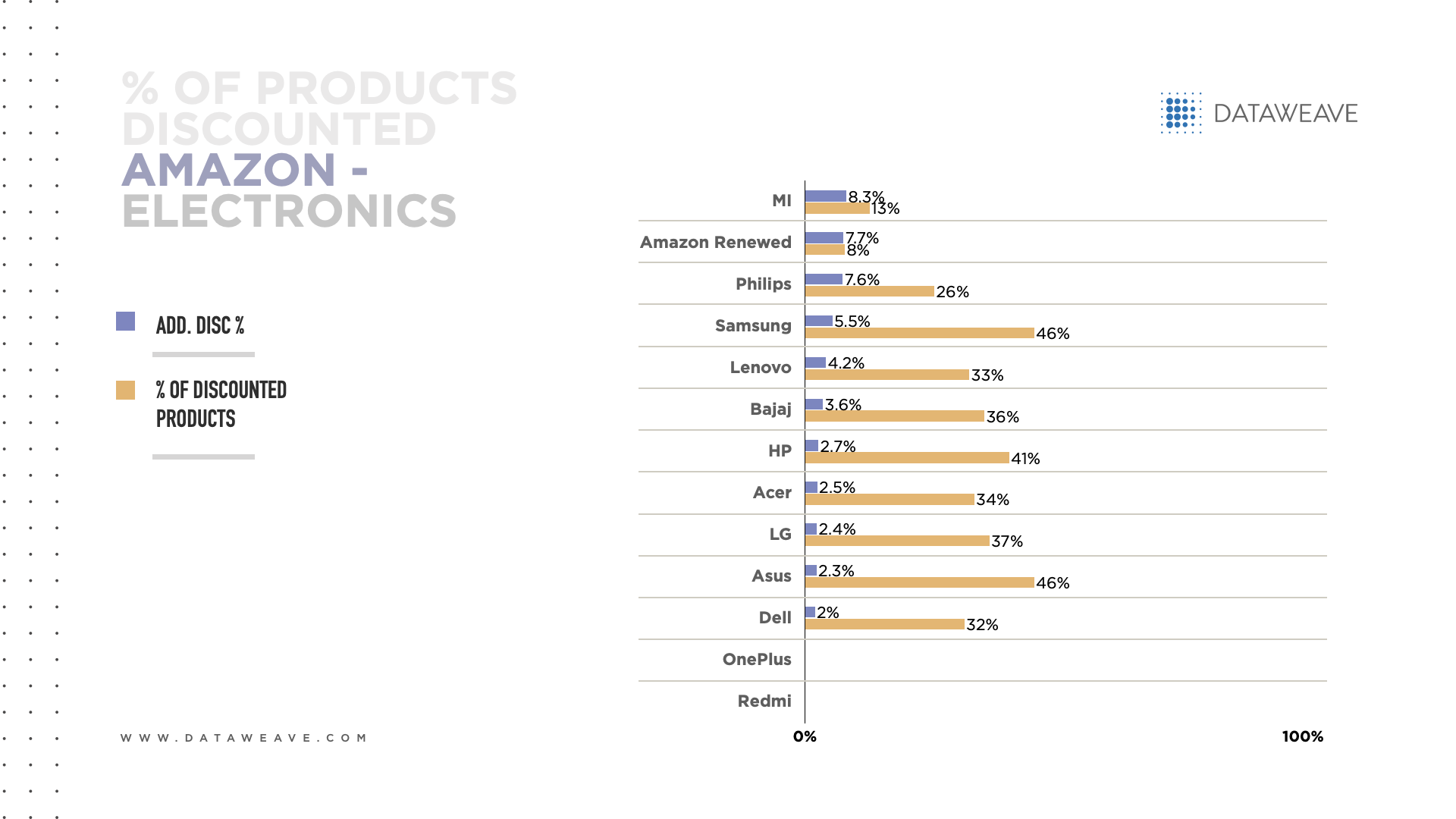

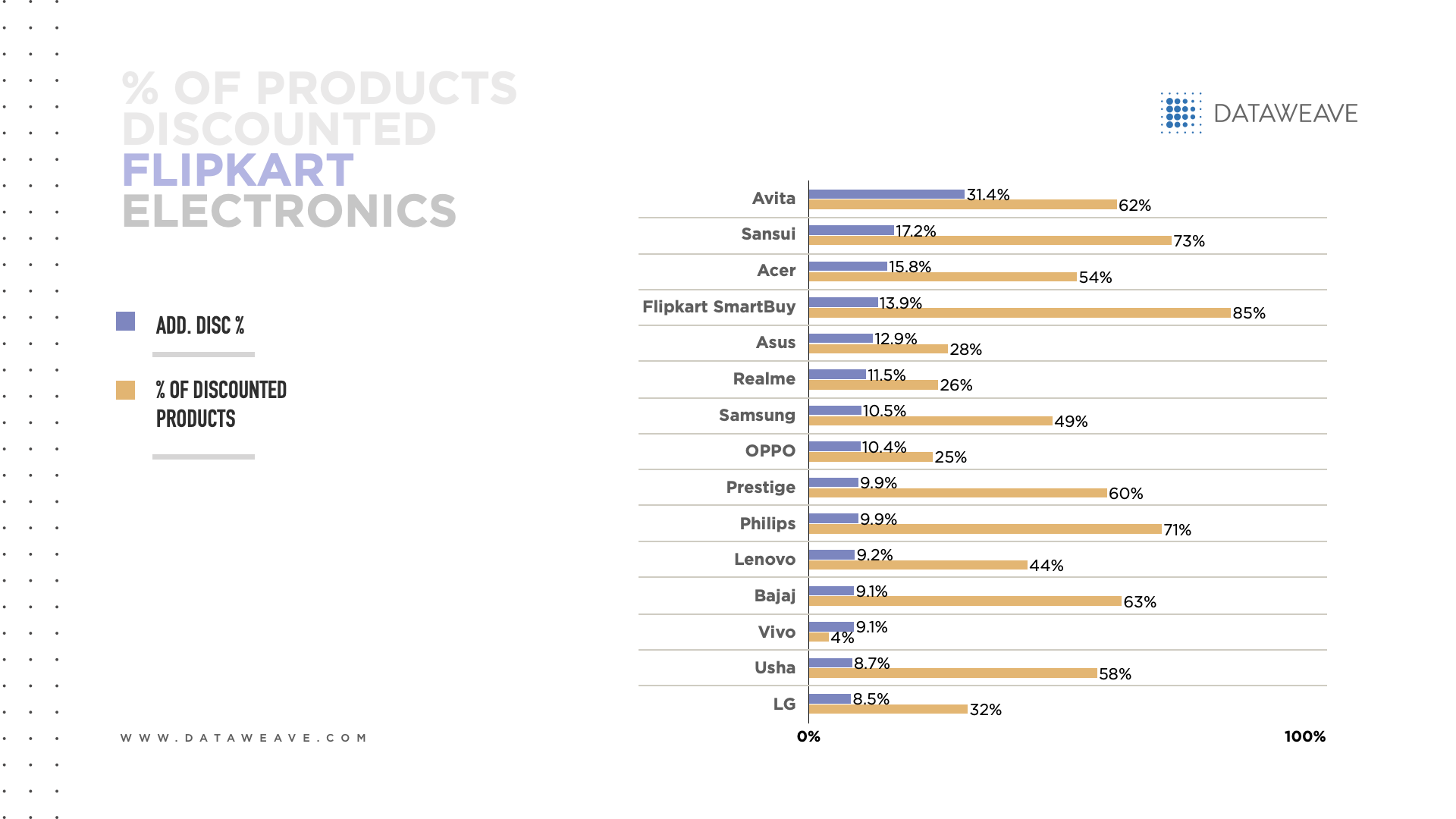

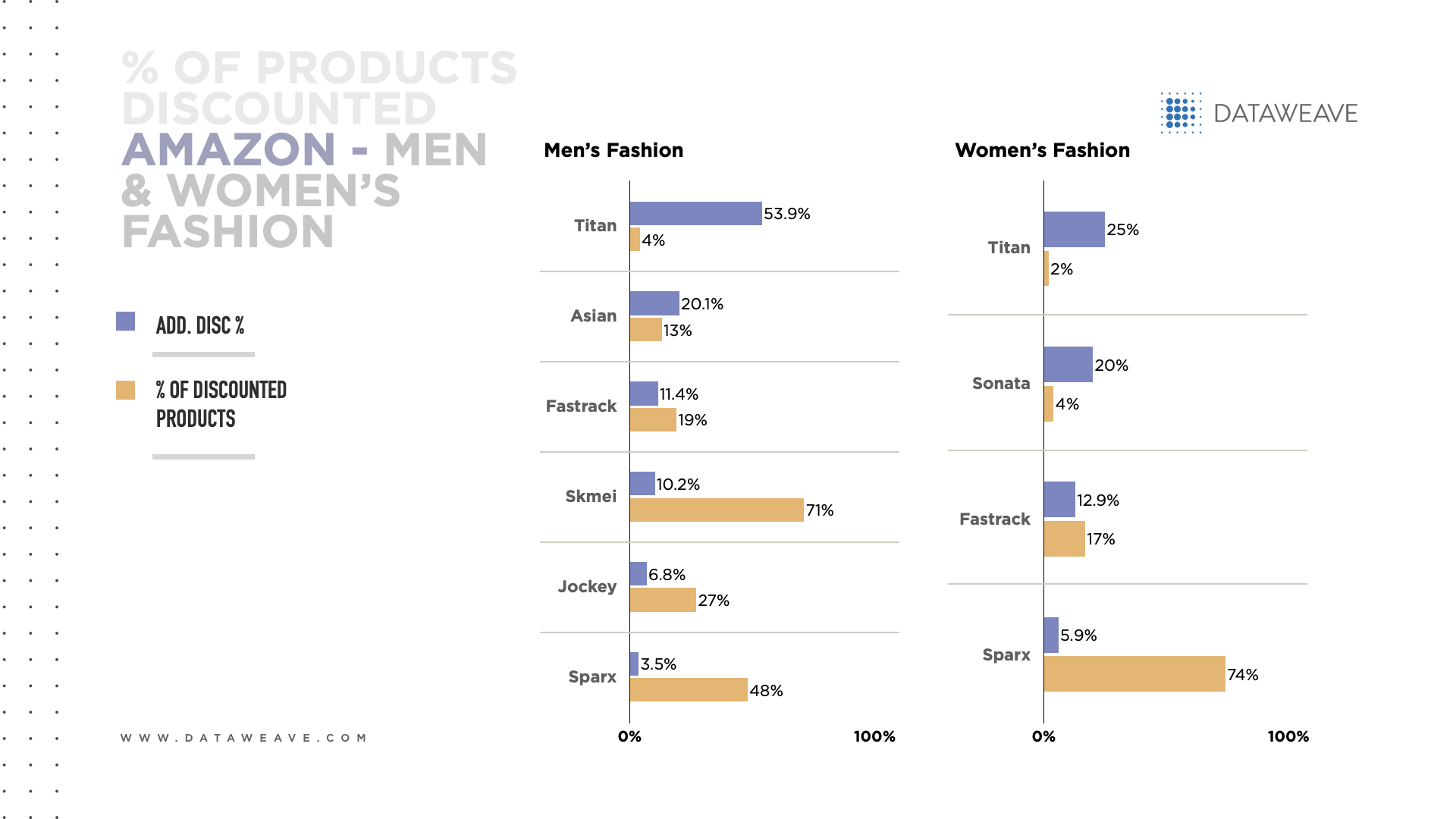

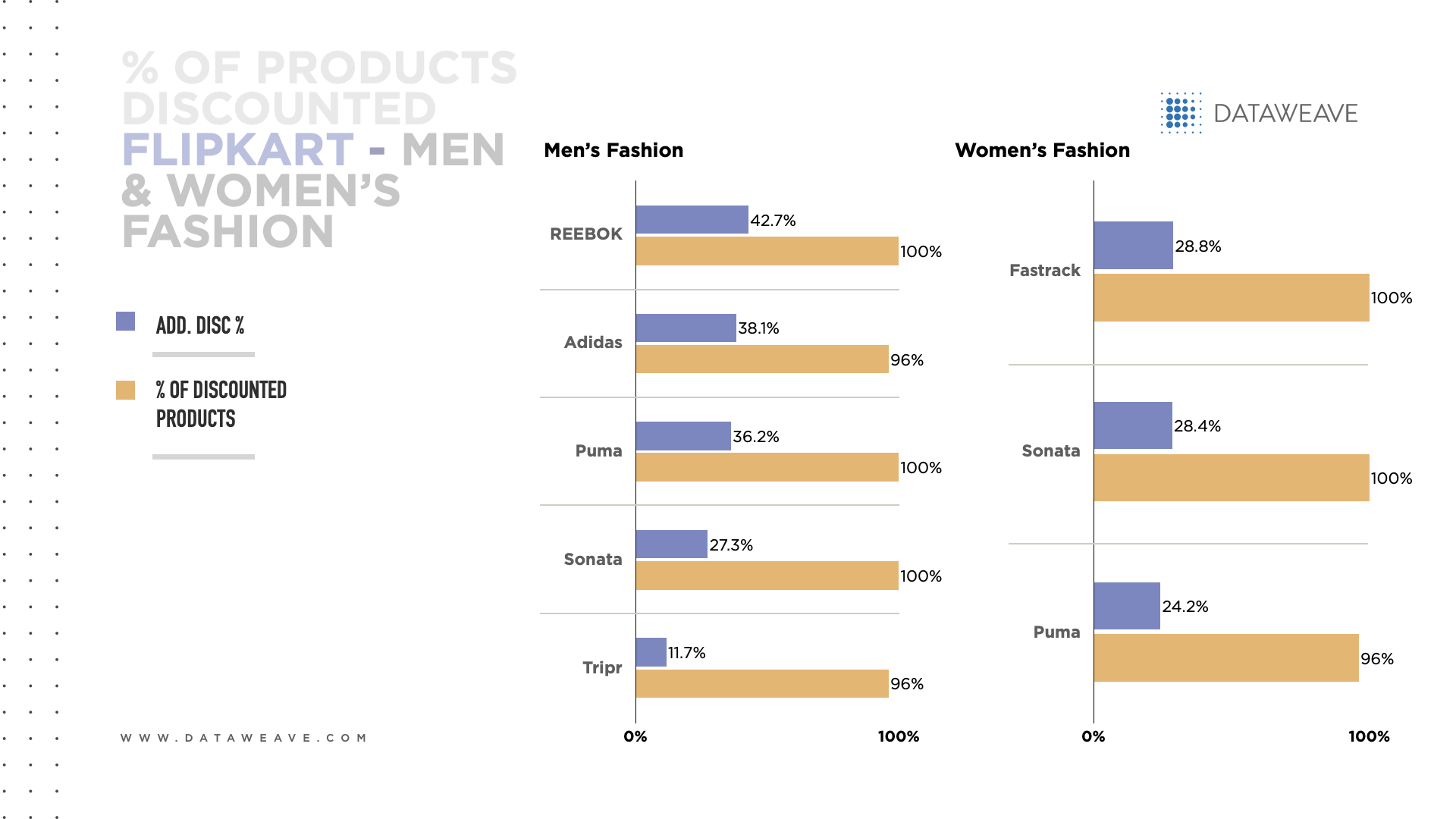

Amazon’s Prime Day 2021 global shopping event took place June 21 and 22, 2021 and smashed previous sales records. At DataWeave, we wanted to know how Prime Day 2021 deals and discounts on electronics compared across retailers and regions. We focused on how retailers adapted their Prime Day pricing strategies to stand out in the competitive consumer electronics category.

Our Methodology

We tracked the pricing of several leading retailers in nine countries across five regions, including:

• The US (Amazon US, Best Buy, Target and Walmart)

• The UK (Amazon UK, Ebay, Etsy and OnBuy)

• Europe (Amazon France, Amazon Germany and Amazon Italy)

• The Middle East (Amazon Saudi Arabia and Amazon UAE)

• Asia (Amazon Japan and Amazon Singapore)

Let’s see how retailers used pricing tactics to gain a competitive advantage during Prime Day, as well as which electronics brands had the highest discounts around the world.

Percentage of items with a price decrease

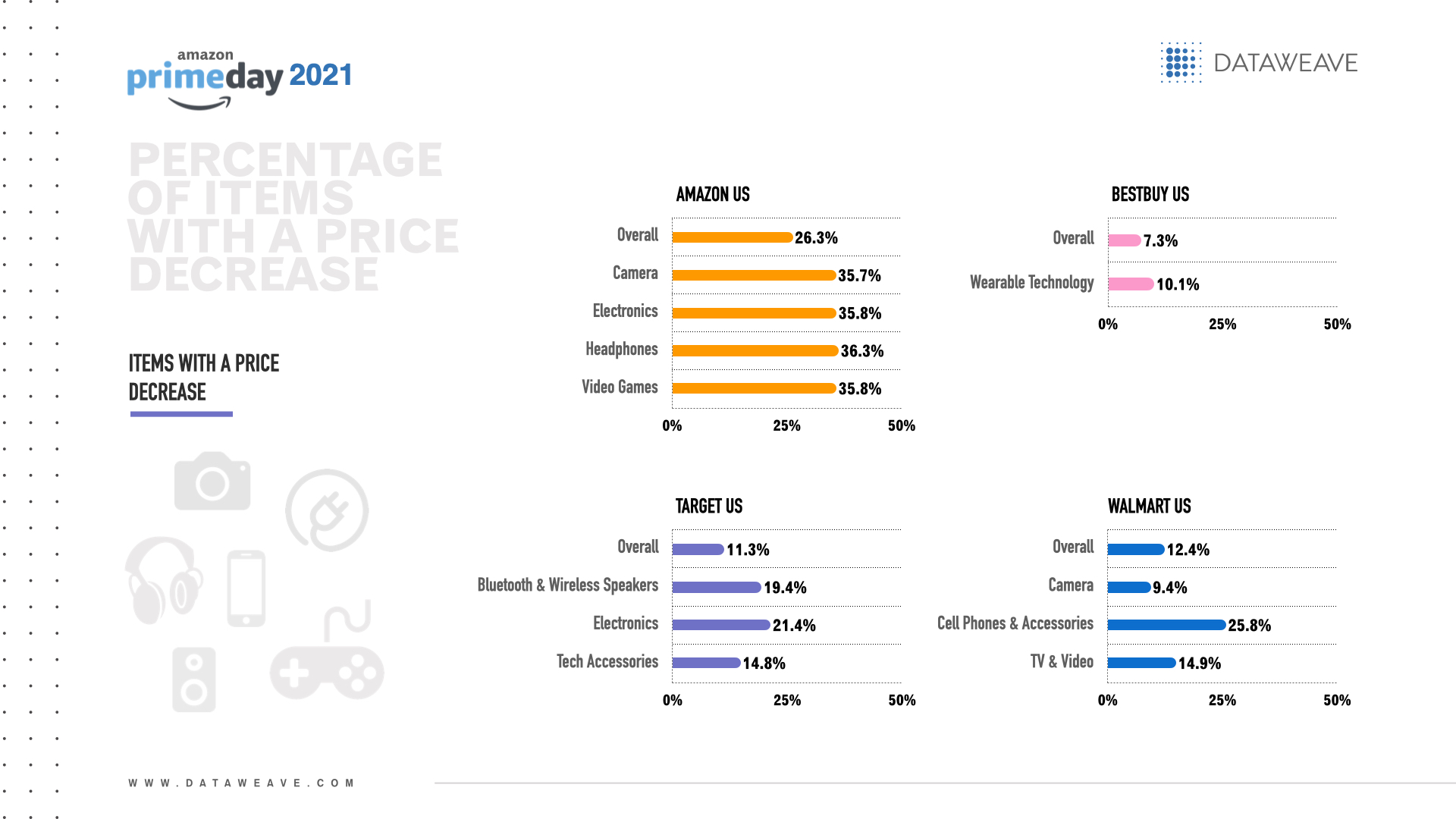

The US retailer with the overall highest percentage of items with a price decrease for Prime Day was Amazon US (26.3%).

Electronics subcategories with the highest percentage of items with a price decrease per US retailer were:

• Amazon US: Headphones (36.3%), video games and electronics (both 35.8%) and cameras (35.7%)

• Best Buy: Wearables (10.1%) and electronics (6.8%)

• Target: Electronics (21.4%), Bluetooth & wireless speakers (19.4%) and tech accessories (14.8%)

• Walmart: Cell phones & accessories (25.8%), TV & video (14.9%) and cameras (9.4%)

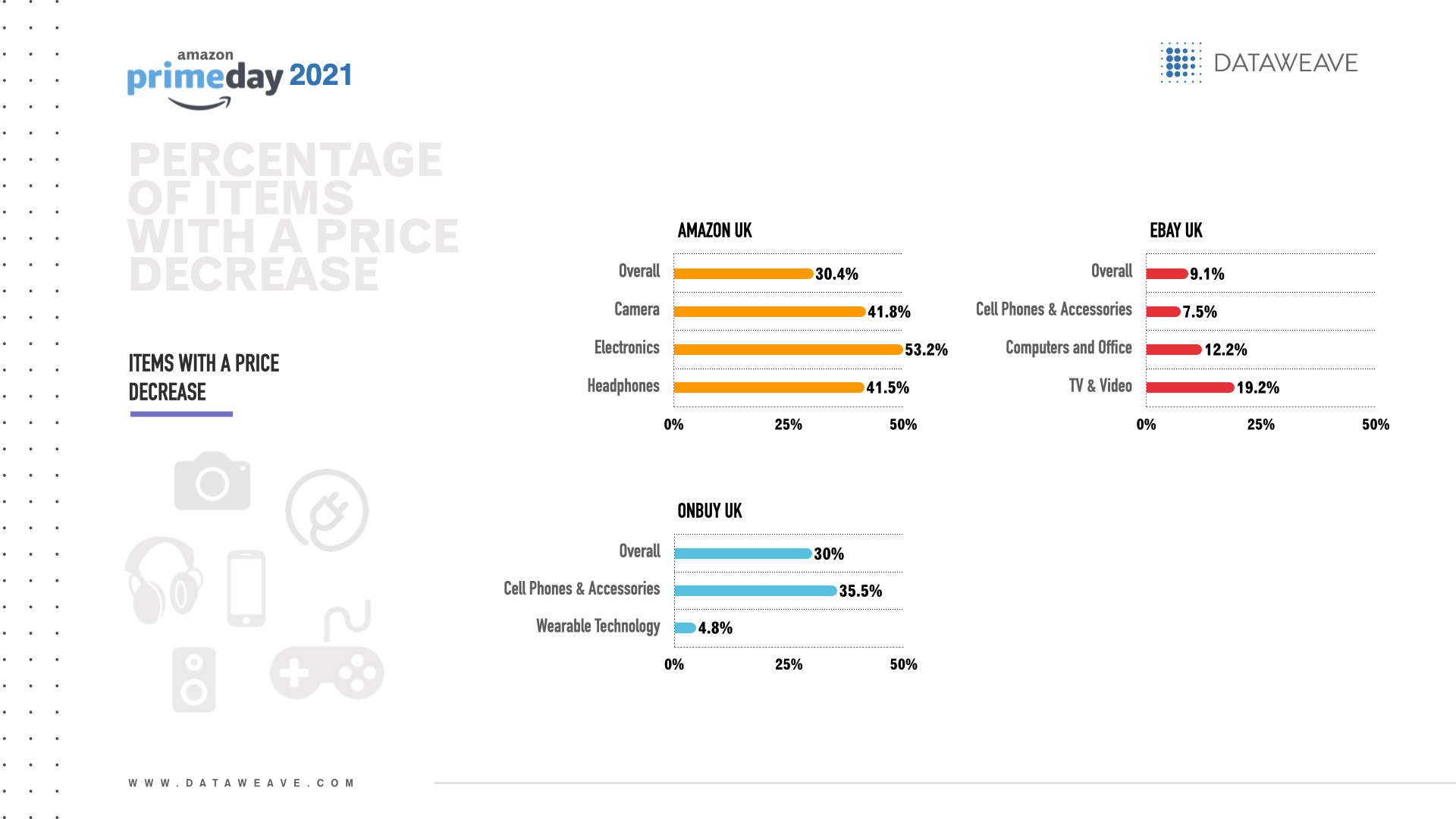

The UK retailer with the overall highest percentage of items with a price decrease for Prime Day was Amazon UK (30.4%), closely followed by OnBuy (30.0%). Of note, Amazon UK offered price increases on 10 times as many products as OnBuy (2379 vs. 237).

Electronics subcategories with the highest percentage of items with a price decrease per UK retailer were:

• Amazon UK: Electronics (53.2%), cameras (41.8%) and headphones (41.5%)

• Ebay: TV & video (19.2%), computers & office (12.2%) and cell phones & accessories (7.5%)

• Etsy: Electronics (1.4%)

• OnBuy: Cell phones & accessories (35.5%) and wearables (4.8%)

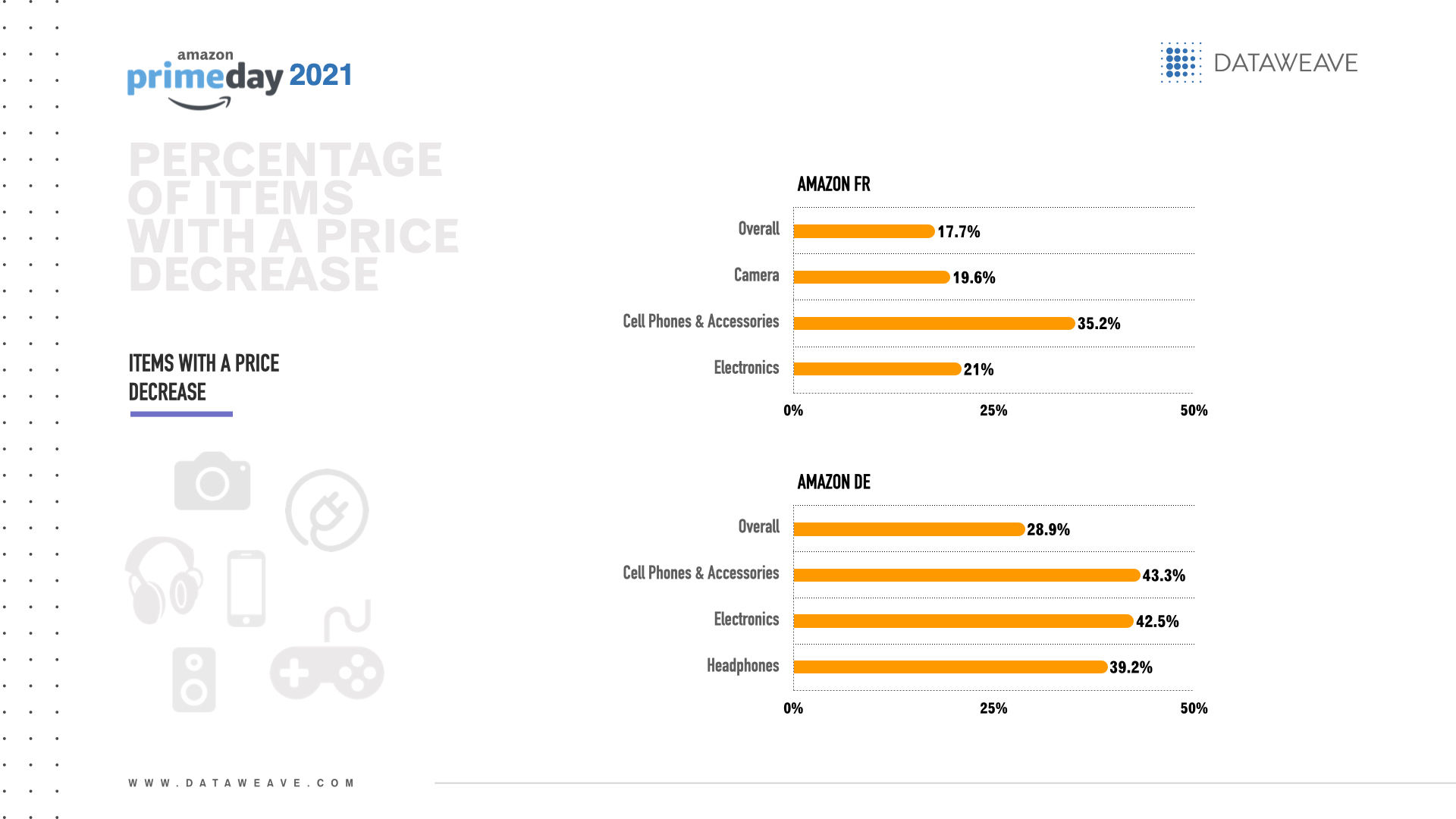

In Europe, Amazon Germany had the overall highest percentage of items with a price decrease for Prime Day (28.9%).

Electronics subcategories with the highest percentage of items with a price decrease per European retailer were:

• Amazon France: Cell phones & accessories (35.2%), electronics (21.0%) and cameras (19.6%)

• Amazon Germany: Cell phones & accessories (43.3%), electronics (42.5%) and headphones (39.2%)

• Amazon Italy: Headphones (25.0%), cell phones & accessories (14.3%) and Bluetooth & wireless speakers (8.3%)

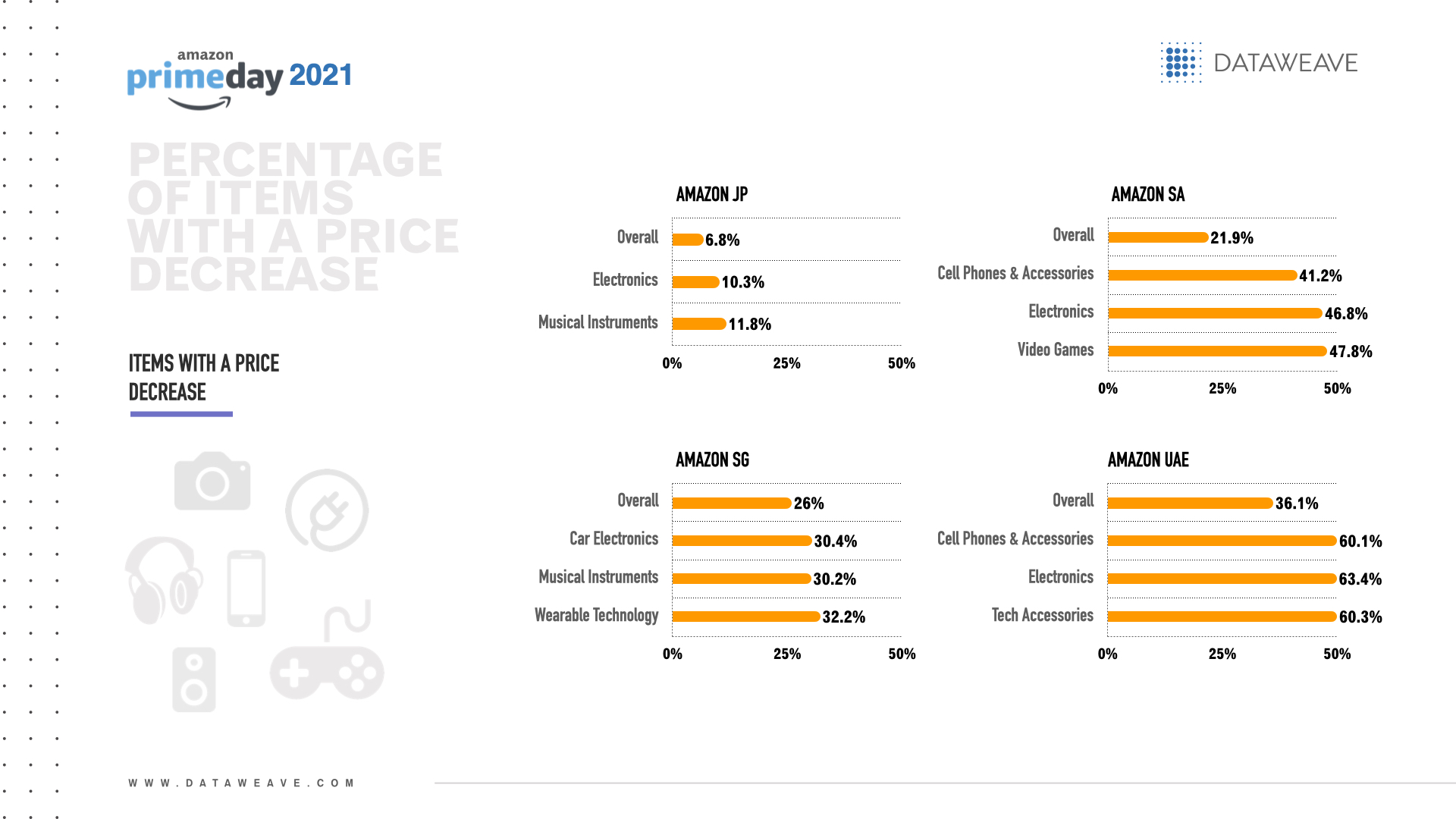

Across the Middle East & Asia, Amazon UAE had the overall highest percentage of items with a price decrease for Prime Day (36.1%).

Electronics subcategories with the highest percentage of items with a price decrease per retailer were:

• Amazon Saudi Arabia: Video games (47.8%), electronics (46.8%) and cell phones & accessories (41.2%)

• Amazon UAE: Electronics (63.4%), tech accessories (60.3%) and cell phones & accessories (60.1%)

• Amazon Japan: TV & video (14.9%), musical instruments (11.8%) and electronics (10.3%)

• Amazon Singapore: Wearables (32.2%), car electronics (30.4%) and musical instruments (30.2%)

Magnitude of price decrease

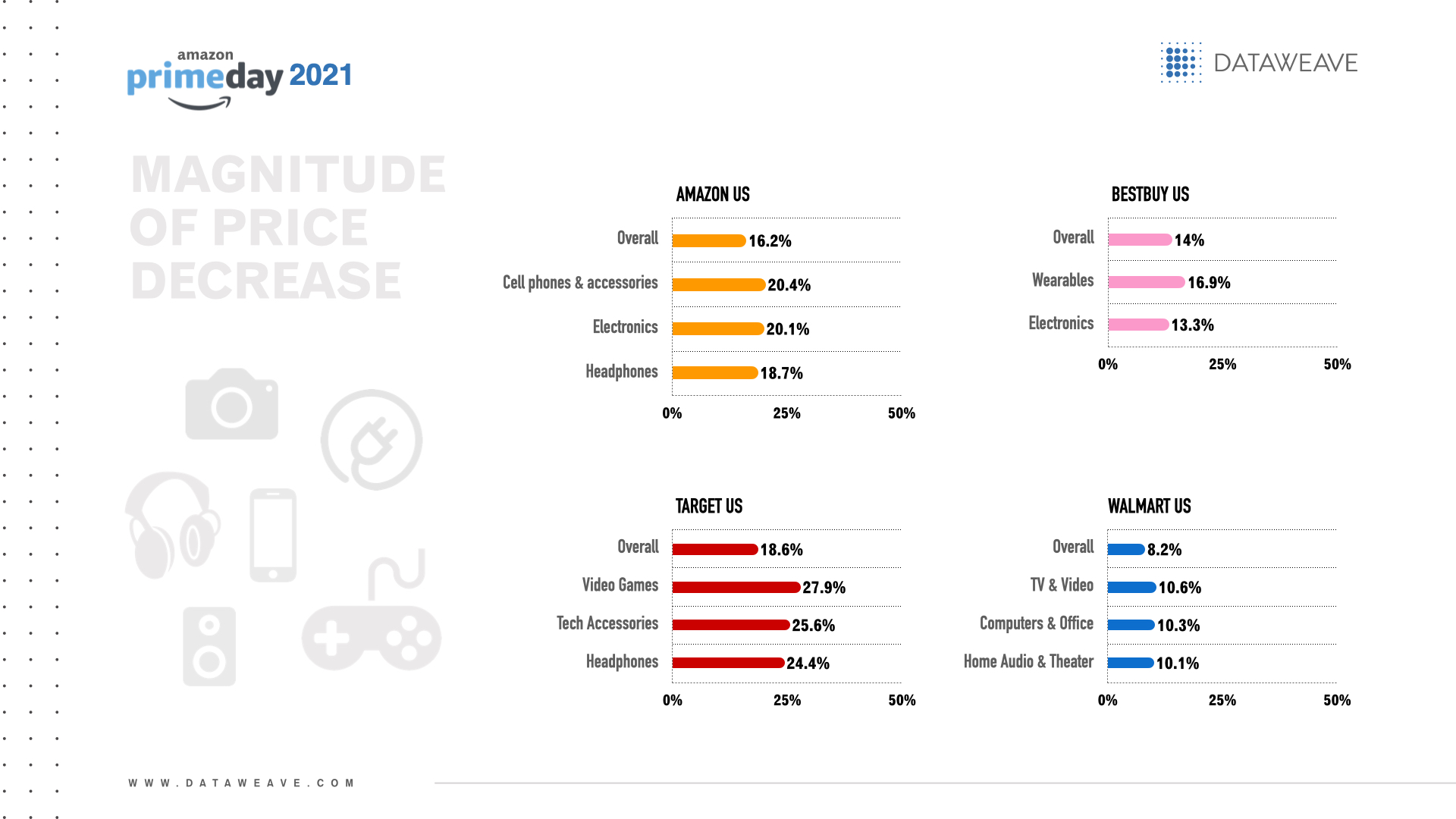

The US retailer with the greatest overall magnitude of price decrease for Prime Day was Target (18.6%).

The electronics subcategories with the greatest magnitude of price decrease per US retailer were:

• Amazon US: Cell phones & accessories (20.4%), electronics (20.1%) and headphones (18.7%)

• Best Buy: Wearables (16.9%) and electronics (13.3%)

• Target: Video games (27.9%), tech accessories (25.6%) and headphones (24.4%)

• Walmart: TV & video (10.6%), computers & office (10.3%) and home audio & theater (10.1%)

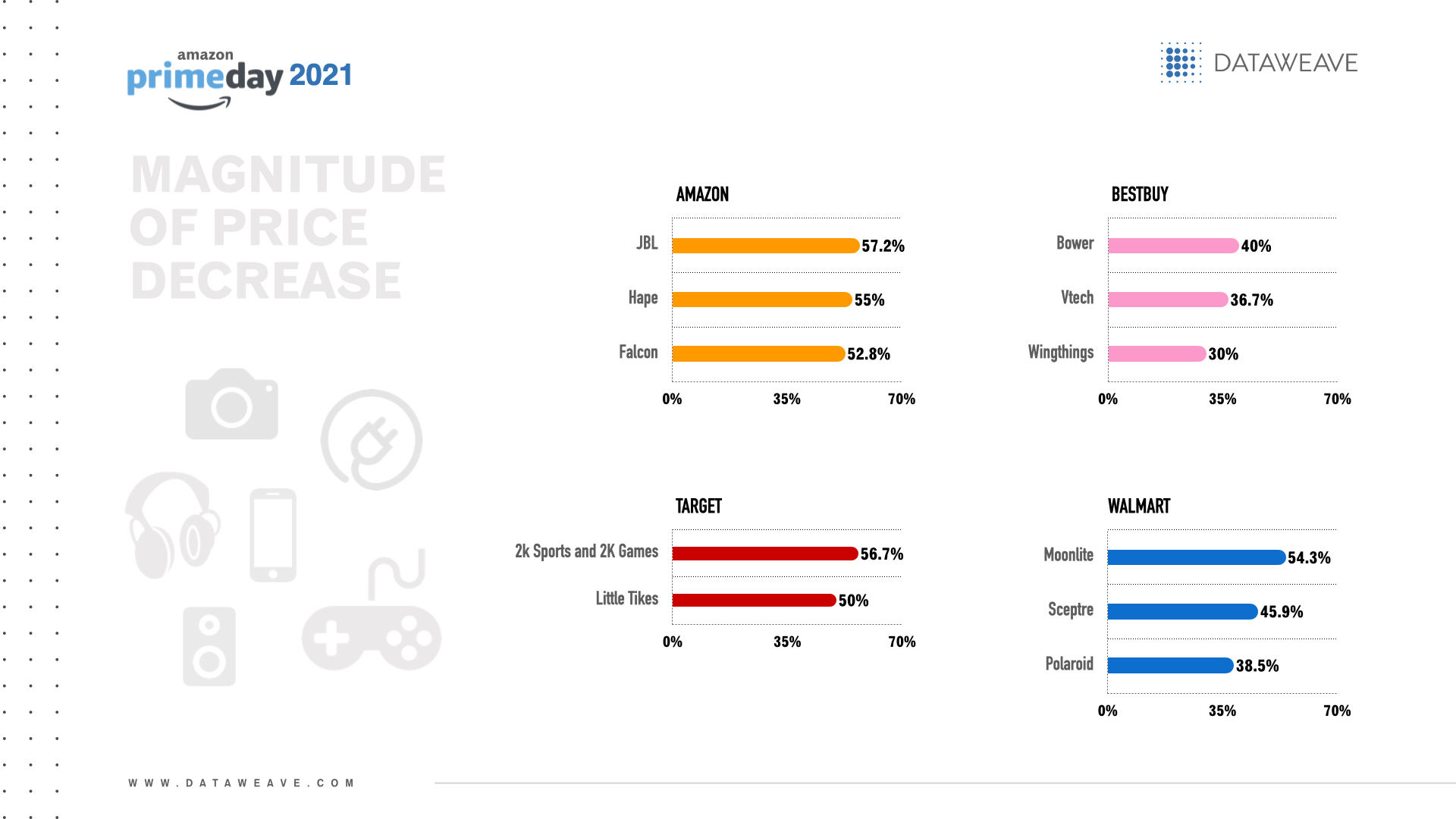

Brands with the greatest magnitude of price decreases per US retailer included:

• Amazon US: JBL (57.2%), Hape (55.0%) and Falcon (52.8%)

• Best Buy: Bower (40.0%), Vtech (36.7%) and Wingthings (30.0%)

• Target: 2k Sports and 2K Games (both 56.7%), Little Tikes (50.0%)

• Walmart: Moonlite (54.3%), Sceptre (45.9%) and Polaroid (38.5%)

The UK retailer with the greatest overall magnitude of price decrease for Prime Day was OnBuy (22.1%).

The electronics subcategories with the greatest magnitude of price decrease per UK retailer were:

• Amazon UK: Home audio & theater (28.4%), electronics (21.7%) and cell phones & accessories (20.1%)

• Ebay: TV & video (19.5%), wearables (18.7%) and computer & office (16.6%)

• Etsy: Electronics (14.8%)

• OnBuy: Cell phones & accessories (22.3%) and wearables (5.9%)

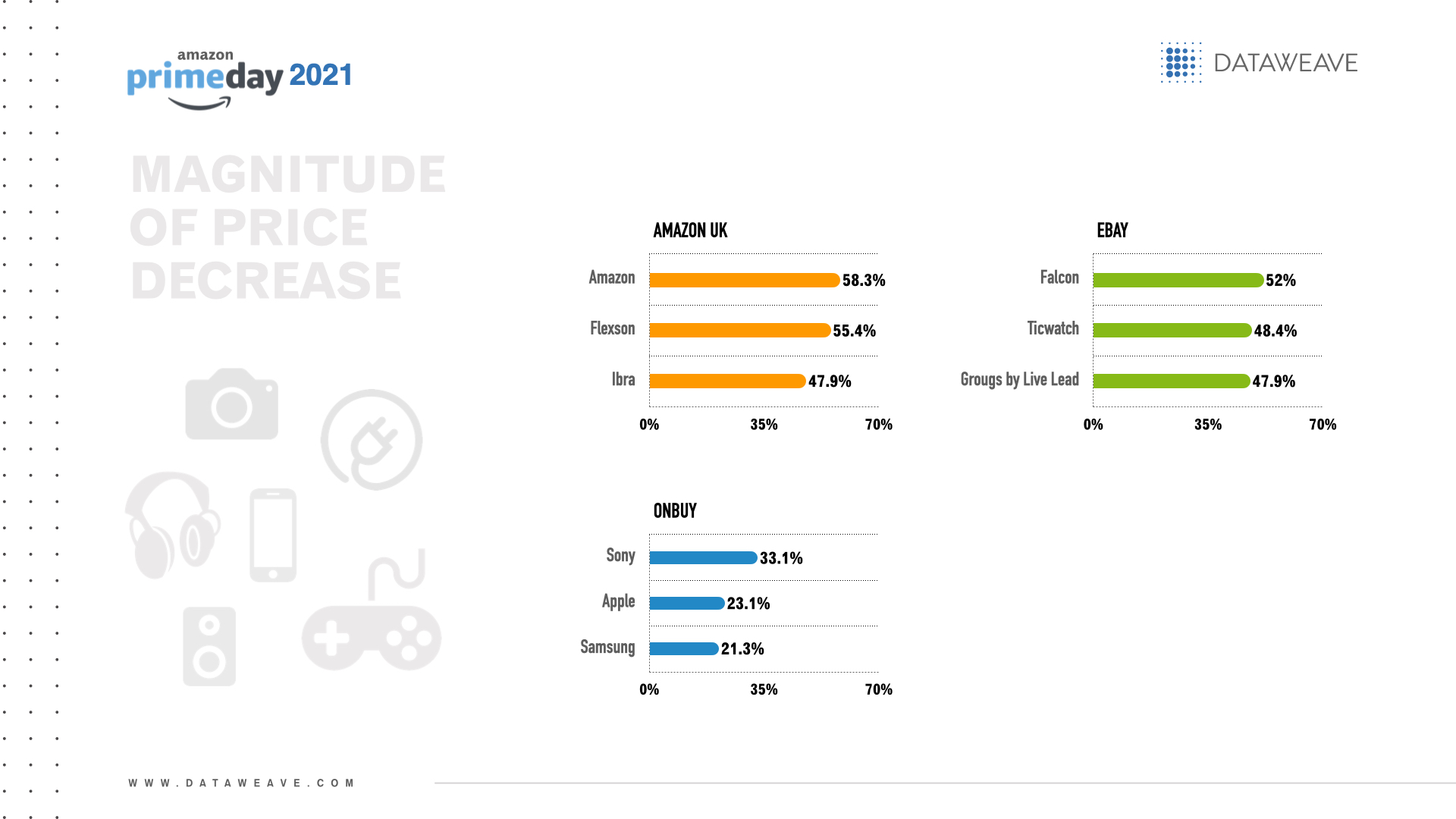

Brands with the greatest magnitude of price decreases across electronics categories per UK retailer included:

• Amazon UK: Amazon (58.3% for both cell phones & accessories and headphones), Flexson (55.4%) and Ibra (47.9% for both cameras and TV & video)

• Ebay: Falcon (52.0%), Ticwatch (48.4%) and Grougs by Live Lead (47.9%)

• OnBuy: Sony (33.1%), Apple (23.1%) and Samsung (21.3%)

Among European retailers, Amazon Italy offered the greatest overall magnitude of price decrease for Prime Day (18.9%) among a total of 66 products.

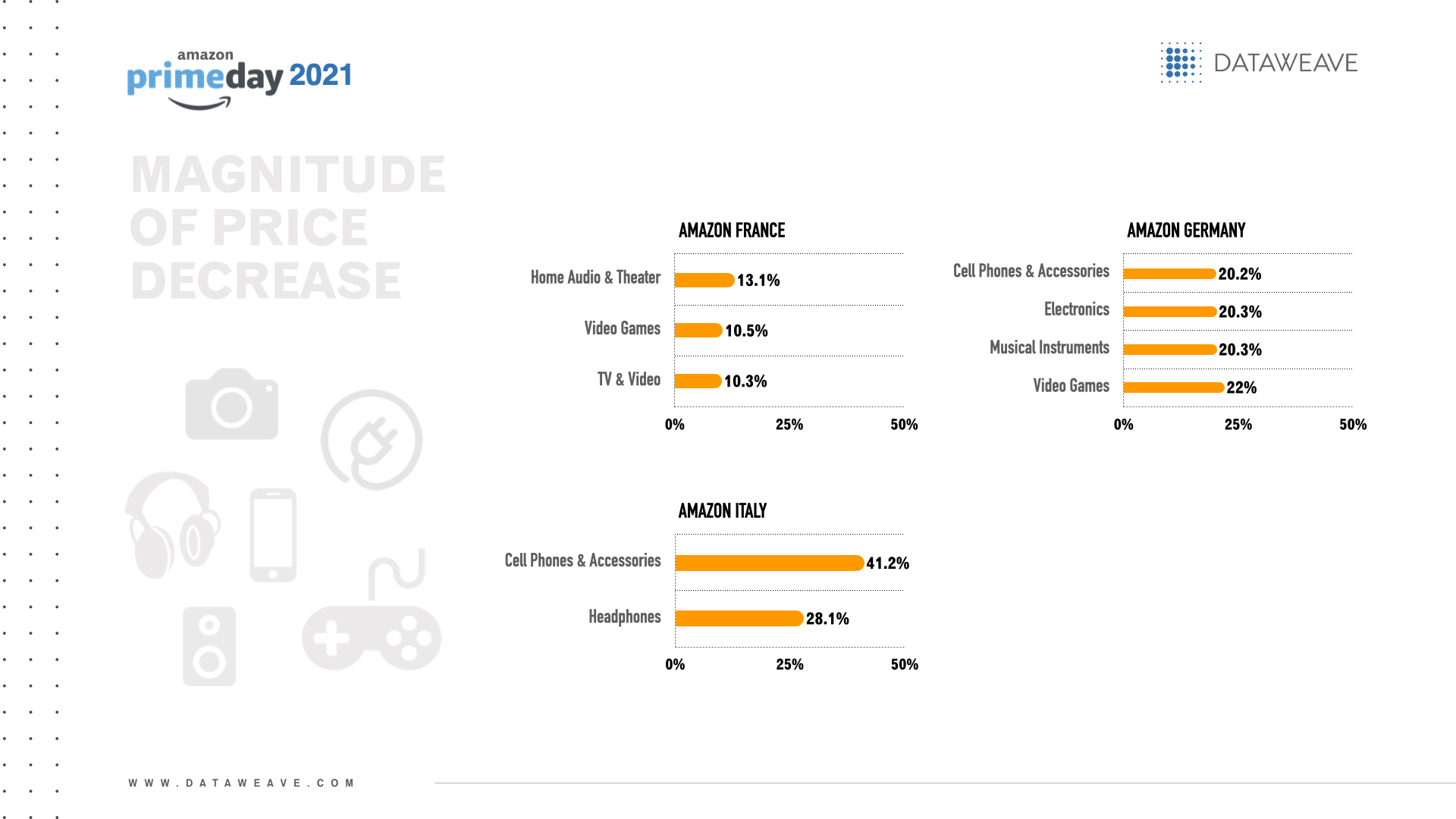

The electronics subcategories with the greatest magnitude of price decrease per European retailer were:

• Amazon France: Home audio & theater (13.1%), video games (10.5%) and TV & video (10.3%)

• Amazon Germany: Video games (22.0%), electronics and musical instruments (both 20.3%) and cell phones & accessories (20.2%)

• Amazon Italy: Cell phones & accessories (41.2%) and headphones (28.1%)

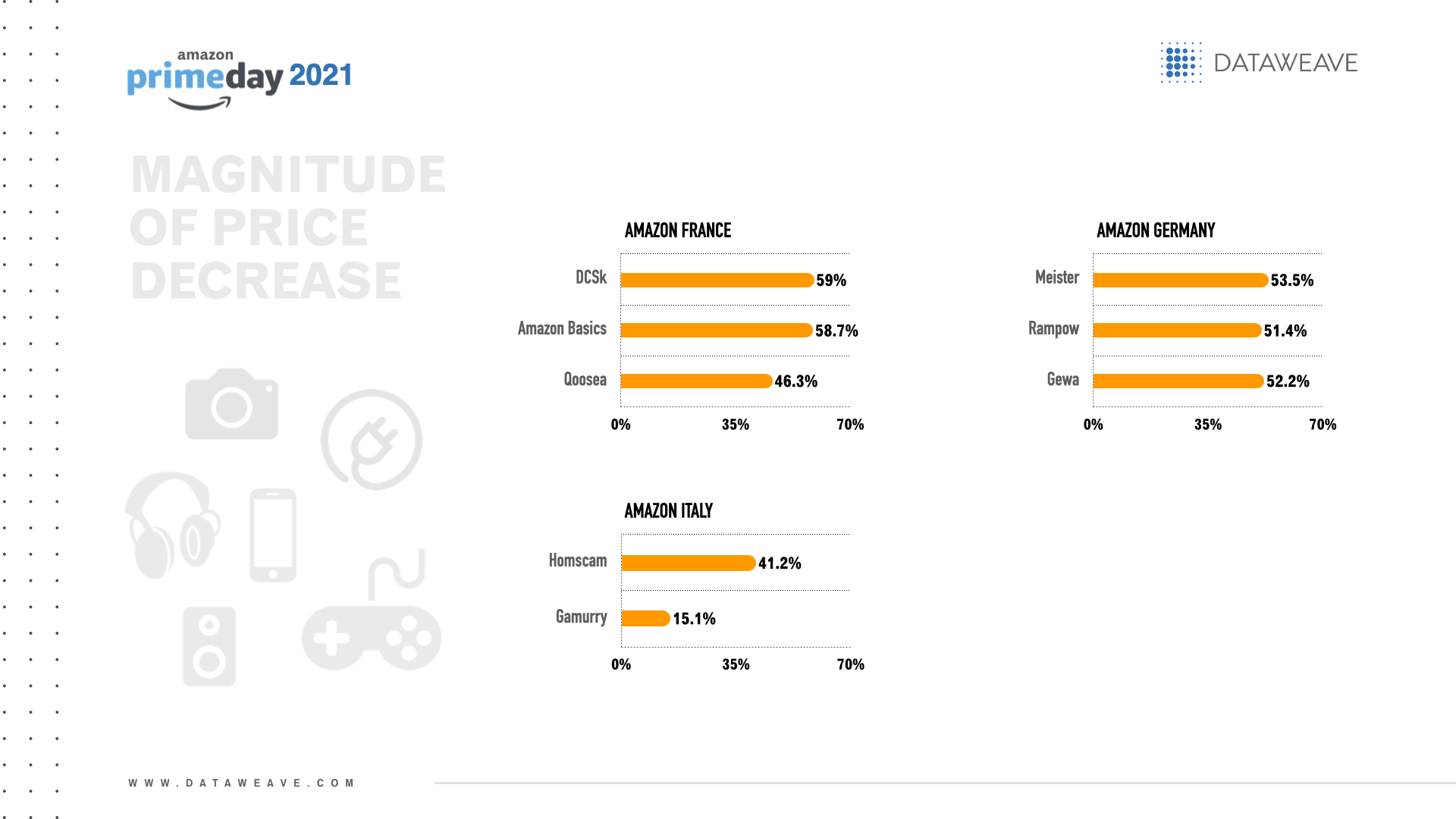

Brands with the greatest magnitude of price decreases per European retailer included:

• Amazon France: DCSk (59.0%), Amazon Basics (58.7%) and Qoosea (46.3%)

• Amazon Germany: Meister (53.5%), Rampow (51.4%) and Gewa (51.1%)

• Amazon Italy: Homscam (41.2%) and Gamurry (15.1)

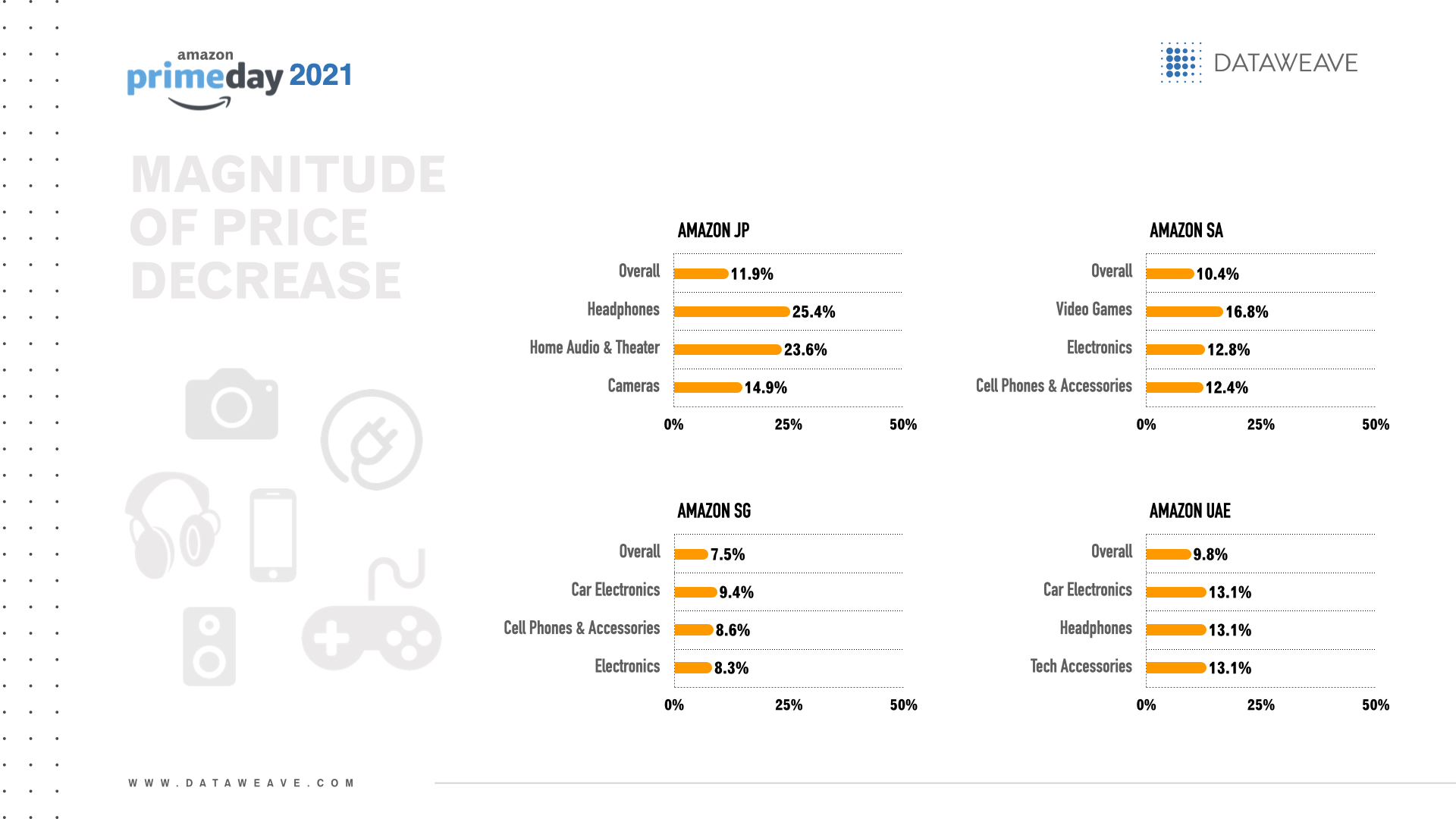

Across the Middle East and Asia, Amazon Japan offered the greatest overall magnitude of price decrease for Prime Day (11.9%) among a total of 66 products.

The electronics subcategories with the greatest magnitude of price decrease per retailer were:

• Amazon Saudi Arabia: Video games (16.8%), electronics (12.8%) and cell phones & accessories (12.4%)

• Amazon UAE: Car electronics, headphones and tech accessories (all 13.1%)

• Amazon Japan: Headphones (25.4%), home audio & theater (23.6%) and cameras (14.9%)

• Amazon Singapore: Car electronics (9.4%), cell phones & accessories (8.6%) and electronics (8.3%)

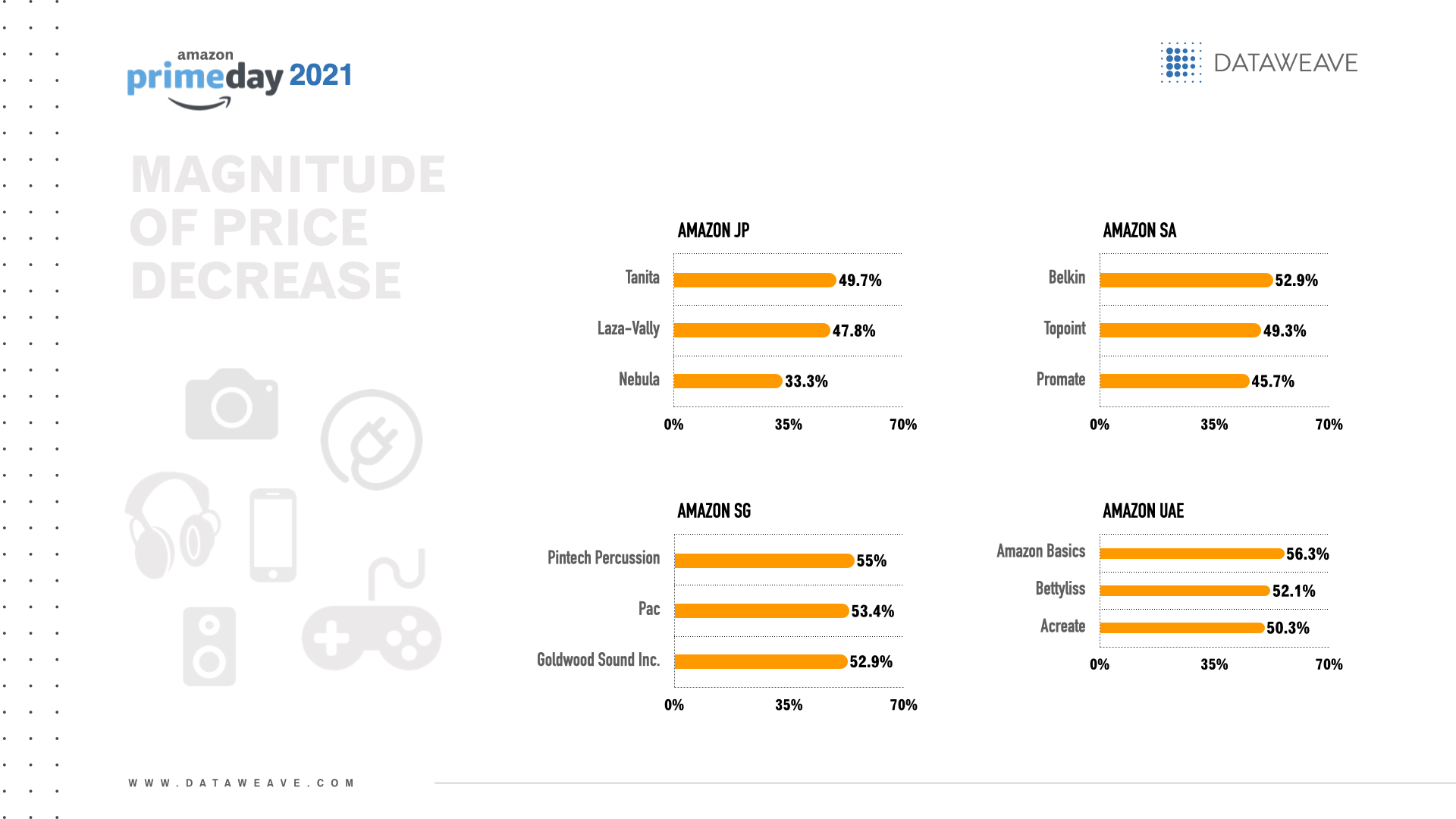

Brands with the greatest magnitude of price decreases per retailer in the Middle East and Asia included:

• Amazon Saudi Arabia: Belkin (52.9%), Topoint (49.3%) and Promate (45.7%)

• Amazon UAE: Amazon Basics (56.3%), Bettyliss (52.1%) and Acreate (50.3%)

• Amazon Japan: タニタ(Tanita) (49.7%), Laza-Vally (47.8%) and Nebula (33.3%)

• Amazon Singapore: Pintech Percussion (55.0%), Pac (53.4%) and Goldwood Sound Inc. (52.9%)

Discounts before, during and after the event

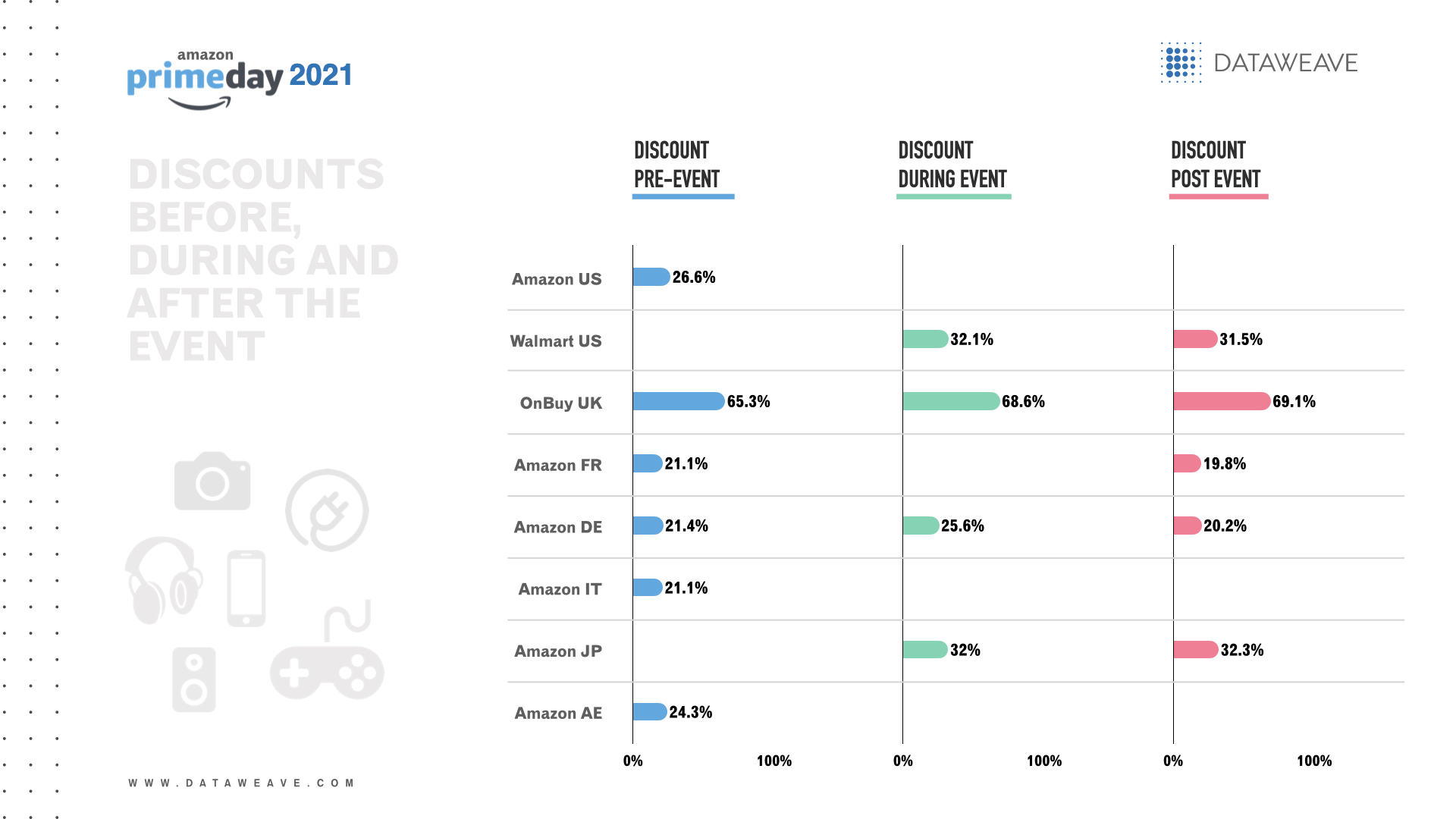

The US retailer with the biggest overall electronics discount before Prime Day was Amazon US (26.6%). Amazon’s biggest discounts were on home audio & theater (30.5%), TV & video (29.1%) and cell phones & accessories (28.6%).

Walmart offered the biggest discounts during (32.1%) and after (31.5%) the event. During the event, Walmart’s biggest discounts were on cell phones & accessories (46.3%), home audio & theater (35.5%) and computers & office (31.0%). Similarly, after the event, Walmart’s biggest discounts were on cell phones & accessories (45.8%), home audio & theater (35.3%) and computers & office (30.8%).

OnBuy was the UK retailer with the biggest overall electronics discount before (65.3%), during (68.6%) and after (69.1%) Prime Day with a product count of 237. OnBuy’s biggest discounts were on cameras (69.5% before, during and after the sales event), cell phones & accessories (rising from 67.6% before the sales event to 71.6% during and 71.8% after the event) and wearables (65.2% before and after the event yet 35.5% during Prime Day).

In Europe, Amazon Germany offered the biggest overall electronics discount before (21.4%), during (25.6%) and after (20.2%) Prime Day. Amazon France and Amazon Italy also offered comparable overall discounts (21.1%) before Prime Day.

In the pre-sales event, Amazon Germany gave the most generous discounts on cameras (34.1%), wearables (24.7%) and headphones (24.3%). During Prime Day, Amazon Germany offered the biggest discounts on video games (30.7%), headphones (30.1%) and electronics (28.3%). After Prime Day, Amazon Germany offered the biggest discounts on headphones (24.2%) electronics (22.6%) and cell phones & accessories (22.1%).

Across retailers in the Middle East & Asia, Amazon UAE offered the biggest overall electronics discount before Prime Day (24.3%), whereas Amazon Japan offered the biggest discount during (32.0%) and after (32.3%) Prime Day.

In the pre-sales event, Amazon UAE offered the most generous discounts on TV & video (31.3%), musical instruments (31.0%) and headphones (25.4%). During and after Prime Day, Amazon Japan offered the biggest discounts on Bluetooth & wireless speakers and electronics (both 99.0%).

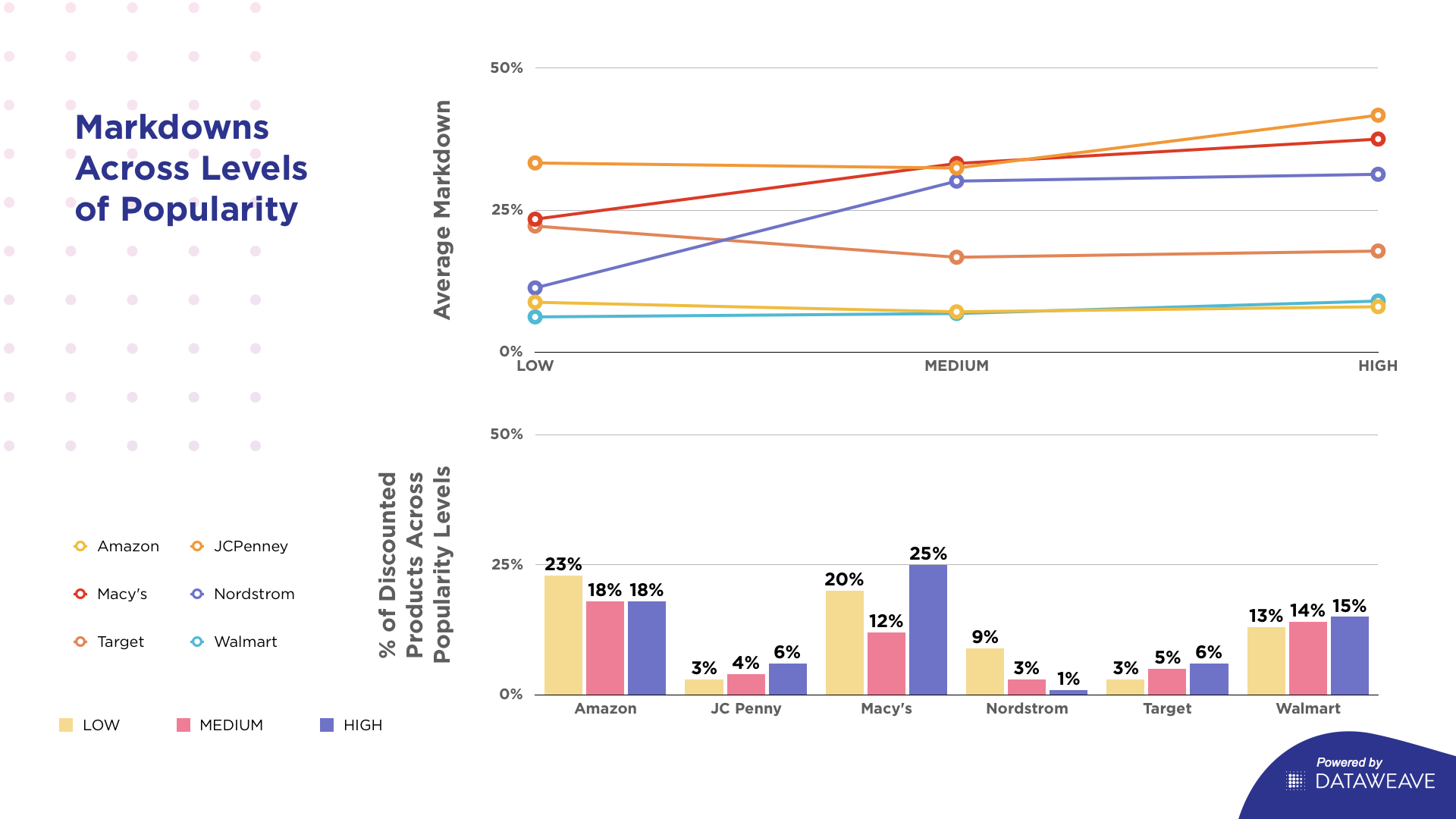

Popularity

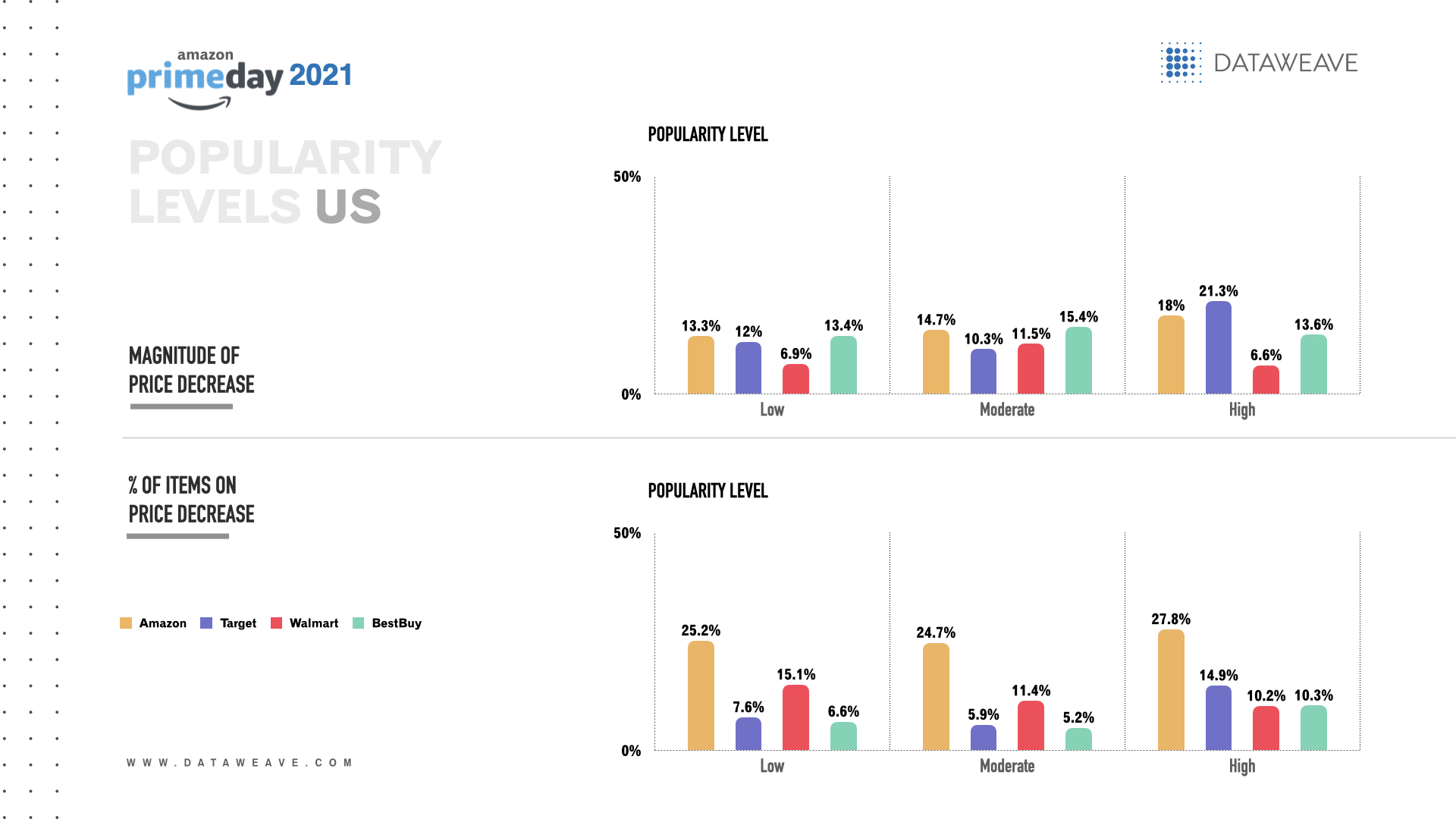

In the US, among electronics with high popularity, Amazon US offered the highest percentage of items with a price decrease (27.8%) and Target offered the greatest magnitude of price decrease (21.3%).

For electronics with moderate popularity, Amazon US offered the highest percentage of items with a price decrease (24.7%) and Best Buy offered the greatest magnitude of price decrease (15.4%).

Among electronics with low popularity, Amazon US offered the highest percentage of items with a price decrease (25.2%) and Best Buy offered the greatest magnitude of price decrease (13.4%), closely followed by Amazon US (13.3%).

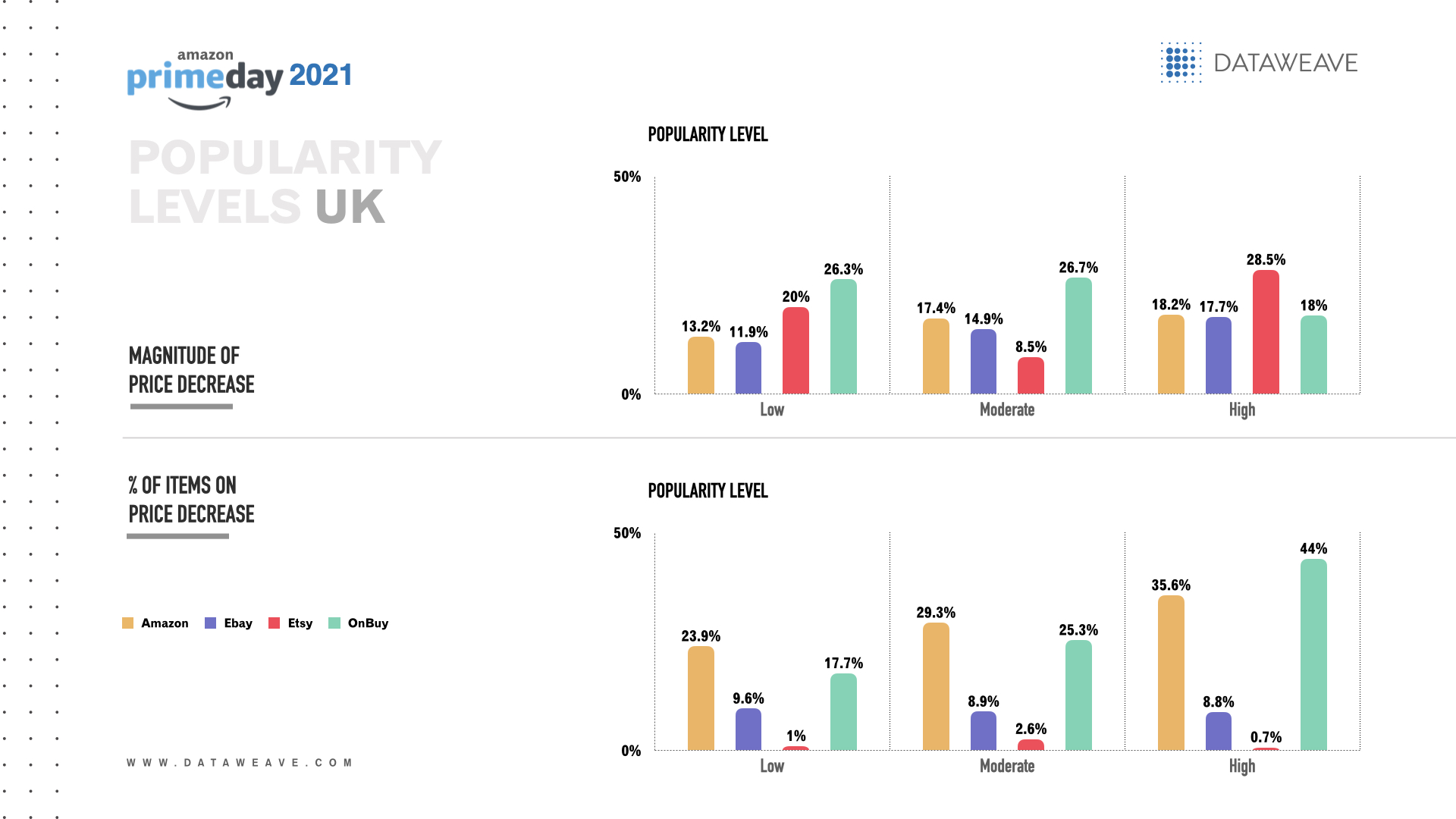

In the UK, among electronics with high popularity, OnBuy offered the highest percentage of items with a price decrease (44.0%) among 84 products and Etsy offered the greatest magnitude of price decrease (28.5%) among 150 products.

For electronics with moderate popularity, Amazon UK offered the highest percentage of items with a price decrease (29.3%) and OnBuy offered the greatest magnitude of price decrease (26.7%).

Electronics with low popularity, Amazon UK offered the highest percentage of items with a price decrease (23.9%) and OnBuy offered the greatest magnitude of price decrease (26.3%).

In Europe, among electronics with high popularity, Amazon Germany offered the highest overall percentage of items with a price decrease (30.1%) and the greatest overall magnitude of price decrease (20.2%).

For electronics with moderate popularity, Amazon Germany offered the highest percentage of items with a price decrease (29.7%) and Amazon Italy offered the greatest magnitude of price decrease (41.2%) among 12 products.

Among electronics with low popularity, Amazon Germany offered the highest percentage of items with a price decrease (26.7%) and the greatest magnitude of price decrease (17.2%).

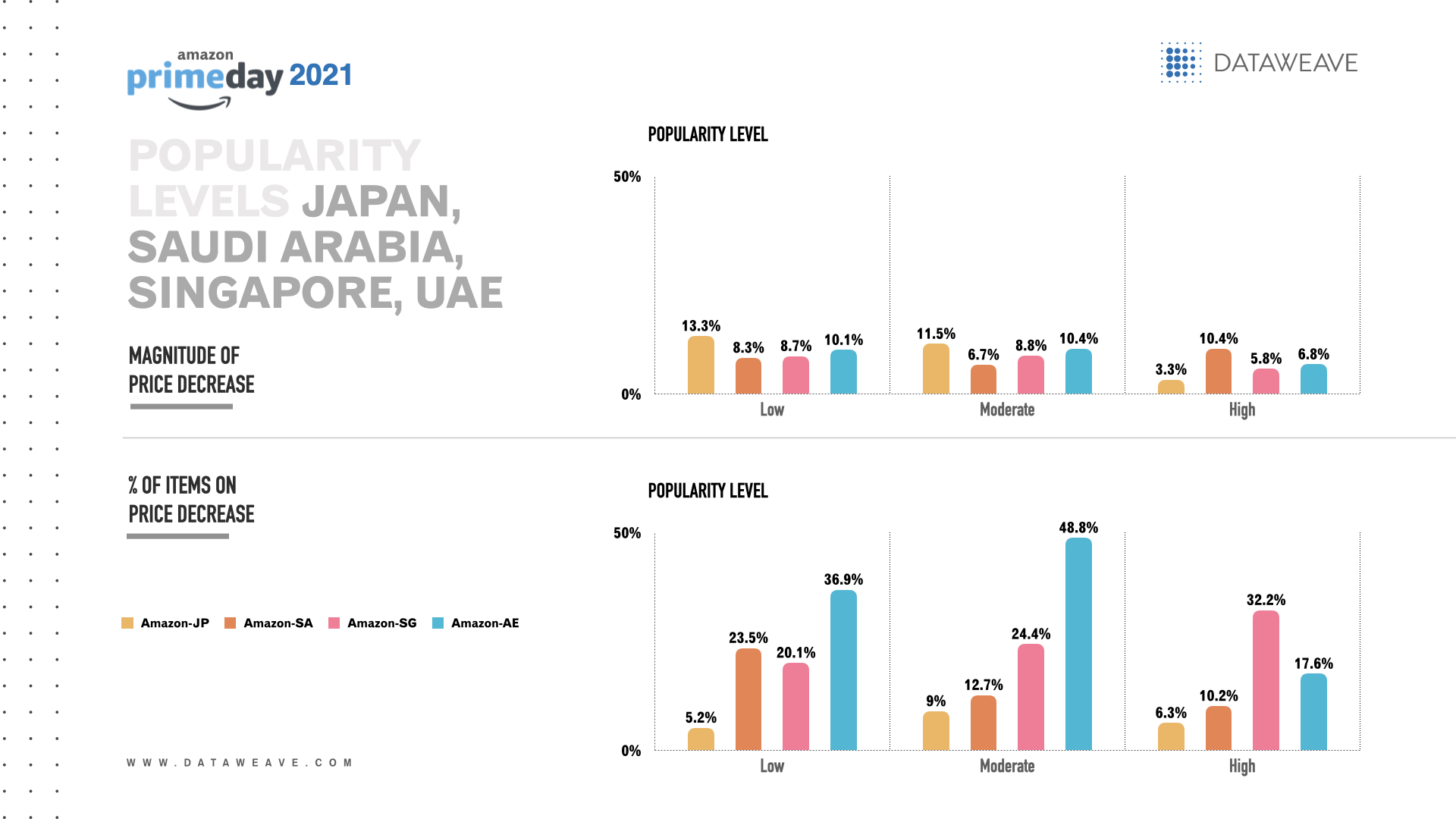

In Middle East & Asia, among electronics with high popularity, Amazon Singapore offered the highest overall percentage of items with a price decrease (32.2%) and Amazon Saudi Arabia had the greatest overall magnitude of price decrease (10.4%).

For electronics with moderate popularity, Amazon UAE offered the highest percentage of items with a price decrease (48.8%) and Amazon Japan offered the greatest magnitude of price decrease (11.5%).

Similarly, among electronics with low popularity, Amazon UAE offered the highest percentage of items with a price decrease (36.9%) and Amazon Japan the greatest magnitude of price decrease (13.3%).

Consumers won big on Prime Day 2021

Overall, Prime Day 2021 offered a wide range of deals across the competitive electronics category in each region. Almost all of the retailers we studied (except for Ebay) showed up in the analysis for offering notable discounts and pricing strategies this year. Amazon US, OnBuy, Amazon Germany, Amazon Japan and Amazon UAE appeared in the results most often among their respective regions. Stay tuned for Prime Day 2021 pricing insights across other categories, including home, health & beauty and fashion.