Fuel retailers today operate in a highly competitive and volatile market. Consumer behavior is increasingly driven by price sensitivity, particularly in industries like fuel where small changes in price can significantly influence where consumers choose to fill up. The stakes are even higher when you consider the razor-thin margins many fuel retailers work with, making every cent count.

For years, retailers have relied on third-party apps and services to provide them with location-based competitive fuel price data. These services collect pricing data based on customer transactions. While these platforms offer a convenient way for consumers to find cheaper fuel prices, their value to retailers is limited. The data they provide is often riddled with inaccuracies, lags, and incomplete coverage, leaving retailers vulnerable to missed pricing opportunities.

In this rapidly shifting landscape, retailers need data that is not only accurate but also real-time. Solving this involves directly tapping into retailers’ own data sources (first-party or 1P data) —such as websites and apps. This is believed to be the most comprehensive and reliable source of fuel price data in the market.

To validate this hypothesis, we conducted a comprehensive analysis comparing first-party and third-party (3P) fuel price data. Our analysis compared pricing (at the same time of the day) across more than 40 gas stations—including major players like Circle K, Costco, Speedway, and Wawa. The data was captured several times a day for over a week.

Accurate Pricing Matters More Than Ever

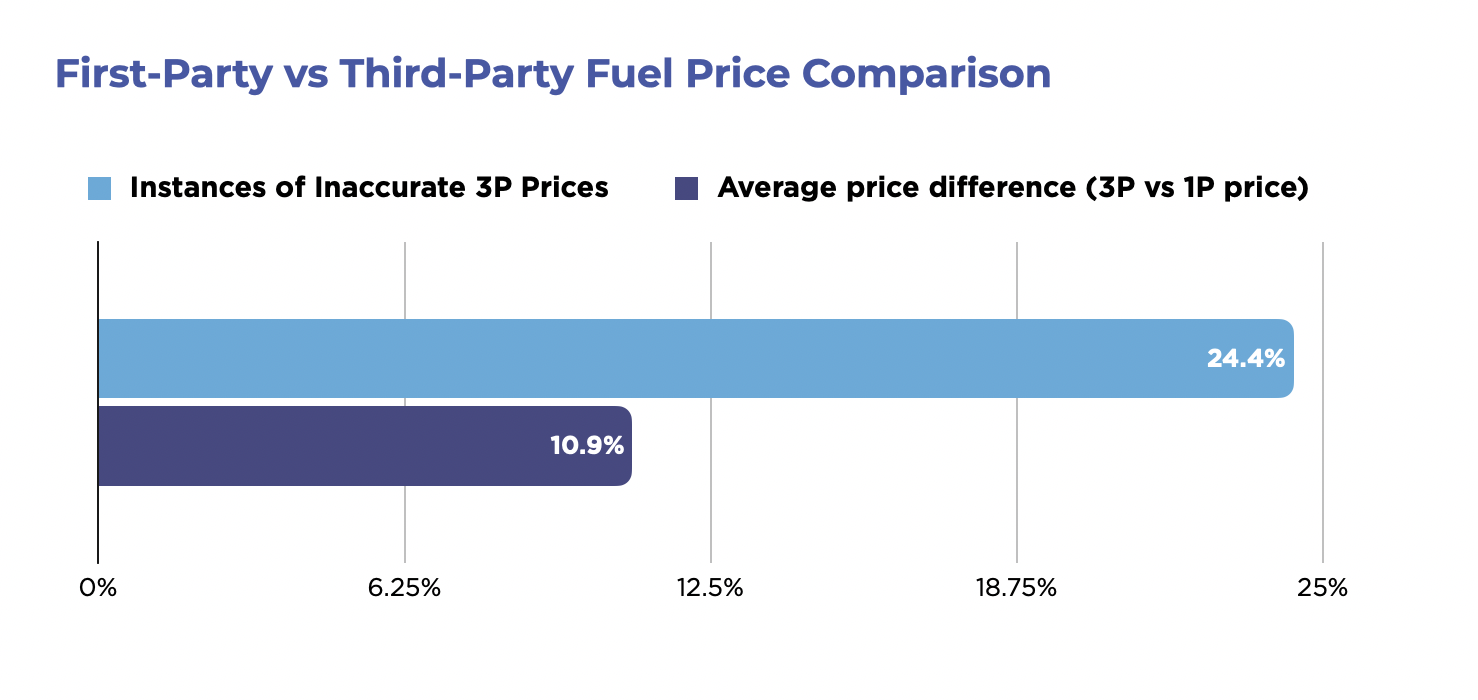

Our analysis revealed that nearly a quarter (24.4%) of the fuel pricing data provided by third-party sources was inaccurate when compared to first-party data. On average, these inaccuracies amounted to a price difference of 10.9%.

Such discrepancies, though seemingly minor, can significantly affect consumer behavior. Inaccurate prices could drive customers to competitors who are listed with lower prices—even if the real difference is negligible. For fuel retailers, this leads to lost revenue, missed opportunities, and reduced market share.

The implications are clear: relying on third-party competitive data alone puts retailers at risk. With inaccurate data, retailers may fail to adjust their prices in time to respond to market changes, losing customers to competitors.

The Core Challenges of Third-Party Data

Third-party data comes with inherent limitations. The way this data is collected presents significant challenges for fuel retailers looking to optimize pricing strategies. Here are the main issues:

- Inconsistent Data Frequency: Third-party pricing data is often gathered through customer card transactions. As a result, pricing data updates only when and where transactions occur. This can lead to irregular data availability, particularly in stations with lower transaction volumes. For instance, in rural areas or during off-peak hours, fewer transactions lead to fewer updates. Retailers are left with outdated data, making it difficult to keep pace with real-time price fluctuations.

- Limited Geographic Coverage: Regions with lower transaction volumes are particularly affected by data gaps. While urban centers may enjoy more frequent updates, rural and less-frequented stations often suffer from a lack of data. This limited geographic coverage creates blind spots, making it impossible for retailers in these regions to stay competitive.

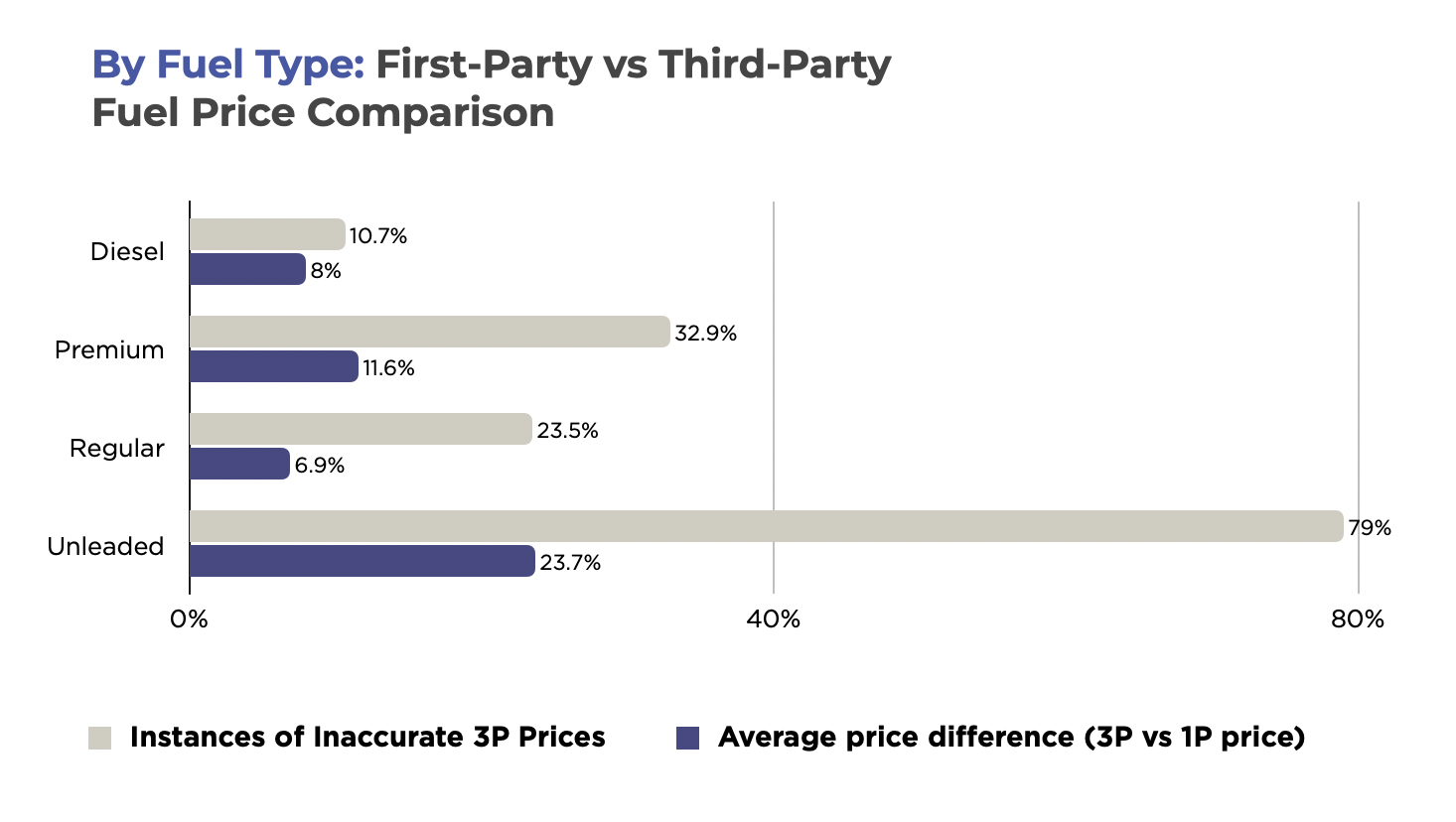

- Potential Data Inaccuracies Across Fuel Types: Our analysis showed that inaccuracies in third-party pricing data were most pronounced for Unleaded fuel, with errors occurring nearly 80% of the time. While Diesel prices fared slightly better, inaccuracies were still frequent. This inconsistency across fuel types further complicates the challenge for retailers relying on third-party data.

Leveraging First-Party Data

At DataWeave, our Fuel Pricing Intelligence solution leverages real-time 1P data directly from fuel retailers’ websites and mobile apps, ensuring that retailers always have access to the most up-to-the-minute and accurate pricing information.

Here’s why first-party data stands out:

- Real-Time Updates: Our solution provides near-instantaneous updates across more than 30,000 ZIP codes, ensuring that retailers always have the most up-to-date pricing information. This real-time accuracy is essential for making dynamic pricing adjustments in a highly competitive market.

- Wide Geographic Coverage: DataWeave’s first-party solution captures data across a broad geographic range, ensuring no blind spots in coverage. Retailers in rural or less-frequented areas benefit from the same level of insight as their urban counterparts, giving them the ability to optimize pricing in real-time.

- Complementary to Existing Solutions: For retailers already using third-party data, DataWeave’s first-party solution can complement and enhance their current systems. By filling in data gaps and providing more frequent updates, our solution ensures that retailers are never left in the dark when it comes to competitive pricing.

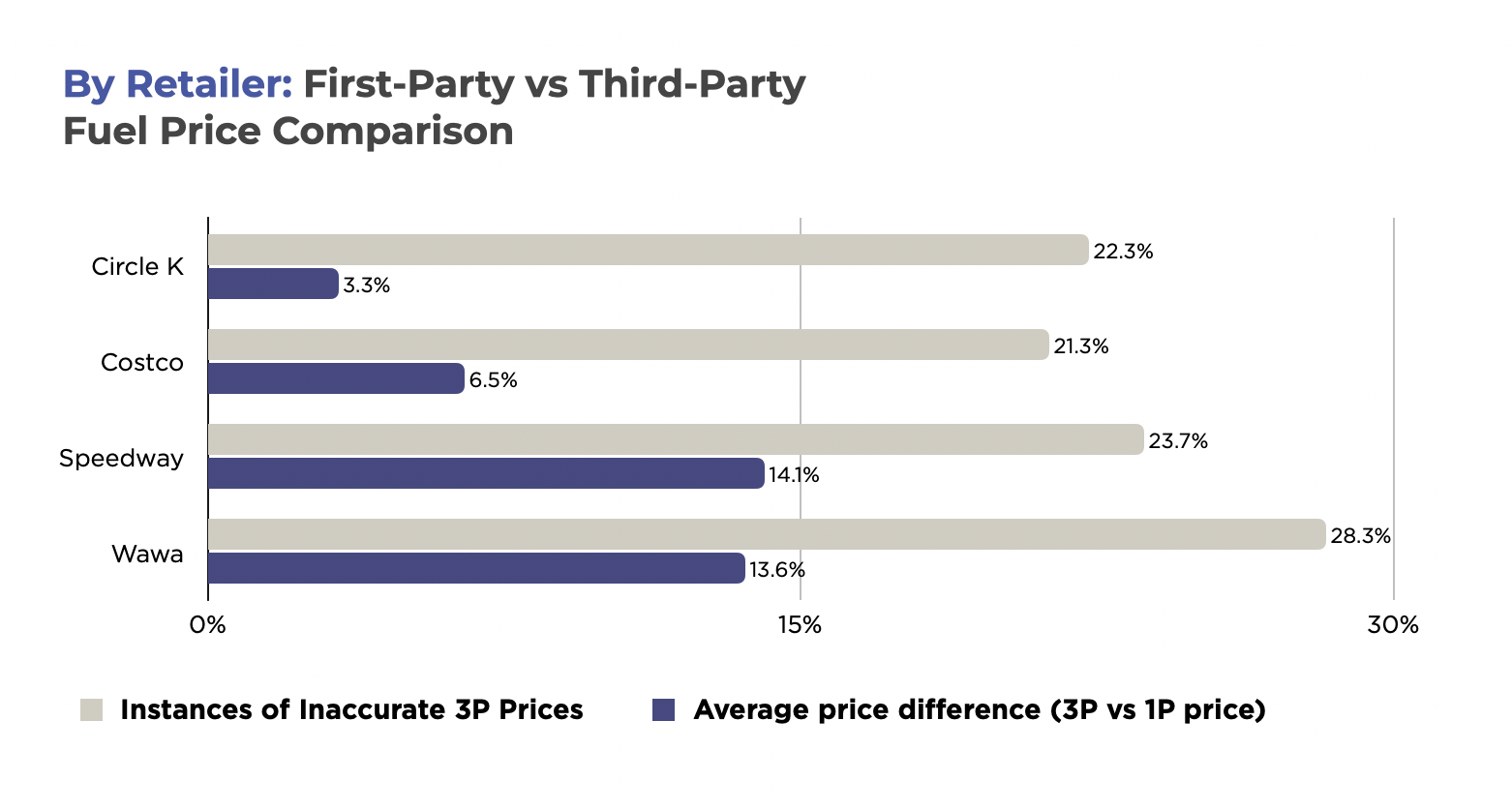

Retailer-Wise Variances

Among the retailers analyzed, we found that some were more affected by third-party data inaccuracies than others. Speedway and Wawa, for instance, experienced inaccuracies in up to 28% of third-party price data. In contrast, Circle K exhibited fewer discrepancies, but even they were not immune to the challenges posed by third-party data.

For their competition, relying on third-party data alone presents a significant risk. By switching to first-party data sources, or complementing their existing third-party data with DataWeave’s first-party solution, retailers can ensure they stay competitive in the eyes of price-sensitive consumers.

In an industry as price-sensitive as fuel retail, accurate data is a strategic asset. Leveraging first-party data allows fuel retailers to:

- Maximize Revenue: By using real-time, accurate data, retailers can avoid under- or over-pricing their fuel, ensuring they capitalize on high-demand periods while minimizing losses during low-demand times.

- Enhance Margins: First-party data provides the precision needed to fine-tune margins, ensuring profitability even in fiercely competitive markets.

- Boost Customer Retention: Competitive pricing fosters customer loyalty. With better data, retailers can maintain customer trust and retention, even during volatile market shifts.

Shift into High Gear with DataWeave

As the fuel retail industry becomes increasingly competitive, the need for accurate, real-time pricing data has never been more important. DataWeave’s Fuel Pricing Intelligence solution empowers retailers with the insights they need to stay ahead of the competition, optimize pricing strategies, and boost profitability.

With first-party data, fuel retailers can eliminate the blind spots and inaccuracies associated with third-party sources. This shift toward data-driven pricing strategies ensures that every price adjustment is backed by real-time insights, giving retailers the edge they need to succeed.

To learn more, talk to us today!