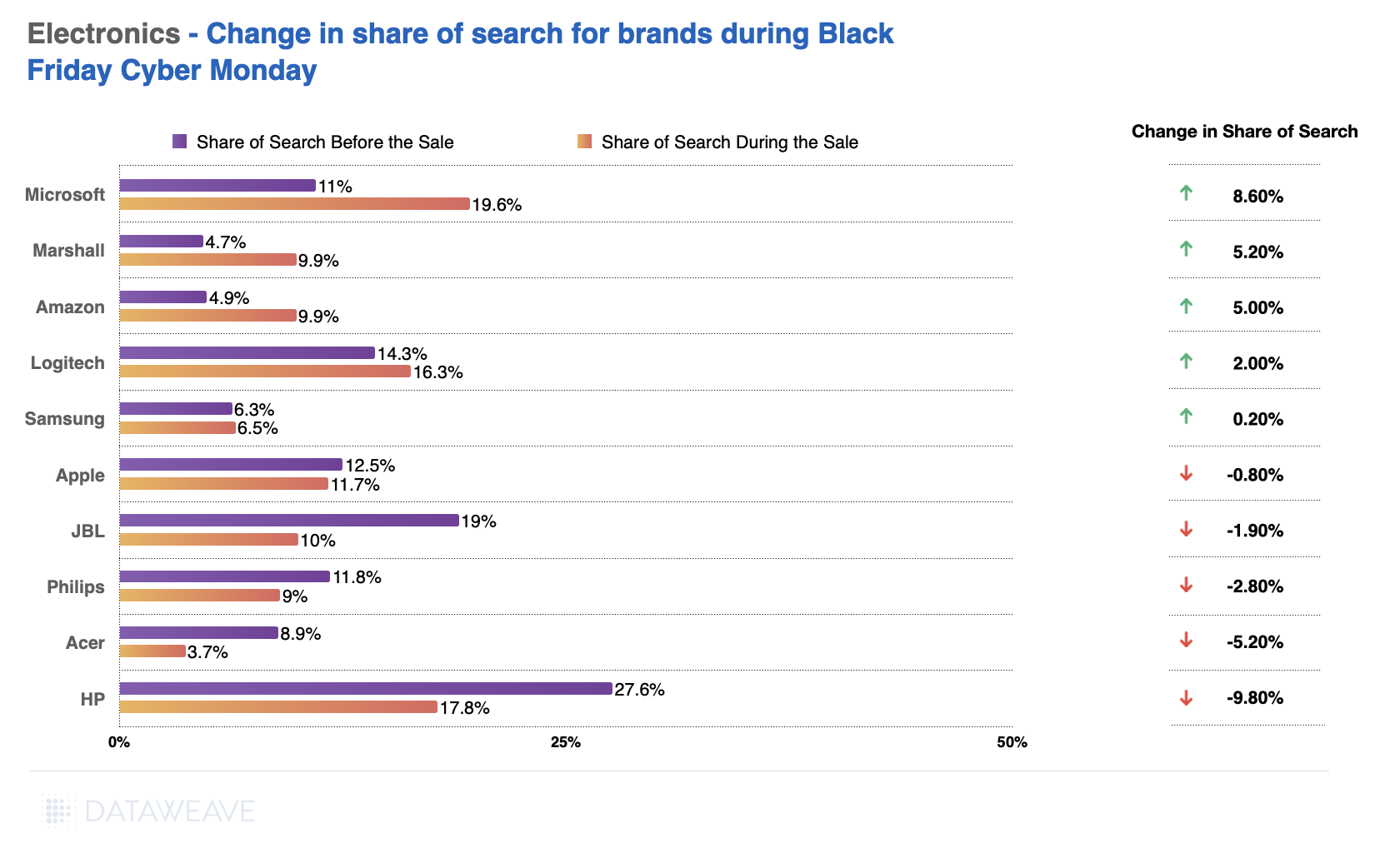

Share of Search: Shifting Consumer Attention

Search trends reveal how discounts shaped brand visibility:

Microsoft saw the largest spike in share of search (+8.6%), thanks to aggressive pricing on gaming consoles and accessories.

Marshall and Amazon also saw significant gains in visibility.

Surprisingly, HP experienced a sharp decline (-9.8%), indicating missed opportunities despite steep discounts.

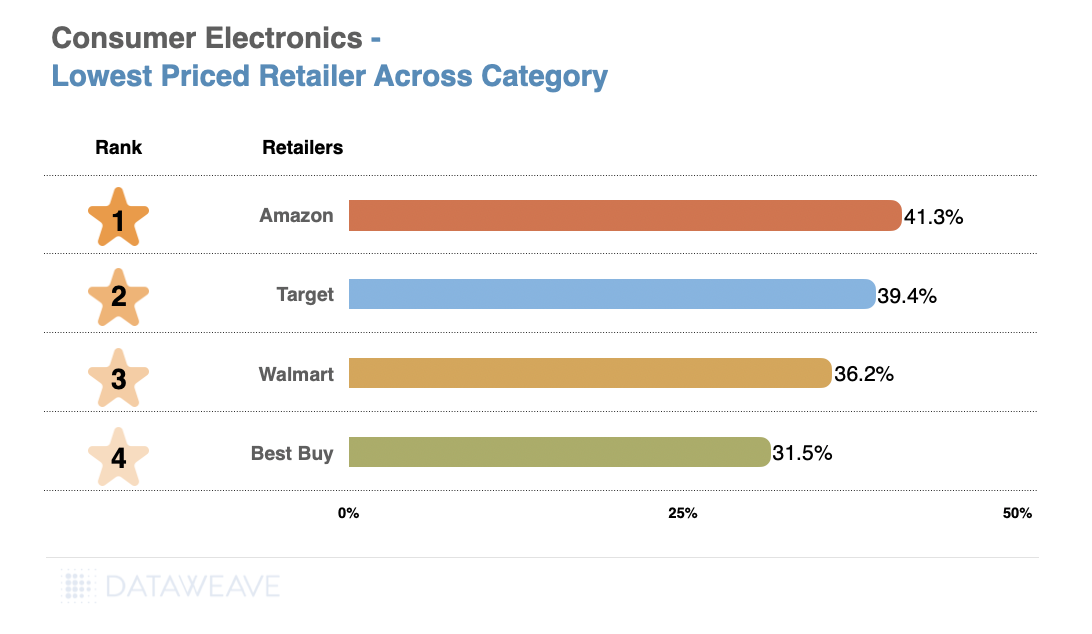

In the previous analysis, we focused on the top 500 products within each subcategory for each retailer, showcasing the discount strategies for their highlighted or featured items. However, to identify which retailer offered the lowest or highest prices for the same set of products, it’s necessary to match items across retailers. For this, we analyzed a separate dataset of 340 matched products across retailers to compare their pricing during Black Friday. This approach provides a clearer picture of price leadership and competitiveness across categories.

Here are the key takeaways from this analysis.

Category-Level Highlights

Amazon leads with the highest average discount (41.35%), offering the most value to consumers. It is followed by Target (39.37%) and Walmart (36.15%).

Best Buy, the specialist consumer electronics retailer, ranks last with an average discount of 31.53%, emphasizing a less aggressive pricing strategy compared to competitors.

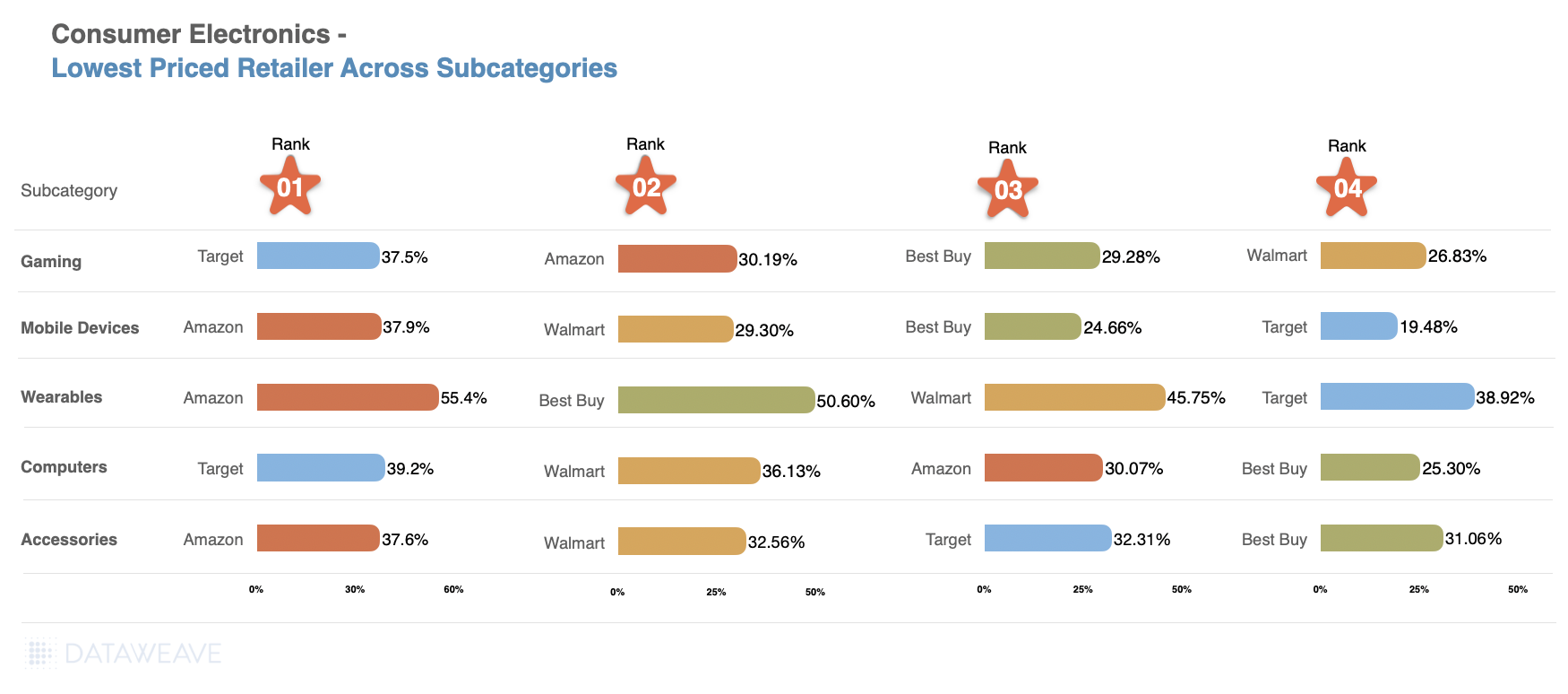

Subcategory Highlights

Wearables: Amazon offers the steepest discounts (55.40%), followed by Best Buy (50.60%) and Walmart (45.75%).

Mobile Devices: Amazon also leads (37.94%), with Walmart (29.30%) in second place and Target trailing at 19.48%.

Gaming: Target takes the lead (37.47%), with Amazon and Best Buy offering similar discounts around 30%.

Computers: Target again emerges as the leader (39.18%), narrowly surpassing Walmart (36.13%).

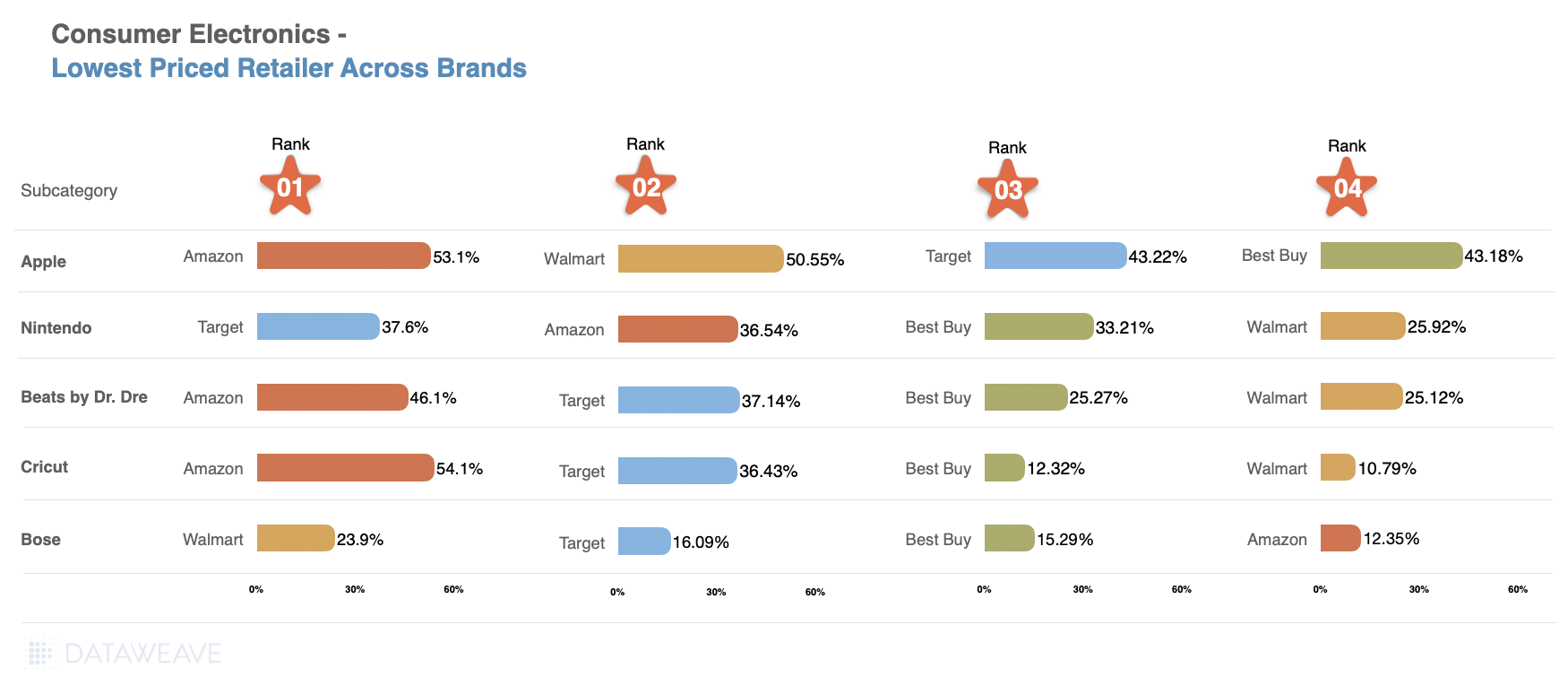

Brand Highlights

Apple: Amazon dominates with 53.06%, closely followed by Walmart (50.55%), while Target and Best Buy hover around 43%.

Nintendo: Target edges out Amazon (37.62% vs. 36.54%), with Best Buy (33.21%) and Walmart (25.92%) trailing.

Beats by Dr. Dre: Amazon leads (46.07%), with Target (37.14%) as the runner-up. Best Buy and Walmart offer comparatively modest discounts around 25%.

Bose: Walmart emerges as the value leader (23.90%), surpassing Target (16.09%) and Best Buy (15.29%).

Cricut: Amazon sets a high benchmark (54.13%), with Target far behind (36.43%) for this viral portable printer brand. Best Buy (12.32%) and Walmart (10.79%) offer significantly lower discounts.

What This Means for Retailers and Brands

Retailers looking to stay competitive should focus on strategic discounting and enhanced brand visibility. Brands must align with consumer expectations by:

Leveraging platforms like DataWeave to analyze discount trends.

Optimizing pricing and assortment strategies for seasonal demand.

For more insights into consumer electronics pricing, contact DataWeave to discover how our AI-powered solutions can drive success in today’s fast-paced market. Stay tuned for more category-specific analyses in the coming weeks!

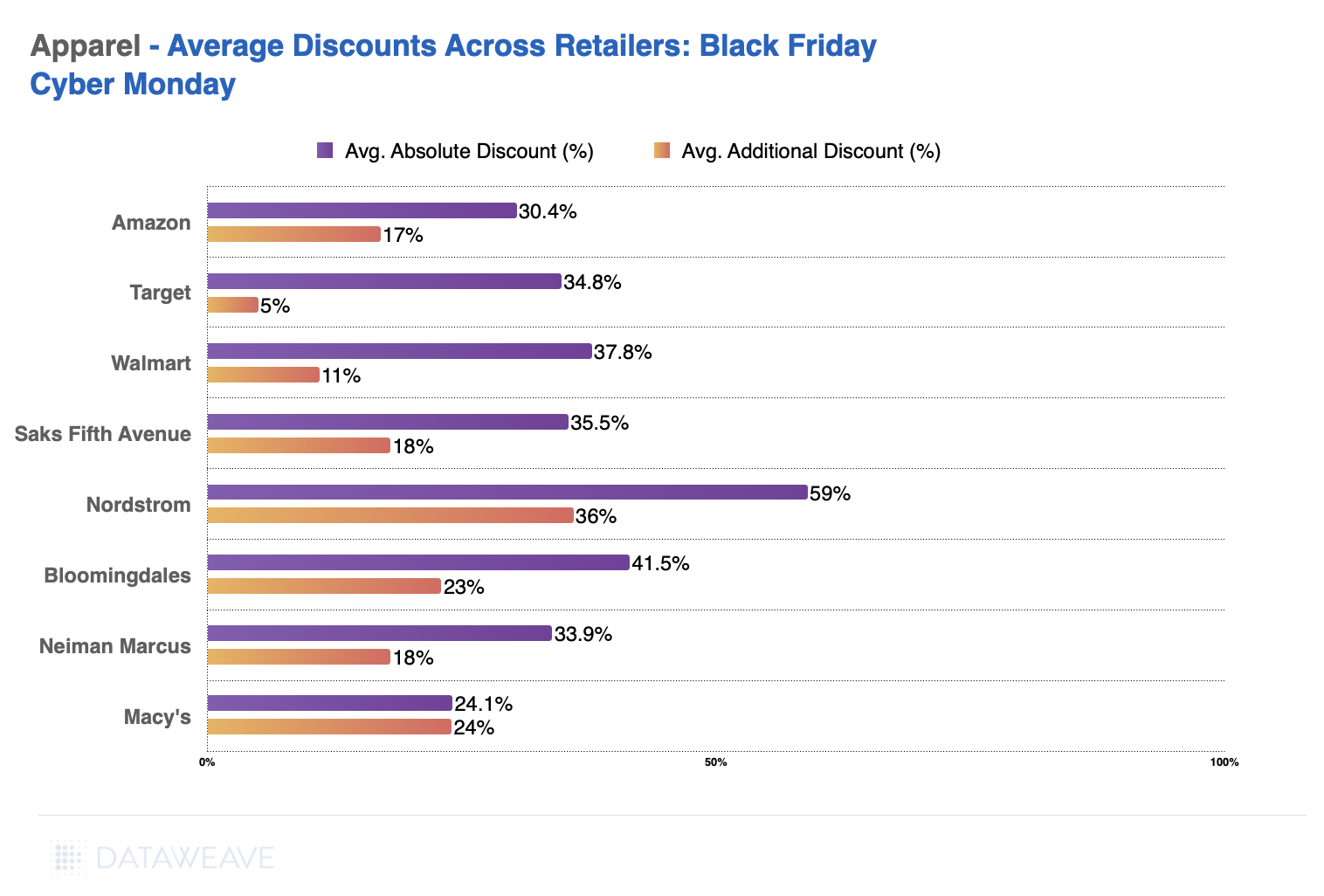

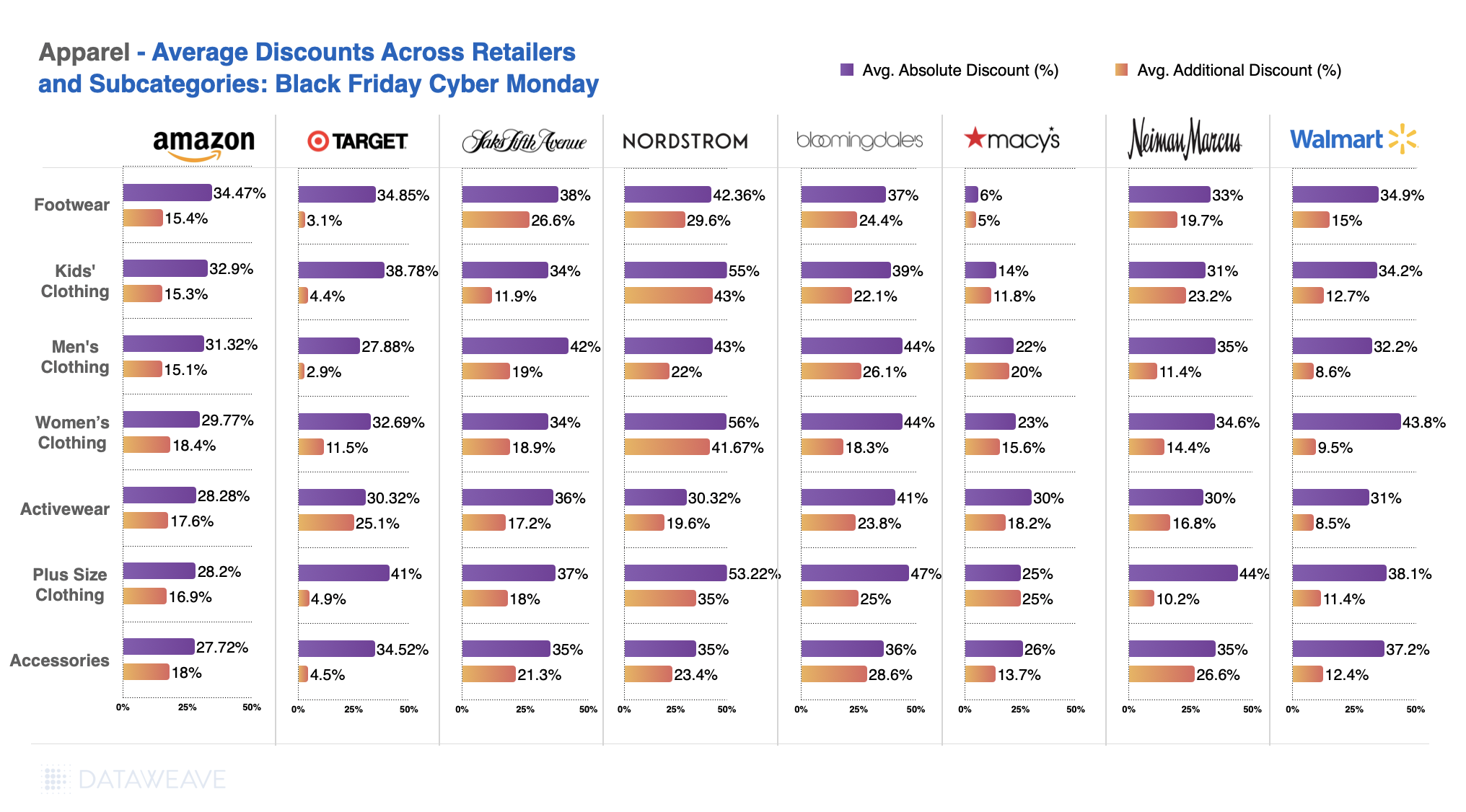

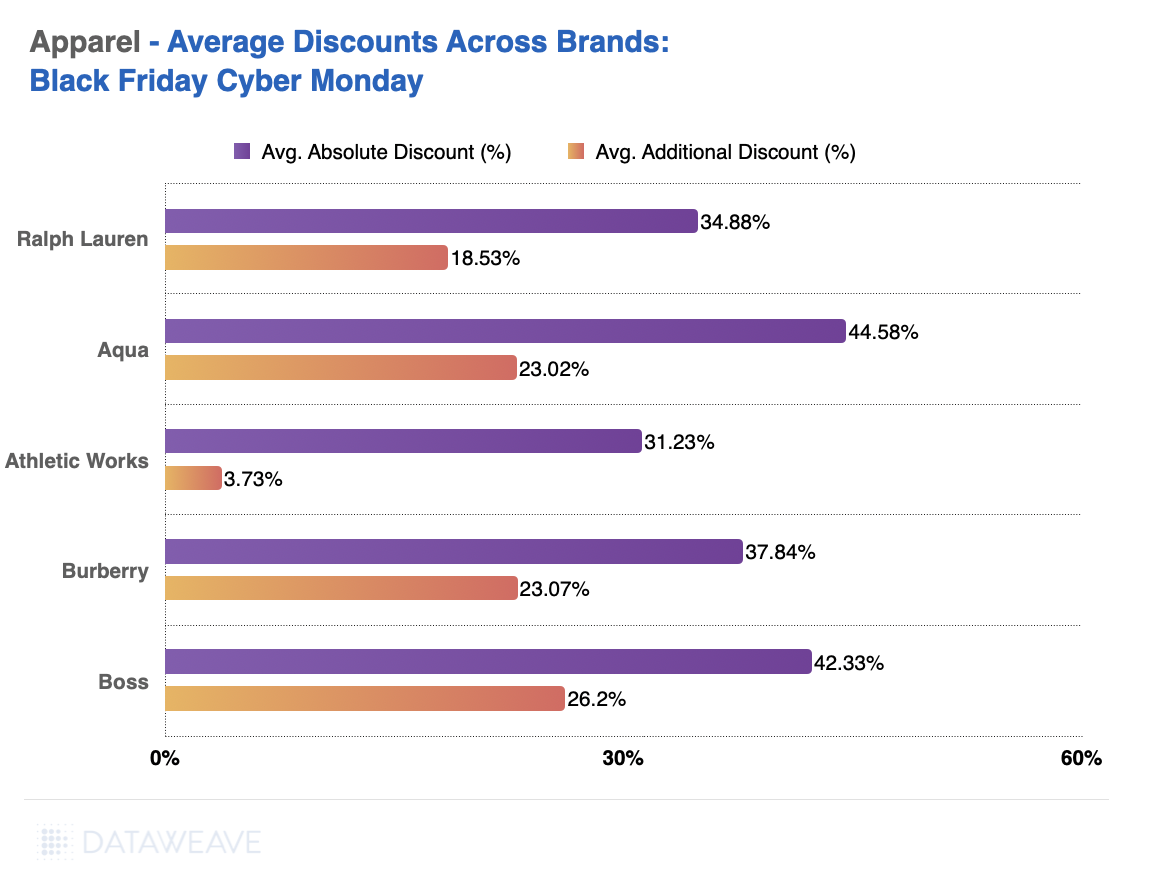

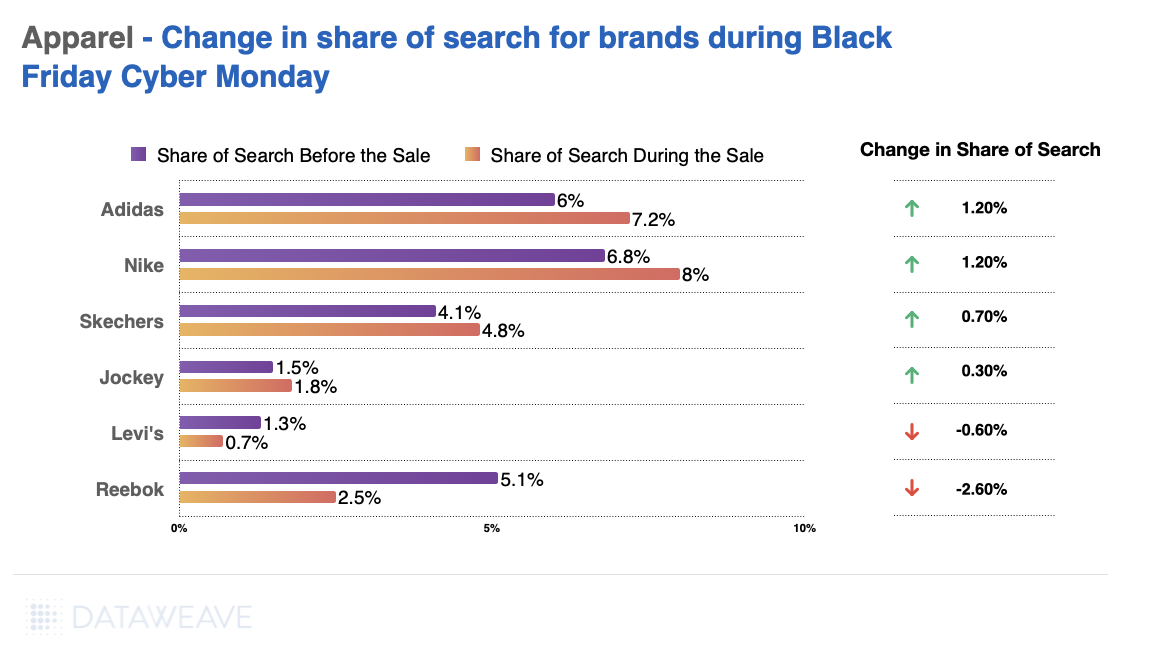

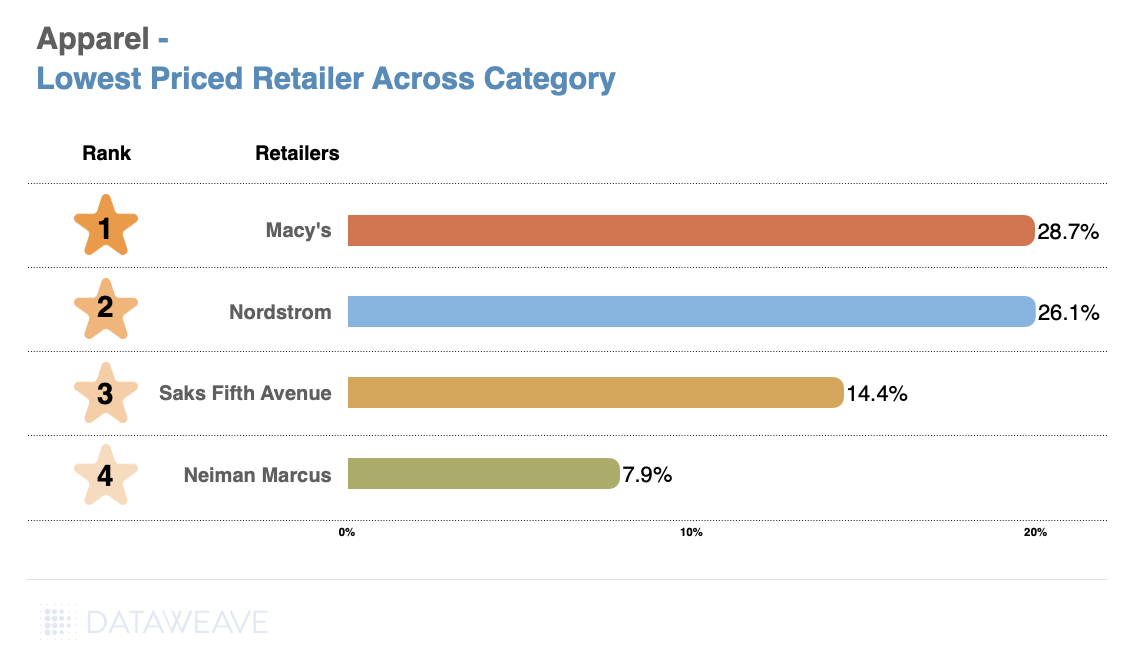

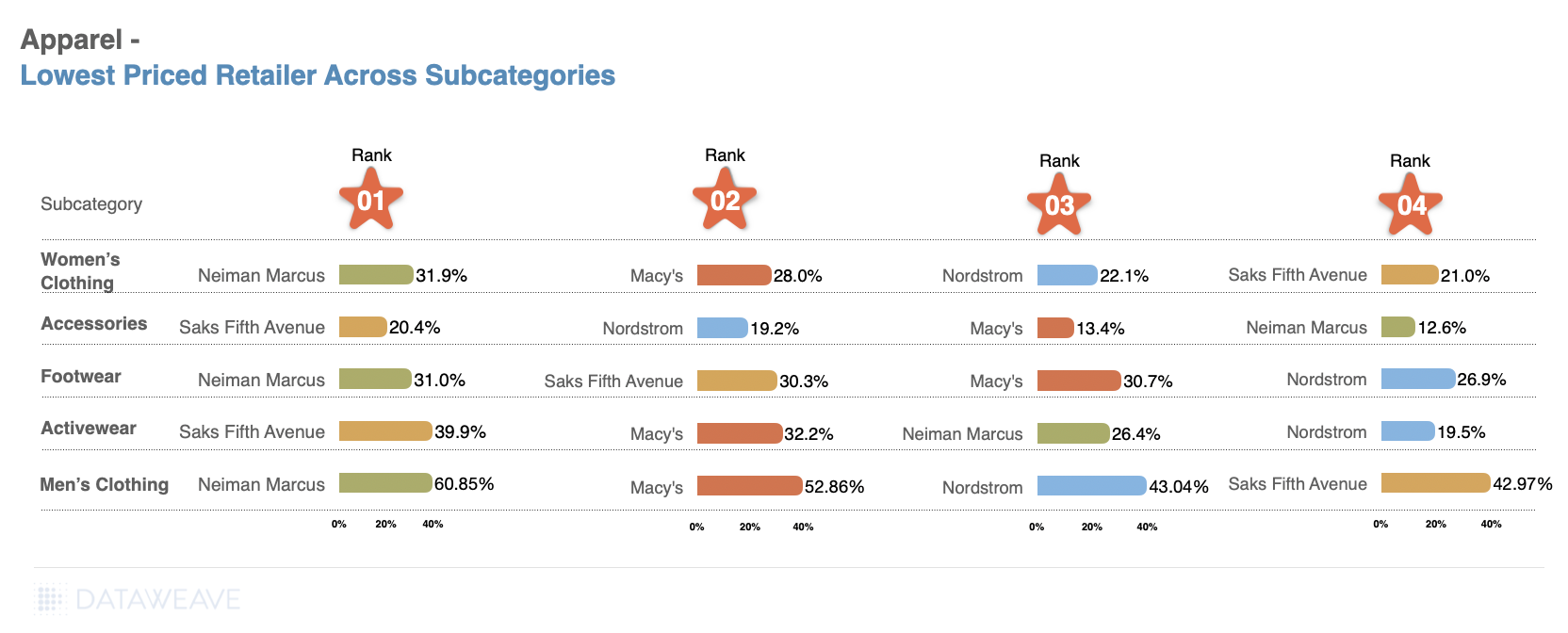

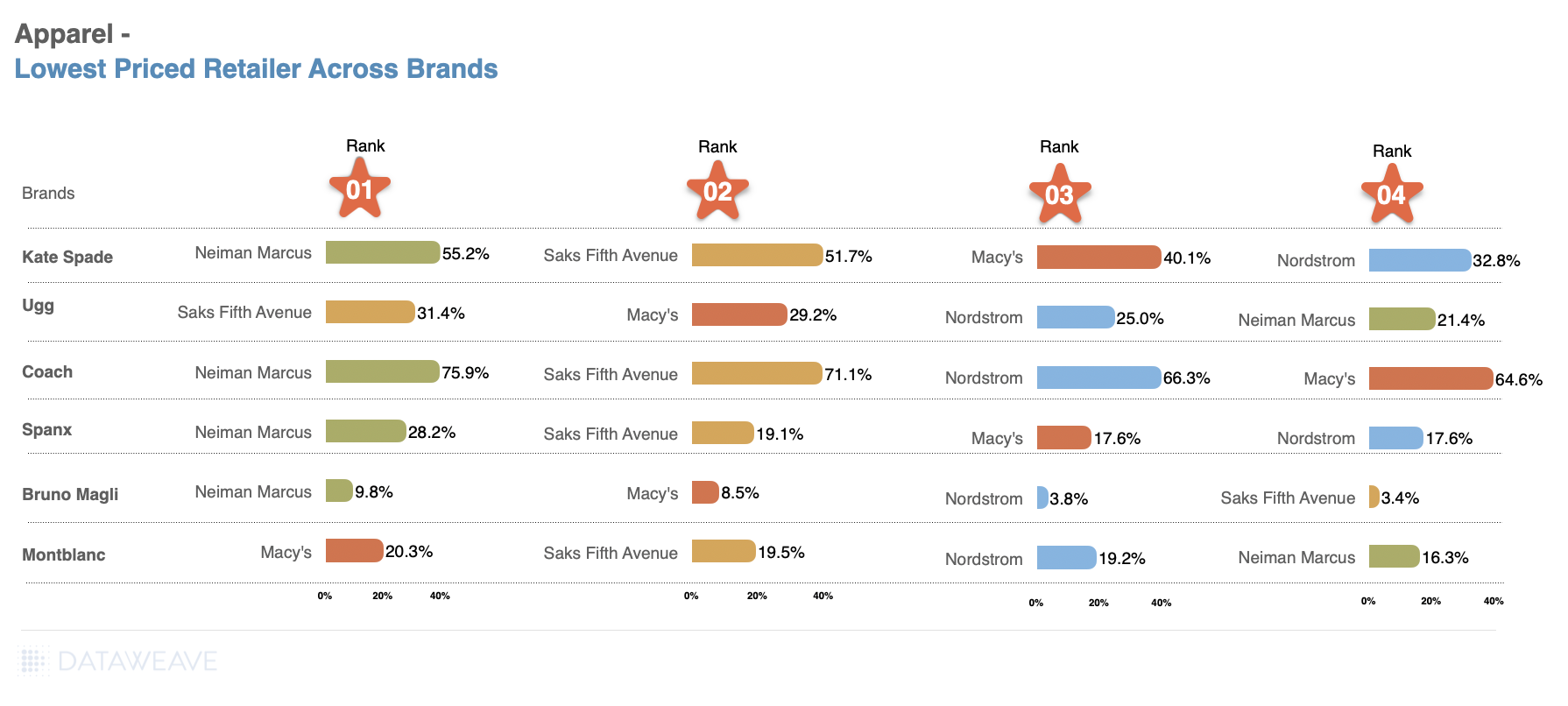

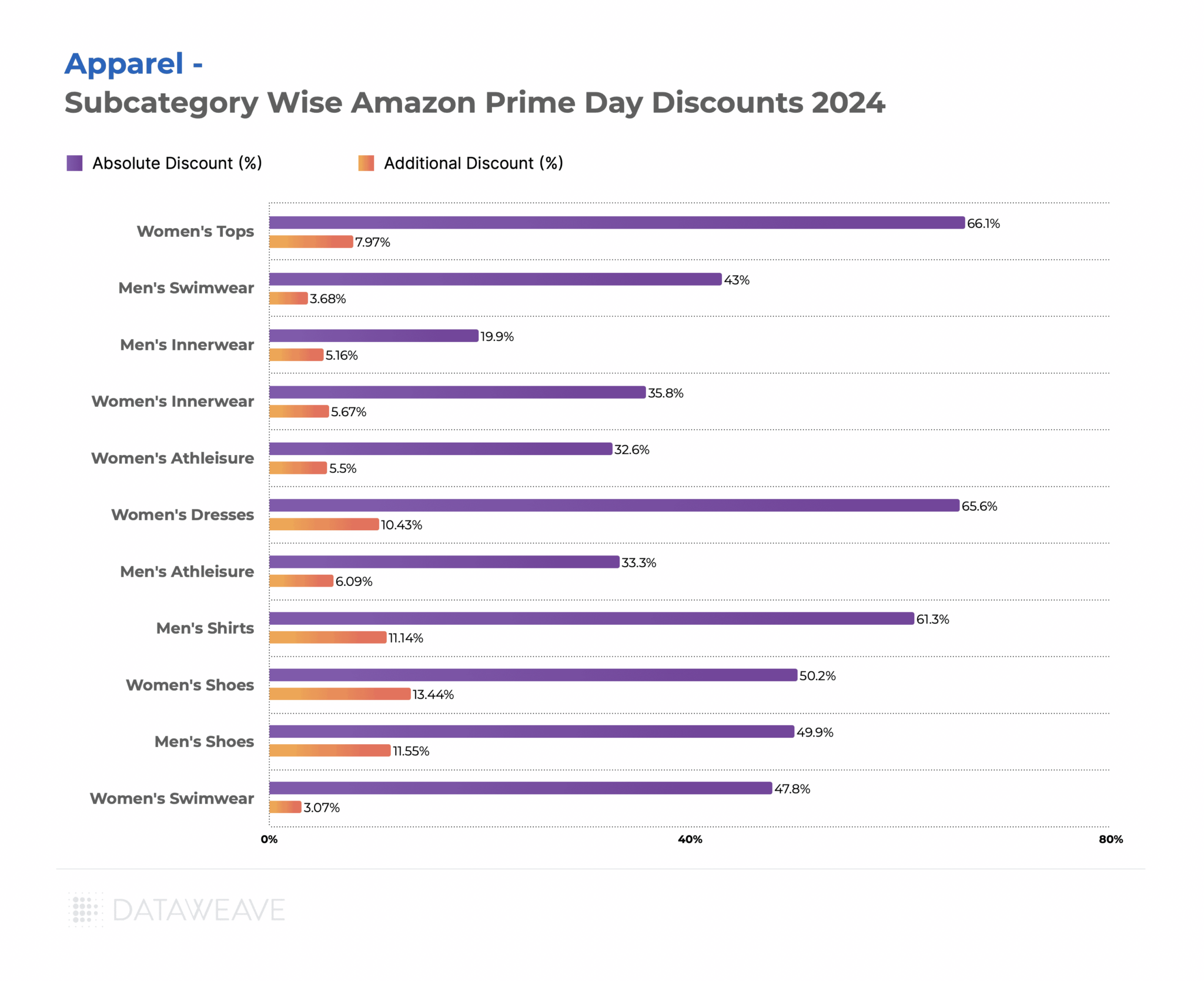

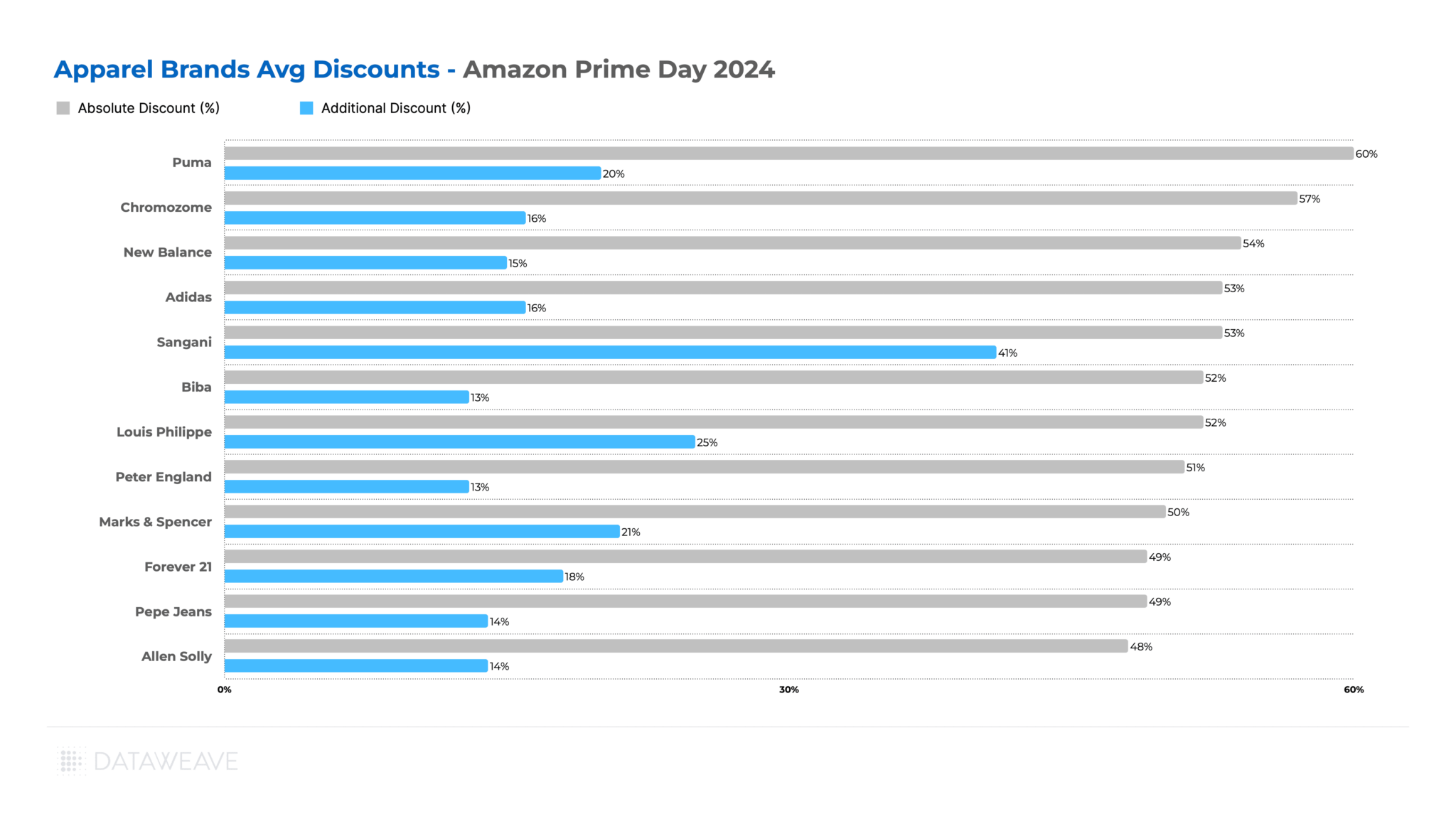

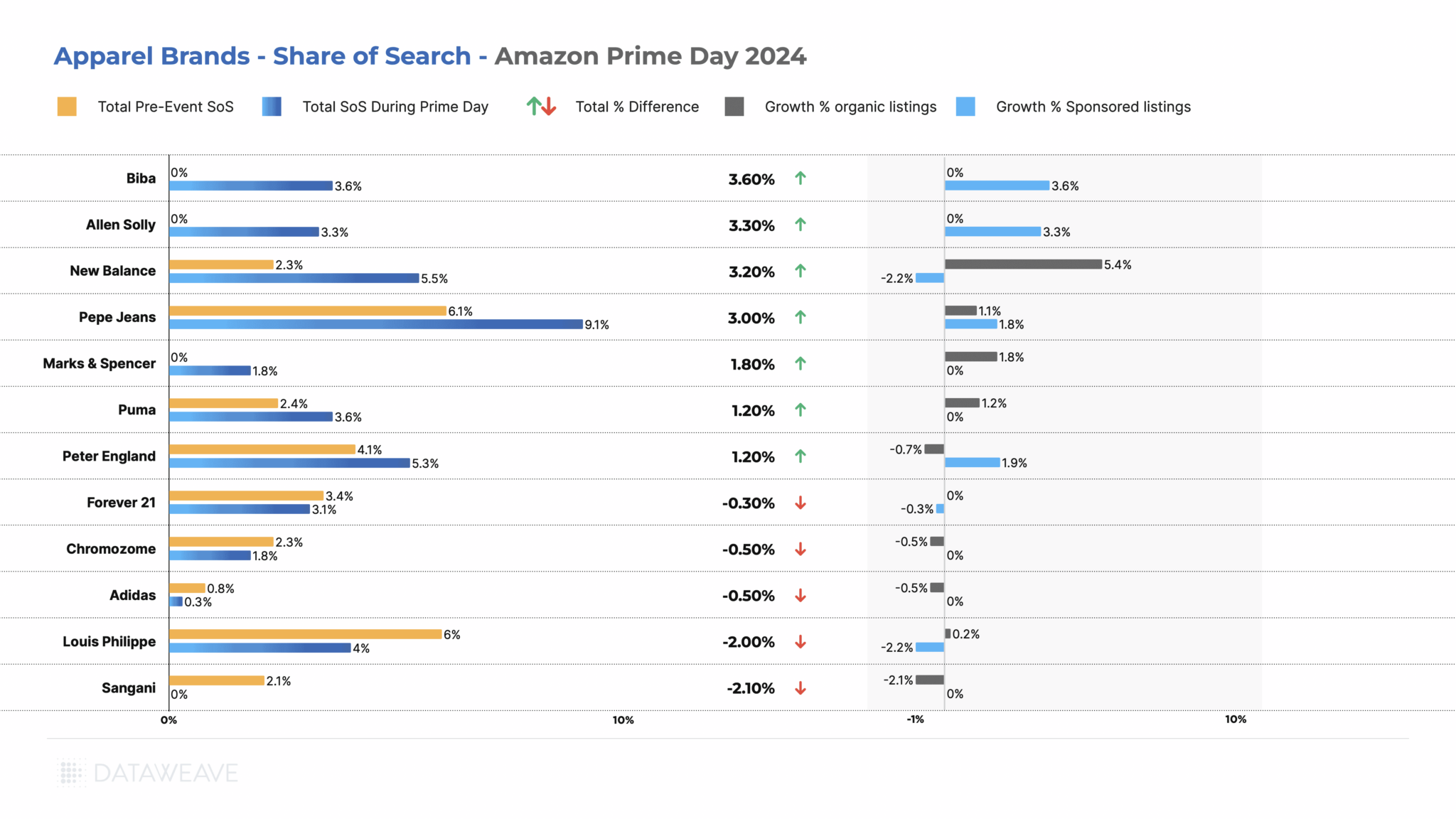

As the holiday shopping season kicked off, savvy shoppers embraced the spirit of the season, drawn by enticing deals. The apparel category is forecasted as the second highest earning category (Source: Statista), expected to generate revenues up to $43.9 billion, closely following consumer electronics. To understand the pricing strategies of top retailers amidst the sale season, DataWeave analyzed the pricing trends for the Apparel category this Black Friday.

We leveraged our AI-powered data platform to analyze the discounting across key retailers. Our analysis focused on the Apparel category, examining how Amazon, Walmart, Target, Saks Fifth Avenue, Nordstrom, Bloomingdales, Neiman Marcus and Macy’s differentiated themselves through their discounts.

For this analysis, we tracked the average discounts of apparel products among leading US retailers during the Thanksgiving weekend sale, including Black Friday. Our sample was chosen to encompass the top 500 ranked products in each product subcategory across during the sale.

Subcategories reported on: Footwear, Kid’s Clothing, Men’s Clothing, Women’s Clothing, Activewear, Plus Size Clothing, Accessories

Timeline of analysis: 10 to 29 November 2024

We focused on the top 500 products ranked for each search keyword on each retail site, using targeted terms aligned with categories like “athleisure” and “plus size clothing”. Our methodology distinguished between standard discounts and Black Friday-specific ‘additional discounts’ or price reductions during the sale compared to the week before, to reveal true consumer value.

Key Findings

This year’s fashion discounts were unprecedented. Let’s take a look.

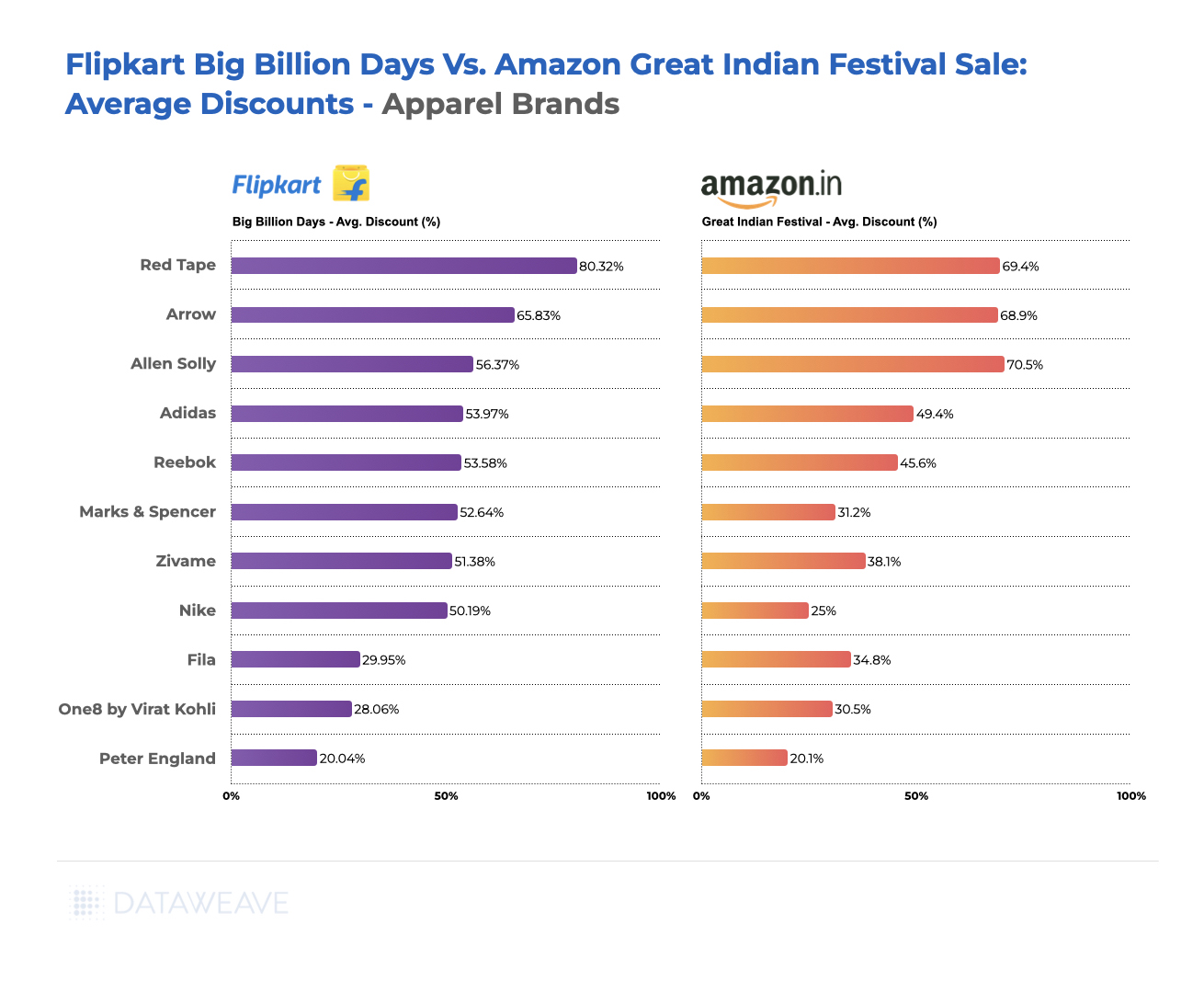

Retailer Level Insights